|

市場調査レポート

商品コード

1850360

スマート水管理:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Smart Water Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スマート水管理:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月23日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

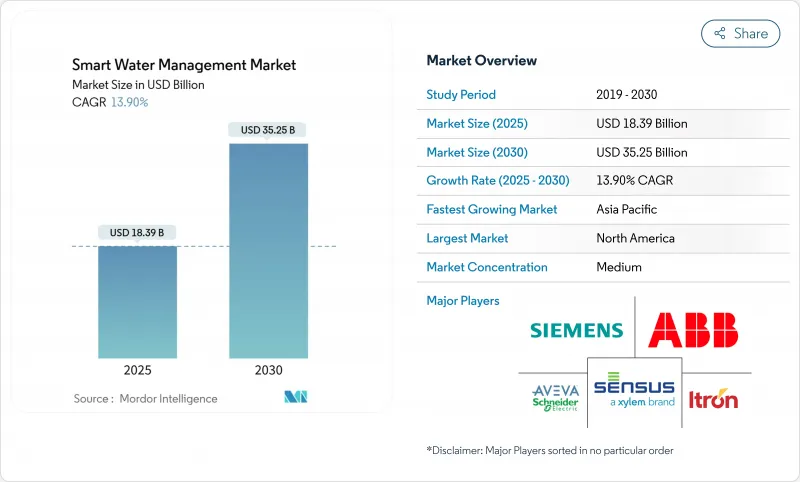

スマート水管理の市場規模は2025年に183億9,000万米ドルと推定・予測され、2030年には352億5,000万米ドルに達し、期間中13.9%のCAGRで進展すると予測されます。

急速なスケールアップは、増加する水ストレスと厳しい環境義務に対抗するため、ユーティリティ企業が漸進的な漏水削減からデータ主導の効率化プログラムへとシフトしていることを反映しています。ユーティリティ企業は現在、従来の配電網を予測的な自己最適化システムに変える統合監視、分析、制御プラットフォームを好んで使用しています。投資の勢いは、LPWAN接続の成熟、実績のあるデジタルツインアプリケーション、デジタル水インフラに資金を計上する大規模な政府刺激策によって強化されています。そのため、かつては十分なものと考えられていた従来のメータリングとSCADAのフレームワークは、測定可能なパフォーマンス向上を文書化できるエンドツーエンドのクラウド対応アーキテクチャに移行しつつあります。

世界のスマート水管理市場の動向と洞察

増加する世界の水需要を管理する必要性の高まり

深刻な干ばつサイクルにより、ユーティリティ企業はリアルタイムでの消費最適化をミッションクリティカルなインフラとして扱う必要に迫られています。フランスでは2025年に30%の降水量不足が記録され、14の県で使用制限が行われました。これらの結果は、予測分析がいかに節約を公共のメッセージから検証可能な需給バランスに変えるかを強調しています。慢性的な水不足に悩む地域、特に米国西部や地中海沿岸の一部では、デジタル水プラットフォームをサービス継続の必須条件とみなすようになり、スマート水管理市場の長期的な需要を確固たるものにしています。

無収水量(NRW)ロスを抑制する圧力の高まり

規制当局の監視が強化され、NRWの削減が公益企業の生き残り指標に転換。オレンジ郡の公益事業会社は、スマートメーターの導入後、年間400万米ドル以上を回収し、ジャクソンビルでは、これまで検出されていなかった10億ガロンの損失が確認されました。欧州では、フランスの一部のネットワークで、輸送された水の50%以上がいまだに損失しており、コンプライアンス遵守の期限が迫っています。シーメンスのSIWAリーク・ファインダーのようなAI対応システムは、スウェーデンのVA SYDがNRWを10%から8%に削減するのに役立ち、即座に運営上の利益を証明しました。金銭的な罰則とパフォーマンスベースの料金体系により、漏水分析の採用は任意ではなく、スマート水管理市場の着実な拡大に拍車をかけています。

資本集約的なメータリングとネットワークアップグレードの性質

本格的なスマート水道の導入には多額の資本支出が必要であり、小規模な公益企業の借入能力を超える可能性があります。テムズ・ウォーターは、2030年までに100万台のスマート・メーターを導入するため、5,000万英ポンドの枠組みを締結しました。政治的な配慮から料金設定が低く抑えられている場合、特にコンセッション・ファイナンスのない新興国では、長い投資回収期間が取締役会の承認を妨げます。このような予算の制約は、普及率を低下させ、スマート水管理市場の短期的成長を抑制します。

セグメント分析

ユーティリティ企業が計測、漏水検知、分析、制御をカバーする統合スイートに傾倒したため、2024年の売上はソリューションが53.7%を占めました。プロフェッショナルサービス、マネージドサービス、成果ベースの契約は、現在CAGR16.2%で成長しています。エンタープライズ資産管理モジュールは、水力モデリングエンジンと統合して、目に見える漏水よりもかなり前に配管の故障を予測し、緊急修理費用を削減します。配電網モニタリングは、地理空間分析をSCADAデータにオーバーラップさせることで、オペレータが経年変化だけでなく、リスクスコアに従って資本プロジェクトの優先順位を決定できるようにします。

ベンダーのロードマップは、アプリケーションマーケットプレースとローコードカスタマイゼーションをサポートするクラウドネイティブアーキテクチャを中心に収束し、将来の統合コストを低減します。その結果、スマート水管理市場では、ユーティリティ企業が、ライセンシングと運用改善の保証をバンドルした複数年のプラットフォーム契約を交渉しています。小規模な事業者は人材不足を補うためにマネージドサービスを採用し、大規模な事業者は知的財産の優位性を守るためにベンダーとアルゴリズムを共同開発しています。これらの動向は、ソリューションをスマート水管理市場の経済的支柱として確固たるものにしています。

スマート水管理市場は、コンポーネント別(ソリューション、サービス)、エンドユーザー別(住宅、商業、産業/公共事業)、通信技術別(セルラー(2G/3G/4G/5G、NB-IoT)、LPWAN(LoRaWAN、Sigfox)、その他)、地域別に分類されています。市場予測は金額(米ドル)で提供されます。

地域別分析

北米は2024年の売上高の27.9%を占め、大規模自治体公益事業者がメーターデータ管理、エッジ分析、サイバーセキュリティ強化の入札を迅速に実施。シュナイダーエレクトリックが2027年までに米国の施設に7億米ドルを投入する計画は、持続的な調達パイプラインへの期待を反映しています。カナダの草原地帯の州は、灌漑による取水に対抗するために漏水分析を加速させ、メキシコの北部の州は、盗難や違法な盗聴を減らすためにLPWANネットワークを試験的に導入しています。成熟した通信バックボーンと豊富なインテグレーター基盤が展開リスクを最小限に抑え、スマート水管理市場における地域のリーダーシップを強化しています。

APACはCAGR14.3%で最も急成長している地域であり、中国の国家レベルのスマートシティにエンド・ツー・エンドのデジタル水質監視を含めるという指令に後押しされています。地方交付金は、都市の排水モデルとリアルタイムの降雨フィードをリンクさせ、洪水防止と消費管理を融合させるクラウドプラットフォームを助成しています。日本の国土交通省のカタログは、相互運用可能なメーター間分析スタックを導入する電力会社のみに資金が流れるように、性能ベンチマークをハードコードしています。オーストラリアは海水淡水化への依存度を高め、エネルギー強度を下げるために漏水の早期発見を奨励し、インドは官民パートナーシップの下、干ばつに見舞われやすいマディヤ・プラデシュ州でプリペイドメーターを展開しています。このような政策モザイクにより、スマート水管理市場はAPAC全域で加速軌道に乗り続けています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 増加する世界の水需要を管理する必要性の高まり

- 無収水(NRW)損失の抑制に向けた圧力の高まり

- 政府のスマートシティと持続可能性に関する義務

- LPWAN接続(LoRaWAN、NB-IoT)の急速な導入

- 予測的な配管破損モデル化を可能にするデジタルツインプラットフォーム

- 米国とEUのインフラ刺激策資金はデジタルウォーターに充てられる

- 市場抑制要因

- メーターとネットワークのアップグレードは資本集約的である

- 従来のOT/ITシステム間の相互運用性のギャップ

- 統合水道OTネットワークにおけるサイバーセキュリティの脆弱性

- 2025年以降、IoTコンポーネントの関税によるコスト上昇

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- ライバル関係の激しさ

- 市場におけるマクロ経済要因の評価

第5章 市場規模と成長予測

- コンポーネント別

- ソリューション別

- エンタープライズ資産管理

- 配電網監視

- 監視制御およびデータ収集(SCADA)

- メーターデータ管理(MDM)

- 分析

- その他のソリューション

- サービス別

- プロフェッショナルサービス

- マネージドサービス

- ソリューション別

- エンドユーザー別

- 住宅

- 商業

- 産業/公共事業

- 通信技術別

- セルラー(2G/3G/4G/5G、NB-IoT)

- LPWAN(LoRaWAN、Sigfox)

- RFメッシュ/Wi-SUN

- 衛星とその他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Xylem Inc.(incl. Sensus)

- Itron Inc.

- ABB Ltd.

- Siemens AG

- Schneider Electric SE(+AVEVA)

- Honeywell International Inc.

- IBM Corporation

- SUEZ Water Technologies and Solutions

- Badger Meter Inc.

- Landis+Gyr AG

- Kamstrup A/S

- Trimble Water

- Huawei Technologies Co. Ltd.

- Esri

- Evoqua Water Technologies

- Sebata Holdings Ltd.

- Hitachi Ltd.

- Arad Group

- TaKaDu Ltd.

- i2O Water Ltd.