|

市場調査レポート

商品コード

1690889

倉庫オートメーション- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Warehouse Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 倉庫オートメーション- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

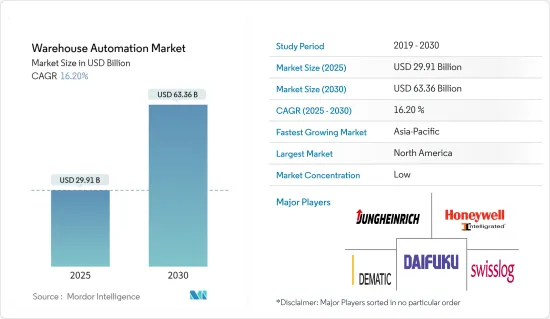

倉庫自動化市場規模は2025年に299億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは16.2%で、2030年には633億6,000万米ドルに達すると予測されます。

主要ハイライト

- ロジスティクスの自動化とは、制御システム、機械、ソフトウェアを使用して業務の効率を高めることを指します。これは通常、倉庫や配送センターで実行されなければならないプロセスに適用され、最小限の人的介入しか必要としないです。自動化ロジスティクスの利点としては、顧客サービスの向上、拡大性とスピード、組織管理、ミスの削減などが挙げられます。

- 倉庫の自動化は、最小限の人的支援で、倉庫への、倉庫内での、倉庫から顧客への在庫移動を自動化します。自動化プロジェクトの一環として、企業は反復的な肉体労働や手作業によるデータ入力・分析を伴う労働集約的な業務を排除することができます。

- さらに、世界のeコマース産業の成長と、効率的な倉庫管理・在庫管理のニーズの高まりが、市場調査の原動力となっています。倉庫管理の自動化は、全体的なビジネスコストを削減し、製品配送のミスを減らす際に非常に便利です。著名な3PL企業であり、倉庫自動化ソリューションの重要なエンドユーザーであるDHLによると、利点があるにもかかわらず、倉庫の80%は「自動化をサポートすることなく、いまだに手作業で運営されている」。さらに、倉庫、すなわちコンベア、ソーター、ピック&プレースソリューションを使用している倉庫は、倉庫全体の15%を占めています。一方、自動化されている倉庫は、現在の倉庫のわずか5%です。

- 予測不可能な需要と、サプライチェーンとの透明性とコラボレーションの欠如は、多くのメーカーにとって、ビジネス目標を達成するための大きな障壁となっています。しかし、メーカーが複雑性の原因を評価し、倉庫管理を最適化することで、サプライチェーンに対する見方を高めながら、変動する需要に効率的に対応することが期待されます。

- 同様に、倉庫管理システム(WMS)は、ワークフローの効率を改善し、エラーを減らし、エラーに関連するコストを節約し、注文処理にかかるターンアラウンドタイムを短縮することができるが、WMSの運用はeコマースビジネスにとって時間とコストがかかります。WMSの運用には、ハードウェアのための莫大な初期費用、大規模なトレーニング、維持のための追加的な月額費用が必要となります。

倉庫自動化市場の動向

小売業が大きく成長

- 倉庫の自動化は、eコマースや食料品など、さまざまな小売業で利用されています。倉庫の自動化には、生産性の向上から労働関連リスクの低減まで、複数の利点があります。eコマース倉庫の自動化は、物流施設に技術を導入し、業務パフォーマンスを高めることで成り立っています。商務省国勢調査局によると、2022年のeコマース総売上高は1兆341億米ドルで、2021年から7.7%増加(+-0.4%)しました。2022年の小売総売上高は、2021年から8.1%増加(+-0.9%)しました。

- この膨大な需要に対応するため、手作業による倉庫を自動化されたフルフィルメント業務に転換する倉庫自動化が急速に拡大しており、将来的に運営コストを管理しながら大規模な顧客需要に対応するために不可欠なものとなっています。現在、多くの小売企業が、規模が拡大し複雑化するeコマース物流業務に対応し、増え続ける顧客の需要をより迅速かつコスト効率よく満たそうと、倉庫自動化ソリューションの導入を進めています。

- 小売店の倉庫には、商品を保管するための自動ハンドリング機器から、商品の整理整頓を最大化するデジタルシステムまで、あらゆる作業を遂行するためのさまざまな自動化ソリューションを導入することができます。大手小売企業は、eコマースやオムニチャネル施設のフルフィルメント業務を簡素化するために、作業員とともに働く自動搬送車(AGV)や、自動化の次のレベルである自動移動ロボット(AMR)を活用しています。

- さらに、急速に拡大するeコマースセグメントに対応し、世界の大流行から学んだ教訓を考慮するため、大手小売企業は倉庫の応答性、回復力、信頼性を高める努力をしています。例えば、Amazonは2022年4月、「サプライチェーン、フルフィルメント、ロジスティクスの革新に拍車をかける」ために、自動化と職場ロボティクスに焦点を当てた10億米ドルの新興企業資金調達プログラムであるAmazon Industrial Innovation Fund(AIIF)を設立しました。

アジア太平洋が大きなシェアを占める見込み

- アジア太平洋の倉庫自動化市場は、同地域の産業数の増加と、投資収益率(ROI)を高めるための自動化との統合により、大幅に拡大しています。アジア太平洋の倉庫自動化は、自動化製品の生産、販売、貿易が増加している中国が支配的であると予測されています。

- さらに、中国政府は国家計画「メイドインチャイナ2025」の下、中国を製造業の巨人から世界の製造大国へと変貌させることを計画しているため、倉庫自動化産業は製造業における中国の優位性から恩恵を受けると予想されます。この計画には、中国のロボットサプライヤーを強化し、中国内外の市場シェアをさらに急増させることも含まれています。

- 倉庫自動化の需要には自動化されたサプライチェーンが含まれ、さらに有利な投資によって支えられています。同国では、市場の成長をさらに促進するための投資がいくつか研究されており、主要な主要企業が同地域に進出したり、ベンチャーキャピタルが将来性のある新興企業に資金を導入したりしています。

- インドでも製造業が高成長セグメントの一つとして浮上しています。例えば、Make in Indiaプログラムは、インドを重要な製造拠点として世界地図に掲載し、インド経済に世界の認知を与えています。Make in Indiaキャンペーンは、インドにおける産業用ロボットの複数の新発売を後押しし、倉庫自動化の機会を促進しています。

倉庫自動化産業概要

倉庫自動化市場は競争が激しくなっています。この市場の主要世界参入企業には、Dematic Group、Daifuku Co.Ltd.、Swisslog Holding AG、Honeywell Intelligrated、Jungheinrich AGなどです。製品の発売、買収、パートナーシップは、倉庫自動化産業で事業を展開する市場参入企業が採用する主要戦略です。

2023年1月、JungheinrichAGは、米国倉庫自動化市場へのアクセス強化のため、米国のラッキングと倉庫自動化ソリューションの主要プロバイダであるインディアナ州のStorage Solutions groupを買収しました。

2022年9月、DematicはUpshoptoと提携し、食料品産業と共に成長する統合フルフィルメントサービスを記載しています。この提携により、フルフィルメントビジネスの拡大を望む食料品店は、消費者データを保管・管理できるツールを利用できるようになります。Dematicは、現在のUpshopプロセスに接続するためのシンプルなソフトウェアとともに、自動化の経験を記載しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 産業バリューチェーン分析

- COVID-19の産業への影響評価

- 倉庫投資のシナリオ

- 倉庫自動化市場に対するマクロ経済要因の影響

第5章 市場力学

- 市場の促進要因

- eコマース産業の急成長と顧客の期待

- 製造の複雑化と技術の利用可能性の増加

- 市場課題

- 高額な設備投資

第6章 市場セグメンテーション

- コンポーネント別

- ハードウェア

- 移動ロボット(AGV、AMR)

- 自動保管・検索システム(AS/RS)

- 自動コンベア・仕分けシステム

- デパレタイジング/パレタイジングシステム

- 自動認識データ収集(AIDC)

- ピースピッキングロボット

- ソフトウェア(倉庫管理システム(WMS)、倉庫実行システム(WES))

- サービス(付加価値サービス、メンテナンスなど)

- ハードウェア

- エンドユーザー別

- 飲食品(製造施設、配送センターを含む)

- 郵便・小包

- 小売

- アパレル

- 製造業(耐久・非耐久)

- その他

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Dematic Group(Kion Group AG)

- Daifuku Co. Limited

- Swisslog Holding AG(KUKA AG)

- Honeywell Intelligrated(Honeywell International Inc.)

- Jungheinrich AG

- Murata Machinery Ltd

- Knapp AG

- TGW Logistics Group GmbH

- Kardex Group

- Mecalux SA

- BEUMER Group GmbH & Co. KG

- SSI Schaefer AG

- Vanderlande Industries BV

- WITRON Logistik+Informatik GmbH

- Oracle Corporation

- One Network Enterprises Inc.

- SAP SE

第8章 投資分析

第9章 市場の将来

The Warehouse Automation Market size is estimated at USD 29.91 billion in 2025, and is expected to reach USD 63.36 billion by 2030, at a CAGR of 16.2% during the forecast period (2025-2030).

Key Highlights

- Automation in logistics refers to using control systems, machinery, and software to enhance the efficiency of operations. It usually applies to the processes that must be performed in a warehouse or distribution center, which requires minimal human intervention. Some benefits of automation logistics are improved customer service, scalability and speed, organizational control, and reduction of mistakes, among others.

- Warehouse automation automates inventory movement into, within, and out of warehouses to customers with minimal human assistance. As part of an automation project, a business can eliminate labor-intensive duties that involve repetitive physical work and manual data entry and analysis.

- Moreover, the growth in the e-commerce industry worldwide and the growing need for efficient warehousing and inventory management are driving the market studied. Automation in warehousing offers extreme convenience when cutting down overall business costs and reducing errors in product deliveries. According to DHL, a prominent 3PL company and a significant end-user of warehouse automation solutions, despite the advantages, 80% of warehouses are 'still manually operated with no supporting automation.' Furthermore, warehouses, i.e., those that use conveyors, sorters, and pick and place solutions, account for 15% of the entire warehouses. In contrast, only 5% of current warehouses are automated.

- Unpredictable demand and a lack of transparency and collaboration with the supply chain present a significant barrier to reaching business goals for many manufacturers. However, when manufacturers evaluate the sources of complexity and optimize warehouse management, they are expected to efficiently meet variable demand while increasing their view of the supply chain.

- Similarly, while warehouse management systems (WMS) can improve workflow efficiency, reduce errors, save on costs associated with errors, and get faster turn-around time for order fulfillment, running a WMS can be time-consuming and expensive for an e-commerce business. It requires huge upfront costs for hardware, extensive training, and additional monthly costs for upkeep.

Warehouse Automation Market Trends

Retail to Have a Significant Growth

- Warehouse automation is used in various retail activities, including e-commerce and grocery. For warehouses, automation has multiple advantages, from boosting production to lowering labor-related risks. E-commerce warehouse automation consists of implementing technologies in logistics facilities to boost operational performance. According to the Census Bureau of the Department of Commerce, Total e-commerce sales for 2022 were USD 1,034.1 billion, an increase of 7.7 percent (+-0.4%) from 2021. Total retail sales in 2022 increased by 8.1 percent (+-0.9%) from 2021.

- To address this massive demand, warehouse automation is rapidly expanding to transform manual warehouses into automated fulfillment operations, which are proving vital to meeting customer demand at scale while managing operating costs in the future. Currently, many retailers are increasingly implementing warehouse automation solutions that seek to handle the growing scale and complexity of their e-commerce logistics operations and meet the ever-increasing demand of their customers more quickly and cost-effectively.

- A retail warehouse can be outfitted with various automated solutions to carry out all tasks, from automatic handling equipment for storing products to digital systems that maximize product organization. Big retailers are utilizing automated guided vehicles (AGVs) and the next level of automation-automated mobile robots (AMRs)-working alongside workers to simplify the fulfillment operations of their e-commerce and omnichannel facilities.

- Moreover, to meet the rapidly expanding e-commerce sector and consider the lessons learned from the worldwide pandemic, leading retailers strive to make warehouses responsive, resilient, and dependable. For instance, in April 2022, Amazon established the Amazon Industrial Innovation Fund (AIIF), a USD 1 billion startup funding program that will be used to "spur supply chain, fulfillment, and logistics innovation," focusing on automation and workplace robotics.

Asia-Pacific is Expected to Hold Significant Share

- The market for warehouse automation in the Asia-Pacific is expanding significantly due to the rising number of industries in the region and their integration with automation to increase the return on investment (ROI). The Asia-Pacific warehouse automation is predicted to be dominated by China with the growing production, sales, and trade of automation products.

- Moreover, The warehouse automation industry is expected to benefit from China's dominance in the manufacturing sector as the Chinese government plans to transform China from a manufacturing giant to a global manufacturing power under the national plan "Made in China 2025". This plan includes strengthening Chinese robot suppliers and further surging their market shares in China and abroad.

- The demand for warehouse automation includes an automated supply chain, further supported by favorable investments. The country has been marked with several investments to further the market's growth studied, with major key players expanding into the region and introducing funds by venture capitalists in emerging start-ups with potential.

- Manufacturing has emerged as one of the high-growth sectors in India as well. For instance, the Make in India program places India on the world map as a significant manufacturing hub and provides global recognition to the Indian economy. The Made in India campaign has bolstered multiple new launches in industrial robots in the country, thus driving opportunities for warehouse automation.

Warehouse Automation Industry Overview

The warehouse automation market is highly competitive. Some key global players in this market are Dematic Group, Daifuku Co. Limited, Swisslog Holding AG, Honeywell Intelligrated, and Jungheinrich AG. Product launch, acquisition, and partnership are key strategies market players operating in the warehouse automation industry adopt.

In January 2023, JungheinrichAG acquired Indiana-based Storage Solutions group, a leading provider of racking and warehouse automation solutions in the United States, to gain enhanced access to the US warehousing and automation market.

In September 2022, Dematic partnered with Upshopto to offer integrated fulfillment services that grow with the grocery industry. With the help of the alliance, grocery stores wishing to expand their fulfillment businesses will have access to tools that let them store and manage their consumer data. Dematic will offer its experience in automation along with simple software to connect with current Upshop processes.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Industry

- 4.5 Warehouse Investment Scenario

- 4.6 Impact of Macro-economic Factors on the Warehouse Automation Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Exponential Growth of the E-commerce Industry and Customer Expectation

- 5.1.2 Increasing Manufacturing Complexity and Technology Availability

- 5.2 Market Challenges

- 5.2.1 High Capital Investment

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Hardware

- 6.1.1.1 Mobile Robots (AGV, AMR)

- 6.1.1.2 Automated Storage and Retrieval Systems (AS/RS)

- 6.1.1.3 Automated Conveyor & Sorting Systems

- 6.1.1.4 De-palletizing/Palletizing Systems

- 6.1.1.5 Automatic Identification and Data Collection (AIDC)

- 6.1.1.6 Piece Picking Robots

- 6.1.2 Software (Warehouse Management Systems(WMS), Warehouse Execution Systems (WES))

- 6.1.3 Services (Value Added Services, Maintenance, etc.)

- 6.1.1 Hardware

- 6.2 By End-User

- 6.2.1 Food and Beverage (Including Manufacturing Facilities and Distribution Centers)

- 6.2.2 Post and Parcel

- 6.2.3 Retail

- 6.2.4 Apparel

- 6.2.5 Manufacturing (Durable and Non-Durable)

- 6.2.6 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Dematic Group (Kion Group AG)

- 7.1.2 Daifuku Co. Limited

- 7.1.3 Swisslog Holding AG (KUKA AG)

- 7.1.4 Honeywell Intelligrated (Honeywell International Inc.)

- 7.1.5 Jungheinrich AG

- 7.1.6 Murata Machinery Ltd

- 7.1.7 Knapp AG

- 7.1.8 TGW Logistics Group GmbH

- 7.1.9 Kardex Group

- 7.1.10 Mecalux SA

- 7.1.11 BEUMER Group GmbH & Co. KG

- 7.1.12 SSI Schaefer AG

- 7.1.13 Vanderlande Industries BV

- 7.1.14 WITRON Logistik + Informatik GmbH

- 7.1.15 Oracle Corporation

- 7.1.16 One Network Enterprises Inc.

- 7.1.17 SAP SE