|

|

市場調査レポート

商品コード

1435219

自動車用触媒:市場シェア分析、産業動向、成長予測(2024年~2029年)Automotive Catalyst - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車用触媒:市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

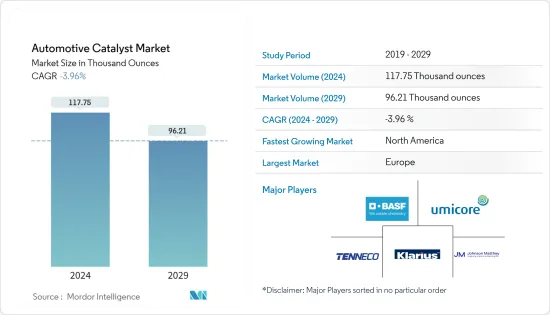

自動車用触媒の市場規模は、2024年に11万7,750オンスと推定され、2029年までに9万6,210オンスに減少すると予想されています。

新型コロナウイルス感染症(COVID-19)のパンデミックは、ロックダウンや制限による製造施設や工場の閉鎖により市場に悪影響を及ぼしました。サプライチェーンと輸送の混乱により、さらに市場に障害が生じました。しかし、業界は2021年に回復を見せ、調査対象市場の需要が回復しました。

主なハイライト

- 短期的には、世界中の政府によって施行されている厳しい排出基準と自動車生産の増加が、調査対象の市場の成長を促進する主な要因です。

- 一方で、電気自動車の人気の高まりが市場の成長を妨げています。

- しかし、発展途上国の排出基準に対する重点の高まりにより、自動車用触媒市場に将来の成長機会がもたらされると予想されます。

- 欧州は、この地域での厳しい排出基準の採用により、市場を独占し、世界最大の市場シェアを持つと予想されています。

自動車用触媒市場動向

乗用車セグメントが市場を独占

- 内燃エンジンは、エンジン内の不完全燃焼により有毒な排出物を生成します。

- COが人体に有毒であるという事実とは別に、都市部の上空の停滞した気団には汚染物質が長期間保持される可能性があります。太陽光がこれらの汚染物質と相互作用すると、HC、NOx、太陽光の化学反応により地表でオゾンが形成されます。

- 自動車用触媒は、炭化水素、炭素酸化物、窒素酸化物などの有害なガスの排出を制御するために車両の排気システムに使用されます。これらの触媒は、有害なガスを窒素や二酸化炭素などの毒性の低いガスに変換するのに役立ちます。

- 国際自動車工業機構(OICA)によると、2022年の世界の乗用車総生産台数は6,159万台で、2021年と比べて8%、2020年と比べて10%増加しました。乗用車の生産の増加により、予測期間中に自動車用触媒の需要が増加すると予想されます。

- インドにおける自動車産業への投資の増加と進歩により、自動車用触媒市場に上向きの需要が生まれると予想されます。たとえば、タタモーターズは2022年4月、今後5年間で乗用車事業に30億8,000万米ドルを投資する計画を発表しました。これは、国内の自動車用触媒市場にプラスの影響を与えることが期待されます。

- 英国では、インフレの上昇、サプライチェーン管理の問題、地政学的不安、新型コロナウイルスが乗用車生産減少の主な要因となった。例えば、OICAによると、2022年の同国の乗用車生産台数は合計 7,75,014台で、2021年の乗用車生産台数は8,59,575台だったのに対し、生産減少率は10%でした。Brexitと緊張による影響米国と中国の間の対立も、同国の自動車生産に大きな影響を与えています。これらの要因は、国内の自動車用触媒市場に悪影響を与えるでしょう。

- 発展途上国の政府は、燃料効率などの新しい排出ガス制御技術に多額の費用を投じて排出ガス規制に取り組んでおり、自動車用触媒市場の成長を後押しすると予想されています。四元触媒は古い触媒よりも効率が優れています。

- 前述の要因は、予測期間中に自動車触媒市場に大きな影響を与えると予想されます。

欧州が市場を独占する

- 欧州地域では排出ガス基準がますます厳しくなっているため、自動車用触媒市場は欧州が独占すると予想されています。

- 汚染を抑制するための政府の厳しい規制により、最近では自動車用触媒の需要が急増しています。

- OICAによると、乗用車部門では、2022年の全体的な生産量が減少しました。2021年と比較して1%減少しており、自動車用触媒市場はまだ回復期を迎えていないです。生産量の大幅な減少は、政府機関が設定した環境基準が絶えず変更されたことが原因でした。これは、この地域の乗用車セグメントからの自動車用触媒の減少に重要な役割を果たしました。スロブニアやウズベキスタンなどの国では乗用車の需要が大幅に減少している一方、オーストリア、ポルトガル、ベラルーシなどの国では自動車生産が急増しており、それによってこの地域での自動車用触媒の需要が増加しています。

- さらにドイツでは、半導体不足と原材料供給の制限により自動車産業が打撃を受けています。同様に、新しい世界調和小型車両試験手順(WLTP)の実施や、国際的な自動車需要を減少させた米中貿易摩擦、自動車メーカーに平均CO2排出量の達成を義務付けるEU-28の新しい排出基準などの他の要因も考えられます。新しく販売された車両全体で1キロメートルあたり95グラムの汚染があり、乗用車の生産に悪影響を及ぼしました。しかし、2022年には半導体不足から国内の自動車生産が徐々に回復しました。たとえば、OICAによると、2022年にドイツでは約3,480,357台の乗用車が生産され、2021年と比較して12%増加しました。したがって、乗用車部門の生産増加は自動車需要の上振れを生み出すと予想されます。触媒市場。

- 半導体不足が続いているため、欧州地域では小型商用車の生産が減少しています。例えば、OICAによると、2022年には約214万8,379台の小型商用車が生産され、2021年と比較して2%減少しました。これらの不足により、国内の自動車用触媒市場の需要の成長が制限されることが予想されます。

- ロシアの小型商用車の生産は、オンラインショッピングと都市化の増加により過去3年間で増加しており、効率的な物流を必要とする新たな小売およびeコマースプラットフォームが国内に誕生しました。対照的に、ロシア・ウクライナ戦争は経済制裁、一次産品価格の高騰、サプライチェーンの中断をもたらし、国内の小型商用車の生産に影響を与え、また国内の自動車用触媒市場にも影響を与えています。たとえば、OICAによると、2022年には約83,813台の小型商用車が生産され、2021年と比較して35%減少しました。

- フランスでは、半導体不足とサプライチェーン不足が続いているため、国内の小型商用車の生産に若干の影響を及ぼしました。例えば、OICAによると、2022年の国内の小型商用車生産台数は、2021年の43万3,401台と比較して、14%減少して37万2,707台となった。

- 上記の要因は、今後数年間で市場に大きな影響を与えると予想されます。

自動車触媒業界の概要

自動車用触媒市場は本質的に部分的に細分化されています。この市場の主要企業(順不同)には、BASF SE、Tenneco Inc.、Johnson Matthey、Klarius Products Ltd、およびUmicoreなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 自動車生産の増加

- 自動車排ガスに関する厳しい規制

- その他の促進要因

- 抑制要因

- 電気自動車の人気上昇

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 種類

- プラチナ

- パラジウム

- ロジウム

- その他のタイプ

- 車種

- 乗用車

- 小型商用車

- 大型商用車

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア分析**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- BASF SE

- CDTi Advanced Materials Inc.

- CLARIANT

- Cummins Inc.

- DCL International Inc.

- Ecocat India Pvt Ltd

- Johnson Matthey

- Klarius Products Ltd

- N.E. CHEMCAT CORPORATION

- Tenneco Inc.

- Umicore

第7章 市場機会と今後の動向

第8章 発展途上国の排出基準重視の高まり

第9章 その他の機会

The Automotive Catalyst Market size is estimated at 117.75 Thousand ounces in 2024, and is expected to decline to 96.21 Thousand ounces by 2029.

The COVID-19 pandemic negatively impacted the market due to the shutdown of the manufacturing facilities and plants due to the lockdown and restrictions. Supply chain and transportation disruptions further created hindrances for the market. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

- Over the short term, stringent emission standards implemented by governments across the world and an increase in the production of automobiles are the major factors driving the growth of the market studied.

- On the flip side, the rise in the popularity of electric vehicles is hindering the growth of the market.

- However, surge in emphasis of developing nations towards the emission standards is anticipated to provide future growth opportunity to the automotive catalyst market.

- Europe is expected to dominate the market and have the largest market share globally, owing to the adoption of stringent emission standards in the region.

Automotive Catalyst Market Trends

The Passenger Cars Segment to Dominate the Market

- Internal combustion engines produce toxic emissions due to incomplete combustion in the engine.

- Apart from the fact that CO is poisonous to humans, the stagnant air masses over urban areas can hold the pollutants for long periods. When sunlight interacts with these pollutants, the formation of ground-level ozone occurs due to the chemical reaction between HC, NOx, and sunlight.

- The automotive catalyst is used in the exhaust system of vehicles to control the emission of harmful gases, such as hydrocarbons, carbon oxides, and nitrogen oxides, as these catalysts help in converting harmful gases into less toxic gases, such as nitrogen and carbon dioxide.

- According to the International Organization of Motor Vehicle Manufacturers (OICA), in 2022, the total number of passenger cars produced globally was 61.59 million units, which showed an increase of 8% compared to 2021 and 10% compared to 2020. Therefore, an increase in the production of passenger cars is expected to create an upside demand for automotive catalysts in the forecast period.

- Increased investments and advancements in the automobile industry in India is expected to create an upside demand for automotive catalyst market. For instance, in April 2022, Tata Motors announced plans to invest USD 3.08 billion in its passenger vehicle business over the next five years. This is expected to have a positive impact on the automotive catalyst market in the country.

- In the United Kingdom, rising inflation, supply chain management issues, geopolitical unrest and COVID were the major contributors for the decrease in the production of passenger cars. For instance, according to OICA, in 2022, the country produced a total of 7,75,014 units of passenger vehicles at a 10% production decline rate as compared to 8,59,575 passenger vehicles produced in 2021. The fallout due to Brexit and the tensions between the United States and China have also significantly affected vehicle production in the country. These factors will negatively affect the market for automotive catalyst in the country.

- The governments of developing nations are taking initiatives in concern of emission control by spending hugely on new emission controlling technologies like fuel efficiency, which is expected to boost the growth of the automotive catalyst market. A four-way catalyst has better efficiency than older catalysts.

- The aforementioned factors are expected to show a significant impact on the automotive catalyst market during the forecast period.

Europe to Dominate the Market

- Europe is expected to dominate the automotive catalyst market due to the increasingly stringent emission standards in the region.

- Stringent government regulations to restrain pollution surged the demand for automotive catalysts in recent times.

- In the Passenger car segment, according to OICA, there was a decline in overall production in 2022. With a decrease of 1% compared to 2021, the automotive catalyst market is yet to see a recovery period. The major decrease in production was due to the constant change in the environmental standards set by the governing bodies. This played a vital role in the decrease of automotive catalysts from the passenger car segment in the region. Countries like Slovnia, and Uzbekistan have seen a major decrease in the demand for passenger cars while countries like Austria, Portugal, Belarus, and others have seen a surge in automotive production thereby increasing the demand for automotive catalysts in the region.

- Moreover, in Germany, the automotive industry has been hampered by the shortage of semiconductors and a limited supply of raw materials. Similarly, other factors such as the implementation of the new Worldwide Harmonized Light-Duty Vehicles Test Procedure (WLTP) and US-China trade conflicts which decreased the international automotive demand, EU-28's new emission standard which mandates carmakers to achieve average CO2 emissions of 95 grams per kilometre across newly sold vehicles had negatively affected the production of passenger cars. However, in 2022 the automobile production in the country recovered gradually from semiconductor shortages. For instance, according to OICA, around 34,80,357 passenger cars were produced in Germany in 2022, which shows an increase of 12% compared to 2021. Therefore, increase in the production of passeger car segment is expected to create an upside demand for automotive catalyst market.

- Due to the ongoing semiconductor shortages, the production of light commercial vehicles in the Europe region is declining. For instance, in 2022, according to OICA, around 21,48,379 units of light commercial vehicles were produced, which declined by 2% compared to 2021. These shortages are expected to restrict the growth of demand for automotive catalysts market in the country.

- Russia's production of light commercial vehicles has increased in the last three years due to an increase in online shopping and urbanization, which has created new retail and e-commerce platforms in the country that require efficient logistics. In contrast, the Russia-Ukraine war has resulted in economic sanctions, a jump in commodity prices, and supply chain interruptions, impacting the production of light commercial vehicles in the country, and affecting the automotive catalysts market in the country. For instance, according to OICA, in 2022, around 83,813 units of light commercial vehicles were produced, which shows a decrease of 35% compared to 2021.

- In France, due to the ongoing semiconductor shortage and supply chain shortages slightly affected the light commercial vehicles production in the country. For instance, according to OICA, in 2022 the country's light commercial vehicles production volume declined by 14% to 3,72,707 units as compared to 4,33,401 units produced in 2021.

- The abovementioned factors are expected to show a significant impact on the market in the coming years.

Automotive Catalyst Industry Overview

The Automotive Catalyst Market is partially fragmented in nature. The major players in this market (not in a particular order) include BASF SE, Tenneco Inc., Johnson Matthey, Klarius Products Ltd, and Umicore, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increase in Automobile Production

- 4.1.2 Stringent Regulations Related to Automotive Emission

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Rise in Popularity of Electric Vehicles

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porters Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Platinum

- 5.1.2 Palladium

- 5.1.3 Rhodium

- 5.1.4 Other Types

- 5.2 Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Heavy Commercial Vehicles

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 CDTi Advanced Materials Inc.

- 6.4.3 CLARIANT

- 6.4.4 Cummins Inc.

- 6.4.5 DCL International Inc.

- 6.4.6 Ecocat India Pvt Ltd

- 6.4.7 Johnson Matthey

- 6.4.8 Klarius Products Ltd

- 6.4.9 N.E. CHEMCAT CORPORATION

- 6.4.10 Tenneco Inc.

- 6.4.11 Umicore