|

|

市場調査レポート

商品コード

1927588

手術用ロボットの世界市場:オファリング別、用途別、エンドユーザー別、地域別 - 2030年までの予測Surgical Robots Market By Product (Instruments & Accessories, Robotic Systems (Laparoscopy, Orthopedic), Services), Application (Urological Surgery, Orthopedic Surgery), End User (Hospitals, Clinics, Ambulatory Surgery Centers) - Global Forecast to 2030 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 手術用ロボットの世界市場:オファリング別、用途別、エンドユーザー別、地域別 - 2030年までの予測 |

|

出版日: 2025年12月09日

発行: MarketsandMarkets

ページ情報: 英文 285 Pages

納期: 即納可能

|

概要

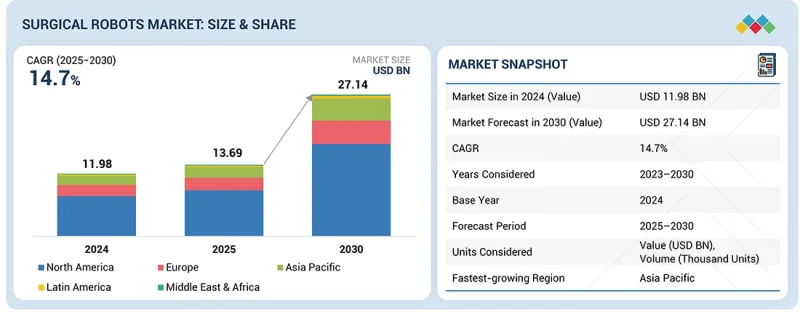

世界の手術用ロボットの市場規模は、予測期間中にCAGR14.7%で成長し、2025年の136億9,000万米ドルから2030年には271億4,000万米ドルに達すると見込まれています。

| 調査範囲 | |

|---|---|

| 調査対象期間 | 2023年~2030年 |

| 基準年 | 2024年 |

| 予測期間 | 2025年~2030年 |

| 対象単位 | 金額(10億米ドル) |

| セグメント | オファリング別、用途別、エンドユーザー別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

手術用ロボット市場は、医療提供者が手術の精度向上、患者アウトカムの改善、低侵襲手術の支援を目的としてロボット支援システムの導入を拡大していることから、著しい成長を遂げています。回復期間の短縮、合併症の減少、入院期間の短縮に対する需要の高まりが、病院において複数の専門分野にわたるロボット技術への投資を促進しています。画像技術の向上、AI駆動のガイダンス、よりコンパクトなロボットプラットフォームなど、継続的な技術進歩により、ロボット手術の臨床応用範囲は拡大しています。同時に、外科医向けトレーニングプログラムの拡充、支援的な償還制度、患者様の意識向上も導入を加速させています。これらの要因が相まって市場を推進し、ロボット支援手術の世界の普及範囲を広げています。

手術用ロボット市場において器具・付属品セグメントが最大のシェアを占める理由は、これらの部品が全てのロボット手術に必須であるため、安定した継続的な需要が生まれるからです。ロボットシステム自体は初期投資型の設備投資ですが、ステープラー、鋏、把持器、エネルギーデバイスなどの器具やその他の消耗品は、一定回数使用後に交換が必要となるため、継続的な利用と収益が保証されます。また、視覚ツール、ポート、トロカールなどの付属品もシステム機能に不可欠であり、頻繁な補充が必要です。ロボット手術件数の増加と病院におけるロボットプログラムの拡充に伴い、器具・付属品の消費量は比例して増加し、このセグメントが市場全体の収益に最も大きく貢献しています。

病院・診療所が手術用ロボット市場を主導している背景には、手術実施の主要拠点であることに加え、ロボット技術導入に必要な施設・資金・訓練済み人材を保有している点が挙げられます。これらの機関は、手術精度向上・患者転帰改善・臨床ワークフロー効率化を目的にロボット技術へ投資しています。低侵襲手術に対する有利な償還政策も、ロボットシステムの導入をさらに後押ししています。加えて、外科医の大半は病院環境内でロボット手術の訓練を受けるため、利用率が向上しています。患者が高度な低侵襲治療を期待する傾向が強まる中、病院・診療所は引き続き市場において最大かつ最も影響力のあるエンドユーザーであり続けています。

米国は、先進医療技術の導入への強い注力、ロボット支援手術プログラムの急速な拡大、病院インフラへの継続的な投資により、北米手術用ロボット市場において最も高いCAGRで成長すると予測されています。同国は、訓練を受けた外科医の豊富な人材基盤、広範な臨床研究活動、低侵襲手術に対する高い患者需要といった利点を有しており、これら全てがロボットプラットフォームの導入を加速させています。有利な償還政策、主要ロボット手術メーカーの強力な存在感、継続的な製品革新がさらなる成長を支えています。加えて、米国医療システムが患者アウトカムの改善、入院期間の短縮、手術精度の向上を重視していることが、同地域の他国と比較して手術用ロボットの導入を加速し続けています。

手術用ロボット市場の主要企業は、Intuitive Surgical(米国)、Stryker(米国)、Medtronic(アイルランド)、Smith+Nephew(英国)、Zimmer Biomet(米国)、Asensus Surgical(米国)、Siemens Healthineers(ドイツ)、CMR Surgical(英国)、Johnson &Johnson(米国)、Renishaw Plc(英国)です。

調査範囲:

当レポートは手術用ロボット市場を分析し、提供内容、用途、エンドユーザー、地域などの様々なセグメントに基づき、市場規模と将来の成長可能性を推定することを目的としています。また、主要企業の競合分析に加え、企業プロファイル、サービス提供内容、最近の動向、主要な市場戦略についても記載しています。

当レポート購入の理由

当レポートは、手術用ロボット市場全体の収益数値に関する最も正確な推定値を提供し、市場リーダーや新規参入企業を支援します。利害関係者の方が競合情勢を理解し、事業ポジショニングの最適化や適切な市場参入戦略の立案に役立つ貴重な知見を得られるよう支援します。また、主要な市場促進要因、抑制要因、課題、機会に関する情報を提供し、市場の動向を把握する上でも役立ちます。

当レポートは以下のポイントに関する洞察を提供します:

- 主要促進要因(ロボット支援手術の利点、技術進歩、償還状況の改善、手術用ロボットの採用拡大、医療ロボット調査への資金増加)、抑制要因(ロボットシステムの高コスト)、機会(外来手術センター(ASCs)における手術用ロボットの浸透拡大、新興市場での成長機会)、課題(手術ミス)の分析。

- 市場浸透:本報告書は、世界の手術用ロボット市場における主要プレイヤーが提供する製品に関する詳細な情報を含みます。提供形態、用途、エンドユーザー、地域別の様々なセグメントを網羅しています。

- 製品強化・革新:世界の手術用ロボット市場における新製品の発売状況と予測される動向に関する包括的な詳細情報。

- 市場開発:提供内容、用途、エンドユーザー、地域別に、収益性の高い成長市場に関する詳細な知見と分析を提供します。

- 市場の多様化:世界の手術用ロボット市場における新製品の投入、市場の拡大、現在の進歩、投資に関する包括的な情報。

- 競合評価:世界の手術用ロボット市場における主要競合他社の市場シェア、成長計画、製品提供内容、生産能力に関する詳細な評価。

よくあるご質問

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

第3章 市場概要

- 促進要因

- 抑制要因

- 機会

- 課題

- アンメットニーズとホワイトスペース

- 相互接続された市場と分野横断的な機会

- ティア1/2/3企業の戦略的動き

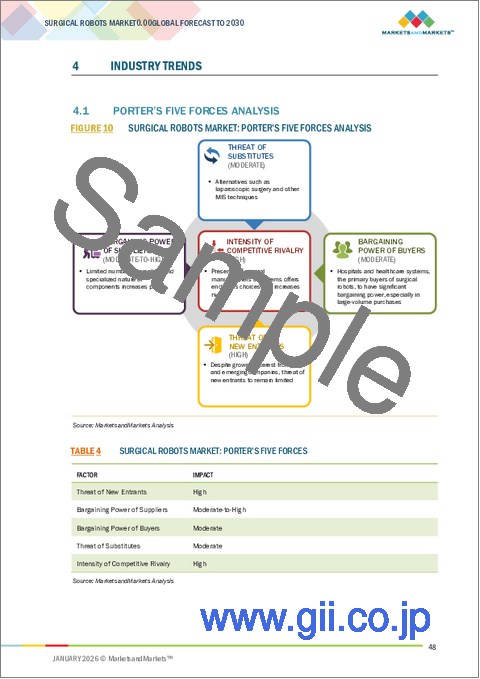

第4章 業界動向

- ポーターのファイブフォース分析

- マクロ経済見通し

- サプライチェーン分析

- バリューチェーン分析

- エコシステム分析

- 価格分析

- 貿易データ分析

- 2025年~2026年の主な会議とイベント

- 顧客のビジネスに影響を与える動向/混乱

- 投資と資金調達のシナリオ

- ケーススタディ分析

- 2025年の米国関税が手術ロボット市場に与える影響

第5章 技術の進歩、AI別影響、特許、イノベーション、将来の応用

- 主要な新興技術

- 技術/製品ロードマップ

- 特許分析

- 手術用ロボットの将来の応用

- AI/生成AIが手術用ロボット市場に与える影響

第6章 規制状況

- 地域の規制とコンプライアンス

- 認証、ラベル、環境基準

第7章 顧客情勢と購買行動

- 意思決定プロセス

- 主要な利害関係者と購入評価基準

- 採用障壁と内部課題

- 最終用途産業のアンメットニーズ

- 市場収益性

第8章 手術用ロボット市場(オファリング別)

- 医療機器および付属品

- ロボットシステム

- サービス

第9章 手術用ロボット市場(用途別)

- 一般外科

- 婦人科手術

- 整形外科

- 泌尿器科手術

- 脳神経外科

- 顕微手術

- 耳鼻科手術

- その他

第10章 手術用ロボット市場(エンドユーザー別)

- 病院とクリニック

- 外来手術センター

第11章 手術用ロボット市場(地域別)

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- その他

- ラテンアメリカ

- ブラジル

- メキシコ

- その他

- 中東・アフリカ

- GCC諸国

- その他

第12章 競合情勢

- 主要参入企業の戦略/強み

- 収益分析、2020年~2024年

- 市場シェア分析、2024年

- 企業評価マトリックス:主要参入企業、2024年

- 企業評価マトリックス:スタートアップ/中小企業、2024年

- 企業評価と財務指標

- ブランド/製品比較

- 競合シナリオ

第13章 企業プロファイル

- 主要参入企業

- INTUITIVE SURGICAL OPERATIONS, INC.

- STRYKER

- ZIMMER BIOMET

- MEDTRONIC

- SMITH+NEPHEW

- ASENSUS SURGICAL US, INC.

- SIEMENS HEALTHINEERS AG

- RENISHAW PLC

- GLOBUS MEDICAL

- JOHNSON & JOHNSON

- CMR SURGICAL LTD.

- THINK SURGICAL, INC.

- CORIN GROUP

- MICROSURE

- AVATERAMEDICAL GMBH

- MEDICAL MICROINSTRUMENTS, INC.

- MEDICAROID CORPORATION

- BRAINLAB SE

- ECENTIAL ROBOTICS

- SS INNOVATIONS INTERNATIONAL, INC.

- その他の企業

- MONTERIS

- MOMENTIS INNOVATIVE SURGERY

- TINAVI MEDICAL TECHNOLOGIES CO., LTD.

- DISTALMOTION SA

- NOVUS SAGLIK URUNLERI AR-GE DANISMANLIK(NOVUS ARGE)