|

|

市場調査レポート

商品コード

1267425

非加熱殺菌の世界市場:技術別 (HPP、PEF、MVH、超音波、照射、その他の技術)・形状別 (固体、液体)・用途別 (食品、飲料、医薬品・化粧品)・地域別の将来予測 (2028年まで)Non-thermal Pasteurization Market by Technique (HPP, PEF, MVH, Ultrasonic, Irradiation, and Other Techniques), Form (Solid, Liquid), Application (Food, Beverage, and Pharmaceutical & Cosmetics) & Region - Global Forecast to 2028 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 非加熱殺菌の世界市場:技術別 (HPP、PEF、MVH、超音波、照射、その他の技術)・形状別 (固体、液体)・用途別 (食品、飲料、医薬品・化粧品)・地域別の将来予測 (2028年まで) |

|

出版日: 2023年04月25日

発行: MarketsandMarkets

ページ情報: 英文 251 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界の非加熱殺菌の市場規模は、2023年の23億米ドルから、2028年までに57億米ドルに達すると予測され、予測期間中に20.0%のCAGR (金額ベース) で成長する見通しです。

非加熱殺菌製品に関心が集まり、消費者はより多くの加工食品や栄養価の高い食品を摂取しようとしています。非加熱殺菌業界の成長要因として、健康への関心の高まり、タンパク質源の嗜好の進化、多様な加工食品・飲料を導入している食品加工部門の繁栄などが挙げられます。

"用途別では、果物・野菜の需要が予測期間中に拡大する"

より健康的で自然な食品を求める消費者の選好を受けて、安全で加工度の低い果物や野菜への需要が高まっています。そのため、栄養素の損失や風味に影響を与える高熱処理を行うことなく、果物や野菜の品質や栄養素を保持できる非加熱殺菌方式の需要が高まっています。米国農務省 (USDA) によると、最小限の加工を施した果物や野菜の需要は、過去10年間で着実に増加しています。この需要に応えるため、食品業界の多くの企業が非加熱殺菌方式に投資しています

"形状別では液体非加熱殺菌が、賞味期限の延長により需要が増加する"

HPP (高圧処理) は、果物や野菜のジュースに含まれるミネラル・ビタミン・抗酸化物質や味覚をすべて維持します。保存期間が長く、食の安全が保証されながら、搾りたてのジュースを飲むのに匹敵するほどです。近年、高圧処理の恩恵を大きく受ける多様な飲料が登場した結果、HPPの普及が進んでいます。HPPは風味・色・成分を保持することができ、まさに今日の顧客のニーズに応えるものです。

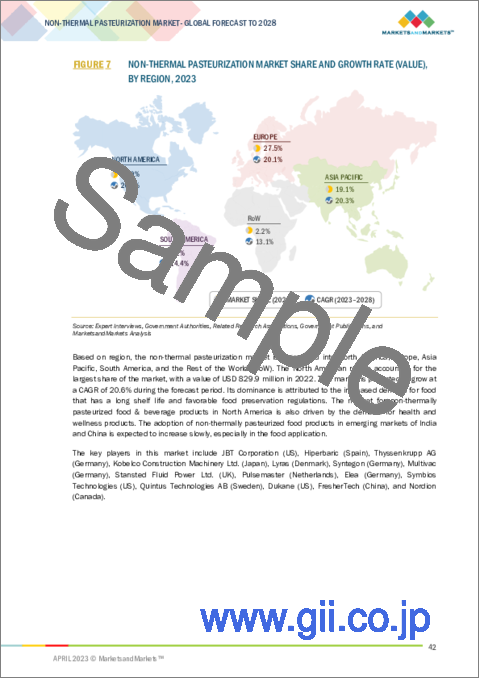

"地域別ではアジア太平洋が、加工食品の需要増により市場成長を牽引する"

アジア太平洋地域では、急速な経済成長により加工食品の需要が増加しています。アジア太平洋地域の人口増加が食品・飲料の需要を促進するため、加工時間の短縮や製造作業の効率化に役立つ、高度な食品加工装置の需要が急増すると予想されています。この地域では、食品加工施設の増加が見込まれており、食品・飲料加工装置の供給と消費をさらに押し上げると予測されます。また、この地域の食品加工部門は自動化が進んでおり、装置メーカーにさらなるビジネスチャンスをもたらしています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

第6章 業界動向

- イントロダクション

- バリューチェーン分析

- 顧客のビジネスに影響を与える動向/混乱

- 技術分析

- 特許分析

- 非加熱殺菌のマーケットマップとエコシステム

- 主な会議とイベント

- 関税と規制状況

- 規制の枠組み

- ポーターのファイブフォース分析

- サプライチェーン分析

- 主な利害関係者と購入基準

- 貿易分析

- ケーススタディ

- 価格分析

第7章 非加熱殺菌市場:技術別

- イントロダクション

- HPP (高圧処理)

- PEF (パルス電界)

- MVH (マイクロ波体積加熱)

- 超音波

- 照射

- その他の技術

第8章 非加熱殺菌市場:形状別

- イントロダクション

- 固体

- 液体

第9章 非加熱殺菌市場:用途別

- イントロダクション

- 食品

- 肉製品

- 果物・野菜

- 乳製品

- レディミール

- 飲料

- アルコール飲料

- ノンアルコール飲料

- 医薬品・化粧品

第10章 非加熱殺菌市場:地域別

- イントロダクション

- 不況の影響分析

- 非加熱殺菌市場に対する不況の影響

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- スペイン

- 英国

- イタリア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- ニュージーランド

- その他アジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他南米

- その他の地域 (ROW)

- 中東

- アフリカ

第11章 競合情勢

- 概要

- 市場シェア分析 (2021年)

- 主要企業のセグメント収益分析

- 主要企業が採用した戦略

- 企業評価クアドラント (主要企業)

- 非加熱殺菌市場:その他の企業の評価クアドラント (2022年)

- 競合シナリオ

第12章 企業プロファイル

- イントロダクション

- 主要企業

- JBT CORPORATION

- HIPERBARIC

- THYSSENKRUPP AG

- KOBELCO CONSTRUCTION MACHINERY LTD.

- SYNTEGON

- LYRAS

- MULTIVAC

- STANSTED FLUID POWER LTD.

- PULSEMASTER

- ELEA

- SYMBIOS TECHNOLOGIES

- QUINTUS TECHNOLOGIES AB

- DUKANE

- FRESHERTECH

- NORDION

- スタートアップ/中小企業

- STERIGENICS U.S., LLC

- COOLWAVE PROCESSING B.V.

- STERIBAR HPP

- YPSICON ADVANCED TECHNOLOGIES SL

- BAO TOU KEFA HIGH PRESSURE TECHNOLOGY CO., LTD

- その他の主要企業

- ADVANCED MICROWAVE TECHNOLOGIES

- EXDIN SOLUTIONS

- HARWOOD ENGINEERING COMPANY, INC.

- UNIVERSAL PURE

- AMERICAN PASTEURIZATION COMPANY

第13章 隣接・関連市場

- イントロダクション

- 制限事項

- 乳製品加工装置市場

- 果物・野菜加工市場

第14章 付録

According to MarketsandMarkets, the non-thermal pasteurization market is projected to reach USD 5.7 billion by 2028 from USD 2.3 billion by 2023, at a CAGR of 20.0% during the forecast period in terms of value. Non-thermal pasteurization products are gaining attention, and consumers are more inclined toward adding more processed and nutritive food. The factors responsible for the growth of the Non-thermal pasteurization industry are the increase in health concerns, evolving protein source preferences, and a thriving food-processing sector that is introducing a wide variety of processed food & beverage products.

"By application, Fruits and vegetables is projected in high demand during the forecast period."

The demand for safe and minimally processed fruits and vegetables has been increasing due to consumer preferences for healthier and more natural food options. This has led to a rise in demand for non-thermal pasteurization methods that can preserve the quality and nutrients of fruits and vegetables without using high heat treatments that can cause nutrient loss and affect flavor. According to the United States Department of Agriculture (USDA), the demand for minimally processed fruits and vegetables has been increasing steadily over the past decade. To meet this demand, many companies in the food industry are investing in non-thermal pasteurization methods

"By form, liquid Non-thermal pasteurization has increased demand due to increasing in shelf life."

The HPP method maintains all the minerals, vitamins, antioxidants, and taste in fruit and vegetable juices. While having a longer shelf life and a guarantee of food safety, it is comparable to drinking freshly squeezed juice. The HPP has seen increased expansion as a result of the diversity of drinks introduced in recent years that benefit greatly from high pressure processing. HPP retains its flavor, color, and composition, which is exactly what today's customer needs.

"By region, Asia Pacific to drive market growth due to increased demand for packaged food."

The Asia Pacific region has an increasing demand for packaged food products due to due to the rapid economic growth. The increasing population in the Asia-Pacific (APAC) region is driving the demand for food and beverages The region is expected to experience a sharp rise in the demand for advanced food processing machinery that helps to reduce processing time and enhance the efficiency of manufacturing operations. The expected growth in the number of food processing units in this region is further projected to boost the supply and consumption of food & beverage processing equipment. The food processing sectors in this region are also witnessing automation, which is further providing opportunities for the equipment manufacturers.

Break-up of Primaries:

By Value Chain Side: Tire 1-30%, Tire 2-45%, Tire3-25%

By Designation: CXOs-31%, Managers - 24%, and Executives- 45%

By Region: Europe - 25%, Asia Pacific - 15%, North America - 45%, RoW - 5%, South America-10%

Leading players profiled in this report:

- JBT Corporation (US),

- Hiperbaric (Spain),

- Thyssenkrupp AG (Germany),

- Kobelco Construction Machinery Ltd. (Japan),

- Lyras (Denmark), Syntegon (Germany),

- Multivac (Germany),

- Stansted Fluid Power Ltd. (UK),

- Pulsemaster (Netherlands),

- Elea (Germany),

- Symbios Technologies (US),

- Clextral (France),

- Dukane (US),

- FresherTech (China)

The study includes an in-depth competitive analysis of these key players in the Non-thermal pasteurization market with their company profiles, recent developments, and key market strategies.

Research Coverage:

The report segments the non-thermal pasteurization market on the basis of Technique, By Form, By Application, By Region. In terms of insights, this report has focused on various levels of analyses-the competitive landscape, end-use analysis, and company profiles, which together comprise and discuss views on the emerging & high-growth segments of the global non-thermal pasteurization market, high-growth regions, countries, government initiatives, drivers, restraints, opportunities, and challenges.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall non-thermal pasteurization market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and to plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Increase in demand for meat, poultry, and dairy products), restraints (high capital investment), opportunity (Government investment in food processing machinery & equipment), and challenges (Lack of consumer awareness) influencing the growth of the non-thermal pasteurization market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the non-thermal pasteurization market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the non-thermal pasteurization market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the non-thermal pasteurization market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players JBT Corporation (US), Hiperbaric (Spain), Thyssenkrupp AG (Germany), Kobelco Construction Machinery Ltd. (Japan), Lyras (Denmark), Syntegon (Germany), Multivac (Germany), Stansted Fluid Power Ltd. (UK), Pulsemaster (Netherlands), Elea (Germany), Symbios Technologies (US), Clextral (France), Dukane (US), FresherTech (China) and Nordion (Canada) are among others in the non-thermal pasteurization market strategies. The report also helps stakeholders understand the market and provides them information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- FIGURE 1 NON-THERMAL PASTEURIZATION MARKET SEGMENTATION

- 1.4 REGIONS COVERED

- 1.5 YEARS CONSIDERED

- 1.6 CURRENCY CONSIDERED

- TABLE 1 USD EXCHANGE RATES CONSIDERED, 2017-2022

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

- 1.9 RECESSION IMPACT ANALYSIS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 NON-THERMAL PASTEURIZATION MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakdown of primaries

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 NON-THERMAL PASTEURIZATION MARKET SIZE ESTIMATION: METHOD 1 (SUPPLY SIDE)

- 2.2.2 NON-THERMAL PASTEURIZATION MARKET SIZE ESTIMATION: METHOD 2 (DEMAND SIDE)

- 2.2.3 NON-THERMAL PASTEURIZATION MARKET SIZE ESTIMATION NOTES

- 2.3 DATA TRIANGULATION

- FIGURE 3 DATA TRIANGULATION METHODOLOGY

- 2.4 RECESSION IMPACT ANALYSIS

- 2.5 ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS AND ASSOCIATED RISKS

3 EXECUTIVE SUMMARY

- TABLE 2 NON-THERMAL PASTEURIZATION MARKET SHARE SNAPSHOT, 2023 VS. 2028 (USD MILLION)

- FIGURE 4 NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023 VS. 2028 (USD MILLION)

- FIGURE 5 NON-THERMAL PASTEURIZATION MARKET, BY FORM, 2023 VS. 2028 (USD MILLION)

- FIGURE 6 NON-THERMAL PASTEURIZATION MARKET, BY APPLICATION, 2023 VS. 2028 (USD MILLION)

- FIGURE 7 NON-THERMAL PASTEURIZATION MARKET SHARE AND GROWTH RATE (VALUE), BY REGION, 2023

4 PREMIUM INSIGHTS

- 4.1 OPPORTUNITIES IN NON-THERMAL PASTEURIZATION MARKET

- FIGURE 8 RISING TREND OF READY-TO-EAT FOOD TO DRIVE GROWTH OF NON-THERMAL PASTEURIZATION MARKET

- 4.2 NON-THERMAL PASTEURIZATION MARKET, BY FOOD SUB-APPLICATION

- FIGURE 9 FRUITS & VEGETABLES ESTIMATED TO DOMINATE MARKET DURING FORECAST PERIOD

- 4.3 NON-THERMAL PASTEURIZATION MARKET, BY BEVERAGE SUB-APPLICATION

- FIGURE 10 NON-ALCOHOLIC BEVERAGES ESTIMATED TO DOMINATE MARKET DURING FORECAST PERIOD

- 4.4 NORTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY KEY COUNTRY AND FORM

- FIGURE 11 SOLID SEGMENT TO BE KEY FORM OF NON-THERMAL PASTEURIZATION IN NORTH AMERICA IN 2023

- 4.5 NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE

- FIGURE 12 HIGH-PRESSURE PASTEURIZATION TO ACCOUNT FOR LARGEST SHARE, 2023 VS. 2028 (VALUE)

- 4.6 NON-THERMAL PASTEURIZATION MARKET: MAJOR REGIONAL SUBMARKETS

- FIGURE 13 US ACCOUNTED FOR LARGEST MARKET SHARE IN 2022

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 14 NON-THERMAL PASTEURIZATION MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Increase in consumption of convenience foods

- 5.2.1.2 Increase in demand for meat, poultry, and dairy products

- 5.2.1.3 Process optimization by non-thermal technologies resulting in greater efficiency during pasteurization

- 5.2.1.4 Rising demand for innovative food & beverage products due to changing consumer trends

- 5.2.2 RESTRAINTS

- 5.2.2.1 High capital investment

- 5.2.2.2 Growing demand for organic and fresh food products

- 5.2.2.3 Implementation of extra regulatory measures for labeling irradiated food

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Government investment in food processing machinery & equipment

- 5.2.3.2 Growing usage of High-pressure Processing (HPP) toll processors

- 5.2.4 CHALLENGES

- 5.2.4.1 Lack of consumer awareness

- 5.2.4.2 Need for technical expertise

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 VALUE CHAIN ANALYSIS

- FIGURE 15 VALUE CHAIN OF NON-THERMAL PASTEURIZATION MARKET

- 6.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 6.3.1 REVENUE SHIFT AND NEW REVENUE POCKETS IN NON-THERMAL PASTEURIZATION MARKET

- FIGURE 16 REVENUE SHIFT IMPACTING TRENDS/DISRUPTIONS IN NON-THERMAL PASTEURIZATION MARKET

- 6.4 TECHNOLOGICAL ANALYSIS

- 6.4.1 RADIO FREQUENCY (RF) HEATING

- 6.4.2 COLD PLASMA TREATMENT

- 6.4.3 OZONE TREATMENT

- 6.5 PATENT ANALYSIS

- FIGURE 17 NUMBER OF PATENTS GRANTED FOR NON-THERMAL PASTEURIZATION, 2012-2022

- FIGURE 18 REGIONAL ANALYSIS OF PATENTS GRANTED FOR NON-THERMAL PASTEURIZATION, 2012-2022

- TABLE 3 LIST OF IMPORTANT PATENTS FOR NON-THERMAL PASTEURIZATION, 2022

- 6.6 MARKET MAP AND ECOSYSTEM OF NON-THERMAL PASTEURIZATION

- 6.6.1 DEMAND SIDE

- 6.6.2 SUPPLY SIDE

- FIGURE 19 NON-THERMAL PASTEURIZATION MARKET: ECOSYSTEM MAP

- 6.7 KEY CONFERENCES AND EVENTS

- TABLE 4 KEY CONFERENCES AND EVENTS IN NON-THERMAL PASTEURIZATION, 2023

- 6.8 TARIFF AND REGULATORY LANDSCAPE

- 6.8.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 5 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 6 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 7 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 8 SOUTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 9 REST OF THE WORLD: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.9 REGULATORY FRAMEWORK

- 6.9.1 INTRODUCTION

- 6.9.2 EUROPEAN UNION

- 6.9.3 NORTH AMERICA (US AND CANADA)

- 6.9.3.1 USFDA - US food and drug administration inspection guide

- 6.9.3.2 Canada

- 6.9.4 ASIA PACIFIC (JAPAN AND CHINA)

- 6.10 PORTER'S FIVE FORCES ANALYSIS

- TABLE 10 NON-THERMAL PASTEURIZATION MARKET: PORTER'S FIVE FORCES ANALYSIS

- 6.10.1 INTENSITY OF COMPETITIVE RIVALRY

- 6.10.2 THREAT OF NEW ENTRANTS

- 6.10.3 THREAT OF SUBSTITUTES

- 6.10.4 BARGAINING POWER OF SUPPLIERS

- 6.10.5 BARGAINING POWER OF BUYERS

- 6.11 SUPPLY CHAIN ANALYSIS

- FIGURE 20 NON-THERMAL PASTEURIZATION MARKET: SUPPLY CHAIN ANALYSIS

- 6.12 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 21 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP END USERS

- TABLE 11 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP END USERS

- 6.12.2 BUYING CRITERIA

- FIGURE 22 KEY CRITERIA FOR SELECTING SUPPLIERS/VENDORS

- TABLE 12 KEY CRITERIA FOR SELECTING SUPPLIERS/VENDORS

- 6.13 TRADE ANALYSIS

- 6.13.1 EXPORT SCENARIO

- FIGURE 23 BEVERAGE EXPORTS, BY KEY COUNTRY, 2017-2021 (USD THOUSAND)

- 6.13.2 IMPORT SCENARIO

- FIGURE 24 BEVERAGE IMPORTS, BY KEY COUNTRY, 2017-2021 (USD THOUSAND)

- 6.14 CASE STUDIES

- 6.14.1 NUTRIFRESH SERVICES EXPANDED PRODUCT OFFERINGS AND ACHIEVED SUSTAINABILITY GOALS

- TABLE 13 HIPERBARIC HELPED NUTRIFRESH SERVICES MEET GROWING DEMAND FOR ECO-FRIENDLY FOOD PRODUCTS WITH HPP TECHNOLOGY

- 6.14.2 JUICEBOT INCREASED PRODUCTION AND EXPANDED PRODUCT OFFERINGS

- TABLE 14 JBT CORPORATION HELPED JUICEBOT MEET DEMAND FOR HEALTHY BEVERAGES

- 6.15 PRICING ANALYSIS

- 6.15.1 SELLING PRICE CHARGED BY COMPANIES IN TERMS OF TECHNIQUE

- FIGURE 25 SELLING PRICE FOR NON-THERMAL PASTEURIZATION TYPES

- TABLE 15 AVERAGE SELLING PRICE FOR TYPES, 2022 (USD/UNIT)

7 NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE

- 7.1 INTRODUCTION

- FIGURE 26 NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023 VS. 2028 (USD MILLION)

- TABLE 16 NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 17 NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 7.2 HIGH-PRESSURE PROCESSING (HPP)

- TABLE 18 HIGH-PRESSURE PROCESSING: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 19 HIGH-PRESSURE PROCESSING: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.2.1 HIGH-PRESSURE PROCESSING MARKET, BY ORIENTATION TYPE

- 7.2.1.1 Beverage sector to drive demand for horizontal orientation type

- TABLE 20 HIGH-PRESSURE PROCESSING MARKET, BY ORIENTATION TYPE, 2018-2022 (USD MILLION)

- TABLE 21 HIGH-PRESSURE PROCESSING MARKET, BY ORIENTATION TYPE, 2023-2028 (USD MILLION)

- 7.2.2 HIGH-PRESSURE PROCESSING MARKET, BY VESSEL VOLUME

- 7.2.2.1 Greater vessel volume to drive demand for high-pressure processing

- TABLE 22 HIGH-PRESSURE PROCESSING MARKET, BY VESSEL VOLUME, 2018-2022 (USD MILLION)

- TABLE 23 HIGH-PRESSURE PROCESSING MARKET, BY VESSEL VOLUME, 2023-2028 (USD MILLION)

- 7.3 PULSE ELECTRIC FIELD (PEF)

- 7.3.1 RISING DEMAND FOR PROCESSED FOOD & BEVERAGES TO DRIVE GROWTH

- TABLE 24 PULSE ELECTRIC FIELD: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 25 PULSE ELECTRIC FIELD: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.4 MICROWAVE VOLUMETRIC HEATING (MVH)

- 7.4.1 NEED FOR ENERGY-EFFICIENT AND SUSTAINABLE FOOD PROCESSING TECHNOLOGIES TO DRIVE MARKET

- TABLE 26 MICROWAVE VOLUMETRIC HEATING (MVH): NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 27 MICROWAVE VOLUMETRIC HEATING (MVH): NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.5 ULTRASONIC

- 7.5.1 SUPPORT OF GOVERNMENTS AND INVESTMENTS BY LEADING COMPANIES TO DRIVE GROWTH

- TABLE 28 ULTRASONIC: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 29 ULTRASONIC: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

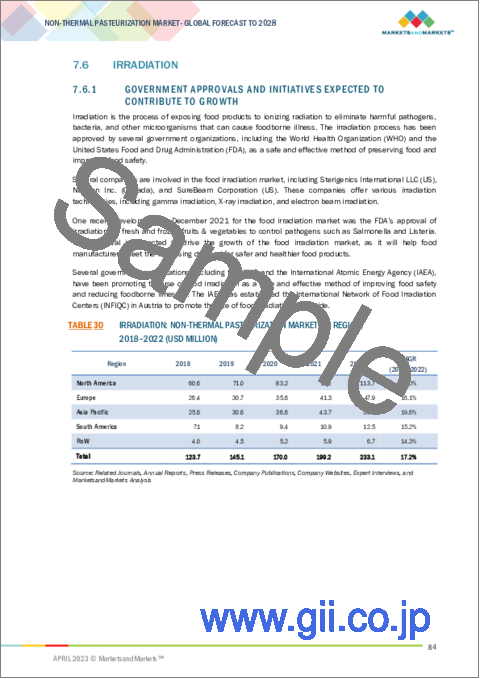

- 7.6 IRRADIATION

- 7.6.1 GOVERNMENT APPROVALS AND INITIATIVES EXPECTED TO CONTRIBUTE TO GROWTH

- TABLE 30 IRRADIATION: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 31 IRRADIATION: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.7 OTHER TECHNIQUES

- TABLE 32 OTHER TECHNIQUES: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 33 OTHER TECHNIQUES: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

8 NON-THERMAL PASTEURIZATION MARKET, BY FORM

- 8.1 INTRODUCTION

- FIGURE 27 NON-THERMAL PASTEURIZATION MARKET, BY FORM, 2023 VS. 2028

- TABLE 34 NON-THERMAL PASTEURIZATION MARKET, BY FORM, 2018-2022 (USD MILLION)

- TABLE 35 NON-THERMAL PASTEURIZATION MARKET, BY FORM, 2023-2028 (USD MILLION)

- 8.2 SOLID

- 8.2.1 PEF CONSIDERED UNSUITABLE FOR SOLID ITEMS

- TABLE 36 SOLID: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 37 SOLID: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 8.3 LIQUID

- 8.3.1 HPP TO BE PRIMARILY USED FOR PROCESSING OF LIQUIDS

- TABLE 38 LIQUID: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 39 LIQUID: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

9 NON-THERMAL PASTEURIZATION MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- FIGURE 28 NON-THERMAL PASTEURIZATION MARKET, BY APPLICATION, 2023 VS. 2028 (USD MILLION)

- TABLE 40 NON-THERMAL PASTEURIZATION MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 41 NON-THERMAL PASTEURIZATION MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 9.2 FOOD

- TABLE 42 NON-THERMAL PASTEURIZATION MARKET, BY FOOD SUB-APPLICATION, 2018-2022 (USD MILLION)

- TABLE 43 NON-THERMAL PASTEURIZATION MARKET, BY FOOD SUB-APPLICATION, 2023-2028 (USD MILLION)

- TABLE 44 FOOD: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 45 FOOD: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.2.1 MEAT PRODUCTS

- 9.2.1.1 Growing demand for minimum processing of meat products to fuel growth

- TABLE 46 MEAT PRODUCTS: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 47 MEAT PRODUCTS: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.2.2 FRUITS & VEGETABLES

- 9.2.2.1 Rising demand for high-quality, safe, and minimally processed food to drive market

- TABLE 48 FRUITS & VEGETABLES: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 49 FRUITS & VEGETABLES: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.2.3 DAIRY PRODUCTS

- 9.2.3.1 Rising demand for nutritional dairy products to encourage producing safer foods at low expenses

- TABLE 50 DAIRY PRODUCTS: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 51 DAIRY PRODUCTS: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.2.4 READY MEALS

- 9.2.4.1 Demand for ready meals to be driven by busy lifestyles and growing geriatric population

- TABLE 52 READY MEALS: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 53 READY MEALS: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.3 BEVERAGES

- TABLE 54 NON-THERMAL PASTEURIZATION MARKET, BY BEVERAGE SUB-APPLICATION, 2018-2022 (USD MILLION)

- TABLE 55 NON-THERMAL PASTEURIZATION MARKET, BY BEVERAGE SUB-APPLICATION, 2023-2028 (USD MILLION)

- 9.3.1 ALCOHOLIC BEVERAGES

- TABLE 56 ALCOHOLIC BEVERAGES: NON-THERMAL PASTEURIZATION MARKET, BY SUB-APPLICATION, 2018-2022 (USD MILLION)

- TABLE 57 ALCOHOLIC BEVERAGES: NON-THERMAL PASTEURIZATION MARKET, BY SUB-APPLICATION, 2023-2028 (USD MILLION)

- 9.3.1.1 Beer

- 9.3.1.1.1 Rising demand for high-quality and safe beer with extended shelf life to augment market growth

- 9.3.1.1 Beer

- TABLE 58 BEER: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 59 BEER: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.3.1.2 Wine

- 9.3.1.2.1 Growing demand for premium and artisanal wines to drive market growth

- 9.3.1.2 Wine

- TABLE 60 WINE: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 61 WINE: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.3.1.3 Other alcoholic beverages

- TABLE 62 OTHER ALCOHOLIC BEVERAGES: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 63 OTHER ALCOHOLIC BEVERAGES: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.3.2 NON-ALCOHOLIC BEVERAGES

- TABLE 64 NON-ALCOHOLIC BEVERAGES: NON-THERMAL PASTEURIZATION MARKET, BY SUB-APPLICATION, 2018-2022 (USD MILLION)

- TABLE 65 NON-ALCOHOLIC BEVERAGES: NON-THERMAL PASTEURIZATION MARKET, BY SUB-APPLICATION, 2023-2028 (USD MILLION)

- 9.3.2.1 Juices

- 9.3.2.1.1 Rising demand for cold-pressed juices to create opportunities

- 9.3.2.1 Juices

- TABLE 66 JUICES: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 67 JUICES: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.3.2.2 Carbonated drinks

- 9.3.2.2.1 Non-thermal pasteurization to increase shelf life of carbonated beverages

- 9.3.2.2 Carbonated drinks

- TABLE 68 CARBONATED DRINKS: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 69 CARBONATED DRINKS: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.3.2.3 Other non-alcoholic beverage applications

- TABLE 70 OTHER NON-ALCOHOLIC BEVERAGES: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 71 OTHER NON-ALCOHOLIC BEVERAGES: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.4 PHARMACEUTICALS & COSMETICS

- 9.4.1 GRADUAL GROWTH IN NOVEL TECHNOLOGIES TO DRIVE MARKET

- TABLE 72 PHARMACEUTICALS AND COSMETICS: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 73 PHARMACEUTICALS AND COSMETICS: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

10 NON-THERMAL PASTEURIZATION MARKET, BY REGION

- 10.1 INTRODUCTION

- FIGURE 29 NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023 VS. 2028 (USD MILLION)

- FIGURE 30 CHINA TO BE FASTEST-GROWING COUNTRY-LEVEL MARKET FROM 2023 TO 2028

- TABLE 74 NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 75 NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 10.2 RECESSION IMPACT ANALYSIS

- 10.3 RECESSION IMPACT ON NON-THERMAL PASTEURIZATION MARKET

- 10.3.1 MACRO INDICATORS OF RECESSION

- FIGURE 31 INDICATORS OF RECESSION

- FIGURE 32 WORLD INFLATION RATE, 2011-2021

- FIGURE 33 GLOBAL GDP, 2011-2021 (USD TRILLION)

- FIGURE 34 RECESSION INDICATORS AND THEIR IMPACT ON NON-THERMAL PASTEURIZATION MARKET

- FIGURE 35 NON-THERMAL PASTEURIZATION MARKET: EARLIER FORECAST VS. RECESSION FORECAST

- 10.4 NORTH AMERICA

- FIGURE 36 NORTH AMERICA: MARKET SNAPSHOT

- TABLE 76 NORTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 77 NORTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 78 NORTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 79 NORTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- TABLE 80 NORTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 81 NORTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 82 NON-THERMAL PASTEURIZATION MARKET, BY FOOD SUB-APPLICATION, 2018-2022 (USD MILLION)

- TABLE 83 NORTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY FOOD SUB-APPLICATION, 2023-2028 (USD MILLION)

- TABLE 84 NORTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY BEVERAGE SUB-APPLICATION, 2018-2022 (USD MILLION)

- TABLE 85 NORTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY BEVERAGE SUB-APPLICATION, 2023-2028 (USD MILLION)

- TABLE 86 NORTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY NON-ALCOHOLIC BEVERAGE, 2018-2022 (USD MILLION)

- TABLE 87 NORTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY NON-ALCOHOLIC BEVERAGE, 2023-2028 (USD MILLION)

- TABLE 88 NORTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY ALCOHOLIC BEVERAGE, 2018-2022 (USD MILLION)

- TABLE 89 NORTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY ALCOHOLIC BEVERAGE, 2023-2028 (USD MILLION)

- TABLE 90 NORTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY FORM, 2018-2022 (USD MILLION)

- TABLE 91 NORTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY FORM, 2023-2028 (USD MILLION)

- 10.4.1 NORTH AMERICA: RECESSION IMPACT

- FIGURE 37 NORTH AMERICA: INFLATION RATES, BY KEY COUNTRY, 2017-2021

- FIGURE 38 NORTH AMERICA: RECESSION IMPACT ANALYSIS, 2023

- 10.4.2 US

- 10.4.2.1 Demand for processed meat, fruits, and vegetables to drive market

- TABLE 92 US: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 93 US: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.4.3 CANADA

- 10.4.3.1 Highly competitive food manufacturers to employ non-thermal pasteurization technologies

- TABLE 94 CANADA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 95 CANADA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.4.4 MEXICO

- 10.4.4.1 Increasing consumer demand for healthier and safer food options to drive growth

- TABLE 96 MEXICO: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 97 MEXICO: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.5 EUROPE

- TABLE 98 EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 99 EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 100 EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 101 EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- TABLE 102 EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 103 EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 104 EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY FOOD SUB-APPLICATION, 2018-2022 (USD MILLION)

- TABLE 105 EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY FOOD SUB-APPLICATION, 2023-2028 (USD MILLION)

- TABLE 106 EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY BEVERAGE SUB-APPLICATION, 2018-2022 (USD MILLION)

- TABLE 107 EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY BEVERAGE SUB-APPLICATION, 2023-2028 (USD MILLION)

- TABLE 108 EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY NON-ALCOHOLIC BEVERAGE, 2018-2022 (USD MILLION)

- TABLE 109 EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY NON-ALCOHOLIC BEVERAGE, 2023-2028 (USD MILLION)

- TABLE 110 EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY ALCOHOLIC BEVERAGE, 2018-2022 (USD MILLION)

- TABLE 111 EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY ALCOHOLIC BEVERAGE, 2023-2028 (USD MILLION)

- TABLE 112 EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY FORM, 2018-2022 (USD MILLION)

- TABLE 113 EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY FORM, 2023-2028 (USD MILLION)

- 10.5.1 EUROPE: RECESSION IMPACT

- FIGURE 39 EUROPE: INFLATION RATES, BY KEY COUNTRY, 2017-2021

- FIGURE 40 EUROPE: RECESSION IMPACT ANALYSIS, 2023

- 10.5.2 GERMANY

- 10.5.2.1 German meat industry to be leading user of HPP technology

- TABLE 114 GERMANY: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 115 GERMANY: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.5.3 FRANCE

- 10.5.3.1 France to be crucial market for food packaging technology & equipment in Europe

- TABLE 116 FRANCE: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 117 FRANCE: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.5.4 SPAIN

- 10.5.4.1 Packaged food market growth to accelerate food & beverage non-thermal pasteurization sector

- TABLE 118 SPAIN: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 119 SPAIN: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.5.5 UK

- 10.5.5.1 Demand for non-thermally processed fruit juices without preservatives to drive market

- TABLE 120 UK: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 121 UK: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.5.6 ITALY

- 10.5.6.1 Strong culture of artisanal and premium food & beverage production to drive demand

- TABLE 122 ITALY: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 123 ITALY: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.5.7 REST OF EUROPE

- TABLE 124 REST OF EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 125 REST OF EUROPE: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.6 ASIA PACIFIC

- TABLE 126 ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 127 ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 128 ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 129 ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- TABLE 130 ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 131 ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 132 ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY FOOD SUB-APPLICATION, 2018-2022 (USD MILLION)

- TABLE 133 ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY FOOD SUB-APPLICATION, 2023-2028 (USD MILLION)

- TABLE 134 ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY BEVERAGE SUB-APPLICATION, 2018-2022 (USD MILLION)

- TABLE 135 ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY BEVERAGE SUB-APPLICATION, 2023-2028 (USD MILLION)

- TABLE 136 ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY NON-ALCOHOLIC BEVERAGE, 2018-2022 (USD MILLION)

- TABLE 137 ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY NON-ALCOHOLIC BEVERAGE, 2023-2028 (USD MILLION)

- TABLE 138 ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY ALCOHOLIC BEVERAGE, 2018-2022 (USD MILLION)

- TABLE 139 ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY ALCOHOLIC BEVERAGE, 2023-2028 (USD MILLION)

- TABLE 140 ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY FORM, 2018-2022 (USD MILLION)

- TABLE 141 ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY FORM, 2023-2028 (USD MILLION)

- 10.6.1 ASIA PACIFIC: RECESSION IMPACT

- FIGURE 41 ASIA PACIFIC: INFLATION RATES, BY KEY COUNTRY, 2017-2021

- FIGURE 42 ASIA PACIFIC: RECESSION IMPACT ANALYSIS, 2023

- 10.6.2 CHINA

- 10.6.2.1 HPP-treated meat & seafood to witness increased demand due to advantages over thermal processing

- TABLE 142 CHINA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 143 CHINA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.6.3 INDIA

- 10.6.3.1 India's expansion of packaged and processed food exports to drive market growth

- TABLE 144 INDIA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 145 INDIA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.6.4 JAPAN

- 10.6.4.1 Commercial availability of non-thermally treated food products to augment growth

- TABLE 146 JAPAN: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 147 JAPAN: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.6.5 AUSTRALIA

- 10.6.5.1 Export of fish, meat, and bakery items to contribute to market growth

- TABLE 148 AUSTRALIA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 149 AUSTRALIA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.6.6 NEW ZEALAND

- 10.6.6.1 Rising demand for processed food and dairy products to fuel market growth

- TABLE 150 NEW ZEALAND: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 151 NEW ZEALAND: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.6.7 REST OF ASIA PACIFIC

- TABLE 152 REST OF ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 153 REST OF ASIA PACIFIC: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.7 SOUTH AMERICA

- TABLE 154 SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 155 SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 156 SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 157 SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- TABLE 158 SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 159 SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 160 SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY FOOD SUB-APPLICATION, 2018-2022 (USD MILLION)

- TABLE 161 SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY FOOD SUB-APPLICATION, 2023-2028 (USD MILLION)

- TABLE 162 SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY BEVERAGE SUB-APPLICATION, 2018-2022 (USD MILLION)

- TABLE 163 SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY BEVERAGE SUB-APPLICATION, 2023-2028 (USD MILLION)

- TABLE 164 SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY NON-ALCOHOLIC BEVERAGE, 2018-2022 (USD MILLION)

- TABLE 165 SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY NON-ALCOHOLIC BEVERAGE, 2023-2028 (USD MILLION)

- TABLE 166 SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY ALCOHOLIC BEVERAGE, 2018-2022 (USD MILLION)

- TABLE 167 SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY ALCOHOLIC BEVERAGE, 2023-2028 (USD MILLION)

- TABLE 168 SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY FORM, 2018-2022 (USD MILLION)

- TABLE 169 SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY FORM, 2023-2028 (USD MILLION)

- 10.7.1 SOUTH AMERICA: RECESSION IMPACT ANALYSIS

- FIGURE 43 SOUTH AMERICA: INFLATION RATES, BY KEY COUNTRY, 2017-2021

- FIGURE 44 SOUTH AMERICA: RECESSION IMPACT ANALYSIS, 2023

- 10.7.2 BRAZIL

- 10.7.2.1 Fast growth in food and agricultural sectors to promote use of non-thermal processing technologies

- TABLE 170 BRAZIL: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 171 BRAZIL: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.7.3 ARGENTINA

- 10.7.3.1 Expansion of well-established retail chains to widen application of non-thermal processing in convenience food

- TABLE 172 ARGENTINA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 173 ARGENTINA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.7.4 REST OF SOUTH AMERICA

- TABLE 174 REST OF SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 175 REST OF SOUTH AMERICA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.8 REST OF THE WORLD (ROW)

- TABLE 176 ROW: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 177 ROW: NON-THERMAL PASTEURIZATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 178 ROW: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 179 ROW: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- TABLE 180 ROW: NON-THERMAL PASTEURIZATION MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 181 ROW: NON-THERMAL PASTEURIZATION MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 182 ROW: NON-THERMAL PASTEURIZATION MARKET, BY FOOD SUB-APPLICATION, 2018-2022 (USD MILLION)

- TABLE 183 ROW: NON-THERMAL PASTEURIZATION MARKET, BY FOOD SUB-APPLICATION, 2023-2028 (USD MILLION)

- TABLE 184 ROW: NON-THERMAL PASTEURIZATION MARKET, BY BEVERAGE SUB-APPLICATION, 2018-2022 (USD MILLION)

- TABLE 185 ROW: NON-THERMAL PASTEURIZATION MARKET, BY BEVERAGE SUB-APPLICATION, 2023-2028 (USD MILLION)

- TABLE 186 ROW: NON-THERMAL PASTEURIZATION MARKET, BY NON-ALCOHOLIC BEVERAGE, 2018-2022 (USD MILLION)

- TABLE 187 ROW: NON-THERMAL PASTEURIZATION MARKET, BY NON-ALCOHOLIC BEVERAGE, 2023-2028 (USD MILLION)

- TABLE 188 ROW: NON-THERMAL PASTEURIZATION MARKET, BY ALCOHOLIC BEVERAGE, 2018-2022 (USD MILLION)

- TABLE 189 ROW: NON-THERMAL PASTEURIZATION MARKET, BY ALCOHOLIC BEVERAGE, 2023-2028 (USD MILLION)

- TABLE 190 ROW: NON-THERMAL PASTEURIZATION MARKET, BY FORM, 2018-2022 (USD MILLION)

- TABLE 191 ROW: NON-THERMAL PASTEURIZATION MARKET, BY FORM, 2023-2028 (USD MILLION)

- 10.8.1 REST OF THE WORLD: RECESSION IMPACT

- FIGURE 45 ROW: INFLATION RATES, BY KEY REGION, 2017-2021

- FIGURE 46 ROW: RECESSION IMPACT ANALYSIS, 2023

- 10.8.2 MIDDLE EAST

- 10.8.2.1 Middle East to present opportunities for domestic as well as international non-thermal pasteurization technique providers

- TABLE 192 MIDDLE EAST: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 193 MIDDLE EAST: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

- 10.8.3 AFRICA

- 10.8.3.1 Expansion of retail chains to increase application of non-thermal processing in convenience food

- TABLE 194 AFRICA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2018-2022 (USD MILLION)

- TABLE 195 AFRICA: NON-THERMAL PASTEURIZATION MARKET, BY TECHNIQUE, 2023-2028 (USD MILLION)

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 MARKET SHARE ANALYSIS, 2021

- TABLE 196 NON-THERMAL PASTEURIZATION MARKET: DEGREE OF COMPETITION (CONSOLIDATED)

- 11.3 SEGMENTAL REVENUE ANALYSIS OF KEY PLAYERS

- FIGURE 47 SEGMENTAL REVENUE ANALYSIS OF KEY PLAYERS, 2018-2021 (USD BILLION)

- 11.4 STRATEGIES ADOPTED BY KEY PLAYERS

- TABLE 197 STRATEGIES ADOPTED BY KEY NON-THERMAL PASTEURIZATION MANUFACTURERS

- 11.5 COMPANY EVALUATION QUADRANT (KEY PLAYERS)

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- FIGURE 48 NON-THERMAL PASTEURIZATION MARKET: COMPANY EVALUATION QUADRANT, 2022 (KEY PLAYERS)

- 11.5.5 FOOTPRINT, BY TECHNIQUE

- TABLE 198 COMPANY FOOTPRINT, BY TECHNIQUE

- TABLE 199 COMPANY FOOTPRINT, BY APPLICATION

- TABLE 200 COMPANY FOOTPRINT, BY REGION

- TABLE 201 OVERALL COMPANY FOOTPRINT

- 11.6 NON-THERMAL PASTEURIZATION MARKET: EVALUATION QUADRANT FOR OTHER PLAYERS, 2022

- 11.6.1 PROGRESSIVE COMPANIES

- 11.6.2 STARTING BLOCKS

- 11.6.3 RESPONSIVE COMPANIES

- 11.6.4 DYNAMIC COMPANIES

- FIGURE 49 NON-THERMAL PASTEURIZATION MARKET: COMPANY EVALUATION QUADRANT, 2022 (OTHER PLAYERS)

- 11.6.5 COMPETITIVE BENCHMARKING OF OTHER PLAYERS

- TABLE 202 NON-THERMAL PASTEURIZATION MARKET: DETAILED LIST OF OTHER PLAYERS

- TABLE 203 NON-THERMAL PASTEURIZATION MARKET: COMPETITIVE BENCHMARKING OF OTHER PLAYERS

- 11.7 COMPETITIVE SCENARIO

- 11.7.1 PRODUCT LAUNCHES

- TABLE 204 NON-THERMAL PASTEURIZATION MARKET: PRODUCT LAUNCHES, 2021-2022

- 11.7.2 DEALS

- TABLE 205 NON-THERMAL PASTEURIZATION MARKET: DEALS, 2018-2022

- 11.7.3 OTHERS

- TABLE 206 NON-THERMAL PASTEURIZATION MARKET: OTHERS, 2018-2022

12 COMPANY PROFILES

- 12.1 INTRODUCTION

- (Business overview, Products offered, Recent Developments, MNM view)**

- 12.2 KEY PLAYERS

- 12.2.1 JBT CORPORATION

- TABLE 207 JBT CORPORATION: BUSINESS OVERVIEW

- FIGURE 50 JBT CORPORATION: COMPANY SNAPSHOT

- TABLE 208 JBT CORPORATION: PRODUCTS OFFERED

- TABLE 209 JBT CORPORATION: PRODUCT LAUNCHES

- TABLE 210 JBT CORPORATION: OTHER DEVELOPMENTS

- 12.2.2 HIPERBARIC

- TABLE 211 HIPERBARIC: BUSINESS OVERVIEW

- TABLE 212 HIPERBARIC: PRODUCTS OFFERED

- TABLE 213 HIPERBARIC: PRODUCT LAUNCHES

- TABLE 214 HIPERBARIC: DEALS

- 12.2.3 THYSSENKRUPP AG

- TABLE 215 THYSSENKRUPP AG: BUSINESS OVERVIEW

- FIGURE 51 THYSSENKRUPP AG: COMPANY SNAPSHOT

- TABLE 216 THYSSENKRUPP AG: PRODUCTS OFFERED

- 12.2.4 KOBELCO CONSTRUCTION MACHINERY LTD.

- TABLE 217 KOBELCO CONSTRUCTION MACHINERY LTD.: BUSINESS OVERVIEW

- FIGURE 52 KOBELCO CONSTRUCTION MACHINERY LTD.: COMPANY SNAPSHOT

- TABLE 218 KOBELCO CONSTRUCTION MACHINERY LTD.: PRODUCTS OFFERED

- TABLE 219 KOBELCO CONSTRUCTION MACHINERY LTD: DEALS

- TABLE 220 KOBELCO CONSTRUCTION MACHINERY LTD.: OTHER DEVELOPMENTS

- 12.2.5 SYNTEGON

- TABLE 221 SYNTEGON: BUSINESS OVERVIEW

- TABLE 222 SYNTEGON: PRODUCTS OFFERED

- 12.2.6 LYRAS

- TABLE 223 LYRAS: BUSINESS OVERVIEW

- TABLE 224 LYRAS: PRODUCTS OFFERED

- TABLE 225 LYRAS: OTHER DEVELOPMENTS

- 12.2.7 MULTIVAC

- TABLE 226 MULTIVAC: BUSINESS OVERVIEW

- TABLE 227 MULTIVAC: PRODUCTS OFFERED

- 12.2.8 STANSTED FLUID POWER LTD.

- TABLE 228 STANSTED FLUID POWER LTD.: BUSINESS OVERVIEW

- TABLE 229 STANSTED FLUID POWER LTD.: PRODUCTS OFFERED

- 12.2.9 PULSEMASTER

- TABLE 230 PULSEMASTER: BUSINESS OVERVIEW

- TABLE 231 PULSEMASTER: PRODUCTS OFFERED

- 12.2.10 ELEA

- TABLE 232 ELEA: BUSINESS OVERVIEW

- TABLE 233 ELEA: PRODUCTS OFFERED

- 12.2.11 SYMBIOS TECHNOLOGIES

- TABLE 234 SYMBIOS TECHNOLOGIES: BUSINESS OVERVIEW

- TABLE 235 SYMBIOS TECHNOLOGIES: PRODUCTS OFFERED

- 12.2.12 QUINTUS TECHNOLOGIES AB

- TABLE 236 QUINTUS TECHNOLOGIES AB: BUSINESS OVERVIEW

- TABLE 237 QUINTUS TECHNOLOGIES AB: PRODUCTS OFFERED

- 12.2.13 DUKANE

- TABLE 238 DUKANE: BUSINESS OVERVIEW

- TABLE 239 DUKANE: PRODUCTS OFFERED

- TABLE 240 DUKANE: DEALS

- 12.2.14 FRESHERTECH

- TABLE 241 FRESHERTECH: BUSINESS OVERVIEW

- TABLE 242 FRESHERTECH: PRODUCTS OFFERED

- 12.2.15 NORDION

- TABLE 243 NORDION: BUSINESS OVERVIEW

- TABLE 244 NORDION: PRODUCTS OFFERED

- TABLE 245 NORDION: DEALS

- 12.3 START-UPS/SMES

- 12.3.1 STERIGENICS U.S., LLC

- TABLE 246 STERIGENICS U.S., LLC: BUSINESS OVERVIEW

- TABLE 247 STERIGENICS U.S., LLC: PRODUCTS OFFERED

- TABLE 248 STERIGENICS U.S., LLC: DEALS

- TABLE 249 STERIGENICS U.S., LLC: OTHER DEVELOPMENTS

- 12.3.2 COOLWAVE PROCESSING B.V.

- TABLE 250 COOLWAVE PROCESSING B.V.: BUSINESS OVERVIEW

- TABLE 251 COOLWAVE PROCESSING B.V.: PRODUCTS OFFERED

- 12.3.3 STERIBAR HPP

- TABLE 252 STERIBAR HPP: BUSINESS OVERVIEW

- TABLE 253 STERIBAR HPP: PRODUCTS OFFERED

- 12.3.4 YPSICON ADVANCED TECHNOLOGIES SL

- TABLE 254 YPSICON ADVANCED TECHNOLOGIES SL: BUSINESS OVERVIEW

- TABLE 255 YPSICON ADVANCED TECHNOLOGIES SL: PRODUCTS OFFERED

- 12.3.5 BAO TOU KEFA HIGH PRESSURE TECHNOLOGY CO., LTD

- TABLE 256 BAO TOU KEFA HIGH PRESSURE TECHNOLOGY CO., LTD: BUSINESS OVERVIEW

- TABLE 257 BAO TOU KEFA HIGH PRESSURE TECHNOLOGY CO., LTD: PRODUCTS OFFERED

- 12.4 OTHER KEY PLAYERS

- 12.4.1 ADVANCED MICROWAVE TECHNOLOGIES

- 12.4.2 EXDIN SOLUTIONS

- 12.4.3 HARWOOD ENGINEERING COMPANY, INC.

- 12.4.4 UNIVERSAL PURE

- 12.4.5 AMERICAN PASTEURIZATION COMPANY

- *Details on Business overview, Products offered, Recent Developments, MNM view might not be captured in case of unlisted companies.

13 ADJACENT & RELATED MARKETS

- 13.1 INTRODUCTION

- TABLE 258 ADJACENT MARKETS TO NON-THERMAL PASTEURIZATION MARKET

- 13.2 LIMITATIONS

- 13.3 DAIRY PROCESSING EQUIPMENT MARKET

- 13.3.1 MARKET DEFINITION

- 13.3.2 MARKET OVERVIEW

- TABLE 259 DAIRY PROCESSING EQUIPMENT MARKET, BY TYPE, 2016-2020 (USD MILLION)

- TABLE 260 DAIRY PROCESSING EQUIPMENT MARKET, BY TYPE, 2021-2026 (USD MILLION)

- 13.4 FRUIT & VEGETABLE PROCESSING MARKET

- 13.4.1 MARKET DEFINITION

- 13.4.2 MARKET OVERVIEW

- TABLE 261 FRUIT & VEGETABLE PROCESSING EQUIPMENT MARKET, BY TYPE, 2017-2021 (USD MILLION)

- TABLE 262 FRUIT & VEGETABLE PROCESSING EQUIPMENT MARKET, BY TYPE, 2022-2027 (USD MILLION)

14 APPENDIX

- 14.1 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.2 CUSTOMIZATION OPTIONS

- 14.3 RELATED REPORTS

- 14.4 AUTHOR DETAILS