産業用ロボット市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Industrial Robotics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1716480

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

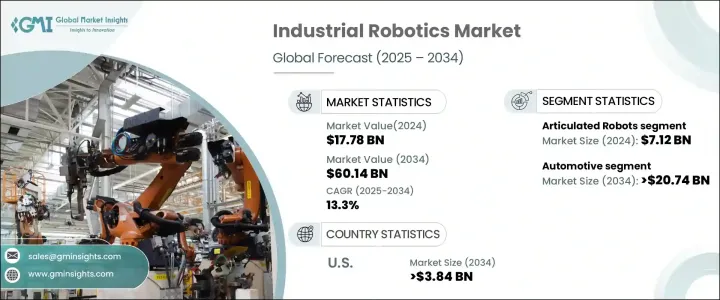

世界の産業用ロボット市場は、2024年に177億8,000万米ドルに達し、2025年から2034年にかけてCAGR 13.3%で成長すると予測されています。

この急拡大の背景には、企業が生産性の向上を図り、労働力不足や人件費の上昇といった課題に対処するために、さまざまな分野で自動化に対する需要が高まっていることがあります。自動化は特に製造業のような産業で支持を集めており、そこではロボットシステムが業務の合理化、経費削減、製品品質の向上に利用されています。特にeコマースの台頭により、ロジスティクスにおける自動化の利用が増加していることも、ロボット需要の急増に寄与しています。企業は現在、倉庫での在庫の仕分けや管理に自動化システムをより多く利用し、効率を高めています。企業がオペレーションの強化に注力する中、ロボット技術の導入はこれまで以上に急速に進むと思われます。

ロボットによる自動化へのシフトに影響を与える主な要因の1つは、熟練労働者の不足と運用コストの上昇です。米国、日本、ドイツなど高齢化が進む新興諸国は、特にこの課題に直面しています。さらに、中国やインドのような開発途上国では賃金が上昇しており、企業はロボット工学のような費用対効果の高い代替手段を模索する必要があります。こうした要因から、産業界は競争力を維持し収益性を維持するために、ロボット・ソリューションの導入を急ピッチで進めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 177億8,000万米ドル |

| 予測金額 | 601億4,000万米ドル |

| CAGR | 13.3% |

市場はロボットタイプによって区分され、多関節ロボット、直交ロボット、スカラロボット、円筒ロボット、協働ロボット(コボット)、パラレルロボット、極座標ロボットが含まれます。多関節ロボットは、溶接やマテリアルハンドリングなどの複雑な作業をこなす優れた敏捷性と能力により、2024年には71億2,000万米ドルとなり、最大の市場シェアを占めています。これらのロボットは、コストを削減し効率を向上させることができるため、自動車、金属加工、重工業などの産業で高い支持を得ています。

用途別では、産業用ロボット市場は自動車、エレクトロニクス、飲食品、医薬品、その他の産業に分類されます。特に自動車産業は、溶接、塗装、組立などの製造工程でロボットが広く使用されているため、2034年までに207億4,000万米ドルに達すると予想されています。ロボット工学は、精度と効率が重要な電気自動車の生産においても重要な役割を果たしています。

米国の産業用ロボット市場は大幅に成長し、2034年には38億4,000万米ドルを超えると予測されています。ロボット工学の採用は、自動車、エレクトロニクス、ロジスティクスなどの分野で拡大が続くと予想されます。さらに、AIとロボティクス・ソフトウェアの統合が勢いを増しており、中小企業ではコボットや自律型システムへの関心が高まっています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 自動化需要の増加

- AIと機械学習の進歩

- 労働力不足とコストの上昇

- スマートファクトリーとインダストリー4.0の成長

- 新産業におけるロボティクスの拡大

- 業界の潜在的リスク&課題

- 高い初期投資とメンテナンスコスト

- 労働力の再配置とスキルギャップ

- 促進要因

- 潜在成長力の分析

- 規制状況

- 技術動向

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021年~2034年

- 多関節ロボット

- 直交ロボット/ガントリーロボット

- スカラロボット

- 円筒型ロボット

- 協働ロボット/COBOTS

- パラレルロボット/デルタロボット

- ポーラーロボット/球体ロボット

第6章 市場推計・予測:最終用途別、2021年~2034年

- 自動車

- 金属・機械

- ゴム・プラスチック

- 飲食品

- 電気・電子

- 消費財

- ヘルスケア

- その他

第7章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第8章 企業プロファイル

- ABB Group

- Comau SpA

- Denso Corporation

- Epson America, Inc.

- Fanuc Corporation

- HD HYUNDAI ROBOTICS

- Kawasaki Heavy Industries, Ltd.

- KUKA AG

- Mitsubishi Electric Corporation

- Nachi Fujikoshi Corp

- Daihen, Inc.

- Omron Corporation

- Panasonic Corporation

- Rethink Robotics Inc.

- Staubli Group

- Universal Robots A/S

- Yamaha Motor Co., Ltd.

目次

The Global Industrial Robotics Market reached USD 17.78 billion in 2024 and is expected to grow at a CAGR of 13.3% from 2025 to 2034. This rapid expansion is being driven by the growing demand for automation across various sectors as businesses seek to improve productivity and address challenges such as labor shortages and rising labor costs. Automation is particularly gaining traction in industries like manufacturing, where robotic systems are used to streamline operations, reduce expenses, and enhance product quality. The increased use of automation in logistics, especially with the rise of e-commerce, has also contributed to the surge in demand for robotics. Companies are now relying more on automated systems for sorting and managing inventory in warehouses, enhancing efficiency. With businesses focusing on boosting their operations, the adoption of robotic technologies is set to increase faster than ever.

One of the main factors influencing the shift toward robotic automation is the lack of available skilled labor, coupled with rising operational expenses. Developed countries with aging populations, such as the U.S., Japan, and Germany, are particularly facing this challenge. In addition, developing nations like China and India are experiencing higher wage growth, making it necessary for businesses to seek cost-effective alternatives such as robotics. These factors are compelling industries to adopt robotic solutions at a much faster rate to remain competitive and maintain profitability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.78 Billion |

| Forecast Value | $60.14 Billion |

| CAGR | 13.3% |

The market is segmented based on the types of robots, which include articulated robots, cartesian robots, SCARA robots, cylindrical robots, collaborative robots (cobots), parallel robots, and polar robots. Articulated robots hold the largest market share, valued at USD 7.12 billion in 2024, due to their exceptional agility and ability to perform complex tasks like welding and material handling. These robots are highly favored in industries such as automotive, metalworking, and heavy industries due to their ability to reduce costs and improve efficiency.

In terms of application, the industrial robotics market is categorized into automotive, electronics, food and beverage, pharmaceuticals, and other industries. The automotive industry, in particular, is expected to reach USD 20.74 billion by 2034, as robotics are widely used in manufacturing processes like welding, painting, and assembly. Robotics also play a significant role in electric vehicle production, where precision and efficiency are crucial.

The U.S. industrial robotics market is set to grow substantially, with projections indicating it will surpass USD 3.84 billion by 2034. Adoption of robotics is expected to continue expanding across sectors such as automotive, electronics, and logistics. Additionally, the integration of AI and robotics software is gaining momentum, with smaller businesses showing increasing interest in cobots and autonomous systems.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing Demand for Automation

- 3.2.1.2 Advancements in AI and Machine Learning

- 3.2.1.3 Rising Labor Shortages and Costs

- 3.2.1.4 Growth of Smart Factories & Industry 4.0

- 3.2.1.5 Expansion of Robotics in New Industries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Investment & Maintenance Costs

- 3.2.2.2 Workforce Displacement & Skill Gaps

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Type, 2021 – 2034 (USD Million and Units)

- 5.1 Articulated robots

- 5.2 Cartesian robots/ Gantry robots

- 5.3 SCARA robots

- 5.4 Cylindrical robots

- 5.5 Collaborative robots/ COBOTS

- 5.6 Parallel robots/ Delta robots

- 5.7 Polar robots/ spherical robots

Chapter 6 Market estimates & forecast, By End Use, 2021 – 2034 (USD Million and Units)

- 6.1 Automotive

- 6.2 Metal & Machinery

- 6.3 Rubber & Plastic

- 6.4 Food & beverage

- 6.5 Electrical & electronics

- 6.6 Consumer goods

- 6.7 Healthcare

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million and Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 ABB Group

- 8.2 Comau SpA

- 8.3 Denso Corporation

- 8.4 Epson America, Inc.

- 8.5 Fanuc Corporation

- 8.6 HD HYUNDAI ROBOTICS

- 8.7 Kawasaki Heavy Industries, Ltd.

- 8.8 KUKA AG

- 8.9 Mitsubishi Electric Corporation

- 8.10 Nachi Fujikoshi Corp

- 8.11 Daihen, Inc.

- 8.12 Omron Corporation

- 8.13 Panasonic Corporation

- 8.14 Rethink Robotics Inc.

- 8.15 Staubli Group

- 8.16 Universal Robots A/S

- 8.17 Yamaha Motor Co., Ltd.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日