|

市場調査レポート

商品コード

1406913

小火器:市場シェア分析、産業動向と統計、2024~2029年の成長予測Small Arms - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 小火器:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 102 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

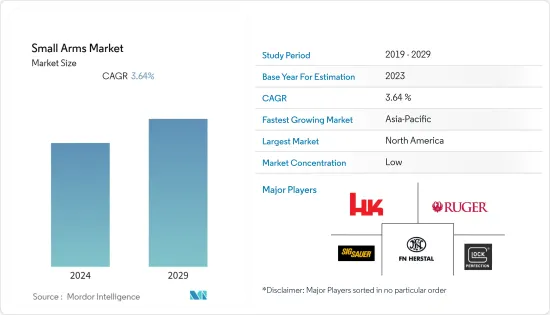

小火器市場は、2024年の94億3,000万米ドルから2029年には112億8,000万米ドルに増加し、予測期間中のCAGRは3.64%を記録すると予想されます。

世界の国防支出の増加と歩兵装備のアップグレードプログラムの開始は、洗練されたより殺傷能力の高い軍用ライフルの調達を促進しています。また、軽量で精度の高い新世代の小火器の独自開発に注力している国もあります。技術の進歩がこうした開発を促進しています。その一方で、個人で銃を入手する際には厳しい法律を設けている国もあります。近年、自殺や銃乱射事件が増加しており、その結果、銃規制が強化されています。この要因は、民間部門における小火器市場の成長に課題となっています。

小火器市場の動向

予測期間中も軍事セグメントが優位を維持する見込み

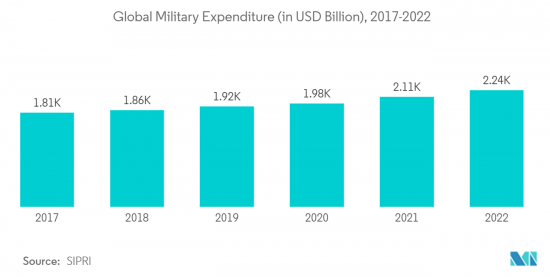

軍事セグメントは予測期間中、市場で顕著な成長を示すと予測されます。世界の国防費は年々増加しており、これが世界の小火器需要を牽引する主要因の一つとなっています。ストックホルム国際平和研究所(SIPRI)によると、2022年の世界軍事支出は2兆2,400億米ドルで、2021年の世界軍事支出を3.7%上回った。また、世界の軍事交戦の増加に伴い、武装勢力は戦闘要件に対処するため、より強力な小火器にアップグレードしています。さらに、軍隊が着用する装甲の貫通が厳しくなっているため、軍隊は周期的な衝撃を与え、敵により大きなダメージを与える銃器に注力しています。いくつかの国は現在、自国軍のために多種多様な最新世代の小火器の調達に力を入れています。例えば2022年1月、インド軍はAK203アサルトライフルの調達・製造という大型契約の一環として、ロシアから7万丁のライフル銃の初回ロットを受け取ったと発表しました。最初のバッチは、COVID-19の大流行にもかかわらず、インドの要求通り速いペースで納入されました。残りのライフルはインド国内で製造され、60万丁以上のAK203を必要とする主要顧客である陸軍に納入される予定です。同様に、フランス軍は抜本的な近代化プログラムを開始し、その一環としてFR-F2ボルトアクション狙撃銃を更新しています。同軍は、ベルギーのFNハースタル社から新型狙撃銃SCAR-H PRを調達しています。陸軍は2023年までに2235丁を実戦投入する計画です。このような調達は、予測期間中の同分野の成長を促進すると予想されます。

北米が小火器市場で上位を占める

予測期間中、北米は主に米国とカナダからの高い需要によって小火器市場をリードすると予想されます。2022年に発表されたSIPRI報告書によると、米国は世界最大の国防支出国であり、国防予算は8,770億米ドルでした。同国の国防費の高さは、新世代小火器の調達により多くの費用をかけることを可能にしています。また、ロシアや中国といった政敵が次世代兵器を採用したことで、米国も同様のアプローチを採用し、軍隊の能力強化に向けて多額の投資を行うようになった。積極的な戦闘活動に加え、米国の要員は通常、いくつかの平和維持活動や軍事派遣、大使館や領事館の警備、その他いくつかの機密任務の一部として派遣されています。こうした派兵は、米国軍による小火器の調達拡大に大きく寄与しています。

米国軍は、敵の陣地を制圧し、友軍の動きを自由にし、遠く離れた目標を攻撃し、要塞化された建造物や車両を無力化するために設計されたいくつかの歩兵用武器を使用しています。米国は現在、歩兵用の次世代分隊兵器の調達に力を入れています。次世代分隊兵器の設計は、5年近くの開発期間を経て、最終決定される予定です。2022年半ばには、現在地上戦の兵士が手にしているM4カービンとM249機関銃に取って代わることになります。次世代分隊兵器プログラムから生まれた2つの兵器は、歩兵、騎兵偵察兵、戦闘衛生兵、前方監視兵、戦闘工兵、特殊作戦部隊など、最前線の軍事職業専門職の兵士に実戦配備されます。他方、米国の民間銃器ユーザー層も著しく高く、同国が長年にわたって堅調な小火器産業の本拠地となるのに貢献しています。したがって、民間部門と軍事部門の両方からの需要は、予測期間中、この地域の市場にプラスの影響を与え続けると予想されます。

小火器産業の概要

小火器市場は適度に断片化されており、複数のプレーヤーが市場で大きなシェアを占めています。同市場の主要プレイヤーには、Heckler &Koch GmbH、Sturm, Ruger &Co.Inc.、GLOCK Gesellschaft m.b.H.、FN Herstal SA、Sig Sauer, Inc.などです。同市場の主要OEMは、新規顧客の獲得につながる高品質で長寿命、高精度、人間工学に基づいた製品の製造に注力しています。例えば、2021年11月、ロシアのLobaev Arms CorporationはDXL-5「Havoc」スナイパーライフルを発表したが、同社によれば、これはロシアで最も強力なスナイパーライフルです。この武器は50 BMG口径のライフル弾を装弾します。この市場で受注される契約の大半は、数量が多い大規模な調達であるため、企業は契約あたりの収益が高いという恩恵を受ける可能性があります。同時に、小火器契約を獲得しようとする企業間の競争も激しいです。小火器製造能力を増強している国もあるため、市場競争は今後さらに激化することが予想されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- エンドユーザー別

- 民間および法執行機関

- 軍事

- タイプ別

- ハンドガン

- マシンガン

- ショットガン

- ライフル

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- エジプト

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Vista Outdoor Inc.

- Sturm, Ruger & Co. Inc.

- Sig Sauer Inc.

- Heckler and Koch GmbH

- JSC Kalashnikov Concern

- Fabbrica d'Armi Pietro Beretta SpA

- FN Herstal

- Barret Firearms

- Springfield Armory Inc.

- Browning Arms Company

- Winchester Repeating Arms

- Benelli Armi SpA

- SMITH & WESSON BRANDS, INC.

- Armscor International Inc.

- GLOCK Gesellschaft m.b.H.

- Colt's Manufacturing Company LLC

第7章 市場機会と今後の動向

The small arms market is expected to increase from USD 9.43 billion in 2024 to USD 11.28 billion by 2029, registering a CAGR of 3.64% during the forecast period.

The growth in global defense spending and initiation of infantry equipment upgrade programs is facilitating the procurement of sophisticated and deadlier military rifles. Also, several countries are focusing on the indigenous development of newer generation small arms that are lightweight and accurate. The growth in technological advancements is fostering such developments. On the other hand, several countries hold strict laws when it comes to acquiring a gun as an individual. In recent years, there is an increase in suicides and gun violence, which resulted in increased gun control measures. This factor is challenging the growth of the small arms market in the civilian sector.

Small Arms Market Trends

Military Segment Expected to Continue its Dominance During the Forecast Period

The military segment is projected to show remarkable growth in the market during the forecast period. Global defense spending is increasing each year, which is among the major factors driving the demand for small arms globally. According to the Stockholm International Peace Research Institute (SIPRI), the global military expenditure in 2022 was USD 2,240 billion, which was 3.7% higher than the global military expenditure in 2021. Also, with the increase in military engagements globally, armed forces are upgrading to more powerful small arms to deal with combat requirements. Additionally, with the armor being worn by the militaries becoming tougher to penetrate, armies are focusing on firearms that cause cyclical impacts, causing more damage to enemies. Several nations are now focusing on procuring a wide variety of latest-generation small arms for their militaries. For instance, in January 2022, the Indian armed forces announced that they had received the first batch of 70,000 rifles from Russia as part of a larger contract to procure and manufacture AK 203 assault rifles. The initial batch was delivered at a fast pace, as requested by India, despite the COVID-19 pandemic. The remaining rifles will be manufactured locally in India and will be delivered to the army, which is the main customer with a requirement of over 600,000 AK 203s. Likewise, the French Armed Forces initiated a radical modernization program as part of which they are replacing their FR-F2 bolt action sniper rifles. The army is procuring a new sniper rifle, SCAR-H PR, from the Belgian company FN Herstal. The army plans to put 2,235 units into service by 2023. Such procurements are expected to drive the segment's growth during the forecast period.

North America Holds Highest Shares in the Small Arms Market

North America is expected to lead the small arms market during the forecast period primarily due to high demand from the United States and Canada. According to the SIPRI report published in 2022, the US was the largest defense spender in the world, with a defense budget of USD 877 billion. The high defense spending of the country is enabling it to spend more on procuring new-generation small arms. Also, the adoption of next-generation weaponry by political rivals such as Russia and China encouraged the United States to adopt a similar approach and invest significantly toward enhancing the capabilities of its armed forces. In addition to active combat, the US personnel are typically deployed as part of several peacekeeping missions and military attaches or are part of the embassy, consulate security, and several other classified missions. Such deployments significantly contributed toward the growth of the procurement of small arms by the US armed forces.

The US forces use several infantry weapons designed to suppress enemy positions, free up movement for friendly troops, assault far-away targets, and neutralize fortified structures and vehicles. The United States is now focused on procuring the next-generation squad weapon for its infantry. After nearly five years of development, the army is expected to finalize the design for its Next Generation Squad Weapon. It is to replace the M4 carbine and M249 machine guns currently in the hands of ground combat soldiers in mid-2022. The two weapons that come out of the Next Generation Squad Weapon program will be fielded to soldiers in frontline military occupational specialties, including infantry, cavalry scouts, combat medics, forward observers, combat engineers, and special operations forces. On the other hand, the civilian gun user base in the United States is also significantly high, helping the country become home to a robust small arms industry over the years. Thus, the demand from both the civilian and military sectors is expected to continue a positive influence on the market in the region during the forecast period.

Small Arms Industry Overview

The small arms market is moderately fragmented, with the presence of several players holding significant shares in the market. Some of the key players in the market are Heckler & Koch GmbH, Sturm, Ruger & Co. Inc., GLOCK Gesellschaft m.b.H., FN Herstal SA, and Sig Sauer, Inc. Key OEMs in the market are focusing on building long-lasting, accurate, ergonomic products with high quality that will help them attract new customers. For instance, in November 2021, Russia's Lobaev Arms Corporation unveiled the DXL-5 'Havoc' sniper rifle, which, according to the company, is the most powerful sniper rifle in Russia. The weapon is chambered with 50 BMG caliber rifle ammunition. As most of the contracts awarded in the market comprise large procurements with higher volumes, companies may benefit from higher revenues per contract. At the same time, there is intense competition among players to obtain small arms contracts. With several countries increasing their local small arms manufacturing capabilities, the competition in the market is expected to intensify further in the years to come.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 End User

- 5.1.1 Civil and Law Enforcement

- 5.1.2 Military

- 5.2 Type

- 5.2.1 Handgun

- 5.2.2 Machine Gun

- 5.2.3 Shotgun

- 5.2.4 Rifle

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Egypt

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Vista Outdoor Inc.

- 6.2.2 Sturm, Ruger & Co. Inc.

- 6.2.3 Sig Sauer Inc.

- 6.2.4 Heckler and Koch GmbH

- 6.2.5 JSC Kalashnikov Concern

- 6.2.6 Fabbrica d'Armi Pietro Beretta SpA

- 6.2.7 FN Herstal

- 6.2.8 Barret Firearms

- 6.2.9 Springfield Armory Inc.

- 6.2.10 Browning Arms Company

- 6.2.11 Winchester Repeating Arms

- 6.2.12 Benelli Armi SpA

- 6.2.13 SMITH & WESSON BRANDS, INC.

- 6.2.14 Armscor International Inc.

- 6.2.15 GLOCK Gesellschaft m.b.H.

- 6.2.16 Colt's Manufacturing Company LLC

7 MARKET OPPORTUNITIES AND FUTURE TRENDS