|

市場調査レポート

商品コード

1690943

冷凍・冷蔵トレーラー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Refrigerated Trailer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 冷凍・冷蔵トレーラー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

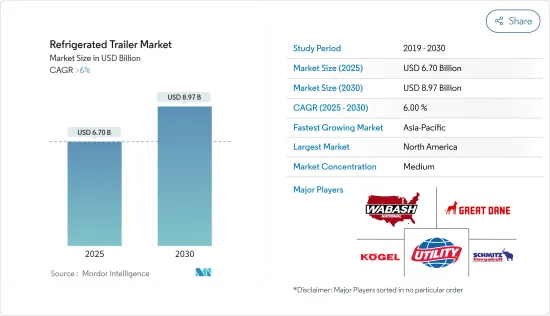

冷凍・冷蔵トレーラー市場規模は2025年に67億米ドルと推定され、予測期間(2025~2030年)のCAGRは6%を超え、2030年には89億7,000万米ドルに達すると予測されます。

冷蔵トレーラー市場は、温度に敏感な商品の輸送需要の増加、冷蔵システムの技術進歩、世界のコールドチェーン物流インフラの拡大など、さまざまな要因によって力強い成長を遂げています。冷凍・冷蔵トレーラー(リーファーとも呼ばれる)は、食品や医薬品などの腐敗しやすい商品を長距離輸送する際に、走行中も望ましい温度を維持しながら輸送するという重要な役割を担っています。世界の食品貿易の増加と食品廃棄を削減する必要性の高まりにより、冷蔵トレーラーの需要は今後数年間で着実に伸びると予想されます。

さらに、世界中の政府や規制機関が定める厳しい食品安全規制や品質基準により、食品生産者、流通業者、物流会社は信頼性の高い冷蔵輸送ソリューションへの投資を余儀なくされています。高度な温度監視・制御システムを搭載した冷蔵トレーラーは、こうした規制の遵守を確実にし、輸送中の生鮮品の品質を守るのに役立ちます。さらに、食品の安全性と品質に関する消費者の意識の高まりが、小売業者やeコマース企業による生鮮食品やその他の温度に敏感な製品の輸送への冷蔵トレーラーの採用を促進しています。

さらに、持続可能なエネルギー源を動力源とする電気式およびハイブリッド式冷蔵トレーラーの登場は、冷蔵トレーラー市場に革命を起こす構えです。環境の持続可能性と温室効果ガス排出に対する懸念が強まる中、フリートオペレーターや物流会社は二酸化炭素排出量を削減するため、環境に優しい冷蔵ソリューションを採用する傾向が強まっています。電気式冷凍・冷蔵トレーラーは、従来のディーゼルエンジン式トレーラーに比べ、より静かな運転、排出ガスの削減、運転コストの削減といったメリットを提供します。

北米が市場をリードする地域であり、アジア太平洋、欧州がこれに続きます。冷凍・冷蔵トレーラーを製造している主な企業は、Wabash National Commercial Trailer Products、Great Dane Trailers、Utility Trailer Manufacturing Company、Schmitz Cargobull AG、Kogle Trailer GmbHなどです。

冷凍・冷蔵トレーラー市場の動向

コールドチェーンロジスティクス活動の拡大が冷凍・冷蔵トレーラー市場を牽引する見込み

ハードウェア、テレマティクス、車両技術における様々な進歩が北米全域の生鮮品輸送を変革しつつあり、冷凍車フリートが競争力を維持するための戦略を検討するよう促しているため、コールドチェーン技術にとってエキサイティングな時期となっています。しかし、冷凍車業界は、かつてないほど複雑化した事業環境の中で課題に直面しています。例えば、

- 2024年2月、Taikoo Motors、Zuellig Pharma、Long Feng Medical Logisticsの3社間の合意により、台湾におけるコールドチェーン物流用ボルボFE電気トラックの初展開が正式に決定しました。この合意は、環境に優しい輸送を推進し、環境的に持続可能なロジスティクスの新たな時代を切り開くための協力的な取り組みを強調するものです。

長期契約運賃は安定しているもの、全体的な貨物量は減少しているため、多くの小規模冷蔵輸送業者はビジネスチャンスをスポット市場に頼るようになっています。スポット冷凍運賃は2022年の同時期より約7%低く、5年間の平均を5%以上下回っています。このような障害にもかかわらず、冷凍フリートは、フリートの閉鎖、規制の変更、市場力学のシフトなどの要因のために大きな動揺を経験しているドライバン輸送のような他のセクターと比較して、トラック運送業界の比較的絶縁セグメントから利益を得ています。

予測期間中、アジア太平洋地域が最大の市場シェアを占める見込み

新鮮な生鮮食品に対する消費者の嗜好が高まり、特に人口密度の高い都市部では、これらの製品を生産センターから流通ハブや小売店まで輸送するための効率的で信頼性の高い冷蔵トレーラーに対するニーズが地域全体で高まっています。さらに、アジア太平洋地域は熱帯から温帯までの多様な気候を含んでおり、サプライチェーン全体を通して生鮮品の品質と安全性を維持する上で冷蔵トレーラーの重要性をさらに際立たせています。例えば、

- 香港のコールドチェーンロジスティクス業界では、集荷から倉庫保管、受注管理、輸送、配送に至るまで、サプライチェーン・プロセス全体で低温を維持する需要が高まっています。香港の現在のコールドチェーン・サービスは、食品輸入業者、卸売業者、小売業者、ケータリング業界の期待に応えられていないです。多くの冷蔵倉庫では、商品が冷蔵室を出た後の温度管理が不十分なため、新鮮な食材が劣化してしまうからです。香港のコールドチェーン物流サービスにおけるこうした欠陥に対処するため、TAHUHUは2023年5月に初の自動化されたインテリジェントなコールドチェーン物流サービスを導入しました。

さらに、食品安全基準の改善と輸送インフラの近代化を目指す政府の取り組みが、アジア太平洋における冷蔵トレーラーの採用に拍車をかけています。中国、インド、日本、韓国などの国々では、温度変化に敏感な製品の需要増加を支えるため、冷蔵倉庫、冷蔵保管施設、冷蔵輸送車両などのコールドチェーン・ロジスティクス・インフラへの大規模な投資が行われています。さらに、IoT(モノのインターネット)センサーやリアルタイム・モニタリング・ソリューションの統合など、冷凍システムの技術的進歩が冷凍・冷蔵トレーラーの効率性と信頼性を高め、同地域の市場成長をさらに促進しています。

冷凍・冷蔵トレーラー産業の概要

冷凍・冷蔵トレーラー製造企業は、環境法を遵守しながらトレーラーをより効率的にするため、様々な先進技術を採用・開発しています。Great Dane LLC、Wabash National Corporation、Kogel GmbH、Schmitz Cargobull AG、Utility Manufacturing Companyなどの企業が冷凍・冷蔵トレーラー市場の主要企業です。

2024年3月、ATAテクノロジー&メンテナンス協議会主催の年次総会&輸送技術展示会は、業界の革新、進歩、功績を称えるプラットフォームとして機能しました。今年の会議の中で、ユーティリティ・トレーラー・マニュファクチャリング・カンパニーLLCは、革新的なカーゴブル北米LLC(CBNA)の輸送用冷凍ユニット(TRU)の発売を発表しました。これらのTRUは、ユーティリティの広範なディーラーネットワークを通じて、北米全域でユーティリティの有名な3000Rリーファートレーラーに独占的に搭載されます。

2023年8月、Muller Milk &Ingredients社は、冷凍・冷蔵トレーラーの代替電源としてソーラーパネルと運動エネルギーをテストしました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ別

- 冷凍食品

- チルド食品

- エンドユーザー別

- 乳製品

- 果物・野菜

- 肉・魚介類

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- 南米

- 中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Wabash National Commercial Trailer Products

- Great Dane Trailers Inc.

- Utility Trailer Manufacturing Company

- Schmitz Cargobull AG

- Kogel GmbH

- Lamberet Refrigerated SAS

- Fahrzeugwerk Beranrd KRONE GmbH

- Montracon Ltd

- Randon Implementos

- Grey & Adams Ltd

第7章 市場機会と今後の動向

The Refrigerated Trailer Market size is estimated at USD 6.70 billion in 2025, and is expected to reach USD 8.97 billion by 2030, at a CAGR of greater than 6% during the forecast period (2025-2030).

The refrigerated trailer market is experiencing robust growth driven by various factors, including the increasing demand for the transportation of temperature-sensitive goods, technological advancements in refrigeration systems, and expanding cold chain logistics infrastructure globally. Refrigerated trailers, also known as reefers, play a crucial role in transporting perishable goods such as food and pharmaceuticals over long distances while maintaining the desired temperature throughout the journey. With the rise in global food trade and the growing need to reduce food wastage, the demand for refrigerated trailers is expected to grow steadily in the coming years.

Moreover, stringent food safety regulations and quality standards set by governments and regulatory bodies across the world are compelling food producers, distributors, and logistics companies to invest in reliable refrigerated transportation solutions. Refrigerated trailers equipped with advanced temperature monitoring and control systems help ensure compliance with these regulations, safeguarding the quality of perishable goods during transit. In addition, increasing consumer awareness regarding food safety and quality is driving the adoption of refrigerated trailers by retailers and e-commerce companies for the transportation of fresh produce and other temperature-sensitive products.

Furthermore, the advent of electric and hybrid refrigerated trailers powered by sustainable energy sources is poised to revolutionize the refrigerated trailer market. As concerns over environmental sustainability and greenhouse gas emissions intensify, fleet operators and logistics companies are increasingly embracing eco-friendly refrigeration solutions to reduce their carbon footprint. Electric refrigerated trailers offer benefits such as quieter operation, reduced emissions, and lower operating costs compared to traditional diesel-powered trailers.

North America is the region leading the market, followed by Asia-Pacific and Europe. The major players manufacturing refrigerated trailers include Wabash National Commercial Trailer Products, Great Dane Trailers, Utility Trailer Manufacturing Company, Schmitz Cargobull AG, and Kogle Trailer GmbH.

Refrigerated Trailer Market Trends

Growing Cold Chain Logistics Activities are Expected to Drive the Refrigerated Trailer Market

This is an exciting period for cold-chain technology as various advancements in hardware, telematics, and vehicle technology are transforming the transportation of perishable goods across North America, prompting refrigerated fleets to contemplate strategies to stay competitive. However, the reefer community is facing challenges amid business conditions that are more complex than ever before. For instance,

- In February 2024, the agreement between Taikoo Motors, Zuellig Pharma, and Long Feng Medical Logistics officially marked the inaugural deployment of a Volvo FE Electric truck for cold chain logistics in Taiwan. The agreement underscores their collaborative efforts to advance eco-friendly transportation and usher in a fresh era of environmentally sustainable logistics.

While long-term contract freight rates remain stable, overall freight volume has decreased, leading many smaller refrigerated haulers to rely on the spot market for business opportunities. Spot refrigerated rates are approximately 7% lower than the same period in 2022 and more than 5% below their five-year average. Despite these obstacles, refrigerated fleets benefit from a relatively insulated segment of the trucking industry compared to other sectors like dry van transportation, which is experiencing significant upheaval due to factors such as fleet closures, regulatory changes, and shifts in market dynamics.

Asia-Pacific is Expected to Hold the Largest Market Share During the Forecast Period

With rising consumer preferences for fresh and perishable goods, particularly in densely populated urban areas, there is a heightened need for efficient and reliable refrigerated trailers to transport these products from production centers to distribution hubs and retail outlets across the region. Moreover, Asia-Pacific encompasses diverse climates ranging from tropical to temperate, further accentuating the importance of refrigerated trailers in maintaining the quality and safety of perishable goods throughout the supply chain. For instance,

- In Hong Kong, the cold chain logistics industry is witnessing increased demand for maintaining low temperatures throughout the supply chain process, from pickup and warehousing to order management, transportation, and delivery. Current cold chain services in Hong Kong have fallen short of meeting the expectations of food importers, wholesalers, retailers, and the catering industry, as many cold storage facilities lack temperature control once goods leave the cold room, resulting in the degradation of fresh ingredients. To address these deficiencies in Hong Kong's cold chain logistics services, TAHUHU introduced its first automated and intelligent cold chain logistics service in May 2023.

Furthermore, government initiatives aimed at improving food safety standards and modernizing transportation infrastructure are fueling the adoption of refrigerated trailers in Asia-Pacific. Countries such as China, India, Japan, and South Korea are witnessing significant investments in cold chain logistics infrastructure, including refrigerated warehouses, cold storage facilities, and refrigerated transportation fleets, to support the growing demand for temperature-sensitive products. Additionally, technological advancements in refrigeration systems, such as the integration of IoT (Internet of Things) sensors and real-time monitoring solutions, are enhancing the efficiency and reliability of refrigerated trailers, further driving market growth in the region.

Refrigerated Trailer Industry Overview

Refrigerated trailer manufacturing companies are adopting and developing various advanced technologies to make the trailers more efficient while adhering to environmental laws. Companies like Great Dane LLC, Wabash National Corporation, Kogel GmbH, Schmitz Cargobull AG, and Utility Manufacturing Company are the major players in the refrigerated trailer market.

In March 2024, the Annual Meeting & Transportation Technology Exhibition organized by the ATA Technology & Maintenance Council served as a platform to celebrate industry innovation, progress, and achievements. During this year's conference, Utility Trailer Manufacturing Company LLC announced the availability of the innovative Cargobull North America LLC (CBNA) transport refrigeration units (TRUs). These TRUs will be exclusively available on Utility's renowned 3000R reefer trailer throughout North America via Utility's extensive dealer network.

In August 2023, Muller Milk & Ingredients tested solar panels and kinetic energy as alternative power sources for its refrigerated trailers, seeking eco-friendly alternatives to diesel-powered refrigeration systems.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Frozen Food

- 5.1.2 Chilled Food

- 5.2 By End User

- 5.2.1 Dairy Products

- 5.2.2 Fruits and Vegetables

- 5.2.3 Meat and Seafood

- 5.2.4 Other End Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Wabash National Commercial Trailer Products

- 6.2.2 Great Dane Trailers Inc.

- 6.2.3 Utility Trailer Manufacturing Company

- 6.2.4 Schmitz Cargobull AG

- 6.2.5 Kogel GmbH

- 6.2.6 Lamberet Refrigerated SAS

- 6.2.7 Fahrzeugwerk Beranrd KRONE GmbH

- 6.2.8 Montracon Ltd

- 6.2.9 Randon Implementos

- 6.2.10 Grey & Adams Ltd