|

|

市場調査レポート

商品コード

1479739

バーチャルリアリティの世界市場:用途別、デバイスタイプ別、オファリング別、技術別、地域別 - 2029年までの予測Virtual Reality Market by Technology (Non-immersive, Semi & Fully Immersive), Offering, Device Type (Head-mounted Devices, Gesture Tracking Devices, Projectors & Display Walls), Application and Region - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| バーチャルリアリティの世界市場:用途別、デバイスタイプ別、オファリング別、技術別、地域別 - 2029年までの予測 |

|

出版日: 2024年05月07日

発行: MarketsandMarkets

ページ情報: 英文 224 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

世界のバーチャルリアリティの市場規模は、2024年に159億米ドルになるとみられ、2029年には380億米ドルに達すると予測されており、予測期間中のCAGRは19.1%になると見込まれています。

ヘルスケアやゲーム・エンターテインメント分野でのデジタル技術の急速な採用が、バーチャルリアリティ市場の成長を促進しています。一方、遅延の問題と高いエネルギー消費がバーチャルリアリティ市場の成長を抑制しています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2020年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 検討単位 | 金額(10億米ドル) |

| セグメント別 | 用途別、デバイスタイプ別、オファリング別、技術別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

ヘッドマウントディスプレイ(HMD's)セグメントは予測期間中、22.5%という2番目に高いCAGRで成長する見込みです。ゲームやエンターテイメントにおけるヘッドマウントディスプレイの使用は、バーチャルリアリティハードウェアデバイスの成長の主な促進要因です。バーチャルリアリティヘッドマウントディスプレイは、ゲーマーやエンターテインメント愛好家が、没入感のあるインタラクティブなバーチャル世界に足を踏み入れることを可能にし、そこでは、探検したり、バーチャルなオブジェクトと相互作用したり、驚くほどリアルに感じられるゲームプレイに参加したりすることができます。この没入感と双方向性のレベルは、従来のゲームやメディア消費を超える体験をユーザーに提供し、ゲーム業界とエンターテインメント業界に革命をもたらしました。その結果、バーチャルリアリティヘッドマウントディスプレイは大きな関心と投資を集め、バーチャルリアリティ技術の進歩とバーチャルリアリティコンテンツのエコシステムの拡大につながっています。

ソフトウェア分野は、予測期間中に16.7%という2番目に高いCAGRで成長する見込みです。この成長は、VRソフトウェアがゲームやエンターテインメント以外の用途にも広がっていることに起因しています。ヘルスケア、教育、小売、自動車などの業界では、トレーニング、シミュレーション、製品設計にVRを活用するケースが増えています。VRソフトウェアは、情報オーバーレイ、インタラクティブゲーム、ナビゲーションエイドなどのバーチャルリアリティ体験を可能にします。一方、バーチャルリアリティソフトウェアは、ユーザーがオブジェクトを探索、対話、操作できる完全なデジタル環境を作り出します。クラウドコンピューティングに基づくVRは、撮影された画像をデータベースと比較し、関連情報をモバイルデバイスに送り返すために使用されます。モバイル・デバイスはさらに画像を処理し、3D画像を検出、リサイズ、生成します。VRでは、クラウド・プラットフォームソリューションには、スケーラブルな処理、アクセス可能なブラウザのダウンロード、信頼性の高いリアルタイム処理、安全なSaaS(Software as a Service)プラットフォームなどの利点があります。

当レポートでは、世界のバーチャルリアリティ市場について調査し、用途別、デバイスタイプ別、オファリング別、技術別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 顧客のビジネスに影響を与える動向/混乱

- 価格分析

- バリューチェーン分析

- エコシステム分析

- 投資と資金調達のシナリオ

- 技術分析

- 特許分析

- 貿易データ分析

- 主な会議とイベント

- ケーススタディ分析

- 関税と規制状況

- ポーターのファイブフォース分析

- 主な利害関係者と購入基準

第6章 バーチャルリアリティ市場、用途別

- イントロダクション

- 消費者

- 商業

- 企業(製造業)

- ヘルスケア

- 航空宇宙・防衛

- その他

第7章 バーチャルリアリティ市場、デバイスタイプ別

- イントロダクション

- ヘッドマウントディスプレイ

- ジェスチャー追跡デバイス

- プロジェクターとディスプレイウォール

第8章 バーチャルリアリティ市場、オファリング別

- イントロダクション

- ハードウェア

- ソフトウェア

第9章 バーチャルリアリティ市場、技術別

- イントロダクション

- 非没入型技術

- 半没入型および完全没入型技術

第10章 バーチャルリアリティ市場、地域別

- イントロダクション

- 北米

- 欧州

- アジア太平洋

- その他の地域

第11章 競合情勢

- 概要

- 主要参入企業の戦略/強み

- 市場シェア分析

- 収益分析、2019年~2023年

- 企業価値評価と財務指標

- バーチャルリアリティ市場:ブランド/製品比較

- 企業評価マトリックス:主要参入企業、2023年

- 企業評価マトリックス:スタートアップ/中小企業、2023年

- 競合シナリオと動向

第12章 企業プロファイル

- 主要参入企業

- SONY

- SAMSUNG ELECTRONICS CO., LTD.

- MICROSOFT

- META

- HTC CORPORATION

- BARCO

- PICO IMMERSIVE PTE.LTD.

- CYBERGLOVE SYSTEMS INC.

- UNITY TECHNOLOGIES

- PENUMBRA, INC.

- DPVR

- その他の企業

- ULTRALEAP

- FOVE INC

- QUYTECH

- HQSOFTWARE

- INNOWISE

- XRHEALTH IL LTD.

- VECTION TECHNOLOGIES

- MINDMAZE

- FIRSTHAND TECHNOLOGY

- WORLDVIZ, INC.

- VIRTUIX

- VIGHNESH INC.

- MERGE LABS, INC.

- SPACEVR

第13章 付録

The global virtual reality market was valued at USD 15.9 billion in 2024 and is projected to reach USD 38.0 billion by 2029; it is expected to register a CAGR of 19.1% during the forecast period. Rapid adoption of digital technologies in healthcare and gaming & entertainment sectors is driving the growth of the virtual reality market. Whereas Latency issues and high energy consumption is restraining the growth of the virtual reality market.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Billion) |

| Segments | By Technology, Offering, Device Type, Application and Region |

| Regions covered | North America, Europe, APAC, RoW |

"The Head-mounted Display (HMD's) segment is expected to grow at the second highest CAGR during the forecast period."

The Head-mounted Display (HMD's) segment is expected to grow at a second highest CAGR of 22.5% during the forecast period. The use of head-mounted displays in gaming and entertainment is a major driver for the growth of virtual reality hardware devices. Virtual reality head-mounted displays enable gamers and entertainment enthusiasts to step into immersive, interactive virtual worlds where they can explore, interact with virtual objects, and engage in gameplay that feels incredibly realistic. This level of immersion and interactivity has revolutionized the gaming and entertainment industries, offering users experiences that go beyond traditional gaming or media consumption. As a result, virtual reality head-mounted displays have garnered significant interest and investment, leading to advancements in virtual reality technology and a growing ecosystem of virtual reality content.

The software segment is likely to grow at the second higher CAGR during the forecast period

The software segment is expected to grow at second higher CAGR of 16.7% during the forecast period. The growth is attributed to VR software finding applications beyond just gaming and entertainment. Industries like healthcare, education, retail, and automotive are increasingly utilizing VR for training, simulations, and product design. It enables virtual reality experiences such as informative overlays, interactive games, and navigation aids. In contrast, virtual reality software creates entirely digital environments where users can explore, interact, and manipulate objects. VR based on cloud computing is used to compare the captured images with the database and send back relevant information to the mobile device. The mobile device further processes the image, and then detects, resizes, and generates 3D images. In VR, cloud platform solutions include benefits such as scalable processing, accessible browser downloads, reliable real-time processes, and secure Software as a Service (SaaS) platform.

"The North America segment is likely to grow at the second highest CAGR during the forecast period."

The market in North America is expected to witness the second highest CAGR of 19.4% during the forecast period. VR's extensive usage across various sectors, particularly in consumer electronics, propels the virtual reality market's expansion. Sectors like aerospace & defense, healthcare, consumer goods, and commercial industries are increasingly adopting virtual reality technologies for further advancements. The US boasts numerous global players offering virtual reality products and solutions, solidifying North America's prominence in the global virtual reality market.

Breakdown of primaries

The study contains insights from various industry experts, ranging from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

- By Company Type - Tier 1 - 35%, Tier 2 - 45%, Tier 3 - 20%

- By Designation- C-level Executives - 40%, Directors - 30%, Others - 30%

- By Region-North America - 40%, Europe - 20%, Asia Pacific - 30%, RoW - 10%

The virtual reality market is dominated by a few globally established players such as Meta (US), Sony (Japan), Samsung Electronics Co., Ltd. (South Korea), Microsoft (US), Unity Technologies (US), Barco (Belgium), Penumbra, Inc. (US), HTC Corporation (Taiwan), PICO Immersive Pte.ltd (US), and DPVR (China). The study includes an in-depth competitive analysis of these key players in the virtual reality market, with their company profiles, recent developments, and key market strategies.

Research Coverage:

The report segments the virtual reality market and forecasts its size by technology, offering, device type, application, and region. The report also discusses the drivers, restraints, opportunities, and challenges pertaining to the market. It gives a detailed view of the market across four main regions-North America, Europe, Asia Pacific, and RoW. Supply chain analysis has been included in the report, along with the key players and their competitive analysis in the virtual reality ecosystem.

Key Benefits to Buy the Report:

- Analysis of key drivers (The growing penetration of the Metaverse, Rapid adoption of digital technologies in healthcare and gaming & entertainment sectors, Increased investments in virtual reality market, Significant adoption of HMDs across various sectors). Restraint (Latency issues and high energy consumption, Health issues caused by excessive use of virtual reality devices), Opportunity (Latency issues and high energy consumption, Health issues caused by excessive use of virtual reality devices), Challenges (Latency issues and high energy consumption, Health issues caused by excessive use of virtual reality devices)

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product launches in the virtual reality market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the virtual reality market across varied regions

- Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the virtual reality market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Meta (US), Sony (Japan), Samsung Electronics Co., Ltd. (South Korea), Microsoft (US), Unity Technologies (US), Barco (Belgium), Penumbra, Inc. (US), HTC Corporation (Taiwan), PICO Immersive Pte.ltd (US), and DPVR (China) among others in the virtual reality market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- FIGURE 1 MARKET SEGMENTATION

- 1.3.2 REGIONAL SCOPE

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 UNITS CONSIDERED

- 1.7 LIMITATIONS

- 1.8 STAKEHOLDERS

- 1.9 SUMMARY OF CHANGES

- 1.9.1 IMPACT OF RECESSION

2 RESEARCH METHODOLOGY

- 2.1 INTRODUCTION

- FIGURE 2 VIRTUAL REALITY MARKET: RESEARCH DESIGN

- 2.2 RESEARCH DATA

- FIGURE 3 VIRTUAL REALITY MARKET: RESEARCH APPROACH

- 2.2.1 SECONDARY DATA

- 2.2.1.1 List of major secondary sources

- 2.2.1.2 Key data from secondary sources

- 2.2.2 PRIMARY DATA

- 2.2.2.1 List of key participants in primary interviews

- 2.2.2.2 Breakdown of primary profiles

- 2.2.2.3 Key data from primary sources

- 2.2.2.4 Key insights from industry experts

- 2.3 FACTOR ANALYSIS

- 2.3.1 SUPPLY-SIDE ANALYSIS

- FIGURE 4 REVENUE GENERATED FROM SALES OF VIRTUAL REALITY SOLUTIONS

- FIGURE 5 VIRTUAL REALITY MARKET: REVENUE ANALYSIS OF SONY

- 2.4 MARKET SIZE ESTIMATION METHODOLOGY

- FIGURE 6 VIRTUAL REALITY MARKET: SUPPLY-SIDE ANALYSIS

- 2.4.1 BOTTOM-UP APPROACH

- 2.4.1.1 Approach to arrive at market size using bottom-up analysis (demand side)

- FIGURE 7 VIRTUAL REALITY MARKET: BOTTOM-UP APPROACH

- 2.4.2 TOP-DOWN APPROACH

- 2.4.2.1 Approach to arrive at market size using top-down approach (supply side)

- FIGURE 8 VIRTUAL REALITY MARKET: TOP-DOWN APPROACH

- 2.4.3 GROWTH PROJECTIONS AND FORECAST-RELATED ASSUMPTIONS

- TABLE 1 VIRTUAL REALITY MARKET: GROWTH ASSUMPTIONS

- 2.5 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 9 VIRTUAL REALITY MARKET: DATA TRIANGULATION

- 2.6 RESEARCH ASSUMPTIONS

- TABLE 2 VIRTUAL REALITY MARKET: RESEARCH ASSUMPTIONS

- 2.7 LIMITATIONS

- 2.8 RISK ASSESSMENT

- TABLE 3 VIRTUAL REALITY MARKET: RISK ASSESSMENT

- 2.9 PARAMETERS CONSIDERED TO ANALYZE RECESSION IMPACT

- TABLE 4 VIRTUAL REALITY MARKET: PARAMETERS CONSIDERED TO ANALYZE RECESSION IMPACT

3 EXECUTIVE SUMMARY

- FIGURE 10 VIRTUAL REALITY MARKET, 2020-2029 (USD MILLION)

- FIGURE 11 HARDWARE SEGMENT TO WITNESS HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 12 GESTURE-TRACKING DEVICES SEGMENT TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 13 HEALTHCARE SEGMENT TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 14 ASIA PACIFIC TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE GROWTH OPPORTUNITIES FOR KEY PLAYERS IN VIRTUAL REALITY MARKET

- FIGURE 15 CONTINUOUS TECHNOLOGICAL ADVANCEMENTS IN VARIOUS SECTORS AND GROWING PENETRATION OF METAVERSE TO DRIVE MARKET

- 4.2 VIRTUAL REALITY MARKET, BY COMPONENT

- FIGURE 16 DISPLAY & PROJECTORS SEGMENT TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

- 4.3 HARDWARE: VIRTUAL REALITY MARKET, BY APPLICATION

- FIGURE 17 HEALTHCARE SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- 4.4 SOFTWARE: VIRTUAL REALITY MARKET, BY APPLICATION

- FIGURE 18 COMMERCIAL SEGMENT TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

- 4.5 CONSUMERS: VIRTUAL REALITY MARKET, BY DEVICE TYPE

- FIGURE 19 GESTURE-TRACKING DEVICES SEGMENT TO WITNESS HIGHEST CAGR DURING FORECAST PERIOD

- 4.6 VIRTUAL REALITY MARKET, BY REGION

- FIGURE 20 ASIA PACIFIC TO HOLD LARGEST MARKET SHARE IN 2029

- 4.7 VIRTUAL REALITY MARKET, BY COUNTRY

- FIGURE 21 CHINA TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 22 VIRTUAL REALITY MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- FIGURE 23 VIRTUAL REALITY MARKET: IMPACT OF DRIVERS

- 5.2.1.1 Growing penetration of metaverse

- 5.2.1.2 Rapid adoption of digital technologies in healthcare and gaming & entertainment sectors

- 5.2.1.3 Potential for transformative change across numerous industries

- 5.2.1.4 Significant adoption of HMDs

- 5.2.1.5 Emergence of virtual classrooms offering immersive and engaging learning experiences

- 5.2.2 RESTRAINTS

- FIGURE 24 VIRTUAL REALITY MARKET: IMPACT OF RESTRAINTS

- 5.2.2.1 Latency issues and high energy consumption

- 5.2.2.2 Health issues caused by excessive use of VR devices

- 5.2.3 OPPORTUNITIES

- FIGURE 25 VIRTUAL REALITY MARKET: IMPACT OF OPPORTUNITIES

- 5.2.3.1 Emerging applications of VR in telemedicine

- 5.2.3.2 Continuous developments in 5G technology

- 5.2.3.3 Growth of global travel & tourism industry

- 5.2.4 CHALLENGES

- FIGURE 26 VIRTUAL REALITY MARKET: IMPACT OF CHALLENGES

- 5.2.4.1 Creating VR systems with user-friendly interface

- 5.2.4.2 Display latency and limited field of view

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 27 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND FOR TOP PLAYERS, BY HEAD-MOUNTED DISPLAY

- FIGURE 28 AVERAGE SELLING PRICE TREND FOR TOP PLAYERS, BY HEAD-MOUNTED DISPLAY

- TABLE 5 AVERAGE SELLING PRICE TREND, BY DEVICE TYPE, 2018-2023 (USD)

- 5.4.2 AVERAGE SELLING PRICE TREND, BY REGION

- TABLE 6 AVERAGE SELLING PRICE TREND, BY REGION, 2019-2023 (USD)

- 5.5 VALUE CHAIN ANALYSIS

- FIGURE 29 VIRTUAL REALITY MARKET: VALUE CHAIN ANALYSIS

- 5.6 ECOSYSTEM ANALYSIS

- FIGURE 30 KEY PLAYERS IN VIRTUAL REALITY MARKET ECOSYSTEM

- TABLE 7 VIRTUAL REALITY MARKET: ECOSYSTEM

- 5.7 INVESTMENT AND FUNDING SCENARIO

- FIGURE 31 INVESTMENT AND FUNDING SCENARIO

- 5.8 TECHNOLOGY ANALYSIS

- 5.8.1 KEY TECHNOLOGIES

- 5.8.1.1 Motion tracking

- 5.8.1.2 Haptic technology

- 5.8.2 COMPLEMENTARY TECHNOLOGY

- 5.8.2.1 Cloud computing

- 5.8.3 ADJACENT TECHNOLOGIES

- 5.8.3.1 Artificial Intelligence (AI)

- 5.8.3.2 5G and high-speed networking

- 5.8.1 KEY TECHNOLOGIES

- 5.9 PATENT ANALYSIS

- TABLE 8 INNOVATIONS AND PATENT REGISTRATIONS, 2022-2023

- FIGURE 32 LIST OF MAJOR PATENTS FOR VIRTUAL REALITY, 2013-2023

- FIGURE 33 REGIONAL ANALYSIS OF PATENTS, 2013-2023

- 5.10 TRADE DATA ANALYSIS

- 5.10.1 IMPORT DATA

- FIGURE 34 IMPORT DATA FOR HS CODE 9504-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 9 IMPORT SCENARIO FOR HS CODE 9504-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023 (USD MILLION)

- 5.10.2 EXPORT DATA

- FIGURE 35 EXPORT DATA FOR HS CODE 9504-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 10 EXPORT SCENARIO FOR HS CODE 9504-COMPLIANT PRODUCTS, BY COUNTRY, 2019-2023 (USD MILLION)

- 5.11 KEY CONFERENCES AND EVENTS

- TABLE 11 KEY CONFERENCES AND EVENTS, 2024-2025

- 5.12 CASE STUDY ANALYSIS

- 5.12.1 EUROPEAN MANUFACTURING COMPANY TRANSFORMED MANUFACTURING TRAINING WITH INNOWISE'S VIRTUAL REALITY APP

- 5.12.2 TSINGHUA UNIVERSITY PARTNERED WITH BARCO TO CREATE VIRTUAL SIMULATION DISASTER EMERGENCY RESPONSE LABORATORY

- 5.12.3 NESTLE PURINA ACHIEVED EFFICIENCY AND GAINED PRODUCTIVITY WITH QUEST VR

- 5.12.4 TATA STEEL LIMITED PARTNERED WITH STEEL SIM VR AND VARJO TO IMPROVE SAFETY AND REDUCE COSTS ASSOCIATED WITH TRADITIONAL TRAINING METHODS

- 5.13 TARIFF AND REGULATORY LANDSCAPE

- 5.13.1 COUNTRY-WISE TARIFFS FOR HS CODE 9504-COMPLIANT PRODUCTS

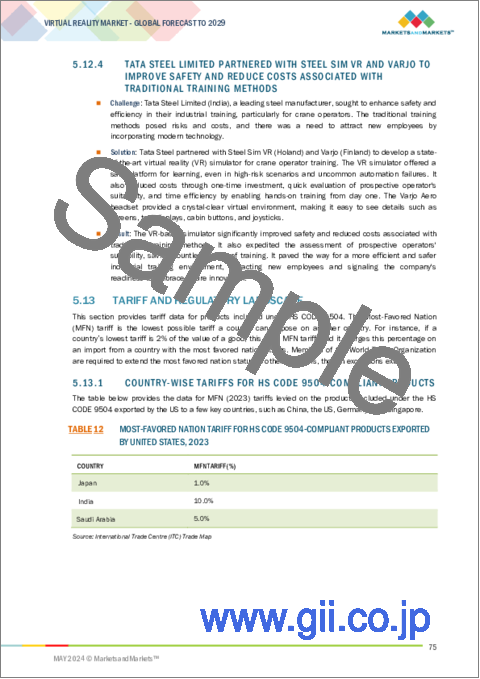

- TABLE 12 MOST-FAVORED NATION TARIFF FOR HS CODE 9504-COMPLIANT PRODUCTS EXPORTED BY UNITED STATES, 2023

- 5.13.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.13.3 REGULATORY STANDARDS

- 5.14 PORTER'S FIVE FORCES ANALYSIS

- TABLE 17 PORTER'S FIVE FORCES' IMPACT ON VIRTUAL REALITY MARKET

- FIGURE 36 PORTER'S FIVE FORCES' ANALYSIS: VIRTUAL REALITY MARKET

- 5.14.1 THREAT OF NEW ENTRANTS

- 5.14.2 THREAT OF SUBSTITUTES

- 5.14.3 BARGAINING POWER OF SUPPLIERS

- 5.14.4 BARGAINING POWER OF BUYERS

- 5.14.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 37 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY OFFERING

- TABLE 18 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY OFFERING (%)

- 5.15.2 BUYING CRITERIA

- FIGURE 38 KEY BUYING CRITERIA, BY APPLICATION

- TABLE 19 KEY BUYING CRITERIA, BY APPLICATION

6 VIRTUAL REALITY MARKET, BY APPLICATION

- 6.1 INTRODUCTION

- FIGURE 39 CONSUMERS SEGMENT TO ACCOUNT FOR LARGEST MARKET DURING FORECAST PERIOD

- TABLE 20 VIRTUAL REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 21 VIRTUAL REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- 6.2 CONSUMERS

- 6.2.1 INCREASING DEMAND, ADVANCED VIRTUAL REALITY HARDWARE EVOLUTION, AND REDUCED COSTS OF VIRTUAL REALITY DEVICES TO CONTRIBUTE TO MARKET GROWTH

- FIGURE 40 HEAD-MOUNTED DISPLAYS SEGMENT FOR CONSUMERS TO ACCOUNT FOR LARGEST MARKET DURING FORECAST PERIOD

- TABLE 22 CONSUMERS: VIRTUAL REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 23 CONSUMERS: VIRTUAL REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 24 CONSUMERS: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2020-2023 (USD MILLION)

- TABLE 25 CONSUMERS: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2024-2029 (USD MILLION)

- TABLE 26 CONSUMERS: VIRTUAL REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 27 CONSUMERS: VIRTUAL REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 28 CONSUMERS: VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 29 CONSUMERS: VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- 6.2.2 GAMING & ENTERTAINMENT

- 6.2.3 SPORTS

- 6.2.4 USE CASES OF VIRTUAL REALITY IN CONSUMER APPLICATIONS

- 6.3 COMMERCIAL

- 6.3.1 STREAMLINED LEARNING EXPERIENCES, EFFECTIVE PROMOTIONS, AND IMPACTFUL ADVERTISING TO FUEL DEMAND FOR VR IN RETAIL AND ECOMMERCE SECTORS

- TABLE 30 COMMERCIAL: VIRTUAL REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 31 COMMERCIAL: VIRTUAL REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 32 COMMERCIAL: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2020-2023 (USD MILLION)

- TABLE 33 COMMERCIAL: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2024-2029 (USD MILLION)

- TABLE 34 COMMERCIAL: VIRTUAL REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 35 COMMERCIAL: VIRTUAL REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 36 COMMERCIAL: VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 37 COMMERCIAL: VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- 6.3.2 RETAIL & ECOMMERCE

- 6.3.3 EDUCATION & TRAINING

- 6.3.4 TRAVEL & TOURISM

- 6.3.5 ADVERTISING

- 6.3.6 USE CASES OF VIRTUAL REALITY IN COMMERCIAL APPLICATIONS

- 6.4 ENTERPRISES (MANUFACTURING)

- 6.4.1 NEED FOR HEIGHTENED LEVEL OF IMMERSION AND ENHANCED COMPREHENSION FOR TRAINEES TO FOSTER MARKET GROWTH

- TABLE 38 ENTERPRISES: VIRTUAL REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 39 ENTERPRISES: VIRTUAL REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 40 ENTERPRISES: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2020-2023 (USD MILLION)

- TABLE 41 ENTERPRISES: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2024-2029 (USD MILLION)

- TABLE 42 ENTERPRISES: VIRTUAL REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 43 ENTERPRISES: VIRTUAL REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 44 ENTERPRISES: VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 45 ENTERPRISES: VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- 6.4.2 USE CASES OF VIRTUAL REALITY IN ENTERPRISE (MANUFACTURING) APPLICATIONS

- 6.5 HEALTHCARE

- 6.5.1 INCREASING ADOPTION OF VIRTUAL REALITY TO ENHANCE SURGICAL PLANNING, TRAINING, AND SKILL DEVELOPMENT TO ACCELERATE MARKET GROWTH

- TABLE 46 HEALTHCARE: VIRTUAL REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 47 HEALTHCARE: VIRTUAL REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 48 HEALTHCARE: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2020-2023 (USD MILLION)

- TABLE 49 HEALTHCARE: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2024-2029 (USD MILLION)

- TABLE 50 HEALTHCARE: VIRTUAL REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 51 HEALTHCARE VIRTUAL REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 52 HEALTHCARE: VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 53 HEALTHCARE: VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- 6.5.2 SURGERY

- 6.5.3 PATIENT CARE MANAGEMENT

- 6.5.4 FITNESS MANAGEMENT

- 6.5.5 PHARMACY MANAGEMENT

- 6.5.6 MEDICAL TRAINING & EDUCATION

- 6.5.7 USE CASES OF VIRTUAL REALITY IN HEALTHCARE APPLICATIONS

- 6.6 AEROSPACE & DEFENSE

- 6.6.1 INTEGRATION OF VIRTUAL REALITY IN COCKPIT DESIGN & TESTING AND VIRTUAL COMBAT TRAINING TO SUPPORT MARKET GROWTH

- TABLE 54 AEROSPACE & DEFENSE: VIRTUAL REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 55 AEROSPACE & DEFENSE: VIRTUAL REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 56 AEROSPACE & DEFENSE: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2020-2023 (USD MILLION)

- TABLE 57 AEROSPACE & DEFENSE: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2024-2029 (USD MILLION)

- TABLE 58 AEROSPACE & DEFENSE: VIRTUAL REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 59 AEROSPACE & DEFENSE: VIRTUAL REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 60 AEROSPACE & DEFENSE: VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 61 AEROSPACE & DEFENSE: VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- 6.6.2 USE CASES OF VIRTUAL REALITY IN AEROSPACE & DEFENSE APPLICATIONS

- 6.7 OTHER APPLICATIONS

- TABLE 62 OTHER APPLICATIONS: VIRTUAL REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 63 OTHER APPLICATIONS: VIRTUAL REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 64 OTHER APPLICATIONS: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2020-2023 (USD MILLION)

- TABLE 65 OTHER APPLICATIONS: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2024-2029 (USD MILLION)

- TABLE 66 OTHER APPLICATIONS: VIRTUAL REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 67 OTHER APPLICATIONS: VIRTUAL REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 68 OTHER APPLICATIONS: VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 69 OTHER APPLICATIONS: VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- 6.7.1 AUTOMOTIVE

- 6.7.2 REAL ESTATE (ARCHITECTURE & BUILDING DESIGN)

- 6.7.3 GEOSPATIAL MINING

- 6.7.4 USE CASES OF VIRTUAL REALITY IN OTHER APPLICATIONS

7 VIRTUAL REALITY MARKET, BY DEVICE TYPE

- 7.1 INTRODUCTION

- FIGURE 41 HEAD-MOUNTED DISPLAYS SEGMENT TO HOLD LARGEST MARKET DURING FORECAST PERIOD

- TABLE 70 VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2020-2023 (USD MILLION)

- TABLE 71 VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2024-2029 (USD MILLION)

- TABLE 72 VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2020-2023 (THOUSAND UNITS)

- TABLE 73 VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2024-2029 (THOUSAND UNITS)

- 7.2 HEAD-MOUNTED DISPLAYS

- 7.2.1 WIDESPREAD USE OF HEAD-MOUNTED DISPLAY DEVICES IN GAMING AND ENTERTAINMENT APPLICATIONS TO DRIVE MARKET

- FIGURE 42 DISPLAY & PROJECTORS SEGMENT FOR HEAD-MOUNTED DISPLAYS TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 74 HEAD-MOUNTED DISPLAYS: VIRTUAL REALITY MARKET, BY COMPONENT, 2020-2023 (USD MILLION)

- TABLE 75 HEAD-MOUNTED DISPLAYS: VIRTUAL REALITY MARKET, BY COMPONENT, 2024-2029 (USD MILLION)

- TABLE 76 HEAD-MOUNTED DISPLAYS: VIRTUAL REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 77 HEAD-MOUNTED DISPLAYS: VIRTUAL REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- 7.3 GESTURE-TRACKING DEVICES

- 7.3.1 GESTURE-TRACKING DEVICES TO MONITOR PATIENTS' MOVEMENTS, PROVIDE REAL-TIME FEEDBACK, AND IMPROVE EFFECTIVENESS OF TREATMENTS

- 7.3.2 DATA GLOVES

- 7.3.3 OTHER GESTURE-TRACKING DEVICES

- FIGURE 43 DISPLAY & PROJECTORS SEGMENT FOR GESTURE-TRACKING DEVICES TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 78 GESTURE-TRACKING DEVICES: VIRTUAL REALITY MARKET, BY COMPONENT, 2020-2023 (USD MILLION)

- TABLE 79 GESTURE-TRACKING DEVICES: VIRTUAL REALITY MARKET, BY COMPONENT, 2024-2029 (USD MILLION)

- TABLE 80 GESTURE-TRACKING DEVICES: VIRTUAL REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 81 GESTURE-TRACKING DEVICES: VIRTUAL REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- 7.4 PROJECTORS & DISPLAY WALLS

- 7.4.1 PROJECTORS AND DISPLAY WALLS TO ENABLE MULTIPLE USERS TO INTERACT WITH VIRTUAL ENVIRONMENTS OR LARGE-SCALE VISUALIZATIONS

- FIGURE 44 DISPLAY & PROJECTORS SEGMENT FOR PROJECTORS & DISPLAY WALLS TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 82 PROJECTORS & DISPLAY WALLS: VIRTUAL REALITY MARKET, BY COMPONENT, 2020-2023 (USD MILLION)

- TABLE 83 PROJECTORS & DISPLAY WALLS: VIRTUAL REALITY MARKET, BY COMPONENT, 2024-2029 (USD MILLION)

- TABLE 84 PROJECTORS & DISPLAY WALLS: VIRTUAL REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 85 PROJECTORS & DISPLAY WALLS: VIRTUAL REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

8 VIRTUAL REALITY MARKET, BY OFFERING

- 8.1 INTRODUCTION

- FIGURE 45 SOFTWARE SEGMENT TO CAPTURE LARGER MARKET DURING FORECAST PERIOD

- TABLE 86 VIRTUAL REALITY MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 87 VIRTUAL REALITY MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- 8.2 HARDWARE

- 8.2.1 VIRTUAL REALITY HARDWARE DEVICES TO CREATE IMMERSIVE AND INTERACTIVE EXPERIENCES IN VARIOUS FIELDS

- FIGURE 46 DISPLAY & PROJECTORS FOR HARDWARE SEGMENT TO CAPTURE LARGEST MARKET DURING FORECAST PERIOD

- TABLE 88 HARDWARE: VIRTUAL REALITY MARKET, BY COMPONENT, 2020-2023 (USD MILLION)

- TABLE 89 HARDWARE: VIRTUAL REALITY MARKET, BY COMPONENT, 2024-2029 (USD MILLION)

- 8.2.2 SENSORS

- 8.2.2.1 Need to detect and capture motions, velocity, magnetic fields, and presence of objects to fuel demand for sensors

- TABLE 90 SENSORS: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2020-2023 (USD MILLION)

- TABLE 91 SENSORS: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2024-2029 (USD MILLION)

- 8.2.2.2 Accelerometers

- 8.2.2.3 Gyroscopes

- 8.2.2.4 Magnetometers

- 8.2.2.5 Proximity sensors

- 8.2.3 SEMICONDUCTOR COMPONENTS

- 8.2.3.1 Significant role of controllers in smartphones and tablets to increase demand for virtual reality devices

- TABLE 92 SEMICONDUCTOR COMPONENTS: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2020-2023 (USD MILLION)

- TABLE 93 SEMICONDUCTOR COMPONENTS: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2024-2029 (USD MILLION)

- 8.2.3.2 Controllers & processors

- 8.2.3.3 Integrated circuits

- 8.2.4 DISPLAY & PROJECTORS

- 8.2.4.1 Display & projectors to shape how users perceive and interact with digital content

- TABLE 94 DISPLAY & PROJECTORS: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2020-2023 (USD MILLION)

- TABLE 95 DISPLAY & PROJECTORS: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2024-2029 (USD MILLION)

- 8.2.5 POSITION TRACKERS

- 8.2.5.1 Position trackers to monitor users' movements accurately and position within virtual or augmented environments

- TABLE 96 POSITION TRACKERS: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2020-2023 (USD MILLION)

- TABLE 97 POSITION TRACKERS: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2024-2029 (USD MILLION)

- 8.2.6 CAMERAS

- 8.2.6.1 Need to enhance user experience, capture user's surroundings, and facilitate outside-in tracking to boost demand for cameras

- TABLE 98 CAMERAS: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2020-2023 (USD MILLION)

- TABLE 99 CAMERAS: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2024-2029 (USD MILLION)

- 8.2.7 OTHER COMPONENTS

- TABLE 100 OTHER COMPONENTS: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2020-2023 (USD MILLION)

- TABLE 101 OTHER COMPONENTS: VIRTUAL REALITY MARKET, BY DEVICE TYPE, 2024-2029 (USD MILLION)

- TABLE 102 HARDWARE: VIRTUAL REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 103 HARDWARE: VIRTUAL REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- 8.3 SOFTWARE

- 8.3.1 VIRTUAL REALITY SOFTWARE TO BLEND DIGITAL INFORMATION AND VIRTUAL OBJECTS SEAMLESSLY WITH REAL-WORLD ENVIRONMENT

- 8.3.2 SDKS

- 8.3.3 CLOUD-BASED SERVICES

- TABLE 104 SOFTWARE: VIRTUAL REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 105 SOFTWARE: VIRTUAL REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

9 VIRTUAL REALITY MARKET, BY TECHNOLOGY

- 9.1 INTRODUCTION

- FIGURE 47 SEMI & FULLY IMMERSIVE SEGMENT TO CAPTURE LARGER MARKET DURING FORECAST PERIOD

- TABLE 106 VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 107 VIRTUAL REALITY MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- 9.2 NON-IMMERSIVE TECHNOLOGY

- 9.2.1 GROWING USE OF NON-IMMERSIVE TECHNOLOGY IN DEVELOPING VIRTUAL REALITY SOFTWARE TO DRIVE MARKET

- 9.3 SEMI-IMMERSIVE AND FULLY IMMERSIVE TECHNOLOGY

- 9.3.1 NEED FOR HIGH LEVEL OF IMMERSION AND AWARENESS OF PHYSICAL WORLD WHILE GAMING TO PROPEL MARKET

10 VIRTUAL REALITY MARKET, BY REGION

- 10.1 INTRODUCTION

- FIGURE 48 NORTH AMERICA ACCOUNTED FOR LARGEST MARKET IN 2023

- TABLE 108 VIRTUAL REALITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 109 VIRTUAL REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 10.2 NORTH AMERICA

- FIGURE 49 NORTH AMERICA: VIRTUAL REALITY MARKET SNAPSHOT

- TABLE 110 NORTH AMERICA: VIRTUAL REALITY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 111 NORTH AMERICA: VIRTUAL REALITY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 112 NORTH AMERICA: VIRTUAL REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 113 NORTH AMERICA: VIRTUAL REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- 10.2.1 US

- 10.2.1.1 Presence of industry giants and need for VR to promote marketing campaigns to drive market

- 10.2.2 CANADA

- 10.2.2.1 Need to streamline workflow automation, enhance operational efficiency, and deliver interactive information within tourism and hospitality sectors to propel market

- 10.2.3 MEXICO

- 10.2.3.1 Advancements in commercial & consumer sectors and utilization of VR in real-life situations to stimulate market expansion

- 10.2.4 RECESSION IMPACT ON VIRTUAL REALITY MARKET IN NORTH AMERICA

- 10.3 EUROPE

- FIGURE 50 EUROPE: VIRTUAL REALITY MARKET SNAPSHOT

- TABLE 114 EUROPE: VIRTUAL REALITY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 115 EUROPE: VIRTUAL REALITY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 116 EUROPE: VIRTUAL REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 117 EUROPE: VIRTUAL REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- 10.3.1 GERMANY

- 10.3.1.1 Widespread adoption of emerging technologies in enterprises to fuel demand for VR solutions

- 10.3.2 FRANCE

- 10.3.2.1 High digital display adoption, increased spending on VR devices, and focus on online advertising to spur market growth

- 10.3.3 UK

- 10.3.3.1 Ongoing investments, presence of major vendors, and predominant focus on content production to foster market growth

- 10.3.4 REST OF EUROPE

- 10.3.5 RECESSION IMPACT ON VIRTUAL REALITY MARKET IN EUROPE

- 10.4 ASIA PACIFIC

- FIGURE 51 ASIA PACIFIC: VIRTUAL REALITY MARKET SNAPSHOT

- TABLE 118 ASIA PACIFIC: VIRTUAL REALITY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 119 ASIA PACIFIC: VIRTUAL REALITY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 120 ASIA PACIFIC: VIRTUAL REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 121 ASIA PACIFIC: VIRTUAL REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- 10.4.1 CHINA

- 10.4.1.1 Emergence of numerous start-ups, focus on exploring emerging technologies, and rising trends of expos and conferences to drive market

- 10.4.2 INDIA

- 10.4.2.1 Heightened awareness of advanced technology and extensive R&D to accelerate market growth

- 10.4.3 JAPAN

- 10.4.3.1 Growing integration of advanced technologies within healthcare sector to boost demand for VR solutions

- 10.4.4 SOUTH KOREA

- 10.4.4.1 Digital transformation within industrial sector to stimulate market growth

- 10.4.5 REST OF ASIA PACIFIC

- 10.4.6 RECESSION IMPACT ON VIRTUAL REALITY MARKET IN ASIA PACIFIC

- 10.5 ROW

- TABLE 122 ROW: VIRTUAL REALITY MARKET, BY SUBREGION, 2020-2023 (USD MILLION)

- TABLE 123 ROW: VIRTUAL REALITY MARKET, BY SUBREGION, 2024-2029 (USD MILLION)

- TABLE 124 ROW: VIRTUAL REALITY MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 125 ROW: VIRTUAL REALITY MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- 10.5.1 SOUTH AMERICA

- 10.5.1.1 Expanding consumer market, favorable low-interest rates, and robust commodity pricing to bolster market growth

- 10.5.2 MIDDLE EAST & AFRICA

- 10.5.2.1 Rising incorporation of virtual reality into various applications of healthcare industry to propel market

- TABLE 126 MIDDLE EAST & AFRICA: VIRTUAL REALITY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 127 MIDDLE EAST & AFRICA: VIRTUAL REALITY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 10.5.2.2 GCC countries

- 10.5.2.2.1 Rising government focus on digital transformation and increasing awareness regarding benefits of wearable VR to spur market growth

- 10.5.2.3 Rest of Middle East & Africa

- 10.5.2.2 GCC countries

- 10.5.3 RECESSION IMPACT ON VIRTUAL REALITY MARKET IN ROW

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- TABLE 128 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS

- 11.3 MARKET SHARE ANALYSIS

- FIGURE 52 VIRTUAL REALITY MARKET SHARE ANALYSIS, 2023

- TABLE 129 VIRTUAL REALITY MARKET: DEGREE OF COMPETITION, 2023

- 11.4 REVENUE ANALYSIS, 2019-2023

- FIGURE 53 VIRTUAL REALITY MARKET: REVENUE ANALYSIS OF TOP PLAYERS, 2019-2023

- 11.5 COMPANY VALUATION AND FINANCIAL METRICS

- FIGURE 54 COMPANY VALUATION AND FINANCIAL METRICS: VIRTUAL REALITY MARKET

- 11.5.1 VIRTUAL REALITY MARKET: FINANCIAL METRICS

- FIGURE 55 FINANCIAL METRICS (EV/EBITDA), 2023

- 11.6 VIRTUAL REALITY MARKET: BRAND/PRODUCT COMPARISON

- FIGURE 56 BRAND COMPARISON

- 11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- FIGURE 57 VIRTUAL REALITY MARKET: COMPANY EVALUATION MATRIX FOR KEY PLAYERS, 2023

- 11.7.5 COMPANY FOOTPRINT

- 11.7.5.1 Company footprint

- FIGURE 58 VIRTUAL REALITY MARKET: OVERALL COMPANY FOOTPRINT

- 11.7.5.2 Technology footprint

- TABLE 130 VIRTUAL REALITY MARKET: TECHNOLOGY FOOTPRINT

- 11.7.5.3 Offering footprint

- TABLE 131 VIRTUAL REALITY MARKET: OFFERING FOOTPRINT

- 11.7.5.4 Device type footprint

- TABLE 132 VIRTUAL REALITY MARKET: DEVICE TYPE FOOTPRINT

- 11.7.5.5 Application footprint

- TABLE 133 VIRTUAL REALITY MARKET: APPLICATION FOOTPRINT

- 11.7.5.6 Regional footprint

- TABLE 134 VIRTUAL REALITY MARKET: REGIONAL FOOTPRINT

- 11.8 COMPANY EVALUATION MATRIX: START-UPS/SMES, 2023

- 11.8.1 PROGRESSIVE COMPANIES

- 11.8.2 RESPONSIVE COMPANIES

- 11.8.3 DYNAMIC COMPANIES

- 11.8.4 STARTING BLOCKS

- FIGURE 59 VIRTUAL REALITY MARKET: COMPANY EVALUATION MATRIX FOR START-UPS/SMES, 2023

- 11.8.5 COMPETITIVE BENCHMARKING, START-UPS/SMES, 2023

- 11.8.5.1 Detailed list of key start-ups/SMEs

- TABLE 135 VIRTUAL REALITY MARKET: LIST OF KEY START-UPS/SMES

- 11.8.6 COMPETITIVE BENCHMARKING OF KEY START-UPS/SMES

- TABLE 136 VIRTUAL REALITY MARKET: COMPETITIVE BENCHMARKING OF KEY START-UPS/SMES

- 11.9 COMPETITIVE SCENARIOS AND TRENDS

- 11.9.1 PRODUCT LAUNCHES

- TABLE 137 VIRTUAL REALITY MARKET: PRODUCT LAUNCHES, 2020-2023

- 11.9.2 DEALS

- TABLE 138 VIRTUAL REALITY MARKET: DEALS, 2020-2023

12 COMPANY PROFILES

- (Business Overview, Products/Solutions/Services Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats))**

- 12.1 KEY PLAYERS

- 12.1.1 SONY

- TABLE 139 SONY: BUSINESS OVERVIEW

- FIGURE 60 SONY: COMPANY SNAPSHOT

- TABLE 140 SONY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 141 SONY: PRODUCT LAUNCHES AND ENHANCEMENTS

- 12.1.2 SAMSUNG ELECTRONICS CO., LTD.

- TABLE 142 SAMSUNG ELECTRONICS CO., LTD.: BUSINESS OVERVIEW

- FIGURE 61 SAMSUNG ELECTRONICS CO., LTD.: COMPANY SNAPSHOT

- TABLE 143 SAMSUNG ELECTRONICS CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.3 MICROSOFT

- TABLE 144 MICROSOFT: BUSINESS OVERVIEW

- FIGURE 62 MICROSOFT: COMPANY SNAPSHOT

- TABLE 145 MICROSOFT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 146 MICROSOFT: DEALS

- 12.1.4 META

- TABLE 147 META: BUSINESS OVERVIEW

- FIGURE 63 META: COMPANY SNAPSHOT

- TABLE 148 META: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 149 META: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 150 META: DEALS

- 12.1.5 HTC CORPORATION

- TABLE 151 HTC CORPORATION: BUSINESS OVERVIEW

- FIGURE 64 HTC CORPORATION: COMPANY SNAPSHOT

- TABLE 152 HTC CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 153 HTC CORPORATION: PRODUCT LAUNCHES AND ENHANCEMENTS

- 12.1.6 BARCO

- TABLE 154 BARCO: BUSINESS OVERVIEW

- FIGURE 65 BARCO: COMPANY SNAPSHOT

- TABLE 155 BARCO: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 156 BARCO: DEALS

- 12.1.7 PICO IMMERSIVE PTE.LTD.

- TABLE 157 PICO IMMERSIVE PTE. LTD.: BUSINESS OVERVIEW

- TABLE 158 PICO IMMERSIVE PTE.LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 159 PICO IMMERSIVE PTE.LTD.: PRODUCT LAUNCHES AND ENHANCEMENTS

- 12.1.8 CYBERGLOVE SYSTEMS INC.

- TABLE 160 CYBERGLOVE SYSTEMS INC.: BUSINESS OVERVIEW

- TABLE 161 CYBERGLOVE SYSTEMS INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.9 UNITY TECHNOLOGIES

- TABLE 162 UNITY TECHNOLOGIES: BUSINESS OVERVIEW

- FIGURE 66 UNITY TECHNOLOGIES: COMPANY SNAPSHOT

- TABLE 163 UNITY TECHNOLOGIES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.10 PENUMBRA, INC.

- TABLE 164 PENUMBRA, INC.: BUSINESS OVERVIEW

- FIGURE 67 PENUMBRA, INC.: COMPANY SNAPSHOT

- TABLE 165 PENUMBRA, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 166 PENUMBRA, INC.: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 167 PENUMBRA, INC.: DEALS

- 12.1.11 DPVR

- TABLE 168 DPVR: BUSINESS OVERVIEW

- TABLE 169 DPVR: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 170 DPVR: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 171 DPVR: DEALS

- 12.2 OTHER PLAYERS

- 12.2.1 ULTRALEAP

- 12.2.2 FOVE INC

- 12.2.3 QUYTECH

- 12.2.4 HQSOFTWARE

- 12.2.5 INNOWISE

- 12.2.6 XRHEALTH IL LTD.

- 12.2.7 VECTION TECHNOLOGIES

- 12.2.8 MINDMAZE

- 12.2.9 FIRSTHAND TECHNOLOGY

- 12.2.10 WORLDVIZ, INC.

- 12.2.11 VIRTUIX

- 12.2.12 VIGHNESH INC.

- 12.2.13 MERGE LABS, INC.

- 12.2.14 SPACEVR

- *Details on Business Overview, Products/Solutions/Services Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats) might not be captured in case of unlisted companies.

13 APPENDIX

- 13.1 INSIGHTS FROM INDUSTRY EXPERTS

- 13.2 DISCUSSION GUIDE

- 13.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.4 CUSTOMIZATION OPTIONS

- 13.5 RELATED REPORTS

- 13.6 AUTHOR DETAILS