|

|

市場調査レポート

商品コード

1488029

感圧接着剤の世界市場:化学別、技術別、用途別、最終用途産業別、地域別 - 2029年までの予測Pressure Sensitive Adhesives Market by Chemistry (Acrylic, Rubber, Silicone), Technology (Water-Based, Solvent-Based, Hot-Melt), Application (Tapes, Labels, Graphics), End-Use Industry (Packaging, Automotive), and Region - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 感圧接着剤の世界市場:化学別、技術別、用途別、最終用途産業別、地域別 - 2029年までの予測 |

|

出版日: 2024年05月27日

発行: MarketsandMarkets

ページ情報: 英文 342 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

世界の感圧接着剤の市場規模は、3.0%のCAGRで拡大し、2023年の138億米ドルから160億米ドルに成長すると予測されています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2021年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 検討単位 | 金額(100万米ドル/10億米ドル) |

| セグメント別 | 化学別、技術別、用途別、最終用途産業別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、南米、中東・アフリカ |

包装業界と自動車業界は、PSA市場の成長に大きく貢献しています。包装業界は、多用途、持続可能、効率的な接着剤ソリューションへのニーズを通じて需要を牽引し、自動車業界は、PSAの性能、耐久性、軽量化の利点を活用しています。これらの産業と感圧接着剤との相乗効果が技術革新と市場拡大を促進し、現代の製造業と消費財における感圧接着剤の重要性を浮き彫りにしています。

感圧接着剤(PSA)テープは、布、紙、金属、プラスチックなどの素材の片面または両面に、常温で機能する粘着性の接着剤を塗布した多用途製品です。これらのテープは、最小限の圧力で様々な表面に接着し、相変化することなく粘着特性を維持します。PSAテープには、技術の進歩や用途のニーズに応じて、シングルコート、ダブルコート、強化、非強化などの種類があります。シングルコートPSAテープは、裏面の片面のみに感圧接着剤が塗布されており、電気絶縁、マスキング、表面保護に適しています。ダブルコートPSAテープは、0.5ミルのポリエステル・フィルムのような基材の両面に感圧接着剤を塗布したもので、取り付け、医療用途、メンブレンスイッチなどに使用されます。強化PSAテープは、織布やニット布、ガラス繊維の層を追加して強度を高めたもので、引張強度が要求される厳しい用途に適しています。非支持型PSAテープは、接着剤と剥離ライナーのみで構成され、一時的な取り付けやスプライシングなどの用途に高い柔軟性を提供します。包装、自動車、エレクトロニクス、ヘルスケアなどの業界でPSAテープが広く使用されていることから、さまざまな用途要件を満たす適応性と信頼性が浮き彫りになっています。

パッケージング産業は、都市化、建設投資の増加、衛生、ヘルスケア、化粧品分野の拡大に牽引され、急速に成長すると予測されています。中国、インド、ブラジルのような経済は、生活水準の向上と可処分所得の増加により、この成長に大きく寄与しており、動きの速い消費財(FMCG)部門に燃料を供給しています。オンライン・ショッピングの急増は、効率的なパッケージングとラベリングプロセスに不可欠な感圧接着剤(PSA)テープとラベルの需要をさらに増大させています。この動向は、経済発展のペースを維持し、成長する消費者基盤に対応するために不可欠なパッケージング業界におけるPSAの需要を押し上げる重要な要因となっています。

当レポートでは、世界の感圧接着剤市場について調査し、化学別、技術別、用途別、最終用途産業別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 主要新興国対EU27か国および米国

- 市場力学

- ポーターのファイブフォース分析

- マクロ経済指標

- バリューチェーン分析

- 価格分析

- 主な利害関係者と購入基準

- 貿易分析

- 規制状況と基準

- エコシステム分析

- 顧客ビジネスに影響を与える動向と混乱

- 投資と資金調達のシナリオ

- 特許分析

- 技術分析

- 市場の成長に影響を与える世界経済のシナリオ

- ケーススタディ分析

- 2024年~2025年の主な会議とイベント

第6章 感圧接着剤市場、化学別

- イントロダクション

第7章 感圧接着剤市場、技術別

- イントロダクション

- 水性

- 溶剤ベース

- ホットメルト

- 放射線

第8章 感圧接着剤市場、用途別

- イントロダクション

- テープ

- ラベル

- グラフィック

- その他

第9章 感圧接着剤市場、最終用途産業別

- イントロダクション

- 包装

- 電気、電子、通信

- 自動車・輸送

- 建築・建設

- 医療・ヘルスケア

- その他

第10章 感圧接着剤市場、地域別

- イントロダクション

- 北米

- 欧州

- アジア太平洋

- 南米

- 中東・アフリカ

第11章 競合情勢

- 概要

- 主要参入企業の戦略

- 市場シェア分析

- 収益分析の主要企業5社

- 企業評価と財務指標、2023年

- ブランド/製品比較分析

- 企業評価マトリックス:主要参入企業、2023年

- 企業評価マトリックス:スタートアップ/中小企業、2023年

- 競合シナリオと動向

第12章 企業プロファイル

- 主要参入企業

- HENKEL AG & CO., KGAA

- DOW

- AVERY DENNISON CORPORATION

- H.B. FULLER COMPANY

- 3M

- ARKEMA SA

- SIKA AG

- SCAPA GROUP PLC

- WACKER CHEMIE AG

- ILLINOIS TOOL WORKS INC.

- その他の企業

- TOYO INK AMERICA, LLC

- PIDILITE INDUSTRIES

- HELMITIN ADHESIVES

- JOWAT SE

- MAPEI S.P.A.

- FRANKLIN ADHESIVES & POLYMERS

- DRYTAC CORPORATION

- JESONS

- ADHESIVES RESEARCH INC.

- SHANGHAI JAOUR ADHESIVE PRODUCTS CO., LTD.

- ESTER CHEMICAL INDUSTRIES PVT. LTD.

- DYNA-TECH ADHESIVES, INC.

- CATTIE ADHESIVES

- ADVANCE POLYMER PRODUCTS

- NANPAO RESINS CHEMICAL GROUP

第13章 隣接市場と関連市場

第14章 付録

The global pressure sensitive adhesives market size is projected to grow from USD 13.8 billion in 2023 to USD 16.0 billion, at a CAGR of 3.0%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Million/Billion) |

| Segments | By chemistry, By Technology, By Application, By End Use Industry, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, and Middle East & Africa, |

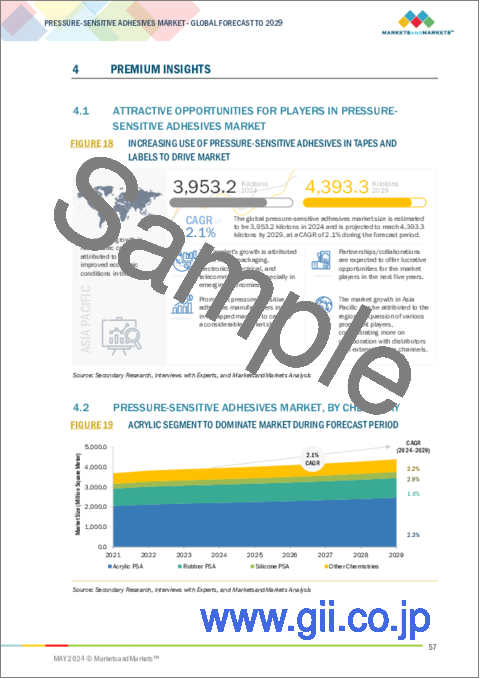

Both the packaging and automotive industries significantly contribute to the growth of the PSA market. The packaging industry drives demand through its need for versatile, sustainable, and efficient adhesive solutions, while the automotive industry leverages the performance, durability, and lightweighting advantages of PSAs. The synergy between these industries and PSAs fosters innovation and market expansion, highlighting the importance of PSAs in modern manufacturing and consumer goods.

The tapes segment is expected to register one of the highest market share during the forecast period

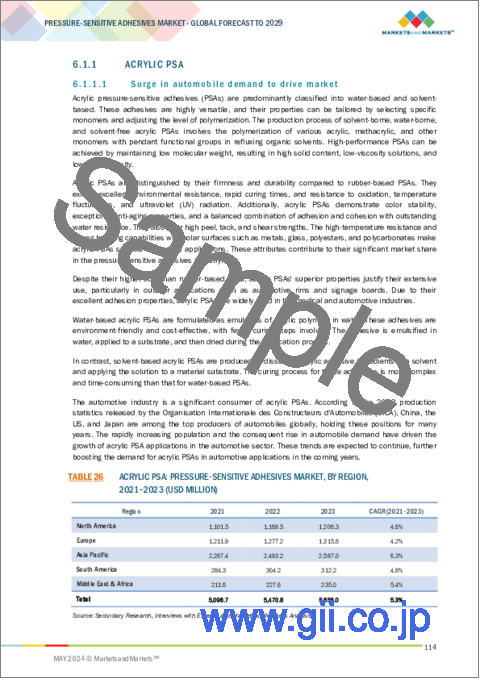

Pressure-sensitive adhesive (PSA) tapes are versatile products made from materials such as cloth, paper, metal, or plastic, coated on one or both sides with a tacky adhesive that functions at room temperature. These tapes adhere to various surfaces with minimal pressure and maintain their adhesive properties without changing phases. PSA tapes come in several types based on technological advancements and application needs: single-coated, double-coated, reinforced, and unsupported. Single-coated PSA tapes have adhesive on only one side of the backing, making them ideal for electrical insulation, masking, and surface protection. Double-coated PSA tapes feature adhesive on both sides of a backing material, such as a 0.5 mil polyester film, and are used for mounting, medical applications, and membrane switches. Reinforced PSA tapes include an additional layer of woven or knitted cloth or glass strands for enhanced strength, suitable for demanding applications requiring extra tensile strength. Unsupported PSA tapes consist solely of adhesives and release liners, offering high flexibility for applications like temporary mounting or splicing. The widespread use of PSA tapes across industries such as packaging, automotive, electronics, and healthcare highlights their adaptability and reliability in meeting various application requirements.

The packaging segment in substrate is expected to register one of the highest CAGR during the forecast period

The packaging industry is projected to grow rapidly, driven by urbanization, increased construction investments, and the expanding hygiene, healthcare, and cosmetic sectors. Economies like China, India, and Brazil are significant contributors to this growth due to their rising standards of living and increasing disposable incomes, which fuel the fast-moving consumer goods (FMCG) sector. The surge in online shopping has further amplified the demand for pressure-sensitive adhesive (PSA) tapes and labels, as they are essential for efficient packaging and labeling processes. This trend is a key factor in boosting the demand for PSAs within the packaging industry, which is vital for maintaining the pace of economic development and catering to the growing consumer base.

North American pressure sensitive adhesives market is estimated to capture one of the highest share in terms of volume during the forecast period

The North American food and beverage and packaging industries share a deeply interconnected relationship. As consumer preferences evolve, influenced by globalization, sustainability initiatives, and a push for innovative solutions, the demand for advanced packaging solutions rises accordingly. Packaging plays a pivotal role in the food and beverage sector by ensuring product preservation, enhancing branding efforts, and meeting stringent regulatory requirements. This symbiosis ultimately drives the success and growth of the food and beverage industry, as effective packaging not only protects and prolongs the shelf life of products but also appeals to consumers through attractive and functional designs. The continuous innovation in packaging materials and technologies thus directly impacts the overall performance and competitiveness of the food and beverage market.

The break-up of the profile of primary participants in the pressure sensitive adhesives market:

- By Company Type: Tier 1 - 46%, Tier 2 - 36%, and Tier 3 - 18%

- By Designation: C Level - 21%, D Level - 23%, and Others - 56%

- By Region: North America - 37%, Europe - 23%, Asia Pacific- 26%, Middle East & Africa - 10%, and South America - 4%

The key companies profiled in this report are Henkel AG & Co., KGaA (Germany), Dow (US), Avery Dennison Company (US), H.B. Fuller Company (US), 3M (US), Arkema S.A. (France), Sika AG (Switzerland), Scapa Group PLC (UK), Wacker Chemie AG (Germany), Illinois Tool Works (US), and others.

Research Coverage:

The pressure sensitive adhesives market is segmented by Chemistry (Acrylic, Rubber, Silicone, and Other Chemistry), Technology (Water-Based, Solvent-Based, Hot-Melt, and Radiation), Applications (Tapes, Labels, Graphics, and Other Application), End-Use Industry (Packaging, Automotive & Transportation, Medical & Healthcare, Building & Construction, Electrical, Electronics & Telecommunication, and Other End-Use Industry), and Region (North America, Europe, Asia Pacific, the Middle East & Africa, and South America). The study's coverage covers detailed information on the key factors influencing the growth of the pressure sensitive adhesives market, such as drivers, constraints, challenges, and opportunities. A thorough examination of the top industry players was carried out in order to provide insights into their company overview, solutions, and services; essential strategies; contracts, partnerships, and agreements. There includes coverage of new product and service launches, mergers and acquisitions, and ongoing developments in the pressure sensitive adhesives market. A competitive analysis of emerging companies in the pressure sensitive adhesives business ecosystem is included in this study. Reasons to buy this report: The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall pressure sensitive adhesives market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Growing demand for pressure sensitive adhesives in emerging economies), restraints (volatility in raw material prices), opportunities (collaboration of distributors in untapped markets), and challenges (strict government regulations).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the pressure sensitive adhesives market

- Market Development: Comprehensive information about lucrative markets - the report analyses the pressure sensitive adhesives market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the pressure sensitive adhesives market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like Henkel AG & Co., KGaA (Germany), Dow (US), Avery Dennison Company (US), H.B. Fuller Company (US), 3M (US), Arkema S.A. (France), Sika AG (Switzerland), Scapa Group PLC (UK), Wacker Chemie AG (Germany), Illinois Tool Works (US). The report also helps stakeholders understand the pulse of the pressure sensitive adhesives market and provides them information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.2.2 DEFINITION AND INCLUSIONS, BY CHEMISTRY

- 1.2.3 DEFINITION AND INCLUSIONS, BY APPLICATION

- 1.2.4 DEFINITION AND INCLUSIONS, BY TECHNOLOGY

- 1.2.5 DEFINITION AND INCLUSIONS, BY END-USE INDUSTRY

- 1.3 MARKET SCOPE

- FIGURE 1 PRESSURE-SENSITIVE ADHESIVES MARKET SEGMENTATION

- 1.3.1 REGIONS COVERED

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- TABLE 1 USD EXCHANGE RATE, 2019-2022

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

- 1.8 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 PRESSURE-SENSITIVE ADHESIVES MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Breakdown of primary interviews

- FIGURE 3 BREAKDOWN OF INTERVIEWS WITH EXPERTS

- 2.1.2.3 Key primary participants

- 2.1.2.4 Key industry insights

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- FIGURE 4 MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- FIGURE 6 PRESSURE-SENSITIVE ADHESIVES MARKET SIZE ESTIMATION, BY CHEMISTRY

- FIGURE 7 PRESSURE-SENSITIVE ADHESIVES MARKET SIZE ESTIMATION, BY REGION

- 2.3 MARKET FORECAST APPROACH

- 2.3.1 SUPPLY-SIDE FORECAST

- FIGURE 8 PRESSURE-SENSITIVE ADHESIVES MARKET: SUPPLY-SIDE FORECAST

- 2.3.2 DEMAND-SIDE FORECAST

- FIGURE 9 PRESSURE-SENSITIVE ADHESIVES MARKET: DEMAND-SIDE FORECAST

- FIGURE 10 METHODOLOGY FOR SUPPLY-SIDE SIZING OF PRESSURE-SENSITIVE ADHESIVES MARKET

- 2.4 FACTOR ANALYSIS

- FIGURE 11 MAJOR FACTORS RESPONSIBLE FOR GLOBAL RECESSION AND THEIR IMPACT ON MARKET

- 2.5 DATA TRIANGULATION

- FIGURE 12 PRESSURE-SENSITIVE ADHESIVES MARKET: DATA TRIANGULATION

- 2.6 ASSUMPTIONS

- 2.7 LIMITATIONS

- 2.8 GROWTH FORECAST

- 2.9 RISK ASSESSMENT

- TABLE 2 PRESSURE-SENSITIVE ADHESIVES MARKET: RISK ASSESSMENT

- 2.10 RECESSION IMPACT ANALYSIS

3 EXECUTIVE SUMMARY

- TABLE 3 PRESSURE-SENSITIVE ADHESIVES MARKET SNAPSHOT (2024 VS. 2029)

- FIGURE 13 ACRYLIC TO BE LARGEST SEGMENT DURING FORECAST PERIOD

- FIGURE 14 WATER-BASED ADHESIVES TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 15 TAPES APPLICATION TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 16 PACKAGING END-USE INDUSTRY TO ACCOUNT FOR LARGEST MARKET DURING FORECAST PERIOD

- FIGURE 17 ASIA PACIFIC TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PRESSURE-SENSITIVE ADHESIVES MARKET

- FIGURE 18 INCREASING USE OF PRESSURE-SENSITIVE ADHESIVES IN TAPES AND LABELS TO DRIVE MARKET

- 4.2 PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY

- FIGURE 19 ACRYLIC SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- 4.3 PRESSURE-SENSITIVE ADHESIVES MARKET IN ASIA PACIFIC, BY CHEMISTRY AND COUNTRY

- FIGURE 20 CHINA ACCOUNTED FOR LARGEST SHARE OF PRESSURE-SENSITIVE ADHESIVES MARKET IN ASIA PACIFIC

- 4.4 PRESSURE-SENSITIVE ADHESIVES MARKET, DEVELOPED VS. EMERGING ECONOMIES

- FIGURE 21 EMERGING ECONOMIES TO REGISTER HIGHER GROWTH DURING FORECAST PERIOD

- 4.5 PRESSURE-SENSITIVE ADHESIVES MARKET, BY KEY COUNTRY

- FIGURE 22 INDIA TO RECORD HIGHEST GROWTH DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- TABLE 4 CHARACTERISTICS OF DIFFERENT ADHESIVE TYPES

- TABLE 5 CHOICE OF BACKING OR CARRIER

- 5.2 KEY EMERGING ECONOMIES VS. EU27 AND US

- FIGURE 23 AVERAGE CHEMICAL PRODUCTION GROWTH PER ANNUM (2011-2021)

- 5.3 MARKET DYNAMICS

- FIGURE 24 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN PRESSURE-SENSITIVE ADHESIVES MARKET

- 5.3.1 DRIVERS

- 5.3.1.1 Growing demand for pressure-sensitive adhesives from packaging industry

- 5.3.1.2 Wide use of pressure-sensitive adhesive tapes in electric vehicles

- 5.3.1.3 Easy application and low cost of adhesives compared to traditional fastening systems

- 5.3.1.4 Increasing use of pressure-sensitive adhesives in tapes and labels

- 5.3.2 RESTRAINTS

- 5.3.2.1 Volatility in raw material prices

- 5.3.3 OPPORTUNITIES

- 5.3.3.1 Potential substitutes to traditional fastening systems

- 5.3.3.2 Emergence of bio-based pressure-sensitive adhesives

- 5.3.4 CHALLENGES

- 5.3.4.1 Stringent regulations reshaping market

- 5.3.4.2 Substitution by mechanical fasteners

- 5.4 PORTER'S FIVE FORCES ANALYSIS

- TABLE 6 PRESSURE-SENSITIVE ADHESIVES MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 25 PORTER'S FIVE FORCES ANALYSIS: PRESSURE-SENSITIVE ADHESIVES MARKET

- 5.4.1 THREAT FROM NEW ENTRANTS

- 5.4.2 THREAT OF SUBSTITUTES

- 5.4.3 BARGAINING POWER OF BUYERS

- 5.4.4 BARGAINING POWER OF SUPPLIERS

- 5.4.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.5 MACROECONOMIC INDICATORS

- 5.5.1 INTRODUCTION

- 5.5.2 GDP TRENDS AND FORECAST

- TABLE 7 GDP TRENDS AND FORECAST, PERCENTAGE CHANGE (2021-2029)

- 5.5.3 TRENDS IN GLOBAL CONSTRUCTION INDUSTRY

- 5.5.4 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

- TABLE 8 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

- 5.6 VALUE CHAIN ANALYSIS

- FIGURE 26 PRESSURE-SENSITIVE ADHESIVES MARKET: VALUE CHAIN ANALYSIS

- 5.7 PRICING ANALYSIS

- 5.7.1 AVERAGE SELLING PRICE TREND, BY REGION

- FIGURE 27 AVERAGE SELLING PRICE TREND OF PRESSURE-SENSITIVE ADHESIVES, BY REGION, 2022-2023

- TABLE 9 AVERAGE SELLING PRICE OF PRESSURE-SENSITIVE ADHESIVES, BY REGION, 2022-2023 (USD/KG)

- 5.7.2 AVERAGE SELLING PRICE TREND, BY CHEMISTRY

- FIGURE 28 AVERAGE SELLING PRICE TREND OF PRESSURE-SENSITIVE ADHESIVES, BY CHEMISTRY (2023)

- 5.7.3 AVERAGE SELLING PRICE TREND, BY TECHNOLOGY

- FIGURE 29 AVERAGE SELLING PRICE TREND OF PRESSURE-SENSITIVE ADHESIVES, BY TECHNOLOGY (2023)

- 5.7.4 AVERAGE SELLING PRICE TREND, BY APPLICATION

- FIGURE 30 AVERAGE SELLING PRICE TREND OF PRESSURE-SENSITIVE ADHESIVES, BY APPLICATION (2023)

- 5.7.5 AVERAGE SELLING PRICE TREND, BY END-USE INDUSTRY

- FIGURE 31 AVERAGE SELLING PRICE TREND OF PRESSURE-SENSITIVE ADHESIVES, BY END-USE INDUSTRY (2023)

- 5.7.6 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY APPLICATION

- FIGURE 32 AVERAGE SELLING PRICE TREND OF KEY PLAYERS FOR TOP 3 APPLICATIONS

- TABLE 10 AVERAGE SELLING PRICE TREND OF KEY PLAYERS FOR TOP 3 APPLICATIONS, 2023 (USD/KG)

- 5.8 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.8.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 33 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 APPLICATIONS

- TABLE 11 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 APPLICATIONS (%)

- 5.8.2 BUYING CRITERIA

- FIGURE 34 KEY BUYING CRITERIA FOR PRESSURE-SENSITIVE ADHESIVES

- TABLE 12 KEY BUYING CRITERIA FOR PRESSURE-SENSITIVE ADHESIVES

- 5.9 TRADE ANALYSIS

- 5.9.1 EXPORT SCENARIO

- FIGURE 35 REGION-WISE EXPORT DATA, 2019-2023 (USD THOUSAND)

- TABLE 13 COUNTRY-WISE EXPORT DATA, 2021-2023 (USD THOUSAND)

- 5.9.2 IMPORT SCENARIO

- FIGURE 36 REGION-WISE IMPORT DATA, 2019-2023 (USD THOUSAND)

- TABLE 14 COUNTRY-WISE IMPORT DATA, 2021-2023 (USD THOUSAND)

- 5.10 REGULATORY LANDSCAPE AND STANDARDS

- 5.10.1 REGULATIONS IMPACTING PRESSURE-SENSITIVE ADHESIVE BUSINESS

- 5.10.1.1 Control of Substances Hazardous to Health (COSHH) Regulations 2002 (UK)

- 5.10.1.2 Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH) (EU)

- 5.10.1.3 Globally Harmonized System of Classification and Labeling of Chemicals (GHS)

- 5.10.1.4 Environmental Protection Agency (EPA) Regulations (USA)

- 5.10.1.5 Occupational Safety and Health Administration (OSHA) Standards (USA)

- 5.10.1.6 California Air Resources Board (CARB) Regulations

- 5.10.1.7 Food and Drug Administration (FDA) Compliance (USA)

- 5.10.1.8 Strategic Implications

- 5.10.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.10.1 REGULATIONS IMPACTING PRESSURE-SENSITIVE ADHESIVE BUSINESS

- 5.11 ECOSYSTEM ANALYSIS

- TABLE 18 PRESSURE-SENSITIVE ADHESIVES MARKET: ROLE IN ECOSYSTEM

- FIGURE 37 PRESSURE-SENSITIVE ADHESIVES MARKET: ECOSYSTEM MAP

- FIGURE 38 PRESSURE-SENSITIVE ADHESIVES MARKET: ECOSYSTEM

- 5.12 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 39 TRENDS IN END-USE INDUSTRIES IMPACTING BUSINESS OF PRESSURE-SENSITIVE ADHESIVE MANUFACTURERS

- 5.13 INVESTMENT AND FUNDING SCENARIO

- TABLE 19 INVESTMENT AND FUNDING SCENARIO

- 5.14 PATENT ANALYSIS

- 5.14.1 METHODOLOGY

- 5.14.2 PUBLICATION TRENDS

- FIGURE 40 PUBLISHED PATENTS, 2019-2024

- 5.14.3 JURISDICTION ANALYSIS

- FIGURE 41 PATENTS PUBLISHED BY JURISDICTION, 2019-2024

- 5.14.4 TOP APPLICANTS

- FIGURE 42 PATENTS PUBLISHED BY MAJOR APPLICANTS, 2019-2024

- TABLE 20 TOP PATENT OWNERS

- FIGURE 43 TOP PATENT APPLICANTS FOR PRESSURE-SENSITIVE ADHESIVES

- 5.15 TECHNOLOGY ANALYSIS

- 5.15.1 KEY TECHNOLOGY

- 5.15.1.1 Emulsion or water-based

- 5.15.1.2 Solvent-based

- 5.15.1.3 Hot-melt

- 5.15.2 COMPLIMENTARY TECHNOLOGY

- 5.15.2.1 Radiation

- 5.15.3 ADJACENT TECHNOLOGY

- 5.15.3.1 Tetra-glycidyl-m-xylenediamine

- 5.15.1 KEY TECHNOLOGY

- 5.16 GLOBAL ECONOMIC SCENARIO AFFECTING MARKET GROWTH

- 5.16.1 RUSSIA-UKRAINE WAR

- 5.16.2 CHINA

- 5.16.2.1 Decreasing FDI cooling China's growth trajectory

- 5.16.2.2 Environmental commitments

- 5.16.3 EUROPE

- 5.16.3.1 Energy crisis in Europe

- 5.16.4 THREATS IN GLOBAL TRADE

- 5.16.5 OUTLOOK FOR CHEMICAL INDUSTRY

- 5.17 CASE STUDY ANALYSIS

- 5.17.1 CASE STUDY 1

- 5.17.2 CASE STUDY 2

- 5.17.3 CASE STUDY 3

- 5.18 KEY CONFERENCES AND EVENTS IN 2024-2025

- TABLE 21 PRESSURE-SENSITIVE ADHESIVES MARKET: KEY CONFERENCES AND EVENTS, 2024-2025

6 PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY

- 6.1 INTRODUCTION

- FIGURE 44 ACRYLIC TO ACCOUNT FOR LARGEST SHARE DURING FORECAST PERIOD

- TABLE 22 PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 23 PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 24 PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 25 PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 6.1.1 ACRYLIC PSA

- 6.1.1.1 Surge in automobile demand to drive market

- TABLE 26 ACRYLIC PSA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 27 ACRYLIC PSA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 28 ACRYLIC PSA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 29 ACRYLIC PSA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

- 6.1.2 RUBBER PSA

- 6.1.2.1 Wide use in industrial and domestic applications to boost market

- TABLE 30 RUBBER PSA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 31 RUBBER PSA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 32 RUBBER PSA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 33 RUBBER PSA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

- 6.1.3 SILICONE

- 6.1.3.1 Increasing demand from consumer goods industry to boost market

- TABLE 34 SILICONE PSA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 35 SILICONE PSA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 36 SILICONE PSA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 37 SILICONE PSA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

- 6.1.4 OTHER CHEMISTRIES

- 6.1.4.1 Eva PSA

- 6.1.4.2 Polyurethane PSA

- 6.1.4.3 Hybrid PSA

- 6.1.4.4 Hydrophilic PSA

- TABLE 38 OTHER CHEMISTRIES: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 39 OTHER CHEMISTRIES: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 40 OTHER CHEMISTRIES: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 41 OTHER CHEMISTRIES: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

7 PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY

- 7.1 INTRODUCTION

- FIGURE 45 WATER-BASED SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- TABLE 42 PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2021-2023 (USD MILLION)

- TABLE 43 PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 44 PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2021-2023 (KILOTON)

- TABLE 45 PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2024-2029 (KILOTON)

- 7.2 WATER-BASED

- 7.2.1 GROWTH OF AUTOMOBILE INDUSTRY TO BOOST MARKET

- TABLE 46 WATER-BASED: PRESSURE-SENSITIVE ADHESIVE MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 47 WATER-BASED: PRESSURE-SENSITIVE ADHESIVE MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 48 WATER-BASED: PRESSURE-SENSITIVE ADHESIVE MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 49 WATER-BASED: PRESSURE-SENSITIVE ADHESIVE MARKET, BY REGION, 2024-2029 (KILOTON)

- 7.3 SOLVENT-BASED

- 7.3.1 PRESSING NEED IN GASKETS AND MOUNTING APPLICATIONS TO DRIVE MARKET

- TABLE 50 SOLVENT-BASED: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 51 SOLVENT -BASED: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 52 SOLVENT -BASED: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 53 SOLVENT -BASED: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

- 7.4 HOT-MELT

- 7.4.1 INCREASING DEMAND IN PAPER AND PACKAGING INDUSTRIES TO BOOST MARKET

- TABLE 54 HOT-MELT: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 55 HOT-MELT: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 56 HOT-MELT: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 57 HOT-MELT: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

- 7.5 RADIATION

- 7.5.1 HIGH DEMAND FROM AUTOMOTIVE AND MEDICAL SECTORS TO DRIVE MARKET

- TABLE 58 RADIATION: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 59 RADIATION: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 60 RADIATION: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 61 RADIATION: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

8 PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- FIGURE 46 TAPES SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- TABLE 62 PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2021-2023 (USD MILLION)

- TABLE 63 PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 64 PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2021-2023 (KILOTON)

- TABLE 65 PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2024-2029 (KILOTON)

- 8.2 TAPES

- 8.2.1 EXTENSIVE DEMAND IN MEDICAL & AUTOMOTIVE INDUSTRY TO BOOST MARKET

- 8.2.2 BY TYPE

- 8.2.2.1 Specialty tapes

- 8.2.2.2 Commodity PSA tapes

- 8.2.2.2.1 Masking tapes

- 8.2.2.2.2 Packaging tapes

- 8.2.2.2.3 Consumer and office tapes

- 8.2.3 BY COATING

- 8.2.3.1 Single-coated PSA tapes

- 8.2.3.2 Double-coated PSA tapes

- 8.2.3.3 Reinforced PSA tapes

- 8.2.3.4 Unsupported PSA tapes

- TABLE 66 TAPES: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 67 TAPES: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 68 TAPES: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 69 TAPES: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

- 8.3 LABELS

- 8.3.1 SURGING DEMAND IN PACKAGING SECTOR TO DRIVE MARKET

- 8.3.2 PERMANENT LABELS

- 8.3.3 PEELABLE LABELS

- 8.3.4 ULTRA-PEELABLE LABELS

- 8.3.5 FREEZER OR FROST FIX LABELS

- 8.3.6 HIGH TACK LABELS

- 8.3.7 SPECIALTY LABELS

- TABLE 70 LABELS: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 71 LABELS: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 72 LABELS: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 73 LABELS: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

- 8.4 GRAPHICS

- 8.4.1 PRESSING NEED IN BUILDING & CONSTRUCTION SECTOR TO DRIVE MARKET

- 8.4.2 SIGNAGE

- 8.4.3 VEHICLE WRAPS

- 8.4.4 EMBLEMS AND LOGOS

- 8.4.5 FLOORS, CARPETS, AND MATS

- 8.4.6 FILMS

- TABLE 74 GRAPHICS: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 75 GRAPHICS: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 76 GRAPHICS: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 77 GRAPHICS: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

- 8.5 OTHER APPLICATIONS

- TABLE 78 OTHER APPLICATIONS: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 79 OTHER APPLICATIONS: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 80 OTHER APPLICATIONS: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 81 OTHER APPLICATIONS: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

9 PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY

- 9.1 INTRODUCTION

- FIGURE 47 PACKAGING SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- TABLE 82 PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 83 PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 84 PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 85 PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 9.2 PACKAGING

- 9.2.1 INCREASING DEMAND IN GRAPHIC FILMS TO DRIVE MARKET

- TABLE 86 PACKAGING: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 87 PACKAGING: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 88 PACKAGING: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 89 PACKAGING: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

- 9.3 ELECTRICAL, ELECTRONICS, AND TELECOMMUNICATION

- 9.3.1 WIDE USE OF PSA TAPES IN ELECTRICAL ASSEMBLY TO BOOST MARKET

- TABLE 90 ELECTRICAL, ELECTRONICS, AND TELECOMMUNICATION: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 91 ELECTRICAL, ELECTRONICS, AND TELECOMMUNICATION: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 92 ELECTRICAL, ELECTRONICS, AND TELECOMMUNICATION: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 93 ELECTRICAL, ELECTRONICS, AND TELECOMMUNICATION: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

- 9.4 AUTOMOTIVE & TRANSPORTATION

- 9.4.1 INVESTMENTS IN TRANSPORTATION INFRASTRUCTURE TO DRIVE GROWTH

- TABLE 94 AUTOMOTIVE & TRANSPORTATION: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 95 AUTOMOTIVE & TRANSPORTATION: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 96 AUTOMOTIVE & TRANSPORTATION: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 97 AUTOMOTIVE & TRANSPORTATION: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

- 9.5 BUILDING & CONSTRUCTION

- 9.5.1 RISING DEMAND FOR WATER-BASED AND HOT-MELT ADHESIVES TO DRIVE MARKET

- TABLE 98 BUILDING & CONSTRUCTION: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 99 BUILDING & CONSTRUCTION: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 100 BUILDING & CONSTRUCTION: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 101 BUILDING & CONSTRUCTION: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

- 9.6 MEDICAL & HEALTHCARE

- 9.6.1 INCREASING DEMAND FOR PSA TRANSFER TAPES TO DRIVE MARKET

- TABLE 102 MEDICAL & HEALTHCARE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 103 MEDICAL & HEALTHCARE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 104 MEDICAL & HEALTHCARE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 105 MEDICAL & HEALTHCARE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

- 9.7 OTHER END-USE INDUSTRIES

- TABLE 106 OTHER END-USE INDUSTRIES: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 107 OTHER END-USE INDUSTRIES: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 108 OTHER END-USE INDUSTRIES: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 109 OTHER END-USE INDUSTRIES: PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

10 PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION

- 10.1 INTRODUCTION

- TABLE 110 PRESSURE-SENSITIVE ADHESIVES MARKET: GLOBAL CONSTRUCTION OUTLOOK

- FIGURE 48 SHARE OF BUILDINGS IN TOTAL FINAL ENERGY CONSUMPTION IN 2022

- FIGURE 49 SHARE OF BUILDINGS IN GLOBAL ENERGY AND PROCESS EMISSIONS IN 2022

- FIGURE 50 ASIA PACIFIC TO REGISTER HIGHEST CAGR FOR PRESSURE-SENSITIVE ADHESIVES BETWEEN 2024 AND 2029

- TABLE 111 PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 112 PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 113 PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 114 PRESSURE-SENSITIVE ADHESIVES MARKET, BY REGION, 2024-2029 (KILOTON)

- 10.2 NORTH AMERICA

- 10.2.1 RECESSION IMPACT

- FIGURE 51 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET SNAPSHOT

- TABLE 115 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 116 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 117 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2021-2023 (KILOTON)

- TABLE 118 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 119 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 120 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 121 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 122 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- TABLE 123 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2021-2023 (USD MILLION)

- TABLE 124 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 125 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2021-2023 (KILOTON)

- TABLE 126 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2024-2029 (KILOTON)

- TABLE 127 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2021-2023 (USD MILLION)

- TABLE 128 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 129 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2021-2023 (KILOTON)

- TABLE 130 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2024-2029 (KILOTON)

- TABLE 131 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 132 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 133 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 134 NORTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 10.2.2 US

- 10.2.2.1 Presence of major manufacturers to drive market

- TABLE 135 US: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 136 US: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 137 US: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 138 US: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.2.3 CANADA

- 10.2.3.1 Growth of automotive sector to drive market

- TABLE 139 CANADA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 140 CANADA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 141 CANADA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 142 CANADA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 10.2.4 MEXICO

- 10.2.4.1 Changing monetary and fiscal policies to drive market

- TABLE 143 MEXICO: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 144 MEXICO: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 145 MEXICO: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 146 MEXICO: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.3 EUROPE

- 10.3.1 RECESSION IMPACT

- FIGURE 52 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET SNAPSHOT

- TABLE 147 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 148 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 149 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2021-2023 (KILOTON)

- TABLE 150 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 151 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 152 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 153 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 154 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- TABLE 155 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2021-2023 (USD MILLION)

- TABLE 156 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 157 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2021-2023 (KILOTON)

- TABLE 158 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2024-2029 (KILOTON)

- TABLE 159 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2021-2023 (USD MILLION)

- TABLE 160 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 161 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2021-2023 (KILOTON)

- TABLE 162 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2024-2029 (KILOTON)

- TABLE 163 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 164 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 165 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 166 EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 10.3.2 GERMANY

- 10.3.2.1 Infrastructure enhancement and high demand for commercial projects to boost market

- TABLE 167 GERMANY: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 168 GERMANY: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 169 GERMANY: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 170 GERMANY: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.3.3 UK

- 10.3.3.1 Rising demand from healthcare industry to fuel market

- TABLE 171 UK: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 172 UK: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 173 UK: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 174 UK: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.3.4 FRANCE

- 10.3.4.1 Infrastructure development for Olympic games to fuel demand for adhesives

- TABLE 175 FRANCE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 176 FRANCE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 177 FRANCE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 178 FRANCE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.3.5 ITALY

- 10.3.5.1 Growth of multifarious industries to drive market

- TABLE 179 ITALY: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 180 ITALY: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 181 ITALY: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 182 ITALY: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.3.6 SPAIN

- 10.3.6.1 Surge in foreign institutional investments to propel market

- TABLE 183 SPAIN: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 184 SPAIN: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 185 SPAIN: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 186 SPAIN: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.3.7 REST OF EUROPE

- TABLE 187 REST OF EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 188 REST OF EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 189 REST OF EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 190 REST OF EUROPE: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.4 ASIA PACIFIC

- 10.4.1 RECESSION IMPACT

- FIGURE 53 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET SNAPSHOT

- TABLE 191 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 192 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 193 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2021-2023 (KILOTON)

- TABLE 194 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 195 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 196 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 197 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 198 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- TABLE 199 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2021-2023 (USD MILLION)

- TABLE 200 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 201 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2021-2023 (KILOTON)

- TABLE 202 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2024-2029 (KILOTON)

- TABLE 203 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2021-2023 (USD MILLION)

- TABLE 204 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 205 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2021-2023 (KILOTON)

- TABLE 206 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2024-2029 (KILOTON)

- TABLE 207 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 208 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 209 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 210 ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 10.4.2 CHINA

- 10.4.2.1 High investments in real estate and non-residential construction to boost market

- TABLE 211 CHINA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 212 CHINA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 213 CHINA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 214 CHINA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.4.3 INDIA

- 10.4.3.1 Growth of packaging and automotive industries to drive market

- TABLE 215 INDIA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 216 INDIA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 217 INDIA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 218 INDIA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.4.4 JAPAN

- 10.4.4.1 Increasing automobile production to drive market

- TABLE 219 JAPAN: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 220 JAPAN: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 221 JAPAN: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 222 JAPAN: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.4.5 SOUTH KOREA

- 10.4.5.1 Rising construction activities to boost demand for adhesives

- TABLE 223 SOUTH KOREA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 224 SOUTH KOREA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 225 SOUTH KOREA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 226 SOUTH KOREA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.4.6 REST OF ASIA PACIFIC

- TABLE 227 REST OF ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 228 REST OF ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 229 REST OF ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 230 REST OF ASIA PACIFIC: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.5 SOUTH AMERICA

- 10.5.1 RECESSION IMPACT

- FIGURE 54 BRAZIL TO REGISTER HIGHEST CAGR BETWEEN 2024 AND 2029

- TABLE 231 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 232 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 233 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2021-2023 (KILOTON)

- TABLE 234 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 235 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 236 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 237 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 238 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- TABLE 239 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2021-2023 (USD MILLION)

- TABLE 240 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 241 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2021-2023 (KILOTON)

- TABLE 242 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2024-2029 (KILOTON)

- TABLE 243 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2021-2023 (USD MILLION)

- TABLE 244 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 245 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2021-2023 (KILOTON)

- TABLE 246 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2024-2029 (KILOTON)

- TABLE 247 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 248 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 249 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 250 SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 10.5.2 BRAZIL

- 10.5.2.1 Easy availability of raw materials to propel market growth

- TABLE 251 BRAZIL: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 252 BRAZIL: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 253 BRAZIL: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 254 BRAZIL: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.5.3 ARGENTINA

- 10.5.3.1 Increase in population and improved economic conditions to drive demand

- TABLE 255 ARGENTINA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 256 ARGENTINA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 257 ARGENTINA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 258 ARGENTINA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.5.4 REST OF THE SOUTH AMERICA

- TABLE 259 REST OF SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 260 REST OF SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 261 REST OF SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 262 REST OF SOUTH AMERICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.6 MIDDLE EAST & AFRICA

- 10.6.1 RECESSION IMPACT

- FIGURE 55 GCC COUNTRIES TO REGISTER HIGHEST CAGR BETWEEN 2024 AND 2029

- TABLE 263 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 264 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 265 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2021-2023 (KILOTON)

- TABLE 266 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 267 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 268 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 269 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 270 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- TABLE 271 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2021-2023 (USD MILLION)

- TABLE 272 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 273 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2021-2023 (KILOTON)

- TABLE 274 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY TECHNOLOGY, 2024-2029 (KILOTON)

- TABLE 275 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2021-2023 (USD MILLION)

- TABLE 276 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 277 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2021-2023 (KILOTON)

- TABLE 278 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY APPLICATION, 2024-2029 (KILOTON)

- TABLE 279 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 280 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 281 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 282 MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- 10.6.2 GCC COUNTRIES

- 10.6.2.1 Saudi Arabia

- 10.6.2.1.1 Increased investments in multifarious sectors to propel demand

- 10.6.2.2 UAE

- 10.6.2.2.1 Growing industrial activities to drive market

- 10.6.2.3 Rest of GCC countries

- 10.6.2.1 Saudi Arabia

- TABLE 283 GCC COUNTRIES: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 284 GCC COUNTRIES: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 285 GCC COUNTRIES: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 286 GCC COUNTRIES: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.6.3 SOUTH AFRICA

- 10.6.3.1 Surge in production of new vehicles to drive market

- TABLE 287 SOUTH AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 288 SOUTH AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 289 SOUTH AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 290 SOUTH AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

- 10.6.4 REST OF MIDDLE EAST & AFRICA

- TABLE 291 REST OF MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (USD MILLION)

- TABLE 292 REST OF MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (USD MILLION)

- TABLE 293 REST OF MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2021-2023 (KILOTON)

- TABLE 294 REST OF MIDDLE EAST & AFRICA: PRESSURE-SENSITIVE ADHESIVES MARKET, BY CHEMISTRY, 2024-2029 (KILOTON)

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES

- TABLE 295 OVERVIEW OF STRATEGIES ADOPTED BY KEY MARKET PLAYERS (JANUARY 2019-MAY 2024)

- 11.3 MARKET SHARE ANALYSIS

- FIGURE 56 MARKET SHARE ANALYSIS, 2023

- TABLE 296 PRESSURE-SENSITIVE ADHESIVES MARKET: DEGREE OF COMPETITION

- 11.3.1 MARKET RANKING ANALYSIS

- FIGURE 57 MARKET RANKING ANALYSIS, 2023

- 11.4 REVENUE ANALYSIS TOP 5 PLAYERS

- FIGURE 58 MARKET REVENUE ANALYSIS OF TOP FIVE PLAYERS

- 11.5 COMPANY VALUATION AND FINANCIAL METRICS, 2023

- 11.5.1 COMPANY VALUATION

- FIGURE 59 PRESSURE-SENSITIVE ADHESIVES MARKET: COMPANY VALUATION

- 11.5.2 FINANCIAL METRICS

- FIGURE 60 PRESSURE-SENSITIVE ADHESIVES MARKET: FINANCIAL METRICS

- 11.6 BRAND/PRODUCT COMPARATIVE ANALYSIS

- FIGURE 61 PRESSURE-SENSITIVE ADHESIVES MARKET: BRAND/PRODUCT COMPARATIVE ANALYSIS

- 11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- FIGURE 62 PRESSURE-SENSITIVE ADHESIVES MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

- 11.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023

- FIGURE 63 PRESSURE-SENSITIVE ADHESIVES MARKET: COMPANY FOOTPRINT (25 COMPANIES)

- TABLE 297 PRESSURE-SENSITIVE ADHESIVES MARKET: REGION FOOTPRINT (25 COMPANIES)

- TABLE 298 PRESSURE-SENSITIVE ADHESIVES MARKET: END-USE INDUSTRY FOOTPRINT (25 COMPANIES)

- TABLE 299 PRESSURE-SENSITIVE ADHESIVES MARKET: TECHNOLOGY FOOTPRINT (25 COMPANIES)

- TABLE 300 PRESSURE-SENSITIVE ADHESIVES MARKET: APPLICATION FOOTPRINT (25 COMPANIES)

- TABLE 301 PRESSURE-SENSITIVE ADHESIVES MARKET: CHEMISTRY FOOTPRINT (25 COMPANIES)

- 11.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 11.8.1 PROGRESSIVE COMPANIES

- 11.8.2 RESPONSIVE COMPANIES

- 11.8.3 DYNAMIC COMPANIES

- 11.8.4 STARTING BLOCKS

- FIGURE 64 PRESSURE-SENSITIVE ADHESIVES MARKET: STARTUP/SME EVALUATION MATRIX, 2023

- 11.8.5 COMPETITIVE BENCHMARKING

- 11.8.5.1 Detailed list of key startups/SMES

- TABLE 302 PRESSURE-SENSITIVE ADHESIVES MARKET: KEY STARTUPS/SMES

- 11.8.5.2 Competitive benchmarking of key startups/SMES

- TABLE 303 PRESSURE-SENSITIVE ADHESIVES MARKET: COMPETITIVE BENCHMARKING OF KEY PLAYERS [STARTUPS/SMES]

- 11.9 COMPETITIVE SCENARIO AND TRENDS

- 11.9.1 PRODUCT LAUNCHES

- TABLE 304 PRESSURE-SENSITIVE ADHESIVES MARKET: PRODUCT LAUNCHES, JANUARY 2019- MAY 2024

- 11.9.2 DEALS

- TABLE 305 PRESSURE-SENSITIVE ADHESIVES MARKET: DEALS, JANUARY 2019- MAY 2024

- 11.9.3 EXPANSIONS

- TABLE 306 PRESSURE-SENSITIVE ADHESIVES MARKET: EXPANSIONS, JANUARY 2019- MAY 2024

12 COMPANY PROFILES

- (Business overview, Products/Solutions/Services offered, Recent Developments, MnM view, Right to win, Strategic choices, Weaknesses and competitive threats) **

- 12.1 KEY PLAYERS

- 12.1.1 HENKEL AG & CO., KGAA

- TABLE 307 HENKEL AG & CO., KGAA: COMPANY OVERVIEW

- FIGURE 65 HENKEL AG & CO., KGAA.: COMPANY SNAPSHOT

- TABLE 308 HENKEL AG & CO., KGAA.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 309 HENKEL AG & CO., KGAA: PRODUCT LAUNCHES

- TABLE 310 HENKEL AG & CO., KGAA: EXPANSION

- 12.1.2 DOW

- TABLE 311 DOW: COMPANY OVERVIEW

- FIGURE 66 DOW: COMPANY SNAPSHOT

- TABLE 312 DOW: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 313 DOW: EXPANSION

- 12.1.3 AVERY DENNISON CORPORATION

- TABLE 314 AVERY DENNISON CORPORATION: COMPANY OVERVIEW

- FIGURE 67 AVERY DENNISON CORPORATION: COMPANY SNAPSHOT

- TABLE 315 AVERY DENNISON CORPORATION: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

- TABLE 316 AVERY DENNISON CORPORATION: PRODUCT LAUNCHES

- TABLE 317 AVERY DENNISON CORPORATION: DEALS

- TABLE 318 AVERY DENNISON CORPORATION: EXPANSION

- 12.1.4 H.B. FULLER COMPANY

- TABLE 319 H.B. FULLER COMPANY: BUSINESS OVERVIEW

- FIGURE 68 H.B. FULLER COMPANY: COMPANY SNAPSHOT

- TABLE 320 H.B. FULLER COMPANY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 321 H.B. FULLER COMPANY: PRODUCT LAUNCHES

- TABLE 322 H.B. FULLER COMPANY: DEALS

- TABLE 323 H.B. FULLER COMPANY: EXPANSION

- 12.1.5 3M

- TABLE 324 3M: COMPANY OVERVIEW

- FIGURE 69 3M: COMPANY SNAPSHOT

- TABLE 325 3M: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 326 3M: EXPANSION

- 12.1.6 ARKEMA SA

- TABLE 327 ARKEMA SA: COMPANY OVERVIEW

- FIGURE 70 ARKEMA SA: COMPANY SNAPSHOT

- TABLE 328 ARKEMA S.A.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 329 ARKEMA S.A.: PRODUCT LAUNCHES

- TABLE 330 ARKEMA S.A.: DEALS

- 12.1.7 SIKA AG

- TABLE 331 SIKA AG: COMPANY OVERVIEW

- FIGURE 71 SIKA AG: COMPANY SNAPSHOT

- TABLE 332 SIKA AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.8 SCAPA GROUP PLC

- TABLE 333 SCAPA GROUP PLC: COMPANY OVERVIEW

- TABLE 334 SCAPA GROUP PLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.9 WACKER CHEMIE AG

- TABLE 335 WACKER CHEMIE AG: COMPANY OVERVIEW

- FIGURE 72 WACKER CHEMIC AG: COMPANY SNAPSHOT

- TABLE 336 WACKER CHEMIE AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 337 WACKER CHEMIE AG: PRODUCT LAUNCHES

- TABLE 338 WACKER CHEMIC AG: DEALS

- 12.1.10 ILLINOIS TOOL WORKS INC.

- TABLE 339 ILLINOIS TOOL WORKS INC.: COMPANY OVERVIEW

- FIGURE 73 ILLINOIS TOOL WORKS INC.: COMPANY SNAPSHOT

- TABLE 340 ILLINOIS TOOL WORKS INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.2 OTHER PLAYERS

- 12.2.1 TOYO INK AMERICA, LLC

- TABLE 341 TOYO INK AMERICA, LLC: COMPANY OVERVIEW

- TABLE 342 TOYO INK AMERICA, LLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.2.2 PIDILITE INDUSTRIES

- TABLE 343 PIDILITE INDUSTRIES: COMPANY OVERVIEW

- TABLE 344 PIDILITE INDUSTRIES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.2.3 HELMITIN ADHESIVES

- TABLE 345 HELMITIN ADHESIVES: COMPANY OVERVIEW

- TABLE 346 HELMITIN ADHESIVES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.2.4 JOWAT SE

- TABLE 347 JOWAT SE: COMPANY OVERVIEW

- TABLE 348 JOWAT SE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.2.5 MAPEI S.P.A.

- TABLE 349 MAPEI S.P.A.: COMPANY OVERVIEW

- TABLE 350 MAPEI S.P.A.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.2.6 FRANKLIN ADHESIVES & POLYMERS

- TABLE 351 FRANKLIN ADHESIVES & POLYMERS: COMPANY OVERVIEW

- TABLE 352 FRANKLIN ADHESIVES & POLYMERS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.2.7 DRYTAC CORPORATION

- TABLE 353 DRYTAC CORPORATION: COMPANY OVERVIEW

- TABLE 354 DRYTAC CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.2.8 JESONS

- TABLE 355 JESONS: COMPANY OVERVIEW

- TABLE 356 JESONS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.2.9 ADHESIVES RESEARCH INC.

- TABLE 357 ADHESIVES RESEARCH INC.: COMPANY OVERVIEW

- TABLE 358 ADHESIVES RESEARCH INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.2.10 SHANGHAI JAOUR ADHESIVE PRODUCTS CO., LTD.

- TABLE 359 SHANGHAI JAOUR ADHESIVE PRODUCTS CO., LTD.: COMPANY OVERVIEW

- TABLE 360 SHANGHAI JAOUR ADHESIVE PRODUCTS CO., LTD.: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

- 12.2.11 ESTER CHEMICAL INDUSTRIES PVT. LTD.

- TABLE 361 ESTER CHEMICAL INDUSTRIES PVT. LTD.: COMPANY OVERVIEW

- TABLE 362 ESTER CHEMICAL INDUSTRIES PVT. LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.2.12 DYNA-TECH ADHESIVES, INC.

- TABLE 363 DYNA-TECH ADHESIVES, INC.: COMPANY OVERVIEW

- TABLE 364 DYNA-TECH ADHESIVES, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.2.13 CATTIE ADHESIVES

- TABLE 365 CATTIE ADHESIVES: COMPANY OVERVIEW

- TABLE 366 CATTIE ADHESIVES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.2.14 ADVANCE POLYMER PRODUCTS

- TABLE 367 ADVANCE POLYMER PRODUCTS: COMPANY OVERVIEW

- TABLE 368 ADVANCE POLYMER PRODUCTS: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

- 12.2.15 NANPAO RESINS CHEMICAL GROUP

- TABLE 369 NANPAO RESINS CHEMICAL GROUP: COMPANY OVERVIEW

- TABLE 370 NANPAO RESINS CHEMICAL GROUP: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

- *Details on Business overview, Products/Solutions/Services offered, Recent Developments, MnM view, Right to win, Strategic choices, Weaknesses and competitive threats might not be captured in case of unlisted companies.

13 ADJACENT & RELATED MARKETS

- 13.1 INTRODUCTION

- 13.2 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET

- 13.2.1 MARKET DEFINITION

- 13.2.2 PRESSURE-SENSITIVE ADHESIVES: MARKET OVERVIEW

- TABLE 371 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY TYPE 2020-2022 (USD MILLION)

- TABLE 372 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY TYPE, 2023-2030 (USD MILLION)

- TABLE 373 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY TYPE, 2020-2022 (MILLION SQUARE METER)

- TABLE 374 PRESSURE-SENSITIVE ADHESIVE TAPES MARKET, BY TYPE, 2023-2030 (MILLION SQUARE METER)

- 13.2.3 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY ADHESIVE TYPE

- TABLE 375 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY ADHESIVE TYPE, 2020-2022 (USD MILLION)

- TABLE 376 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY ADHESIVE TYPE, 2023-2030 (USD MILLION)

- TABLE 377 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY ADHESIVE TYPE, 2020-2022 (MILLION SQUARE METER)

- TABLE 378 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY ADHESIVE TYPE, 2023-2030 (MILLION SQUARE METER)

- 13.2.4 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY TECHNOLOGY

- TABLE 379 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY TECHNOLOGY, 2020-2022 (USD MILLION)

- TABLE 380 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY TECHNOLOGY, 2023-2030 (USD MILLION)

- TABLE 381 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY TECHNOLOGY, 2020-2022 (MILLION SQUARE METER)

- TABLE 382 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY TECHNOLOGY, 2023-2030 (MILLION SQUARE METER)

- 13.2.5 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY BACKING AND CARRIER MATERIAL

- TABLE 383 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY BACKING OR CARRIER MATERIAL, 2020-2022 (USD MILLION)

- TABLE 384 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY BACKING OR CARRIER MATERIAL, 2023-2030 (USD MILLION)

- TABLE 385 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY BACKING OR CARRIER MATERIAL, 2020-2022 (MILLION SQUARE METER)

- TABLE 386 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY BACKING OR CARRIER MATERIAL, 2023-2030 (MILLION SQUARE METER)

- 13.2.6 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY END-USE INDUSTRY

- TABLE 387 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY END-USE INDUSTRY, 2020-2022 (USD MILLION)

- TABLE 388 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY END-USE INDUSTRY, 2023-2030 (USD MILLION)

- TABLE 389 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY END-USE INDUSTRY, 2020-2022 (MILLION SQUARE METER)

- TABLE 390 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY END-USE INDUSTRY, 2023-2030 (MILLION SQUARE METER)

- 13.2.7 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY REGION

- TABLE 391 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 392 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 393 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY REGION, 2020-2022 (MILLION SQUARE METER)

- TABLE 394 PRESSURE-SENSITIVE ADHESIVES TAPES MARKET, BY REGION, 2020-2022 (MILLION SQUARE METER)

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS