|

市場調査レポート

商品コード

1690856

コンサルティングサービス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Consulting Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| コンサルティングサービス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 151 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

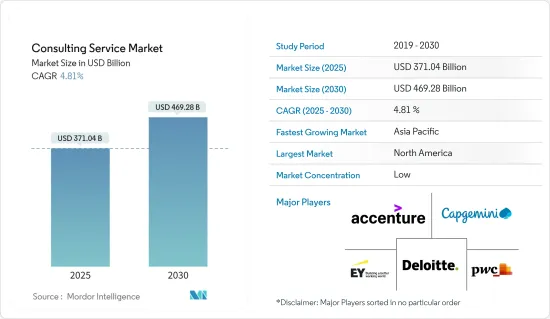

コンサルティングサービス市場規模は2025年に3,710億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.81%で、2030年には4,692億8,000万米ドルに達すると予測されます。

主要ハイライト

- コンサルティングサービス市場の成長は、いくつかの要因に影響されています。事業運営の複雑化、技術環境の進化、戦略的意思決定への注目の高まりが需要を後押ししています。企業は、課題を解決し、デジタル変革を実施し、全体的な効率を高めるために、外部の専門知識を求めています。グローバリゼーション、規制の変更、革新的なソリューションの必要性も市場の拡大に寄与しています。さらに、中小企業におけるコンサルティングサービスのメリットに対する意識の高まりも、市場の成長を後押ししています。

- 技術がビジネスに与える影響が拡大する中、コンサルティング会社は、技術とデータ分析をサービスに取り入れ、クライアントが時代の最先端を走り続けられるよう支援することを期待しています。技術主導型コンサルティングは、AI、機械学習、データ分析などの先進技術を活用して、複雑なビジネス問題の解決を支援するものです。このタイプのコンサルティングは、データ主導の意思決定、手作業によるプロセスの自動化、全体的なパフォーマンスの向上を支援します。コンサルティング会社はまた、技術を活用して、より革新的な方法でサービスを提供しています。例えば、仮想現実やオーグメンテッド・リアリティの技術を活用し、複雑なコンセプトを可視化したり、クラウドベースのプラットフォームを活用し、クライアントとリアルタイムで共同作業を行ったりすることができます。

- さらに、技術進歩の急速なペースは、人工知能、サイバーセキュリティ、イノベーションマネジメントなどのセグメントにおける専門コンサルティングの必要性を煽っています。企業は競合を維持するために、最先端のソリューションや産業のベストプラクティスを求めてコンサルタントを利用します。

- 世界のコンサルティング市場は、適応性と革新性で繁栄しています。変化への抵抗は、新しい手法や技術の採用を妨げ、このダイナミズムを阻害します。デジタルトランスフォーメーションが必要な時代において、変革に抵抗する組織は、イノベーションをより容易に受け入れる競合他社に追いつく必要があり、コンサルティングサービスの需要にさらに影響を与える可能性があります。

- COVID-19の流行により、全国の組織は従業員と地域社会の安全を確保するために必要なあらゆる措置を講じるようになりました。COVID-19の流行は、リモートワークの増加や企業のデジタル変革の拡大により、市場に利益をもたらしました。企業は、シームレスで効率的で、どこからでもアクセスできるビジネスプロセスを求めています。

コンサルティングサービス市場動向

業務コンサルティングサービスタイプが市場シェアの大半を占める

- 業務コンサルティングサービスは、主に業務効率を高めるために利用されます。このセグメントにおけるコンサルティング活動は、一次機能(営業、マーケティング、生産など)や二次機能(財務、人事、サプライチェーン、ICT、法務など)に対するアドバイザリーサービスから実践的な導入支援まで様々です。業務コンサルティングは、アドバイザリー部門で最大のセグメントを形成しています。

- 製造、サプライチェーンマネジメント、プロセスマネジメント、業務廃棄物削減などのアプリケーションの成長が、主に業務コンサルティングサービスの需要を牽引しています。サプライチェーン管理、プロセス管理、調達、アウトソーシングは、最も採用されている業務コンサルティングサービスの一部です。

- 業務効率を高め、業務コストを削減するために、業務コンサルティングの需要は伸びると予想されます。業務の非効率性は、企業にとって年間収益のかなりの部分を占めるコストになりかねないです。Acuity Knowledge Partnersのようなコンサルティング会社はSCMコンサルティングサービスを提供しており、同社はパンデミック後に大幅な需要の急増を目の当たりにしています。過去10年間で、サプライチェーンマネジメントソフトウェアと調達市場は2倍以上に拡大しました。

- 企業が事業のエコロジカル・フットプリントを高めるために多大な投資を行っているため、持続可能性に関するサプライチェーンマネジメントコンサルティングサービスが増加しています。この地域の企業は、過去数年間に確認されたサプライチェーンの混乱を認識し、将来を維持するために弾力性のあるサプライチェーンに焦点を当てています。

- また、先進地域では、公共部門における業務マネジメントの革新の実施に経営コンサルタントを起用する傾向が強まっています。異なる文化、構造、経営知識、投資パターンが公共サービスの妨げになることも多いです。業務コンサルティングサービスは、しばしば戦略や技術コンサルティングサービスと関連しているため、一方の成長が他方への需要を高めることになります。

北米が大きな市場シェアを占める見込み

- COVID-19のパンデミックは、パンデミックの課題から組織的にも財務的にも最善の形で脱却するために、産業を問わず企業による広範な変革の取り組みを加速させ、米国におけるコンサルティングサービスの需要につながりました。企業によって今後数年間計画されていた計画は、変化を起こし事業運営を推進するためのコンサルティングサービスの必要性を必要とし、市場に成長をもたらしました。

- エンドユーザーにおける気候制御とネットゼロ戦略の動向は、米国の市場ベンダーに機会をもたらしています。企業は、環境・社会・ガバナンス(ESG)への配慮を自社の戦略や業務に統合するため、コンサルティング支援を求める傾向が強まっています。

- 例えば、2023年1月、Boston Consulting Group(BCG)と米国船級協会(ABS)は、海洋とオフショアのバリューチェーンの顧客に脱炭素コンサルティングの共同サービスを提供するMoUを締結しました。この新たな共同サービスは、海運資産家がネットゼロ目標を達成するための技術的・運航的改善を支援し、炭素回収技術や代替・低炭素燃料の導入などに関するアドバイスを記載しています。

- カナダにおける技術コンサルティングの成長は緩やかです。カナダ製造業者・輸出業者協会(CME)とカナダ統計局(Statistics Canada)によるCME 2023技術導入調査によると、企業は事業運営のための技術投資に消極的でした。カナダの製造業部門は小規模企業で構成されており、従業員数百人以下の企業が93%を占め、技術導入率も低調でした。さらに調査では、製造業の28%がデジタル変革の初期段階にあり、12%はまだ着手していないと回答しています。

- 最近のカナダ・デジタル導入プログラム(CDAP)の取り組みは、中小企業のデジタル変革を支援し、カナダ連邦政府による国全体のデジタル導入を加速させるものです。これらは、カナダにおける技術コンサルティングサービスの需要を増大させることで、その前途を切り開くことになりそうです。

コンサルティングサービス産業概要

コンサルティングサービス市場は非常に細分化されており、数十年の産業経験を持つ国内外の参入企業が存在します。ベンダーは専門知識を活用することで、強力な競争戦略を取り入れています。市場参入企業の撤退障壁が比較的低いため、新規参入企業は参入しやすく、既存企業は利益が低くなると撤退しやすいです。McKinsey & Company、Bain & Company、Boston Consulting Group(BCG)、Deloitteなどの産業大手企業は、統合ソリューションの提供に重点を置き、顧客を惹きつけています。

- 2024年1月:Deloitteは、ニューヨークを拠点とするデジタル製品会社Giant Machinesの全資産を買収。Giant Machinesは革新的なデジタル製品の開発・設計に注力しており、Deloitte DigitalとDeloitte Engineeringは、戦略やスケールのソリューションを提供するためのエンジニアリングサービス一式をクライアントに提供する能力を強化しています。

- 2023年11月:Accentureは、Salesforceソリューションに特化したデジタルトランスフォーメーションコンサルティング会社であるIncapsulateを買収しました。Salesforceのプラチナコンサルティングパートナーとして、AccentureのSalesforce機能を強化。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の産業への影響評価

- 産業エコシステム分析

- 主要地域のホットスポット

- インダストリー4.0とデジタルトランスフォーメーションがコンサルティングサービス市場に与える影響

- コンサルティングサービス市場におけるデジタル化の役割分析

- 経営コンサルティング領域における一般的なビジネスモデル

第5章 市場力学

- 市場の促進要因

- 組織の効率化ニーズの高まり

- 市場課題

- クライアントのコスト削減策とクライアント組織内の変革への抵抗

第6章 市場セグメンテーション

- サービスタイプ別

- 業務コンサルティング

- 戦略コンサルティング

- 財務アドバイザリー

- 技術アドバイザリー

- その他

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- アジア

- オーストラリアとニュージーランド

- ラテンアメリカ

- ブラジル

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Deloitte Touche Tohmatsu Limited

- Accenture PLC

- Pricewaterhousecoopers LLP

- Ernst & Young Global Limited

- Capgemini SE

- KPMG International

- Boston Consulting Group Inc.

- A T Kearney Inc.

- Mckinsey & Company

- Bain & Company Inc.

- Roland Berger Holding Gmbh & Co. KGAA

- Simon-Kucher & Partners

- OC& C Strategy Consultants LLP

- Gartner Inc.

- Tata Consultancy Services

第8章 投資分析

第9章 市場機会と今後の動向

The Consulting Service Market size is estimated at USD 371.04 billion in 2025, and is expected to reach USD 469.28 billion by 2030, at a CAGR of 4.81% during the forecast period (2025-2030).

Key Highlights

- The growth of the consulting services market is influenced by several factors. Increased complexity in business operations, evolving technology landscapes, and a growing focus on strategic decision-making drive demand. Companies seek external expertise to navigate challenges, implement digital transformations, and enhance overall efficiency. Globalization, regulatory changes, and the need for innovative solutions also contribute to the expanding market. Additionally, the surge in awareness of the benefits of consulting services among small and medium-sized enterprises further fuels the market's growth.

- With the growing impact of technology on business, consulting firms anticipate incorporating technology and data analytics into their services to assist clients in staying ahead of the curve. Technology-driven consulting comprises the leverage of advanced technologies, like AI, machine learning, and data analytics, to assist clients in solving complex business problems. This type of consulting assists organizations in making data-driven decisions, automating manual processes, and increasing overall performance. Consulting firms are also leveraging the technology to offer their services in more innovative ways. For instance, they may leverage virtual and augmented reality technologies to assist the clients in visualizing complex concepts or leverage cloud-based platforms to collaborate with clients in real time.

- Furthermore, the rapid pace of technological advancement fuels the need for specialized consulting in areas such as artificial intelligence, cybersecurity, and innovation management. As organizations strive to stay competitive, they turn to consultants for cutting-edge solutions and industry best practices.

- The global consulting market thrives on adaptability and innovation. Resistance to change hinders this dynamic by impeding the adoption of new methodologies and technologies. In an age where digital transformation is necessary, organizations that resist transformation may need to catch up to competitors who embrace innovation more readily, further impacting the demand for consulting services.

- The outbreak of COVID-19 prompted organizations across the country to undertake all the necessary steps to ensure the safety of their employees and the community. The COVID-19 pandemic benefited the market, owing to the rise in remote working and the expanding digital transformation of enterprises. Businesses are looking for business processes that are seamless, efficient, and accessible from any location.

Consulting Service Market Trends

Operations Consulting Service Type to Hold Major Market Share

- Operations consulting services are mainly used to enhance operational efficiency. Consultancy activities in this segment differ from advisory services to hands-on implementation support for primary functions (e.g., sales, marketing, production, etc.) and secondary functions (e.g., finance, HR, supply chain, ICT, legal, etc.). Operations consultancy forms the largest segment within the advisory branch.

- Growth in applications such as manufacturing, supply chain management, process management, and operation waste reduction, among others, mainly drives the demand for operation consulting services. Supply chain management, process management, procurement, and outsourcing are some of the most adopted operations consulting services.

- Demand for operation consulting is expected to grow to enhance operational efficiency and reduce operations costs. Operation inefficiency can cost a business a considerable share of its revenue annually. Consultancies such as Acuity Knowledge Partners offer SCM consulting services, and the company has witnessed a significant surge in demand after the pandemic. Over the last decade, the supply chain management software and procurement market expanded more than twice.

- Supply chain management consulting services concerning sustainability practices are increasing as companies invest significantly in boosting the ecological footprint of their operations. Businesses in the region have acknowledged the supply chain disruption witnessed in the past years and focused on resilient supply chains to sustain the future.

- The developed regions also witnessed the growing trend of engaging management consultancies in implementing operations management innovations in the public sector. Different cultures, structures, managerial knowledge, and investment patterns often hamper public services. Operations consulting services are often associated with strategy and technology consulting services; therefore, growth in one eventually fuels the demand for others.

North America is Expected to Hold Significant Market Share

- The COVID-19 pandemic accelerated broader transformation initiatives by businesses across industries to come out of pandemic challenges in the best possible organizational and financial shape, leading to the demand for consulting services in the United States. The plan that had been planned for the coming years by the business has necessitated the need for consulting services to make changes and drive business operations, adding growth to the market.

- The trend of climate control and net zero strategy in end users is creating an opportunity for market vendors in the United States. Companies increasingly seek consulting support to integrate environmental, social, and governance (ESG) considerations into their strategies and operations.

- For instance, in January 2023, Boston Consulting Group (BCG) and the American Bureau of Shipping (ABS) signed a MoU to offer joint services in decarbonization consulting to marine and offshore value chain clients. The new joint offering can support shipping asset owners in making technical and operational improvements to reach net-zero goals and provide advice on carbon capture technology and the uptake of alternative and low-carbon fuels, among other areas.

- Technology consulting in Canada is growing slowly as technology adoption among businesses in the country needs to catch up. According to the CME 2023 Technology Adoption Survey by Canadian Manufacturers & Exporters (CME) and Statistics Canada, businesses were reluctant to invest in technology for their operations. The manufacturing sector in Canada was composed of small businesses, with 93% of businesses having fewer than 100 workers and a slower technology adoption rate. Further, the survey stated that 28% of manufacturing businesses were at the beginning of digital transformation, and 12% said they were yet to start.

- Recent Canadian Digital Adoption Program (CDAP) initiatives support small and medium-sized enterprises (SMEs) to digitally transform their businesses and accelerate digital adoption across the country by the Canadian Federal Government. These are likely to create their way ahead by increasing the demand for technology consulting services in Canada.

Consulting Service Industry Overview

The consulting service market is highly fragmented, with local and international players having decades of industry experience. The vendors are incorporating a powerful competitive strategy by leveraging their expertise. The market has relatively low exit barriers, which encourages new enterprises to participate and established firms to withdraw when profits are low. Major industry players, like McKinsey & Company, Bain & Company, Boston Consulting Group (BCG), and Deloitte, emphasize providing integrated solutions to attract customers.

- January 2024: Deloitte acquired all assets of Giant Machines, a digital product company based in New York City. Giant Machines focuses on developing and designing innovative digital products, helping Deloitte Digital and Deloitte Engineering to strengthen their ability to provide clients with a full suite of engineering services to deliver strategy and scale solutions.

- November 2023: Accenture acquired Incapsulate, a digital transformation consulting firm specializing in Salesforce solutions. As a Salesforce Platinum Consulting partner, Incapsulate strengthens Accenture's Salesforce capabilities, which mainly focus on assisting clients to utilize data and AI-driven insights to transform how they connect with customers and meet their ever-evolving needs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers/Consumers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Industry

- 4.4 Industry Ecosystem Analysis

- 4.5 Key Regional Hotspots

- 4.6 Impact of Industry 4.0 and Digital transformation -Related Practices on the Consulting Services Market

- 4.7 Analysis of the Role of Digitization in the Consulting Services Market

- 4.8 Prevalent Business Models in the Management Consulting Domain

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Need for Organizational Efficiency

- 5.2 Market Challenges

- 5.2.1 Client Cost-cutting Measures and Resistance to Change Within Client Organization

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 Operations Consulting

- 6.1.2 Strategy Consulting

- 6.1.3 Financial Advisory

- 6.1.4 Technology Advisory

- 6.1.5 Other Service Types

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.2.4 Italy

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.5.1 Brazil

- 6.2.6 Middle East and Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Deloitte Touche Tohmatsu Limited

- 7.1.2 Accenture PLC

- 7.1.3 Pricewaterhousecoopers LLP

- 7.1.4 Ernst & Young Global Limited

- 7.1.5 Capgemini SE

- 7.1.6 KPMG International

- 7.1.7 Boston Consulting Group Inc.

- 7.1.8 A T Kearney Inc.

- 7.1.9 Mckinsey & Company

- 7.1.10 Bain & Company Inc.

- 7.1.11 Roland Berger Holding Gmbh & Co. KGAA

- 7.1.12 Simon-Kucher & Partners

- 7.1.13 OC&C Strategy Consultants LLP

- 7.1.14 Gartner Inc.

- 7.1.15 Tata Consultancy Services