|

市場調査レポート

商品コード

1740841

冷凍トレーラー市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Refrigerated Trailer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 冷凍トレーラー市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年04月30日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

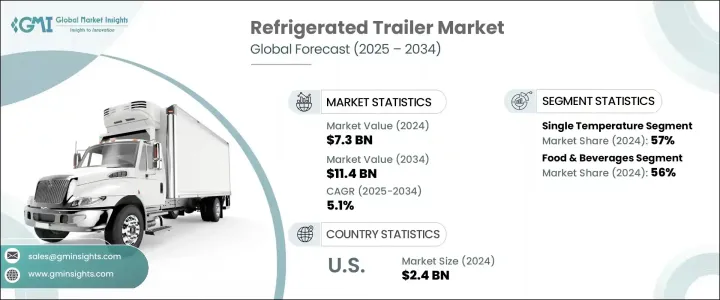

冷凍冷蔵トレーラーの世界市場規模は、2024年に73億米ドルとなり、CAGR 5.1%で拡大し、2034年には114億米ドルに達すると推定されています。

この成長の主な要因は、サプライチェーンの世界化の進展と、長距離にわたる生鮮品の効率的な輸送ニーズの高まりです。消費者の嗜好が世界中の新鮮で高品質な季節外れの商品へとシフトするにつれ、信頼性の高いコールドチェーン・ロジスティクスの需要が急増しています。この動向は、輸送品の完全性と品質を維持するために特定の温度帯の維持に依存する分野で特に顕著です。厳密な温度管理を必要とする国際輸送が増える中、冷蔵トレーラーは現代のロジスティクスに欠かせない要素となっています。世界の食品・医薬品ネットワークの進化は、都市化の進展やライフスタイルの変化と相まって、温度管理された輸送システムの必要性をさらに高めています。これらのトレーラーは、温度に敏感な商品を安全に到着させ、消費者の期待と規制基準の両方を満たすという重要な役割を果たしています。

食品流通に加え、医薬品・ヘルスケア業界も市場拡大の原動力としてますます重要な役割を果たしています。多くの医療品目では、輸送中も効果を維持するために正確な温度条件が要求されるようになっています。生物製剤や温度に敏感な治療薬の使用が増加しているため、信頼性の高いコールドチェーンインフラの必要性が高まっています。冷蔵トレーラーは、製品の有効性を保護し、厳しい業界ガイドラインへの準拠をサポートし、患者の安全性を高めるソリューションを提供します。医療システムと製薬会社がその範囲を拡大するにつれて、高度な温度制御ロジスティクス・ソリューションに対する需要は大きく伸びると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 73億米ドル |

| 予測金額 | 114億米ドル |

| CAGR | 5.1% |

温度タイプ別に見ると、冷凍冷蔵トレーラー市場は単一温度、マルチ温度、極低温のカテゴリーに区分されます。2024年には、単一温度セグメントが世界市場の約57%を占め、2034年までのCAGRは5%を超えると予測されています。単一温度トレーラーは、一定の温度条件下で均一な製品タイプを効率的に輸送できるため、広く好まれています。このセグメントの人気は、より複雑な構成に比べ、わかりやすい設計、操作の容易さ、運用コストの低さに起因しています。長距離輸送には、積載量が多く、メンテナンスの手間が少ない単一温度ユニットが好まれることが多いです。そのシンプルさは、特定の温度範囲を変動なく維持することを要求する数多くの世界の輸送ガイドラインにも合致しています。

用途別に分析すると、市場は飲食品、医薬品、化学品、その他に分類されます。2024年には、飲食品セグメントが56%の市場シェアを占め、2025年から2034年までのCAGRは5.4%を超えると予想されています。この分野は、生鮮品の腐敗を防ぐために輸送中に冷蔵保存する必要性が一貫してあるため、引き続きリードしています。食生活パターンの変化、冷凍食品消費の増加、食料品宅配サービスの拡大により、冷蔵トレーラーはこの分野で不可欠なものとなっています。食品の安全性と保管を取り巻く規制順守も、温度管理ロジスティクスの重要な役割を強化しています。国際的なサプライチェーンや進化する小売業態からの需要の高まりにより、効率的な低温輸送が最優先事項となっています。

材料の観点からは、軽量構造、強度、耐環境摩耗性などの有利な特性により、アルミニウムが市場で主導的地位を占めています。アルミベースのトレーラーは、燃費の向上と積載量の増加により、優位性を維持すると予測されます。2024年には、アルミニウムがメーカーやエンドユーザーの間で好まれています。その優れた熱伝導性により、内部温度が安定し、温度に敏感な商品の保存に不可欠です。耐用年数が長く、メンテナンスの必要性が低いことも、運用コストの削減に貢献しています。さらに、リサイクル可能な性質は、環境的に持続可能な輸送オプションを優先する企業にアピールします。

地域別では、米国が2024年の北米の冷凍冷蔵トレーラー市場をリードし、地域別シェアの約86%を占め、約24億米ドルの売上を生み出しました。この国の強い地位は、広範な物流ネットワーク、温度に敏感な製品の大規模な流通、厳格な輸送基準の実施によってもたらされました。エネルギー効率の高いシステムやスマートモニタリング機能など、トレーラー技術の進歩により、コールドチェーン事業の効率性と信頼性が向上しています。その結果、事業者は新しいフリート技術とリアルタイムの追跡に投資し、温度コンプライアンスを確保し、腐敗リスクを減らしています。

主な市場参入企業には、持続可能な技術、高度な断熱材、スマート・テレマティクスに多額の投資を行い、環境目標や業務上のニーズに応えている企業が含まれます。これらの企業はまた、より優れたエネルギー効率と低排出ガスを提供する電気式およびハイブリッド式冷凍ユニットを開発しています。製品革新は中核的な焦点であり、企業は多様な産業要件に対応するため、より軽量な素材、モジュール設計、カスタマイズ可能な機能を優先しています。戦略的提携と地理的拡大は、市場での存在感を強化し、地域横断的な顧客サービス能力を強化するために不可欠な戦術であり続けています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料サプライヤー

- 部品メーカー

- トレーラーメーカー

- ディーラーと販売代理店

- 最終用途

- 利益率分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 他国による報復措置

- 業界への影響

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 価格動向

- 地域

- コスト内訳分析

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 食品貿易の世界化と生鮮食品の需要の増加

- 加工食品と冷凍食品の需要増加

- 製薬・ヘルスケア分野の成長

- 冷凍ユニットの技術的進歩

- 厳格な食品安全および規制基準

- 業界の潜在的リスク&課題

- 初期費用と運用コストが高め

- 厳格な温度管理要件

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:温度別、2021-2034

- 主要動向

- 単一温度

- マルチ温度

- 極低温

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 食品と飲料

- 医薬品

- 化学薬品

- その他

第7章 市場推計・予測:材料別、2021-2034

- 主要動向

- アルミニウム

- 鋼鉄

- 複合

- プラスチック

第8章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 交通機関

- ストレージ

- 分布

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Carrier Transicold

- Faymonville

- Fruehauf Trailers

- Gray &Adams

- Great Dane Trailers

- Hwasung Thermo

- Hyundai Translead

- Kidron

- Kogel Trailer

- Krone Trailer

- Lamberet

- Manac

- MaxiTRANS

- Montracon

- Schmitz Cargobull

- Singamas Container

- Sinotruk

- Thermo King

- Utility Trailer Manufacturing Company

- Wabash National

The Global Refrigerated Trailer Market was valued at USD 7.3 billion in 2024 and is estimated to expand at a CAGR of 5.1% to reach USD 11.4 billion by 2034. This growth is largely fueled by the increasing globalization of supply chains and the rising need for efficient transportation of perishable products across long distances. As consumer preferences shift toward fresh, high-quality, and out-of-season items from around the world, the demand for reliable cold chain logistics has surged. This trend is particularly evident in sectors that depend on maintaining specific temperature ranges to preserve the integrity and quality of transported goods. With more international shipments requiring strict temperature control, refrigerated trailers have become a vital component of modern logistics. The evolution of global food and pharmaceutical networks, combined with growing urbanization and lifestyle changes, has further intensified the need for temperature-controlled transportation systems. These trailers play a key role in ensuring that temperature-sensitive goods arrive safely, meeting both consumer expectations and regulatory standards.

In addition to food distribution, the pharmaceutical and healthcare industries are playing an increasingly important role in driving market expansion. Many medical items now require precise temperature conditions to remain effective throughout transit. The growing use of biologics and temperature-sensitive therapeutics has heightened the need for dependable cold chain infrastructure. Refrigerated trailers provide a solution that safeguards product efficacy, supports compliance with strict industry guidelines, and enhances patient safety. As health systems and pharmaceutical companies expand their reach, the demand for advanced temperature-controlled logistics solutions is expected to grow significantly.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.3 Billion |

| Forecast Value | $11.4 Billion |

| CAGR | 5.1% |

By temperature type, the refrigerated trailer market is segmented into single temperature, multi-temperature, and cryogenic categories. In 2024, the single temperature segment accounted for approximately 57% of the global market and is projected to register a CAGR of over 5% through 2034. Single temperature trailers are widely preferred due to their efficiency in transporting uniform product types under consistent thermal conditions. This segment's popularity stems from its straightforward design, ease of operation, and lower operational costs compared to more complex configurations. Fleet managers often favor single-temperature units for long-distance hauls, as they offer higher payload capacity and demand less maintenance. Their simplicity also aligns with numerous global transportation guidelines, which require specific temperature ranges to be maintained without fluctuation.

When analyzed by application, the market is categorized into food and beverages, pharmaceuticals, chemicals, and others. In 2024, the food and beverages segment dominated with a 56% market share and is expected to grow at a CAGR exceeding 5.4% from 2025 to 2034. This segment continues to lead due to the consistent need for cold storage during transport to prevent spoilage of perishable goods. Shifting dietary patterns, the rise in frozen food consumption, and the expansion of grocery delivery services have made refrigerated trailers indispensable in this field. Regulatory compliance surrounding food safety and storage also reinforces the critical role of temperature-controlled logistics. Enhanced demand from international supply chains and evolving retail formats has made efficient cold transport a top priority.

From a materials standpoint, aluminum holds the leading position in the market due to its favorable attributes, such as lightweight construction, strength, and resistance to environmental wear. Aluminum-based trailers are projected to maintain dominance due to their ability to improve fuel efficiency and increase load capacity. In 2024, aluminum was the preferred choice among manufacturers and end-users alike. Its excellent thermal conductivity ensures that internal temperatures remain stable, which is essential for preserving temperature-sensitive goods. Its long service life and low maintenance requirements also contribute to reduced operating costs. Furthermore, its recyclable nature appeals to companies prioritizing environmentally sustainable transport options.

Regionally, the United States led the refrigerated trailer market in North America in 2024, accounting for nearly 86% of the regional share and generating around USD 2.4 billion in revenue. The country's strong position is driven by its extensive logistics networks, large-scale distribution of temperature-sensitive products, and the implementation of strict transportation standards. Advancements in trailer technologies, including energy-efficient systems and smart monitoring features, have made cold chain operations more efficient and reliable. As a result, operators are investing in new fleet technologies and real-time tracking to ensure temperature compliance and reduce spoilage risks.

Key market participants include companies that are investing heavily in sustainable technologies, advanced insulation, and smart telematics to meet environmental targets and operational needs. These companies are also developing electric and hybrid refrigeration units, offering better energy efficiency and lower emissions. Product innovation is a core focus, with firms prioritizing lighter materials, modular designs, and customizable features to serve diverse industry requirements. Strategic collaborations and geographic expansion remain essential tactics for reinforcing their market presence and enhancing customer service capabilities across regions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component manufacturers

- 3.2.3 Trailer manufacturers

- 3.2.4 Dealers and distributors

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures by other countries

- 3.4.2 Impact on the industry

- 3.4.2.1 Price volatility in key materials

- 3.4.2.2 Supply chain restructuring

- 3.4.2.3 Production cost implications

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Price trends

- 3.6.1 Region

- 3.7 Cost breakdown analysis

- 3.8 Patent analysis

- 3.9 Key news & initiatives

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Increasing globalization of food trade and demand for perishable goods

- 3.11.1.2 Rising demand for processed and frozen foods

- 3.11.1.3 Growth in the pharmaceutical and healthcare sectors

- 3.11.1.4 Technological advancements in refrigeration units

- 3.11.1.5 Stringent food safety and regulatory standards

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High initial and operational costs

- 3.11.2.2 Stringent temperature control requirements

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Temperature, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Single temperature

- 5.3 Multi-temperature

- 5.4 Cryogenic

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Food & beverages

- 6.3 Pharmaceuticals

- 6.4 Chemicals

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Aluminum

- 7.3 Steel

- 7.4 Composite

- 7.5 Plastic

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Transportation

- 8.3 Storage

- 8.4 Distribution

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Carrier Transicold

- 10.2 Faymonville

- 10.3 Fruehauf Trailers

- 10.4 Gray & Adams

- 10.5 Great Dane Trailers

- 10.6 Hwasung Thermo

- 10.7 Hyundai Translead

- 10.8 Kidron

- 10.9 Kogel Trailer

- 10.10 Krone Trailer

- 10.11 Lamberet

- 10.12 Manac

- 10.13 MaxiTRANS

- 10.14 Montracon

- 10.15 Schmitz Cargobull

- 10.16 Singamas Container

- 10.17 Sinotruk

- 10.18 Thermo King

- 10.19 Utility Trailer Manufacturing Company

- 10.20 Wabash National