|

市場調査レポート

商品コード

1910712

ポリシリコン:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Polysilicon - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ポリシリコン:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

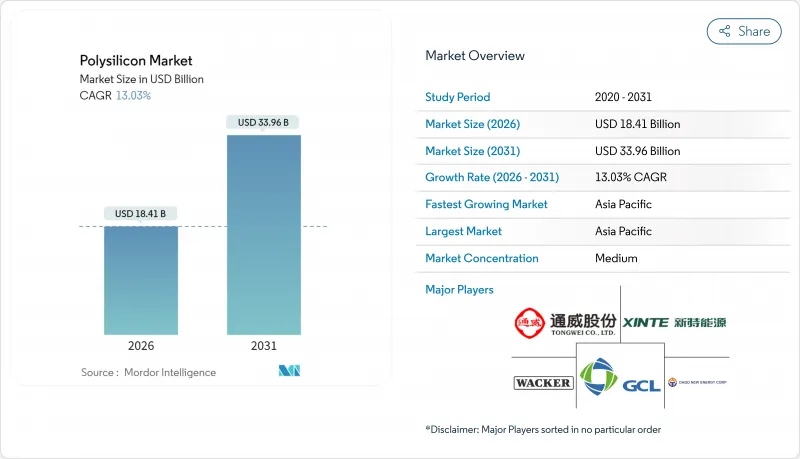

ポリシリコン市場は2025年に162億9,000万米ドルと評価され、2026年の184億1,000万米ドルから2031年までに339億6,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは13.03%と見込まれます。

この成長軌道は、太陽光発電設備の急増、半導体設備投資の拡大、地域的な供給多様化を促進する政策インセンティブに起因しています。N型TOPConおよびヘテロ接合セル構造への急激な転換により、汎用品とプレミアムグレードの純度格差が拡大する一方、クローズドループシリコンリサイクルはグリッドパリティ経済に向けて着実に進展しています。一方、欧米の強制労働規制により貿易ルートが再編され、新疆産原料以外のトレーサビリティが確保された原料を優遇する二重価格環境が生まれています。中国の稼働率が40%を下回る状況が続く中、コスト圧力は依然として強く、長期半導体契約により超高純度生産者の利益率は維持されているもの、スポット価格は下落傾向にあります。

世界のポリシリコン市場の動向と展望

世界の太陽光発電の大規模な拡大

世界の太陽光発電設備導入量は、2022年の191GWから2023年には444GWへと132%急増し、上流サプライチェーンを逼迫させつつポリシリコン市場の需要を強化しました。開発業者は、中国における2025年6月の固定価格買取制度(FIT)変更に先立ちモジュール確保を急ぎ、原料調達リードタイムを通常の18ヶ月を超える増産ペースに拡大させました。中国では新規反応炉が稼働を開始しているもの、試運転の遅れにより高効率グレードの在庫は逼迫した状態が続いております。インドや東南アジアにおけるプロジェクト計画が供給量の逼迫に拍車をかけ、現在の価格軟調にもかかわらず、複数年にわたる成長基盤を強化しております。先物契約の動向からは、米国や欧州における規制順守を確保するため、トレーサビリティのある新疆産以外の素材に対して、買い手が依然としてプレミアム価格を支払う意思があることが示されております。

AI主導の半導体設備投資スーパーサイクル

3nm以下の先進ロジック・メモリ工場では、汚染許容値が厳格化されたため、従来のラインと比較してウエハー当たり最大3倍の高純度ポリシリコンを消費します。年間2,000億米ドルを超えるファウンダリ投資は、長期供給契約を支え、サプライヤーを太陽電池価格の変動から保護しています。米国CHIPS法(520億米ドル)とEUチップス法は、2030年までに地域のウエハー生産量を世界シェアの20%に引き上げることを目指しており、これにより北米と欧州に追加のポリシリコン需要が創出されます。11Nグレードの仕様を満たす生産者は、太陽電池グレードの製品と比較して300~400%の価格プレミアムを獲得でき、これによりマージンが確保され、プロセスアップグレードの資金調達が可能となります。

長期化する生産能力過剰

中国メーカーの稼働率は2025年第1四半期に約33%で推移し、スポット価格がトン当たり7万2,100元から3万4,000元に急落したため、現金コストを下回る販売を余儀なくされました。この供給過剰は、2021年から2023年にかけての生産能力拡大がウエハーライン拡張を上回ったことに起因し、ポリシリコン市場は2026年まで清算価格志向の構造に固定される見込みです。北京の省エネルギー監査により、小規模反応炉の20~30%が閉鎖される可能性がありますが、その時期は不透明です。合理化が実現するまでは、電力コストやTCSコストが高い生産者はマージンがマイナスとなり、設備投資が制約されるため、短期的な技術改修は限定的です。

セグメント分析

シーメンス製反応炉は2025年時点でポリシリコン市場シェア66.42%を維持し、太陽光・半導体両分野の買い手から高く評価される11Nグレード製品を生産しております。しかしながら、持続的な商品価格下落により電力消費への注目が高まっております。シーメンス製ラインは1キログラム当たり60~70kWhを消費するため、高料金地域では利益率に圧迫が生じております。流動層反応器(FBR)によるポリシリコン市場規模は、電力使用量が25%低減され、連続粉末排出によりトン当たり設備投資が削減されることから、14.18%のCAGRで急成長すると予測されています。清華大学の最新研究では、最適化されたFBRカラムにおける堆積速度が40%向上することが確認され、既存設備の改修における採用が促進されています。しかしながら、FBRベンダーが半導体市場に参入するには、粉末汚染リスクへの対応が必須です。現在、高度な冶金級シリコンはニッチ市場に留まりますが、カナダとノルウェーのパイロットプラントは、コスト上限を求める垂直統合型ウエハー企業の間で関心が高まっていることを示しています。

電力価格の裁定取引が世界の投資パターンを形成しています。中東プロジェクトでは0.03米ドル/kWh未満の再生可能エネルギーを活用し、10Nグレードの太陽電池原料をターゲットとするシーメンス製設備の導入を正当化。一方、米国メキシコ湾岸のラインでは複合サイクルガス発電を採用し、セクション45X税還付制度を活用しています。環境規制も影響しており、欧州の金融関係者はライフサイクルCO2開示を要求。FBRの低炭素フットプリントが評価されています。全体として、ポリシリコン市場における地域ごとのエネルギー環境において、技術選択は資本支出、運営費、純度、炭素基準をバランスさせる戦略的手段となりつつあります。

地域別分析

アジア太平洋地域は2025年にポリシリコン市場の売上高シェア65.70%を占め、石英採掘からモジュール組立までを網羅する中国の統合サプライチェーンを背景に主導的立場を維持しました。地方自治体の優遇政策により中国の名目生産能力は400キロトンを超えましたが、慢性的な供給過剰がプラント稼働率を低下させ、利益率の悪化を招きました。インドは戦略的な需要層を追加します。2030年までに500GWの再生可能エネルギー目標を達成するためには、国内事業が実現しない限り、年間150キロトンを超えるシリコン輸入が必要となります。日本と韓国は半導体グレードの生産量に注力し、長年にわたる純度に関する専門知識を活用していますが、高い電力コストが既存設備の拡張を妨げています。

北米はインフレ抑制法により製造業が再活性化し、復興期に入りました。RECシリコン社のモーゼスレイク工場再稼働により2026年までに14キロトンのFBR粉末が供給されますが、米国の太陽光発電設備導入量は年間50GWを超える可能性があり、マレーシアやドイツからの輸入で補う構造的不足が生じます。セクション301関税とウイグル強制労働防止法に基づく差し押さえが物流を複雑化させ、トレーサビリティのある貨物向けのプレミアムスポット市場を育んでいます。カナダは水力発電による低炭素電力を提供し、1万トン規模を目指す半導体グレード工場の実現可能性調査が進められています。

欧州では野心的な「Fit for 55」目標と、平均0.27ユーロ/kWh(米国と比較して2倍)という高騰した産業用電力料金のバランスが課題です。しかしながら、ノルウェーの水力余剰を背景に、スコープ2排出量ネットゼロを目指すFBR施設の提案が進んでおり、これはEUのモジュール購入者が重視する認証要件となっています。

中東諸国はエネルギーコストの裁定取引を追求しています。オマーンの10万トン級プロジェクトは、0.03米ドル/kWh未満の太陽光発電と港湾の近接性を活用し、アジアとアフリカへの供給を目指しています。アフリカは新興市場であり、エジプトとモロッコは国内の太陽光目標と連動した製錬所を活用したUMG(超微細粒)経路を調査中です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 世界の太陽光発電の大規模な建設拡大(大規模発電所+分散型)

- AI主導の半導体設備投資スーパーサイクル(3nm以下のプロセスノード)

- IRA-/Fit-for-55によるポリシリコン国内回帰促進策

- 次世代N型TOPCon/IBCセル向け超高純度ポリシリコン需要

- クローズドループ・シリコンリサイクルの経済性がグリッドパリティに到達(2030年)

- 市場抑制要因

- 2024-26年にわたる長期的な供給過剰と現金コストを下回る価格設定

- 低スペック太陽光発電セグメントにおけるUMG-Si代替リスク

- 新疆ウイグル自治区産原料に対する欧米の強制労働監査規則

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 技術的概況

第5章 市場規模と成長予測

- 製造プロセス別

- シーメンス(TCS-CVD)

- 流動層反応器(シラン-FBR)

- アップグレードされた冶金グレード(UMG)

- エンドユーザー業界別

- 太陽光発電

- 単結晶太陽電池パネル

- 多結晶太陽電池パネル

- 電子機器および半導体

- 太陽光発電

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)**/順位分析

- 企業プロファイル

- Asia Silicon(Qinghai)Co. Ltd

- DAQO NEW ENERGY CO. LTD

- GCL-TECH

- Hemlock Semiconductor Operations LLC and Hemlock Semiconductor LLC

- Mitsubishi Polycrystalline Silicon America Corporation

- OCI Company Ltd

- Qatar Solar Technologies

- REC Silicon ASA

- Sichuan Yongxiang Co. Ltd(Tongwei)

- Tokuyama Corporation

- Tongwei Co., Ltd

- United Solar Polysilicon(FZC)SPC

- Wacker Chemie AG

- Xinte Energy Co. Ltd