|

市場調査レポート

商品コード

1523382

特殊ガラスの世界市場:市場シェア分析、産業動向・統計、成長予測(2024~2029年)Specialty Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 特殊ガラスの世界市場:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

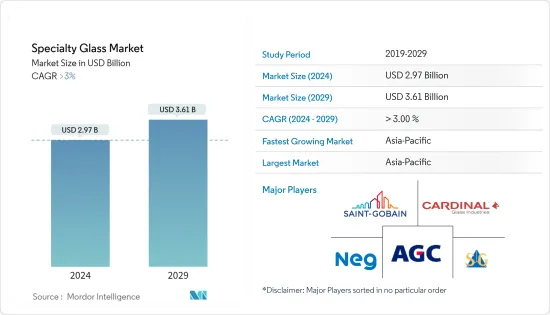

世界の特殊ガラスの市場規模は、2024年に29億7,000万米ドルに達し、2024~2029年の予測期間中にCAGR 3%以上で成長し、2029年には36億1,000万米ドルに達すると予測されています。

特殊ガラス市場の一部の分野の需要は、COVID-19が全世界の製造・開発部門に与えた影響により打撃を受けました。しかし、医薬品と医療機器に対する需要は高く、他のガラスカテゴリーに関する消費の落ち込みを大きく抑制しました。COVID-19の流行後、再生可能エネルギーと製薬産業における一貫した開発イニシアティブが世界中で実施されていることから、特殊ガラスの需要は予測期間中堅調に推移すると予測されます。

主なハイライト

- 再生可能エネルギーや建設分野でのソーラーガラス需要の増加、ヘルスケア分野での市場開拓の増加が市場を牽引すると予想されます。

- 大気汚染や水質汚濁の基準に関する厳しい環境規制は、市場の成長を妨げると予想されます。

- 再生可能エネルギー分野での研究開発活動の活発化は、予測期間中に市場にチャンスをもたらすと予想されます。

- アジア太平洋が市場を独占すると予想されます。また、通信、アーキテクチャ、医療機器、再生可能エネルギー産業における特殊ガラスの需要増加により、予測期間中に最も高いCAGRで推移するものと予想されます。

特殊ガラス市場の動向

建築用途でのソーラーガラス利用重視の高まり

- 特殊ガラスは、その効率的な特性により、様々な国の住宅や建築プロジェクトでソーラーガラスの主要な材料として使用されています。これらのガラスは光を最大限に反射し、室内を涼しく保ちます。建築用途にソーラーガラスを使用することで、様々な国が周囲の温度を最適に保ちながら、全体的なエネルギー消費を削減することを目指しています。

- ソーラーガラスは、その高い光透過性能によりソーラーパネルに高い効率を提供する高性能特殊ガラスです。このような理想的な特性により、ソーラーガラスは建物の太陽光発電技術に不可欠な部品とみなされています。また、ソーラーガラスは様々な環境条件からソーラーパネルを保護することができます。

- 断熱性、透明性、耐候性といった特殊ガラスの優れた特性により、様々な建築要件に対応する理想的な選択肢となっています。建設・開発セクターの成長は、今後数年間、機能性ガラスの需要に直接影響を与えると予想されます。

- 建設活動の増加は、特殊ガラス市場を牽引すると予想されます。アジア太平洋と北米は、世界的に住宅建設が最も盛んな地域です。北米では、米国やカナダなどで住宅建設が増加しており、これが特殊ガラス市場を牽引しています。米国国勢調査局によると、米国の年間建設生産額は2021年の1兆6,260億米ドルに対し、2022年には1,790億米ドルと評価されています。

- 同様に、欧州でも住宅建設が増加しています。ドイツは同地域最大の住宅建設市場です。同国の建設業界は、新規住宅建設活動の増加に牽引され、成長を続けています。例えば、Eurostatによると、建築建設収入は2022年に1,140億米ドルで登録され、2024年には1,254億米ドルに達すると予想されています。

- これらの要因から、特殊ガラス市場は予測期間中に世界的に成長すると考えられます。

アジア太平洋が市場を独占する

- 予測期間中、アジア太平洋が特殊ガラス市場を独占すると予想されます。照明、眼鏡レンズ、ディスプレイスクリーン、通信、アーキテクチャ、医療機器などの用途で特殊ガラスの需要が高まっています。

- 中国は、建築用途でのガラス利用の増加に伴い、世界有数のガラスの生産国であり輸出国でもあります。中国国家統計局によると、同国の建設工事生産額は2021年の4兆840億米ドルに対し、2022年には4兆3,400億米ドルに達しています。

- 同様に、インドでも建設活動が増加しています。2023~2024年度予算では、都市インフラ開発資金として年間12億1,800万米ドルがTier IIとTier IIIの都市に割り当てられています。これにより、建設用途に使用される特殊ガラスの需要が高まるでしょう。

- 主要新興経済諸国の一つであるインドは、世界市場におけるガラス需要の大きな割合を占めています。再生可能エネルギー分野の発展を促進する政府の意向の高まりが、インド市場における特殊太陽電池用ガラスとパネルの需要を牽引しています。

- インド政府は最近、気候変動という課題に対応するための重要なミッションの一つとして、国家太陽光ミッション(National Solar Mission)を開始しました。このミッションでは、2022年までに100GWの系統連系太陽光発電所を設置することを目標としています。これは、非化石燃料ベースのエネルギー資源による累積電力設備容量の約40%を達成し、2030年までにGDPの排出原単位を2005年比で33~35%削減するというインドのINDCs(Intended Nationally Determined Contributions)の目標に沿ったものです。

- インド政府は、新・再生可能エネルギー省(MNRE)の系統連系屋根上太陽光発電プログラムの第2段階を開始しました。このプログラムのもと、2022年4月、タミル・ナンドゥ・エネルギー開発庁は、タミル・ナンドゥ州に12MWの系統連系住宅用屋根上太陽光発電システムを設置する入札を実施しました。同様に、テランガナ州再生可能エネルギー局は、50MWの系統連系住宅用屋根上太陽光発電プロジェクトを建設する業者を指名する入札を募集しています。

- ヘルスケアは、雇用と収益の両面でインド経済最大のセクターの一つです。IBEFによると、インドのヘルスケア部門は3倍の伸びを記録し、2016~2022年にかけてCAGR22%で成長し、2016年の1,100億米ドルから2022年には3,720億米ドル以上に達するといいます。さらに、インドの医療機器市場は2025年までに500億米ドルに成長すると予想されています。国内の医療施設数の増加が医療機器需要を押し上げ、特殊ガラス市場を牽引します。

- このような要因から、同地域の特殊ガラス市場は予測期間中に成長すると見込まれています。

特殊ガラス産業の概要

特殊ガラス市場は部分的に統合されています。市場の主要企業としては、AGC Inc., Cardinal Glass Industries, Inc.,CSG HOLDING, Nippon Electric Glass, and Saint-Gobainなどが挙げられます(順不同)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 再生可能エネルギーと建設セクターにおけるソーラーガラス需要の増加

- ヘルスケア分野における需要の増加

- その他の促進要因

- 抑制要因

- 大気・水質汚染基準に関する厳しい環境規制

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模:金額)

- タイプ

- ホウケイ酸ガラス

- ソーダ石灰ガラス

- その他のタイプ

- 用途

- 照明用

- 光学レンズ

- ディスプレイスクリーン

- 通信ガラス

- アーキテクチャ

- 医療機器

- 再生可能エネルギー

- その他の用途

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- ノルディック

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- AGC Inc.

- AGI Glaspec

- Cardinal Glass Industries, Inc.

- Corning Incorporated

- CSG HOLDING CO., LTD.

- DWK Life Sciences

- Fuyao Glass Industry

- Gerresheimer AG

- Kanger Enterprise

- Lino

- Nippon Electric Glass Co.,Ltd.

- Saint-Gobain

- SCHOTT AG

- Sichuan Shubo(Group)Co., Ltd.

- Ta Hsiang

第7章 市場機会と今後の動向

- 再生可能エネルギー分野における研究開発活動の活発化

- その他の機会

The Specialty Glass Market size is estimated at USD 2.97 billion in 2024, and is expected to reach USD 3.61 billion by 2029, growing at a CAGR of greater than 3% during the forecast period (2024-2029).

Demand in some of the segments in the specialty glass market was hit due to the repercussions of COVID-19 on the manufacturing and development sector across the globe. However, appreciable demand for pharmaceuticals and medical equipment largely restrained the severe fall in its consumption concerning other categories of glass. Post-COVID pandemic, with the consistent development initiatives in the renewable energy and pharmaceutical industry being undertaken across the globe, the demand for specialty glass is projected to remain robust during the forecast period.

Key Highlights

- The rising demand for solar glass in the renewable energy and construction sector and the increasing developments in the healthcare sector are expected to drive the market.

- The stringent environmental regulation regarding air and water pollution standards is expected to hinder the market's growth.

- The increasing R&D activities in the renewable energy sector are expected to create opportunities for the market during the forecast period.

- The Asia-Pacific region is expected to dominate the market. It is also expected to register the highest CAGR during the forecast period due to rising demand for specialty glass in telecommunication, architecture, medical equipment, and renewable energy industries.

Specialty Glass Market Trends

Increasing Emphasis on Utilizing Solar Glass Architecture Construction Application

- Specialty glass is a majorly preferred material in solar glass for housing and building projects in various countries due to its efficient properties. These formulated glasses are perceived to reflect maximum light, thereby keeping the interiors cool. With the use of solar glass in architectural applications, various countries aim to reduce overall energy consumption while maintaining an optimum temperature for the surroundings.

- Solar Glass is a high-performance specialty glass that provides high efficiency to solar panels due to their high light transmittance performance. Owing to these ideal properties, solar glass is also regarded as an integral part of the building's integrated photovoltaic technology. Solar glass can also guard the solar panel from various environmental conditions.

- The superior properties of specialty glass, like insulation, transparency, and weather resistance, make it an ideal choice for various architectural requirements. Growth in the construction and development sector is expected to directly impact the demand for Specialty Glass in the coming years.

- The increasing construction activities are expected to drive the market for specialty glass. The Asia-Pacific and North America are the most significant regions for residential construction globally. In North America, residential construction activities are increasing in countries like the United States and Canada, which are driving the market for specialty glass. According to the United States Census Bureau, the annual value of construction output in the United States was valued at USD 1792 billion in 2022, compared to USD 1626 billion in 2021.

- Similarly, in Europe, residential construction activities are increasing. Germany is the largest market for residential construction in the region. The country's construction industry has been growing, driven by an increase in new residential construction activities. For instance, according to Eurostat, the building construction revenue is registered at USD 114 billion in 2022 and is expected to reach USD 125.4 billion by 2024.

- Owing to all these factors, the specialty glass market will likely grow globally during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to dominate the market for specialty glass during the forecast period. There is a rising demand for specialty glass from lighting, ophthalmic lenses, display screens, telecommunication, architecture, and medical equipment applications.

- China is the world's leading producer and exporter of glass, in line with the increasing utilization of glass in architectural construction applications. According to the National Bureau of Statistics of China, the output value of construction works in the country accounted for USD 4.34 trillion in 2022, as compared to USD 4.084 trillion in 2021.

- Similarly, in India, construction activities are increasing. As per the 2023-2024 budget, a dedicated amount of USD 1,218 million per annum has been allocated through urban infra-development funds for Tier II and Tier III cities. This will create a buoyant demand for specialty glass used in construction applications.

- India, one of the major developing economies, constitutes a large share of glass demand in the global market. The increasing inclination of the government to promote the development of the renewable energy sector has been driving the demand for specialty solar glass and panels in the Indian market.

- The Indian government has recently started the National Solar Mission as one of the critical Missions to meet the challenges of climate change. The Mission targets installing 100 GW grid-connected solar power plants by the year 2022. This is in line with India's Intended Nationally Determined Contributions (INDCs) target to achieve about 40 percent cumulative electric power installed capacity from non-fossil fuel-based energy resources and to reduce the emission intensity of its GDP by 33 to 35 percent from the 2005 level by 2030.

- The Government of India initiated phase II of the Ministry of New and Renewable Energy's (MNRE) grid-connected rooftop solar program. Under this program, in April 2022, the Tamil Nandu Energy Development Agency issued a tender to install 12 MW of grid-connected residential rooftop solar systems in Tamil Nandu. Similarly, Telangana state's Renewable Energy Department Corporation invited bids to appoint suppliers to build 50 MW of grid-connected residential rooftop solar projects.Thus the growth in the renewable energy sector is expected to drive the demand for specialty glass in the region.

- Healthcare is one of the largest sectors of the Indian economy in terms of both employment and revenue. According to IBEF (India Brand Equity Foundation), the Indian healthcare sector recorded a three-fold rise, growing at a CAGR of 22% between 2016-22 to reach over USD 372 billion in 2022 from USD 110 billion in 2016. Furthermore, it is anticipated that India's market for medical equipment will grow to USD 50 billion by 2025. The increasing number of medical facilities in the country will boost the demand for medical devices, thereby driving the market for specialty glass.

- Due to all such factors, the market for specialty glass in the region is expected to grow during the forecast period.

Specialty Glass Industry Overview

The specialty glass market is partially consolidated in nature. Some of the major players in the market include (not in any particular order) AGC Inc., Cardinal Glass Industries, Inc.,CSG HOLDING CO., LTD., Nippon Electric Glass Co., Ltd., and Saint-Gobain, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand for Solar Glass in the Renewable Energy and Construction Sector

- 4.1.2 Increasing Developments in Healthcare Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent environmental regulation regarding air and water pollution standards

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Borosilicate Glass

- 5.1.2 Soda-Lime Glass

- 5.1.3 Other Types (Insulated Glass, Decorative Glass, etc.)

- 5.2 Applications

- 5.2.1 Lighting

- 5.2.2 Ophthamalic Lenses

- 5.2.3 Display Screens

- 5.2.4 Telecommunication

- 5.2.5 Architecture

- 5.2.6 Medical Equipments

- 5.2.7 Renewable Energy

- 5.2.8 Other Applications (Beam Splitters, Semiconductor Assemblies, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 UAE

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AGC Inc.

- 6.4.2 AGI Glaspec

- 6.4.3 Cardinal Glass Industries, Inc.

- 6.4.4 Corning Incorporated

- 6.4.5 CSG HOLDING CO., LTD.

- 6.4.6 DWK Life Sciences

- 6.4.7 Fuyao Glass Industry

- 6.4.8 Gerresheimer AG

- 6.4.9 Kanger Enterprise

- 6.4.10 Lino

- 6.4.11 Nippon Electric Glass Co.,Ltd.

- 6.4.12 Saint-Gobain

- 6.4.13 SCHOTT AG

- 6.4.14 Sichuan Shubo (Group) Co., Ltd.

- 6.4.15 Ta Hsiang

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing R&D activities in the Renewable Energy Sector

- 7.2 Other Opportunities