|

市場調査レポート

商品コード

1548564

故障解析:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Failure Analysis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 故障解析:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

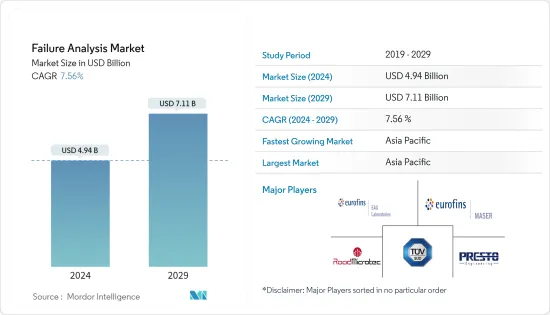

故障解析市場規模は2024年に49億4,000万米ドルと推定され、2029年には71億1,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは7.56%で成長する見込みです。

故障解析とは、データを収集・分析して故障の原因を特定し、是正措置や賠償責任を決定するプロセスです。故障の根本原因を理解することは、将来の同様の事故を防ぐために極めて重要です。一般的な原因としては、組立ミス、誤用や乱用、ファスナーの不具合、不十分なメンテナンス、製造上の欠陥、低品質の材料、不適切な熱処理、予期せぬ使用条件、設計ミス、不十分な品質保証、不十分な環境保護、鋳造の不連続性などが挙げられます。

根本原因分析(RCA)は、全産業にわたる継続的な品質改善のために極めて重要です。これは、インシデント、欠陥、品質問題を調査し、その根本原因を特定することから始まる。このプロセスは、組織が製品やサービスの品質を損なう要因に対処し、将来の再発を防止するのに役立ちます。RCAはまた、プロセスの非効率性を明らかにし、品質と業務効率の両方を向上させる。RCAが故障解析の範囲を拡大するにつれて、その成長によって故障解析市場に新たな機会が生まれることが期待されます。

老朽化したインフラはシステムに脅威をもたらします。不安定なインフラは、過酷で長期にわたる緊張時に故障の可能性を高めるためで、特に極端な状況下では憂慮されます。特に、自然災害の発生件数と深刻度が増加し、経済的な影響と人命の損失を大きく引き起こしているため、インフラの回復力が最近注目されています。

これに加えて、自動車メーカーの間で故障解析に対する要求が高まっており、性能解析、動的車両研究、事故再現などにビジョンやAIベースの解析ツールを採用していることも、市場を拡大しています。このほか、ナノテクノロジー分野の進歩に向けた投資が活発化していることも、予測期間中の故障解析市場の活性化につながると予想されます。

透過型電子顕微鏡(TEM)、走査型電子顕微鏡(SEM)、集束イオンビームシステムなどの故障解析装置のコストはかなり高いです。一方、光学顕微鏡は、電子顕微鏡よりも高度な機能を備え、応用範囲が広いにもかかわらず、電子顕微鏡よりも安価です。

2023年、半導体産業の世界の重要性はますます高まっています。半導体チップは今日の必須技術に不可欠であるだけでなく、明日の変革的イノベーションへの道を開いています。

しかし、その将来が期待される一方で、半導体産業は無数の課題に直面しています。米国と中国の根強い緊張は世界のサプライチェーンを再構築し、世界最大の半導体市場であり続ける中国へのチップ販売に対する政府の規制強化につながっています。これらの課題に対処するため、政策立案者は半導体設計における米国のリーダーシップを強化する戦略を実施し、包括的な移民およびSTEM教育改革を通じて国内労働力を強化し、業界の成長軌道を維持するために自由貿易および市場アクセスを提唱することが求められています。

故障解析の市場動向

建設セクターの成長が家具製品の需要を押し上げる

- 電子・半導体業界では、故障解析サービスの利用率が高いことから、多くの企業が故障解析を提供しており、その結果、市場シェアが最も高くなっています。

- 電子機器や半導体の故障解析は、ショート、オープン、汚染、材料の不整合など、半導体製造中の欠陥を特定・分類するのに役立ちます。故障解析の主な目的は、故障につながる根本的な問題を理解し、製造プロセスを改善し、製品の信頼性を高め、品質基準への準拠を確実にすることです。

- より小型で複雑な集積回路(IC)やシステムオンチップ(SoC)設計の開発など、半導体技術の絶え間ない進歩は、故障モードの複雑さを増大させるため、徹底した故障解析の需要を促進しています。

- 例えば、2024年 2月、NVIDIAのハードウェア製品は、シームレスに連携して機能する多数のコンポーネントを備えた重要なエンジニアリングの一例です。こうした製品の複雑さが増すにつれて、コンポーネントの故障の可能性も高まります。NVIDIAの故障解析ラボは、シリコンや基板レベルでの課題解決に注力しています。このチームは、半導体が設計上の欠陥に起因するものであれ、製造上のエラーに起因するものであれ、信頼性試験の失敗に起因するものであれ、あるいは異物混入に起因するものであれ、故障の根本的な原因を突き止めることによって、半導体業界の難問に取り組むことで知られています。

- 半導体の売上が増加すれば、生産量も増加します。生産規模が拡大するにつれて、欠陥や故障が発生する可能性も高くなり、品質を維持するために厳密な故障解析が必要になります。例えば、SIA(半導体産業協会)によると、中国の半導体売上高は2024年1月に147億6,000万米ドルに達します。この数字は、中国の売上高が116億6,000万米ドルであった2023年1月と比較して大幅な成長を示しています。

アジア太平洋が大きな市場シェアを占める見込み

- アジア太平洋地域は、中国やインドのような新興経済諸国により、予測期間中に最も急成長すると予想されます。また、日本、タイ、マレーシアなどの国々では、製造業や官民インフラ産業が増加しています。この地域の故障解析市場は、都市化や工業化の進展、インフラ整備への多額の投資、設備コストの低下など、いくつかの重要な要因によって成長を遂げています。

- アジア太平洋地域は一体となって経済と人口の大幅な成長を遂げており、これは今後も継続し、インフラ整備を促進することで市場の成長をさらに後押しすると予想されます。故障解析は、インフラ故障の根本的な原因を特定するためのフォレンジック・エンジニアリングです。これらの原因を特定することで、将来の発生を防ぐために必要な対策を講じる道が開かれます。構造物の故障がもたらす影響は深刻で、人的、社会的、環境的、経済的な影響を含みます。したがって、インフラに大きく依存している組織にとって、故障解析の重要性はいくら強調してもしすぎることはないです。

- インドの建設業界は、持続可能な政策とサービス中心の経済シフトに後押しされて急成長しています。インド政府が大規模なインフラ投資を重視していることは、成長促進へのコミットメントを強調しています。IBEFによると、2024-25年度中間予算では、インフラへの設備投資への割り当てが11.1%増の111億1,000万インドルピー(1,338億6,000万米ドル相当)に達し、GDPの3.4%に相当します。

- また、同地域では半導体製造施設の拡張が進んでおり、故障解析の需要が高まると思われます。例えば、インド政府は2024年3月、同国の旗艦奨励プログラムの下で3つの新しい半導体製造施設の設立を承認しました。

故障解析業界の概要

故障解析市場は断片的で競争が激しく、複数の主要企業が参入しています。市場での存在感が大きいことで知られるこれらの主要企業は、さまざまな産業分野での事業拡大を積極的に目指しています。これらの企業の多くは、市場シェアと収益性を強化するために戦略的提携を採用しています。また、この市場で事業を展開する企業は、製品力を強化するために企業買収も行っています。この分野の注目すべき企業には、Presto Engineering Inc.、TUV SUD、Rood Microtec GmbH、Eurofins EAG Laboratories、Eurofins Maser BVなどがあります。

2024年5月- 株式会社日立ハイテクは、最新の製品である高分解能ショットキー走査電子顕微鏡SU3900SEおよびSU3800SEを発表しました。これらの装置は、大きくて重い試料をナノレベルで精密に観察できるように設計されています。特筆すべきは、画像をシームレスに統合するカメラナビゲーション機能を備えており、オペレーターが試料の全体を見渡しやすくなっていることです。この機能強化は、関心のある領域をピンポイントで特定するのに役立つだけでなく、全体的なユーザー体験を向上させる。

2024年1月-インドの電気自動車に再びスポットライトが当たるようになったのは、63,000インドルピーという高額のボルボC40リチャージ電気SUVが最近の事故で炎上したためです。正確な原因はまだつかめていないが、この事故は製品の故障解析の重要性を浮き彫りにしました。調査によると、新製品の最大80%が発売後1年以内に不具合を起こすことが明らかになっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- インフラの老朽化とメンテナンスニーズの増加

- 技術進歩が市場成長を牽引

- 材料、設計、生産方法の革新

- 市場抑制要因

- 設備コストの高さが市場の課題

第6章 技術スナップショット

- 故障モード影響解析(FMEA)

- 故障モード影響致命度解析(FMECA)

- 機能故障解析

- 破壊物理解析

- 故障の物理解析

- フォールトツリー解析(FTA)

- その他の故障モード影響解析

第7章 市場セグメンテーション

- 技術別

- 二次イオン質量分析(SIMS)

- エネルギー分散型X線分光法(EDX)

- 化学的機械的平坦化(CMP)

- 走査型プローブ顕微鏡

- 集束イオンビーム(FIB)

- 相対イオンエッチング(RIE)

- その他の技術

- 装置別

- 走査型電子顕微鏡(SEM)

- 集束イオンビーム(FIB)装置

- 透過型電子顕微鏡(TEM)

- デュアルビームシステム

- その他装置

- 業界別

- 自動車

- 石油・ガス

- 防衛

- 建設

- 製造業

- エレクトロニクスと半導体

- その他業界別

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第8章 競合情勢

- 企業プロファイル

- Presto Engineering Inc.

- TUV SUD

- Rood Microtec GmbH

- Eurofins EAG Laboratories

- Eurofins Maser BV

- NanoScope Services Ltd

- CoreTest Technologies

- Materials Testing

- McDowell Owens Engineering Inc.

- Leonard C Quick & Associates Inc.

- Crane Engineering

- Exponent Inc.

第9章 投資の展望

第10章 市場の将来

The Failure Analysis Market size is estimated at USD 4.94 billion in 2024, and is expected to reach USD 7.11 billion by 2029, growing at a CAGR of 7.56% during the forecast period (2024-2029).

Failure analysis is the process of gathering and analyzing data to determine the cause of failure and determine corrective actions or liability. It is crucial to understand the root cause of failure to prevent similar incidents in the future. Some of the common causes include assembly error, misuse or abuse, fastener failure, inadequate maintenance, manufacturing defects, low-quality material, improper heat treatments, unforeseen operating conditions, design errors, insufficient quality assurance, inadequate environmental protection, and casting discontinuities.

Root Cause Analysis (RCA) is crucial for continuous quality improvement across industries. It begins by examining incidents, defects, and quality issues to identify their root causes. This process helps organizations address factors compromising product or service quality, preventing future recurrences. RCA also reveals process inefficiencies, enhancing both quality and operational efficiency. As RCA expands the scope of failure analysis, its growth is expected to create new opportunities in the failure analysis market.

Aged infrastructure poses a threat to the system, as unstable infrastructure raises the chances of breakdowns during severe and prolonged strain, which is particularly worrisome during extreme circumstances. Infrastructure resiliency has recently come into focus, especially as the number and severity of natural disasters are increasing, causing significant economic impacts and loss of life.

In addition to this, the increasing requirement for failure analysis among automobile manufacturers, who are also employing vision and AI-based analysis tools for performance analysis, dynamic vehicle studies, accident reconstruction, etc., is augmenting the market. Besides this, the inflating investments in the advancement of the nanotechnology sector are anticipated to fuel the failure analysis market over the forecasted period.

The cost of failure analysis equipment, including transmission electron microscopes (TEM), scanning electron microscopes (SEM), and focused ion beam systems, is considerably high. In contrast, optical microscopes are less expensive than electron microscopes despite the fact that the latter provides more advanced capabilities and a wider range of applications.

In 2023, the semiconductor industry's global significance continues to escalate. Semiconductor chips are not only integral to the essential technologies of today but are also paving the way for the transformative innovations of tomorrow.

However, alongside its promising future, the industry faces a myriad of challenges. Persistent US-China tensions are reshaping the global supply chain, leading to heightened government restrictions on chip sales to China, which remains the world's largest semiconductor market. Addressing these challenges, policymakers are urged to implement strategies that bolster US leadership in semiconductor design, enhance the domestic workforce through comprehensive immigration and STEM education reforms, and advocate for free trade and market access to sustain the industry's growth trajectory.

Failure Analysis Market Trends

Growth in the Construction Sector Boosting the Demand for Furniture Products

- A large number of companies provide failure analysis for the electronics and semiconductor industry, considering the high usage of these services in the sector, which in turn resulted in its highest market share.

- Failure analysis in electronics and semiconductors helps identify and categorize defects during the semiconductor fabrication, such as shorts, opens, contamination, or material inconsistencies. The primary aim of failure analysis is to understand the underlying issues that lead to failures, improve manufacturing processes, enhance product reliability, and ensure compliance with quality standards.

- The continuous advancements in semiconductor technology, such as the development of smaller, more complex integrated circuits (ICs) and system-on-chip (SoC) designs, increase the complexity of failure modes, thus driving the demand for thorough failure analysis.

- For instance, in February 2024, NVIDIA's hardware products are significant engineering examples, with numerous components that function together seamlessly. As the complexity of these products increases, so does the possibility of component failures. The Failure Analysis Lab at NVIDIA focuses on resolving challenges at the silicon and board levels. This team is known for tackling challenging problems in the semiconductor industry by determining the underlying cause of malfunctions, whether the semiconductors stem from a design flaw, a production error, a reliability test failure, or foreign contaminants.

- Higher semiconductor sales result in increased production volumes. As production scales up, the likelihood of defects and failures also rises, necessitating rigorous failure analysis to maintain quality. For instance, according to the SIA (Semiconductor Industry Association), semiconductor sales in China reached USD 14.76 billion in January 2024. This figure represents substantial growth compared to January 2023, when sales in China were USD 11.66 billion.

Asia-Pacific is Expected to Hold Significant Market Share

- Asia-Pacific is expected to grow fastest during the forecast period due to developing economies like China and India. Countries such as Japan, Thailand, and Malaysia are also home to increasing manufacturing and public-private infrastructure industries. The region's failure analysis market is experiencing growth due to several critical factors, such as the rise in urbanization and industrialization, significant investment in infrastructure development, and decreasing equipment costs.

- Asia-Pacific is united in experiencing substantial economic and population growth, which is anticipated to continue over the years and fuel infrastructure development, further supporting the market growth. Failure analysis is a forensic engineering component dedicated to identifying the underlying reasons behind infrastructure failures. Pinpointing these causes paves the way for implementing necessary measures to prevent future occurrences. The repercussions of structural failures can be severe, encompassing human, social, environmental, and financial consequences. Hence, the significance of failure analysis cannot be overstated for organizations heavily reliant on infrastructure.

- India's construction industry has surged, propelled by sustainable policies and a service-centric economic shift. The Indian government's emphasis on large-scale infrastructure investments underscores its commitment to driving growth. According to IBEF, in the 2024-25 Interim Budget, the allocation for capital investment in infrastructure increased by 11.1% to reach INR 11.11 lakh crore (equivalent to USD 133.86 billion), representing 3.4% of the GDP.

- In addition, the growing expansion of semiconductor manufacturing facilities in the region will drive the demand for failure analysis. For instance, in March 2024, The Indian government approved establishing three new semiconductor manufacturing facilities under the country's flagship incentive program.

Failure Analysis Industry Overview

The failure analysis market is fragmented and highly competitive, featuring several key players. These leading companies, known for their significant market presence, are actively seeking to expand their operations across various industry sectors. Many of these firms are employing strategic collaborations to bolster their market share and profitability. Companies operating within this market are also engaging in acquisitions to enhance their product capabilities. Notable players in this sector include Presto Engineering Inc., TUV SUD, Rood Microtec GmbH, Eurofins EAG Laboratories, and Eurofins Maser BV.

May 2024 - Hitachi High-Tech Corporation unveiled its latest offerings, the SU3900SE and SU3800SE High-Resolution Schottky Scanning Electron Microscopes. These devices are designed to deliver precise observations of large, weighty specimens at the nano level. Notably, they have a camera navigation feature that seamlessly merges images, facilitating operators to view the complete specimen. This enhancement not only aids in pinpointing areas of interest but also elevates the overall user experience.

January 2024 - India's spotlight once again turned to electric vehicles after a Volvo C40 Recharge electric SUV, priced at a hefty INR 63 lakh, caught fire in a recent accident. While the exact cause remains elusive, the incident underscores the criticality of product failure analysis. Studies underscore this, revealing that up to 80% of new products falter within their inaugural year on the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Ageing Infrastructure and Increasing Need for Maintenance

- 5.1.2 Technological Advancements Drive the Market Growth

- 5.1.3 Innovation in Materials, Design, and Production Methods

- 5.2 Market Restraints

- 5.2.1 High Equipment Cost Challenge the Market

6 TECHNOLOGY SNAPSHOT

- 6.1 Failure Modes Effect Analysis (FMEA)

- 6.1.1 Failure Modes, Effects, and Criticality Analysis (FMECA)

- 6.1.2 Functional Failure Analysis

- 6.1.3 Destructive Physical Analysis

- 6.1.4 Physics of Failure Analysis

- 6.1.5 Fault Tree Analysis(FTA)

- 6.1.6 Other Failure Mode Effect Analysis

7 MARKET SEGMENTATION

- 7.1 By Technology

- 7.1.1 Secondary ION Mass Spectrometry (SIMS)

- 7.1.2 Energy Dispersive X-ray Spectroscopy (EDX)

- 7.1.3 Chemical Mechanical Planarization (CMP)

- 7.1.4 Scanning Probe Microscopy

- 7.1.5 Focused Ion Beam (FIB)

- 7.1.6 Relative Ion Etching (RIE)

- 7.1.7 Other Technologies

- 7.2 By Equipment

- 7.2.1 Scanning Electron Microscope (SEM)

- 7.2.2 Focused Ion Beam (FIB) System

- 7.2.3 Transmission Electron Microscope (TEM)

- 7.2.4 Dual Beam System

- 7.2.5 Other Equipment

- 7.3 By End-user Vertical

- 7.3.1 Automotive

- 7.3.2 Oil and Gas

- 7.3.3 Defense

- 7.3.4 Construction

- 7.3.5 Manufacturing

- 7.3.6 Electronics and Semiconductors

- 7.3.7 Other End-user Verticals

- 7.4 By Geography

- 7.4.1 North America

- 7.4.2 Europe

- 7.4.3 Asia

- 7.4.4 Australia and New Zealand

- 7.4.5 Latin America

- 7.4.6 Middle East and Africa

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Presto Engineering Inc.

- 8.1.2 TUV SUD

- 8.1.3 Rood Microtec GmbH

- 8.1.4 Eurofins EAG Laboratories

- 8.1.5 Eurofins Maser BV

- 8.1.6 NanoScope Services Ltd

- 8.1.7 CoreTest Technologies

- 8.1.8 Materials Testing

- 8.1.9 McDowell Owens Engineering Inc.

- 8.1.10 Leonard C Quick & Associates Inc.

- 8.1.11 Crane Engineering

- 8.1.12 Exponent Inc.