|

市場調査レポート

商品コード

1850405

世界の臨床検査インフォマティクス:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Global Laboratory Informatics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界の臨床検査インフォマティクス:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月13日

発行: Mordor Intelligence

ページ情報: 英文 116 Pages

納期: 2~3営業日

|

概要

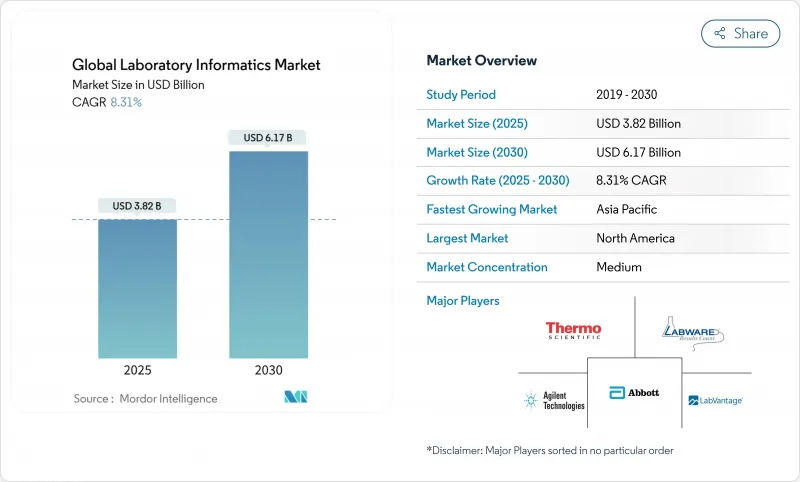

ラボラトリーインフォマティクス市場の2024年の市場規模は38億2,000万米ドルで、2030年には61億7,000万米ドルに達し、2025~2030年のCAGRは8.31%で推移すると予測されています。

成長を下支えしているのは、クラウド展開に移行するラボ、創薬のアウトソーシングペースの上昇、堅牢なマルチオミクスデータ管理を必要とする精密医療バイオバンクの拡大です。クラウド配信はすでに最大の収益プールを支配しており、製薬研究開発ではリモートアクセス・ワークフローが標準となっているため、リードを広げています。規制当局によるデータ統合の義務化により、レガシーなラボ情報管理システム(LIMS)から、設計によるコンプライアンスを組み込んだ最新のプラットフォームへの置き換えが加速しています。同時に、人工知能モジュールがインフォマティクス・スイートに組み込まれ、特に腫瘍学や希少疾患研究において、分析サイクルを短縮し、予測的洞察を表面化するようになっています。

世界の臨床検査インフォマティクス市場動向と洞察

規制が求めるデータ完全性のアップグレードがLIMSのリプレースサイクルを促進

レガシーLIMSは、今日の監査証跡、CoC、電子署名の要件を満たすことができないため、米国とカナダの製薬会社や臨床検査室では、リプレースプロジェクトの波が押し寄せています。米国食品医薬品局は、アボット社のSTARLIMSを検査施設全体に採用し、コンプライアンス・ワークフローを自動化するプラットフォームに対する規制当局の嗜好を示しています。感染症報告が手動のログから、州のサーベイランスネットワークと統合された義務化された電子検査報告へと移行するにつれて、病院もこれに追随しています。実際的には、アップグレードサイクルは、きめ細かな監査証跡、検証された機器インターフェース、21 CFR Part 11のサポートを備えたシステムへのベンダー選択を強化し、検査情報学市場を、より高い年間メンテナンス収入とより長い複数年サポート契約へと押し上げています。

アジアのCROへのアウトソーシングブームがクラウドファーストのラボラトリーインフォマティクスへの需要を高める

中国、インド、東南アジアの研究開発受託機関は、初期段階の医薬品開発でより大きなシェアを獲得しており、この地域のCROの収益は2025年に460億米ドルへと上昇します。スポンサーは、外部委託したアッセイをリアルタイムで可視化することを求めており、CROは顧客ポータルにデータをストリーミングするクラウド型LIMSの導入を余儀なくされています。LabVantageはこのニーズに対応するため、2020年から2023年の間にアジアと南米におけるプロフェッショナルサービスの拠点を80%拡大した。クラウドホスティングはオンプレミスデータセンターの資本支出を回避できるため、小規模バイオテクノロジー企業はCROパートナーとの提携を迅速に行うことができ、ラボラトリーインフォマティクス市場の持続的な2桁成長に寄与しています。

ラテンアメリカにおけるLIMS統合の障害となるレガシー機器の断片化

ラテンアメリカの多くの検査室は、数十年かけて取得された異機種混合のベンチトップ機器に依存しており、それぞれが独自のファイルフォーマットと古いファームウェアを実行しています。Science誌の2024年の試薬協力ネットワークの報道で強調されたように、地元の試薬サプライヤーの不足と消耗品の輸入コストの高騰は、課題をさらに複雑にしています。ラボが試薬を現地で製造するよう指導する取り組みは、消耗品コストを削減するもの、中核となる統合の問題を解決するものではないです。その結果、LIMSの新規展開にはカスタムドライバーの開発とインターフェイスの検証を含める必要があり、プロジェクト予算は増加し、スケジュールは長期化し、この地域のラボラトリーインフォマティクス市場の拡大ペースを弱めています。

地域分析

北米は2024年の売上高の43.0%を占め、厳しい規制監督と高い研究開発集約度を反映しています。米国疾病管理予防センターは、COVID-19緊急事態のずっと前に電子検査報告インフラを組み込み、公衆衛生研究所に迅速なデータ交換の先鞭をつけた。この地域に拠点を置く製薬大手は、AIを活用したデータ分析のためのデジタル変革予算を日常的に計上し、情報科学プラットフォームの安定した更新サイクルを確保しています。パンデミック対策と抗菌薬耐性サーベイランスのための連邦補助金が需要をさらに刺激し、ラボラトリーインフォマティクス市場における北米のリードは維持されています。

アジア太平洋地域のCAGRは9.0%で、世界最速です。中国とインドでは、国内CROがグローバルスポンサーにサービスを提供するためにキャパシティを拡大しているため、設置数が圧倒的に多いです。各国政府は、ラボの自動化とスタッフトレーニングに補助金を出す国家品質インフラプログラムを展開し、導入スケジュールを短縮しています。LabVantageの現地導入チーム強化の決定は、輸出主導のサービスモデルから地域内サポート体制への軸足を移すことを示すものであり、顧客にとって言語や時間帯の摩擦を軽減する動きです。多くの新しいラボでは、凝り固まったレガシーシステムが存在しないため、クラウド導入への直接的な飛躍が可能であり、アジア太平洋全域のラボラトリーインフォマティクス市場の成長の勢いを拡大しています。

欧州では、高度な精密医療への取り組みと厳格なデータ保護体制が両立しています。がん画像バイオバンクやマルチオミクスリポジトリでは、個人識別情報を保護しながら画像、ゲノム、臨床データをシームレスに統合するプラットフォームが求められています。GDPRへの準拠は、暗号化、トークン化、国境を越えたデータ転送管理へのベンダー投資を促します。規制によるオーバーヘッドで短期的な予算は削られるもの、国の医療サービスや市場セグメンテーションの資金源は、デジタルインフラストラクチャのアップグレードに助成金を充てており、ラボラトリーインフォマティクス市場規模の欧州セグメントにサービスを提供するベンダーの中期的なパイプラインは盤石なものとなっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 規制により義務付けられたデータ整合性のアップグレードが北米におけるLIMS交換サイクルを促進

- アジアのCROへのアウトソーシングブームがクラウドファーストのラボラトリーインフォマティクスの需要を押し上げる

- 欧州におけるプレシジョンオンコロジーバイオバンクの拡大にはハイスループットデータ管理が必要

- 日本と韓国における個別化医療ワークフローのためのAI対応分析統合

- リモートおよびハイブリッドR&Dポリシーにより、世界中の製薬ラボにおけるWebホスト型ELNの導入が加速

- EUグリーンディールデジタル製品パスポートパイロット、化学物質トレーサビリティのためのSDMSを義務化

- 市場抑制要因

- 旧来の機器の断片化がラテンアメリカの臨床検査室におけるLIMS統合を阻害

- EU GDPRによる検証とサイバーセキュリティのコストがクラウド移行予算を制限

- 公的調査機関における独自のデータ標準によるベンダーロックインの懸念

- LATAMの食品安全ラボにおけるAPIスクリプトのスキルギャップがLES統合を阻害

- 規制の見通し

- ポーターのファイブフォース分析

- 買い手の交渉力/消費者

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(価値/USD)

- 製品別

- 検査情報管理システム(LIMS)

- 電子実験ノート(ELN)

- エンタープライズコンテンツ管理(ECM)

- 実験実行システム(LES)

- クロマトグラフィーデータシステム(CDS)

- 科学データ管理システム(SDMS)

- 電子データキャプチャ(EDC)と臨床データ管理システム(CDMS)

- コンポーネント別

- サービス

- ソフトウェア

- 配送方法別

- オンプレミス

- ウェブホスト

- クラウドベース

- エンドユーザー別

- 製薬・バイオテクノロジー企業

- 契約調査機関(CRO)

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Thermo Fisher Scientific Inc.

- LabWare

- Abbott(STARLIMS Corporation)

- LabVantage Solutions Inc.

- Agilent Technologies Inc.

- PerkinElmer Inc.

- Waters Corporation

- Siemens Healthineers AG

- Illumina Inc.

- Oracle

- McKesson Corporation

- Autoscribe Informatics

- LabLynx Inc.

- Dotmatics Ltd.

- IDBS(Danaher)

- Accelerated Technology Laboratories(ATL)

- LabCollector(AgileBio)

- RURO Inc.

- Clinisys, Inc.

- Dassault Systmes SE(BIOVIA)

- Benchling Inc.

- Axtria