|

|

市場調査レポート

商品コード

1364962

IVD品質管理市場:提供サービス別(製品、データ管理、サービス)、技術別(生化学、分子、免疫測定、血液学)、用途別(感染症、腫瘍学、心臓病学)、エンドユーザー別-2030年までの世界予測IVD Quality Control Market by Offering (Product, Data Management, Service), Technology (Biochemistry, Molecular, Immunoassay, Hematology), Application (Infectious Diseases, Oncology, Cardiology), and End User - Global Forecast to 2030 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| IVD品質管理市場:提供サービス別(製品、データ管理、サービス)、技術別(生化学、分子、免疫測定、血液学)、用途別(感染症、腫瘍学、心臓病学)、エンドユーザー別-2030年までの世界予測 |

|

出版日: 2023年10月17日

発行: Meticulous Research

ページ情報: 英文 267 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

IVD品質管理市場:オファリング別(製品[血清、血液、尿ベース]、データ管理、サービス)、技術別(生化学、分子、免疫測定、血液学)、用途別(感染症、腫瘍学、心臓病学)、エンドユーザー別-2030年までの世界予測

IVD品質管理市場は、2023年から2030年までのCAGRが4.3%で、2030年には21億9,000万米ドルに達すると予測されます。

広範な1次調査と2次調査を経て、当レポートはIVD品質管理市場の詳細な分析を提供しています。また、IVD品質管理市場の主な促進要因・市場抑制要因・課題・機会に関する洞察も提供しています。IVD品質管理市場の成長は、高齢者人口の増加と相まって慢性疾患の有病率が上昇していること、第三者品質管理に対する需要の高まり、内部および外部品質評価報告書の必要性、臨床検査室数の増加、POC(ポイントオブケア)および迅速診断に対する需要の高まりが原動力となっています。しかし、品質管理に関する厳しい技術要件や規制プロセスがこの市場の成長を抑制しています。

多項目・多検体検査に対する需要の高まりは、市場成長の機会となります。しかし、規制状況の進化と品質管理/品質保証材料へのアクセス不足が、市場成長の主な課題です。

2023年には、品質管理製品セグメントがIVD品質管理市場で最大のシェアを占めると推定されます。診断製品の採用の増加、外部品質評価プログラムの需要(これらのプログラムでは品質管理が使用されるため)、複数分析項目の品質管理の開発、新製品の発売、独立した管理に対する需要の増加が、このセグメントの最大シェアに寄与しています。

技術別では、2023年には免疫測定/免疫化学分野がIVD品質管理市場で最大のシェアを占めると推定されます。慢性疾患や感染症の流行が拡大し、免疫測定/免疫化学検査の採用が増加していること、これらの検査における技術革新、品質管理の同時開発がこのセグメントの最大シェアに寄与しています。

アプリケーションのうち、2023年には感染症分野がIVD品質管理市場で最大のシェアを占めると推定されます。感染症の流行が拡大していることから、肝炎、レトロウイルス、性感染症、先天性疾患などの感染症に対する体外診断用医薬品(IVD)検査の測定精度を監視するための品質管理が幅広く提供されています。WHOによると、2020年には全世界で3億7,600万件の性感染症(STI)が新たに報告され、そのうちクラミジアが1億2,900万件、淋病が8,200万件、梅毒が710万件、トリコモナス症が1億5,600万件と推定されています。このような感染症の診断の必要性は、検査の品質評価のための品質管理も必要とし、これがさらにこのセグメントの最大シェアを支えています。

エンドユーザーのうち、2023年には病院・診療所セグメントがIVD品質管理市場で最大のシェアを占めると推定されます。この大きなセグメントシェアは、病院で実施される大量の診断検査、医療関連感染(HAI)の有病率の上昇、医療費の増加、新興市場全体での病院・クリニック数の増加が主な要因です。

IVD品質管理市場の地域別シナリオの詳細分析では、5つの主要地域(北米、欧州、アジア太平洋、ラテンアメリカ、中東&アフリカ)の詳細な定性的・定量的洞察を、各地域の主要国のカバレッジとともに提供しています。2023年には、北米がIVD品質管理市場で最大のシェアを占め、次いで欧州、アジア太平洋、ラテンアメリカ、中東&アフリカが続くと推定されます。慢性疾患や感染症の有病率の高さ、疾患の早期診断に関する意識の高まり、先進的な診断製品の採用拡大、資金調達活動の活発化、診断技術の新規開発と相まって、この市場の最大シェアを支える要因となっています。

調査範囲:

IVD品質管理市場の提供製品別評価

- 品質管理製品

- 品質管理製品、製品タイプ別

- 血清/血漿ベースのコントロール

- 全血ベース

- 尿ベースコントロール

- その他のコントロール

- 品質管理製品、機能別

- 独立したコントロール

- 機器別コントロール

- 品質評価サービス

- データ管理ソリューション

注釈その他のコントロールには、唾液ベースのコントロール、脳脊髄液ベースのコントロール、タンパク質コントロールが含まれます。

IVD品質管理市場の技術別評価

- 免疫測定/免疫化学

- 生化学/臨床化学

- 分子診断学

- 血液学

- 凝固/止血

- 微生物学

- その他の技術

注釈その他の技術には、組織化学、尿検査、全血グルコースモニタリングなどが含まれる

IVD品質管理市場のアプリケーション別評価

- 感染症

- 腫瘍学

- 心臓病学

- 自己免疫疾患

- 神経学

- その他

注釈その他のアプリケーションには、妊娠・不妊検査、薬物乱用検査、糖尿病、遺伝子疾患、微量元素検査などが含まれます。

IVD品質管理市場のエンドユーザー別評価

- 病院・クリニック

- 診断研究所

- 学術機関および調査研究所

- その他のエンドユーザー

注その他のエンドユーザーには、在宅ケア、介護施設、外来ケアセンター、輸血検査室などが含まれます。

IVD品質管理市場の地域別評価

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場

- 概要

- 市場成長への影響要因

- 市場力学の影響分析

- 要因分析

- 技術動向

- 規制分析

- IVD製品に対する規制

- 北米

- 米国

- カナダ

- 欧州

- アジア太平洋

- 中国

- 日本

- インド

- ラテンアメリカ

- 中東・アフリカ

- 北米

- 品質管理に関する規制

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- その他欧州(RoE)

- アジア太平洋

- 中国

- 日本

- インド

- その他アジア太平洋地域(RoAPAC)

- ラテンアメリカ

- 中東・アフリカ

- 北米

- IVD製品に対する規制

- 価格分析

- ポーターのファイブフォース分析

- 関連市場分析:体外診断(IVD)市場

第5章 体外診断用医薬品(IVD)品質管理市場:製品別アセスメント

- 概要

- 品質管理製品

- 品質管理製品(タイプ別)

- 血清/血漿ベースコントロール

- 全血ベース

- 尿ベースコントロール

- その他のコントロール

- 品質管理製品、機能別

- 独立したコントロール

- 機器別コントロール

- 品質管理製品(タイプ別)

- 品質評価サービス

- データ管理ソリューション

第6章 IVD品質管理市場の技術別評価

- 概要

- 免疫測定/免疫化学

- 生化学/臨床化学

- 分子診断学

- 血液学

- 凝固/止血

- 微生物学

- その他の技術

第7章 IVD品質管理の世界市場:アプリケーション別評価

- 概要

- 感染症

- 腫瘍学

- 循環器

- 自己免疫疾患

- 神経学

- その他の用途

第8章 IVD品質管理市場のエンドユーザー別評価

- 概要

- 病院・クリニック

- 診断研究所

- 学術機関・研究所

- その他のエンドユーザー

第9章 IVD品質管理市場の地域別評価

- 概要

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

第10章 競合分析

- イントロダクション

- 主要成長戦略

- 競合ベンチマーキング

- 競合ダッシュボード

- 業界リーダー

- 市場差別化要因

- 先行企業

- 新興企業

第11章 企業プロファイル

- Siemens Healthineers AG

- 会社概要

- 財務概要

- 製品ポートフォリオ

- SWOT分析

- Bio-Rad Laboratories, Inc.

- 会社概要

- 財務概要

- 製品ポートフォリオ

- 戦略的展開

- SWOT分析

- Danaher Corporation

- 会社概要

- 財務概要

- 製品ポートフォリオ

- SWOT分析

- LGC Group

- 会社概要

- 財務概要

- 製品ポートフォリオ

- 戦略的展開

- SWOT分析

- Thermo Fisher Scientific Inc.

- 事業概要

- 財務概要

- 製品ポートフォリオ

- 戦略的展開

- SWOT分析

- Randox Laboratories Ltd.

- 会社概要

- 製品ポートフォリオ

- 戦略的展開

- SWOT分析

- SERO AS

- 会社概要

- 製品ポートフォリオ

- 戦略的展開

- QuidelOrtho Corporation

- 事業概要

- 財務概要

- 製品ポートフォリオ

- 戦略的展開

- Streck LLC

- 会社概要

- 製品ポートフォリオ

- 戦略的展開

- Microbiologics, Inc.

- 会社概要

- 製品ポートフォリオ

- 戦略的開発

- Bio-Techne Corporation

- 会社概要

- 財務概要

- 製品ポートフォリオ

- 戦略的展開

第12章 付録

- Table 1 A Comparison Between the Characteristics of PBRTQC and Statistical IQC

- Table 2 Regulatory Authorities Governing IVD Quality Controls, by Country/Region

- Table 3 IVD Quality Control Product Pricing

- Table 4 Global IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 5 Global Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 6 Global Quality Control Products Market, by Country/Region, 2021-2030 (USD Million)

- Table 7 Global Serum/Plasma-Based Controls Market, by Country/Region, 2021-2030 (USD Million)

- Table 8 Global Whole Blood-Based Controls Market, by Country/Region, 2021-2030 (USD Million)

- Table 9 Global Urine-Based Controls Market, by Country/Region, 2021-2030 (USD Million)

- Table 10 Global Other Controls Market, by Country/Region, 2021-2030 (USD Million)

- Table 11 Global Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 12 Global Independent Controls Market, by Country/Region, 2021-2030 (USD Million)

- Table 13 Global Instrument-Specific Controls Market, by Country/Region, 2021-2030 (USD Million)

- Table 14 Global Quality Assessment Services Market, by Country/Region, 2021-2030 (USD Million)

- Table 15 Global Data Management Solutions Market, by Country/Region, 2021-2030 (USD Million)

- Table 16 Global IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 17 Global IVD Quality Control Market for Immunoassay/Immunochemistry, by Country/Region, 2021-2030 (USD Million)

- Table 18 Global IVD Quality Control Market for Biochemistry/Clinical Chemistry, by Country/Region, 2021-2030 (USD Million)

- Table 19 Global IVD Quality Control Market for Molecular Diagnostics, by Country/Region, 2021-2030 (USD Million)

- Table 20 Global IVD Quality Control Market for Hematology, by Country/Region, 2021-2030 (USD Million)

- Table 21 Global IVD Quality Control Market for Coagulation/Hemostasis, by Country/Region, 2021-2030 (USD Million)

- Table 22 Global IVD Quality Control Market for Microbiology, by Country/Region, 2021-2030 (USD Million)

- Table 23 Global IVD Quality Control Market for Other Technologies, by Country/Region, 2021-2030 (USD Million)

- Table 24 Global IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 25 Global IVD Quality Control Market for Infectious Diseases, by Country/Region, 2021-2030 (USD Million)

- Table 26 Increase in the Number of New Cancer Cases Globally (2020-2040)

- Table 27 Global IVD Quality Control Market for Oncology, by Country/Region, 2021-2030 (USD Million)

- Table 28 Global IVD Quality Control Market for Cardiology, by Country/Region, 2021-2030 (USD Million)

- Table 29 Global IVD Quality Control Market for Autoimmune Disorders, by Country/Region, 2021-2030 (USD Million)

- Table 30 Global IVD Quality Control Market for Neurology, by Country/Region, 2021-2030 (USD Million)

- Table 31 Global IVD Quality Control Market for Other Applications, by Country/Region, 2021-2030 (USD Million)

- Table 32 Global IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 33 Global IVD Quality Control Market for Hospitals & Clinics, by Country/Region, 2021-2030 (USD Million)

- Table 34 Global IVD Quality Control Market for Diagnostic Laboratories, by Country/Region, 2021-2030 (USD Million)

- Table 35 Global IVD Quality Control Market for Academic Institutes & Research Laboratories, by Country/Region, 2021-2030 (USD Million)

- Table 36 Global IVD Quality Control Market for Other End Users, by Country/Region, 2021-2030 (USD Million)

- Table 37 Global IVD Quality Control Market, by Country/Region, 2021-2030 (USD Million)

- Table 38 North America: Estimated Cancer Cases, 2020-2030

- Table 39 North America: IVD Quality Control Market, by Country, 2021-2030 (USD Million)

- Table 40 North America: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 41 North America: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 42 North America: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 43 North America: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 44 North America: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 45 North America: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 46 U.S.: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 47 U.S.: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 48 U.S.: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 49 U.S.: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 50 U.S.: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 51 U.S.: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 52 Canada: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 53 Canada: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 54 Canada: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 55 Canada: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 56 Canada: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 57 Canada: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 58 Europe: IVD Quality Control Market, by Country/Region, 2021-2030 (USD Million)

- Table 59 Europe: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 60 Europe: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 61 Europe: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 62 Europe: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 63 Europe: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 64 Europe: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 65 Germany: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 66 Germany: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 67 Germany: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 68 Germany: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 69 Germany: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 70 Germany: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 71 France: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 72 France: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 73 France: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 74 France: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 75 France: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 76 France: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 77 U.K.: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 78 U.K.: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 79 U.K.: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 80 U.K.: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 81 U.K.: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 82 U.K.: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 83 Italy: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 84 Italy: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 85 Italy: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 86 Italy: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 87 Italy: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 88 Italy: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 89 Spain: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 90 Spain: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 91 Spain: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 92 Spain: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 93 Spain: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 94 Spain: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 95 Rest of Europe: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 96 Rest of Europe: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 97 Rest of Europe: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 98 Rest of Europe: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 99 Rest of Europe: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 100 Rest of Europe: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 101 Asia-Pacific: IVD Quality Control Market, by Country/Region, 2021-2030 (USD Million)

- Table 102 Asia-Pacific: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 103 Asia-Pacific: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 104 Asia-Pacific: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 105 Asia-Pacific: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 106 Asia-Pacific: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 107 Asia-Pacific: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 108 China: Mass Testing Drives to Control The Spread of Covid-19 Infections

- Table 109 China: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 110 China: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 111 China: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 112 China: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 113 China: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 114 China: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 115 Japan: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 116 Japan: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 117 Japan: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 118 Japan: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 119 Japan: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 120 Japan: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 121 India: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 122 India: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 123 India: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 124 India: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 125 India: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 126 India: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 127 Rest of Asia-Pacific: Estimated Number of New Cancer Cases, by Country (2020-2030)

- Table 128 Rest of Asia-Pacific: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 129 Rest of Asia-Pacific: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 130 Rest of Asia-Pacific: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 131 Rest of Asia-Pacific: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 132 Rest of Asia-Pacific: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 133 Rest of Asia-Pacific: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 134 Latin America: IVD Quality Control Market, by Country/Region, 2021-2030 (USD Million)

- Table 135 Latin America: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 136 Latin America: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 137 Latin America: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 138 Latin America: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 139 Latin America: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 140 Latin America: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 141 Brazil: Testing Initiatives for COVID-19

- Table 142 Brazil: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 143 Brazil: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 144 Brazil: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 145 Brazil: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 146 Brazil: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 147 Brazil: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 148 Mexico: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 149 Mexico: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 150 Mexico: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 151 Mexico: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 152 Mexico: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 153 Mexico: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 154 Rest of Latin America: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 155 Rest of Latin America: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 156 Rest of Latin America: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 157 Rest of Latin America: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 158 Rest of Latin America: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 159 Rest of Latin America: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 160 Middle East & Africa: IVD Quality Control Market, by Offering, 2021-2030 (USD Million)

- Table 161 Middle East & Africa: Quality Control Products Market, by Type, 2021-2030 (USD Million)

- Table 162 Middle East & Africa: Quality Control Products Market, by Function, 2021-2030 (USD Million)

- Table 163 Middle East & Africa: IVD Quality Control Market, by Technology, 2021-2030 (USD Million)

- Table 164 Middle East & Africa: IVD Quality Control Market, by Application, 2021-2030 (USD Million)

- Table 165 Middle East & Africa: IVD Quality Control Market, by End User, 2021-2030 (USD Million)

- Table 166 Recent Developments, by Company, 2020-2023

IVD Quality Control Market by Offering (Product [Serum, Blood, Urine-based], Data Management, Service), Technology (Biochemistry, Molecular, Immunoassay, Hematology), Application (Infectious Diseases, Oncology, Cardiology), and End User-Global Forecast to 2030

The IVD quality control market is expected to reach $2.19 billion by 2030, at a CAGR of 4.3% from 2023 to 2030.

After extensive primary and secondary research, the report provides an in-depth analysis of the IVD quality control market. The report also provides insights into the key drivers, restraints, challenges, and opportunities in the IVD quality control market. The growth of the IVD quality control market is driven by the rising prevalence of chronic diseases, coupled with the increasing geriatric population, growing demand for third-party quality controls, need for internal and external quality assessment reports, increasing number of clinical laboratories, growing demand for Point-of-Care (POC) and rapid diagnostics. However, stringent technical requirements and regulatory processes for quality controls restrain this market's growth.

The growing demand for multi-analyte and multi-instrument controls offers opportunities for market growth. However, the evolving regulatory landscape and lack of access to quality control/quality assurance materials are the major challenges to market growth.

Among the offering, in 2023, the quality control products segment is estimated to account for the largest share of the IVD quality control market. Increasing adoption of diagnostic products, demand for external quality assessment programs as these programs use quality controls in their programs, development of multi-analyte quality controls, new product launches, and increasing demand for independent controls contribute to the segments' largest share.

Among the technologies, in 2023, the immunoassay/immunochemistry segment is estimated to account for the largest share of the IVD quality control market. The growing prevalence of chronic and infectious diseases and the increased adoption of immunoassay/immunochemistry tests, technological innovations in these tests, and the simultaneous development of quality control contributed to the segment's largest share.

Among the application, in 2023, the infectious diseases segment is estimated to account for the largest share of the IVD quality control market. The increasing prevalence of infectious diseases has led to the availability of a broad range of quality controls that are designed to monitor the assay precision of IVD tests for infectious diseases such as hepatitis, retrovirus, sexually transmitted diseases, congenital diseases, and other infectious diseases. According to the WHO, in 2020, there were an estimated 376 million new cases of sexually transmitted infections (STIs) worldwide, with chlamydia accounting for 129 million, gonorrhea for 82 million, syphilis for 7.1 million, and trichomoniasis for 156 million of the reported cases. The need for diagnosis of such infectious diseases also required quality controls for the quality assessment of tests, which further supported the largest share of the segment.

Among the end users, in 2023, the hospitals & clinics segment is estimated to account for the largest share of the IVD quality control market. The large segment share is majorly attributed to the large volume of diagnostics tests carried out in the hospitals, the rising prevalence of healthcare-associated infections (HAIs), increasing healthcare expenditure, and the rising number of hospitals and clinics across emerging markets.

An in-depth analysis of the geographical scenario of the IVD quality control market provides detailed qualitative and quantitative insights into the five major geographies (North America, Europe, Asia-Pacific, Latin America, the Middle East & Africa) along with the coverage of major countries in each region. In 2023, North America is estimated to account for the largest share of the IVD quality control market, followed by Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The high prevalence of chronic and infectious diseases, increasing awareness regarding early disease diagnosis, growing adoption of advanced diagnostic products, and increasing funding activities, coupled with novel developments in diagnostic technologies, are the factors supporting the largest share of this market.

The key players operating in the IVD quality control market are Seimens Healthineers AG (Germany), Bio-Rad Laboratories, Inc. (U.S.), Danaher Corporation (U.S.), LGC Group (U.K.), Thermo Fisher Scientific Inc. (U.S.), SERO AS (Norway), Randox Laboratories Ltd. (U.K.), QuidelOrtho Corporation (U.S.), Streck LLC (U.S.), Microbiologics, Inc. (U.S.), and Bio-Techne Corporation (U.S.)

Scope of the Report:

IVD Quality Control Market Assessment-by Offering

- Quality Control Products

- Quality Control Products, by Type

- Serum/Plasma-based Controls

- Whole Blood-based Controls

- Urine-based Controls

- Other Controls

- Quality Control Products, by Function

- Independent Controls

- Instrument-Specific Controls

- Quality Assessment Services

- Data Management Solutions

Notes: Other controls include saliva-based controls, cerebrospinal fluid-based, and protein controls.

IVD Quality Control Market Assessment-by Technology

- Immunoassay/Immunochemistry

- Biochemistry/Clinical Chemistry

- Molecular Diagnostics

- Hematology

- Coagulation/Hemostasis

- Microbiology

- Other Technologies

Notes: Other technologies include histochemistry, urinalysis, and whole-blood glucose monitoring

IVD Quality Control Market Assessment-by Application

- Infectious Diseases

- Oncology

- Cardiology

- Autoimmune Disorders

- Neurology

- Other Applications

Notes: Other applications include pregnancy and fertility testing, drug abuse testing, diabetes, genetic disorders, and trace elements testing

IVD Quality Control Market Assessment-by End User

- Hospitals & Clinics

- Diagnostic Laboratories

- Academic Institutes & Research Laboratories

- Other End Users

Notes: Other end users include home care, nursing homes, ambulatory care centers, and transfusion laboratories.

IVD Quality Control Market Assessment-by Geography

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Rest of Asia-Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

TABLE OF CONTENTS

1. Introduction

- 1.1. Market Definition & Scope

- 1.2. Market Ecosystem

- 1.3. Currency & Limitations

- 1.4. Key Stakeholders

2. Research Methodology

- 2.1. Research Approach

- 2.2. Process of Data Collection and Validation

- 2.2.1. Secondary Research

- 2.2.2. Primary Research/Interviews with Key Opinion Leaders of the Industry

- 2.3. Market Sizing and Forecast

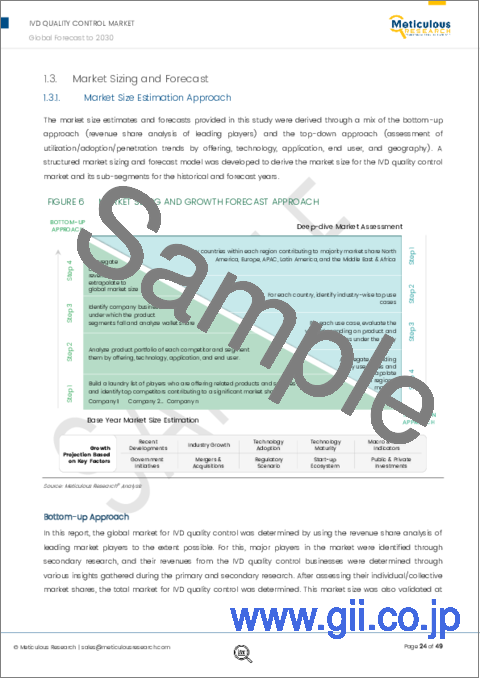

- 2.3.1. Market Size Estimation Approach

- 2.3.2. Growth Forecast Approach

- 2.4. Assumptions for the Study

3. Executive Summary

4. Market Insights

- 4.1. Overview

- 4.2. Factors Affecting Market Growth

- 4.2.1. Impact Analysis of Market Dynamics

- 4.2.2. Factor Analysis

- 4.3. Technology Trends

- 4.4. Regulatory Analysis

- 4.4.1. Regulations for IVD Products

- 4.4.1.1. North America

- 4.4.1.1.1. U.S.

- 4.4.1.1.2. Canada

- 4.4.1.2. Europe

- 4.4.1.3. Asia-Pacific

- 4.4.1.3.1. China

- 4.4.1.3.2. Japan

- 4.4.1.3.3. India

- 4.4.1.4. Latin America

- 4.4.1.5. Middle East & Africa

- 4.4.1.1. North America

- 4.4.2. Regulations for Quality Management

- 4.4.2.1. North America

- 4.4.2.1.1. U.S.

- 4.4.2.1.2. Canada

- 4.4.2.2. Europe

- 4.4.2.2.1. Germany

- 4.4.2.2.2. France

- 4.4.2.2.3. U.K.

- 4.4.2.2.4. Italy

- 4.4.2.2.5. Spain

- 4.4.2.2.6. Rest of Europe (RoE)

- 4.4.2.3. Asia-Pacific

- 4.4.2.3.1. China

- 4.4.2.3.2. Japan

- 4.4.2.3.3. India

- 4.4.2.3.4. Rest of Asia-Pacific (RoAPAC)

- 4.4.2.4. Latin America

- 4.4.2.5. Middle East & Africa

- 4.4.2.1. North America

- 4.4.1. Regulations for IVD Products

- 4.5. Pricing Analysis

- 4.6. Porter's Five Forces Analysis

- 4.6.1. Bargaining Power of Buyers

- 4.6.2. Bargaining Power of Suppliers

- 4.6.3. Threat of Substitutes

- 4.6.4. Threat of New Entrants

- 4.6.5. Degree of Competition

- 4.7. Associated Market Analysis: In Vitro Diagnostics (IVD) Market

5. IVD Quality Control Market Assessment-by Offering

- 5.1. Overview

- 5.2. Quality Control Products

- 5.2.1. Quality Control Products, by Type

- 5.2.1.1. Serum/Plasma-based Controls

- 5.2.1.2. Whole Blood-based Controls

- 5.2.1.3. Urine-based Controls

- 5.2.1.4. Other Controls

- 5.2.2. Quality Control Products, by Function

- 5.2.2.1. Independent Controls

- 5.2.2.2. Instrument-specific Controls

- 5.2.1. Quality Control Products, by Type

- 5.3. Quality Assessment Services

- 5.4. Data Management Solutions

6. IVD Quality Control Market Assessment-by Technology

- 6.1. Overview

- 6.2. Immunoassay/Immunochemistry

- 6.3. Biochemistry/Clinical Chemistry

- 6.4. Molecular Diagnostics

- 6.5. Hematology

- 6.6. Coagulation/Hemostasis

- 6.7. Microbiology

- 6.8. Other Technologies

7. Global IVD Quality Control Market Assessment-by Application

- 7.1. Overview

- 7.2. Infectious Diseases

- 7.3. Oncology

- 7.4. Cardiology

- 7.5. Autoimmune Disorders

- 7.6. Neurology

- 7.7. Other Applications

8. IVD Quality Control Market Assessment-by End User

- 8.1. Overview

- 8.2. Hospitals & Clinics

- 8.3. Diagnostic Laboratories

- 8.4. Academic Institutes & Research Laboratories

- 8.5. Other End Users

9. IVD Quality Control Market Assessment-by Geography

- 9.1. Overview

- 9.2. North America

- 9.2.1. U.S.

- 9.2.2. Canada

- 9.3. Europe

- 9.3.1. Germany

- 9.3.2. France

- 9.3.3. U.K.

- 9.3.4. Italy

- 9.3.5. Spain

- 9.3.6. Rest of Europe

- 9.4. Asia-Pacific

- 9.4.1. China

- 9.4.2. Japan

- 9.4.3. India

- 9.4.4. Rest of Asia-Pacific

- 9.5. Latin America

- 9.5.1. Brazil

- 9.5.2. Mexico

- 9.5.3. Rest of Latin America

- 9.6. Middle East & Africa

10. Competition Analysis

- 10.1. Introduction

- 10.2. Key Growth Strategies

- 10.3. Competitive Benchmarking

- 10.4. Competitive Dashboard

- 10.4.1. Industry Leaders

- 10.4.2. Market Differentiators

- 10.4.3. Vanguards

- 10.4.4. Emerging Companies

11. Company Profiles

- 11.1. Siemens Healthineers AG

- 11.1.1. Company Overview

- 11.1.2. Financial Overview

- 11.1.3. Product Portfolio

- 11.1.4. SWOT Analysis

- 11.2. Bio-Rad Laboratories, Inc.

- 11.2.1. Company Overview

- 11.2.2. Financial Overview

- 11.2.3. Product Portfolio

- 11.2.4. Strategic Developments

- 11.2.5. SWOT Analysis

- 11.3. Danaher Corporation

- 11.3.1. Company Overview

- 11.3.2. Financial Overview

- 11.3.3. Product Portfolio

- 11.3.4. SWOT Analysis

- 11.4. LGC Group

- 11.4.1. Company Overview

- 11.4.2. Financial Overview

- 11.4.3. Product Portfolio

- 11.4.4. Strategic Developments

- 11.4.5. SWOT Analysis

- 11.5. Thermo Fisher Scientific Inc.

- 11.5.1. Business Overview

- 11.5.2. Financial Overview

- 11.5.3. Product Portfolio

- 11.5.4. Strategic Developments

- 11.5.5. SWOT Analysis

- 11.6. Randox Laboratories Ltd.

- 11.6.1. Company Overview

- 11.6.2. Product Portfolio

- 11.6.3. Strategic Developments

- 11.6.4. SWOT Analysis

- 11.7. SERO AS

- 11.7.1. Company Overview

- 11.7.2. Product Portfolio

- 11.7.3. Strategic Developments

- 11.8. QuidelOrtho Corporation

- 11.8.1. Business Overview

- 11.8.2. Financial Overview

- 11.8.3. Product Portfolio

- 11.8.4. Strategic Developments

- 11.9. Streck LLC

- 11.9.1. Company Overview

- 11.9.2. Product Portfolio

- 11.9.3. Strategic Developments

- 11.10. Microbiologics, Inc.

- 11.10.1. Company Overview

- 11.10.2. Product Portfolio

- 11.10.3. Strategic Developments

- 11.11. Bio-Techne Corporation

- 11.11.1. Company Overview

- 11.11.2. Financial Overview

- 11.11.3. Product Portfolio

- 11.11.4. Strategic Developments

12. Appendix

- 12.1. Available Customization

- 12.2. Related Reports