ヘルスケアアナリティクスの世界市場:コンポーネント別、展開モデル別、タイプ別、用途別、エンドユーザー別、地域別 - 2030年までの予測

Healthcare Analytics Market by Type, Application (Claim, RCM, Fraud, Precision Health, RWE, Imaging, Supply Chain, Workforce, Population Health), End User (Payer, Hospital, ACO, ASC), AI, Market Insights, Trends - Forecast to 2030- 発行日

- ページ情報

- 英文 454 Pages

- 納期

-

即納可能

営業時間内にお支払方法などの確認が取れ次第、Eメールにて納品となります。営業時間: 9:00am - 6:00pm (土日祝除く)。

- 商品コード

- 2057474

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

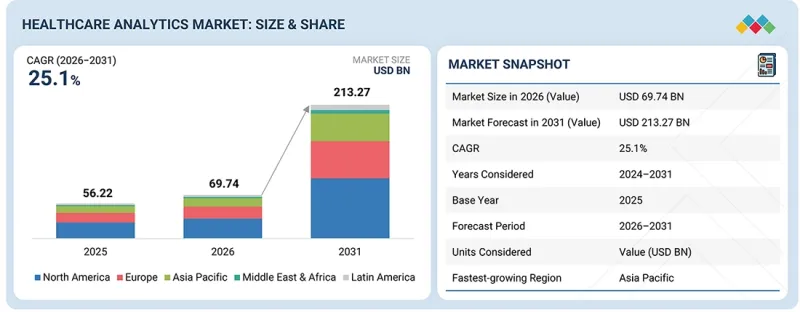

ヘルスケアアナリティクスの市場規模は、2025年の555億2,000万米ドルから2030年までに1,666億5,000万米ドルへと成長し、予測期間中のCAGRは24.6%になると見込まれています。

電子カルテ(EHR)の導入が、ヘルスケアアナリティクス市場の成長を後押ししています。北米では、開業医や連邦政府管轄外の急性期病院がEHRシステムを導入しています。

| 調査範囲 | |

|---|---|

| 調査対象期間 | 2024年~2030年 |

| 基準年 | 2024年 |

| 予測期間 | 2025年~2030年 |

| 対象単位 | 金額(10億米ドル) |

| セグメント | コンポーネント別、展開モデル別、タイプ別、用途別、エンドユーザー別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、ラテンアメリカ、中東・アフリカ。 |

「経済・臨床保健のための医療情報技術法(HITECH法)」を通じて、電子健康記録(EHR)システムを支援するための政府によるインセンティブが提供されています。この市場を牽引する要因としては、人工知能の進歩、価値に基づく医療システム、実世界データに加え、医療保険者、医療提供者、ライフサイエンス企業、および急性期後の医療機関によるヘルスケアアナリティクスサービスへの関心などが挙げられます。

「用途別では、予測期間中に臨床分析セグメントが最も高い成長率を示すと予想されます。」

用途別に見ると、ヘルスケアアナリティクス市場は、財務分析、臨床分析、業務・管理分析、および人口健康分析に区分されます。臨床分析セグメントは、AIを活用した臨床意思決定支援、予測リスクモデリング、およびリアルタイムの患者インサイトの採用拡大に牽引され、予測期間中に最も高い成長率を示すと見込まれています。これらは、ケア成果の向上、再入院の削減、および医療提供者や医療システム全体における価値に基づくケアの取り組みを支援することを目的としています。

構成要素別では、予測期間中にサービスセグメントが最も高い成長率を示すと見込まれています。」

構成要素別に見ると、ヘルスケアアナリティクス市場はソフトウェアとサービスに分類されます。予測期間中、臨床アナリティクスセグメントが最も高い成長率を示すと見込まれています。これは、医療機関が相互運用性、規制順守、および価値実現までの時間短縮を確保しつつ、複雑なAIおよびクラウドベースのアナリティクスプラットフォームを導入しようとする中で、実装、システム統合、データ管理、および高度なアナリティクスコンサルティングに対する需要が高まっていることが要因です。

「APAC地域は、予測期間中に最も高いCAGRを記録すると推定されています。」

ヘルスケアアナリティクス市場は、北米、欧州、アジア太平洋、ラテンアメリカ、中東・アフリカに分類されます。アジア太平洋地域のヘルスケアアナリティクス市場は、予測期間中に最も高いCAGRを記録すると見込まれています。これは、医療提供者や保険者における電子健康記録(EHR)の急速な普及、クラウドネイティブな導入、およびAI/MLの採用が牽引しています。政府主導のデジタルヘルスプログラムやデータ相互運用性基準の改善に支えられ、人口健康分析、実世界データ(REW)、予測モデリングの利用が増加しており、中国、インド、日本、東南アジア全域で大規模な分析導入が加速しています。

Merative(米国)、Optum, Inc.(米国)、SAS Institute Inc.(米国)、Oracle(米国)、Citiustech Inc(米国)は、ヘルスケアアナリティクス市場の主要企業の一部です。

本調査では、ヘルスケアアナリティクス市場におけるこれらの主要企業について、企業プロファイル、最近の動向、および主要な市場戦略を含む詳細な競合分析を行っています。

調査範囲

当レポートは、ヘルスケアアナリティクス市場を分析しています。コンポーネント、タイプ、用途、エンドユーザー、地域に基づいて、各市場セグメントの市場規模と将来の成長可能性を推定することを目的としています。また、当レポートでは、この市場の主要企業について、企業プロファイル、製品ラインナップ、最近の動向、主要な市場戦略とともに、競合分析も提供しています。

当レポートを購入する理由

当レポートは、ヘルスケアアナリティクス市場およびそのサブセグメントの売上高に関する最も正確な推計値に関する情報を提供することで、この市場の市場リーダーや新規参入企業を支援します。当レポートは、利害関係者が競合情勢を理解し、自社のビジネスをより良い位置に据え、適切な市場参入戦略を策定するためのさらなる洞察を得るのに役立ちます。また、当レポートは利害関係者が市場の動向を把握するのを助け、主要な市場促進要因、抑制要因、課題、および機会に関する情報を提供します。

当レポートでは、以下のポイントに関する洞察を提供します:

- 主要な促進要因(電子健康記録(EHR)導入に向けた政府の好意的な取り組み、スタートアップへのベンチャーキャピタル投資の増加、医療費削減の必要性、実世界データ(REW)への注目の高まり、遠隔医療および遠隔患者モニタリングの台頭、規制遵守への注目の高まり)、制約要因(分析ソリューションの高コスト、データ漏洩に対する懸念の高まり)、機会(価値ベース医療への注目の高まり、医療分野における分析の活用拡大、患者レジストリの増加、ソーシャルメディアおよびデジタルヘルス技術の台頭)、ならびに課題(不正確かつ一貫性のないデータに関する懸念、発展途上国におけるヘルスケアアナリティクスソリューション導入への消極性、医療記録の維持管理の不備、熟練人材の不足)について、ヘルスケアアナリティクス市場の成長に影響を与える要因として分析しています。

- 製品開発・イノベーション:ヘルスケアアナリティクス市場における今後の技術、研究開発活動、および新製品・サービスの発売に関する詳細な洞察

- 市場開発:収益性の高い市場に関する包括的な情報。当レポートでは、様々な地域にわたるヘルスケアアナリティクス市場を分析しています。

- 市場の多様化:ヘルスケアアナリティクス市場における新製品・サービス、未開拓地域、最近の動向、および投資に関する網羅的な情報

- 競合分析:Merative(米国)、Optum, Inc.(米国)、SAS Institute Inc.(米国)、Oracle(米国)、Citiustech Inc(米国)、Inovalon(米国)、Mckesson Corporation(米国)、MedeAnalytics, Inc.(米国)、Cotiviti, Inc.(米国)、Exlservice Holdings, Inc.(米国)、Wipro(インド)など、ヘルスケアアナリティクス市場における主要参入企業について、市場シェア、成長戦略、サービス提供内容に関する詳細な評価を行います

よくあるご質問

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

第3章 重要考察

第4章 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- アンメットニーズと未開拓分野

- 相互接続された市場と異業種間の機会

- ティア1/2/3企業による戦略的な動き

第5章 業界動向

- ポーターの5つの競争要因分析

- マクロ経済指標

- バリューチェーン分析

- エコシステム分析

- 価格分析

- 2026年~2027年の主な会議およびイベント

- 顧客ビジネスに影響を与える動向/混乱

- 投資と資金調達のシナリオ

- 事例研究分析

- 2025年米国関税の影響- ヘルスケアアナリティクス市場

第6章 技術進歩、AIによる影響、特許、イノベーション、そして将来の応用

- 技術分析

- 技術/製品ロードマップ

- 特許分析

- 将来の応用

- AI/生成AIがヘルスケアアナリティクス市場に与える影響

第7章 規制状況

- 地域規制および遵守事項

- 政府規制

- 規制機関、政府機関、その他の組織

- 業界標準

第8章 顧客情勢と購買行動

- 意思決定プロセス

- 購買プロセスにおける主要な利害関係者とその評価基準

- 導入における障壁と内部課題

- 最終用途産業におけるアンメットニーズ

- 市場収益性

第9章 ヘルスケアアナリティクス市場(コンポーネント別)

- サービス

- ソフトウェア

第10章 ヘルスケアアナリティクス市場(展開モデル別)

- オンプレミス

- クラウドベース

第11章 ヘルスケアアナリティクス市場(タイプ別)

- 記述分析

- 予測分析

- 処方分析

- 診断分析

第12章 ヘルスケアアナリティクス市場(用途別)

- 財務分析

- 臨床分析

- 業務・管理分析

- 人口健康分析

- 患者の診療過程とエンゲージメント分析

第13章 ヘルスケアアナリティクス市場(エンドユーザー別)

- 医療従事者

- 医療費支払者

- 薬局

- その他

第14章 ヘルスケアアナリティクス市場(地域別)

- 北米

- 北米のマクロ経済見通し

- 米国

- カナダ

- 欧州

- 欧州のマクロ経済見通し

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他

- アジア太平洋

- アジア太平洋のマクロ経済見通し

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- その他

- ラテンアメリカ

- ラテンアメリカのマクロ経済見通し

- ブラジル

- メキシコ

- その他

- 中東・アフリカ

- 中東・アフリカのマクロ経済見通し

- GCC諸国

- サウジアラビア

- アラブ首長国連邦

- その他のGCC諸国

- 南アフリカ

- その他

第15章 競合情勢

- 主要参入企業の競争戦略/強み、2023年~2026年

- 収益分析、2021年~2025年

- 市場シェア分析、2025年

- ブランド/ソフトウェア比較

- 企業評価マトリックス:主要企業、2025年

- 企業評価マトリックス:スタートアップ/中小企業、2025年

- 企業評価と財務指標

- 競合シナリオ

第16章 企業プロファイル

- 主要参入企業

- MERATIVE

- SAS INSTITUTE INC.

- OPTUM, INC.

- ORACLE

- HEALTH CATALYST

- EXLSERVICE HOLDINGS, INC.

- VERADIGM LLC

- CITIUSTECH INC.

- CVS HEALTH

- INOVALON

- MCKESSON CORPORATION

- MEDEANALYTICS, INC.

- COTIVITI, INC.

- DATAVANT, INC.

- DEFINITIVE HEALTHCARE, LLC

- KOMODO HEALTH, INC.

- ATHENAHEALTH, INC.

- IQVIA

- WIPRO

- CLOUDERA, INC.

- その他の企業

- HEALTHVERITY, INC.

- KYRUUS, INC.

- HEALTHCORUM

- LUMA HEALTH INC.

- VALIDIC, INC.

第17章 調査手法

第18章 付録

- 発行日

- 発行

- MarketsandMarkets

- ページ情報

- 英文 454 Pages

- 納期

- 即納可能