|

|

市場調査レポート

商品コード

1467216

決済ゲートウェイの世界市場:タイプ別、業界別、地域別 - 2029年までの予測Payment Gateway Market by Type (Hosted, Self-hosted), Vertical (Retail & E-commerce, BFSI, Telecom, Healthcare, Media & Entertainment, Travel & Hospitality, IT & ITeS) and Region - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 決済ゲートウェイの世界市場:タイプ別、業界別、地域別 - 2029年までの予測 |

|

出版日: 2024年04月10日

発行: MarketsandMarkets

ページ情報: 英文 227 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

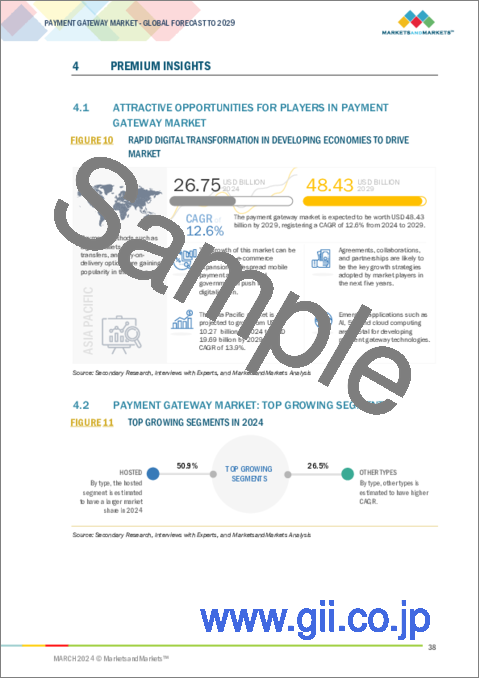

決済ゲートウェイの市場規模は、2024年には267億米ドルになるとみられ、2029年には484億米ドルに達すると予測されており、年間平均成長率(CAGR)は12.6%になると見込まれています。

ブロックチェーン技術は、安全で分散化された透明性の高い台帳システムを提供することで、決済処理に革命をもたらす計り知れない可能性を秘めています。ブロックチェーンの統合を模索する決済ゲートウェイは、業界の将来的な進歩に向けて自らを位置づけることができます。ブロックチェーン技術を活用することで、決済ゲートウェイは取引プロセスを合理化し、手数料を削減し、暗号プロトコルと分散型コンセンサスメカニズムを通じてセキュリティを強化することができます。さらに、ブロックチェーンを利用した決済ソリューションは透明性を高め、取引のリアルタイム追跡を可能にし、決済履歴の不変記録を提供します。この透明性は、加盟店と消費者間の信頼を高めるだけでなく、詐欺や紛争のリスクを軽減します。さらに、ブロックチェーン技術は国境を越えた決済をより効率的に実行することを可能にし、仲介者の必要性を排除し、取引時間とコストを削減します。ブロックチェーン技術の採用が拡大し続ける中、ブロックチェーン統合を採用する決済ゲートウェイは、決済処理の効率性、安全性、革新性の向上というメリットを享受し、進化するフィンテックの展望におけるリーダーとしての地位を確立することになるでしょう。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2018年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 検討単位 | 金額(10億米ドル) |

| セグメント別 | タイプ別(ホスト型、セルフホスト型、その他)業界別 |

| 対象地域 | 北米、欧州、アジア太平洋、中東・アフリカ、ラテンアメリカ |

ゲーム内の仮想通貨は現代のゲームの定番となっており、プレイヤーがゲーム内のさまざまなアイテムや機能強化、追加コンテンツのためにマイクロトランザクションを行う手段として機能しています。決済ゲートウェイは、これらの仮想通貨を管理するシステムと統合することで、これらの取引を促進する重要な役割を果たしています。そうすることで、ユーザーは実際のお金で安全に仮想通貨を購入することができ、面倒な決済プロセスを必要とせずにゲーム体験を向上させることができます。この統合は、ゲーマーの購入プロセスを合理化するだけでなく、取引の安全性と信頼性を確保し、ゲーム・エコシステム内でマイクロトランザクションを行うユーザーに信頼感を与えます。さらに、ゲーム内の仮想通貨システムとのシームレスな統合を可能にすることで、決済ゲートウェイはゲーム開発者の収益化戦略に貢献し、有利な収益源としてマイクロトランザクションを活用することを可能にします。ゲーム業界が進化を続け、デジタルエコノミーを受け入れるにつれ、リアルマネーとゲーム内仮想通貨とのシームレスな交換を促進する決済ゲートウェイは、ゲーム商取引の未来を形作る上でますます重要な役割を果たすようになっています。

北米はデジタルウォレットの導入におけるリーダーとして際立っており、Apple PayやGoogle Pay、Venmoのような地域プレイヤーといった広く受け入れられているプラットフォームが消費者の間で大きな支持を得ています。これらの一般的なデジタルウォレットオプションとシームレスに統合する決済ゲートウェイは、消費者の嗜好に対応し、チェックアウトプロセスを合理化する上で極めて重要な役割を果たします。広く利用されているこれらのデジタルウォレットとの互換性を提供することで、決済ゲートウェイは顧客に便利で使い慣れた決済体験を提供し、数回のタップやクリックだけで安全に取引を完了できるようにします。この統合により、チェックアウトプロセスの全体的な利便性が向上するだけでなく、消費者は信頼できるデジタルウォレットプロバイダーに支払い情報の保護を任せることができるため、信頼感を抱くようになります。さらに、一般的なデジタルウォレットとのシームレスな統合を促進することで、決済ゲートウェイは、加盟店がこれらのプラットフォームの広範な採用を活用することを可能にし、競争の激しい北米市場でより高いコンバージョン率を促進し、顧客ロイヤルティを育成します。デジタルウォレットの利用が急増し続ける中、これらの一般的な選択肢との統合を優先する決済ゲートウェイは、消費者と加盟店双方の進化するニーズに対応し、決済エコシステムのさらなる成長と革新を促進する好位置にあります。

当レポートでは、世界の決済ゲートウェイ市場について調査し、タイプ別、業界別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要と業界動向

- イントロダクション

- 市場力学

- 決済ゲートウェイ技術の略歴

- エコシステム/市場マップ

- 決済ゲートウェイ投資の情勢

- ケーススタディ分析

- バリューチェーン分析

- 北米

- 欧州

- アジア太平洋

- その他の地域

- 特許分析

- 価格分析

- ポーターのファイブフォース分析

- 顧客のビジネスに影響を与える動向と混乱

- 主な利害関係者と購入基準

- 2024年の主な会議とイベント

- 技術分析

- 決済ゲートウェイ市場におけるベストプラクティス

- 現在のビジネスモデルと新たなビジネスモデル

- 決済ゲートウェイツール、フレームワーク、テクニック

- 決済ゲートウェイ市場の将来情勢

第6章 決済ゲートウェイ市場、タイプ別

- イントロダクション

- ホスト型

- セルフホスト型

- その他

第7章 決済ゲートウェイ市場、業界別

- イントロダクション

- BFSI

- 通信

- ヘルスケア

- メディアとエンターテイメント

- 旅行とホスピタリティ

- ITとITES

- 小売・eコマース

- その他

第8章 決済ゲートウェイ市場、地域別

- イントロダクション

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

第9章 競合情勢

- イントロダクション

- 主要参入企業の戦略/強み

- 収益分析

- 市場シェア分析

- 企業評価マトリックス

- スタートアップ/中小企業評価マトリックス

- 競合シナリオと動向

- 決済ゲートウェイ製品のベンチマーク

- 主要な決済ゲートウェイプロバイダーの評価と財務指標

第10章 企業プロファイル

- 主要参入企業

- PAYPAL

- FISERV

- STRIPE

- VISA

- AMAZON

- MASTERCARD

- FIS

- BLOCK

- GLOBAL PAYMENTS

- ADYEN

- APPLE

- J.P. MORGAN

- ALIBABA GROUP

- RAZORPAY

- PHONEPE

- PAYSAFE

- VERIFONE

第11章 企業プロファイル

- スタートアップ/中小企業

- FIDELITY PAYMENT SERVICES

- EASEBUZZ

- BLUESNAP

- WINDCAVE

- HELCIM

- INFIBEAM AVENUES LIMITED(IAL)

- NOWPAYMENTS

- INSTAMOJO

- COINGATE

- IPPOPAY

- PAYJUNCTION

- LYRA NETWORK

第12章 隣接/関連市場

第13章 付録

The payment gateway market is estimated at USD 26.7 billion in 2024 to USD 48.4 billion by 2029, at a Compound Annual Growth Rate (CAGR) of 12.6%. Blockchain technology holds immense potential to revolutionize payment processing by offering a secure, decentralized, and transparent ledger system. Payment gateways that explore blockchain integration can position themselves for future advancements in the industry. By leveraging blockchain technology, payment gateways can streamline transaction processes, reduce fees, and enhance security through cryptographic protocols and distributed consensus mechanisms. Additionally, blockchain-based payment solutions offer greater transparency, enabling real-time tracking of transactions and providing an immutable record of payment history. This transparency not only enhances trust between merchants and consumers but also mitigates the risk of fraud and disputes. Furthermore, blockchain technology enables cross-border payments to be executed more efficiently, eliminating the need for intermediaries and reducing transaction times and costs. As the adoption of blockchain technology continues to grow, payment gateways that embrace blockchain integration stand to benefit from greater efficiency, security, and innovation in payment processing, positioning themselves as leaders in the evolving fintech landscape.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2018-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD) Billion |

| Segments | By type (hosted, self-hosted, other types) vertical |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

"The other payment gateway types segment is expected to hold the second largest market size during the forecast period." Integrating with local banks presents a significant opportunity for payment gateways to leverage existing security protocols and fraud prevention measures implemented by these institutions. By aligning with the security infrastructure of trusted local banks, payment gateways can enhance the overall security and reliability of their payment processing services. This integration not only helps to mitigate the risk of fraud but also builds trust with customers who may be hesitant to use unfamiliar payment methods or platforms. Customers often place a high value on the security measures implemented by their banks, and by partnering with these institutions, payment gateways can reassure customers that their financial transactions are conducted in a secure environment. Moreover, integrating with local banks allows payment gateways to offer a wider range of payment options, including bank transfers and direct debits, catering to the preferences of customers who prefer traditional banking methods. Overall, this collaboration between payment gateways and local banks not only enhances security but also fosters customer trust and satisfaction, driving greater adoption and usage of digital payment solutions.

"The media & entertainment segment to register the fastest growth rate during the forecast period." In-game virtual currencies have become a staple of modern gaming, serving as a means for players to make microtransactions for various in-game items, enhancements, or additional content. Payment gateways play a crucial role in facilitating these transactions by integrating with the systems managing these virtual currencies. By doing so, users can securely purchase these virtual currencies with real money, enhancing their gaming experience without the need for cumbersome payment processes. This integration not only streamlines the purchasing process for gamers but also ensures the security and reliability of transactions, instilling confidence in users as they engage in microtransactions within the gaming ecosystem. Furthermore, by enabling seamless integration with in-game virtual currency systems, payment gateways contribute to the monetization strategies of game developers, allowing them to leverage microtransactions as a lucrative revenue stream. As the gaming industry continues to evolve and embrace digital economies, payment gateways that facilitate the seamless exchange between real money and in-game virtual currencies are poised to play an increasingly vital role in shaping the future of gaming commerce.

"North America to hold second largest highest market size during the forecast period."

North America stands out as a leader in the adoption of digital wallets, with widely embraced platforms such as Apple Pay, Google Pay, and regional players like Venmo gaining significant traction among consumers. Payment gateways that seamlessly integrate with these popular digital wallet options play a pivotal role in catering to consumer preferences and streamlining the checkout process. By offering compatibility with these widely used digital wallets, payment gateways provide customers with a convenient and familiar payment experience, allowing them to securely complete transactions with just a few taps or clicks. This integration not only enhances the overall convenience of the checkout process but also instills confidence in consumers, as they can rely on trusted digital wallet providers to safeguard their payment information. Moreover, by facilitating seamless integration with popular digital wallets, payment gateways enable merchants to capitalize on the widespread adoption of these platforms, driving higher conversion rates and fostering customer loyalty in the competitive North American market. As digital wallet usage continues to soar, payment gateways that prioritize integration with these popular options are well-positioned to meet the evolving needs of consumers and merchants alike, driving further growth and innovation in the payment ecosystem.

In-depth interviews have been conducted with chief executive officers (CEOs), Directors, and other executives from various key organizations operating in the payment gateway market.

- By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: C-level -35%, D-level - 25%, and Others - 40%

- By Region: North America - 30%, Europe - 30%, Asia Pacific - 25%, Latin America- 5%, and Middle East & Africa - 10%,

The major players in the payment gateway JP Morgan (US), Paypal (US), Amazon (US), Visa (US), Mastercard (US), PhonPe (India), Razorpay (India), Alibaba (China), Stripe (Ireland), Adyen (Netherlands), Block, Inc (US), FIS (US), Global Payments (US), Apple (US), Fiserv (US), Verifone (US), Paysafe (UK), Fidelity payments (US), Easebuzz (India), Bluesnap (US), Windcave (US), Helcim (US), Instamojo (India), Infibeam Avenue (US), NOWPayments (Netherlands), CoinGate (Lithuania), Ippopay (India), PayJunction (US), Lyra Network (US). These players have adopted various growth strategies, such as partnerships, agreements and collaborations, new product launches, enhancements, and acquisitions to expand their payment gateway market footprint.

Research Coverage

The market study covers the payment gateway market size across different segments. It aims at estimating the market size and the growth potential across different segments, including By type ( hosted, self-hosted, other types) vertical (BFSI, retail & ecommerce, telecom, healthcare, media and entertainment, travel and hospitality, it & ites, other verticals)and Region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The study includes an in-depth competitive analysis of the leading market players, their company profiles, key observations related to product and business offerings, recent developments, and market strategies.

Key Benefits of Buying the Report

The report will help the market leaders/new entrants with information on the closest approximations of the global payment gateway market's revenue numbers and subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. Moreover, the report will provide insights for stakeholders to understand the market's pulse and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

1.Analysis of key drivers ( Rapid growth in eCommerce, Mobile payment Adoption, globalization of business transactions ), restraints (Regulatory Compliance, dependency on Banking Infrastructure, ), opportunities (Blockchain and cryptocurrency Integration, Value-Added Services), and challenges (Customer trust and data privacy, changing consumer behavior) influencing the growth of the payment gateway market.

2.Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the payment gateway market.

3.Market Development: Comprehensive information about lucrative markets - the report analyses the payment gateway market across various regions.

4.Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the payment gateway market.

5.Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading include JP Morgan (US), Paypal (US), Amazon (US), Visa (US), Mastercard (US), PhonPe (India), Razorpay (India), Alibaba (China), Stripe (Ireland), Adyen (Netherlands), Block, Inc (US), FIS (US), Global Payments (US), Apple (US), Fiserv (US), Verifone (US), Paysafe (UK), Fidelity payments (US), Easebuzz (India), Bluesnap (US), Windcave (US), Helcim (US), Instamojo (India), Infibeam Avenue (US), NOWPayments (Netherlands), CoinGate (Lithuania), Ippopay (India), PayJunction (US), Lyra Network (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- 1.3.3 INCLUSIONS & EXCLUSIONS

- 1.3.4 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- TABLE 1 USD EXCHANGE RATES, 2021-2023

- 1.5 STAKEHOLDERS

- 1.6 IMPACT OF RECESSION

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 PAYMENT GATEWAY MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary interviews with experts

- 2.1.2.2 Breakdown of primary profiles

- FIGURE 2 BREAKDOWN OF PRIMARY INTERVIEWS, BY COMPANY TYPE, DESIGNATION, AND REGION

- 2.1.2.3 Key insights from industry experts

- 2.2 MARKET SIZE ESTIMATION

- FIGURE 3 PAYMENT GATEWAY MARKET: TOP-DOWN AND BOTTOM-UP APPROACHES

- 2.2.1 TOP-DOWN APPROACH

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY - APPROACH 1 (SUPPLY SIDE): REVENUE OF VENDORS IN PAYMENT GATEWAY MARKET

- 2.2.2 BOTTOM-UP APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY - APPROACH 2 (DEMAND SIDE): PAYMENT GATEWAY MARKET

- FIGURE 6 MARKET SIZE ESTIMATION USING BOTTOM-UP APPROACH

- 2.3 DATA TRIANGULATION

- FIGURE 7 DATA TRIANGULATION AND MARKET BREAKUP

- 2.4 RISK ASSESSMENT

- TABLE 2 RISK ASSESSMENT

- 2.5 RESEARCH ASSUMPTIONS

- TABLE 3 RESEARCH ASSUMPTIONS

- 2.6 LIMITATIONS

- 2.7 IMPLICATION OF RECESSION ON PAYMENT GATEWAY MARKET

3 EXECUTIVE SUMMARY

- FIGURE 8 PAYMENT GATEWAY MARKET TO WITNESS SIGNIFICANT GROWTH DURING FORECAST PERIOD

- FIGURE 9 PAYMENT GATEWAY MARKET: REGIONAL SNAPSHOT

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PAYMENT GATEWAY MARKET

- FIGURE 10 RAPID DIGITAL TRANSFORMATION IN DEVELOPING ECONOMIES TO DRIVE MARKET

- 4.2 PAYMENT GATEWAY MARKET: TOP GROWING SEGMENTS

- FIGURE 11 TOP GROWING SEGMENTS IN 2024

- 4.3 PAYMENT GATEWAY MARKET, BY TYPE

- FIGURE 12 HOSTED SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- 4.4 PAYMENT GATEWAY MARKET, BY VERTICAL

- FIGURE 13 RETAIL & E-COMMERCE TO HOLD LARGEST MARKET DURING FORECAST PERIOD

- 4.5 NORTH AMERICA: PAYMENT GATEWAY MARKET, BY OFFERING AND VERTICAL

- FIGURE 14 HOSTED SEGMENT AND RETAIL & E-COMMERCE ESTIMATED TO HOLD LARGEST MARKET SHARES IN 2024

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 15 PAYMENT GATEWAY MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Rapid Growth in E-commerce

- 5.2.1.2 Mobile Payment Adoption

- FIGURE 16 RISING VOLUME OF UPI PAYMENTS, 2016 TO 2023 (MILLION)

- 5.2.1.3 Globalization of Business Transactions

- 5.2.2 RESTRAINTS

- 5.2.2.1 Regulatory Compliance

- 5.2.2.2 Dependency on Banking Infrastructure

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Blockchain and Cryptocurrency Integration

- 5.2.3.2 Value-added Services

- 5.2.4 CHALLENGES

- 5.2.4.1 Customer Trust and Data Privacy

- 5.2.4.2 Changing Consumer Behavior

- 5.3 BRIEF HISTORY OF PAYMENT GATEWAY TECHNOLOGY

- FIGURE 17 BRIEF HISTORY OF PAYMENT GATEWAY TECHNOLOGY

- 5.3.1 1960-1990

- 5.3.2 1990-2000

- 5.3.3 2000-2010

- 5.3.4 2010-2020

- 5.3.5 202O-PRESENT

- 5.4 ECOSYSTEM/MARKET MAP

- FIGURE 18 KEY PLAYERS IN PAYMENT GATEWAY MARKET ECOSYSTEM

- TABLE 4 PAYMENT GATEWAY MARKET: ECOSYSTEM

- 5.5 PAYMENT GATEWAY INVESTMENT LANDSCAPE

- 5.6 CASE STUDY ANALYSIS

- 5.6.1 CASE STUDY 1: RAZORPAY OPTIMIZER HELPED CRAFT FABINDIA'S PAYMENTS SUCCESS STORY

- 5.6.2 CASE STUDY 2: SRI BALAJI UNIVERSITY REDUCED 90% OF RECONCILIATION EFFORTS USING FEESBUZZ AND FORMS

- 5.6.3 CASE STUDY 3: PAN HOME COLLABORATED WITH AMAZON PAYMENT SERVICES TO TRANSFORM CUSTOMER EXPERIENCE

- 5.6.4 CASE STUDY 4: COINGATE EMPOWERED BACLOUD WITH CRYPTOCURRENCY PAYMENT SOLUTIONS

- 5.6.5 CASE STUDY 5: STRIPE HELPED INCREASE TWILIO'S 10% AUTHORIZATION RATE

- 5.6.6 CASE STUDY 6: NAMELY STREAMLINED PAYMENTS AND BOOSTED EFFICIENCY WITH BLUESNAP INTEGRATION

- 5.7 VALUE CHAIN ANALYSIS

- FIGURE 19 PAYMENT GATEWAY MARKET: VALUE CHAIN ANALYSIS

- 5.7.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 5 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 6 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 7 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 8 REST OF THE WORLD: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.8 NORTH AMERICA

- 5.8.1 US

- 5.8.2 CANADA

- 5.9 EUROPE

- 5.9.1 GERMANY

- 5.9.2 UK

- 5.10 ASIA PACIFIC

- 5.10.1 CHINA

- 5.10.2 INDIA

- 5.10.3 JAPAN

- 5.11 REST OF THE WORLD

- 5.11.1 QATAR

- 5.11.2 MEXICO

- 5.12 PATENT ANALYSIS

- FIGURE 20 LIST OF MAJOR PATENTS FOR PAYMENT GATEWAY

- 5.12.1 LIST OF MAJOR PATENTS

- 5.13 PRICING ANALYSIS

- 5.13.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY BILLING CYCLE

- FIGURE 21 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY BILLING CYCLE

- TABLE 9 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY PAYMENT TYPE (USD)

- 5.13.2 INDICATIVE PRICING ANALYSIS OF KEY PLAYERS, BY FEATURE

- TABLE 10 INDICATIVE PRICING ANALYSIS OF PAYMENT GATEWAYS, BY FEATURE (USD)

- 5.14 PORTER'S FIVE FORCES ANALYSIS

- TABLE 11 PAYMENT GATEWAY MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 22 PORTER'S FIVE FORCES ANALYSIS: PAYMENT GATEWAY MARKET

- 5.14.1 THREAT OF NEW ENTRANTS

- 5.14.2 THREAT OF SUBSTITUTES

- 5.14.3 BARGAINING POWER OF BUYERS

- 5.14.4 BARGAINING POWER OF SUPPLIERS

- 5.14.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.15 TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 23 TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.16 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.16.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 24 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS

- TABLE 12 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS (%)

- 5.16.2 BUYING CRITERIA

- FIGURE 25 KEY BUYING CRITERIA FOR TOP THREE END USERS

- TABLE 13 KEY BUYING CRITERIA FOR TOP END USERS

- 5.17 KEY CONFERENCES & EVENTS IN 2024

- TABLE 14 PAYMENT GATEWAY MARKET: DETAILED LIST OF CONFERENCES & EVENTS, 2024

- 5.18 TECHNOLOGY ANALYSIS

- 5.18.1 KEY TECHNOLOGIES

- 5.18.1.1 Encryption and Tokenization

- 5.18.1.2 Artificial Intelligence

- 5.18.1.3 Contactless Payments

- 5.18.2 ADJACENT TECHNOLOGIES

- 5.18.2.1 Biometric Authentication

- 5.18.2.2 IoT

- 5.18.2.3 Blockchain

- 5.18.3 COMPLEMENTARY TECHNOLOGIES

- 5.18.3.1 5G Technology

- 5.18.3.2 Voice Recognition Technology

- 5.18.1 KEY TECHNOLOGIES

- 5.19 BEST PRACTICES IN PAYMENT GATEWAY MARKET

- 5.19.1 SECURITY COMPLIANCE

- 5.19.2 FRAUD PREVENTION

- 5.19.3 RELIABILITY AND UPTIME

- 5.19.4 USER-FRIENDLY INTERFACE

- 5.19.5 FAST TRANSACTION PROCESSING

- 5.19.6 SCALABILITY

- 5.19.7 TRANSPARENT PRICING

- 5.19.8 GLOBAL PAYMENT SUPPORT

- 5.19.9 ROBUST API DOCUMENTATION

- 5.19.10 CUSTOMER SUPPORT

- 5.19.11 REGULAR UPDATES AND INNOVATION

- 5.19.12 COMPLIANCE WITH REGULATORY STANDARDS

- 5.20 CURRENT AND EMERGING BUSINESS MODELS

- 5.20.1 TRANSACTION-BASED MODEL

- 5.20.2 SUBSCRIPTION-BASED MODELS

- 5.20.3 VALUE-ADDED SERVICES MODEL

- 5.20.4 API-FIRST APPROACH

- 5.20.5 INTEGRATED SERVICE MODELS

- 5.20.6 CROSS-BORDER PAYMENT SOLUTIONS

- 5.20.7 CONTACTLESS AND NFC PAYMENTS

- 5.20.8 EMBEDDED FINANCE

- 5.21 PAYMENT GATEWAY TOOLS, FRAMEWORKS, AND TECHNIQUES

- 5.22 FUTURE LANDSCAPE OF PAYMENT GATEWAY MARKET

- 5.22.1 SHORT-TERM ROADMAP (2023-2025)

- 5.22.2 MID-TERM ROADMAP (2025-2028)

- 5.22.3 LONG-TERM ROADMAP (2029-2030)

6 PAYMENT GATEWAY MARKET, BY TYPE

- 6.1 INTRODUCTION

- FIGURE 26 HOSTED SEGMENT TO HOLD LARGEST MARKET SIZE DURING FORECAST PERIOD

- 6.1.1 TYPE: PAYMENT GATEWAY MARKET DRIVERS

- TABLE 15 PAYMENT GATEWAY MARKET, BY TYPE, 2018-2023 (USD MILLION)

- TABLE 16 PAYMENT GATEWAY MARKET, BY TYPE, 2024-2029 (USD MILLION)

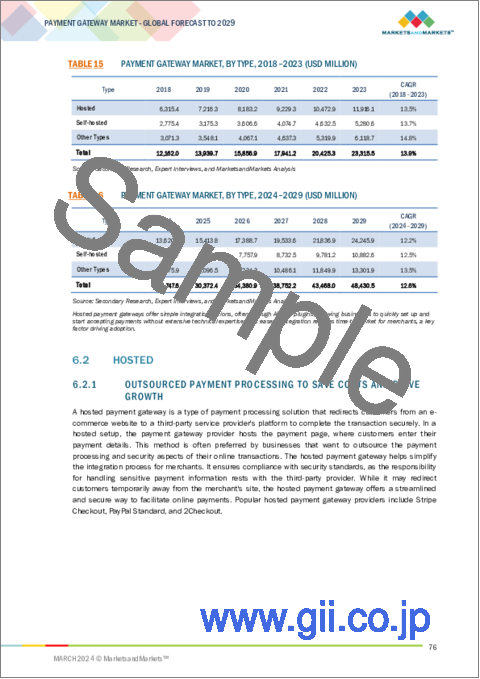

- 6.2 HOSTED

- 6.2.1 OUTSOURCED PAYMENT PROCESSING TO SAVE COSTS AND DRIVE GROWTH

- TABLE 17 HOSTED: PAYMENT GATEWAY MARKET, BY REGION, 2018-2023 (USD MILLION)

- TABLE 18 HOSTED: PAYMENT GATEWAY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 6.3 SELF-HOSTED

- 6.3.1 CUSTOMIZED PAYMENT PROCESSING TO DRIVE GROWTH

- TABLE 19 SELF-HOSTED: PAYMENT GATEWAY MARKET, BY REGION, 2018-2023 (USD MILLION)

- TABLE 20 SELF-HOSTED: PAYMENT GATEWAY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 6.4 OTHER TYPES

- TABLE 21 OTHER TYPES: PAYMENT GATEWAY MARKET, BY REGION, 2018-2023 (USD MILLION)

- TABLE 22 OTHER TYPES: PAYMENT GATEWAY MARKET, BY REGION, 2024-2029 (USD MILLION)

7 PAYMENT GATEWAY MARKET, BY VERTICAL

- 7.1 INTRODUCTION

- 7.1.1 VERTICAL: PAYMENT GATEWAY MARKET DRIVERS

- FIGURE 27 MEDIA & ENTERTAINMENT SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 23 PAYMENT GATEWAY MARKET, BY VERTICAL, 2018-2023 (USD MILLION)

- TABLE 24 PAYMENT GATEWAY MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- 7.2 BFSI

- 7.2.1 SECURE AND FASTER BANKING TRANSACTIONS TO DRIVE GROWTH

- 7.2.2 USE CASE

- 7.2.2.1 Secure online banking transactions

- 7.2.2.2 Credit card payments

- TABLE 25 BFSI: PAYMENT GATEWAY MARKET, BY REGION, 2018-2023 (USD MILLION)

- TABLE 26 BFSI: PAYMENT GATEWAY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 7.3 TELECOM

- 7.3.1 DIVERSE PAYMENT OPTIONS TO DRIVE MARKET GROWTH

- 7.3.2 USE CASE

- 7.3.2.1 Mobile recharge and top-ups

- 7.3.2.2 Value-added service purchases

- TABLE 27 TELECOM: PAYMENT GATEWAY MARKET, BY REGION, 2018-2023 (USD MILLION)

- TABLE 28 TELECOM: PAYMENT GATEWAY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 7.4 HEALTHCARE

- 7.4.1 ONLINE MEDICAL BILLING AND FASTER INSURANCE PROCESSING TO DRIVE GROWTH

- 7.4.2 USE CASE

- 7.4.2.1 Patient payments and co-payments

- 7.4.2.2 Medical bill payments

- TABLE 29 HEALTHCARE: PAYMENT GATEWAY MARKET, BY REGION, 2018-2023 (USD MILLION)

- TABLE 30 HEALTHCARE: PAYMENT GATEWAY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 7.5 MEDIA & ENTERTAINMENT

- 7.5.1 RECURRING SUBSCRIPTIONS AND GROWTH OF ONLINE PLATFORMS TO DRIVE GROWTH

- 7.5.2 USE CASE

- 7.5.2.1 Pay-per-view events

- 7.5.2.2 Digital content purchases

- TABLE 31 MEDIA & ENTERTAINMENT: PAYMENT GATEWAY MARKET, BY REGION, 2018-2023 (USD MILLION)

- TABLE 32 MEDIA & ENTERTAINMENT: PAYMENT GATEWAY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 7.6 TRAVEL & HOSPITALITY

- 7.6.1 EASE OF MULTICURRENCY TRANSACTIONS TO DRIVE GROWTH

- 7.6.2 USE CASE

- 7.6.2.1 Hotel booking payments

- 7.6.2.2 Flight reservations

- TABLE 33 TRAVEL & HOSPITALITY: PAYMENT GATEWAY MARKET, BY REGION, 2018-2023 (USD MILLION)

- TABLE 34 TRAVEL & HOSPITALITY: PAYMENT GATEWAY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 7.7 IT & ITES

- 7.7.1 ENHANCED SECURITY AND ENCRYPTION TO DRIVE GROWTH

- 7.7.2 USE CASE

- 7.7.2.1 Licensing and royalties

- 7.7.2.2 Training and certification programs

- TABLE 35 IT & ITES: PAYMENT GATEWAY MARKET, BY REGION, 2018-2023 (USD MILLION)

- TABLE 36 IT & ITES: PAYMENT GATEWAY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 7.8 RETAIL & E-COMMERCE

- 7.8.1 INCREASE IN GLOBAL E-COMMERCE SALES TO DRIVE GROWTH

- 7.8.2 USE CASE

- 7.8.2.1 Inventory management

- 7.8.2.2 Customizable checkout experience

- TABLE 37 RETAIL & E-COMMERCE: PAYMENT GATEWAY MARKET, BY REGION, 2018-2023 (USD MILLION)

- TABLE 38 RETAIL & E-COMMERCE: PAYMENT GATEWAY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 7.9 OTHER VERTICALS

- 7.9.1 USE CASE

- 7.9.1.1 Event registrations

- 7.9.1.2 Property sales

- 7.9.1.3 Toll payments

- 7.9.1.4 Catering services

- TABLE 39 OTHER VERTICALS: PAYMENT GATEWAY MARKET, BY REGION, 2018-2023 (USD MILLION)

- TABLE 40 OTHER VERTICALS: PAYMENT GATEWAY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 7.9.1 USE CASE

8 PAYMENT GATEWAY MARKET, BY REGION

- 8.1 INTRODUCTION

- TABLE 41 PAYMENT GATEWAY MARKET, BY REGION, 2018-2023 (USD MILLION)

- TABLE 42 PAYMENT GATEWAY MARKET, BY REGION, 2024-2029 (USD MILLION)

- 8.2 NORTH AMERICA

- 8.2.1 NORTH AMERICA: PAYMENT GATEWAY MARKET DRIVERS

- 8.2.2 NORTH AMERICA: RECESSION IMPACT

- FIGURE 28 NORTH AMERICA: PAYMENT GATEWAY MARKET SNAPSHOT

- TABLE 43 NORTH AMERICA: PAYMENT GATEWAY MARKET, BY TYPE, 2018-2023 (USD MILLION)

- TABLE 44 NORTH AMERICA: PAYMENT GATEWAY MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 45 NORTH AMERICA: PAYMENT GATEWAY MARKET, BY VERTICAL, 2018-2023 (USD MILLION)

- TABLE 46 NORTH AMERICA: PAYMENT GATEWAY MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- TABLE 47 NORTH AMERICA: PAYMENT GATEWAY MARKET, BY COUNTRY, 2018-2023 (USD MILLION)

- TABLE 48 NORTH AMERICA: PAYMENT GATEWAY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- 8.2.3 US

- 8.2.3.1 Robust financial ecosystem and major players to drive market

- TABLE 49 US: PAYMENT GATEWAY MARKET, BY TYPE, 2018-2023 (USD MILLION)

- TABLE 50 US: PAYMENT GATEWAY MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 51 US: PAYMENT GATEWAY MARKET, BY VERTICAL, 2018-2023 (USD MILLION)

- TABLE 52 US: PAYMENT GATEWAY MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- 8.2.4 CANADA

- 8.2.4.1 Government initiatives and immense participation from private players to drive market growth

- TABLE 53 CANADA: PAYMENT GATEWAY MARKET, BY TYPE, 2018-2023 (USD MILLION)

- TABLE 54 CANADA: PAYMENT GATEWAY MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 55 CANADA: PAYMENT GATEWAY MARKET, BY VERTICAL, 2018-2023 (USD MILLION)

- TABLE 56 CANADA: PAYMENT GATEWAY MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- 8.3 EUROPE

- 8.3.1 EUROPE: PAYMENT GATEWAY MARKET DRIVERS

- 8.3.2 EUROPE: RECESSION IMPACT

- TABLE 57 EUROPE: PAYMENT GATEWAY MARKET, BY TYPE, 2018-2023 (USD MILLION)

- TABLE 58 EUROPE: PAYMENT GATEWAY MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 59 EUROPE: PAYMENT GATEWAY MARKET, BY VERTICAL, 2018-2023 (USD MILLION)

- TABLE 60 EUROPE: PAYMENT GATEWAY MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- TABLE 61 EUROPE: PAYMENT GATEWAY MARKET, BY COUNTRY, 2018-2023 (USD MILLION)

- TABLE 62 EUROPE: PAYMENT GATEWAY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- 8.3.3 GERMANY

- 8.3.3.1 Robust financial ecosystem to drive growth

- 8.3.4 UK

- 8.3.4.1 Government initiatives and availability of advanced connectivity to drive growth

- TABLE 63 UK: PAYMENT GATEWAY MARKET, BY TYPE, 2018-2023 (USD MILLION)

- TABLE 64 UK: PAYMENT GATEWAY MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 65 UK: PAYMENT GATEWAY MARKET, BY VERTICAL, 2018-2023 (USD MILLION)

- TABLE 66 UK: PAYMENT GATEWAY MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- 8.3.5 ITALY

- 8.3.5.1 Surge in digital payments and e-commerce sector to drive growth

- 8.3.6 FRANCE

- 8.3.6.1 Strategic investments and innovative solutions to fuel market growth

- 8.3.7 SPAIN

- 8.3.7.1 Government funding and major players to drive growth of market

- 8.3.8 REST OF EUROPE

- 8.4 ASIA PACIFIC

- 8.4.1 ASIA PACIFIC: PAYMENT GATEWAY MARKET DRIVERS

- 8.4.2 ASIA PACIFIC: RECESSION IMPACT

- FIGURE 29 ASIA PACIFIC: PAYMENT GATEWAY MARKET SNAPSHOT

- TABLE 67 ASIA PACIFIC: PAYMENT GATEWAY MARKET, BY TYPE, 2018-2023 (USD MILLION)

- TABLE 68 ASIA PACIFIC: PAYMENT GATEWAY MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 69 ASIA PACIFIC: PAYMENT GATEWAY MARKET, BY VERTICAL, 2018-2023 (USD MILLION)

- TABLE 70 ASIA PACIFIC: PAYMENT GATEWAY MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- TABLE 71 ASIA PACIFIC: PAYMENT GATEWAY MARKET, BY COUNTRY, 2018-2023 (USD MILLION)

- TABLE 72 ASIA PACIFIC: PAYMENT GATEWAY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- 8.4.3 CHINA

- 8.4.3.1 Substantial investments and robust e-commerce ecosystem to drive market

- TABLE 73 CHINA: PAYMENT GATEWAY MARKET, BY TYPE, 2018-2023 (USD MILLION)

- TABLE 74 CHINA: PAYMENT GATEWAY MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 75 CHINA: PAYMENT GATEWAY MARKET, BY VERTICAL, 2018-2023 (USD MILLION)

- TABLE 76 CHINA: PAYMENT GATEWAY MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- 8.4.4 INDIA

- 8.4.4.1 Innovative digital payment solutions to drive growth

- 8.4.5 JAPAN

- 8.4.5.1 Initiatives such as Society 5.0 and digital payment industry to drive growth

- 8.4.6 AUSTRALIA & NEW ZEALAND

- 8.4.6.1 Government regulations and open banking initiatives to drive growth

- 8.4.7 REST OF ASIA PACIFIC

- 8.5 MIDDLE EAST & AFRICA

- 8.5.1 MIDDLE EAST & AFRICA: PAYMENT GATEWAY MARKET DRIVERS

- 8.5.2 MIDDLE EAST & AFRICA: RECESSION IMPACT

- TABLE 77 MIDDLE EAST & AFRICA: PAYMENT GATEWAY MARKET, BY REGION/COUNTRY, 2018-2023 (USD MILLION)

- TABLE 78 MIDDLE EAST & AFRICA: PAYMENT GATEWAY MARKET, BY REGION/COUNTRY, 2024-2029 (USD MILLION)

- TABLE 79 MIDDLE EAST & AFRICA: PAYMENT GATEWAY MARKET, BY TYPE, 2018-2023 (USD MILLION)

- TABLE 80 MIDDLE EAST & AFRICA: PAYMENT GATEWAY MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 81 MIDDLE EAST & AFRICA: PAYMENT GATEWAY MARKET, BY VERTICAL, 2018-2023 (USD MILLION)

- TABLE 82 MIDDLE EAST & AFRICA: PAYMENT GATEWAY MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- 8.5.3 GCC COUNTRIES

- TABLE 83 GCC COUNTRIES: PAYMENT GATEWAY MARKET, BY COUNTRY, 2018-2023 (USD MILLION)

- TABLE 84 GCC COUNTRIES: PAYMENT GATEWAY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 85 GCC COUNTRIES: PAYMENT GATEWAY MARKET, BY TYPE, 2018-2023 (USD MILLION)

- TABLE 86 GCC COUNTRIES: PAYMENT GATEWAY MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 87 GCC COUNTRIES: PAYMENT GATEWAY MARKET, BY VERTICAL, 2018-2023 (USD MILLION)

- TABLE 88 GCC COUNTRIES: PAYMENT GATEWAY MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- 8.5.3.1 UAE

- 8.5.3.1.1 Increasing adoption of digital payments to drive growth

- 8.5.3.2 Kingdom of Saudi Arabia

- 8.5.3.2.1 Supportive regulatory frameworks for payment gateway market to drive growth

- 8.5.3.1 UAE

- 8.5.4 REST OF GCC COUNTRIES

- 8.5.5 SOUTH AFRICA

- 8.5.5.1 Innovations in digital payment solutions to drive growth

- 8.5.6 REST OF MIDDLE EAST & AFRICA

- 8.6 LATIN AMERICA

- 8.6.1 LATIN AMERICA: PAYMENT GATEWAY MARKET DRIVERS

- 8.6.2 LATIN AMERICA: RECESSION IMPACT

- TABLE 89 LATIN AMERICA: PAYMENT GATEWAY MARKET, BY COUNTRY, 2018-2023 (USD MILLION)

- TABLE 90 LATIN AMERICA: PAYMENT GATEWAY MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 91 LATIN AMERICA: PAYMENT GATEWAY MARKET, BY TYPE, 2018-2023 (USD MILLION)

- TABLE 92 LATIN AMERICA: PAYMENT GATEWAY MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 93 LATIN AMERICA: PAYMENT GATEWAY MARKET, BY VERTICAL, 2018-2023 (USD MILLION)

- TABLE 94 LATIN AMERICA: PAYMENT GATEWAY MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- 8.6.3 BRAZIL

- 8.6.3.1 Surging e-commerce sector in country to drive growth

- TABLE 95 BRAZIL: PAYMENT GATEWAY MARKET, BY TYPE, 2018-2023 (USD MILLION)

- TABLE 96 BRAZIL: PAYMENT GATEWAY MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 97 BRAZIL: PAYMENT GATEWAY MARKET, BY VERTICAL, 2018-2023 (USD MILLION)

- TABLE 98 BRAZIL: PAYMENT GATEWAY MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- 8.6.4 MEXICO

- 8.6.4.1 Diverse digital payment options to drive growth

- 8.6.5 REST OF LATIN AMERICA

9 COMPETITIVE LANDSCAPE

- 9.1 INTRODUCTION

- 9.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 9.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PAYMENT GATEWAY PROVIDERS

- 9.3 REVENUE ANALYSIS

- FIGURE 30 HISTORICAL REVENUE ANALYSIS OF KEY PLAYERS, 2018-2022 (USD MILLION)

- 9.4 MARKET SHARE ANALYSIS

- FIGURE 31 PAYMENT GATEWAY MARKET SHARE ANALYSIS, 2023

- TABLE 99 PAYMENT GATEWAY MARKET: DEGREE OF COMPETITION

- TABLE 100 TYPE FOOTPRINT FOR KEY PLAYERS

- TABLE 101 VERTICAL FOOTPRINT FOR KEY PLAYERS

- TABLE 102 REGION FOOTPRINT FOR KEY PLAYERS

- 9.4.1 COMPANY FOOTPRINT: KEY PLAYERS, 2023

- FIGURE 32 COMPANY FOOTPRINT

- 9.5 COMPANY EVALUATION MATRIX

- 9.5.1 STARS

- 9.5.2 EMERGING LEADERS

- 9.5.3 PERVASIVE PLAYERS

- 9.5.4 PARTICIPANTS

- FIGURE 33 PAYMENT GATEWAY MARKET: COMPANY EVALUATION MATRIX, 2023

- 9.6 STARTUP/SME EVALUATION MATRIX

- 9.6.1 PROGRESSIVE COMPANIES

- 9.6.2 RESPONSIVE COMPANIES

- 9.6.3 DYNAMIC COMPANIES

- 9.6.4 STARTING BLOCKS

- FIGURE 34 PAYMENT GATEWAY MARKET: STARTUP/SME EVALUATION MATRIX

- 9.6.5 COMPETITIVE BENCHMARKING

- TABLE 103 DETAILED LIST OF STARTUPS/SMES

- TABLE 104 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 9.7 COMPETITIVE SCENARIO AND TRENDS

- 9.7.1 PRODUCT LAUNCHES

- TABLE 105 PAYMENT GATEWAY MARKET: PRODUCT LAUNCHES, JANUARY 2021-DECEMBER 2023

- 9.7.2 DEALS

- TABLE 106 PAYMENT GATEWAY MARKET: DEALS, JANUARY 2021-SEPTEMBER 2023

- 9.8 PAYMENT GATEWAY PRODUCT BENCHMARKING

- 9.8.1 PROMINENT PAYMENT GATEWAY PLAYERS

- FIGURE 35 COMPARATIVE ANALYSIS OF PROMINENT PAYMENT GATEWAY VENDORS

- 9.9 VALUATION AND FINANCIAL METRICS OF KEY PAYMENT GATEWAY PROVIDERS

- FIGURE 36 VALUATION AND FINANCIAL METRICS OF KEY PAYMENT GATEWAY VENDORS

10 COMPANY PROFILES

- (Business overview, Products/Solutions/Services offered, Recent Developments, MNM view)**

- 10.1 MAJOR PLAYERS

- 10.1.1 PAYPAL

- TABLE 107 PAYPAL: BUSINESS OVERVIEW

- FIGURE 37 PAYPAL: COMPANY SNAPSHOT

- TABLE 108 PAYPAL: PRODUCTS OFFERED

- TABLE 109 PAYPAL: PRODUCT LAUNCHES

- TABLE 110 PAYPAL: DEALS

- TABLE 111 PAYPAL: EXPANSIONS

- 10.1.2 FISERV

- TABLE 112 FISERV: BUSINESS OVERVIEW

- FIGURE 38 FISERV: COMPANY SNAPSHOT

- TABLE 113 FISERV: PRODUCTS OFFERED

- TABLE 114 FISERV: PRODUCT LAUNCHES

- TABLE 115 FISERV: DEALS

- TABLE 116 FISERV: EXPANSIONS

- 10.1.3 STRIPE

- TABLE 117 STRIPE: BUSINESS OVERVIEW

- TABLE 118 STRIPE: PRODUCTS OFFERED

- TABLE 119 STRIPE: PRODUCT LAUNCHES

- TABLE 120 STRIPE: DEALS

- TABLE 121 STRIPE: EXPANSIONS

- 10.1.4 VISA

- TABLE 122 VISA: BUSINESS OVERVIEW

- FIGURE 39 VISA: COMPANY SNAPSHOT

- TABLE 123 VISA: PRODUCTS OFFERED

- TABLE 124 VISA: DEALS

- TABLE 125 VISA: EXPANSIONS

- 10.1.5 AMAZON

- TABLE 126 AMAZON: COMPANY OVERVIEW

- FIGURE 40 AMAZON: COMPANY SNAPSHOT

- TABLE 127 AMAZON: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 128 AMAZON: DEALS

- 10.1.6 MASTERCARD

- TABLE 129 MASTERCARD: BUSINESS OVERVIEW

- FIGURE 41 MASTERCARD: COMPANY SNAPSHOT

- TABLE 130 MASTERCARD: PRODUCTS OFFERED

- TABLE 131 MASTERCARD: PRODUCT LAUNCHES

- TABLE 132 MASTERCARD: DEALS

- 10.1.7 FIS

- TABLE 133 FIS: BUSINESS OVERVIEW

- FIGURE 42 FIS: COMPANY SNAPSHOT

- TABLE 134 FIS: PRODUCTS OFFERED

- TABLE 135 FIS: PRODUCT LAUNCHES

- TABLE 136 FIS: DEALS

- TABLE 137 FIS: EXPANSIONS

- 10.1.8 BLOCK

- TABLE 138 BLOCK: BUSINESS OVERVIEW

- FIGURE 43 BLOCK: COMPANY SNAPSHOT

- TABLE 139 BLOCK: PRODUCTS OFFERED

- TABLE 140 BLOCK: PRODUCT LAUNCHES

- TABLE 141 BLOCK: DEALS

- TABLE 142 BLOCK: EXPANSIONS

- 10.1.9 GLOBAL PAYMENTS

- TABLE 143 GLOBAL PAYMENTS: BUSINESS OVERVIEW

- FIGURE 44 GLOBAL PAYMENTS: COMPANY SNAPSHOT

- TABLE 144 GLOBAL PAYMENTS: PRODUCTS OFFERED

- TABLE 145 GLOBAL PAYMENTS: DEALS

- 10.1.10 ADYEN

- TABLE 146 ADYEN: BUSINESS OVERVIEW

- FIGURE 45 ADYEN: COMPANY SNAPSHOT

- TABLE 147 ADYEN: PRODUCTS OFFERED

- TABLE 148 ADYEN: PRODUCT LAUNCHES

- TABLE 149 ADYEN: DEALS

- TABLE 150 ADYEN: EXPANSIONS

- 10.1.11 APPLE

- TABLE 151 APPLE: BUSINESS OVERVIEW

- FIGURE 46 APPLE: COMPANY SNAPSHOT

- TABLE 152 APPLE: PRODUCTS OFFERED

- 10.1.12 J.P. MORGAN

- TABLE 153 J.P. MORGAN: COMPANY OVERVIEW

- FIGURE 47 J.P. MORGAN: COMPANY SNAPSHOT

- TABLE 154 J.P. MORGAN CHASE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 155 J.P. MORGAN CHASE: PRODUCT LAUNCHES

- TABLE 156 J.P. MORGAN CHASE: DEALS

- 10.1.13 ALIBABA GROUP

- TABLE 157 ALIBABA GROUP: COMPANY OVERVIEW

- FIGURE 48 ALIBABA GROUP: COMPANY SNAPSHOT

- TABLE 158 ALIBABA GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 159 ALIBABA GROUP: DEALS

- 10.1.14 RAZORPAY

- 10.1.15 PHONEPE

- 10.1.16 PAYSAFE

- 10.1.17 VERIFONE

11 COMPANY PROFILES

- 11.1 STARTUPS/SMES

- 11.1.1 FIDELITY PAYMENT SERVICES

- 11.1.2 EASEBUZZ

- 11.1.3 BLUESNAP

- 11.1.4 WINDCAVE

- 11.1.5 HELCIM

- 11.1.6 INFIBEAM AVENUES LIMITED (IAL)

- 11.1.7 NOWPAYMENTS

- 11.1.8 INSTAMOJO

- 11.1.9 COINGATE

- 11.1.10 IPPOPAY

- 11.1.11 PAYJUNCTION

- 11.1.12 LYRA NETWORK

12 ADJACENT/RELATED MARKETS

- 12.1 INTRODUCTION

- 12.2 DIGITAL PAYMENT MARKET

- 12.2.1 MARKET DEFINITION

- 12.2.2 MARKET OVERVIEW

- 12.3 SOLUTIONS

- TABLE 160 DIGITAL PAYMENT MARKET, BY SOLUTION, 2018-2022 (USD MILLION)

- TABLE 161 DIGITAL PAYMENT MARKET, BY SOLUTION, 2023-2028 (USD MILLION)

- 12.3.1 DIGITAL PAYMENT MARKET, BY TRANSACTION TYPE

- TABLE 162 DIGITAL PAYMENT MARKET, BY TRANSACTION TYPE, 2018-2022 (USD MILLION)

- TABLE 163 DIGITAL PAYMENT MARKET, BY TRANSACTION TYPE, 2023-2028 (USD MILLION)

- 12.3.2 DIGITAL PAYMENT MARKET, BY PAYMENT MODE

- TABLE 164 DIGITAL PAYMENT MARKET, BY PAYMENT MODE, 2018-2022 (USD MILLION)

- TABLE 165 DIGITAL PAYMENT MARKET, PAYMENT MODE, 2023-2028 (USD MILLION)

- 12.3.3 DIGITAL PAYMENT MARKET, BY VERTICAL

- TABLE 166 DIGITAL PAYMENT MARKET, BY VERTICAL, 2018-2022 (USD MILLION)

- TABLE 167 DIGITAL PAYMENT MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- 12.3.4 DIGITAL PAYMENT MARKET, BY REGION

- TABLE 168 DIGITAL PAYMENT MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 169 DIGITAL PAYMENT MARKET, BY REGION, 2023-2028 (USD MILLION)

- 12.4 PAYMENT PROCESSING SOLUTIONS MARKET

- 12.4.1 MARKET DEFINITION

- 12.4.2 MARKET OVERVIEW

- 12.4.3 PAYMENT PROCESSING SOLUTIONS, BY PAYMENT METHOD

- TABLE 170 PAYMENT PROCESSING SOLUTIONS MARKET, BY PAYMENT METHOD, 2018-2022 (USD MILLION)

- TABLE 171 PAYMENT PROCESSING SOLUTIONS MARKET, BY PAYMENT METHOD, 2023-2028 (USD MILLION)

- 12.4.4 PAYMENT PROCESSING SOLUTIONS MARKET, BY VERTICAL

- TABLE 172 PAYMENT PROCESSING SOLUTIONS MARKET, BY VERTICAL, 2018-2022 (USD MILLION)

- TABLE 173 PAYMENT PROCESSING SOLUTIONS MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- 12.4.5 PAYMENT PROCESSING SOLUTIONS MANAGEMENT MARKET, BY REGION

- TABLE 174 PAYMENT PROCESSING SOLUTIONS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 175 PAYMENT PROCESSING SOLUTIONS MARKET, BY REGION, 2023-2028 (USD MILLION)

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS