ココア・チョコレートの世界市場:ココアタイプ別、チョコレートタイプ別、性質別、用途別、製品形態別、流通チャネル別、地域別 - 予測(~2030年)

Cocoa and Chocolate Market by Cocoa Type (Butter, Powder, Liquor), Chocolate Type (Dark, Milk, White, Filled), Nature (Conventional, Organic), Application, Product Form, Distribution Channel, and Region - Global Forecast to 2030- 発行日

- ページ情報

- 英文 309 Pages

- 納期

-

即納可能

営業時間内にお支払方法などの確認が取れ次第、Eメールにて納品となります。営業時間: 9:00am - 6:00pm (土日祝除く)。

- 商品コード

- 1795419

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

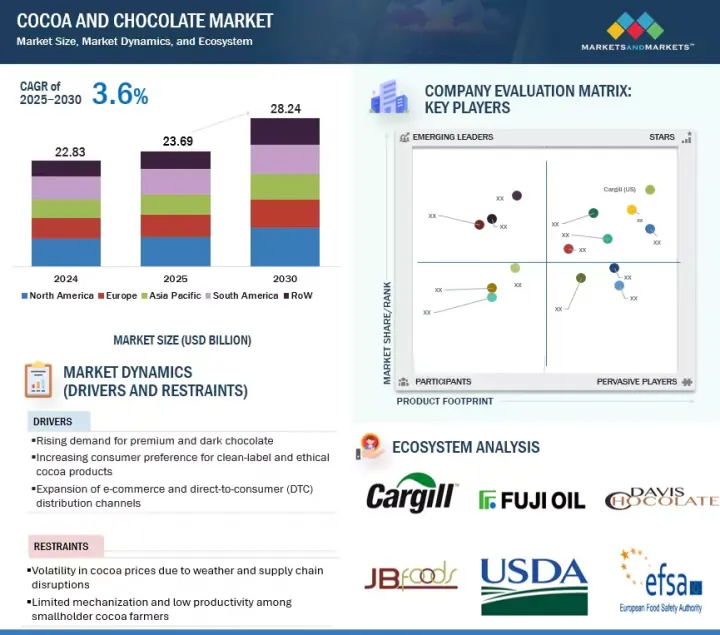

世界のココア・チョコレートの市場規模は、2025年の推定236億9,000万米ドルから2030年までに282億4,000万米ドルに達すると予測され、予測期間にCAGRで3.6%の成長が見込まれます。

ココア・チョコレートは、菓子類、ベーカリー製品、飲料、乳製品、健康用途などで利用されており、世界の消費パターンにおいて重要な役割を果たしています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2025年~2030年 |

| 基準年 | 2024年 |

| 予測期間 | 2025年~2030年 |

| 単位 | 米ドル |

| セグメント | ココアタイプ、用途、性質、チョコレートタイプ、流通チャネル、製品形態、地域 |

| 対象地域 | 北米、欧州、アジア太平洋、南米、その他の地域 |

市場成長の主な促進要因は、健康効果と贅沢な体験の組み合わせに対する需要の高まりと、倫理的な調達への注目です。さらに、多様なフレーバーや形態に対する選好の高まりもあります。

消費者層の変化に加え、都市化やデジタルコマースの拡大により、市場は消費者にとってより身近なものとなっています。持続可能性が重要な関心事となり、メーカー各社はトレーサビリティのある調達と環境にやさしい活動を優先するようになっています。こうした動向を受け、企業は競争力を維持するため、研究開発、製品のカスタマイズ、高級品への投資を増やしています。

この産業の成長可能性は、可処分所得の上昇と小売インフラの改良がココア・チョコレートの消費にプラスの影響を与えている新興経済圏において特に高いです。

「従来式ココアが、そのコスト効率、確立されたサプライチェーン、マスマーケット用途からの持続的な需要により、大きく成長しています。」

従来式ココアは、チョコレート製造、ベーカリー製品、乳製品、飲料に広く使用されているため、世界市場を独占しています。オーガニックココアやスペシャルティココアと比較して競争力のある価格設定は、低コストの大量販売に重点を置く大手メーカーにとって特に魅力的です。コートジボワール、ガーナ、ナイジェリアなどの主なカカオ生産国は、従来式カカオの供給に大きく寄与しており、安定した十分な市場を確保しています。

さらに、購買力と価格の考慮が消費者の意思決定に影響する新興経済圏では、従来式カカオへの強い需要が生じています。主要メーカーとして、多国籍チョコレート企業は、バルク調達や長期契約を通じて、主力製品用の従来式カカオを調達しています。オーガニックココアやフェアトレードココアといったセグメントは徐々に受け入れられつつありますが、従来式カカオの主流の訴求力に比べるとニッチ市場にとどまっています。全体として、従来式ココアは拡張性、汎用性、価格競争力により、産業の主な成長セグメントとなっています。

「ダークチョコレートセグメントが、ココア・チョコレート市場のチョコレートタイプセグメントで大きなシェアを占めています。」

消費者はカカオ含有率の高いダークチョコレートを好むようになってきています。カカオの割合が高いほど、ミルクチョコレートに比べて心臓の健康状態の向上、抗酸化作用、低い糖度といった健康上の利点につながることが多いです。この動向は、低糖度な植物由来の選択肢を求める需要の高まりと一致しています。National Confectioners Association(NCA)によると、2024年の調査では、消費者の61%が、健康上の利点からダークチョコレートを好むと回答しています。

このシフトは近年、大手チョコレートメーカーの注目を集めています。例えば2023年3月、Lindt & Sprungliは、高強度カカオプロファイルの需要に応えるため、カカオ95%のダークチョコレートを加え、EXCELLENCEポートフォリオを拡大しました。2024年4月、NestleはKitKatをフィーチャーしたMindful Chocolateシリーズを欧州で発売し、マグネシウムやカモミールエキスなど、機能的効果を提供するダークチョコレートを目立たせました。

消費者がより少ない原料、オーガニック認証、倫理的な調達を支持するラベルを持つダークチョコレートを好むことから、クリーンラベル製品への動向はさらに成長を促進します。このような選好は北米と欧州で顕著に拡大しており、チョコレート市場でもっとも急成長しているセグメントの1つとなっています。

当レポートでは、世界のココア・チョコレート市場について調査分析し、主な促進要因と抑制要因、競合情勢、将来の動向などの情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要な知見

- ココア市場における魅力的な機会

- チョコレート市場における魅力的な機会

- ココア市場:主な地域サブマーケットの成長率

- チョコレート市場:主な地域サブマーケットの成長率

- アジア太平洋のココア市場:タイプ別、国別

- 欧州のチョコレート市場:タイプ別、国別

- ココア市場:タイプ別

- ココア市場:用途別

- ココア市場:地域別

- チョコレート市場:タイプ別

- チョコレート市場:地域別

第5章 市場の概要

- イントロダクション

- マクロ経済指標

- 世界のGDP成長率

- 1人当たり所得の伸び(新興市場の拡大)

- 貿易の自由化と自由貿易協定

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- ココア・チョコレートに対する生成AIの影響

- イントロダクション

- ココア・チョコレートにおける生成AIの使用

- ケーススタディ分析

- ココア・チョコレート市場に対する影響

- 生成AIに取り組む隣接エコシステム

第6章 産業動向

- イントロダクション

- サプライチェーン分析

- バリューチェーン分析

- 貿易分析

- HSコード18の輸出データ(2020年~2024年)

- HSコード18の輸入データ(2020年~2024年)

- 技術分析

- 主要技術

- 補完技術

- 隣接技術

- 価格設定の分析

- 平均販売価格:主要企業別

- 平均販売価格の動向:製品タイプ別

- 平均販売価格:地域別

- エコシステム分析

- 栽培者

- 仲介業者

- ココア加工業者

- チョコレートメーカー

- 小売業者

- カスタマービジネスに影響を与える動向/混乱

- 特許分析

- 主な会議とイベント

- 規制情勢

- 規制機関、政府機関、その他の組織

- 規制枠組み

- ポーターのファイブフォース分析

- 主なステークホルダーと購入基準

- ケーススタディ分析

- ケーススタディ1:チョコレートメーカーに影響を与えるココア不足危機(2024年~2025年)

- ケーススタディ2:BARRY CALLEBAUTの第2世代チョコレート

- ケーススタディ3:インドネシアにおけるCARGILLとNESTLEのココア計画

- 投資と資金調達のシナリオ

- 2025年の米国関税の影響 - ココア・チョコレート市場

- イントロダクション

- 主な関税率

- ココア・チョコレートの混乱

- 価格の影響の分析

- 国・地域に対する影響

- 最終用途産業に対する影響

第7章 ココア市場:タイプ別

- イントロダクション

- ココアバター

- ココアパウダー

- ココアリキュール

第8章 ココア市場:用途別

- イントロダクション

- 食品・飲料

- 菓子類

- ベーカリー

- その他の食品・飲料用途

- 化粧品

- 医薬品

第9章 ココア市場:性質別

- イントロダクション

- 従来式ココア

- オーガニックココア

第10章 チョコレート市場:タイプ別

- イントロダクション

- ダークチョコレート

- ミルクチョコレート

- ホワイトチョコレート

- フィルドチョコレート

第11章 チョコレート市場:流通チャネル別

- イントロダクション

- オフライン

- eコマース

第12章 チョコレート市場:用途別

- イントロダクション

- 食品・飲料(B2C・フードサービス)

- ベーカリー・菓子類製品

- 機能性・栄養製品

- パーソナルケア・化粧品

- 医薬品

- プレミアムチョコレート・ギフトチョコレート

第13章 チョコレート市場:製品形態別

- イントロダクション

- ブロック/スラブ/バー

- パウダー

- チップス・ドロップス

- 液体(シロップ/コーティング)

- ペースト/スプレッド

- カカオ豆(生または焙煎)

- 顆粒/削り

第14章 ココア・チョコレート市場:プロセス別

- イントロダクション

- 豆の調達

- 焙煎・選別

- 粉砕・プレス

- 混合・コンチング

- 成形・コーティング

- 品質チェック

- アレルゲンコントロール

- バッチトレーサビリティ

- 持続可能なプロセス

第15章 ココア・チョコレート市場:技術別

- イントロダクション

- 発酵制御

- コンチングシステム

- 焙煎技術

- フレーバーカプセル化

- 品質モニタリングにおけるAI

- IoT統合

- 3Dプリンティングの応用

- スマート包装

- コールドチェーン技術

第16章 ココア・チョコレート市場:地域別

- イントロダクション

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- フランス

- ドイツ

- 英国

- スペイン

- イタリア

- ベルギー

- スイス

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア・ニュージーランド

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- その他の地域

- アフリカ

- 中東

第17章 競合情勢

- 概要

- 主要参入企業の戦略/強み(2021年~2024年)

- 収益分析、2022年 - 2024年

- 市場シェア分析(2024年)

- 企業の評価と財務指標

- ブランド/製品の比較

- 企業の評価マトリクス:主要企業(2024年)

- 企業の評価マトリクス:スタートアップ/中小企業(2024年)

- 競合シナリオ

第18章 企業プロファイル

- 主要企業

- CARGILL, INCORPORATED

- BARRY CALLEBAUT

- OLAM GROUP

- FUJI OIL CO., LTD.

- GUAN CHONG BERHAD (GCB)

- JB COCOA, A SUBSIDIARY OF JB FOODS LIMITED

- ECOM AGROINDUSTRIAL CORP. LIMITED.

- NATRA

- KRUGER GROUP

- MAX FELCHLIN AG

- VALRHONA

- SUCESORES DE JOSE JESUS RESTREPO & CIA. S.A.

- PURATOS GROUP

- UNITED COCOA PROCESSOR, INC.

- COCOA PROCESSING COMPANY LIMITED (CPC)

- その他の企業

- SIERRA NATURALS

- CHOCOLATERIE DE L'OPERA

- COCOA FAMILY

- REPUBLICA DEL CACAO

- CAMPCO CHOCOLATES

- JINDAL COCOA

- GENCAU.BR

- FRIIS-HOLM CHOKOLADE

- DAVIS CHOCOLATE

- LOTUS CHOCOLATE COMPANY LTD

第19章 付録

図表

List of Tables

- TABLE 1 USD EXCHANGE RATES, 2020-2024

- TABLE 2 RESEARCH ASSUMPTIONS

- TABLE 3 COCOA MARKET SNAPSHOT, 2025 VS. 2030

- TABLE 4 CHOCOLATE MARKET SNAPSHOT, 2025 VS. 2030

- TABLE 5 NUTRIENT CONTENT OF DIFFERENT CHOCOLATE FORMS/100G

- TABLE 6 TOP 10 EXPORTERS UNDER HS CODE 18, 2020-2024 (USD THOUSAND)

- TABLE 7 TOP 10 IMPORTERS UNDER HS CODE 18, 2020-2024 (USD THOUSAND)

- TABLE 8 AVERAGE SELLING PRICE OF COCOA, BY KEY PLAYER (USD/MT)

- TABLE 9 AVERAGE SELLING PRICE OF CHOCOLATE, BY KEY PLAYER (USD/UNIT)

- TABLE 10 AVERAGE SELLING PRICE OF COCOA, BY PRODUCT TYPE, 2020-2024 (USD/KG)

- TABLE 11 AVERAGE SELLING PRICE OF CHOCOLATE, BY TYPE, 2020-2024 (USD/KG)

- TABLE 12 AVERAGE SELLING PRICE OF COCOA, BY REGION, 2020-2024 (USD/KG)

- TABLE 13 AVERAGE SELLING PRICE OF CHOCOLATE, BY REGION, 2020-2024 (USD/KG)

- TABLE 14 LIST OF MAJOR PATENTS PERTAINING TO COCOA AND CHOCOLATE MARKET, 2020-2023

- TABLE 15 COCOA AND CHOCOLATE MARKET: DETAILED LIST OF CONFERENCES & EVENTS, 2025-2026

- TABLE 16 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 REST OF THE WORLD: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 20 COCOA AND CHOCOLATE MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 21 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR CHOCOLATE PRODUCTS

- TABLE 22 KEY BUYING CRITERIA FOR TOP 3 APPLICATIONS (COCOA)

- TABLE 23 US-ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 24 EXPECTED IMPACT OF TARIFFS ON TARGET PRODUCTS WITH RELEVANT HS CODES

- TABLE 25 EXPECTED TARIFF IMPACT ON END-USE INDUSTRIES: COCOA AND CHOCOLATE

- TABLE 26 COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 27 COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 28 COCOA MARKET, BY TYPE, 2020-2024 (KT)

- TABLE 29 COCOA MARKET, BY TYPE, 2025-2030 (KT)

- TABLE 30 COCOA BUTTER MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 31 COCOA BUTTER MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 32 COCOA BUTTER MARKET, BY REGION, 2020-2024 (KT)

- TABLE 33 COCOA BUTTER MARKET, BY REGION, 2025-2030 (KT)

- TABLE 34 COCOA POWDER MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 35 COCOA POWDER MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 36 COCOA POWDER MARKET, BY REGION, 2020-2024 (KT)

- TABLE 37 COCOA POWDER MARKET, BY REGION, 2025-2030 (KT)

- TABLE 38 COCOA LIQUOR MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 39 COCOA LIQUOR MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 40 COCOA LIQUOR MARKET, BY REGION, 2020-2024 (KT)

- TABLE 41 COCOA LIQUOR MARKET, BY REGION, 2025-2030 (KT)

- TABLE 42 COCOA MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 43 COCOA MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 44 COCOA MARKET FOR FOOD & BEVERAGE APPLICATIONS, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 45 COCOA MARKET FOR FOOD & BEVERAGE APPLICATIONS, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 46 COCOA MARKET FOR FOOD & BEVERAGE APPLICATIONS, BY REGION, 2020-2024 (USD MILLION)

- TABLE 47 COCOA MARKET FOR FOOD & BEVERAGE APPLICATIONS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 48 CONFECTIONERY: COCOA MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 49 CONFECTIONERY: COCOA MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 50 BAKERY: COCOA MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 51 BAKERY: COCOA MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 52 OTHER FOOD & BEVERAGE APPLICATIONS: COCOA MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 53 OTHER FOOD & BEVERAGE APPLICATIONS: COCOA MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 54 COCOA MARKET FOR COSMETICS, BY REGION, 2020-2024 (USD MILLION)

- TABLE 55 COCOA MARKET FOR COSMETICS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 56 COCOA MARKET FOR PHARMACEUTICALS, BY REGION, 2020-2024 (USD MILLION)

- TABLE 57 COCOA MARKET FOR PHARMACEUTICALS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 58 COCOA MARKET, BY NATURE, 2020-2024 (USD MILLION)

- TABLE 59 COCOA MARKET, BY NATURE, 2025-2030 (USD MILLION)

- TABLE 60 CONVENTIONAL COCOA MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 61 CONVENTIONAL COCOA MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 62 ORGANIC COCOA MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 63 ORGANIC COCOA MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 64 CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 65 CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 66 CHOCOLATE MARKET, BY TYPE, 2020-2024 (KT)

- TABLE 67 CHOCOLATE MARKET, BY TYPE, 2025-2030 (KT)

- TABLE 68 DARK CHOCOLATE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 69 DARK CHOCOLATE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 70 DARK CHOCOLATE MARKET, BY REGION, 2020-2024 (KT)

- TABLE 71 DARK CHOCOLATE MARKET, BY REGION, 2025-2030 (KT)

- TABLE 72 MILK CHOCOLATE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 73 MILK CHOCOLATE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 74 MILK CHOCOLATE MARKET, BY REGION, 2020-2024 (KT)

- TABLE 75 MILK CHOCOLATE MARKET, BY REGION, 2025-2030 (KT)

- TABLE 76 WHITE CHOCOLATE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 77 WHITE CHOCOLATE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 78 WHITE CHOCOLATE MARKET, BY REGION, 2020-2024 (KT)

- TABLE 79 WHITE CHOCOLATE MARKET, BY REGION, 2025-2030 (KT)

- TABLE 80 FILLED CHOCOLATE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 81 FILLED CHOCOLATE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 82 FILLED CHOCOLATE MARKET, BY REGION, 2020-2024 (KT)

- TABLE 83 FILLED CHOCOLATE MARKET, BY REGION, 2025-2030 (KT)

- TABLE 84 CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2020-2024 (USD MILLION)

- TABLE 85 CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2025-2030 (USD MILLION)

- TABLE 86 OFFLINE: CHOCOLATE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 87 OFFLINE: CHOCOLATE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 88 E-COMMERCE: CHOCOLATE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 89 E-COMMERCE: CHOCOLATE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 90 COCOA MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 91 COCOA MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 92 COCOA MARKET, BY REGION, 2020-2024 (KT)

- TABLE 93 COCOA MARKET, BY REGION, 2025-2030 (KT)

- TABLE 94 CHOCOLATE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 95 CHOCOLATE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 96 CHOCOLATE MARKET, BY REGION, 2020-2024 (KT)

- TABLE 97 CHOCOLATE MARKET, BY REGION, 2025-2030 (KT)

- TABLE 98 NORTH AMERICA: COCOA MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 99 NORTH AMERICA: COCOA MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 100 NORTH AMERICA: COCOA MARKET, BY NATURE, 2020-2024 (USD MILLION)

- TABLE 101 NORTH AMERICA: COCOA MARKET, BY NATURE, 2025-2030 (USD MILLION)

- TABLE 102 NORTH AMERICA: COCOA MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 103 NORTH AMERICA: COCOA MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 104 NORTH AMERICA: COCOA MARKET FOR FOOD & BEVERAGE APPLICATIONS, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 105 NORTH AMERICA: COCOA MARKET FOR FOOD & BEVERAGE APPLICATIONS, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 106 NORTH AMERICA: CHOCOLATE MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 107 NORTH AMERICA: CHOCOLATE MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 108 NORTH AMERICA: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 109 NORTH AMERICA: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 110 NORTH AMERICA: CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2020-2024 (USD MILLION)

- TABLE 111 NORTH AMERICA: CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2025-2030 (USD MILLION)

- TABLE 112 US: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 113 US: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 114 US: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 115 US: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 116 CANADA: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 117 CANADA: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 118 CANADA: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 119 CANADA: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 120 MEXICO: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 121 MEXICO: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 122 MEXICO: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 123 MEXICO: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 124 EUROPE: COCOA MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 125 EUROPE: COCOA MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 126 EUROPE: COCOA MARKET, BY NATURE, 2020-2024 (USD MILLION)

- TABLE 127 EUROPE: COCOA MARKET, BY NATURE, 2025-2030 (USD MILLION)

- TABLE 128 EUROPE: COCOA MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 129 EUROPE: COCOA MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 130 EUROPE: COCOA MARKET FOR FOOD & BEVERAGE APPLICATIONS, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 131 EUROPE: COCOA MARKET FOR FOOD & BEVERAGE APPLICATIONS, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 132 EUROPE: CHOCOLATE MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 133 EUROPE: CHOCOLATE MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 134 EUROPE: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 135 EUROPE: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 136 EUROPE: CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2020-2024 (USD MILLION)

- TABLE 137 EUROPE: CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2025-2030 (USD MILLION)

- TABLE 138 FRANCE: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 139 FRANCE: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 140 FRANCE: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 141 FRANCE: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 142 GERMANY: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 143 GERMANY: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 144 GERMANY: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 145 GERMANY: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 146 UK: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 147 UK: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 148 UK: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 149 UK: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 150 SPAIN: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 151 SPAIN: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 152 SPAIN: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 153 SPAIN: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 154 ITALY: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 155 ITALY: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 156 ITALY: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 157 ITALY: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 158 BELGIUM: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 159 BELGIUM: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 160 BELGIUM: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 161 BELGIUM: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 162 SWITZERLAND: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 163 SWITZERLAND: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 164 SWITZERLAND: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 165 SWITZERLAND: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 166 REST OF EUROPE: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 167 REST OF EUROPE: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 168 REST OF EUROPE: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 169 REST OF EUROPE: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 170 ASIA PACIFIC: COCOA MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 171 ASIA PACIFIC: COCOA MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 172 ASIA PACIFIC: COCOA MARKET, BY NATURE, 2020-2024 (USD MILLION)

- TABLE 173 ASIA PACIFIC: COCOA MARKET, BY NATURE, 2025-2030 (USD MILLION)

- TABLE 174 ASIA PACIFIC: COCOA MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 175 ASIA PACIFIC: COCOA MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 176 ASIA PACIFIC: COCOA MARKET FOR FOOD & BEVERAGE APPLICATIONS, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 177 ASIA PACIFIC: COCOA MARKET FOR FOOD & BEVERAGE APPLICATIONS, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 178 ASIA PACIFIC: CHOCOLATE MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 179 ASIA PACIFIC: CHOCOLATE MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 180 ASIA PACIFIC: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 181 ASIA PACIFIC: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 182 ASIA PACIFIC: CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2020-2024 (USD MILLION)

- TABLE 183 ASIA PACIFIC: CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2025-2030 (USD MILLION)

- TABLE 184 CHINA: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 185 CHINA: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 186 CHINA: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 187 CHINA: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 188 JAPAN: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 189 JAPAN: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 190 JAPAN: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 191 JAPAN: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 192 INDIA: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 193 INDIA: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 194 INDIA: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 195 INDIA: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 196 SOUTH KOREA: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 197 SOUTH KOREA: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 198 SOUTH KOREA: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 199 SOUTH KOREA: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 200 AUSTRALIA & NEW ZEALAND: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 201 AUSTRALIA & NEW ZEALAND: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 202 AUSTRALIA & NEW ZEALAND: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 203 AUSTRALIA & NEW ZEALAND: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 204 REST OF ASIA PACIFIC: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 205 REST OF ASIA PACIFIC: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 206 REST OF ASIA PACIFIC: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 207 REST OF ASIA PACIFIC: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 208 SOUTH AMERICA: COCOA MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 209 SOUTH AMERICA: COCOA MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 210 SOUTH AMERICA: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 211 SOUTH AMERICA: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 212 SOUTH AMERICA: COCOA MARKET, BY NATURE, 2020-2024 (USD MILLION)

- TABLE 213 SOUTH AMERICA: COCOA MARKET, BY NATURE, 2025-2030 (USD MILLION)

- TABLE 214 SOUTH AMERICA: COCOA MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 215 SOUTH AMERICA: COCOA MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 216 SOUTH AMERICA: COCOA MARKET FOR FOOD & BEVERAGE APPLICATIONS, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 217 SOUTH AMERICA: COCOA MARKET FOR FOOD & BEVERAGE APPLICATIONS, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 218 SOUTH AMERICA: CHOCOLATE MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 219 SOUTH AMERICA: CHOCOLATE MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 220 SOUTH AMERICA: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 221 SOUTH AMERICA: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 222 SOUTH AMERICA: CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2020-2024 (USD MILLION)

- TABLE 223 SOUTH AMERICA: CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2025-2030 (USD MILLION)

- TABLE 224 BRAZIL: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 225 BRAZIL: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 226 BRAZIL: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 227 BRAZIL: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 228 ARGENTINA: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 229 ARGENTINA: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 230 ARGENTINA: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 231 ARGENTINA: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 232 REST OF SOUTH AMERICA: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 233 REST OF SOUTH AMERICA: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 234 REST OF SOUTH AMERICA: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 235 REST OF SOUTH AMERICA: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 236 REST OF THE WORLD: COCOA MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 237 REST OF THE WORLD: COCOA MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 238 REST OF THE WORLD: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 239 REST OF THE WORLD: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 240 REST OF THE WORLD: COCOA MARKET, BY NATURE, 2020-2024 (USD MILLION)

- TABLE 241 REST OF THE WORLD: COCOA MARKET, BY NATURE, 2025-2030 (USD MILLION)

- TABLE 242 REST OF THE WORLD: COCOA MARKET, BY APPLICATION, 2020-2024 (USD MILLION)

- TABLE 243 REST OF THE WORLD: COCOA MARKET, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 244 REST OF THE WORLD: COCOA MARKET FOR FOOD & BEVERAGE APPLICATIONS, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 245 REST OF THE WORLD: COCOA MARKET FOR FOOD & BEVERAGE APPLICATIONS, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 246 REST OF THE WORLD: CHOCOLATE MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 247 REST OF THE WORLD: CHOCOLATE MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 248 REST OF THE WORLD: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 249 REST OF THE WORLD: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 250 REST OF THE WORLD: CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2020-2024 (USD MILLION)

- TABLE 251 REST OF THE WORLD: CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2025-2030 (USD MILLION)

- TABLE 252 AFRICA: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 253 AFRICA: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 254 AFRICA: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 255 AFRICA: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 256 MIDDLE EAST: COCOA MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 257 MIDDLE EAST: COCOA MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 258 MIDDLE EAST: CHOCOLATE MARKET, BY TYPE, 2020-2024 (USD MILLION)

- TABLE 259 MIDDLE EAST: CHOCOLATE MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 260 OVERVIEW OF STRATEGIES DEPLOYED BY KEY MARKET PLAYERS

- TABLE 261 COCOA MARKET: DEGREE OF COMPETITION, 2024

- TABLE 262 CHOCOLATE MARKET: DEGREE OF COMPETITION, 2024

- TABLE 263 COCOA AND CHOCOLATE MARKET: REGION FOOTPRINT

- TABLE 264 COCOA AND CHOCOLATE MARKET: TYPE FOOTPRINT

- TABLE 265 COCOA AND CHOCOLATE MARKET: APPLICATION FOOTPRINT

- TABLE 266 COCOA MARKET: NATURE FOOTPRINT

- TABLE 267 COCOA AND CHOCOLATE MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 268 COCOA AND CHOCOLATE MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES, 2024

- TABLE 269 COCOA AND CHOCOLATE MARKET: PRODUCT LAUNCHES, JANUARY 2020-FEBRUARY 2025

- TABLE 270 COCOA AND CHOCOLATE MARKET: DEALS, JANUARY 2020-FEBRUARY 2025

- TABLE 271 COCOA AND CHOCOLATE MARKET: EXPANSIONS, JANUARY 2020-FEBRUARY 2025

- TABLE 272 CARGILL, INCORPORATED: COMPANY OVERVIEW

- TABLE 273 CARGILL, INCORPORATED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 274 CARGILL, INCORPORATED: PRODUCT LAUNCHES

- TABLE 275 CARGILL, INCORPORATED: DEALS

- TABLE 276 CARGILL, INCORPORATED: EXPANSIONS

- TABLE 277 BARRY CALLEBAUT: COMPANY OVERVIEW

- TABLE 278 BARRY CALLEBAUT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 279 BARRY CALLEBAUT: PRODUCT LAUNCHES

- TABLE 280 BARRY CALLEBAUT: EXPANSIONS

- TABLE 281 OLAM GROUP: COMPANY OVERVIEW

- TABLE 282 OLAM GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 283 FUJI OIL CO., LTD.: COMPANY OVERVIEW

- TABLE 284 FUJI OIL CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 285 GUAN CHONG BERHAD (GCB): COMPANY OVERVIEW

- TABLE 286 GUAN CHONG BERHAD (GCB): PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 287 GUAN CHONG BERHAD (GCB): DEALS

- TABLE 288 JB COCOA: COMPANY OVERVIEW

- TABLE 289 JB COCOA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 290 ECOM AGROINDUSTRIAL CORP. LIMITED.: COMPANY OVERVIEW

- TABLE 291 ECOM AGROINDUSTRIAL CORP. LIMITED.: PRODUCTS/SOLUTIONS/ SERVICES OFFERED

- TABLE 292 NATRA: COMPANY OVERVIEW

- TABLE 293 NATRA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 294 KRUGER GROUP: COMPANY OVERVIEW

- TABLE 295 KRUGER GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 296 MAX FELCHLIN AG: COMPANY OVERVIEW

- TABLE 297 MAX FELCHLIN AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 298 VALRHONA: COMPANY OVERVIEW

- TABLE 299 VALRHONA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 300 SUCESORES DE JOSE JESUS RESTREPO & CIA. S.A.: COMPANY OVERVIEW

- TABLE 301 SUCESORES DE JOSE JESUS RESTREPO & CIA. S.A.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 302 PURATOS GROUP: COMPANY OVERVIEW

- TABLE 303 PURATOS GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 304 PURATOS GROUP: DEALS

- TABLE 305 UNITED COCOA PROCESSOR, INC.: COMPANY OVERVIEW

- TABLE 306 UNITED COCOA PROCESSOR, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 307 COCOA PROCESSING COMPANY LIMITED (CPC): COMPANY OVERVIEW

- TABLE 308 COCOA PROCESSING COMPANY LIMITED (CPC): PRODUCTS/SOLUTIONS/ SERVICES OFFERED

- TABLE 309 SIERRA NATURALS: COMPANY OVERVIEW

- TABLE 310 SIERRA NATURALS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 311 CHOCOLATERIE DE L'OPERA: COMPANY OVERVIEW

- TABLE 312 CHOCOLATERIE DE L'OPERA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 313 COCOA FAMILY: COMPANY OVERVIEW

- TABLE 314 COCOA FAMILY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 315 REPUBLICA DEL CACAO: COMPANY OVERVIEW

- TABLE 316 REPUBLICA DEL CACAO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 317 CAMPCO CHOCOLATES: COMPANY OVERVIEW

- TABLE 318 CAMPCO CHOCOLATES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 319 JINDAL COCOA: COMPANY OVERVIEW

- TABLE 320 GENCAU.BR: COMPANY OVERVIEW

- TABLE 321 FRIIS-HOLM CHOKOLADE: COMPANY OVERVIEW

- TABLE 322 DAVIS CHOCOLATE: COMPANY OVERVIEW

- TABLE 323 LOTUS CHOCOLATE COMPANY LTD: COMPANY OVERVIEW

List of Figures

- FIGURE 1 COCOA AND CHOCOLATE MARKET: RESEARCH DESIGN

- FIGURE 2 KEY DATA FROM SECONDARY SOURCES

- FIGURE 3 KEY INDUSTRY INSIGHTS

- FIGURE 4 BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY, DESIGNATION, AND REGION

- FIGURE 5 COCOA AND CHOCOLATE MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

- FIGURE 6 COCOA AND CHOCOLATE MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- FIGURE 7 DATA TRIANGULATION METHODOLOGY

- FIGURE 8 DATA TRIANGULATION: SUPPLY-SIDE

- FIGURE 9 DATA TRIANGULATION: DEMAND-SIDE

- FIGURE 10 RESEARCH LIMITATIONS

- FIGURE 11 COCOA MARKET, BY TYPE, 2025 VS. 2030 (USD MILLION)

- FIGURE 12 COCOA MARKET, BY NATURE, 2025 VS. 2030 (USD MILLION)

- FIGURE 13 COCOA MARKET, BY APPLICATION, 2025 VS. 2030 (USD MILLION)

- FIGURE 14 COCOA MARKET SHARE AND GROWTH RATE, BY REGION

- FIGURE 15 CHOCOLATE MARKET, BY TYPE, 2025 VS. 2030 (USD MILLION)

- FIGURE 16 CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL, 2025 VS. 2030 (USD MILLION)

- FIGURE 17 CHOCOLATE MARKET SHARE AND GROWTH RATE, BY REGION

- FIGURE 18 PRODUCT LAUNCHES AND EXPANSIONS TO DRIVE COCOA MARKET

- FIGURE 19 STRONG DEMAND FROM ASIA PACIFIC TO DRIVE CHOCOLATE MARKET

- FIGURE 20 COCOA CONSUMPTION IN CHINA AND INDIA TO INCREASE AT HIGH RATE DURING FORECAST PERIOD

- FIGURE 21 EMERGING MARKETS TO SHOWCASE HIGHEST DEMAND FOR CHOCOLATE

- FIGURE 22 CHINA TO ACCOUNT FOR LARGEST SHARE IN ASIA PACIFIC IN 2025

- FIGURE 23 GERMANY TO ACCOUNT FOR LARGEST SHARE IN EUROPE IN 2025

- FIGURE 24 COCOA BUTTER TO DOMINATE COCOA MARKET IN 2025

- FIGURE 25 FOOD & BEVERAGES TO DOMINATE COCOA MARKET DURING FORECAST PERIOD

- FIGURE 26 EUROPE TO DOMINATE COCOA MARKET DURING FORECAST PERIOD

- FIGURE 27 MILK CHOCOLATE TO DOMINATE CHOCOLATE MARKET IN 2025

- FIGURE 28 EUROPE TO DOMINATE CHOCOLATE MARKET DURING FORECAST PERIOD

- FIGURE 29 GLOBAL GDP GROWTH (2022-2026)

- FIGURE 30 GDP PER CAPITA, CURRENT PRICES (USD PER CAPITA) 2020-2030

- FIGURE 31 PER CAPITA INCOME GROWTH (EMERGING MARKET EXPANSION-INDIA)

- FIGURE 32 GHANA: COCOA PRODUCER PRICE (GH¢ PER TONNE), 2022-2025

- FIGURE 33 COCOA AND CHOCOLATE MARKET DYNAMICS

- FIGURE 34 ORAC VALUE OF HIGH-FLAVANOL-CONTAINING FOOD PRODUCTS

- FIGURE 35 ADOPTION OF GEN AI IN COCOA AND CHOCOLATE

- FIGURE 36 RISING DEMAND FOR SUSTAINABLE, ETHICAL, AND FUNCTIONAL CHOCOLATES ACCELERATES GROWTH ACROSS GLOBAL COCOA VALUE CHAIN

- FIGURE 37 COCOA AND CHOCOLATE MARKET: VALUE CHAIN ANALYSIS

- FIGURE 38 EXPORT DATA FOR COCOA AND CHOCOLATE UNDER HS CODE 18 FOR KEY COUNTRIES, 2020-2024 (USD THOUSAND)

- FIGURE 39 IMPORT DATA FOR COCOA AND CHOCOLATE UNDER HS CODE 18 FOR KEY COUNTRIES, 2020-2024 (USD THOUSAND)

- FIGURE 40 AVERAGE SELLING PRICE OF COCOA, BY KEY PLAYER, 2024 (USD/PER KG)

- FIGURE 41 AVERAGE SELLING PRICE OF CHOCOLATE, BY KEY PLAYER, 2024 (USD/PER KG)

- FIGURE 42 AVERAGE SELLING PRICE TREND OF COCOA, BY PRODUCT TYPE (USD/KG)

- FIGURE 43 AVERAGE SELLING PRICE TREND OF CHOCOLATE, BY TYPE (USD/KG)

- FIGURE 44 AVERAGE SELLING PRICE TREND OF COCOA, BY REGION (USD/KG)

- FIGURE 45 AVERAGE SELLING PRICE TREND OF CHOCOLATE, BY REGION (USD/KG)

- FIGURE 46 COCOA AND CHOCOLATE MARKET: ECOSYSTEM ANALYSIS

- FIGURE 47 COCOA AND CHOCOLATE MARKET: TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 48 NUMBER OF PATENTS GRANTED FOR COCOA AND CHOCOLATE MARKET, 2014-2024

- FIGURE 49 REGIONAL ANALYSIS OF PATENTS GRANTED FOR COCOA AND CHOCOLATE MARKET, 2014-2024

- FIGURE 50 PORTER'S FIVE FORCES ANALYSIS: COCOA AND CHOCOLATE MARKET

- FIGURE 51 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR CHOCOLATE PRODUCTS

- FIGURE 52 KEY BUYING CRITERIA FOR TOP 3 APPLICATIONS (COCOA)

- FIGURE 53 COCOA AND CHOCOLATE MARKET: INVESTMENT AND FUNDING SCENARIO, 2020-2025 (USD MILLION)

- FIGURE 54 COCOA BUTTER TO DOMINATE COCOA MARKET TILL 2030

- FIGURE 55 FOOD & BEVERAGES TO DOMINATE COCOA APPLICATIONS MARKET

- FIGURE 56 CONVENTIONAL SEGMENT TO DOMINATE THE COCOA MARKET

- FIGURE 57 MILK CHOCOLATE TO DOMINATE CHOCOLATE MARKET

- FIGURE 58 OFFLINE SEGMENT TO REMAIN LARGEST DISTRIBUTION CHANNEL

- FIGURE 59 COCOA MARKET: REGIONAL SCENARIO

- FIGURE 60 CHOCOLATE MARKET: REGIONAL SCENARIO

- FIGURE 61 EUROPE: COCOA MARKET SNAPSHOT

- FIGURE 62 EUROPE: CHOCOLATE MARKET SNAPSHOT

- FIGURE 63 ASIA PACIFIC: COCOA MARKET SNAPSHOT

- FIGURE 64 ASIA PACIFIC: CHOCOLATE MARKET SNAPSHOT

- FIGURE 65 COCOA AND CHOCOLATE MARKET: REVENUE ANALYSIS FOR KEY COMPANIES IN LAST 3 YEARS, 2022-2024 (USD BILLION)

- FIGURE 66 MARKET SHARE ANALYSIS OF LEADING PLAYERS IN COCOA MARKET, 2024

- FIGURE 67 MARKET SHARE ANALYSIS OF LEADING PLAYERS IN CHOCOLATE MARKET, 2024

- FIGURE 68 COMPANY VALUATION OF KEY PLAYERS IN COCOA AND CHOCOLATE MARKET

- FIGURE 69 EV/EBITDA OF KEY PLAYERS IN COCOA AND CHOCOLATE MARKET

- FIGURE 70 COCOA AND CHOCOLATE MARKET: BRAND/PRODUCT COMPARISON

- FIGURE 71 COCOA AND CHOCOLATE MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 72 COCOA AND CHOCOLATE MARKET: COMPANY FOOTPRINT

- FIGURE 73 COCOA AND CHOCOLATE MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 74 CARGILL, INCORPORATED: COMPANY SNAPSHOT

- FIGURE 75 BARRY CALLEBAUT: COMPANY SNAPSHOT

- FIGURE 76 OLAM GROUP: COMPANY SNAPSHOT

- FIGURE 77 FUJI OIL CO., LTD.: COMPANY SNAPSHOT

- FIGURE 78 GUAN CHONG BERHAD (GCB): COMPANY SNAPSHOT

- FIGURE 79 JB COCOA: COMPANY SNAPSHOT

目次

The cocoa and chocolate market is projected to reach USD 28.24 billion by 2030 from an estimated USD 23.69 billion in 2025, registering a CAGR of 3.6% during the forecast period. Cocoa and chocolate play a significant role in global consumption patterns, finding use in confectionery, bakery products, beverages, dairy items, and health applications.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2025-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD) |

| Segments | By Cocoa Type, Application, Nature, Chocolate Type, Distribution Channel, Product Form, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, and RoW |

The primary driver of market growth is the rising demand for a combination of health benefits and indulgent experiences, along with a focus on ethical sourcing. Additionally, there is a rising preference for diverse flavors and formats.

Shifting consumer demographics, coupled with urbanization and the expansion of digital commerce, are making the market more accessible to consumers. Sustainability has become a critical concern, prompting manufacturers to prioritize traceable sourcing and environmentally friendly practices. In response to these trends, companies are increasingly investing in research and development, product customization, and premium offerings to remain competitive.

The growth potential in this industry is particularly strong in emerging economies, where rising disposable incomes and improved retail infrastructure are positively impacting cocoa and chocolate consumption.

"Conventional cocoa is experiencing significant growth due to its cost-efficiency, established supply chains, and sustained demand from mass-market applications."

Conventional cocoa dominates the global market due to its widespread use in chocolate manufacturing, bakery products, dairy items, and beverages. Its competitive pricing compared to organic or specialty cocoa makes it particularly attractive to large manufacturers focused on low-cost, high-volume sales. The primary cocoa-producing countries, like Cote d'Ivoire, Ghana, and Nigeria, contribute significantly to the supply of conventional cocoa, ensuring a stable and adequate market.

Additionally, strong demand for conventional cocoa arises in emerging economies, where purchasing power and price considerations influence consumer decisions. As major producers, multinational chocolate companies source conventional cocoa for their mainstream products through bulk procurement and long-term contracts. While segments such as organic or fair trade cocoa are gradually gaining acceptance, they remain niche markets compared to the mainstream appeal of conventional cocoa. Overall, the scalability, versatility, and price competitiveness of conventional cocoa make it the primary growth segment in the industry.

"The dark chocolate segment holds a significant share in the chocolate type segment of the cocoa and chocolate market."

Consumers are increasingly favoring dark chocolates with higher cocoa content. Higher cocoa percentages are often linked to health benefits such as improved heart health, antioxidant properties, and lower sugar levels compared to milk chocolate. This trend aligns with the growing demand for low-sugar and plant-based options. According to the National Confectioners Association (NCA), 61% of consumers surveyed in 2024 expressed a preference for dark chocolate due to its perceived health benefits.

This shift has captured the attention of major chocolate manufacturers in recent years. For example, in March 2023, Lindt & Sprungli expanded its EXCELLENCE portfolio with a 95% cocoa dark chocolate to cater to the demand for high-intensity cocoa profiles. In April 2024, Nestle launched its "Mindful Chocolate" range featuring KitKat in Europe, highlighting dark chocolate that offers functional benefits, such as magnesium and chamomile extract.

The trend towards clean-label products further drives growth, as consumers prefer dark chocolate with fewer ingredients, organic certifications, and labels that support ethical sourcing. This preference is notably growing in North America and Europe, making it one of the fastest-growing segments in the chocolate market.

Europe holds a significant share of the global cocoa and chocolate market.

Europe holds a significant market share in the global cocoa and chocolate industry due to its long-standing tradition of manufacturing, strong consumer preferences, and robust regulatory frameworks. In countries like Switzerland, Belgium, France, and Germany, major companies such as Lindt & Sprungli, Barry Callebaut, and Ferrero continuously innovate in product development, ethical sourcing, and high-quality formulations. European consumers are presented with an abundance of premium chocolate options, including dark, organic, and sugar-free varieties, which cater to health-conscious trends.

In January 2025, the Bean-to-Bar Sustainability Line of Lindt & Sprungli (Switzerland) was inaugurated in Olten, Switzerland, enhancing traceability and ethical sourcing with the help of blockchain validation for cocoa sourced from Ghana and Ecuador. The investment highlights the region's commitment to sustainability and production-level transparency. Europe's advanced retail setup, strong export capability, and regional authority in sustainability together counterpoise its superior share in the global cocoa and chocolate market to keep itself abreast of trends in ethical and premium chocolate-making.

In-depth interviews were conducted with chief executive officers (CEOs), Directors, and other executives from various key organizations operating in the cocoa and chocolate market:

- By Company Type: Tier 1 - 25%, Tier 2 - 45%, and Tier 3 - 30%

- By Designation: Directors- 20%, Managers - 50%, Executives- 30%

- By Region: North America - 25%, Europe - 30%, Asia Pacific - 20%, South America - 15% and Rest of the World -10%

In the cocoa and chocolate industry, the major players are Barry Callebaut (Switzerland), Cargill (US), Olam International (Singapore), Nestle (Switzerland), Mondelez International (US), and Ferrero Group (Italy). These companies maintain great market positions because of their global status, integrated supply chains, and diversified product portfolios that sell across industrial and consumer segments.

The other important ones include Lindt & Sprungli (Switzerland), Mars, Incorporated (US), Blommer Chocolate Company (US), Guan Chong Berhad (Malaysia), JB Foods Limited (Singapore), and ECOM Agroindustrial Corp. (Switzerland). These companies are given credit for their strategic emphasis on sustainable sourcing and product innovation, investing heavily in traceability and ethical supply chain practices.

Additionally, mid-sized and emerging competitors like Natra (Spain), Luker Chocolate (Colombia), Cocoa Family (Dominican Republic), and GENCAU.BR (Brazil) serve as demand generators for their single-origin and artisanal chocolates in niche markets throughout Europe and the Americas. These companies are fostering market competition, product differentiation, and innovation to meet the growing global demand for ethically sourced, high-end, and health-conscious chocolate products.

Research Coverage:

This research report categorizes the cocoa and chocolate market by Cocoa Type (Cocoa Butter, Cocoa Powder, Cocoa Liquor), Application (Food & Beverages, Cosmetics, Pharmaceuticals), Nature (Conventional, Organic), Chocolate Type (Dark Chocolate, Milk Chocolate, White Chocolate, Filled Chocolates), Distribution Channel (Offline, E-commerce), Product Form (Blocks/Slabs/Bars, Powder, Chips & Drops, Liquid (Syrup/Coating), Paste/Spread, Beans (Raw or Roasted), Granules/Shavings), and region (North America, Europe, Asia Pacific, South America, and Rest of the World). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the cocoa and chocolate market. A detailed analysis of the key industry players was carried out to provide insights into their business overview, services, key strategies, contracts, partnerships, agreements, new service launches, mergers and acquisitions, and recent developments associated with the cocoa and chocolate market. This report covers a competitive analysis of upcoming start-ups in the cocoa and chocolate market ecosystem. Furthermore, industry-specific trends such as technology analysis, ecosystem and market mapping, and patent and regulatory landscape, among others, are also covered in the study.

Reasons to Buy this Report:

The report will help market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall cocoa and chocolate market and the subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Health benefits of chocolates), restraints (Highly unstable economies in cocoa-producing countries), opportunities (Low penetration rate in developing countries), and challenges (Increase in counterfeit products) influencing the growth of the cocoa and chocolate market.

- New Launches/Innovation: Detailed insights on research & development activities and new service launches in the cocoa and chocolate market.

- Market Development: Comprehensive information about lucrative markets - the report analyzes the cocoa and chocolate market across varied regions.

- Market Diversification: Exhaustive information about new services, untapped geographies, recent developments, and investments in the cocoa and chocolate market.

- Competitive Assessment: The cocoa and chocolate market features an in-depth evaluation of competitive positioning based on market share, product portfolios, innovation capabilities, and strategic initiatives. Leading players such as Cargill (US), Barry Callebaut (Switzerland), Olam Group (Singapore), Lindt & Sprungli (Switzerland), and Mondelez International (US) are analyzed for their sourcing practices, processing capabilities, and branded offerings. The assessment includes a comparison of product footprints across cocoa derivatives and finished chocolate goods, with a focus on sustainability certifications, origin traceability, and premium product lines. Additionally, market strategies such as vertical integration, origin partnerships, and investments in ethical sourcing are reviewed to gauge competitive differentiation and long-term positioning.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 UNITS CONSIDERED

- 1.4.1 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key industry insights

- 2.1.2.2 Breakdown of primary interviews

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 MARKET BREAKDOWN & DATA TRIANGULATION

- 2.3.1 SUPPLY-SIDE

- 2.3.2 DEMAND-SIDE

- 2.4 RESEARCH ASSUMPTIONS AND LIMITATIONS

- 2.4.1 ASSUMPTIONS

- 2.4.2 LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES IN COCOA MARKET

- 4.2 ATTRACTIVE OPPORTUNITIES IN CHOCOLATE MARKET

- 4.3 COCOA MARKET: GROWTH RATE OF MAJOR REGIONAL SUBMARKETS

- 4.4 CHOCOLATE MARKET: GROWTH RATE OF MAJOR REGIONAL SUBMARKETS

- 4.5 ASIA PACIFIC: COCOA MARKET, BY TYPE AND COUNTRY

- 4.6 EUROPE: CHOCOLATE MARKET, BY TYPE AND COUNTRY

- 4.7 COCOA MARKET, BY TYPE

- 4.8 COCOA MARKET, BY APPLICATION

- 4.9 COCOA MARKET, BY REGION

- 4.10 CHOCOLATE MARKET, BY TYPE

- 4.11 CHOCOLATE MARKET, BY REGION

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 GLOBAL GDP GROWTH

- 5.2.2 PER CAPITA INCOME GROWTH (EMERGING MARKET EXPANSION)

- 5.2.3 TRADE LIBERALIZATION & FREE TRADE AGREEMENTS

- 5.3 MARKET DYNAMICS

- 5.3.1 DRIVERS

- 5.3.1.1 Health benefits of chocolate

- 5.3.1.2 Rising demand for premium and dark chocolate

- 5.3.1.3 Seasonal and festive sales

- 5.3.2 RESTRAINTS

- 5.3.2.1 Unstable economies in cocoa-producing countries

- 5.3.2.2 High volatility in cocoa prices

- 5.3.3 OPPORTUNITIES

- 5.3.3.1 Low penetration rate in developing countries

- 5.3.3.2 Cocoa derivatives in adjacent sectors

- 5.3.3.3 E-commerce & DTC expansion in chocolate

- 5.3.4 CHALLENGES

- 5.3.4.1 Increase in counterfeit products

- 5.3.4.2 Fragmented smallholder farming system

- 5.3.4.3 Sustainability concerns in cocoa industry

- 5.3.1 DRIVERS

- 5.4 IMPACT OF GEN AI ON COCOA AND CHOCOLATE

- 5.4.1 INTRODUCTION

- 5.4.2 USE OF GEN AI IN COCOA AND CHOCOLATE

- 5.4.3 CASE STUDY ANALYSIS

- 5.4.3.1 Mars Inc.: Gen AI for Recipe Innovation

- 5.4.3.2 Barry Callebaut: AI-Powered Traceability Platform

- 5.4.4 IMPACT ON COCOA AND CHOCOLATE MARKET

- 5.4.5 ADJACENT ECOSYSTEM WORKING ON GEN AI

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 SUPPLY CHAIN ANALYSIS

- 6.3 VALUE CHAIN ANALYSIS

- 6.4 TRADE ANALYSIS

- 6.4.1 EXPORT DATA FOR HS CODE 18 (2020-2024)

- 6.4.2 IMPORT DATA FOR HS CODE 18 (2020-2024)

- 6.5 TECHNOLOGY ANALYSIS

- 6.5.1 KEY TECHNOLOGIES

- 6.5.1.1 Fermentation optimization

- 6.5.1.2 Conching automation

- 6.5.2 COMPLEMENTARY TECHNOLOGIES

- 6.5.2.1 Cocoa bean roasting control systems

- 6.5.3 ADJACENT TECHNOLOGIES

- 6.5.3.1 Flavor encapsulation technology

- 6.5.1 KEY TECHNOLOGIES

- 6.6 PRICING ANALYSIS

- 6.6.1 AVERAGE SELLING PRICE, BY KEY PLAYER

- 6.6.1.1 Cocoa market

- 6.6.1.2 Chocolate market

- 6.6.2 AVERAGE SELLING PRICE TREND, BY PRODUCT TYPE

- 6.6.2.1 Cocoa market

- 6.6.2.2 Chocolate market

- 6.6.3 AVERAGE SELLING PRICE, BY REGION

- 6.6.3.1 Cocoa market

- 6.6.3.2 Chocolate market

- 6.6.1 AVERAGE SELLING PRICE, BY KEY PLAYER

- 6.7 ECOSYSTEM ANALYSIS

- 6.7.1 GROWERS

- 6.7.2 INTERMEDIARIES

- 6.7.3 COCOA PROCESSORS

- 6.7.4 CHOCOLATE MANUFACTURERS

- 6.7.5 RETAILERS

- 6.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 6.9 PATENT ANALYSIS

- 6.9.1 LIST OF MAJOR PATENTS

- 6.10 KEY CONFERENCES & EVENTS

- 6.11 REGULATORY LANDSCAPE

- 6.11.1 REGULATORY BODIES, GOVERNMENT AGENCIES, & OTHER ORGANIZATIONS

- 6.11.2 REGULATORY FRAMEWORK

- 6.11.2.1 Codex Alimentarius Commission (CAC)

- 6.11.2.2 North America

- 6.11.2.3 Europe

- 6.11.2.4 Asia Pacific

- 6.12 PORTER'S FIVE FORCES ANALYSIS

- 6.12.1 THREAT OF NEW ENTRANTS

- 6.12.2 THREAT OF SUBSTITUTES

- 6.12.3 BARGAINING POWER OF SUPPLIERS

- 6.12.4 BARGAINING POWER OF BUYERS

- 6.12.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.13 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.13.2 BUYING CRITERIA

- 6.14 CASE STUDY ANALYSIS

- 6.14.1 CASE STUDY 1: COCOA SHORTAGE CRISIS IMPACTING CHOCOLATE MAKERS (2024-2025)

- 6.14.2 CASE STUDY 2: BARRY CALLEBAUT'S 2ND GENERATION CHOCOLATE

- 6.14.3 CASE STUDY 3: CARGILL AND NESTLE COCOA PLAN IN INDONESIA

- 6.15 INVESTMENT AND FUNDING SCENARIO

- 6.16 IMPACT OF 2025 US TARIFFS-COCOA AND CHOCOLATE MARKET

- 6.16.1 INTRODUCTION

- 6.16.2 KEY TARIFF RATES

- 6.16.3 DISRUPTION IN COCOA AND CHOCOLATE

- 6.16.4 PRICE IMPACT ANALYSIS

- 6.16.5 IMPACT ON COUNTRIES/REGIONS

- 6.16.5.1 Cote d'Ivoire

- 6.16.5.2 Ghana

- 6.16.5.3 United States

- 6.16.5.4 Canada and Europe

- 6.16.6 IMPACT ON END-USE INDUSTRY

7 COCOA MARKET, BY TYPE

- 7.1 INTRODUCTION

- 7.2 COCOA BUTTER

- 7.2.1 RISING DEMAND FOR NATURAL INGREDIENTS AND PREMIUM CHOCOLATE APPLICATIONS GLOBALLY

- 7.3 COCOA POWDER

- 7.3.1 RISING DEMAND FOR FUNCTIONAL FOODS AND CLEAN-LABEL COCOA-BASED PRODUCTS

- 7.4 COCOA LIQUOR

- 7.4.1 RISING DEMAND FOR PREMIUM CHOCOLATE AND CLEAN-LABEL INGREDIENTS GLOBALLY

8 COCOA MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 FOOD & BEVERAGES

- 8.2.1 CONFECTIONERY

- 8.2.1.1 Rising demand for premium and functional cocoa-based confectionery products

- 8.2.2 BAKERY

- 8.2.2.1 Rising demand for premium cocoa in artisanal and industrial bakery

- 8.2.3 OTHER FOOD & BEVERAGE APPLICATIONS

- 8.2.1 CONFECTIONERY

- 8.3 COSMETICS

- 8.3.1 RISING INTEREST IN COCOA-BASED COSMETICS AND GROWING AWARENESS PROPELS MARKET

- 8.4 PHARMACEUTICALS

- 8.4.1 INCREASING CONSUMER DEMAND FOR NATURAL INGREDIENTS AND BENEFITS OF COCOA SUPPORTS GROWTH

9 COCOA MARKET, BY NATURE

- 9.1 INTRODUCTION

- 9.2 CONVENTIONAL COCOA

- 9.2.1 RISING GLOBAL DEMAND FOR AFFORDABLE COCOA-BASED MASS MARKET PRODUCTS

- 9.3 ORGANIC COCOA

- 9.3.1 RISING DEMAND FOR ETHICAL, CLEAN-LABEL, AND SUSTAINABLE COCOA PRODUCTS

10 CHOCOLATE MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.2 DARK CHOCOLATE

- 10.2.1 RISING HEALTH AWARENESS AND DEMAND FOR ANTIOXIDANT-RICH PRODUCTS

- 10.3 MILK CHOCOLATE

- 10.3.1 EXPANDING CONSUMER BASE AND INNOVATION FUEL MILK CHOCOLATE GROWTH

- 10.4 WHITE CHOCOLATE

- 10.4.1 GROWING DEMAND FOR PREMIUM, UNIQUE FLAVORS AND CLEAN-LABEL INGREDIENTS TO DRIVE DEMAND

- 10.5 FILLED CHOCOLATE

- 10.5.1 GROWING DEMAND FOR INDULGENT AND INNOVATIVE TEXTURES TO DRIVE MARKET

11 CHOCOLATE MARKET, BY DISTRIBUTION CHANNEL

- 11.1 INTRODUCTION

- 11.2 OFFLINE

- 11.3 E-COMMERCE

12 CHOCOLATE MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.2 FOOD & BEVERAGES (B2C & FOODSERVICE)

- 12.3 BAKERY & CONFECTIONERY PRODUCTS

- 12.4 FUNCTIONAL & NUTRITIONAL PRODUCTS

- 12.5 PERSONAL CARE & COSMETICS

- 12.6 PHARMACEUTICALS

- 12.7 PREMIUM & GIFT CHOCOLATES

13 CHOCOLATE MARKET, BY PRODUCT FORM

- 13.1 INTRODUCTION

- 13.2 BLOCKS/SLABS/BARS

- 13.3 POWDERS

- 13.4 CHIPS & DROPS

- 13.5 LIQUIDS (SYRUPS/COATINGS)

- 13.6 PASTES/SPREADS

- 13.7 COCOA BEANS (RAW OR ROASTED)

- 13.8 GRANULES/SHAVINGS

14 COCOA AND CHOCOLATE MARKET, BY PROCESS

- 14.1 INTRODUCTION

- 14.2 BEAN SOURCING

- 14.3 ROASTING & WINNOWING

- 14.4 GRINDING & PRESSING

- 14.5 MIXING & CONCHING

- 14.6 MOLDING & COATING

- 14.7 QUALITY CHECKS

- 14.8 ALLERGEN CONTROL

- 14.9 BATCH TRACEABILITY

- 14.10 SUSTAINABLE PROCESSING

15 COCOA AND CHOCOLATE MARKET, BY TECHNOLOGY

- 15.1 INTRODUCTION

- 15.2 FERMENTATION CONTROL

- 15.3 CONCHING SYSTEMS

- 15.4 ROASTING TECHNOLOGIES

- 15.5 FLAVOR ENCAPSULATION

- 15.6 AI IN QUALITY MONITORING

- 15.7 IOT INTEGRATION

- 15.8 3D PRINTING APPLICATIONS

- 15.9 SMART PACKAGING

- 15.10 COLD CHAIN TECHNOLOGIES

16 COCOA AND CHOCOLATE MARKET, BY REGION

- 16.1 INTRODUCTION

- 16.2 NORTH AMERICA

- 16.2.1 US

- 16.2.1.1 Rising seasonal demand and premiumization trends driving market growth

- 16.2.2 CANADA

- 16.2.2.1 Rising demand for premium and ethical chocolate products driving cocoa imports

- 16.2.3 MEXICO

- 16.2.3.1 Rising chocolate consumption and artisan trends drive cocoa processing demand

- 16.2.1 US

- 16.3 EUROPE

- 16.3.1 FRANCE

- 16.3.1.1 Growing artisan chocolate demand and ethical sourcing preferences propel cocoa imports

- 16.3.2 GERMANY

- 16.3.2.1 Premiumization, ethical sourcing, and vegan product innovations make Germany a prominent market

- 16.3.3 UK

- 16.3.3.1 Rising demand for premium, ethical, and sustainable chocolate products

- 16.3.4 SPAIN

- 16.3.4.1 Rising artisan chocolate culture and sustainable cocoa sourcing drive market demand

- 16.3.5 ITALY

- 16.3.5.1 Growing premium chocolate demand and cocoa bean imports drive market expansion

- 16.3.6 BELGIUM

- 16.3.6.1 High-quality exports and artisanal legacy drive cocoa and chocolate leadership

- 16.3.7 SWITZERLAND

- 16.3.7.1 Strong domestic consumption, premium exports, and sustainable sourcing drive chocolate industry's growth

- 16.3.8 REST OF EUROPE

- 16.3.1 FRANCE

- 16.4 ASIA PACIFIC

- 16.4.1 CHINA

- 16.4.1.1 Rising premium chocolate demand and e-commerce expansion fuel cocoa market growth

- 16.4.2 JAPAN

- 16.4.2.1 Growing demand for premium, plant-based, and travel-retail chocolates drives Japan's market.

- 16.4.3 INDIA

- 16.4.3.1 Rising urbanization and local sourcing bolster India's cocoa and chocolate demand

- 16.4.4 SOUTH KOREA

- 16.4.4.1 Growing premium chocolate demand and tech-driven product innovation fuel South Korea's market expansion

- 16.4.5 AUSTRALIA & NEW ZEALAND

- 16.4.5.1 Rising premium chocolate demand and ethical sourcing drive regional cocoa market growth

- 16.4.6 REST OF ASIA PACIFIC

- 16.4.1 CHINA

- 16.5 SOUTH AMERICA

- 16.5.1 BRAZIL

- 16.5.1.1 Rising domestic consumption and strategic imports drive Brazil's cocoa market

- 16.5.2 ARGENTINA

- 16.5.2.1 Rising cocoa imports and export growth driving Argentina's chocolate industry

- 16.5.3 REST OF SOUTH AMERICA

- 16.5.1 BRAZIL

- 16.6 REST OF THE WORLD

- 16.6.1 AFRICA

- 16.6.1.1 Strong cocoa production, export dominance, and sustainability push drive market growth

- 16.6.2 MIDDLE EAST

- 16.6.2.1 Rising premium chocolate demand and import dependency drive market expansion

- 16.6.1 AFRICA

17 COMPETITIVE LANDSCAPE

- 17.1 OVERVIEW

- 17.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2024

- 17.3 REVENUE ANALYSIS, 2022-2024

- 17.4 MARKET SHARE ANALYSIS, 2024

- 17.5 COMPANY VALUATION AND FINANCIAL METRICS

- 17.6 BRAND/PRODUCT COMPARISON

- 17.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 17.7.1 STARS

- 17.7.2 EMERGING LEADERS

- 17.7.3 PERVASIVE PLAYERS

- 17.7.4 PARTICIPANTS

- 17.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 17.7.5.1 Company footprint

- 17.7.5.2 Regional footprint

- 17.7.5.3 Type footprint

- 17.7.5.4 Application footprint

- 17.7.5.5 Nature footprint

- 17.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2024

- 17.8.1 PROGRESSIVE COMPANIES

- 17.8.2 RESPONSIVE COMPANIES

- 17.8.3 DYNAMIC COMPANIES

- 17.8.4 STARTING BLOCKS

- 17.8.5 COMPETITIVE BENCHMARKING OF STARTUPS/SMES, 2024

- 17.8.5.1 Detailed list of key startups/SMEs

- 17.8.5.2 Competitive benchmarking of key startups/SMEs

- 17.9 COMPETITIVE SCENARIO

- 17.9.1 PRODUCT LAUNCHES

- 17.9.2 DEALS

- 17.9.3 EXPANSIONS

18 COMPANY PROFILES

- 18.1 KEY PLAYERS

- 18.1.1 CARGILL, INCORPORATED

- 18.1.1.1 Business overview

- 18.1.1.2 Products/Solutions/Services offered

- 18.1.1.3 Recent developments

- 18.1.1.3.1 Product launches

- 18.1.1.4 MnM view

- 18.1.1.4.1 Key strengths

- 18.1.1.4.2 Strategic choices

- 18.1.1.4.3 Weaknesses and competitive threats

- 18.1.2 BARRY CALLEBAUT

- 18.1.2.1 Business overview

- 18.1.2.2 Products/Solutions/Services offered

- 18.1.2.3 Recent developments

- 18.1.2.3.1 Expansions

- 18.1.2.4 MnM view

- 18.1.2.4.1 Key strengths

- 18.1.2.4.2 Strategic choices

- 18.1.2.4.3 Weaknesses and competitive threats

- 18.1.3 OLAM GROUP

- 18.1.3.1 Business overview

- 18.1.3.2 Products/Solutions/Services offered

- 18.1.3.3 MnM view

- 18.1.3.3.1 Key strengths

- 18.1.3.3.2 Strategic choices

- 18.1.3.3.3 Weaknesses and competitive threats

- 18.1.4 FUJI OIL CO., LTD.

- 18.1.4.1 Business overview

- 18.1.4.2 Products/Solutions/Services offered

- 18.1.4.3 MnM view

- 18.1.4.3.1 Key strengths

- 18.1.4.3.2 Strategic choices

- 18.1.4.3.3 Weaknesses and competitive threats

- 18.1.5 GUAN CHONG BERHAD (GCB)

- 18.1.5.1 Business overview

- 18.1.5.2 Products/Solutions/Services offered

- 18.1.5.3 Recent developments

- 18.1.5.4 MnM view

- 18.1.5.4.1 Key strengths

- 18.1.5.4.2 Strategic choices

- 18.1.5.4.3 Weaknesses and competitive threats

- 18.1.6 JB COCOA, A SUBSIDIARY OF JB FOODS LIMITED

- 18.1.6.1 Business overview

- 18.1.6.2 Products/Solutions/Services offered

- 18.1.6.3 MnM view

- 18.1.7 ECOM AGROINDUSTRIAL CORP. LIMITED.

- 18.1.7.1 Business overview

- 18.1.7.2 Products/Solutions/Services offered

- 18.1.7.3 MnM view

- 18.1.8 NATRA

- 18.1.8.1 Business overview

- 18.1.8.2 Products/Solutions/Services offered

- 18.1.8.3 MnM view

- 18.1.9 KRUGER GROUP

- 18.1.9.1 Business overview

- 18.1.9.2 Products/Solutions/Services offered

- 18.1.9.3 MnM view

- 18.1.10 MAX FELCHLIN AG

- 18.1.10.1 Business overview

- 18.1.10.2 Products/Solutions/Services offered

- 18.1.10.3 MnM view

- 18.1.11 VALRHONA

- 18.1.11.1 Business overview

- 18.1.11.2 Products/Solutions/Services offered

- 18.1.11.3 MnM view

- 18.1.12 SUCESORES DE JOSE JESUS RESTREPO & CIA. S.A.

- 18.1.12.1 Business overview

- 18.1.12.2 Products/Solutions/Services offered

- 18.1.12.3 MnM view

- 18.1.13 PURATOS GROUP

- 18.1.13.1 Business overview

- 18.1.13.2 Products/Solutions/Services offered

- 18.1.13.3 Recent developments

- 18.1.13.3.1 Deals

- 18.1.13.4 MnM view

- 18.1.14 UNITED COCOA PROCESSOR, INC.

- 18.1.14.1 Business overview

- 18.1.14.2 Products/Solutions/Services offered

- 18.1.14.3 MnM view

- 18.1.15 COCOA PROCESSING COMPANY LIMITED (CPC)

- 18.1.15.1 Business overview

- 18.1.15.2 Products/Solutions/Services offered

- 18.1.15.3 MnM view

- 18.1.1 CARGILL, INCORPORATED

- 18.2 OTHER PLAYERS

- 18.2.1 SIERRA NATURALS

- 18.2.1.1 Business overview

- 18.2.1.2 Products/Solutions/Services offered

- 18.2.1.3 MnM view

- 18.2.2 CHOCOLATERIE DE L'OPERA

- 18.2.2.1 Business overview

- 18.2.2.2 Products/Solutions/Services offered

- 18.2.2.3 MnM view

- 18.2.3 COCOA FAMILY

- 18.2.3.1 Business overview

- 18.2.3.2 Products/Solutions/Services offered

- 18.2.3.3 MnM view

- 18.2.4 REPUBLICA DEL CACAO

- 18.2.4.1 Business overview

- 18.2.4.2 Products/Solutions/Services offered

- 18.2.4.3 MnM view

- 18.2.5 CAMPCO CHOCOLATES

- 18.2.5.1 Business overview

- 18.2.5.2 Products/Solutions/Services offered

- 18.2.5.3 MnM view

- 18.2.6 JINDAL COCOA

- 18.2.7 GENCAU.BR

- 18.2.8 FRIIS-HOLM CHOKOLADE

- 18.2.9 DAVIS CHOCOLATE

- 18.2.10 LOTUS CHOCOLATE COMPANY LTD

- 18.2.1 SIERRA NATURALS

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS

- 発行日

- 発行

- MarketsandMarkets

- ページ情報

- 英文 309 Pages

- 納期

- 即納可能