|

市場調査レポート

商品コード

1248157

ネオバンキング市場- 成長、動向、予測(2023年-2028年)Neobanking Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| ネオバンキング市場- 成長、動向、予測(2023年-2028年) |

|

出版日: 2023年03月25日

発行: Mordor Intelligence

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

ネオバンキング市場は、今年度2兆4,000億米ドルの収益を上げ、予測期間には24.6%のCAGRを達成する予定です。

ネオバンクとは、従来の物理的な支店網を持たず、オンラインのみでビジネスを行うダイレクトバンクの一種で、オンラインバンク、インターネット専用銀行、バーチャルバンク、デジタルバンクと呼ばれることもあります。ネオバンクと呼ばれる金融機関は、ライセンスを持つ銀行と連携してビジネスを展開します。彼らはAPIバンキングを利用して財務プロセスを自動化し、顧客が単一のダッシュボードにアクセスできるようにし、会計から照合、支払いに至るまですべてを処理できるようにしています。

COVID-19パンデミックの影響は、オンラインバンキングサービスへの依存度が高まっているため、ネオバンキングアプリに好影響を与えました。銀行と企業が協力して新しいバンキング・プラットフォームを導入していたのです。金融サービスプロバイダーは、技術的な向上と世界中のインターネット利用率の上昇により、顧客にデジタルサービスを供給してきました。パンデミックは、企業が通常の金融業務を行う方法にも大きな影響を与えました。従来、企業向けの銀行業務には、支払承認プロセスの変更から当座預金の開設に至るまで、手間のかかる書類作成や実店舗への訪問が必要でした。ネオバンクは、ウイルス感染後、従来の銀行業務が抱えていた問題のいくつかを解決することに成功し、その導入がこれまで以上に重要な意味を持つようになりました。さらに、流行中にネオバンクが採用された割合は、利用者が両手を広げて採用したことを示しています。

ネオバンクによって、銀行の手続きはすべてデジタル化されました。支払い手続きや現金の引き出しに長い行列はもはや必要ないです。当座預金の開設や融資を受けるために、企業は実店舗を訪れ、膨大な量の書類に記入する必要がないです。

ネオバンキングの市場動向

銀行業務のデジタル化の進展

ネオバンクの設立は、銀行活動のデジタル化の進展によって急がれました。政府の発表した移動・渡航制限の強化により、消費者がデジタルバンキングシステムを利用せざるを得なくなったことも、サービスの普及に好影響を与えました。ネオバンクは「課題ャーバンク」とも呼ばれ、さまざまな銀行業務を簡単にこなすことができるため、金融機関が提供するさまざまな銀行商品の有効性を高めることができました。ネオバンクが提供する数多くのデジタルオプションやサービスによって、お客さまの体験は大きく向上しています。

銀行セクターは常にテクノロジーの恩恵を受けてきました。ネオバンクは、テクノロジーのおかげで、より効果的、効率的、革新的になっています。テクノロジーが、ネオバンクの経費削減や顧客満足度の向上に役立っていることは言うまでもありません。ネオバンクが完全にデジタル化されたことで、取引データの自動取得が可能になり、ネオバンクはより最先端の商品やサービスに集中することができるようになりました。ネオバンクは、アナリティクス、人工知能、音声インターフェースなどの最新技術を統合することで、その潜在能力を最大限に発揮できるよう、より良い方向に変化しています。ネオバンクは、そうした技術の進歩を統合することで、顧客体験を向上させることができると思われます。

ネオバンクにおける資金調達が市場を牽引する

銀行は人類の歴史の中で圧倒的な役割を担ってきました。しかし、この現実の変化のスピードは、新しいテクノロジーの結果、加速しています。新しい世代のネオバンク、つまりデジタルバンクが利用できるようになったのです。ネオバンクは銀行と同じようなものですが、その大きな特徴のひとつは、完全にオンラインで運営されていることです。利用者をサポートするために特別に作られたオンラインツールやアプリケーションを備えているのです。その結果、ネオバンクは利用者の金融需要を満たすことができます。現代のユーザーはデジタル化が進んでおり、特にZ世代の多くがすでに社会で生産性の高い大人であることを考えると、ネオバンクの資金調達は、そのようなニーズに応えるものです。そのため、世界のさまざまな地域でネオバンクの資金調達が増加しており、それが市場を牽引しているのも事実です。

ネオバンキング市場の競合他社分析

世界のネオバンキング市場は細分化されています。現在、市場を独占している大手企業はほとんどなく、技術の進歩やサービスの革新に伴い、国内から海外までの企業が新規契約の獲得や新市場の開拓により、市場での存在感を高めています。Chime、Monzo Bank Limited、Starling Bank、N26などの主要企業が存在します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提条件条件

- 調査対象範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場の洞察と力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- テクノロジーの進化を洞察する

- 規制政策への洞察

- バリューチェーン/サプライチェーン分析

- ポーターズ5フォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19が市場に与える影響

第5章 市場セグメンテーション

- アカウントタイプ

- 業務用アカウント

- 普通預金口座

- サービス内容

- モバイルバンキング

- 支払い方法

- 送金

- 普通預金口座

- 貸出金

- その他

- 用途

- パーソナル

- エンタープライズ

- その他用途

- 地域

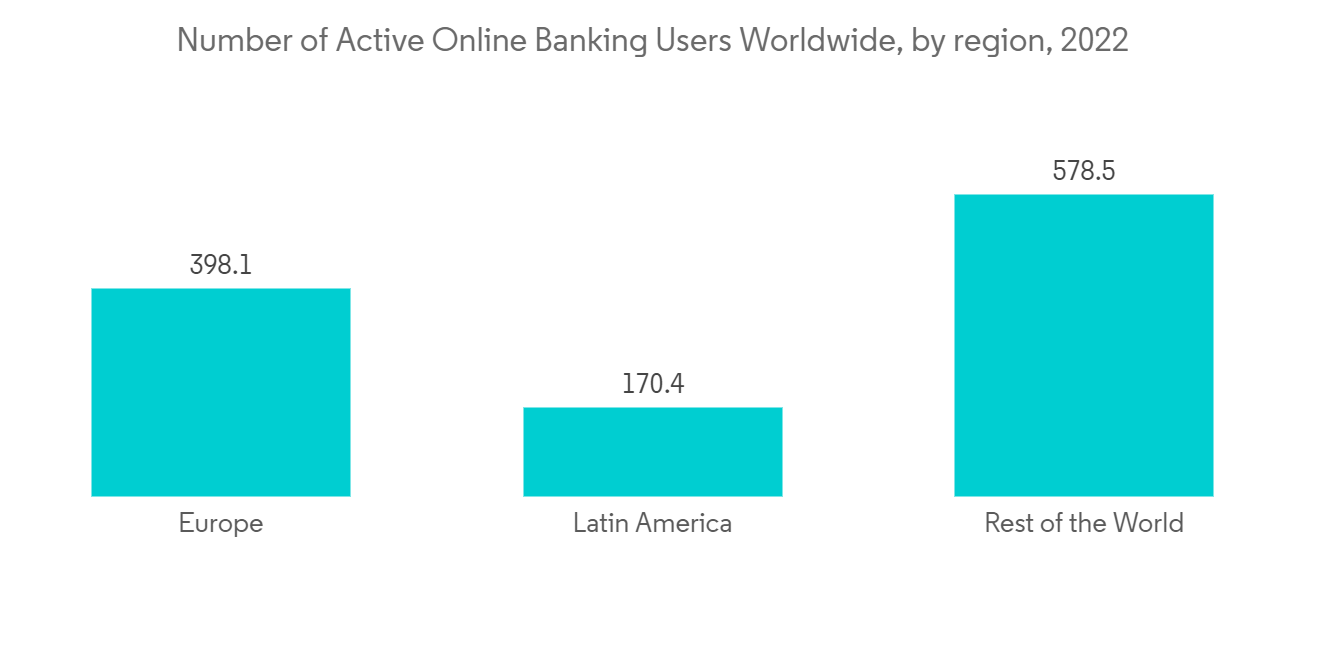

- 北米

- 欧州

- アジア太平洋地域

- 中東・アフリカ地域

- 南米

第6章 競合情勢

- 市場集中度

- 企業プロファイル

- Monzo Bank Ltd.

- Chime Financial Inc.

- Starling Banks

- MoneyLion

- Sofi

- N26

- Judo Bank

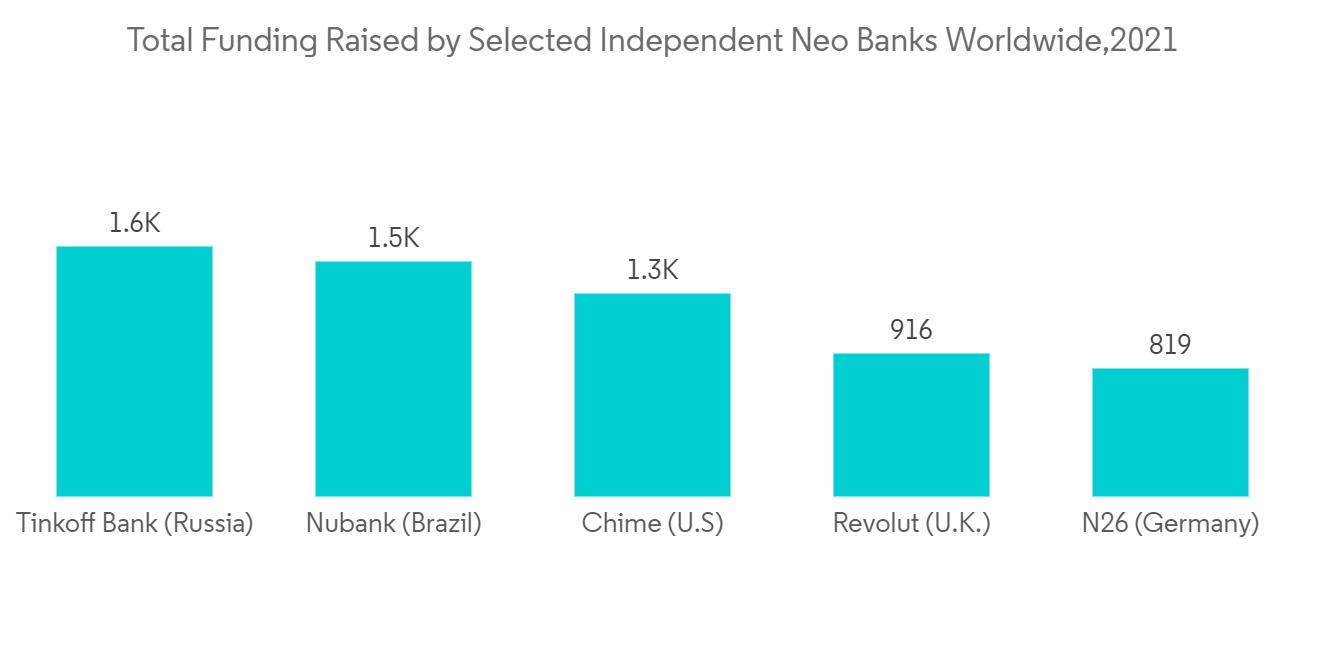

- Tinkoff Bank

- Nubank

- Revolut*

第7章 市場の将来の展望

第8章 免責事項

Neobanking Market has generated a revenue of USD 2400 Billion in the current year and is poised to achieve a CAGR of 24.6% for the forecast period. A Neo bank is a sort of direct bank that solely does business online and lacks conventional physical branch networks, sometimes referred to as an online bank, internet-only bank, virtual bank, or digital bank. The financial institutions known as Neo Banks collaborate with licensed banks to do business. They use API banking to automate financial processes and give their customers access to a single dashboard where they can handle everything from accounting to reconciliations, and payments.

The Impact of COVID-19 pandemic had a favorable effect on Neobanking Apps because of the growing reliance on online banking services. Banks and businesses were collaborating to introduce new banking platforms. Financial service providers have supplied customers with digital services thanks to technological improvements and rising internet usage around the world. The pandemic had a significant impact on how firms conduct their regular financial operations. Traditionally, every banking procedure for businesses involved laborious paperwork and physical branch visits, from changing the payout approval process to opening a current account. Neo banks helped traditional banking in the wake of the virus by successfully resolving some of its operational issues, making their adoption more crucial than ever. Additionally, the rate at which neo-banks were adopted during the epidemic shows that users did so with open arms.

The entire banking procedure has been digitalized by Neo banks. Long lines are no longer necessary to process payments or withdraw cash. To open a current account or get their loan accepted, businesses don't need to visit a physical branch or fill out an endless amount of paperwork.

Neobanking Market Trends

Increase in Digitalization of Banking Activities

The establishment of neo-banks has been hastened by the increased digitization of banking activity. Government announcements of tight movement and travel limitations, which forced consumers to use digital banking systems, had a favorable impact on the uptake of the services. Neobanks, also known as "challenger banks," are capable of carrying out a variety of banking operations with ease, which has allowed them to increase the effectiveness of various banking products provided by financial institutions. Customers' entire experience has been greatly enhanced by the numerous digital options and services that neobanks offer.

The banking sector has always benefited from technology. Neo-banks are now more effective, efficient, and innovative thanks to technology. Technology goes without saying that technology has aided Neo Banks in lowering expenses and enhancing client satisfaction. The fact that neo-banks are completely digital aids in the automatic acquisition of transactional data, allowing the neo-bank to concentrate more on cutting-edge goods and services. Neo-banks have changed for the better to realize their full potential by integrating the newest technologies, such as analytics, artificial intelligence, voice interfaces, etc. Neo-banks could improve their client experience by integrating such technological advances.

Funding In the Neo Banks is driving the market

Banks have played a dominant role in human history. However, the pace of change in this reality is accelerating as a result of new technology. New generations of neobanks, or digital banks, are now accessible. Neobanks are comparable to banks, but one of their key distinctions is that they operate entirely online. They have online tools and applications created especially to support their users. As a result, the users' financial demands are met by the neobanks. Modern users are more digitized, especially considering a large part of Gen Z is already productive adults in society. That is why neo-bank funding is increasing in different parts of the world and it is also driving the market.

Neobanking Market Competitor Analysis

The Global Neobanking Market is fragmented. Few of the major players currently dominate the market and with technological advancement and service innovation, domestic to international companies are increasing their market presence by securing new contracts and tapping new markets. It has major players, including Chime, Monzo Bank Limited, Starling Bank, N26, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Insights on Technology Advancement

- 4.5 Insights on Regulatory Policies

- 4.6 Value Chain / Supply Chain Analysis

- 4.7 Porters 5 Force Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Covid 19 on market

5 MARKET SEGMENTATION

- 5.1 Account Type

- 5.1.1 Bussiness Account

- 5.1.2 Savings Account

- 5.2 Services

- 5.2.1 Mobile- Banking

- 5.2.2 Payments

- 5.2.3 Money- Transfers

- 5.2.4 Savings Account

- 5.2.5 Loans

- 5.2.6 Others

- 5.3 Application

- 5.3.1 Personal

- 5.3.2 Enterprise

- 5.3.3 Other Application

- 5.4 Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia - Pacific

- 5.4.4 Middle- East & Africa

- 5.4.5 South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Company Profiles

- 6.2.1 Monzo Bank Ltd.

- 6.2.2 Chime Financial Inc.

- 6.2.3 Starling Banks

- 6.2.4 MoneyLion

- 6.2.5 Sofi

- 6.2.6 N26

- 6.2.7 Judo Bank

- 6.2.8 Tinkoff Bank

- 6.2.9 Nubank

- 6.2.10 Revolut*