|

|

市場調査レポート

商品コード

1643204

インドの決済ゲートウェイ:市場シェア分析、産業動向、成長予測(2025年~2030年)India Payment Gateway - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの決済ゲートウェイ:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

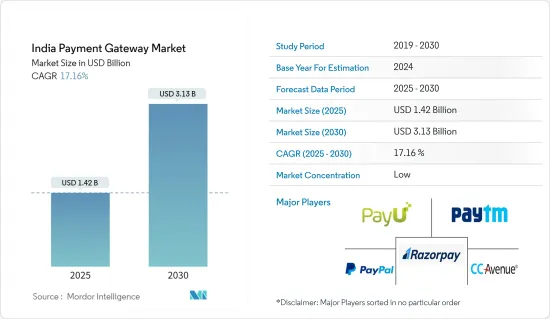

インドの決済ゲートウェイ市場規模は2025年に14億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは17.16%で、2030年には31億3,000万米ドルに達すると予測されています。

決済ゲートウェイの統合は、あらゆる産業のあらゆるビジネスにおいて最も重要な側面の1つとなっています。これにより、機密データを危険にさらすことなく、顧客の希望する銀行を通じてお金を集めることができます。

主要ハイライト

- インターネットの普及が進み、オンライン取引の手軽さが知られるようになったことで、消費者のオンライン決済に対する嗜好は変わりつつあります。ハードルのない取引は、オンライン取引への切り替えに対するユーザーの信頼を生み出しています。こうしたオンライン決済の急速な普及が、インドの決済ゲートウェイ市場の成長を後押ししています。

- デジタル決済は政府の「デジタルインディア」構想の目玉の1つであり、オンライン決済プラットフォームやサービスは国内に普及しています。悪魔解放後、デジタル決済は飛躍的に増加し、決済ゲートウェイベンダーの急浮上につながりました。

- インドの決済ゲートウェイ市場は、インドにおけるデジタル決済動向の増加によって後押しされています。政府のイニシアチブは、デジタル決済セグメントの強化に役立っており、キャッシュレス経済への移行を強調しています。例えば、デジタルインディア・プログラムは、インドをデジタルエンパワーメントされた社会に変革することをビジョンとするインド政府の旗艦プログラムです。

- Worldlineによると、近い将来、アセットライト技術が登場し、加盟店のアクワイアリングが確立されます。アセットライトとは、カードを含むあらゆる形態のデジタル決済を、従来のPOS機器ではなく、加盟店の携帯電話で受け付けることを指します。この技術プラットフォームでは、加盟店は携帯電話のアプリを使ってQRやカードによる決済を受け付けることができます。これにより、インド全土でデジタルコストの導入がさらに進むと考えられます。

- デジタル決済の認知度や普及率は高まっているが、ティア2、ティア3の都市や農村部に一貫したリーチと普及を確保するためには、デジタルインフラをさらに強化する必要があります。小規模加盟店は、費用対効果が高く、簡単に利用できるアクセプタンス・ツールを必要としています。多くの場合、零細加盟店にとって、ウォレット、UPI、銀行アプリなどさまざまな手段を把握することは難しいです。

- 小規模な都市や町は、パンデミックの中でデジタル決済や取引の回復の最前線にいます。National Payments Corporation of Indiaの統一決済インターフェース(UPI)によると、COVID-19の流行により取引が活発化するといいます。インドの小売決済システムを運営する統括組織によると、UPIの関連性は、COVID後の世界では、物理的空間とデジタル空間を組み合わせた「物理的」世界で高まるだろうとしています。

インドの決済ゲートウェイ市場動向

eコマース取引の増加が市場成長を牽引

- eコマース取引の増加により、インドでは様々な決済ゲートウェイの導入が進んでいます。Indian Brand Equity Foundationによると、インドのeコマース産業は上昇基調にあり、2034年には米国を抜いて世界第2位のeコマース市場になると予想されています。eコマース市場は2020年までに640億米ドル、2026年までに2,000億米ドルに達すると予想されています。

- 様々な政府規制がインドのeコマース産業を後押ししています。インドでは、B2B eコマースにおいて100%のFDIが認められています。eコマースにおけるFDIに関する新ガイドラインによると、市場・モデルのeコマースでは自動ルートによる100%のFDIが認められています。

- コロナウィルスの大流行により、加盟店やユーザーが店舗や近隣の店舗に殺到することを避けるため、加盟店はオンライン決済を依頼しながら、デジタルで注文を受け、管理するようになります。Flipkart傘下のPhonePeとGoogle Payは、ユーザーがそれぞれのアプリを通じて決済を行いながら、営業している近隣の店舗をデジタルで特定し、配達することを可能にしました。RBIによると、2020年4月のUPI取引は小売決済で1兆5,110億インドルピーを超えました。

- 新たなベンダーがeコマースに参入し、国内の各種決済ゲートウェイの利用を後押ししています。2020年5月、Reliance IndustriesはJioMartブランドで食料品事業のオンライン拡大を200都市で開始しました。JioMartで提供される商品には、果物や野菜、乳製品や焼き菓子、主食、スナックやブランド食品、飲食品、パーソナルケアや在宅医療などがあります。

- カード取引やUPIのような他の商品の急増も心強いです。RBIによると、デビットカードの取引額は6兆8,000億インドルピー、クレジットカードの取引額は7兆1,000億インドルピーで、2019年と2020年にそれぞれ前年比21%と33%の成長を記録しました。

市場成長を後押しする有利な政府イニシアティブと規制基準

- 決済アグリゲーター(PA)と決済ゲートウェイ(PG)に関するRBIの2020年3月のガイドラインは、インドにおける決済ゲートウェイの成長を促進する上で極めて重要です。新ガイドラインは、顧客資金の保護(2009年のRBIの「仲介業者を含む電子決済取引に関する指示」による)に加え、PAを認可された事業体として認め、業務や資金管理について柔軟性と統制を与えることを表明しています。

- RBIの新基準では、エスクロー口座への融資や利息の付与は認められていないです。PAの業務は指定決済システムを構成します。1日の平均残高に基づいて計算される「コア部分」に利息を積み立て、別口座に移すことができるため、PAの新たな収入源となります。

- また、国産のリアルタイム決済システムによる決済を促進するため、政府はUPIとRuPayの決済モードによる取引に対する加盟店割引率(MDR)手数料の免除を発表しました。

- また、NPCIは、UPIを利用した納税を可能にするため、インドの所得税部門と協力する予定です。これらすべての取り組みにより、インドにおける決済ゲートウェイの普及が進むと期待されています。

- Worldlineによると、アセットライト技術が登場し、加盟店獲得がまもなく確立されます。アセットライトとは、従来のPOS機器ではなく、加盟店の携帯電話でカードを含むあらゆる形態のデジタル決済を受け付けることを指します。この技術プラットフォームでは、加盟店は携帯電話のアプリを使ってQRやカードによる決済を受け付けることができます。これにより、インド全土でデジタル決済の導入がさらに進むと考えられます。

インドの決済ゲートウェイ産業概要

インドの決済ゲートウェイ市場は競争が激しいです。大小さまざまな参入企業が存在するため、市場は非常に集中しています。主要参入企業は、PayU、Paytm、Razorpay Software Private Limited、PayPal India Private Limited、CCAvenue、BillDesk、Instamojo Technologies Private Limitedなどです。各社は複数のパートナーシップを結び、プロジェクトに投資し、市場に新製品を投入することで市場シェアを拡大しています。

- 2022年3月-Razorpayは、銀行向けの革新的な決済ソリューションを提供するIZealiant Technologiesを買収しました。この買収により、エンドユーザーの決済体験を向上させる優れた技術インフラで銀行をサポートできるようになりました。銀行は決済エコシステムにおける重要な利害関係者です。IZealiant Technologiesの買収により、両社は銀行向けに産業初のソリューションを構築し、企業や顧客に世界クラスの決済体験を提供することができます。

- 2021年9月-PayUは決済ゲートウェイ企業のBilldeskを買収しました。この買収により、20以上の市場で事業を展開する同社の決済とフィンテック事業であるPayUは、総決済件数(TPV)で世界有数のオンライン決済プロバイダーとして浮上しました。統合された企業は、年間40億件の取引を行うことになります。Prosusが支援するフィンテック企業PayUは、インドの決済セグメントが2021年に大きな牽引力を見せたときにBilldeskを買収しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19がインドの決済ゲートウェイ市場に与える影響

第5章 市場力学

- 市場促進要因

- 国内におけるeコマース取引量の増加

- 新規ベンダー参入への道を開く市場情勢の進化と、デジタル取引の普及をさらに後押しする(特にセキュリティに焦点を当てた)継続的な技術進歩

- 市場課題

- インドにおける決済ゲートウェイの進化

- 政府の主要取り組みと規制基準(MDRの撤廃と現金取引に対する課税強化)

第6章 市場セグメンテーション

- 組織規模別

- 中小規模

- 大規模

第7章 競合情勢

- 企業プロファイル

- PayU

- Paytm

- Razorpay Software Private Limited

- PayPal India Private Limited

- CCAvenue

- BillDesk

- Instamojo Technologies Private Limited

- One MobiKwik Systems Private Limited

- IMSL-Fiserv

- Ingenico

第8章 投資分析

第9章 市場の将来

The India Payment Gateway Market size is estimated at USD 1.42 billion in 2025, and is expected to reach USD 3.13 billion by 2030, at a CAGR of 17.16% during the forecast period (2025-2030).

Integrating a payment gateway has become one of the most critical aspects of any business in every industry. It allows collecting money through the customer's preferred bank without compromising sensitive data.

Key Highlights

- With the increasing internet penetration and awareness about the ease of online transactions, consumers are changing their preferences for making payments online. The hurdle-free transactions generate confidence among the users for switching to online transactions. This rapid adoption of the online payment method is fueling India's payment gateway market growth.

- Digital payment has been one of the highlights of the government's 'Digital India' initiative, and online payment platforms and services have spread themselves in the country. Post demonetization, digital transactions witnessed a tremendous increase, which led to the sudden emergence of payment gateway vendors.

- The payment gateway market in India is boosted by an increase in digital payment trends in India. Government initiatives are helping enhance the digital payment space and emphasize moving toward a cashless economy. For instance, the Digital India program is a flagship program of the Government of India with a vision to transform India into a digitally empowered society.

- As per Worldline, asset-lite technologies will emerge and establish merchant acquiring in the near future. Asset-lite refers to the acceptance of all forms of digital payments, including cards, not on traditional POS machines but merchants' mobile phones. On this technology platform, merchants using an app on their phones will be able to accept payments through QR and cards. This will further increase the adoption of digital costs all over India.

- Although the awareness and adoption of digital payments are increasing, the digital infrastructure needs to be strengthened further to ensure consistent reach and penetration across the Tier 2 and Tier 3 cities and rural areas. Small merchants need acceptance tools that are cost-effective and easy to enable. In many cases, it is difficult for a micro-merchant to keep tabs on different means such as wallets, UPI, and bank apps.

- Smaller cities and towns have been at the forefront of digital payments and transactions recovery amid the pandemic. According to the National Payments Corporation of India, Unified Payments Interface (UPI), transactions will see a boost due to the outbreak of Covid-19. The umbrella organization for operating retail payments and settlement systems in India said that the relevance of UPI would grow in the 'physical' world, combining the physical and digital space, in a post-COVID world.

India Payment Gateway Market Trends

Growing E-Commerce Transactions to Drive Market Growth

- The rise in e-commerce transactions is increasing the adoption of various payment gateways in India. According to the Indian Brand Equity Foundation, the Indian e-commerce industry has been on an upward growth trajectory and is expected to surpass the United States to become the second-largest e-commerce market in the world by 2034. The e-commerce market is expected to reach USD 64 billion by 2020 and USD 200 billion by 2026.

- Various government regulations are boosting the e-commerce industry in the country. In India, 100% FDI is permitted in B2B e-commerce. As per new guidelines on FDI in e-commerce, 100% FDI under automatic route is allowed in the marketplace model of e-commerce.

- As merchants and users avoid crowding in shops and neighborhood stores due to the coronavirus pandemic, merchants will start taking and managing orders digitally while requesting online payments. Flipkart-owned PhonePe and Google Pay allowed users to digitally identify neighborhood stores in a customer's locality, which were open and delivering while allowing users to pay them through their respective apps. According to the RBI, UPI transactions for April 2020 exceeded INR 1511 billion for retail payments.

- New vendors are entering the e-commerce space, which will boost the use of various payment gateways in the country. In May 2020, Reliance Industries launched an online extension of its grocery business under the JioMart brand across 200 cities. Products offered on JioMart include fruits and vegetables, dairy and baked goods, staples, snacks and branded foods, beverages, and personal and home care.

- The surge in card transactions and other products like UPI has also been encouraging. As per RBI, the transaction value of debit cards stood at INR 6.8 trillion while the transaction value of credit cards stood at INR 7.1 trillion, registering YoY growth of 21% and 33%, respectively, in 2019 & 2020.

Favourable Government Initiatives and Regulatory Standards to Boost the Market Growth

- The RBI's March 2020 guidelines on Payment Aggregators (PAs) and Payment Gateways (PGs) are crucial to driving the growth of payment gateways in India. Besides protecting customer funds (as per the RBI's 2009 Directions for Electronic Payment Transactions involving Intermediaries), the new guidelines also express recognition of PAs as authorized entities and grant flexibility and control with operations and funds management.

- Under the new norms of RBI, neither loans nor earning interest is permissible for the escrow account. The PA's operations will constitute designated payment systems. Interest can be accumulated over a 'core portion,' computed based on the average daily outstanding balance, and transferred to a separate account, thus creating a new avenue of income for the PA.

- Also, to boost payments through home-grown real-time payment systems, the government announced the exemption of Merchant Discount Rate (MDR) charges on transactions via UPI and RuPay payment modes.

- Besides, NPCI is planning to collaborate with the income tax department of India to enable tax payments using UPI. All these initiatives are expected to increase the adoption of payment gateways in India.

- As per Worldline, asset-lite technologies will emerge and establish merchant acquisition shortly. Asset-lite refers to the acceptance of all forms of digital payments, including cards, not on traditional POS machines but on merchants' mobile phones. On this technology platform, merchants using an app on their phones will be able to accept payments through QR and cards. This will further increase the adoption of digital payment all over India.

India Payment Gateway Industry Overview

The India Payment Gateway Market is very competitive. The market is highly concentrated due to various small and large players. The major players in the market are PayU, Paytm, Razorpay Software Private Limited, PayPal India Private Limited, CCAvenue, BillDesk, Instamojo Technologies Private Limited, and many more. The companies are increasing the market share by forming multiple partnerships, investing in projects, and launching new products in the market.

- March 2022 - Razorpay acquired IZealiant Technologies, a provider of innovative payment solutions for banks. The acquisition enables support banks with excellent tech infrastructure that enhances the payment experience for end-users. Banks are key stakeholders in the payments ecosystem. With the acquisition of IZealiant technologies, both companies can build industry-first solutions for banks to create a world-class payments experience for businesses and customers.

- September 2021 - PayU acquired Billdesk, a payment gateway company. This acquisition helped PayU, the payments and fintech business of the company, which operates in more than 20 markets, emerge as the leading online payment provider globally by total payment volume (TPV). The combined entity will have a total of 4 billion transactions annually. The Prosus-backed fintech firm PayU acquired Billdesk when the Indian payments segment saw huge traction in 2021.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the India Payment Gateway Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Volume of E-Commerce Transactions in the Country

- 5.1.2 Evolving Market Landscape To Pave Way For Entry of New Vendors and the Ongoing Technological Advancements (Specifically Focused on Security) to Further Aid Penetration of Digital Transactions

- 5.2 Market Challenges

- 5.2.1 Evolution of Payment Gateway Landscape in India

- 5.2.2 Key Government Initiatives and Regulatory Standards (Removal of MDR and Higher Tax on Cash Transactions)

6 MARKET SEGMENTATION

- 6.1 By Organization Size

- 6.1.1 Small and Medium

- 6.1.2 Large-Scale

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 PayU

- 7.1.2 Paytm

- 7.1.3 Razorpay Software Private Limited

- 7.1.4 PayPal India Private Limited

- 7.1.5 CCAvenue

- 7.1.6 BillDesk

- 7.1.7 Instamojo Technologies Private Limited

- 7.1.8 One MobiKwik Systems Private Limited

- 7.1.9 IMSL-Fiserv

- 7.1.10 Ingenico