|

|

市場調査レポート

商品コード

1440258

ジェネリック医薬品:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Generic Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ジェネリック医薬品:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

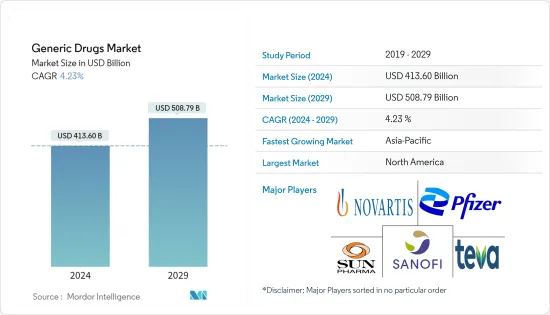

ジェネリック医薬品市場規模は、2024年に4,136億米ドルと推定され、2029年までに5,087億9,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に4.23%のCAGRで成長します。

新型コロナウイルス感染COVID-19は、ロックダウンの制限やサプライチェーンの混乱により、パンデミック初期にジェネリック医薬品市場に深刻な影響を与えました。その後、COVID-19感染症によりジェネリック医薬品メーカーがこの感染症の治療薬を製造する機会が多くなったため、ジェネリック医薬品の需要が増加しました。患者に対するウイルスの影響に対抗するために、人工呼吸器やステロイドを使用している患者向けの点滴薬などの後発医薬品が使用され、COVID-19感染症による死亡者数の減少に貢献しました。たとえば、2021年11月に発行されたUSFDAの報告書によると、FDAはジェネリック医薬品プログラムを実施しました。この取り組みは、開発プロセスの初期および申請審査中に規制当局の期待を明確にするために書面による連絡を送信し、会議を開催することにより、ジェネリック医薬品開発者の製品開発を支援しました。 2020年にFDAは、製品開発および提出前の事前短縮NDA会議に関する121件の要請を受け取りました。したがって、このような取り組みは、パンデミック後の段階で市場の成長にプラスの影響を与えました。したがって、分析によると、調査対象の市場は、ジェネリック医薬品の需要が増加すると予想されるため、予測期間にわたって同じ傾向に従うと予想されます。

さらに、市場の成長の理由として、慢性疾患の有病率の増加、高齢者人口の急増、ヘルスケア費の増加が挙げられています。世界185カ国における36のがんの発生率と死亡率を推定した国際がん調査機関(IARC)の2020年報告書によると、2020年には世界中で推定1,930万人の新たながん症例が診断され、がんと診断された症例の総数は、男性で1,010万件以上、女性で930万件以上が報告されています。さらに、世界RAネットワークの2021年の報告書によると、世界で3億5,000万人以上の人々が関節炎を抱えて暮らしており、その負担はさまざまな要因により増加すると予想されており、その1つは世界中の高齢者人口の負担の増加です。したがって、慢性疾患の有病率の増加により、効果的な治療に対する需要が急増し、それによって予測期間中にジェネリック医薬品市場の成長が促進されると予想されます。

さらに、高齢者は慢性疾患にかかりやすいため、予防と治療のための効果的な治療オプションに対する需要が増加し、それによって市場の成長が促進されます。 2021年のWHOのデータによると、世界人口に占める60歳以上の人口の割合は、2015年から2050年の間に12%から22%へとほぼ2倍に増加します。2050年までに、世界の高齢者の80%が低所得者および中所得者層で暮らすことになります。人口の高齢化は以前に比べてかなり急速に進んでおり、この人口構成は慢性疾患に苦しむ可能性も高いため、ジェネリック医薬品の需要が増加し、市場の拡大が加速すると考えられます。

さらに、主要な市場プレーヤーが採用するさまざまな有機的および無機的戦略が市場の成長をサポートすると予想されます。 2022年2月、ジャム・ファーマ・グループは、注意欠陥多動性障害(ADHD)を治療する武田カナダ社の参考製品INTUNIV XRのジェネリック版であるグアンファシンXRを発売しました。さらに、2021年10月、中国の長江製薬グループは、てんかん患者の治療に使用されるクラス3のジェネリック医薬品である酢酸エスリカルバゼピンの最初の販売申請を提出しました。さらに、2021年7月には、鉄欠乏性貧血(IDA)の治療に使用される注射薬であるジェネリックフェルモキシトールが、ジェネリック医薬品およびバイオシミラー医薬品の世界的リーダーであるサンド社によって米国で発売されました。

したがって、前述の要因に基づいて、市場は予測期間中に大幅に成長すると予想されます。ただし、政府の厳しい規制により、予測期間中に市場が抑制される可能性があります。

ジェネリック医薬品市場動向

経口セグメントは予測期間中に市場でかなりのシェアを保持すると予想される

経口ジェネリック医薬品は、最も簡単、最も便利、そして最も安全な薬剤投与手段です。繰り返して長期間使用するのに便利で、自己投与でき、痛みもありません。したがって、それらは最も使用され、製造される薬物の形態です。

新製品の発売とコラボレーションの増加により、この分野の成長が促進されると予想されます。 上市により、経口ジェネリック製品の販売と製造が増加し、この部門の成長が促進されます。

さらに、メルク社は2021年10月に、国連が支援する医薬品特許プール(MPP)とライセンシング契約を締結し、より多くの企業が同社の実験的経口抗ウイルスCOVID-19感染症治療薬のジェネリック版を製造できるようになった。このようなコラボレーションにより、今後数年間でこの分野の成長が促進される可能性があります。

したがって、上記の要因により、このセグメントは予測期間中に成長が拡大すると予想されます。

アジア太平洋は市場で健全なCAGRで推移すると予想されており、予測期間中にも同様の成長が見込まれる

アジア太平洋は、この地域における医学的疾患に関する人々の意識の高まりと高齢化人口の増加により、世界のジェネリック市場で最も急成長する傾向にあると予想されています。アジア太平洋地域のインドや中国のような国は、他の国よりも多くの貢献をしています。国際人口科学研究所(IIPS)が2021年1月に発表した研究結果によると、60歳以上のインド人約7,500万人が何らかの慢性疾患を抱えていました。約4,500万人が心血管疾患と高血圧を患っており、約2,000万人が糖尿病に苦しんでいます。したがって、この国における慢性疾患の罹患率の高さは、費用対効果の高い治療薬への需要を高め、それによって調査対象市場を推進すると考えられます。

IBEFが2021年11月に発行したインド製薬産業レポートによると、インドはジェネリック医薬品の世界最大の供給国です。インドの製薬産業は、米国のジェネリック需要の40%、英国の全医薬品の25%を供給しています。

主要な市場プレーヤーによるパートナーシップ、合併、買収などの戦略的および非戦略的取り組みは、市場の成長にさらに貢献すると予想されます。たとえば、2022年1月、Lupinはインドの患者に高品質のジェネリック医薬品および複雑なジェネリック医薬品を提供するために、深センFoncoo Pharmaceutical Co.とパートナーシップ契約を締結しました。

したがって、前述の要因により、アジア太平洋地域は予測期間中により速いペースで成長すると予想されます。

ジェネリック医薬品業界の概要

世界のジェネリック医薬品市場は競争が激しく、多くのプレーヤーが市場を独占しています。市場関係者は、激化する市場競争を維持するために、研究開発投資の増加、合併、買収、製品革新などの戦略を採用しています。主要な市場プレーヤーには、Mylan NV、Eli Lilly and Company、GlaxoSmithKline PLC、Pfizer Inc.、Sun Pharma、Novartis、Sanofiが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 慢性疾患の有病率の増加

- 高齢者人口の増加

- ヘルスケア費の増加

- 市場抑制要因

- 政府の厳しい規制

- 薬に伴う副作用

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 投与経路別

- 経口

- 外用

- 注射

- その他の投与経路(舌下、直腸)

- 用途別

- 心臓血管製品

- 抗感染症薬

- 抗関節炎薬

- 中枢神経系の薬

- 抗がん剤

- 呼吸器製品

- その他の用途(胃腸薬、ホルモン薬)

- 流通チャネル別

- 病院・診療所

- 小売薬局

- その他の流通チャネル(オンライン薬局、専門ドラッグストア)

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Mylan(Viatris Inc.)

- Abbott Laboratories

- Teva Pharmaceutical Industries Limited

- Eli Lilly and Company

- STADA Arzneimittel AG

- GlaxoSmithKline PLC

- Baxter International Inc.

- Pfizer Inc.

- Sanofi

- Novartis AG(Sandoz International)

- Sun Pharma

- AbbVie Inc.(Allergan)

第7章 市場機会と将来の動向

The Generic Drugs Market size is estimated at USD 413.60 billion in 2024, and is expected to reach USD 508.79 billion by 2029, growing at a CAGR of 4.23% during the forecast period (2024-2029).

COVID-19 severely impacted the generic drugs market during the early pandemic due to lockdown restrictions and supply chain disruption. Later, there was an increased demand for generic pharmaceuticals as the COVID-19 infections provided many opportunities for generic drug manufacturers to manufacture the drugs to treat this infection. As the COVID-19 public health emergency unfolded last year, the FDA shifted its focus to generic drug submissions involving potential treatments and supportive therapies for COVID-19 patients. To combat the virus's effects on patients, generic medicines such as intravenous drugs for patients on ventilators and steroids were used, which helped reduce COVID-19 fatalities. For instance, according to a report by the USFDA published in November 2021, the FDA has implemented a generic drug program. This initiative assisted generic medication developers with product development by sending written communications and holding meetings to clarify regulatory expectations early in the development process and during application review. The FDA received 121 requests for product development and pre-submission pre-abbreviated NDA meetings in 2020. Thus, such initiatives have positively impacted market growth in the post-pandemic phase. Thus, as per the analysis, the market studied is expected to follow the same trend over the forecast period as the demand for generic drugs is expected to increase.

Furthermore, the reasons attributed to the growth of the market are the increasing prevalence of chronic diseases, a surge in the geriatric population, and growing healthcare expenditure. As per the 2020 report of the International Agency for Research on Cancer (IARC), which estimated the incidence and mortality of 36 cancers in 185 countries globally, an estimated 19.3 million new cases of cancer were diagnosed in 2020 all over the world, and from the total number of diagnosed cancer cases, over 10.1 million cases were reported in males and 9.3 million cases were reported in females. Additionally, according to the 2021 report of the Global RA Network, more than 350 million people are living with arthritis around the world, and its burden is expected to increase owing to various factors, one of which is the rising burden of the geriatric population around the globe. Thus, the growing prevalence of chronic diseases is expected to surge the demand for effective treatment, thereby boosting the growth of the generic drug market over the forecast period.

Furthermore, the geriatric population is more susceptible to chronic diseases, which increases the demand for effective treatment options for prevention and treatment, thereby boosting the market's growth. According to the WHO data for 2021, the proportion of the global population aged 60 and above will nearly double from 12% to 22% between 2015 and 2050. By 2050, 80% of the world's elderly will live in low- and middle-income countries. The population is aging considerably more quickly than in the past, and this demographic is also more likely to suffer from chronic diseases, which will likely increase demand for generic drugs and accelerate market expansion.

Additionally, various organic and inorganic strategies adopted by the key market players are expected to support the growth of the market. In February 2022, Jamp Pharma Group launched Guanfacine XR, a generic version of the reference product INTUNIV XR from Takeda Canada Inc. that treats attention deficit hyperactivity disorder (ADHD). Moreover, in October 2021, The Yangtze River Pharmaceutical Group in China submitted the first marketing application for eslicarbazepine acetate, a class 3 generic medication used to treat epileptic patients. In addition, in July 2021, Generic Ferumoxytol, an injectable drug used to treat iron deficiency anemia (IDA), was launched in the United States by Sandoz, a global leader in generic and biosimilar medicines.

Hence, based on the aforementioned factors, the market is expected to grow significantly during the forecast period. However, stringent government regulation may restrain the market over the forecast period.

Generic Drugs Market Trends

Oral Segment is Expected to Hold Significant Share in the Market Over the Forecast Period

Oral generics are the simplest, most convenient, and safest means of drug administration. They are convenient for repeated and prolonged use and can be self-administered and pain-free; hence, they are the most used and manufactured form of drugs.

The growing launches and collaborations are expected to boost the segment's growth. In January 2022, the Medicines Patent Pool (MPP) announced that it had signed agreements with 27 generic manufacturing companies for the manufacturing of the oral COVID-19 antiviral medication molnupiravir and its supply in 105 low- and middle-income countries. In February 2022, Oakrum Pharma, LLC, in collaboration with ANI Pharmaceuticals, announced that the USFDA had approved the ANDA for a generic version of Cystadane1 (betaine anhydrous for oral solution) Powder in a 180-gram bottle and granted competitive generic therapy (CGT) 180 days of exclusivity. Such launches increase the sales and manufacture of oral generic products, boosting the segment's growth.

In addition, in October 2021, Merck & Co. signed a licensing agreement with the United Nations-backed Medicines Patent Pool (MPP) that will allow more companies to manufacture generic versions of its experimental oral antiviral COVID-19 treatment. Such collaborations are likely to boost the segment's growth over the coming years.

Thus, owing to the factors mentioned above, the segment is expected to expand its growth over the forecasted period.

Asia-Pacific is Expected to Registered Healthy CAGR in the Market and Expected to do Same in the Forecast Period

Asia-Pacific is anticipated to witness the fastest-growing trend in the global generic market owing to increased awareness among people related to medical disorders and the growing aging population in the region. Countries like India and China in the Asia-Pacific region contribute more than the other nations. According to a study published by the International Institute for Population Sciences (IIPS), in January 2021, approximately 75 million Indians over the age of 60 had some form of chronic disease. About 45 million people have cardiovascular disease and hypertension, and about 20 million suffer from diabetes. Thus, the high prevalence of chronic diseases in the country will boost the demand for cost-effective therapeutics, thereby driving the studied market.

According to the Indian Pharmaceutical Industry Report published in November 2021 by IBEF, India is the world's top supplier of generic pharmaceuticals. The Indian pharmaceutical industry supplies 40% of the generic demand in the United States and 25% of all pharmaceuticals in the United Kingdom.

Strategic and non-strategic initiatives such as partnerships, mergers, and acquisitions by key market players are further expected to contribute to market growth. For instance, in January 2022, Lupin signed a partnership agreement with Shenzhen Foncoo Pharmaceutical Co. to bring high-quality generic and complex generic medicines to patients in India. Further, in October 2021, Dr. Reddy's Laboratories launched an anti-cancer drug in the Chinese market through its joint venture, Kunshan Rotam Reddy Pharmaceutical Co. Ltd. (KRRP). The drug is a therapeutic equivalent generic version of Zytiga, which is owned by Johnson & Johnson.

Therefore, owing to the aforementioned factors, the Asia-Pacific region is expected to show growth at a faster pace over the forecast period.

Generic Drugs Industry Overview

The global generic drugs market is highly competitive, with many players dominating the market. The market players are adopting strategies such as rising R&D investment, mergers, acquisitions, and product innovations to sustain the increasing market rivalry. The key market players include Mylan NV, Eli Lilly and Company, GlaxoSmithKline PLC, Pfizer Inc., Sun Pharma, Novartis, and Sanofi.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Chronic Diseases

- 4.2.2 Rise in Geriatric Population

- 4.2.3 Increase in Healthcare Expenditure

- 4.3 Market Restraints

- 4.3.1 Stringent Government Regulations

- 4.3.2 Adverse Effects Associated with the Drugs

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Route of Administration

- 5.1.1 Oral

- 5.1.2 Topical

- 5.1.3 Injectable

- 5.1.4 Other Routes of Administration (Sublingual, Rectal)

- 5.2 By Application

- 5.2.1 Cardiovascular Products

- 5.2.2 Anti-infective Drugs

- 5.2.3 Anti-arthritis Drugs

- 5.2.4 Central Nervous System Drugs

- 5.2.5 Anti-cancer Drugs

- 5.2.6 Respiratory Products

- 5.2.7 Other Applications (Gastrointestinal, Hormonal Drug)

- 5.3 By Distribution Channel

- 5.3.1 Hospitals/Clinics

- 5.3.2 Retail Pharmacies

- 5.3.3 Other Distribution Channels (Online Pharmacy, Specialty Drug Stores)

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Mylan (Viatris Inc.)

- 6.1.2 Abbott Laboratories

- 6.1.3 Teva Pharmaceutical Industries Limited

- 6.1.4 Eli Lilly and Company

- 6.1.5 STADA Arzneimittel AG

- 6.1.6 GlaxoSmithKline PLC

- 6.1.7 Baxter International Inc.

- 6.1.8 Pfizer Inc.

- 6.1.9 Sanofi

- 6.1.10 Novartis AG (Sandoz International)

- 6.1.11 Sun Pharma

- 6.1.12 AbbVie Inc. (Allergan)