|

|

市場調査レポート

商品コード

1345515

GaN半導体デバイスの世界市場:ウエハサイズ別、タイプ別、デバイス別、用途別、電圧範囲別、業界別、地域別-2028年までの予測GaN Semiconductor Device Market by Type (Opto-semiconductor, RF Semiconductor, Power Semiconductor), Device (Discrete, Integrated, HEMT, MMIC), Application (Lighting and Lasers, Power Drives), Voltage Range, Vertical and Region- Global Forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| GaN半導体デバイスの世界市場:ウエハサイズ別、タイプ別、デバイス別、用途別、電圧範囲別、業界別、地域別-2028年までの予測 |

|

出版日: 2023年09月04日

発行: MarketsandMarkets

ページ情報: 英文 246 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

GaN半導体デバイスの市場規模は、2023年の211億米ドルから2028年には283億米ドルに達すると予測されており、2023年から2028年までのCAGRは6.1%と見込まれています。

GaN半導体デバイス市場の成長を促進する主な要因には、民生およびビジネス企業におけるGaN半導体デバイスの採用の増加、GaN半導体デバイスの採用を促進する政府主導のスキームの増加、よりコンパクトなサイズのシステムに対する需要の変化、エネルギーおよび電力産業におけるGaN半導体デバイスの用途拡大などがあります。さらに、GaN半導体デバイスの継続的な技術進歩や自動車産業におけるGaN半導体デバイスの展開の拡大は、GaN半導体デバイス市場の市場プレーヤーにいくつかの成長機会を提供すると期待されています。

民生用電子機器は、GaN半導体デバイスの顕著な成長志向のエンドユーザー領域の1つであり、GaN光半導体デバイスの領域から顕著な収入源が発生しています。GaN半導体デバイスのラップトップ、ディスプレイ、モバイル機器への統合の増加は、GaN半導体デバイスの市場シェアに大きく貢献すると予想されます。

集積型GaN半導体には、GaN MMICとGaNアンプが含まれます。これらのソリューションでは、GaNトランジスタとゲート 促進要因、保護回路、温度センサなどの必須コンポーネントを統合パッケージ内に集積しています。この戦略的統合は、スイッチング速度の高速化、コンパクトな磁気回路、電力密度の向上など、多くの利点を提供します。

電気自動車とハイブリッド電気自動車(EVとHEV)の市場拡大が、市場成長に大きく寄与しています。GaN半導体デバイスの統合は、車両全体の重量を軽減し、バッテリー管理を強化する、よりコンパクトなシステムを実現するため、これらの車両の電子システム全体の状況に革命をもたらしています。北米のGaN半導体デバイス市場の主要企業には、GaN Systems、Wolfspeed、Qorvo、Analog Devicesなどがあります。

当レポートでは、世界のGaN半導体デバイス市場について調査し、ウエハサイズ別、タイプ別、デバイス別、用途別、電圧範囲別、業界別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- バリューチェーン分析

- エコシステム分析

- 顧客のビジネスに影響を与える動向/混乱

- 技術分析

- 価格分析

- ポーターのファイブフォース分析

- 主要な利害関係者と購入基準

- ケーススタディ分析

- 貿易分析

- 特許分析

- 規制分析

- 2023年~2024年の主要な会議とイベント

第6章 GaN半導体デバイス市場、ウエハサイズ別

- イントロダクション

- 2インチ

- 4インチ

- 6インチ以上

第7章 GaN半導体デバイス市場、タイプ別

- イントロダクション

- 光半導体

- パワー半導体

- 高周波半導体

第8章 GaN半導体デバイス市場、デバイス別

- イントロダクション

- ディスクリート半導体

- 集積半導体

第9章 GaN半導体デバイス市場、電圧範囲別

- イントロダクション

- 100V未満

- 100~500V

- 500V以上

第10章 GaN半導体デバイス市場、用途別

- イントロダクション

- 照明とレーザー

- パワードライブ

- 電源とインバータ

- 無線周波数

第11章 GaN半導体デバイス市場、業界別

- イントロダクション

- 消費者および企業

- 電気通信

- 自動車

- 産業用

- エネルギーと電力

- ヘルスケア

- 航空宇宙と防衛

第12章 GaN半導体デバイス市場、地域別

- イントロダクション

- 北米

- 欧州

- アジア太平洋

- その他の地域

第13章 競合情勢

- 概要

- 大手企業が採用した主な戦略

- 市場シェア分析、2022年

- 収益分析、2018~2022年

- 企業評価マトリックス、2022年

- 主要企業の競合ベンチマーキング

- スタートアップ/中小企業(SMES)の評価マトリックス、2022年

- スタートアップ/中小企業の競合ベンチマーキング

- 競争シナリオと動向

第14章 企業プロファイル

- イントロダクション

- 主要参入企業

- NEXGEN POWER SYSTEMS

- WOLFSPEED, INC.

- GAN SYSTEMS

- SUMITOMO ELECTRIC INDUSTRIES, LTD.

- INFINEON TECHNOLOGIES AG

- MACOM TECHNOLOGY SOLUTIONS HOLDINGS, INC.

- QORVO, INC.

- MITSUBISHI ELECTRIC GROUP

- EFFICIENT POWER CONVERSION CORPORATION

- ODYSSEY SEMICONDUCTOR TECHNOLOGIES, INC.

- ROHM CO., LTD.

- STMICROELECTRONICS N.V.

- NXP SEMICONDUCTORS N.V.

- その他の企業

- TRANSPHORM, INC.

- ANALOG DEVICES, INC.

- TEXAS INSTRUMENTS INCORPORATED

- NAVITAS SEMICONDUCTOR

- MICROCHIP TECHNOLOGY INCORPORATED

- POWDEC

- NORTHROP GRUMMAN CORPORATION

- SHINDENGEN ELECTRIC MANUFACTURING CO., LTD.

- TOSHIBA INFRASTRUCTURE SYSTEMS & SOLUTIONS CORPORATION

- RENESAS ELECTRONICS CORPORATION

- GALLIUM SEMICONDUCTOR

- GANPOWER

第15章 付録

The GaN semiconductor device market is projected to reach USD 28.3 billion by 2028 from USD 21.1 billion in 2023, at a CAGR of 6.1% from 2023 to 2028. The major factors driving the market growth of the GaN semiconductor device market include the growing adoption of GaN semiconductor devices in consumer & business enterpirses, increasing government-led schemes for boosting adoption of GaN semiconductor devices, ever changing demand for more compact sized systems, rising applications of GaN semiconductor devices in energy & power industry. Moreover, continuous technological advancement in GaN semiconductor devices and growing deployment of GaN semiconductor devices in automotive industry is expected to provide several growth opportunities for market players in the GaN semiconductor device market.

Consumer & Business Enterprises is expected to account for the largest market share in GaN semiconductor device market during the forecast period

Consumer electronics is one of the prominent growth-oriented end-user domains for GaN semiconductor devices, with notable income streams originating from the domain of GaN opto-semiconductor devices. The increasing integration of GaN semiconductor devices into laptops, displays and mobile devices is expected to majorly contribute to the market share of GaN semiconductor devices.

Integrated Semiconductor segment is expected to account for the highest CAGR in GaN semiconductor device market during the forecast period

Integrated GaN semiconductors include GaN MMICs and GaN amplifiers. These solutions entail the integration of GaN transistors with essential components like gate drivers, protection circuits, and temperature sensors within a unified package. This strategic integration offers many advantages, such as accelerated switching speeds, compact magnetics, and heightened power density.

North America is expected to account for the second- largest market share during the forecast period

The growing market for electric and hybrid electric vehicles (EVs and HEVs) significantly contributes to the market growth of the region. GaN semiconductor devices have revolutionized the entire electronic system landscape of these vehicles, as their integration delivers more compact systems that reduce the overall vehicle weight and enhance battery management. Key players in the GaN semiconductor device market in North America include GaN Systems (Canada), Wolfspeed, Inc. (US), Qorvo, Inc. (US), and Analog Devices (US).

The break-up of profile of primary participants in the GaN semiconductor device market-

- By Company Type: Tier 1 - 30%, Tier 2 - 50%, Tier 3 - 20%

- By Designation Type: C Level - 25%, Director Level - 35% , Others - 40%

- By Region Type: North America - 30%, Europe - 25%, Asia Pacific - 35%, Rest of the World (RoW) - 10%

The major players of GaN semiconductor device market are are Qorvo, Inc. (US), Wolfspeed, Inc. (US), Sumitomo Electric Industries, Ltd. (Japan), MACOM Technology Solutions Holdings, Inc. (US) and Infineon Technologies AG (Germany) among others.

Research Coverage

The report segments the GaN semiconductor device market and forecasts its size based on type, device, application, vertical, voltage range and region. The report also provides a comprehensive review of drivers, restraints, opportunities, and challenges influencing the market growth. The report also covers qualitative aspects in addition to the quantitative aspects of the market.

Reasons to buy the report:

The report will help the market leaders/new entrants in this market with information on the closest approximate revenues for the overall GaN semiconductor device market and related segments. This report will help stakeholders understand the competitive landscape and gain more insights to strengthen their position in the market and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of key drivers (growing adoption of GaN semiconductor devices in consumer & business enterpirses, increasing government-led schemes for boosting adoption of GaN semiconductor devices, ever changing demand for more compact sized systems, rising applications of GaN semiconductor devices in energy & power industry), restraints (High manufacturing cost and excellent efficacy of alternative technologies in high-voltage semiconductor applications), opportunities (continuous technological advancement in GaN semiconductor devices and growing deployment of GaN semiconductor devices in automotive industry), and challenges (Designing complexities associated with GaN semiconductor devices) influencing the growth of the GaN semiconductor device market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the GaN semiconductor device market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the GaN semiconductor device market across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the GaN semiconductor device market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and product offerings of leading players like are Qorvo, Inc. (US), Wolfspeed, Inc. (US), Sumitomo Electric Industries, Ltd. (Japan), MACOM Technology Solutions Holdings, Inc. (US) and Infineon Technologies AG (Germany)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 INCLUSIONS AND EXCLUSIONS

- 1.3.1 INCLUSIONS AND EXCLUSIONS: BY COMPANY

- 1.3.2 INCLUSIONS AND EXCLUSIONS: BY TYPE

- 1.3.3 INCLUSIONS AND EXCLUSIONS: BY DEVICE

- 1.3.4 INCLUSIONS AND EXCLUSIONS: BY WAFER SIZE

- 1.3.5 INCLUSIONS AND EXCLUSIONS: BY APPLICATION

- 1.3.6 INCLUSIONS AND EXCLUSIONS: BY VERTICAL

- 1.3.7 INCLUSIONS AND EXCLUSIONS: BY VOLTAGE RANGE

- 1.3.8 INCLUSIONS AND EXCLUSIONS: BY REGION

- 1.4 STUDY SCOPE

- 1.4.1 MARKETS COVERED

- FIGURE 1 GAN SEMICONDUCTOR DEVICE MARKET: SEGMENTATION

- 1.4.2 REGIONAL SCOPE

- 1.4.3 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 UNITS CONSIDERED

- 1.7 LIMITATIONS

- 1.8 STAKEHOLDERS

- 1.9 SUMMARY OF CHANGES

- 1.10 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH APPROACH

- FIGURE 2 GAN SEMICONDUCTOR DEVICE MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Major secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary interviews with experts

- 2.1.2.2 List of key primary interview participants

- 2.1.2.3 Breakdown of primaries

- 2.1.2.4 Key data from primary sources

- 2.1.3 SECONDARY AND PRIMARY RESEARCH

- 2.1.3.1 Key industry insights

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach to derive market size using bottom-up analysis

- FIGURE 3 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach to derive market size using top-down analysis

- FIGURE 4 TOP-DOWN APPROACH

- 2.2.1 BOTTOM-UP APPROACH

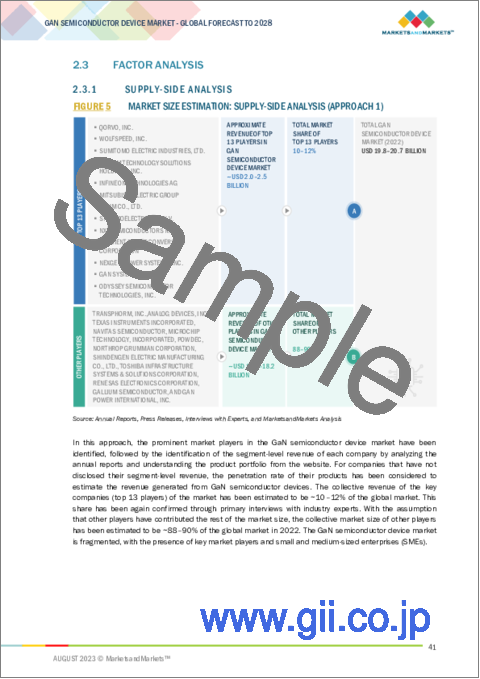

- 2.3 FACTOR ANALYSIS

- 2.3.1 SUPPLY-SIDE ANALYSIS

- FIGURE 5 MARKET SIZE ESTIMATION: SUPPLY-SIDE ANALYSIS (APPROACH 1)

- FIGURE 6 MARKET SIZE ESTIMATION: SUPPLY-SIDE ANALYSIS (APPROACH 2)

- 2.3.2 GROWTH FORECAST ASSUMPTIONS

- TABLE 1 GAN SEMICONDUCTOR DEVICE MARKET: GROWTH FORECAST ASSUMPTIONS

- 2.4 APPROACH TO ANALYZE RECESSION IMPACT ON GAN SEMICONDUCTOR DEVICE MARKET

- 2.5 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 7 DATA TRIANGULATION

- 2.6 RESEARCH ASSUMPTIONS

- 2.7 RISK ASSESSMENT

- TABLE 2 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- FIGURE 8 GAN SEMICONDUCTOR DEVICE MARKET: GROWTH PROJECTION

- FIGURE 9 POWER SEMICONDUCTOR SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 10 DISCRETE SEMICONDUCTOR SEGMENT TO ACCOUNT FOR LARGER MARKET SHARE IN 2028

- FIGURE 11 POWER DRIVES SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 12 ENERGY & POWER SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 13 MORE THAN 500 V SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 14 ASIA PACIFIC TO DOMINATE GAN SEMICONDUCTOR DEVICE MARKET DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN GAN SEMICONDUCTOR DEVICE MARKET

- FIGURE 15 GROWING ADOPTION OF GAN SEMICONDUCTOR DEVICES IN AUTOMOTIVE VERTICAL

- 4.2 GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE

- FIGURE 16 OPTO-SEMICONDUCTOR SEGMENT TO ACCOUNT FOR LARGEST SHARE OF GAN SEMICONDUCTOR DEVICE MARET IN 2028

- 4.3 GAN SEMICONDUCTOR DEVICE MARKET, BY DEVICE

- FIGURE 17 DISCRETE SEMICONDUCTOR SEGMENT TO DOMINATE GAN SEMICONDUCTOR DEVICE MARKET FROM 2023 TO 2028

- 4.4 GAN SEMICONDUCTOR DEVICE MARKET, BY APPLICATION

- FIGURE 18 LIGHTING & LASERS SEGMENT TO WITNESS SIGNIFICANT GROWTH IN GAN SEMICONDUCTOR DEVICE MARKET DURING FORECAST PERIOD

- 4.5 GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL

- FIGURE 19 CONSUMER & BUSINESS ENTERPRISES SEGMENT TO DOMINATE GAN SEMICONDUCTOR DEVICE MARKET DURING FORECAST PERIOD

- 4.6 GAN SEMICONDUCTOR DEVICE MARKET, BY VOLTAGE RANGE

- FIGURE 20 LESS THAN 100 V SEGMENT TO DOMINATE GAN SEMICONDUCTOR DEVICE MARKET BETWEEN 2023 AND 2028

- 4.7 ASIA PACIFIC GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE AND COUNTRY

- FIGURE 21 OPTO-SEMICONDUCTOR SEGMENT AND CHINA HELD LARGEST SHARES OF ASIA PACIFIC GAN SEMICONDUCTOR DEVICE MARKET IN 2022

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 22 GAN SEMICONDUCTOR DEVICE MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Growing adoption of GaN semiconductor devices in consumer & business enterprises

- 5.2.1.2 Rising applications of GaN semiconductor devices in energy & power vertical

- 5.2.1.3 Growing need for miniaturization in various industries

- 5.2.1.4 Increasing government-led schemes for boosting adoption of GaN semiconductor devices

- FIGURE 23 GAN SEMICONDUCTOR DEVICE MARKET: DRIVERS AND THEIR IMPACT

- 5.2.2 RESTRAINTS

- 5.2.2.1 High manufacturing cost

- 5.2.2.2 Excellent efficacy of alternative technologies in high-voltage semiconductor applications

- FIGURE 24 GAN SEMICONDUCTOR DEVICE MARKET: RESTRAINTS AND THEIR IMPACT

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increasing deployment of GaN semiconductor devices in automotive vertical

- FIGURE 25 VEHICLE PRODUCTION IN ASIA PACIFIC, 2019-2022

- 5.2.3.2 Technological advancements in GaN semiconductor devices

- FIGURE 26 GAN SEMICONDUCTOR DEVICE MARKET: OPPORTUNITIES AND THEIR IMPACT

- 5.2.4 CHALLENGES

- 5.2.4.1 Manufacturing and designing complexities associated with GaN semiconductor devices

- FIGURE 27 GAN SEMICONDUCTOR DEVICE MARKET: CHALLENGES AND THEIR IMPACT

- 5.3 VALUE CHAIN ANALYSIS

- FIGURE 28 GAN SEMICONDUCTOR DEVICE MARKET: VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- TABLE 3 GAN SEMICONDUCTOR DEVICE MARKET: ECOSYSTEM ANALYSIS

- FIGURE 29 GAN SEMICONDUCTOR DEVICE MARKET: ECOSYSTEM ANALYSIS

- 5.5 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 30 REVENUE SHIFT AND NEW REVENUE POCKETS FOR PLAYERS IN GAN SEMICONDUCTOR DEVICE MARKET

- 5.6 TECHNOLOGY ANALYSIS

- 5.6.1 VERTICAL GAN

- 5.6.1.1 Key applications

- TABLE 4 VERTICAL GAN MARKET POTENTIAL FOR 2022 AND 2028

- 5.6.1.2 Recent developments

- 5.6.1.2.1 Product launches

- 5.6.1.2 Recent developments

- 5.6.2 GAN-ON-SIC

- 5.6.3 GAN-ON-SI

- 5.6.4 INGAN

- 5.6.5 GAN-ON-DIAMOND

- 5.6.1 VERTICAL GAN

- 5.7 PRICING ANALYSIS

- 5.7.1 AVERAGE SELLING PRICE (ASP) OF GAN TRANSISTORS (GAN HEMTS) AND GAN AMPLIFIERS OFFERED BY FOUR KEY PLAYERS

- FIGURE 31 AVERAGE SELLING PRICE (ASP) OF GAN TRANSISTORS (GAN HEMTS) AND GAN AMPLIFIERS OFFERED BY FOUR KEY PLAYERS

- TABLE 5 AVERAGE SELLING PRICE (ASP) OF GAN TRANSISTORS (GAN HEMTS) AND GAN AMPLIFIERS OFFERED BY FOUR KEY PLAYERS

- 5.7.2 AVERAGE SELLING PRICE (ASP) TREND

- FIGURE 32 AVERAGE SELLING PRICE (ASP) TREND FOR GAN TRANSISTORS (GAN HEMTS) AND GAN AMPLIFIERS

- 5.8 PORTER'S FIVE FORCES ANALYSIS

- TABLE 6 GAN SEMICONDUCTOR DEVICE MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 33 GAN SEMICONDUCTOR DEVICE MARKET: PORTER'S FIVE FORCES ANALYSIS, 2022

- FIGURE 34 GAN SEMICONDUCTOR DEVICE MARKET: IMPACT OF PORTER'S FIVE FORCES, 2022

- 5.8.1 THREAT OF NEW ENTRANTS

- 5.8.2 THREAT OF SUBSTITUTES

- 5.8.3 BARGAINING POWER OF SUPPLIERS

- 5.8.4 BARGAINING POWER OF BUYERS

- 5.8.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.9 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.9.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 35 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR FOUR KEY APPLICATIONS

- TABLE 7 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR FOUR KEY APPLICATIONS

- 5.9.2 BUYING CRITERIA

- FIGURE 36 KEY BUYING CRITERIA FOR FOUR KEY APPLICATIONS OF GAN SEMICONDUCTOR DEVICES

- TABLE 8 KEY BUYING CRITERIA FOR FOUR KEY APPLICATIONS OF GAN SEMICONDUCTOR DEVICES

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 ORCHARD AUDIO INTEGRATED GAN SYSTEMS' GAN TRANSISTORS INTO STARKRIMSON STREAMER ULTRA TO ENHANCE AUDIO PERFORMANCE AND REDUCE SIZE

- 5.10.2 MAXLINEAR USED WOLFSPEED'S GAN-ON-SIC AMPLIFIERS TO INCREASE WIRELESS CAPACITY OF ULTRA-WIDEBAND LINEARIZATION SOLUTION

- 5.10.3 BRIGHTLOOP CONVERTERS DEPLOYED GAN SYSTEMS' GAN TRANSISTORS TO ENHANCE PERFORMANCE OF DCDC CONVERTERS

- 5.10.4 CORSAIR GAMING USED TRANSPHORM'S GAN FETS TO DELIVER HIGH POWER OUTPUT IN GAMING APPLICATIONS

- 5.11 TRADE ANALYSIS

- TABLE 9 IMPORT DATA FOR HS CODE 381800, BY COUNTRY, 2018-2022 (USD MILLION)

- FIGURE 37 IMPORT DATA FOR HS CODE 831800, 2018-2022

- TABLE 10 EXPORT DATA FOR HS CODE 381800, BY COUNTRY, 2018-2022 (USD MILLION)

- FIGURE 38 EXPORT DATA FOR HS CODE 381800, 2018-2022

- 5.12 PATENT ANALYSIS

- TABLE 11 PATENTS FILED BETWEEN JANUARY 2012 AND DECEMBER 2022

- FIGURE 39 NUMBER OF PATENTS GRANTED, 2012-2022

- FIGURE 40 TOP 10 COMPANIES WITH HIGHEST NUMBER OF PATENTS GRANTED

- TABLE 12 KEY PATENTS RELATED TO GAN SEMICONDUCTOR DEVICES

- 5.13 REGULATORY ANALYSIS

- 5.13.1 GLOBAL

- 5.13.2 GOVERNMENT REGULATIONS

- 5.13.2.1 Asia Pacific

- 5.13.2.2 North America

- 5.13.2.3 Europe

- 5.14 KEY CONFERENCES AND EVENTS, 2023-2024

- TABLE 13 GAN SEMICONDUCTOR DEVICE MARKET: LIST OF KEY CONFERENCES AND EVENTS

6 GAN SEMICONDUCTOR DEVICE MARKET, BY WAFER SIZE

- 6.1 INTRODUCTION

- 6.2 2 INCHES

- 6.3 4 INCHES

- 6.4 6 INCHES AND ABOVE

7 GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE

- 7.1 INTRODUCTION

- FIGURE 41 POWER SEMICONDUCTOR SEGMENT TO REGISTER HIGHEST CAGR IN GAN SEMICONDUCTOR DEVICE MARKET DURING FORECAST PERIOD

- TABLE 14 GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 15 GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 7.2 OPTO-SEMICONDUCTOR

- 7.2.1 INCREASING DEMAND FOR LEDS IN INDUSTRIAL AND AUTOMOTIVE VERTICALS

- TABLE 16 OPTO-SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 17 OPTO-SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 18 OPTO-SEMICONDUCTOR: NORTH AMERICA GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 19 OPTO-SEMICONDUCTOR: NORTH AMERICA GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 20 OPTO-SEMICONDUCTOR: EUROPE GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 21 OPTO-SEMICONDUCTOR: EUROPE GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 22 OPTO-SEMICONDUCTOR: ASIA PACIFIC GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 23 OPTO-SEMICONDUCTOR: ASIA PACIFIC GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 24 OPTO-SEMICONDUCTOR: ROW GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 25 OPTO-SEMICONDUCTOR: ROW GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 26 OPTO-SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 27 OPTO-SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.3 POWER SEMICONDUCTOR

- 7.3.1 GROWING DEMAND FOR HIGH-SPEED SWITCHING SYSTEMS

- TABLE 28 POWER SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 29 POWER SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 30 POWER SEMICONDUCTOR: NORTH AMERICA GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 31 POWER SEMICONDUCTOR: NORTH AMERICA GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 32 POWER SEMICONDUCTOR: EUROPE GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 33 POWER SEMICONDUCTOR: EUROPE GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 34 POWER SEMICONDUCTOR: ASIA PACIFIC GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 35 POWER SEMICONDUCTOR: ASIA PACIFIC GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 36 POWER SEMICONDUCTOR: ROW GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 37 POWER SEMICONDUCTOR: ROW GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 38 POWER SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 39 POWER SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 40 POWER SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 41 POWER SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 42 POWER SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY DEVICE, 2019-2022 (USD MILLION)

- TABLE 43 POWER SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY DEVICE, 2023-2028 (USD MILLION)

- TABLE 44 POWER SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY DEVICE, 2019-2022 (MILLION UNITS)

- TABLE 45 POWER SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY DEVICE, 2023-2028 (MILLION UNITS)

- 7.3.1.1 Discrete power semiconductor

- 7.3.1.2 Integrated power semiconductor

- 7.4 RF SEMICONDUCTOR

- 7.4.1 RISING NEED FOR HIGH-POWER SOLUTIONS IN VERY HIGH FREQUENCY (VHF), ULTRA-HIGH FREQUENCY (UHF), AND MICROWAVE BANDS

- TABLE 46 RF SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 47 RF SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 48 RF SEMICONDUCTOR: NORTH AMERICA GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 49 RF SEMICONDUCTOR: NORTH AMERICA GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 50 RF SEMICONDUCTOR: EUROPE GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 51 RF SEMICONDUCTOR: EUROPE GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 52 RF SEMICONDUCTOR: ASIA PACIFIC GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 53 RF SEMICONDUCTOR: ASIA PACIFIC GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 54 RF SEMICONDUCTOR: ROW GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 55 RF SEMICONDUCTOR: ROW GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 56 RF SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 57 RF SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 58 RF SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY DEVICE, 2019-2022 (USD MILLION)

- TABLE 59 RF SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY DEVICE, 2023-2028 (USD MILLION)

- TABLE 60 RF SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY DEVICE, 2019-2022 (MILLION UNITS)

- TABLE 61 RF SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY DEVICE, 2023-2028 (MILLION UNITS)

- 7.4.1.1 Discrete RF semiconductor

- 7.4.1.2 Integrated RF semiconductor

8 GAN SEMICONDUCTOR DEVICE MARKET, BY DEVICE

- 8.1 INTRODUCTION

- FIGURE 42 INTEGRATED SEMICONDUCTOR SEGMENT TO EXHIBIT HIGHER CAGR DURING FORECAST PERIOD

- TABLE 62 GAN SEMICONDUCTOR DEVICE MARKET, BY DEVICE, 2019-2022 (USD MILLION)

- TABLE 63 GAN SEMICONDUCTOR DEVICE MARKET, BY DEVICE, 2023-2028 (USD MILLION)

- 8.2 DISCRETE SEMICONDUCTOR

- TABLE 64 DISCRETE SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 65 DISCRETE SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 8.2.1 GAN TRANSISTOR

- 8.2.1.1 Increasing adoption of GaN High Electron Mobility Transistors (HEMTs) in 5G wireless and satellite communication and radar systems

- 8.2.2 GAN DIODE

- 8.2.2.1 Growing use in power electronics

- 8.3 INTEGRATED SEMICONDUCTOR

- TABLE 66 INTEGRATED SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 67 INTEGRATED SEMICONDUCTOR: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 8.3.1 GAN MONOLITHIC MICROWAVE INTEGRATED CIRCUIT (MMIC)

- 8.3.1.1 Increasing demand for advanced communication systems

- 8.3.2 GAN AMPLIFIER

- 8.3.2.1 Rising need for high-frequency and high-power capabilities in satellite communication

9 GAN SEMICONDUCTOR DEVICE MARKET, BY VOLTAGE RANGE

- 9.1 INTRODUCTION

- FIGURE 43 MORE THAN 500 V SEGMENT TO EXHIBIT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 68 GAN SEMICONDUCTOR DEVICE MARKET, BY VOLTAGE RANGE, 2019-2022 (USD MILLION)

- TABLE 69 GAN SEMICONDUCTOR DEVICE MARKET, BY VOLTAGE RANGE, 2023-2028 (USD MILLION)

- 9.2 LESS THAN 100 V

- 9.2.1 INCREASING NEED FOR HIGH SWITCHING SPEED AND POWER EFFICIENCY IN CHARGERS AND LAPTOPS

- 9.3 100-500 V

- 9.3.1 GROWING REQUIREMENT FOR ELEVATED VOLTAGE LEVELS IN VARIOUS APPLICATIONS

- 9.4 MORE THAN 500 V

- 9.4.1 RISING NEED FOR EFFICIENCY IN HIGH-VOLTAGE POWER DRIVE APPLICATIONS

10 GAN SEMICONDUCTOR DEVICE MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- FIGURE 44 POWER DRIVES SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 70 GAN SEMICONDUCTOR DEVICE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 71 GAN SEMICONDUCTOR DEVICE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 10.2 LIGHTING AND LASERS

- 10.2.1 INCREASING DEMAND FOR HIGH-POWER LASER SYSTEMS

- 10.3 POWER DRIVES

- FIGURE 45 EV DRIVES SEGMENT TO REGISTER HIGHEST CAGR IN GAN SEMICONDUCTOR DEVICE MARKET FOR POWER DRIVES DURING FORECAST PERIOD

- TABLE 72 POWER DRIVES: GAN SEMICONDUCTOR DEVICE MARKET, BY APPLICATION, 2019-2022 (USD THOUSAND)

- TABLE 73 POWER DRIVES: GAN SEMICONDUCTOR DEVICE MARKET, BY APPLICATION, 2023-2028 (USD THOUSAND)

- 10.3.1 LIGHT DETECTION AND RANGING (LIDAR)

- 10.3.1.1 Integration of GaN semiconductor devices into LiDAR systems to deliver rapid switching efficiency

- 10.3.2 INDUSTRIAL DRIVES

- 10.3.2.1 Growing demand for GaN-based motor drives to enhance efficiency and performance within minimal timeframe

- 10.3.3 EV DRIVES

- 10.3.3.1 Increasing demand for GaN-based motor drives to reduce power conversion losses

- 10.4 SUPPLIES AND INVERTERS

- TABLE 74 SUPPLIES AND INVERTERS: GAN SEMICONDUCTOR DEVICE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 75 SUPPLIES AND INVERTERS: GAN SEMICONDUCTOR DEVICE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 10.4.1 SWITCH-MODE POWER SUPPLIES

- 10.4.1.1 Implementation of GaN-based switch-mode power supplies (SMPSs) in refrigerators, freezers, and air conditioners

- 10.4.2 INVERTERS

- 10.4.2.1 Rising use of PV solar inverters and renewable energy solutions

- 10.4.3 WIRELESS CHARGING

- 10.4.3.1 Growing use of wireless chargers to enhance efficiency of wireless power transmission units

- 10.4.4 EV CHARGING

- 10.4.4.1 Increasing deployment of GaN semiconductor devices in EV charging infrastructure

- 10.5 RADIO FREQUENCY

- TABLE 76 RADIO FREQUENCY: GAN SEMICONDUCTOR DEVICE MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 77 RADIO FREQUENCY: GAN SEMICONDUCTOR DEVICE MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 10.5.1 RADIO FREQUENCY FRONT-END MODULES

- 10.5.1.1 Deployment of GaN semiconductor devices in 5G base stations and terminals

- 10.5.2 REPEATERS/BOOSTERS/DASS

- 10.5.2.1 Increasing demand for GaN semiconductor devices to enhance transmission of radio waves

- 10.5.3 RADARS AND SATELLITES

- 10.5.3.1 Efficient power conversion and switching capabilities at high-frequency bands

11 GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL

- 11.1 INTRODUCTION

- FIGURE 46 ENERGY & POWER SEGMENT TO REGISTER HIGHEST CAGR IN GAN SEMICONDUCTOR MARKET DURING FORECAST PERIOD

- TABLE 78 GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 79 GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- 11.2 CONSUMER & BUSINESS ENTERPRISES

- 11.2.1 INTEGRATION OF GAN SEMICONDUCTOR DEVICES INTO LAPTOPS, DISPLAYS, AND MOBILE DEVICES

- TABLE 80 CONSUMER & BUSINESS ENTERPRISES: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 81 CONSUMER & BUSINESS ENTERPRISES: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 82 CONSUMER & BUSINESS ENTERPRISES: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 83 CONSUMER & BUSINESS ENTERPRISES: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2023-2028 (USD MILLION)

- 11.3 TELECOMMUNICATIONS

- 11.3.1 GROWING NEED FOR FAST DATA TRANSMISSION, IMPROVED SIGNAL QUALITY, AND REDUCED POWER CONSUMPTION

- TABLE 84 TELECOMMUNICATIONS: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 85 TELECOMMUNICATIONS: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 86 TELECOMMUNICATIONS: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 87 TELECOMMUNICATIONS: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2023-2028 (USD MILLION)

- 11.4 AUTOMOTIVE

- 11.4.1 RISING DEPLOYMENT OF GAN SEMICONDUCTOR DEVICES IN ELECTRIC AND HYBRID VEHICLES

- TABLE 88 AUTOMOTIVE: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 89 AUTOMOTIVE: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 90 AUTOMOTIVE: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 91 AUTOMOTIVE: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2023-2028 (USD MILLION)

- 11.5 INDUSTRIAL

- 11.5.1 GROWING USE OF GAN SEMICONDUCTOR DEVICES IN POWER DISTRIBUTION SYSTEMS TO DELIVER EFFICIENT OPERATIONS

- TABLE 92 INDUSTRIAL: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 93 INDUSTRIAL: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 94 INDUSTRIAL: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 95 GAN SEMICONDUCTOR DEVICE MARKET FOR INDUSTRIAL, BY REGION, 2023-2028 (USD MILLION)

- 11.6 ENERGY & POWER

- 11.6.1 INTEGRATION OF GAN SEMICONDUCTOR DEVICES INTO ELECTRONIC SYSTEMS TO HARNESS PERFORMANCE

- FIGURE 47 RF SEMICONDUCTOR SEGMENT TO HOLD LARGER SHARE OF GAN SEMICONDUCTOR DEVICE MARKET FOR ENERGY & POWER IN 2028

- TABLE 96 ENERGY & POWER: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 97 ENERGY & POWER: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 98 ENERGY & POWER: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 99 ENERGY & POWER: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2023-2028 (USD MILLION)

- 11.7 HEALTHCARE

- 11.7.1 INSTALLATION OF GAN SEMICONDUCTOR DEVICES IN WIRELESS POWER CHARGING SYSTEMS AND PRECISION SURGICAL ROBOTS

- TABLE 100 HEALTHCARE: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 101 HEALTHCARE: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 102 HEALTHCARE: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 103 HEALTHCARE: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2023-2028 (USD MILLION)

- 11.8 AEROSPACE & DEFENSE

- 11.8.1 INCREASING USE OF GAN-BASED SOLUTIONS IN RADAR SYSTEMS AND MILITARY RF TECHNOLOGY

- TABLE 104 AEROSPACE & DEFENSE: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 105 AEROSPACE & DEFENSE: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 106 AEROSPACE & DEFENSE: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 107 AEROSPACE & DEFENSE: GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2023-2028 (USD MILLION)

12 GAN SEMICONDUCTOR DEVICE MARKET, BY REGION

- 12.1 INTRODUCTION

- FIGURE 48 SOUTH KOREA GAN SEMICONDUCTOR DEVICE MARKET TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 108 GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 109 GAN SEMICONDUCTOR DEVICE MARKET, BY REGION, 2023-2028 (USD MILLION)

- 12.2 NORTH AMERICA

- FIGURE 49 NORTH AMERICA: SNAPSHOT OF GAN SEMICONDUCTOR DEVICE MARKET

- TABLE 110 NORTH AMERICA: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 111 NORTH AMERICA: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 112 NORTH AMERICA: GAN SEMICONDUCTOR DEVICE MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 113 NORTH AMERICA: GAN SEMICONDUCTOR DEVICE MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 114 NORTH AMERICA: GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 115 NORTH AMERICA: GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- 12.2.1 NORTH AMERICA: RECESSION IMPACT

- 12.2.2 US

- 12.2.2.1 Growing demand for electric and hybrid electric vehicles and electric vehicle charging stations

- 12.2.3 CANADA

- 12.2.3.1 Increasing demand for energy and power generators

- 12.2.4 MEXICO

- 12.2.4.1 Rising demand for cellular base stations

- 12.3 EUROPE

- FIGURE 50 EUROPE: SNAPSHOT OF GAN SEMICONDUCTOR DEVICE MARKET

- TABLE 116 EUROPE: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 117 EUROPE: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 118 EUROPE: GAN SEMICONDUCTOR DEVICE MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 119 EUROPE: GAN SEMICONDUCTOR DEVICE MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 120 EUROPE: GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 121 EUROPE: GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- 12.3.1 EUROPE: RECESSION IMPACT

- 12.3.2 UK

- 12.3.2.1 Increasing government-led initiatives and research and development

- 12.3.3 GERMANY

- 12.3.3.1 Rising focus on infrastructure development

- 12.3.4 FRANCE

- 12.3.4.1 Increasing demand for GaN transistors and GaN power amplifiers in major industries and sectors

- 12.3.5 REST OF EUROPE

- 12.4 ASIA PACIFIC

- FIGURE 51 ASIA PACIFIC: SNAPSHOT OF GAN SEMICONDUCTOR DEVICE MARKET

- TABLE 122 ASIA PACIFIC: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 123 ASIA PACIFIC: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 124 ASIA PACIFIC: GAN SEMICONDUCTOR DEVICE MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 125 ASIA PACIFIC: GAN SEMICONDUCTOR DEVICE MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 126 ASIA PACIFIC: GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 127 ASIA PACIFIC: GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- 12.4.1 ASIA PACIFIC: RECESSION IMPACT

- 12.4.2 CHINA

- 12.4.2.1 Growing adoption of GaN semiconductor devices in electric vehicle (EV) industry

- 12.4.3 JAPAN

- 12.4.3.1 Large presence of semiconductor manufacturing companies

- 12.4.4 SOUTH KOREA

- 12.4.4.1 Government-led initiatives for innovation and industrial development

- 12.4.5 REST OF ASIA PACIFIC

- 12.5 ROW

- TABLE 128 ROW: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 129 ROW: GAN SEMICONDUCTOR DEVICE MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 130 ROW: GAN SEMICONDUCTOR DEVICE MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 131 ROW: GAN SEMICONDUCTOR DEVICE MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 132 ROW: GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2019-2022 (USD MILLION)

- TABLE 133 ROW: GAN SEMICONDUCTOR DEVICE MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- 12.5.1 ROW: RECESSION IMPACT

- 12.5.2 MIDDLE EAST & AFRICA

- 12.5.2.1 Rising focus on development of telecommunications and power industries

- 12.5.3 SOUTH AMERICA

- 12.5.3.1 Increasing use of advanced technologies in telecommunications industry

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY STRATEGIES ADOPTED BY MAJOR PLAYERS

- TABLE 134 GAN SEMICONDUCTOR DEVICE MARKET: KEY STRATEGIES ADOPTED BY MAJOR PLAYERS

- FIGURE 52 COMPANIES ADOPTED ACQUISITIONS AS KEY GROWTH STRATEGY FROM 2021 TO 2023

- 13.2.1 ORGANIC/INORGANIC GROWTH STRATEGIES

- 13.2.2 PRODUCT PORTFOLIO

- 13.2.3 GEOGRAPHICAL PRESENCE

- 13.2.4 MANUFACTURING FOOTPRINT

- 13.3 MARKET SHARE ANALYSIS, 2022

- TABLE 135 GAN SEMICONDUCTOR DEVICE MARKET: DEGREE OF COMPETITION

- 13.4 REVENUE ANALYSIS, 2018-2022

- FIGURE 53 REVENUE ANALYSIS OF TOP FIVE COMPANIES, 2018-2022 (USD BILLION)

- 13.5 COMPANY EVALUATION MATRIX, 2022

- 13.5.1 STARS

- 13.5.2 EMERGING LEADERS

- 13.5.3 PERVASIVE PLAYERS

- 13.5.4 PARTICIPANTS

- FIGURE 54 GAN SEMICONDUCTOR DEVICE MARKET (GLOBAL): COMPANY EVALUATION MATRIX, 2022

- 13.6 COMPETITIVE BENCHMARKING OF KEY PLAYERS

- TABLE 136 COMPANY FOOTPRINT

- TABLE 137 DEVICE: COMPANY FOOTPRINT

- TABLE 138 APPLICATION: COMPANY FOOTPRINT

- TABLE 139 REGION: COMPANY FOOTPRINT

- 13.7 STARTUPS/SMALL AND MEDIUM-SIZED ENTERPRISES (SMES) EVALUATION MATRIX, 2022

- 13.7.1 PROGRESSIVE COMPANIES

- 13.7.2 RESPONSIVE COMPANIES

- 13.7.3 DYNAMIC COMPANIES

- 13.7.4 STARTING BLOCKS

- FIGURE 55 GAN SEMICONDUCTOR DEVICE MARKET: STARTUPS/SMES EVALUATION MATRIX, 2022

- 13.8 COMPETITIVE BENCHMARKING OF STARTUPS/SMES

- TABLE 140 GAN SEMICONDUCTOR DEVICE MARKET: LIST OF KEY STARTUPS/SMES

- TABLE 141 DEVICE: STARTUPS/SMES FOOTPRINT

- TABLE 142 APPLICATION: STARTUPS/SMES FOOTPRINT

- TABLE 143 REGION: STARTUPS/SMES FOOTPRINT

- 13.9 COMPETITIVE SCENARIOS AND TRENDS

- 13.9.1 PRODUCT LAUNCHES

- TABLE 144 GAN SEMICONDUCTOR DEVICE MARKET: PRODUCT LAUNCHES, 2020-2023

- 13.9.2 DEALS

- TABLE 145 GAN SEMICONDUCTOR DEVICE MARKET: DEALS, 2021-2023

- 13.9.3 OTHERS

- TABLE 146 GAN SEMICONDUCTOR DEVICE MARKET: OTHERS, 2020-2023

14 COMPANY PROFILES

(Business Overview, Products Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats))**

- 14.1 INTRODUCTION

- 14.2 KEY PLAYERS

- 14.2.1 NEXGEN POWER SYSTEMS

- TABLE 147 NEXGEN POWER SYSTEMS: COMPANY OVERVIEW

- TABLE 148 NEXGEN POWER SYSTEMS: PRODUCTS OFFERED

- TABLE 149 NEXGEN POWER SYSTEMS: PRODUCT LAUNCHES

- 14.2.2 WOLFSPEED, INC.

- TABLE 150 WOLFSPEED, INC.: COMPANY OVERVIEW

- FIGURE 56 WOLFSPEED, INC.: COMPANY SNAPSHOT

- TABLE 151 WOLFSPEED, INC.: PRODUCTS OFFERED

- TABLE 152 WOLFSPEED, INC.: PRODUCT LAUNCHES

- TABLE 153 WOLFSPEED, INC.: DEALS

- 14.2.3 GAN SYSTEMS

- TABLE 154 GAN SYSTEMS: COMPANY OVERVIEW

- TABLE 155 GAN SYSTEMS: PRODUCTS OFFERED

- TABLE 156 GAN SYSTEMS: PRODUCT LAUNCHES

- TABLE 157 GAN SYSTEMS: DEALS

- TABLE 158 GAN SYSTEMS: OTHERS

- 14.2.4 SUMITOMO ELECTRIC INDUSTRIES, LTD.

- TABLE 159 SUMITOMO ELECTRIC INDUSTRIES, LTD.: COMPANY OVERVIEW

- FIGURE 57 SUMITOMO ELECTRIC INDUSTRIES, LTD.: COMPANY SNAPSHOT

- TABLE 160 SUMITOMO ELECTRIC INDUSTRIES, LTD.: PRODUCTS OFFERED

- TABLE 161 SUMITOMO ELECTRIC INDUSTRIES, LTD.: PRODUCT LAUNCHES

- 14.2.5 INFINEON TECHNOLOGIES AG

- TABLE 162 INFINEON TECHNOLOGIES AG: COMPANY OVERVIEW

- FIGURE 58 INFINEON TECHNOLOGIES AG: COMPANY SNAPSHOT

- TABLE 163 INFINEON TECHNOLOGIES AG: PRODUCTS OFFERED

- TABLE 164 INFINEON TECHNOLOGIES AG: DEALS

- TABLE 165 INFINEON TECHNOLOGIES AG: OTHERS

- 14.2.6 MACOM TECHNOLOGY SOLUTIONS HOLDINGS, INC.

- TABLE 166 MACOM TECHNOLOGY SOLUTIONS HOLDINGS, INC.: COMPANY OVERVIEW

- FIGURE 59 MACOM TECHNOLOGY SOLUTIONS HOLDINGS, INC.: COMPANY SNAPSHOT

- TABLE 167 MACOM TECHNOLOGY SOLUTIONS HOLDINGS, INC.: PRODUCTS OFFERED

- TABLE 168 MACOM TECHNOLOGY SOLUTIONS HOLDINGS, INC.: PRODUCT LAUNCHES

- TABLE 169 MACOM TECHNOLOGY SOLUTIONS HOLDINGS, INC.: DEALS

- TABLE 170 MACOM TECHNOLOGY SOLUTIONS HOLDINGS, INC.: OTHERS

- 14.2.7 QORVO, INC.

- TABLE 171 QORVO, INC.: COMPANY OVERVIEW

- FIGURE 60 QORVO, INC.: COMPANY SNAPSHOT

- TABLE 172 QORVO, INC.: PRODUCTS OFFERED

- TABLE 173 QORVO, INC.: PRODUCT LAUNCHES

- 14.2.8 MITSUBISHI ELECTRIC GROUP

- TABLE 174 MITSUBISHI ELECTRIC GROUP: COMPANY OVERVIEW

- FIGURE 61 MITSUBISHI ELECTRIC GROUP: COMPANY SNAPSHOT

- TABLE 175 MITSUBISHI ELECTRIC GROUP: PRODUCTS OFFERED

- TABLE 176 MITSUBISHI ELECTRIC CORPORATION: PRODUCT LAUNCHES

- 14.2.9 EFFICIENT POWER CONVERSION CORPORATION

- TABLE 177 EFFICIENT POWER CONVERSION CORPORATION: COMPANY OVERVIEW

- TABLE 178 EFFICIENT POWER CONVERSION CORPORATION: PRODUCTS OFFERED

- TABLE 179 EFFICIENT POWER CONVERSION CORPORATION: PRODUCT LAUNCHES

- TABLE 180 EFFICIENT POWER CONVERSION: DEALS

- 14.2.10 ODYSSEY SEMICONDUCTOR TECHNOLOGIES, INC.

- TABLE 181 ODYSSEY SEMICONDUCTOR TECHNOLOGIES, INC.: COMPANY OVERVIEW

- FIGURE 62 ODYSSEY SEMICONDUCTOR TECHNOLOGIES, INC.: COMPANY SNAPSHOT

- TABLE 182 ODYSSEY SEMICONDUCTOR TECHNOLOGIES, INC.: PRODUCTS OFFERED

- TABLE 183 ODYSSEY SEMICONDUCTOR TECHNOLOGIES, INC.: PRODUCT LAUNCHES

- 14.2.11 ROHM CO., LTD.

- TABLE 184 ROHM CO., LTD.: COMPANY OVERVIEW

- FIGURE 63 ROHM CO., LTD.: COMPANY SNAPSHOT

- TABLE 185 ROHM CO., LTD.: PRODUCTS OFFERED

- TABLE 186 ROHM CO., LTD.: PRODUCT LAUNCHES

- 14.2.12 STMICROELECTRONICS N.V.

- TABLE 187 STMICROELECTRONICS N.V.: COMPANY OVERVIEW

- FIGURE 64 STMICROELECTRONICS N.V.: COMPANY SNAPSHOT

- TABLE 188 STMICROELECTRONICS N.V.: PRODUCTS OFFERED

- TABLE 189 STMICROELECTRONICS N.V.: PRODUCT LAUNCHES

- TABLE 190 STMICROELECTRONICS N.V.: DEALS

- 14.2.13 NXP SEMICONDUCTORS N.V.

- TABLE 191 NXP SEMICONDUCTORS N.V.: COMPANY OVERVIEW

- FIGURE 65 NXP SEMICONDUCTORS N.V.: COMPANY SNAPSHOT

- TABLE 192 NXP SEMICONDUCTORS N.V.: PRODUCTS OFFERED

- TABLE 193 NXP SEMICONDUCTORS N.V.: PRODUCT LAUNCHES

- TABLE 194 NXP SEMICONDUCTORS N.V.: OTHERS

- 14.3 OTHER PLAYERS

- 14.3.1 TRANSPHORM, INC.

- 14.3.2 ANALOG DEVICES, INC.

- 14.3.3 TEXAS INSTRUMENTS INCORPORATED

- 14.3.4 NAVITAS SEMICONDUCTOR

- 14.3.5 MICROCHIP TECHNOLOGY INCORPORATED

- 14.3.6 POWDEC

- 14.3.7 NORTHROP GRUMMAN CORPORATION

- 14.3.8 SHINDENGEN ELECTRIC MANUFACTURING CO., LTD.

- 14.3.9 TOSHIBA INFRASTRUCTURE SYSTEMS & SOLUTIONS CORPORATION

- 14.3.10 RENESAS ELECTRONICS CORPORATION

- 14.3.11 GALLIUM SEMICONDUCTOR

- 14.3.12 GANPOWER

- *Details on Business Overview, Products Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats) might not be captured in case of unlisted companies.

15 APPENDIX

- 15.1 INSIGHTS FROM INDUSTRY EXPERTS

- 15.2 DISCUSSION GUIDE

- 15.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.4 CUSTOMIZATION OPTIONS

- 15.5 RELATED REPORTS

- 15.6 AUTHOR DETAILS