|

|

市場調査レポート

商品コード

1535296

次世代シーケンス(NGS)市場:提供製品別、用途別、エンドユーザー別の業界展望、2031年までの世界予測Next-Generation Sequencing (NGS) Market: Industry Outlook by Offering (Sample Preparation, Systems, Bioinformatics, Sequencing Services) Application (Clinical, Research) End User - Global Forecast to 2031 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 次世代シーケンス(NGS)市場:提供製品別、用途別、エンドユーザー別の業界展望、2031年までの世界予測 |

|

出版日: 2024年08月14日

発行: Meticulous Research

ページ情報: 英文 451 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

世界の次世代シーケンス(NGS)市場は、2024年から2031年までのCAGRが15.7%で、2031年までに427億米ドルに達すると予測されます。

広範な2次調査と1次調査、市場シナリオの詳細な分析を経て、当レポートは主要な業界促進要因、抑制要因、課題、機会の分析から構成されています。

NGS市場の成長は、がん罹患率の上昇とがん治療および研究におけるNGSの応用の増加、NGSサービスプロバイダーと製薬企業間の提携、NGSの技術進歩、最適化および合理化されたNGSワークフローに対する需要の高まり、ゲノム配列決定のコスト低下、配列決定手順の技術進歩、NGSインフォマティクスソリューションの技術進歩、医薬品研究開発費の増加、ゲノムマッピングプログラムの急増、NGSベースの診断検査に対する規制および償還シナリオの改善によって促進されます。

さらに、NGSの用途の増加、バイオインフォマティクスおよびゲノムデータ管理ソリューションの採用の増加、ライブラリ調製プロトコルの開発におけるベンダー間の協力、大規模なデータ解析および解釈のためのバイオインフォマティクスおよびゲノムデータ管理ソリューションの使用の増加、病院および臨床検査室におけるNGSインフォマティクスツールの採用の増加、大規模なゲノムシークエンシングプロジェクトを支援する政府のイニシアティブは、NGS市場で事業を展開する企業に成長機会をもたらすと期待されています。

本レポートでは、4年間(2021年~2024年)の製品ポートフォリオの提供、地域情勢、業界の主要な市場企業が採用した主な戦略的発展の広範な評価に基づく競合情勢を提供しています。世界の次世代シーケンス(NGS)市場で事業を展開している主要企業は、Illumina, Inc.(米国)、Thermo Fisher Scientific Inc.(米国)、F. Hoffmann-La Roche Ltd.(スイス)、Revvity, Inc.(スイス)、Revvity, Inc.(米国)、QIAGEN N.V.(オランダ)、Agilent Technologies, Inc.(米国)、Pacific Biosciences of California, Inc.(米国)、Danaher Corporation(米国)、Oxford Nanopore Technologies Plc.(英国)、MGI Tech Co.Ltd.(中国)、Tecan Group Ltd.(スイス)、Beijing Genomics Co.(スイス)、Beijing Genomics Institute(BGI)(中国)、Eppendorf AG(ドイツ)、Hamilton Company(米国)、Hudson Robotics(米国)、LGC Limited(英国)、Fabric Genomics, Inc.(米国)、DNASTAR, Inc.(米国)、Eurofins Scientific SE(ルクセンブルク)、Novogene Co.Ltd.(中国)、Novogene Co.Ltd.(中国)、Quest Diagnostics Incorporated(米国)です。

本レポートで調査した提供製品のうち、2024年には商用シーケンス/アウトソーシングサービスセグメントが市場の38.0%という最大シェアを占めると予想されます。このセグメントの市場シェアが大きいのは、NGSサービスプロバイダーが提供する、迅速な結果、費用対効果、さまざまな用途に利用可能な幅広いサービスなどの利点に起因しています。

本レポートで調査した用途のうち、2024年には研究およびその他の用途分野が次世代シーケンス(NGS)市場で62.2%の最大シェアを占めると予測されます。このセグメントの大きなシェアは、シーケンス手順のコスト低下、製薬企業やバイオテクノロジー企業による創薬のための調査研究の増加、複数の臨床および研究環境におけるNGSの応用の増加、薬理学的標的の発見、治療仮説の確認、分子標的を狙った阻害化合物の潜在的な安全性の予測を目的としたインフォマティクスソリューションの利用の増加に起因しています。

本レポートで調査したエンドユーザーのうち、2024年には製薬・バイオテクノロジー企業セグメントが次世代シーケンス(NGS)市場で43.5%の最大シェアを占めると予想されます。このセグメントの市場シェアが大きいのは、製薬・バイオテクノロジー企業による研究開発費の増加と慢性疾患の罹患率の上昇が、製薬・バイオテクノロジー企業における次世代シーケンス製品の採用を促進しているためと考えられます。

世界の次世代シーケンス(NGS)市場の地域別シナリオの詳細分析では、5つの主要地域(北米、欧州、アジア太平洋、ラテンアメリカ、中東・アフリカ)の詳細な質的・量的洞察を、各地域の主要国の範囲とともに提供しています。2024年には、北米が次世代シーケンシング(NGS)市場で48.7%を超える最大シェアを占めると予測されています。また、2024年には米国が北米の次世代シーケンス(NGS)市場で最大のシェアを占めると予想されています。北米の市場シェアが大きいのは、ゲノム研究に対する政府の取り組みが良好であること、シーケンスに基づく研究の用途が拡大していること、次世代シーケンス技術の大手プロバイダーが同地域に存在すること、製薬企業やバイオ製薬企業による研究投資が増加していること、高度なシーケンス製品やソリューションの利用可能性が高まっていることと相まってシーケンスコストが低下していること、がん罹患率が増加していること、同地域の償還シナリオが良好であることなどが背景にあります。

調査範囲:

次世代シーケンス(NGS)市場評価:提供製品別

- サンプル調製

- キットおよび試薬

- 核酸抽出と増幅

- ライブラリー調製

- DNAライブラリー調製

- RNAライブラリー調製

- 品質管理

- その他の試薬(1)

- ライブラリー調製用ワークステーション/ロボットプラットフォーム

- シーケンス

- NGSシステム

- 合成によるシーケンス

- イオン半導体シーケンス

- 単一分子リアルタイムシーケンス(SMRT)

- DNAナノボール(DNB)シーケンス

- その他のテクノロジー(2)

- サービス(3)

- データ解析/バイオインフォマティクス

- ソフトウェア

- タイプ別

- データ解析ソフトウェア

- データ解釈・レポーティングツール

- データ保存・計算ツール

- ラボ情報管理システム(LIMS)

- 展開形態別

- ウェブおよびクラウドベース

- オンプレミス

- NGSインフォマティクスサービス(4)

- 商業シーケンス/アウトソーシングサービス

- ターゲットシーケンスサービス

- RNAシーケンスサービス

- 全ゲノムシーケンスサービス

- デノボシーケンスサービス

- エクソームシーケンスサービス

- ChIPシーケンスサービス

- メチルシーケンスサービス

- その他の商業シーケンスサービス(5)

次世代シーケンス(NGS)市場評価:用途別

- 研究およびその他の用途

- 創薬

- 農業・動物研究

- その他の用途(6)

- 臨床用途

- 生殖医療診断

- 腫瘍学

- 感染症

- その他の臨床用途(7)

次世代シーケンス(NGS)市場評価:エンドユーザー別

- 病院・診断研究所

- 製薬・バイオテクノロジー企業

- 学術機関・研究センター

- その他のエンドユーザー(8)

注:1.その他の試薬には、希釈バッファー、DNA標準、ターゲット濃縮キット/試薬、およびNGSサンプル調製ワークフローをサポートするために必要なその他の試薬が含まれます。

2.その他の技術には、NanoporeシーケンスおよびAvidityシーケンス技術が含まれます。

3.サービスには、ソフトウェアのアップグレード、カスタマーサポート、機器トレーニング、モニタリング、設置サービスなどのサポートサービスが含まれます。

4.NGSインフォマティクスサービスには、バイオインフォマティクスデータ解析サービス、バイオインフォマティクスコンサルティングサービス、バイオインフォマティクストレーニング、ITプロフェッショナルサービスなどのサポートサービスが含まれます。

5.その他の商業シーケンスサービスには、デグレードームシーケンス、リボソームプロファイリング、アンプリコンシーケンス、CRISPRバリデーション、ウイルスゲノムシーケンス、イムノゲノミクスサービスが含まれます。

6.その他の用途には、食品微生物学、飲食品産業における微生物叢分析、環境調査が含まれます。

7.その他の臨床応用には、神経疾患、希少疾患、代謝・免疫疾患、食品由来疾患における遺伝子異常の検出が含まれます。

8.その他のエンドユーザーには、法医学研究所や警備機関、飲食品会社、農業会社などが含まれます。

次世代シーケンス(NGS)市場評価:エンドユーザー別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- イタリア

- 英国

- スペイン

- その他欧州(RoE)

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域(RoAPAC)

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場

- 概要

- 市場成長への影響要因

- 市場力学の影響分析

- がん罹患率の上昇とがん治療・研究におけるNGS適用の増加が市場成長を促進

- 代替技術の利用可能性が市場成長を抑制

- 個別化医療におけるNGS応用の拡大が市場企業の成長機会を生み出す

- データの保存、取り扱い、解釈、機密性への懸念が市場利害関係者の主要課題であり続ける見込み

- 要因分析

- 市場力学の影響分析

- 業界動向

- NGSソリューションプロバイダー間のパートナーシップとコラボレーションの増加による製品提供の拡大と進歩

- ポータブルシーケンステクノロジーの開発

- NGS自動化への需要の高まり

- 価格分析

- NGS装置および消耗品

- NGSサービス

- 規制分析

- NGS装置と消耗品

- 北米

- 米国

- カナダ

- 欧州

- アジア太平洋

- 中国

- 日本

- インド

- ラテンアメリカ

- 中東

- 北米

- NGSインフォマティクス

- NGS装置と消耗品

- ケーススタディ/使用事例

- ケーススタディA

- ケーススタディB

- ケーススタディC

- ケーススタディD

- ポーターのファイブフォース分析

第5章 次世代シーケンス(NGS)市場評価:提供製品別

- 概要

- サンプル調製

- キットおよび試薬

- 核酸抽出および増幅

- ライブラリー調製

- DNAライブラリー調製

- RNAライブラリー調製

- 品質管理

- その他のキットおよび試薬

- NGSワークステーション

- キットおよび試薬

- シーケンス

- NGSシステム

- 合成によるシーケンス

- イオン半導体シーケンス

- 単一分子リアルタイムシーケンス(SMRT)

- DNAナノボール(DNB)シーケンス

- その他のテクノロジー

- 消耗品

- サービス

- NGSシステム

- データ解析/バイオインフォマティクス

- ソフトウェア

- ソフトウェア市場、タイプ別

- データ解析ソフトウェア

- データ解釈・レポーティングツール

- データ保存およびコンピューティングツール

- ラボ情報管理システム(LIMS)

- ソフトウェア市場:展開モード別

- ウェブおよびクラウドベース

- オンプレミス

- ソフトウェア市場、タイプ別

- NGSインフォマティクスサービス

- ソフトウェア

- 商業シーケンス/アウトソーシングサービス

- ターゲットシーケンスサービス

- RNAシーケンスサービス

- デノボシーケンスサービス

- エクソームシーケンスサービス

- チップシーケンスサービス

- メチルシーケンスサービス

- 全ゲノムシーケンスサービス

- その他の商業シーケンスサービス

第6章 次世代シーケンス(NGS)市場評価:用途別

- 概要

- 研究およびその他の用途

- 創薬

- 農業および動物研究

- その他の用途

- 臨床応用

- 腫瘍学

- 生殖医療

- 感染症

- その他の臨床応用

第7章 次世代シーケンス(NGS)市場評価:エンドユーザー別

- 概要

- 製薬・バイオテクノロジー企業

- 病院および診断研究所

- 学術機関および研究センター

- その他のエンドユーザー

第8章 次世代シーケンス(NGS)市場評価:地域別

- 概要

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- その他欧州(RoE)

- アジア太平洋

- 中国

- 日本

- インド

- その他アジア太平洋地域(RoAPAC)

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ(RoLATAM)

- 中東・アフリカ

第9章 競合分析

- 概要

- 主要成長戦略

- 競合ベンチマーキング

- 競合ダッシュボード

- 業界リーダー

- 市場差別化要因

- 先行企業

- 新興企業

- 市場シェア分析(2023年)

- Instrument & Consumables

- Data Analysis/Bioinformatics

- Commercial Sequencing/Outsourced Services

- NGS Workstations

第10章 企業プロファイル(企業概要、財務概要、製品ポートフォリオ、戦略的展開)

- Illumina, Inc.

- Thermo Fisher Scientific Inc.

- F. Hoffmann-La Roche Ltd

- Eurofins Scientific Se

- Beijing Genomics Institute(BGI)

- Qiagen N.V.

- Agilent Technologies, Inc.

- Revvity, Inc.

- Pacific Biosciences of California Inc.

- Danaher Corporation

- Oxford Nanopore Technologies Plc.

- Tecan Group Ltd.

- Hamilton Company

- Hudson Robotics

- LGC Limited

- Eppendorf AG

- Novogene Co., Ltd.

- Dnastar, Inc.

- Fabric Genomics, Inc.

- MGI Tech Co., Ltd.

- Quest Diagnostics Incorporated

(*注:SWOT分析は上位5社*に提供)

第11章 付録

LIST OF TABLES

- Table 1 Global NGS Market: Impact Analysis of Market Dynamics (2024-2031)

- Table 2 Global Estimated Number of New Cancer Cases, by Type (2020 Vs. 2030)

- Table 3 Incidence of Common Genetic Disorders

- Table 4 Major Genome Sequencing Projects, by Country

- Table 5 Portable Sequencers Vs. Benchtop Sequencers

- Table 6 NGS Instruments Price List

- Table 7 NGS Consumables Price List

- Table 8 Key NGS Service Providers' Price List

- Table 9 Regulatory Authorities Governing In Vitro Diagnostics & NGS Products, by Country/Region

- Table 10 NGS Software: Standards and Compliance Guidelines

- Table 11 NGS Informatics: Standards and Compliance Guidelines

- Table 12 Global NGS Market, by Offering, 2022-2031 (USD Million)

- Table 14 Global NGS Sample Preparation Market, by Country/Region, 2022-2031 (USD Million)

- Table 15 Global NGS Sample Preparation Kits & Reagents Market, by Type, 2022-2031 USD Million)

- Table 16 Global NGS Sample Preparation Kits & Reagents Market, by Country/Region, 2022-2031 (USD Million)

- Table 17 Global Nucleic Acid Extraction and Amplification Kits & Reagents Market, by Country/Region, 2022-2031 (USD Million)

- Table 18 Global Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 19 Global Library Preparation Kits & Reagents Market, by Country/Region, 2022-2031 (USD Million)

- Table 20 Global DNA Library Preparation Kits & Reagents Market, by Country/Region, 2022-2031 (USD Million)

- Table 21 Global RNA Library Preparation Kits & Reagents Market, by Country/Region, 2022-2031 (USD Million)

- Table 22 Global Quality Control Kits & Reagents Market, by Country/Region, 2022-2031 (USD Million)

- Table 23 Global Other Kits & Reagents Market, by Country/Region, 2022-2031 (USD Million)

- Table 24 Global NGS Workstations Market for NGS Library Preparation, by Country/Region, 2022-2031 (USD Million)

- Table 25 Global Sequencing Market, by Offering, 2022-2031 (USD Million)

- Table 26 Global Sequencing Market, by Country/Region, 2022-2031 (USD Million)

- Table 27 Global NGS Systems Market, by Technology, 2022-2031 (USD Million)

- Table 28 Global NGS Systems Market, by Country/Region, 2022-2031 (USD Million)

- Table 29 Global Sequencing by Synthesis Systems Market, by Country/Region, 2022-2031 (USD Million)

- Table 30 Major Applications of Ion Torrent Sequencing

- Table 31 Global Ion Semi Conductor Sequencing Systems Market, by Country/Region, 2022-2031 (USD Million)

- Table 32 Global Smrt Systems Market, by Country/Region, 2022-2031 (USD Million)

- Table 33 Global DNA Nanoball Sequencing Systems Market, by Country/Region, 2022-2031 (USD Million)

- Table 34 Global Other Technologies Market, by Country/Region, 2022-2031 (USD Million)

- Table 35 Global Consumables Market, by Country/Region, 2022-2031 (USD Million)

- Table 36 Global Services Market, by Country/Region, 2022-2031 (USD Million)

- Table 37 Global Data Analysis/Bioinformatics Market, by Offering, 2022-2031 (USD Million)

- Table 38 Global Data Analysis/Bioinformatics Market, by Country/Region, 2022-2031 (USD Million)

- Table 39 Global Data Analysis/Bioinformatics Software Market, by Country/Region, 2022-2031 (USD Million)

- Table 40 Global Data Analysis/Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 41 Global Data Analysis Software Market, by Country/Region, 2022-2031 (USD Million)

- Table 42 Global Data Interpretation and Reporting Tools Market, by Country/Region, 2022-2031 (USD Million)

- Table 43 Global Data Storage and Computing Tools Market, by Country/Region, 2022-2031 (USD Million)

- Table 44 Global Laboratory Information Management Systems (LIMS) Market by Country/Region, 2022-2031 (USD Million)

- Table 45 Global Data Analysis/Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 46 Global Web and Cloud-Based Data/Analysis and Bioinformatics Market by Country/Region, 2022-2031 (USD Million)

- Table 47 Global On-Premise Data/Analysis and Bioinformatics Market by Country/Region, 2022-2031 (USD Million)

- Table 48 Global NGS Informatics Services Market by Country/Region, 2022-2031 (USD Million)

- Table 49 Global NGS Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 50 Global Commercial Sequencing/Outsourced Services Market by Country/Region, 2022-2031 (USD Million)

- Table 51 Global Targeted Sequencing Services Market by Country/Region, 2022-2031 (USD Million)

- Table 52 Global RNA Sequencing Services Market by Country/Region, 2022-2031 (USD Million)

- Table 53 Global De Novo Sequencing Services Market by Country/Region, 2022-2031 (USD Million)

- Table 54 Global Exome Sequencing Services Market by Country/Region, 2022-2031 (USD Million)

- Table 55 Global Chip Sequencing Services Market by Country/Region, 2022-2031 (USD Million)

- Table 56 Global Methylation Sequencing Services Market, by Country/Region, 2022-2031 (USD Million)

- Table 57 Global Whole Genome Sequencing Services Market, by Country/Region, 2022-2031 (USD Million)

- Table 58 Global Other Commercial Sequencing Services Market, by Country/Region, 2022-2031 (USD Million)

- Table 59 Global Next-Generation Sequencing (NGS) Market, by Application, 2022-2031 (USD Million)

- Table 60 Global NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 61 Global NGS Market for Research & Other Applications by Country/Region, 2022-2031 (USD Million)

- Table 62 Global NGS Market for Drug Discovery, by Country/Region, 2022-2031 (USD Million)

- Table 63 Global NGS Market for Agriculture & Animal Research, by Country/Region, 2022-2031 (USD Million)

- Table 64 Global NGS Market for Other Applications, by Country/Region, 2022-2031 (USD Million)

- Table 65 Global NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 66 Global NGS Market for Clinical Applications, by Country/Region, 2022-2031 (USD Million)

- Table 67 Currently Available Targeted Therapies and Corresponding Biomarkers

- Table 68 Global NGS Market for Oncology, by Country/Region, 2022-2031 (USD Million)

- Table 69 Global NGS Market for Reproductive Health, by Country/Region, 2022-2031 (USD Million)

- Table 70 Number of New HIV Infections, by Region, 2022

- Table 71 Global NGS Market for Infectious Diseases, by Country/Region, 2022-2031 (USD Million)

- Table 72 Global NGS Market for Other Clinical Applications, by Country/Region, 2022-2031 (USD Million)

- Table 73 Global Next-Generation Sequencing Market, by End User, 2022-2031 (USD Million)

- Table 74 Pharmaceutical Spending in Major Countries

- Table 75 Global Next-Generation Sequencing Market for Pharmaceutical & Biotechnology Companies, by Offering, 2022-2031 (USD Million)

- Table 76 Global Next-Generation Sequencing Market for Pharmaceutical & Biotechnology Companies, by Country/Region, 2022-2031 (USD Million)

- Table 77 Global Next-Generation Sequencing Market for Hospitals & Diagnostic Laboratories, by Offering, 2022-2031 (USD Million)

- Table 78 Global Next-Generation Sequencing Market for Hospitals & Diagnostic Laboratories, by Country/Region, 2022-2031 (USD Million)

- Table 79 Global Next-Generation Sequencing Market for Academic Institutes & Research Centers, by Offering, 2022-2031 (USD Million)

- Table 80 Global Next-Generation Sequencing Market for Academic Institutes & Research Centers, by Country/Region, 2022-2031 (USD Million)

- Table 81 Global Next-Generation Sequencing Market for Other End Users, by Offering, 2022-2031 (USD Million)

- Table 82 Global Next-Generation Sequencing Market for Other End Users, by Country/Region, 2022-2031 (USD Million)

- Table 83 Global NGS Market, by Country/Region, 2022-2031 (USD Million)

- Table 84 North America: NGS Market, by Country, 2022-2031 (USD Million)

- Table 85 North America: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 86 North America: Sample Preparation Market, by Type, 2022-2031 (USD Million)

- Table 87 North America: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 88 North America: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 89 North America: Sequencing Market, by Type, 2022-2031 (USD Million)

- Table 90 North America: Sequencing Systems Market, by Technology, 2022-2031 (USD Million)

- Table 91 North America: Data Analysis/Bioinformatics Market, by Type, 2022-2031 (USD Million)

- Table 92 North America: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 93 North America: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 94 North America: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 95 North America: NGS Market, by Application, 2022-2031 (USD Million)

- Table 96 North America: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 97 North America: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 98 North America: NGS Market, by End User, 2022-2031 (USD Million)

- Table 99 U.S.: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 100 U.S.: Sample Preparation Market, by Type, 2022-2031 (USD Million)

- Table 101 U.S.: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 102 U.S.: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 103 U.S.: Sequencing Market, by Type, 2022-2031 (USD Million)

- Table 104 U.S.: Sequencing Systems Market, by Technology, 2022-2031 (USD Million)

- Table 105 U.S.: Data Analysis/Bioinformatics Market, by Type, 2022-2031 (USD Million)

- Table 106 U.S.: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 107 U.S.: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 108 U.S.: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 109 U.S.: NGS Market, by Application, 2022-2031 (USD Million)

- Table 110 U.S.: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 111 U.S.: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 112 U.S.: NGS Market, by End User, 2022-2031 (USD Million)

- Table 113 Canada: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 114 Canada: Sample Preparation Market, by Type, 2022-2031 (USD Million)

- Table 115 Canada: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 116 Canada: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 117 Canada: Sequencing Market, by Type, 2022-2031 (USD Million)

- Table 118 Canada: Sequencing Systems Market, by Technology, 2022-2031 (USD Million)

- Table 119 Canada: Data Analysis/Bioinformatics Market, by Type, 2022-2031 (USD Million)

- Table 120 Canada: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 121 Canada: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 122 Canada: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 123 Canada: NGS Market, by Application, 2022-2031 (USD Million)

- Table 124 Canada: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 125 Canada: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 126 Canada: NGS Market, by End User, 2022-2031 (USD Million)

- Table 127 Europe: NGS Market, by Country/Region, 2022-2031 (USD Million)

- Table 128 Europe: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 129 Europe: Sample Preparation Market, by Offering, 2022-2031 (USD Million)

- Table 130 Europe: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 131 Europe: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 132 Europe: Sequencing Market, by Offering, 2022-2031 (USD Million)

- Table 133 Europe: NGS Market, by Technology, 2022-2031 (USD Million)

- Table 134 Europe: Data Analysis/Bioinformatics Market, by Offering, 2022-2031 (USD Million)

- Table 135 Europe: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 136 Europe: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 137 Europe: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 138 Europe: NGS Market, by Application, 2022-2031 (USD Million)

- Table 139 Europe: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 140 Europe: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 141 Europe: NGS Market, by End User, 2022-2031 (USD Million)

- Table 142 Germany: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 143 Germany: Sample Preparation Market, by Offering, 2022-2031 (USD Million)

- Table 144 Germany: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 145 Germany: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 146 Germany: Sequencing Market, by Offering, 2022-2031 (USD Million)

- Table 147 Germany: NGS Market, by Technology, 2022-2031 (USD Million)

- Table 148 Germany: Data Analysis/Bioinformatics Market, by Offering, 2022-2031 (USD Million)

- Table 149 Germany: NGS Bioinformatics Software Market, by Offering, 2022-2031 (USD Million)

- Table 150 Germany: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 151 Germany: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 152 Germany: NGS Market, by Application, 2022-2031 (USD Million)

- Table 153 Germany: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 154 Germany: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 155 Germany: NGS Market, by End User, 2022-2031 (USD Million)

- Table 156 France: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 157 France: Sample Preparation Market, by Offering, 2022-2031 (USD Million)

- Table 158 France: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 159 France: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 160 France: Sequencing Market, by Offering, 2022-2031 (USD Million)

- Table 161 France: NGS Market, by Technology, 2022-2031 (USD Million)

- Table 162 France: Data Analysis/Bioinformatics Market, by Offering, 2022-2031 (USD Million)

- Table 163 France: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 164 France: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 165 France: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 166 France: NGS Market, by Application, 2022-2031 (USD Million)

- Table 167 France: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 168 France: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 169 France: NGS Market, by End User, 2022-2031 (USD Million)

- Table 170 U.K.: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 171 U.K.: Sample Preparation Market, by Offering, 2022-2031 (USD Million)

- Table 172 U.K.: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 173 U.K.: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 174 U.K.: Sequencing Market, by Offering, 2022-2031 (USD Million)

- Table 175 U.K.: NGS Market, by Technology, 2022-2031 (USD Million)

- Table 176 U.K.: Data Analysis/Bioinformatics Market, by Offering, 2022-2031 (USD Million)

- Table 177 U.K.: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 178 U.K.: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 179 U.K.: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 180 U.K.: NGS Market, by Application, 2022-2031 (USD Million)

- Table 181 U.K.: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 182 U.K.: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 183 U.K.: NGS Market, by End User, 2022-2031 (USD Million)

- Table 184 Italy: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 185 Italy: Sample Preparation Market, by Offering, 2022-2031 (USD Million)

- Table 186 Italy: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 187 Italy: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 188 Italy: Sequencing Market, by Offering, 2022-2031 (USD Million)

- Table 189 Italy: NGS Market, by Technology, 2022-2031 (USD Million)

- Table 190 Italy: Data Analysis/Bioinformatics Market, by Offering, 2022-2031 (USD Million)

- Table 191 Italy: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 192 Italy: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 193 Italy: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 194 Italy: NGS Market, by Application, 2022-2031 (USD Million)

- Table 195 Italy: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 196 Italy: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 197 Italy: NGS Market, by End User, 2022-2031 (USD Million)

- Table 198 Spain: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 199 Spain: Sample Preparation Market, by Offering, 2022-2031 (USD Million)

- Table 200 Spain: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 201 Spain: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 202 Spain: Sequencing Market, by Offering, 2022-2031 (USD Million)

- Table 203 Spain: NGS Market, by Technology, 2022-2031 (USD Million)

- Table 204 Spain: Data Analysis/Bioinformatics Market, by Type, 2022-2031 (USD Million)

- Table 205 Spain: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 206 Spain: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 207 Spain: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 208 Spain: NGS Market, by Application, 2022-2031 (USD Million)

- Table 209 Spain: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 210 Spain: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 211 Spain: NGS Market, by End User, 2022-2031 (USD Million)

- Table 212 Roe: Estimated Number of New Cancer Cases, by Country, 2022 Vs. 2030

- Table 213 Rest of Europe: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 214 Rest of Europe: Sample Preparation Market, by Offering, 2022-2031 (USD Million)

- Table 215 Rest of Europe: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 216 Rest of Europe: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 217 Rest of Europe: Sequencing Market, by Offering, 2022-2031 (USD Million)

- Table 218 Rest of Europe: Sequencing Systems Market, by Technology, 2022-2031 (USD Million)

- Table 219 Rest of Europe: Data Analysis/Bioinformatics Market, by Offering, 2022-2031 (USD Million)

- Table 220 Rest of Europe: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 221 Rest of Europe: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 222 Rest of Europe: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 223 Rest of Europe: NGS Market, by Application, 2022-2031 (USD Million)

- Table 224 Rest of Europe: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 225 Rest of Europe: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 226 Rest of Europe: NGS Market, by End User, 2022-2031 (USD Million)

- Table 227 Asia-Pacific: NGS Market, by Country/Region, 2022-2031 (USD Million)

- Table 228 Asia-Pacific: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 229 Asia-Pacific: Sample Preparation Market, by Offering, 2022-2031 (USD Million)

- Table 230 Asia-Pacific: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 231 Asia-Pacific: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 232 Asia-Pacific: Sequencing Market, by Offering, 2022-2031 (USD Million)

- Table 233 Asia-Pacific: NGS Market, by Technology, 2022-2031 (USD Million)

- Table 234 Asia-Pacific: Data Analysis/Bioinformatics Market, by Offering, 2022-2031 (USD Million)

- Table 235 Asia-Pacific: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 236 Asia-Pacific: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 237 Asia-Pacific: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 238 Asia-Pacific: NGS Market, by Application, 2022-2031 (USD Million)

- Table 239 Asia-Pacific: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 240 Asia-Pacific: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 241 Asia-Pacific: NGS Market, by End User, 2022-2031 (USD Million)

- Table 242 China: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 243 China: Sample Preparation Market, by Offering, 2022-2031 (USD Million)

- Table 244 China: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 245 China: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 246 China: Sequencing Market, by Offering, 2022-2031 (USD Million)

- Table 247 China: NGS Market, by Technology, 2022-2031 (USD Million)

- Table 248 China: Data Analysis/Bioinformatics Market, by Offering, 2022-2031 (USD Million)

- Table 249 China: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 250 China: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 251 China: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 252 China: NGS Market, by Application, 2022-2031 (USD Million)

- Table 253 China: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 254 China: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 255 China: NGS Market, by End User, 2022-2031 (USD Million)

- Table 256 Japan: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 257 Japan: Sample Preparation Market, by Offering, 2022-2031 (USD Million)

- Table 258 Japan: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 259 Japan: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 260 Japan: Sequencing Market, by Offering, 2022-2031 (USD Million)

- Table 261 Japan: NGS Market, by Technology, 2022-2031 (USD Million)

- Table 262 Japan: Data Analysis/Bioinformatics Market, by Type, 2022-2031 (USD Million)

- Table 263 Japan: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 264 Japan: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 265 Japan: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 266 Japan: NGS Market, by Application, 2022-2031 (USD Million)

- Table 267 Japan: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 268 Japan: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 269 Japan: NGS Market, by End User, 2022-2031 (USD Million)

- Table 270 India: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 271 India: Sample Preparation Market, by Offering, 2022-2031 (USD Million)

- Table 272 India: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 273 India: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 274 India: Sequencing Market, by Offering, 2022-2031 (USD Million)

- Table 275 India: Sequencing Systems Market, by Technology, 2022-2031 (USD Million)

- Table 276 India: Data Analysis/Bioinformatics Market, by Type, 2022-2031 (USD Million)

- Table 277 India: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 278 India: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 279 India: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 280 India: NGS Market, by Application, 2022-2031 (USD Million)

- Table 281 India: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 282 India: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 283 India: NGS Market, by End User, 2022-2031 (USD Million)

- Table 284 Rest of Asia-Pacific: Estimated Number of New Cancer Cases, by Country, 2022 Vs. 2030

- Table 285 Rest of Asia-Pacific: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 286 Rest of Asia-Pacific: Sample Preparation Market, by Offering, 2022-2031 (USD Million)

- Table 287 Rest of Asia-Pacific: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 288 Rest of Asia-Pacific: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 289 Rest of Asia-Pacific: Sequencing Market, by Offering, 2022-2031 (USD Million)

- Table 290 Rest of Asia-Pacific: Sequencing Systems Market, by Technology, 2022-2031 (USD Million)

- Table 291 Rest of Asia-Pacific: Data Analysis/Bioinformatics Market, by Offering, 2022-2031 (USD Million)

- Table 292 Rest of Asia-Pacific: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 293 Rest of Asia-Pacific: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 294 Rest of Asia-Pacific: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 295 Rest of Asia-Pacific: NGS Market, by Application, 2022-2031 (USD Million)

- Table 296 Rest of Asia-Pacific: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 297 Rest of Asia-Pacific: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 298 Rest of Asia-Pacific: NGS Market, by End User, 2022-2031 (USD Million)

- Table 299 Latin America: NGS Market, by Country/Region, 2022-2031 (USD Million)

- Table 300 Latin America: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 301 Latin America: Sample Preparation Market, by Offering, 2022-2031 (USD Million)

- Table 302 Latin America: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 303 Latin America: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 304 Latin America: Sequencing Market, by Offering, 2022-2031 (USD Million)

- Table 305 Latin America: NGS Market, by Technology, 2022-2031 (USD Million)

- Table 306 Latin America: Data Analysis/Bioinformatics Market, by Type, 2022-2031 (USD Million)

- Table 307 Latin America: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 308 Latin America: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 309 Latin America: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 310 Latin America: NGS Market, by Application, 2022-2031 (USD Million)

- Table 311 Latin America: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 312 Latin America: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 313 Latin America: NGS Market, by End User, 2022-2031 (USD Million)

- Table 314 Brazil: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 315 Brazil: Sample Preparation Market, by Offering, 2022-2031 (USD Million)

- Table 316 Brazil: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 317 Brazil: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 318 Brazil: Sequencing Market, by Offering, 2022-2031 (USD Million)

- Table 319 Brazil: NGS Market, by Technology, 2022-2031 (USD Million)

- Table 320 Brazil: Data Analysis/Bioinformatics Market, by Offering, 2022-2031 (USD Million)

- Table 321 Brazil: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 322 Brazil: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 323 Brazil: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 324 Brazil: NGS Market, by Application, 2022-2031 (USD Million)

- Table 325 Brazil: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 326 Brazil: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 327 Brazil: NGS Market, by End User, 2022-2031 (USD Million)

- Table 328 Mexico: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 329 Mexico: Sample Preparation Market, by Type, 2022-2031 (USD Million)

- Table 330 Mexico: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 331 Mexico: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 332 Mexico: Sequencing Market, by Offering, 2022-2031 (USD Million)

- Table 333 Mexico: NGS Market, by Technology, 2022-2031 (USD Million)

- Table 334 Mexico: Data Analysis/Bioinformatics Market, by Offering, 2022-2031 (USD Million)

- Table 335 Mexico: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 336 Mexico: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 337 Mexico: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 338 Mexico: NGS Market, by Application, 2022-2031 (USD Million)

- Table 339 Mexico: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 340 Mexico: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 341 Mexico: NGS Market, by End User, 2022-2031 (USD Million)

- Table 342 Rest of Latin America: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 343 Rest of Latin America: Sample Preparation Market, by Type, 2022-2031 (USD Million)

- Table 344 Rest of Latin America: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 345 Rest of Latin America: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 346 Rest of Latin America: Sequencing Market, by Type, 2022-2031 (USD Million)

- Table 347 Rest of Latin America: NGS Market, by Technology, 2022-2031 (USD Million)

- Table 348 Rest of Latin America: Data Analysis/Bioinformatics Market, by Type, 2022-2031 (USD Million)

- Table 349 Rest of Latin America: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 350 Rest of Latin America: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 351 Rest of Latin America: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 352 Rest of Latin America: NGS Market, by Application, 2022-2031 (USD Million)

- Table 353 Rest of Latin America: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 354 Rest of Latin America: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 355 Rest of Latin America: NGS Market, by End User, 2022-2031 (USD Million)

- Table 356 Middle East & Africa: NGS Market, by Offering, 2022-2031 (USD Million)

- Table 357 Middle East & Africa: Sample Preparation Market, by Offering, 2022-2031 (USD Million)

- Table 358 Middle East & Africa: Sample Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 359 Middle East & Africa: Library Preparation Kits & Reagents Market, by Type, 2022-2031 (USD Million)

- Table 360 Middle East & Africa: Sequencing Market, by Offering, 2022-2031 (USD Million)

- Table 361 Middle East & Africa: NGS Market, by Technology, 2022-2031 (USD Million)

- Table 362 Middle East & Africa: Data Analysis/Bioinformatics Market, by Offering, 2022-2031 (USD Million)

- Table 363 Middle East & Africa: NGS Bioinformatics Software Market, by Type, 2022-2031 (USD Million)

- Table 364 Middle East & Africa: NGS Bioinformatics Software Market, by Deployment Mode, 2022-2031 (USD Million)

- Table 365 Middle East & Africa: Commercial Sequencing/Outsourced Services Market, by Type, 2022-2031 (USD Million)

- Table 366 Middle East & Africa: NGS Market, by Application, 2022-2031 (USD Million)

- Table 367 Middle East & Africa: NGS Market for Research & Other Applications, by Type, 2022-2031 (USD Million)

- Table 368 Middle East & Africa: NGS Market for Clinical Applications, by Type, 2022-2031 (USD Million)

- Table 369 Middle East & Africa: NGS Market, by End User, 2022-2031 (USD Million)

- Table 370 Recent Developments, by Company, 2021-2024

- Table 371 Illumina IVD Instrument Specification

- Table 372 Illumina Informatics Options for Dx Instruments

- Table 373 Supported IVD Assays

- Table 374 Supported Clinical Research Panels in Ruo Mode

- Table 375 IVD Instrument Comparison Table

- Table 376 Key Specifications (Dx Mode)

- Table 377 Production-Scale Sequencers Specifications

- Table 378 Production-Scale Sequencers - Key Applications and Methods

- Table 379 Illumina, Inc. (U.S.): NGS Systems Installed Base & New Installations In 2022

- Table 380 Illumina, Inc. (U.S.): NGS Systems Installed Base & New Installations In 2023

LIST OF FIGURES

- Figure 1 Research Process

- Figure 2 Secondary Sources Referenced for This Study

- Figure 3 Primary Research Techniques

- Figure 4 Key Executives Interviewed

- Figure 5 Breakdown of Primary Interviews (Supply-Side & Demand-Side)

- Figure 6 Market Sizing and Growth Forecast Approach

- Figure 7 Global Next-Generation Sequencing Market, By Offering, 2024 Vs. 2031 (USD Million)

- Figure 8 Global Next-Generation Sequencing Market, By Application, 2024 Vs. 2031 (USD Million)

- Figure 9 Global Next-Generation Sequencing Market, By End User, 2024 Vs. 2031 (USD Million)

- Figure 10 Global Next-Generation Sequencing Market, By Geography, 2024 Vs. 2031 (USD Million)

- Figure 11 Global Pharmaceutical R&D Expenditure, 2012-2026 (USD Billion)

- Figure 12 U.S.: Percentage of Personalized Medicine Approvals Among Total FDA Approvals, 2015-2022 (%)

- Figure 13 Genome Sequencing Costs, 2016-2022 (USD)

- Figure 14 USFDA Regulatory Pathways for IVD Kits

- Figure 15 Eu Regulatory Pathway - IVDR 2017/746

- Figure 16 China: Medical Device Classification and Pre-Market Requirements for NGS Instruments

- Figure 17 Porter's Five Forces Analysis

- Figure 18 Global NGS Market, By Offering, 2024 Vs 2031 (USD Million)

- Figure 19 Steps of Sample Preparation in A Typical NGS Workflow

- Figure 20 Global: Estimated Number of New Cancer Cases, 2022 - 2030

- Figure 21 Global Next-Generation Sequencing (NGS) Market, By Application, 2024 Vs. 2031 (USD Million)

- Figure 22 U.S.: New Molecular Entity (NME) Approvals, 2011-2022

- Figure 23 Estimated Number of New Cancer Cases, 2020-2040 (In Million)

- Figure 24 Global Next-Generation Sequencing Market, By End User, 2024 Vs. 2031 (USD Million)

- Figure 25 Global Pharmaceutical R&D Spending, 2014-2028 (USD Billion)

- Figure 26 NGS Market Assessment, By Region, 2024 Vs. 2031 (USD Million)

- Figure 27 North America: Per Capita Healthcare Expenditure, 2017-2022

- Figure 28 North America: NGS Market Snapshot

- Figure 29 Europe: Pharmaceutical R&D Expenditure Annual Growth Rate (%)

- Figure 30 Europe: NGS Market Snapshot

- Figure 31 Italy: Number of Biotechnology and Biotechnology R&D-Dedicated Firms, 2014-2022

- Figure 32 Spain Pharmaceutical R&D Expenditure, 2018-2022 (USD Million)

- Figure 33 Rest of Europe: Pharmaceutical R&D Expenditure, 2021 (USD Million)

- Figure 34 Asia-Pacific: NGS Market Snapshot

- Figure 35 Japan: Pharmaceutical Industry R&D Expenditure, 2017-2022 (USD Million)

- Figure 36 Japan: Number of New Molecular Entities Approved, 2017-2022

- Figure 37 Latin America: NGS Market Snapshot

- Figure 38 Number of Active Life Science Companies in Israel (2017-2022)

- Figure 39 Key Growth Strategies Adopted by Leading Players, 2021- 2024

- Figure 40 Next-Generation Sequencing Market: Competitive Benchmarking by Offering

- Figure 41 Next-Generation Sequencing Market: Competitive Benchmarking, by Region

- Figure 42 Competitive Dashboard: Next-Generation Sequencing Market

- Figure 43 Illumina, Inc.: Financial Snapshot (2023)

- Figure 44 Thermo Fisher Scientific Inc.: Financial Snapshot (2023)

- Figure 45 F. Hoffmann-La Roche Ltd.: Financial Snapshot (2023)

- Figure 46 Eurofins Scientific Se: Financial Overview (2023)

- Figure 47 Beijing Genomics Institute (BGI): Financial Snapshot (2023)

- Figure 48 Qiagen N.V: Financial Snapshot (2023)

- Figure 49 Agilent Technologies, Inc.: Financial Snapshot (2023)

- Figure 50 Revvity, Inc.: Financial Snapshot (2023)

- Figure 51 Pacific Biosciences of California Inc.: Financial Snapshot (2023)

- Figure 52 Danaher Corporation: Financial Snapshot (2023)

- Figure 53 Oxford Nanopore Technologies Plc.: Financial Snapshot (2023)

- Figure 54 Tecan Group Ltd.: Financial Snapshot (2023)

- Figure 55 LGC Limited: Financial Overview (2023)

- Figure 56 Eppendorf Ag: Financial Overview (2023)

- Figure 57 Novogene Co., Ltd.: Financial Overview (2023)

- Figure 58 MGI Tech Co., Ltd.: Financial Snapshot (2023)

- Figure 59 Quest Diagnostics Incorporated: Financial Overview (2023)

Next-Generation Sequencing (NGS) Market: Industry Outlook by Offering (Sample Preparation [DNA Extraction, Library Preparation, Automation], Systems, Bioinformatics, Sequencing Services) Application (Clinical, Research) End User-Global Forecast to 2031

The global next-generation sequencing (NGS) market is projected to reach $42.7 billion by 2031 at a CAGR of 15.7% from 2024 to 2031.

Succeeding extensive secondary and primary research and in-depth analysis of the market scenario, the report comprises the analysis of key industry drivers, restraints, challenges, and opportunities.

The growth of the NGS market is driven by the rising cancer prevalence & the increasing application of NGS in cancer treatment and research, partnerships between NGS service providers & pharmaceutical companies, technological advancements in NGS, the growing demand for optimized & streamlined NGS workflows, the declining costs of genome sequencing, technological advancements in sequencing procedures, technological advancements in NGS informatics solutions, increasing pharmaceutical R&D expenditures, the surge in genome mapping programs, and improvements in regulatory & reimbursement scenarios for NGS-based diagnostic tests.

Furthermore, the increasing applications of NGS, the rising adoption of bioinformatics and genomic data management solutions, collaborations between vendors to develop library preparation protocols, the growing use of bioinformatics and genomic data management solutions for large-scale data analysis and interpretation, the increasing adoption of NGS informatics tools among hospitals and clinical laboratories, and government initiatives supporting large-scale genomic sequencing projects are expected to generate growth opportunities for the players operating in the NGS market.

The report offers a competitive landscape based on an extensive assessment of the product portfolio offerings, geographic presences, and key strategic developments adopted by leading market players in the industry over four years (2021-2024). The key players operating in the global next-generation sequencing (NGS) market are Illumina, Inc. (U.S.), Thermo Fisher Scientific Inc. (U.S.), F. Hoffmann-La Roche Ltd. (Switzerland), Revvity, Inc. (U.S.), QIAGEN N.V. (Netherlands), Agilent Technologies, Inc. (U.S.), Pacific Biosciences of California, Inc. (U.S.), Danaher Corporation (U.S.), Oxford Nanopore Technologies Plc. (U.K.), MGI Tech Co., Ltd. (China), Tecan Group Ltd. (Switzerland), Beijing Genomics Institute (BGI) (China), Eppendorf AG (Germany), Hamilton Company (U.S.), Hudson Robotics (U.S.), LGC Limited (U.K.), Fabric Genomics, Inc. (U.S.), DNASTAR, Inc. (U.S.), Eurofins Scientific SE (Luxembourg), Novogene Co. Ltd. (China), and Quest Diagnostics Incorporated (U.S.).

Among the offerings studied in this report, in 2024, the commercial sequencing/outsourced services segment is expected to account for the largest share of 38.0% of the market. The large market share of this segment can be attributed to the benefits offered by NGS service providers, including quick results, cost-effectiveness, and a wide array of services available for various applications.

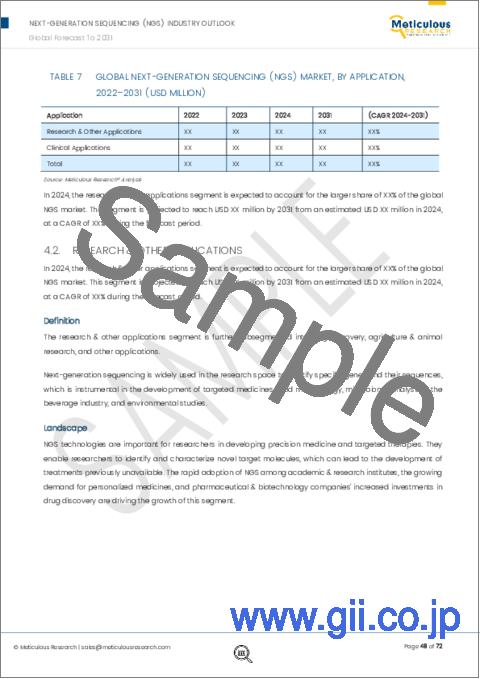

Among the applications studied in this report, in 2024, the research & other applications segment is expected to account for the largest share of 62.2% of the next-generation sequencing (NGS) market. The large share of the segment is attributed to the decreasing cost of sequencing procedures, increasing R&D by pharmaceutical and biotechnology companies for drug discovery, the increasing applications of NGS in multiple clinical and research settings, and the increasing use of informatics solutions to find pharmacological targets, confirm therapeutic hypotheses, and predict the potential safety of inhibitory compounds aimed at molecular targets.

Among the end users studied in this report, in 2024, the pharmaceutical & biotechnology companies segment is expected to account for the largest share of 43.5% of the next-generation sequencing (NGS) market. The large market share of this segment can be attributed to the increasing R&D spending by pharmaceutical & biotechnology companies and the rising incidence of chronic diseases, which drive the adoption of next-generation sequencing products among pharmaceutical & biotechnology companies.

An in-depth analysis of the geographical scenario of the global next-generation sequencing (NGS) market provides detailed qualitative and quantitative insights into five major regions (North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa) along with the coverage of major countries in each region. In 2024, North America is expected to account for the largest share of over 48.7% of the next-generation sequencing (NGS) market. Additionally, in 2024, the U.S. is expected to account for the largest share of the next-generation sequencing (NGS) market in North America. North America's large market share is attributed to the favorable government initiatives for genomic research, growing applications of sequencing-based research, presence of leading providers of next-generation sequencing technologies in the region, increasing research investments by pharmaceutical and biopharmaceutical companies, declining cost of sequencing coupled with the rising availability of advanced sequencing products and solutions, increasing cancer prevalence, and favorable reimbursement scenario in the region.

Scope of the Report:

Next-Generation Sequencing (NGS) Market Assessment-by Offering

- Sample Preparation

- Kits & Reagents

- Nucleic Acid Extraction and Amplification

- Library Preparation

- DNA Library Preparation

- RNA Library Preparation

- Quality Control

- Other Reagents (1)

- Workstations/Robotic Platforms for Library Preparation

- Sequencing

- NGS Systems

- Sequencing by Synthesis

- Ion Semiconductor Sequencing

- Single-molecule Real-time Sequencing (SMRT)

- DNA Nanoball (DNB) Sequencing

- Other Technologies (2)

- Services (3)

- Data Analysis/Bioinformatics

- Software

- By Type

- Data Analysis Software

- Data Interpretation and Reporting Tools

- Data Storage and Computing Tools

- Laboratory Information Management Systems (LIMS)

- By Deployment Mode

- Web and Cloud-based

- On-premise

- NGS Informatics Services (4)

- Commercial Sequencing/ Outsourced Services

- Targeted Sequencing Services

- RNA Sequencing Services

- Whole Genome Sequencing Services

- De Novo Sequencing Services

- Exome Sequencing Services

- ChIP Sequencing Services

- Methyl Sequencing Services

- Other Commercial Sequencing Services (5)

Next-Generation Sequencing (NGS) Market Assessment-by Application

- Research & Other Applications

- Drug Discovery

- Agriculture & Animal Research

- Other Applications (6)

- Clinical Applications

- Reproductive Health Diagnosis

- Oncology

- Infectious Diseases

- Other Clinical Applications (7)

Next-Generation Sequencing (NGS) Market Assessment-by End User

- Hospitals & Diagnostic Laboratories

- Pharmaceutical & Biotechnology Companies

- Academic Institutes & Research Centers

- Other End Users (8)

Note: 1. Other Reagents include dilution buffers, DNA standards, target enrichment kits/reagents, and other reagents required to support the NGS sample preparation workflow

2. Other Technologies include Nanopore sequencing & Avidity Sequencing Technology

3. Services include support services, such as the upgradation of software, customer support, equipment training, monitoring, installation services, and more

4. NGS informatics services include support services, such as bioinformatics data analysis services, bioinformatics consulting services, bioinformatics training, and IT professional services.

5. Other Commercial Sequencing Services include degradome sequencing, ribosome profiling, amplicon sequencing, CRISPR validation, viral genome sequencing, and immunogenomics services

6. Other Applications include food microbiology, microbiota analysis in the beverage industry, and environmental studies

7. Other Clinical Applications include detection of genetic aberrations in neurological disorders, rare diseases, metabolic and immune disorders, and food-borne illnesses

8. Other End Users include forensic laboratories & security agencies, food & beverage companies, and agriculture companies.

Next-Generation Sequencing (NGS) Market Assessment-by Geography

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- Italy

- U.K.

- Spain

- Rest of Europe (RoE)

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific (RoAPAC)

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

TABLE OF CONTENTS

1. Introduction

- 1.1. Market Definition & Scope

- 1.2. Market Ecosystem

- 1.3. Currency & Limitations

- 1.4. Key Stakeholders

2. Research Methodology

- 2.1. Research Approach

- 2.2. Process of Data Collection and Validation

- 2.2.1. Secondary Research

- 2.2.2. Primary Research/Interviews with Key Opinion Leaders of the Industry

- 2.3. Market Sizing and Forecasting

- 2.3.1. Market Size Estimation Approach

- 2.3.2. Growth Forecast Approach

- 2.4. Assumptions for the Study

3. Executive Summary

4. Market Insights

- 4.1. Overview

- 4.2. Factors Affecting Market Growth

- 4.2.1. Impact Analysis of Market Dynamics

- 4.2.1.1. Rising Cancer Prevalence & Increasing Application of NGS in Cancer Treatment and Research Driving Market Growth

- 4.2.1.2. Availability of Alternative Technologies Restraining Market Growth

- 4.2.1.3. Increasing Application of NGS in Personalized Medicine Generating Growth Opportunities for Market Players

- 4.2.1.4. Data Storage, Handling, Interpretation, and Confidentiality Concerns Expected to Remain a Major Challenge for Market Stakeholders

- 4.2.2. Factor Analysis

- 4.2.1. Impact Analysis of Market Dynamics

- 4.3. Industry Trends

- 4.3.1. Increasing Partnerships & Collaborations Among NGS Solution Providers to Expand and Advance Product Offerings

- 4.3.2. Development of Portable Sequencing Technologies

- 4.3.3. Increasing Demand for NGS Automation

- 4.4. Pricing Analysis

- 4.4.1. NGS Instruments and Consumables

- 4.4.2. NGS Services

- 4.5. Regulatory Analysis

- 4.5.1. NGS Instruments & Consumables

- 4.5.1.1. North America

- 4.5.1.1.1. U.S.

- 4.5.1.1.2. Canada

- 4.5.1.2. Europe

- 4.5.1.3. Asia-Pacific

- 4.5.1.3.1. China

- 4.5.1.3.2. Japan

- 4.5.1.3.3. India

- 4.5.1.4. Latin America

- 4.5.1.5. Middle East

- 4.5.1.1. North America

- 4.5.2. NGS Informatics

- 4.5.1. NGS Instruments & Consumables

- 4.6. Case Studies/Use Cases

- 4.6.1. Case Study A

- 4.6.2. Case Study B

- 4.6.3. Case Study C

- 4.6.4. Case Study D

- 4.7. Porter's Five Forces Analysis

- 4.7.1. Bargaining Power of Buyers

- 4.7.2. Bargaining Power of Suppliers

- 4.7.3. Threat of Substitutes

- 4.7.4. Threat of New Entrants

- 4.7.5. Degree of Competition

5. Next-Generation Sequencing (NGS) Market Assessment - by Offering

- 5.1. Overview

- 5.2. Sample Preparation

- 5.2.1. Kits & Reagents

- 5.2.1.1. Nucleic Acid Extraction and Amplification

- 5.2.1.2. Library Preparation

- 5.2.1.2.1. DNA Library Preparation

- 5.2.1.2.2. RNA Library Preparation

- 5.2.1.3. Quality Control

- 5.2.1.4. Other Kits & Reagents

- 5.2.2. NGS Workstations

- 5.2.1. Kits & Reagents

- 5.3. Sequencing

- 5.3.1. NGS Systems

- 5.3.1.1. Sequencing by Synthesis

- 5.3.1.2. Ion Semiconductor Sequencing

- 5.3.1.3. Single-Molecule Real-Time Sequencing (SMRT)

- 5.3.1.4. DNA Nanoball (DNB) Sequencing

- 5.3.1.5. Other Technologies

- 5.3.2. Consumables

- 5.3.3. Services

- 5.3.1. NGS Systems

- 5.4. Data Analysis/Bioinformatics

- 5.4.1. Software

- 5.4.1.1. Software Market, by Type

- 5.4.1.1.1. Data Analysis Software

- 5.4.1.1.2. Data Interpretation and Reporting Tools

- 5.4.1.1.3. Data Storage and Computing Tools

- 5.4.1.1.4. Laboratory Information Management Systems (LIMS)

- 5.4.1.2. Software Market, by Deployment Mode

- 5.4.1.2.1. Web and Cloud-Based

- 5.4.1.2.2. On-Premise

- 5.4.1.1. Software Market, by Type

- 5.4.2. NGS Informatics Services

- 5.4.1. Software

- 5.5. Commercial Sequencing/Outsourced Services

- 5.5.1. Targeted Sequencing Services

- 5.5.2. RNA Sequencing Services

- 5.5.3. De Novo Sequencing Services

- 5.5.4. Exome Sequencing Services

- 5.5.5. Chip Sequencing Services

- 5.5.6. Methyl Sequencing Services

- 5.5.7. Whole Genome Sequencing Services

- 5.5.8. Other Commercial Sequencing Services

6. Next-Generation Sequencing (NGS) Market Assessment - by Application

- 6.1. Overview

- 6.2. Research & Other Applications

- 6.2.1. Drug Discovery

- 6.2.2. Agriculture & Animal Research

- 6.2.3. Other Applications

- 6.3. Clinical Applications

- 6.3.1. Oncology

- 6.3.2. Reproductive Health

- 6.3.3. Infectious Diseases

- 6.3.4. Other Clinical Applications

7. Next-Generation Sequencing (NGS) Market Assessment - by End User

- 7.1. Overview

- 7.2. Pharmaceutical & Biotechnology Companies

- 7.3. Hospitals & Diagnostic Laboratories

- 7.4. Academic Institutes & Research Centers

- 7.5. Other End Users

8. Next-Generation Sequencing (NGS) Market Assessment - by Geography

- 8.1. Overview

- 8.2. North America

- 8.2.1. U.S.

- 8.2.2. Canada

- 8.3. Europe

- 8.3.1. Germany

- 8.3.2. France

- 8.3.3. U.K.

- 8.3.4. Italy

- 8.3.5. Spain

- 8.3.6. Rest of Europe (RoE)

- 8.4. Asia-Pacific

- 8.4.1. China

- 8.4.2. Japan

- 8.4.3. India

- 8.4.4. Rest of Asia-Pacific (RoAPAC)

- 8.5. Latin America

- 8.5.1. Brazil

- 8.5.2. Mexico

- 8.5.3. Rest of Latin America (RoLATAM)

- 8.6. Middle East & Africa

9. Competition Analysis

- 9.1. Overview

- 9.2. Key Growth Strategies

- 9.3. Competitive Benchmarking

- 9.4. Competitive Dashboard

- 9.4.1. Industry Leaders

- 9.4.2. Market Differentiators

- 9.4.3. Vanguards

- 9.4.4. Emerging Companies

- 9.5. Market Share Analysis (2023)

- 9.5.1. Instrument & Consumables

- 9.5.2. Data Analysis/Bioinformatics

- 9.5.3. Commercial Sequencing/Outsourced Services

- 9.5.4. NGS Workstations

10. Company Profiles (Company Overview, Financial Overview, Product Portfolio, and Strategic Developments)

- 10.1. Illumina, Inc.

- 10.2. Thermo Fisher Scientific Inc.

- 10.3. F. Hoffmann-La Roche Ltd

- 10.4. Eurofins Scientific Se

- 10.5. Beijing Genomics Institute (BGI)

- 10.6. Qiagen N.V.

- 10.7. Agilent Technologies, Inc.

- 10.8. Revvity, Inc.

- 10.9. Pacific Biosciences of California Inc.

- 10.10. Danaher Corporation

- 10.11. Oxford Nanopore Technologies Plc.

- 10.12. Tecan Group Ltd.

- 10.13. Hamilton Company

- 10.14. Hudson Robotics

- 10.15. LGC Limited

- 10.16. Eppendorf AG

- 10.17. Novogene Co., Ltd.

- 10.18. Dnastar, Inc.

- 10.19. Fabric Genomics, Inc.

- 10.20. MGI Tech Co., Ltd.

- 10.21. Quest Diagnostics Incorporated

(*Note: SWOT Analysis Provided for Top 5 Companies*)

11. Appendix

- 11.1. Available Customization

- 11.2. Related Reports