宇宙推進の世界市場 (~2031年):プラットフォーム・タイプ (固体・液体・電気・ハイブリッド)・コンポーネント (ホール効果スラスタ・バイオ推進剤・推進剤タンク・ロケットエンジン・ノズル・PPU)・エンドユーザー・サービス・地域別

Space Propulsion Market By Platform, Type (Solid, Liquid, Electric, Hybrid), Component (Hall-Effect Thrusters, Biopropellant, Propellant Tanks, Rocket Motor, Nozzle, PPU), End User, Services and Region - Global Forecast to 2031- 発行日

- ページ情報

- 英文 285 Pages

- 納期

-

即納可能

営業時間内にお支払方法などの確認が取れ次第、Eメールにて納品となります。営業時間: 9:00am - 6:00pm (土日祝除く)。

- 商品コード

- 2055593

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

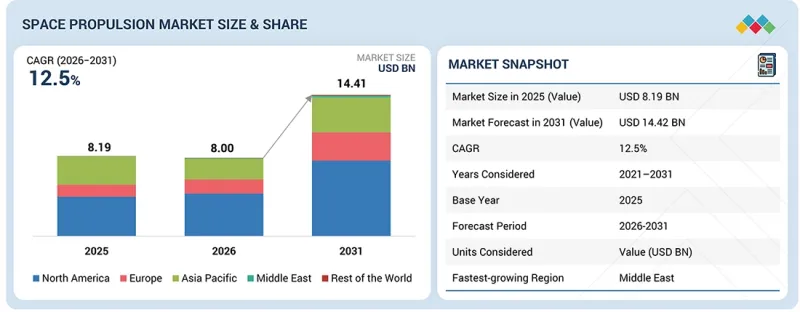

宇宙推進の市場規模は、予測期間中にCAGR 12.5%で拡大し、2026年の80億米ドルから、2031年には144億1,000万米ドルに達すると見込まれています。

| 調査範囲 | |

|---|---|

| 調査対象期間 | 2020年~2031年 |

| 基準年 | 2025年 |

| 予測期間 | 2026年~2031年 |

| 単位 | 金額 (米ドル) |

| セグメント | プラットフォーム、タイプ、コンポーネント、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

軌道上サービス、スペースタグミッション、宇宙デブリ除去、軌道間輸送機により、の拡大により、繰り返しの軌道変更や柔軟なミッション運用をサポートできる推進システムへの需要が高まっており、市場成長を後押ししています。

「エンドユーザー別では、予測期間中、商業セグメントが最も大きなシェアを占めると見込まれています。」

これは、新規衛星打ち上げ、ブロードバンドコンステレーション、地球観測プラットフォーム、および商業打ち上げ活動の大部分が民間企業によって牽引されているためです。また、このセグメントは、LEOコンステレーションにおける交換サイクルの長期化や、コスト効率の高い推進パッケージへの需要拡大の恩恵も受けています。

「コンポーネント別では、スラスタセグメントが2026年から2031年にかけて最も高いCAGRで成長すると予測されています。」

スラスタセグメントが最も高い成長率を示すと予測されるのは、宇宙機の軌道制御、姿勢制御、軌道修正、および制御された軌道離脱にスラスタが直接必要とされるためです。衛星プラットフォームの小型化が進み、ミッションにおける機動の頻度が高まるにつれ、コンパクトな化学式および電気式スラスタへの需要が高まっています。また、LEO衛星、スペースタグ、月探査機、軌道上サービス機 (OOSV) の増加により、ミッション全体で多様なスラスタ構成へのニーズが高まっています。

「予測期間中、中東地域が最も急速に成長する地域になると予測されています。」

これは主に、同地域の各国が衛星通信、地球観測、国家宇宙計画、および防衛宇宙能力への投資を拡大しているためです。同地域は、主に衛星の購入者である状態から、パートナーシップ、現地機関、および国家衛星計画を通じて、より強固な国内宇宙インフラを構築する方向へと移行しています。これにより、衛星、打ち上げアクセス、および将来の深宇宙探査への参加に関連する推進システムに対する新たな需要が生まれています。

当レポートでは、世界の宇宙推進の市場を調査し、市場概要、市場成長への各種影響因子の分析、技術・特許の動向、法規制環境、ケーススタディ、市場規模の推移・予測、各種区分・地域/主要国別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

よくあるご質問

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

第3章 重要考察

第4章 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- アンメットニーズとホワイトスペース

- 関連市場・異業種との分野横断的機会

- ティア1/2/3企業による戦略的な動き

第5章 業界動向

- エコシステム分析

- バリューチェーン分析

- 貿易分析

- ケーススタディ分析

- 2026年の主要な会議およびイベント

- 投資と資金調達のシナリオ

- 顧客の事業に影響を与える動向/ディスラプション

- マクロ経済見通し

- GDPの動向と予測

- 世界の宇宙産業の動向

- 世界の宇宙推進産業の動向

- 2025年の米国関税の影響

- ボリュームデータ

- 価格分析

- ビジネスモデル

第6章 技術の進歩、AIの影響、特許、イノベーション、将来の応用

- 主要技術

- 電気推進システム

- ソーラーセイル

- イオン推進

- 補完的技術

- 熱管理システム

- 高度な推進剤管理

- 隣接技術

- 磁気プラズマ動力学スラスタ

- 自律推進

- 技術ロードマップ

- AI/生成AIの影響

- 特許分析

- 将来の応用

第7章 規制状況と持続可能性への取り組み

- 地域の規制および遵守事項

- 持続可能性への取り組み

- 認証、ラベル表示、環境基準

第8章 顧客情勢と購買行動

- 意思決定プロセス

- 購買プロセスにおける主要なステークホルダーとその評価基準

- 導入における障壁と内部課題

- 様々なエンドユーザー産業におけるアンメットニーズ

第9章 宇宙推進市場:コンポーネント別

- スラスタ

- 化学スラスタ

- 電気スラスタ

- 推進剤供給システム

- 推進剤タンク

- 圧力・流量調整器

- バルブ

- ターボポンプ

- 燃焼室

- ロケットモーター

- ノズル

- 推進熱制御システム

- 電力処理ユニット

- その他

第10章 宇宙推進市場:エンドユーザー別

- 商業

- 衛星事業者および所有者

- 宇宙打ち上げサービスプロバイダー

- 政府・防衛

- 国立宇宙機関

- その他

第11章 宇宙推進市場:プラットフォーム別

- 衛星

- 小型衛星 (1~1,200kg)

- 中型衛星 (1,201~2,000kg)

- 大型衛星 (2,000kg以上)

- カプセルおよび貨物宇宙船

- 有人宇宙船

- 無人宇宙船

- 惑星間宇宙船および探査機

- 着陸機およびローバー

- 打ち上げロケット

- 小型ロケット

- 中型~大型ロケット

- 再利用可能ロケット

第12章 宇宙推進市場:推進方式別

- 化学推進

- 固体

- 液体

- ハイブリッド

- コールド/ウォームガス

- 非化学推進

- 電気

- 太陽光

- テザー

- 原子力

第13章 宇宙推進市場:支援サービス別

- 設計、エンジニアリング、運用、保守

- ホットファイア試験および環境試験の実施

- 燃料充填、打ち上げ、地上支援

第14章 宇宙推進市場:地域別

- 北米

- 米国

- カナダ

- 欧州

- ロシア

- フランス

- ドイツ

- 英国

- イタリア

- アジア太平洋

- 中国

- 韓国

- 日本

- オーストラリア

- インド

- 中東

- GCC

- その他中東

- 世界のその他の地域

- ラテンアメリカ

- アフリカ

第15章 競合情勢

- 主要参入企業の戦略/強み

- 市場シェア分析

- 収益分析

- ブランド/製品比較

- 企業評価と財務指標

- 企業評価マトリックス:主要企業

- 企業評価マトリックス:スタートアップ/中小企業

- 競合シナリオ

第16章 企業プロファイル

- 主要企業

- SPACEX

- NORTHROP GRUMMAN

- L3HARRIS TECHNOLOGIES, INC.

- ARIANEGROUP

- SAFRAN

- IHI CORPORATION

- LOCKHEED MARTIN CORPORATION

- MOOG INC.

- THALES ALENIA SPACE

- SIERRA NEVADA CORPORATION

- VACCO INDUSTRIES

- BLUE ORIGIN

- EATON

- RAFAEL ADVANCED DEFENSE SYSTEMS LTD.

- OHB SE

- AIRBUS

- AVIO

- その他の企業

- THRUSTME

- URSA MAJOR

- PHASEFOUR

- EXOTRAIL

- DAWN AEROSPACE

- AST ADVANCED SPACE TECHNOLOGIES GMBH

- STANFORD MU CORPORATION

- MANASTU SPACE TECHNOLOGIES PRIVATE LIMITED

- KREIOS SPACE

- FIREFLY AEROSPACE

- BUSEK CO. INC.

- BELLATRIX AEROSPACE

- BENCHMARK SPACE SYSTEMS

- NAMMO

- ENPULSION

第17章 調査手法

第18章 付録

- 発行日

- 発行

- MarketsandMarkets

- ページ情報

- 英文 285 Pages

- 納期

- 即納可能