|

|

市場調査レポート

商品コード

1459082

光トランシーバーの世界市場:フォームファクター別、データレート別、波長別、ファイバータイプ別、コネクタ別、プロトコル別、用途別、地域別 - 予測(~2029年)Optical Transceiver Market by Form Factor (SFF and SFP; SFP+ and SFP28; XFP; CXP), Data Rate, Wavelength, Fiber Type (Single-mode Fiber; Multimode Fiber), Connector (LC; SC; MPO; and RJ-45), Protocol, Application and Region - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 光トランシーバーの世界市場:フォームファクター別、データレート別、波長別、ファイバータイプ別、コネクタ別、プロトコル別、用途別、地域別 - 予測(~2029年) |

|

出版日: 2024年03月26日

発行: MarketsandMarkets

ページ情報: 英文 344 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

世界の光トランシーバーの市場規模は、2024年に136億米ドル、2029年までに250億米ドルに達し、2024年~2029年のCAGRで13.0%の成長が予測されています。

コンパクトでエネルギー効率に優れたトランシーバーに対する需要の高まり、メガデータセンターの重要性の高まりなどの要因が、予測期間の市場成長を促進する可能性が高いです。メガデータセンターの重要性の高まりにより、企業はより高速なデータ伝送速度を求めており、光トランシーバーの成長につながっています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2020年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 単位 | 10億米ドル |

| セグメント | フォームファクター別、データレート別、波長別、ファイバータイプ別、プロトコル別、用途別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

「FTTxプロトコルセグメントが予測期間にもっとも速いCAGRで成長します。」

FTTxプロトコルは、光ファイバーネットワークを介した高速インターネット、ビデオ、音声サービスの提供を容易にし、従来の銅線ベースのネットワークに比べて優れた性能と信頼性を提供します。世界中の政府やサービスプロバイダーが、より速いインターネット速度への需要の増加に対応するために光ファイバーインフラ拡大に投資していることから、FTTx光トランシーバー市場は安定して成長します。

「予測期間に850nm波長セグメントが市場を独占します。」

850nmトランシーバーは、1GbE~100GbEとそれを超えるデータレートをサポートし、短距離での高速データ伝送に不可欠な製品となっています。この波長は、サーバーとスイッチ間の距離が比較的短いデータセンターの相互接続に特に適しています。850nm帯は、マルチモードファイバーで動作する光トランシーバーに使用されます。この市場は、マルチモード光ファイバーの手頃な価格と汎用性の恩恵を受けています。マルチモードファイバーは、短距離用途に費用対効果の高いソリューションを提供し、多くのデータセンターや企業ネットワークで好まれています。850nmトランシーバーは、マルチモードファイバーの利点を生かし、信頼性の高い高速接続を提供します。

「北米が光トランシーバー市場を独占します。」

北米は光トランシーバーの最大の市場の1つであり、データセンター用途、通信、コンシューマーエレクトロニクス(ラップトップ、デスクトップ、スマートテレビ)、インターネット接続、企業用途などのさまざまなセグメントで需要が伸びています。高いデータ伝送速度に対する需要や、5Gネットワーク接続を備えたスマートフォン、タブレット、コンピューターなどの通信機器に対する需要の増加、スマートデバイス(ウェアラブルデバイス、ホームアシスタント、IoTベースのホームセキュリティシステム、ゲーム機など)市場の拡大、複数のOTTプラットフォーム(Netflix、Amazon Primeなど)の台頭、データセンターの応用範囲の拡大などが、北米の光トランシーバー市場の成長を促進しています。

当レポートでは、世界の光トランシーバー市場について調査分析し、主な促進要因と抑制要因、競合情勢、将来の動向などの情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

- 光トランシーバー市場における成長機会

- 光トランシーバー市場:フォームファクター別

- 光トランシーバー市場:用途別

- 北米の光トランシーバー市場:用途別・国別

- 光トランシーバー市場:国別

第5章 市場の概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- バリューチェーン分析

- 研究開発

- 製造

- 組み立て

- 流通

- アフターサービス

- エコシステム分析

- 顧客のビジネスに影響を与える動向

- ケーススタディ分析

- ポーターのファイブフォース分析

- 技術動向

- 主要技術

- 補完技術

- 隣接技術

- 貿易分析

- 輸入シナリオ

- 輸出シナリオ

- 特許分析

- 関税と規制情勢

- 光トランシーバーに関する関税

- 規制情勢

- 標準

- 規制

- 主な会議とイベント(2024年~2025年)

- 価格分析

- 主要企業の平均販売価格の動向:データレート別

- 平均販売価格の動向:地域別

- 主なステークホルダーと購入プロセス

- 購入プロセスにおける主なステークホルダー

- 購入基準

- 投資と資金調達のシナリオ

第6章 光トランシーバー市場:フォームファクター別

- イントロダクション

- SFF、SFP

- SFP+、SFP28

- QSFP、QSFP+、QSFP-DD、QSFP28、QSFP56

- CFP、CFP2、CFP4、CFP8

- XFP

- CXP

第7章 光トランシーバー市場:データレート別

- イントロダクション

- 10Gbps未満

- 10Gbps~40Gbps

- 41Gbps~100Gbps

- 100Gbps超

第8章 光トランシーバー市場:ファイバータイプ別

- イントロダクション

- シングルモードファイバー(SMF)

- マルチモードファイバー(MMF)

第9章 光トランシーバー市場:距離別

- イントロダクション

- 1km未満

- 1~10km

- 11~100km

- 100km超

第10章 光トランシーバー市場:波長別

- イントロダクション

- 850nmバンド

- 1310nmバンド

- 1550nmバンド

- その他の波長

第11章 光トランシーバー市場:コネクタ別

- イントロダクション

- LC

- SC

- MPO

- RJ-45

第12章 光トランシーバー市場:プロトコル別

- イントロダクション

- イーサネット

- ファイバーチャネル

- CWDM/DWDM

- FTTx

- その他のプロトコル

第13章 光トランシーバー市場:用途別

- イントロダクション

- 通信

- 超長距離ネットワーク

- 長距離ネットワーク

- メトロネットワーク

- データセンター

- データセンター間接続

- データセンター内接続

- 企業

第14章 光トランシーバー市場:地域別

- イントロダクション

- 北米

- 北米市場に対する不況の影響

- 米国

- カナダ

- メキシコ

- 欧州

- 欧州市場に対する不況の影響

- ドイツ

- 英国

- フランス

- その他の欧州

- アジア太平洋

- アジア太平洋の市場に対する不況の影響

- 中国

- 日本

- 韓国

- その他のアジア太平洋

- その他の地域

- その他の地域の市場に対する不況の影響

- 南米

- GCC

- その他の中東・アフリカ

第15章 競合情勢

- 概要

- 主要企業の戦略/有力企業

- 収益分析

- 市場シェア分析

- 企業評価と財務指標

- ブランド/製品の比較

- 企業の評価マトリクス:主要企業

- 企業の評価マトリクス:スタートアップ/中小企業

- 競合シナリオ

第16章 企業プロファイル

- 主要企業

- COHERENT CORP.

- INNOLIGHT

- ACCELINK TECHNOLOGY CO. LTD.

- HISENSE BROADBAND, INC.

- CISCO SYSTEMS, INC.

- BROADCOM INC.

- LUMENTUM OPERATIONS LLC

- SUMITOMO ELECTRIC INDUSTRIES, LTD.

- INTEL CORPORATION

- FUJITSU OPTICAL COMPONENTS LIMITED

- その他の主要企業

- CIENA CORPORATION

- NVIDIA CORPORATION

- APPLIED OPTOELECTRONICS, INC.

- HUAGONG ZHENGYUAN

- NEC CORPORATION

- PERLE SYSTEMS

- SMITHS INTERCONNECT

- SMARTOPTICS

- SOLID OPTICS

- SOURCE PHOTONICS

- HUAWEI TECHNOLOGIES CO., LTD.

- EOPTOLINK TECHNOLOGY INC.

- INFINERA

- FOCI

- AMPHENOL COMMUNICATIONS SOLUTIONS

第17章 付録

The optical transceiver market is valued at USD 13.6 billion in 2024 and is expected to reach USD 25.0 billion by 2029, growing at a CAGR of 13.0% from 2024 to 2029. Factors such as rising demand for compact and energy-efficient transceivers, and growing importance of mega data centers are likely to drive market growth during the forecast period. Organizations are demanding faster data transmission speeds due to the growing importance of mega data centers, resulting in the growth of optical transceivers.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Billion) |

| Segments | By Form Factor, Data Rate, Wavelength, Fiber Type, Protocol, Application and Region |

| Regions covered | North America, Europe, APAC, RoW |

"FTTx protocol segment to grow at the fastest CAGR during the forecast period."

The FTTx protocol facilitates the delivery of high-speed internet, video, and voice services over fiber optic networks, offering superior performance and reliability compared to traditional copper-based networks. As governments and service providers worldwide invest in expanding fiber optic infrastructures to meet the growing demand for faster internet speeds, the FTTx optical transceiver market will experience steady growth.

"850 nm wavelength segment to dominates the market during the forecast period."

850 nm transceivers support data rates ranging from 1 GbE to 100 GbE and beyond, making them essential for high-speed data transmission over short distances. This wavelength is particularly suited for data center interconnects, with relatively short distances between servers and switches. The 850 nm band is used for optical transceivers operating on multimode fibers. This market benefits from the affordability and versatility of multimode fiber optics. Multimode fibers offer cost-effective solutions for short-range applications, making them the preferred choice for many data centers and enterprise networks. 850 nm transceivers leverage the advantages of multimode fibers. providing reliable and high-speed connectivity.

"North America to dominate the optical transceiver market."

North America is one of the largest markets for optical transceivers, with a growing demand in various sectors, such as data center applications, telecommunications, consumer electronics (laptops, desktops, and smart televisions), internet connectivity, and enterprise applications. The demand for high data transfer rates; the increasing demand for communication devices like smartphones, tablets, and computers with 5G network connectivity; the growing market for smart devices (such as wearable devices, home assistants, IoT-based home security systems, and gaming consoles); the rise of several OTT platforms (such as Netflix and Amazon Prime); and the growing applicability of data centers are driving the growth of the optical transceiver market in North America.

The breakup of primaries conducted during the study is depicted below:

- By Company Type: Tier 1 - 55 %, Tier 2 - 25%, and Tier 3 -20%

- By Designation Directors - 50%, Managers - 30%, and Others - 20%

- By Region: North America- 40%, Europe - 35%, Asia Pacific - 20%, RoW - 5%

Research Coverage

The report segments the optical transceiver market and forecasts its size, by value and volume, based on Form Factor (SFF and SFP; SFP+, and SFP28; QSFP, QSFP+, QSFP-DD, QSFP28, and QSFP56; CFP, CFP2, CFP4, and CFP8; XFP; and CXP); Data Rate (Less Than 10 Gbps; 10 Gbps to 40 Gbps; 41 Gbps to 100 Gbps; and More Than 100 Gbps); Wavelength (850 nm Band; 1310 nm Band; 1550 nm Band; and Other Wavelengths (C-Band DWDM Fixed and C-Band DWDM Tunable)); Fiber Type( Single-mode fiber; and Multimode fiber); Connector (LC; SC; MPO; and RJ-45); Distance (Less than 1 Km; 1 Km to 10 Km; 11 Km to 100 Km; and More Than 100 Km); Protocol (Ethernet; Fiber Channels; CWDM/DWDM; FTTx; Other Protocols); Application (Telecommunication; Data Center; and Enterprise); and Region (North America; Europe; Asia Pacific; and RoW). The report also provides a comprehensive review of market drivers, restraints, opportunities, and challenges in the optical transceiver market. The report also covers qualitative aspects in addition to the quantitative aspects of these markets.

Reason to Buy Report

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall optical transceiver market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (increasing adoption of smart devices and rise in data traffic, growing demand for cloud-based services, rising demand for compact and energy-efficient transceivers, growing importance of mega data centers, and emerging focus on 5G networks), restraints (Increasing network complexity, and high cost of optical transceivers), opportunities (Advancements in optical technology, and expansion of telecom infrastructure in developing economies), and challenges (Changing customer demands for portable devices and better speeds, and minimizing power consumption)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the optical transceiver market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the optical transceiver market across varied regions.

- Market Diversification: Exhaustive information about new services, untapped geographies, recent developments, and investments in the optical transceiver market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players Coherent Corp. (US), INNOLIGHT (China), Accelink Technology Co. Ltd. (China), Cisco Systems, Inc. (US), and Hisense Broadband, Inc. (China) among others in the optical transceiver market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS & EXCLUSIONS

- 1.3 STUDY SCOPE

- FIGURE 1 OPTICAL TRANSCEIVER MARKET SEGMENTATION

- 1.3.1 REGIONAL SCOPE

- FIGURE 2 OPTICAL TRANSCEIVER MARKET: REGIONAL SEGMENTATION

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY, PRICING, AND VOLUME

- TABLE 1 CURRENCY CONVERSION RATES

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

- 1.7.1 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 3 OPTICAL TRANSCEIVER MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY AND PRIMARY RESEARCH

- 2.1.2 SECONDARY DATA

- 2.1.2.1 Major secondary sources

- 2.1.2.2 Key data from secondary sources

- 2.1.3 PRIMARY DATA

- 2.1.3.1 Primary Interviews with experts

- 2.1.3.2 Key data from primary sources

- 2.1.3.3 Key industry insights

- 2.1.3.4 Breakdown of primaries

- 2.2 MARKET SIZE ESTIMATION

- FIGURE 4 RESEARCH FLOW: OPTICAL TRANSCEIVER MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach to estimate market size using bottom-up analysis (demand side)

- FIGURE 5 OPTICAL TRANSCEIVER MARKET: BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach to estimate market size using top-down analysis (supply side)

- FIGURE 6 OPTICAL TRANSCEIVER MARKET: TOP-DOWN APPROACH

- FIGURE 7 MARKET SIZE ESTIMATION METHODOLOGY: SUPPLY-SIDE ANALYSIS

- 2.3 MARKET BREAKDOWN & DATA TRIANGULATION

- FIGURE 8 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 RECESSION ASSUMPTION

- 2.6 RISK ASSESSMENT

- 2.7 LIMITATIONS

3 EXECUTIVE SUMMARY

- FIGURE 9 OPTICAL TRANSCEIVERS WITH FORM FACTORS OF QSFP, QSFP+, QSFP-DD, QSFP28, AND QSFP56 TO HOLD LARGEST SHARE DURING FORECAST PERIOD

- FIGURE 10 MULTIMODE OPTICAL TRANSCEIVERS TO EXHIBIT HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 11 OPTICAL TRANSCEIVERS WITH LC CONNECTORS TO HOLD LARGER SHARE DURING FORECAST PERIOD

- FIGURE 12 OPTICAL TRANSCEIVER MARKET FOR DATA CENTER APPLICATIONS TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 13 NORTH AMERICA HELD LARGEST SHARE OF OPTICAL TRANSCEIVER MARKET IN 2023

4 PREMIUM INSIGHTS

- 4.1 GROWTH OPPORTUNITIES IN OPTICAL TRANSCEIVER MARKET

- FIGURE 14 INCREASING ADOPTION OF SMART DEVICES AND RISING DATA TRAFFIC TO FUEL MARKET GROWTH

- 4.2 OPTICAL TRANSCEIVER MARKET, BY FORM FACTOR

- FIGURE 15 QSFP FORM FACTOR TO HOLD LARGEST SHARE IN 2024

- 4.3 OPTICAL TRANSCEIVER MARKET, BY APPLICATION

- FIGURE 16 DATA CENTER PROJECTED TO ACCOUNT FOR LARGEST SHARE OF OPTICAL TRANSCEIVER MARKET IN 2024

- 4.4 NORTH AMERICAN OPTICAL TRANSCEIVER MARKET, BY APPLICATION AND COUNTRY

- FIGURE 17 DATA CENTER TO ACCOUNT FOR LARGEST SHARE OF NORTH AMERICAN OPTICAL TRANSCEIVER MARKET IN 2023

- 4.5 OPTICAL TRANSCEIVER MARKET, BY COUNTRY

- FIGURE 18 CHINA TO GROW AT HIGHEST RATE DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 19 INCREASING ADOPTION OF SMART DEVICES AND RISING DATA TRAFFIC TO DRIVE GROWTH IN OPTICAL TRANSCEIVER MARKET

- 5.2.1 DRIVERS

- FIGURE 20 IMPACT OF DRIVERS ON OPTICAL TRANSCEIVER MARKET

- 5.2.1.1 Increasing adoption of smart devices and rise in data traffic

- TABLE 2 DATA TRAFFIC FROM SMART DEVICES (%), 2024

- FIGURE 21 GLOBAL INTERNET USERS DURING 2013-2023

- 5.2.1.2 Growing demand for cloud-based services

- 5.2.1.3 Rising demand for compact and energy-efficient transceivers

- 5.2.1.4 Growing importance of mega data centers

- 5.2.1.5 Emerging focus on 5G networks

- 5.2.1.6 Increasing popularity of bandwidth-intensive applications like virtual reality (VR) and augmented reality (AR)

- 5.2.2 RESTRAINTS

- FIGURE 22 IMPACT OF RESTRAINTS ON OPTICAL TRANSCEIVER MARKET

- 5.2.2.1 Increasing network complexity

- 5.2.2.2 High cost of optical transceivers

- 5.2.3 OPPORTUNITIES

- FIGURE 23 IMPACT OF OPPORTUNITIES ON OPTICAL TRANSCEIVER MARKET

- 5.2.3.1 Advancements in optical technology

- 5.2.3.2 Introduction of 800G optical transceivers for extended wavelengths over longer distances without regeneration

- 5.2.3.3 Expansion of telecom infrastructure in developing economies

- 5.2.4 CHALLENGES

- FIGURE 24 IMPACT OF CHALLENGES ON OPTICAL TRANSCEIVER MARKET

- 5.2.4.1 Changing customer demands for portable devices and better speeds

- 5.2.4.2 Minimizing power consumption

- 5.2.4.3 Device compatibility and sustainability issues

- 5.3 VALUE CHAIN ANALYSIS

- FIGURE 25 VALUE CHAIN ANALYSIS OF OPTICAL TRANSCEIVER ECOSYSTEM: R&D AND MANUFACTURING PHASE CONTRIBUTE MOST VALUE

- 5.3.1 RESEARCH & DEVELOPMENT

- 5.3.2 MANUFACTURING

- 5.3.3 ASSEMBLY

- 5.3.4 DISTRIBUTION

- 5.3.5 AFTER-SALES SERVICE

- 5.4 ECOSYSTEM ANALYSIS

- FIGURE 26 OPTICAL TRANSCEIVER ECOSYSTEM

- TABLE 3 LIST OF COMPANIES AND THEIR ROLE IN OPTICAL TRANSCEIVER ECOSYSTEM

- 5.5 TRENDS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 27 REVENUE SHIFT IN OPTICAL TRANSCEIVER MARKET

- 5.6 CASE STUDY ANALYSIS

- 5.6.1 CASE STUDY 1: EMPOWERING CRITICAL BUSINESS WITH QSFPTEK'S 100G QSFP28 TRANSCEIVERS

- 5.6.2 CASE STUDY 2: TELIA CARRIER'S STRATEGIC APPROACH TO CONVERGED NETWORKING

- 5.6.3 CASE STUDY 3: CHAMPION ONE RESOLVES CONNECTIVITY CHALLENGES FOR US UNIVERSITY

- 5.6.4 CASE STUDY 4: LONG LEAD TIMES AND HIGH COSTS THREATEN NETWORK EXPANSION

- 5.6.5 CASE STUDY 5: FS (US) PROVIDED LONG-DISTANCE 10G DWDM SOLUTION WITH LINK PROTECTION FOR BUSINESS EXPANSION

- 5.7 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 28 PORTER'S FIVE FORCES ANALYSIS

- TABLE 4 OPTICAL TRANSCEIVER MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.7.1 THREAT OF NEW ENTRANTS

- 5.7.2 THREAT OF SUBSTITUTES

- 5.7.3 BARGAINING POWER OF BUYERS

- 5.7.4 BARGAINING POWER OF SUPPLIERS

- 5.7.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.8 TECHNOLOGY TRENDS

- 5.8.1 KEY TECHNOLOGIES

- 5.8.1.1 Silicon photonics (SiPh) technology

- 5.8.1.2 XR optics-based networking solutions

- 5.8.1.3 PAM4 for 100G and 400G applications

- 5.8.1.4 Ultra-high-speed 800G optical transceivers

- 5.8.1.5 High-performance coherent pluggable modules with greater reach

- 5.8.2 COMPLEMENTARY TECHNOLOGIES

- 5.8.2.1 5G networks and integration with AI and IoT

- 5.8.3 ADJACENT TECHNOLOGIES

- 5.8.3.1 Laser technology for modulation of high data rate

- 5.8.1 KEY TECHNOLOGIES

- 5.9 TRADE ANALYSIS

- 5.9.1 IMPORT SCENARIO

- 5.9.1.1 Import scenario of optical transceiver market

- TABLE 5 IMPORT OF TRANSMISSION OR RECEPTION APPARATUS (INCLUDING OPTICAL TRANSCEIVERS), BY KEY COUNTRY, 2018-2022 (USD MILLION)

- 5.9.2 EXPORT SCENARIO

- 5.9.2.1 Export scenario of optical transceiver market

- TABLE 6 EXPORT OF TRANSMISSION OR RECEPTION APPARATUS (INCLUDING OPTICAL TRANSCEIVERS), BY KEY COUNTRY, 2018-2022 (USD MILLION)

- 5.9.1 IMPORT SCENARIO

- 5.10 PATENT ANALYSIS

- TABLE 7 PATENTS FILED FOR VARIOUS TYPES OF OPTICAL TRANSCEIVERS, 2020-2023

- FIGURE 29 PATENTS GRANTED FOR OPTICAL TRANSCEIVERS (2013-2023)

- FIGURE 30 TOP 10 COMPANIES WITH LARGEST NO. OF PATENT APPLICATIONS, 2013-2023

- 5.11 TARIFF & REGULATORY LANDSCAPE

- 5.11.1 TARIFFS RELATED TO OPTICAL TRANSCEIVERS

- TABLE 8 US: MFN TARIFFS FOR TRANSMISSION OR RECEPTION APPARATUS (INCLUDING OPTICAL TRANSCEIVERS) EXPORTED, BY KEY COUNTRY, 2023

- TABLE 9 CHINA: MFN TARIFFS FOR TRANSMISSION OR RECEPTION APPARATUS (INCLUDING OPTICAL TRANSCEIVERS) EXPORTED, BY KEY COUNTRY, 2023

- 5.11.2 REGULATORY LANDSCAPE

- 5.11.2.1 Regulatory bodies, government agencies, and other organizations

- TABLE 10 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.11.3 STANDARDS

- FIGURE 31 VARIOUS STANDARDS FOR OPTICAL TRANSCEIVERS

- 5.11.3.1 ISO 9001:2015

- 5.11.3.2 IEEE

- 5.11.3.3 IEC laser safety regulation

- 5.11.3.4 RoHS

- 5.11.3.5 REACH

- 5.11.3.6 CB

- 5.11.3.7 CE

- 5.11.3.8 FCC

- 5.11.3.9 FDA

- TABLE 14 FDA AND IEC LASER CLASS AND LASER PRODUCT HAZARD

- 5.11.3.10 RCM

- 5.11.4 REGULATIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 China

- 5.11.4.4 India

- 5.12 KEY CONFERENCES & EVENTS, 2024-2025

- TABLE 15 OPTICAL TRANSCEIVER MARKET: KEY CONFERENCES & EVENTS, 2024-2025

- 5.13 PRICING ANALYSIS

- 5.13.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY DATA RATE

- TABLE 16 AVERAGE SELLING PRICE OF OPTICAL TRANSCEIVERS BASED ON DATA RATES SUPPORTED

- FIGURE 32 AVERAGE SELLING PRICE TREND FOR OPTICAL TRANSCEIVERS, BY KEY PLAYER (USD)

- 5.13.2 AVERAGE SELLING PRICE TREND, BY REGION

- FIGURE 33 AVERAGE SELLING PRICE TREND FOR OPTICAL TRANSCEIVERS, BY REGION, 2020-2029 (USD)

- 5.14 KEY STAKEHOLDERS & BUYING PROCESS

- 5.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 34 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 APPLICATIONS

- TABLE 17 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 APPLICATIONS (%)

- 5.14.2 BUYING CRITERIA

- FIGURE 35 KEY BUYING CRITERIA FOR TOP 3 APPLICATIONS

- TABLE 18 KEY BUYING CRITERIA FOR TOP 3 APPLICATIONS

- 5.15 INVESTMENT & FUNDING SCENARIO

- FIGURE 36 FUNDS FOR OPTICAL TRANSCEIVERS, 2019-2023

- TABLE 19 FUNDING FOR OPTICAL TRANSCEIVERS, BY COMPANY, 2019-2023

6 OPTICAL TRANSCEIVER MARKET, BY FORM FACTOR

- 6.1 INTRODUCTION

- TABLE 20 OPTICAL TRANSCEIVER MARKET, BY FORM FACTOR, 2020-2023 (USD MILLION)

- FIGURE 37 OPTICAL TRANSCEIVERS WITH QSFP, QSFP+, QSFP-DD, QSFP28, AND QSFP56 TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 21 OPTICAL TRANSCEIVER MARKET, BY FORM FACTOR, 2024-2029 (USD MILLION)

- 6.2 SFF AND SFP

- 6.2.1 LOWER DATA RATE TRANSMISSION ASSOCIATED WITH SFF AND SFP TO BOOST MARKET

- TABLE 22 OPTICAL TRANSCEIVER MARKET FOR SFF AND SFP, BY WAVELENGTH, 2020-2023 (USD MILLION)

- FIGURE 38 1310 NM BAND WAVELENGTH FOR SFF AND SFP OPTICAL TRANSCEIVERS TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 23 OPTICAL TRANSCEIVER MARKET FOR SFF AND SFP, BY WAVELENGTH, 2024-2029 (USD MILLION)

- TABLE 24 OPTICAL TRANSCEIVER MARKET FOR SFF AND SFP, BY DATA RATE, 2020-2023 (USD MILLION)

- TABLE 25 OPTICAL TRANSCEIVER MARKET FOR SFF AND SFP, BY DATA RATE, 2024-2029 (USD MILLION)

- TABLE 26 OPTICAL TRANSCEIVER MARKET FOR SFF AND SFP, BY FIBER TYPE, 2020-2023 (USD MILLION)

- TABLE 27 OPTICAL TRANSCEIVER MARKET FOR SFF AND SFP, BY FIBER TYPE, 2024-2029 (USD MILLION)

- TABLE 28 OPTICAL TRANSCEIVER MARKET FOR SFF AND SFP, BY CONNECTOR, 2020-2023 (USD MILLION)

- TABLE 29 OPTICAL TRANSCEIVER MARKET FOR SFF AND SFP, BY CONNECTOR, 2024-2029 (USD MILLION)

- 6.3 SFP+ AND SFP28

- 6.3.1 AVAILABILITY OF BOTH SINGLE-MODE AND MULTIMODE FIBER OPTIC COMMUNICATION TO SUPPORT MARKET GROWTH

- TABLE 30 OPTICAL TRANSCEIVER MARKET FOR SFP+ AND SFP28, BY WAVELENGTH, 2020-2023 (USD MILLION)

- FIGURE 39 850 NM BAND WAVELENGTH FOR SFP+ AND SFP28 TO HOLD LARGEST SHARE DURING FORECAST PERIOD

- TABLE 31 OPTICAL TRANSCEIVER MARKET FOR SFP+ AND SFP28, BY WAVELENGTH, 2024-2029 (USD MILLION)

- TABLE 32 OPTICAL TRANSCEIVER MARKET FOR SFP+ AND SFP28, BY DATA RATE, 2020-2023 (USD MILLION)

- TABLE 33 OPTICAL TRANSCEIVER MARKET FOR SFP+ AND SFP28, BY DATA RATE, 2024-2029 (USD MILLION)

- TABLE 34 OPTICAL TRANSCEIVER MARKET FOR SFP+ AND SFP28, BY FIBER TYPE, 2020-2023 (USD MILLION)

- FIGURE 40 SINGLE-MODE FIBER FOR SFP+ AND SFP28 SEGMENT TO HOLD LARGER SHARE DURING FORECAST PERIOD

- TABLE 35 OPTICAL TRANSCEIVER MARKET FOR SFP+ AND SFP28, BY FIBER TYPE, 2024-2029 (USD MILLION)

- 6.4 QSFP, QSFP+, QSFP-DD, QSFP28, AND QSFP56

- 6.4.1 GROWING ADOPTION OF HIGH DATA RATE TRANSMISSION TO BOOST SEGMENTAL GROWTH

- TABLE 36 OPTICAL TRANSCEIVER MARKET FOR QSFP, QSFP+, QSFP-DD, QSFP28, AND QSFP56, BY WAVELENGTH, 2020-2023 (USD MILLION)

- FIGURE 41 850 NM BAND WAVELENGTH FOR QSFP, QSFP+, QSFP-DD, QSFP28, AND QSFP56 TO HOLD LARGER SHARE DURING FORECAST PERIOD

- TABLE 37 OPTICAL TRANSCEIVER MARKET FOR QSFP, QSFP+, QSFP-DD, QSFP28, AND QSFP56, BY WAVELENGTH, 2024-2029 (USD MILLION)

- TABLE 38 OPTICAL TRANSCEIVER MARKET FOR QSFP, QSFP+, QSFP-DD, QSFP28, AND QSFP56, BY DATA RATE, 2020-2023 (USD MILLION)

- TABLE 39 OPTICAL TRANSCEIVER MARKET FOR QSFP, QSFP+, QSFP-DD, QSFP28, AND QSFP56, BY DATA RATE, 2024-2029 (USD MILLION)

- TABLE 40 OPTICAL TRANSCEIVER MARKET FOR QSFP, QSFP+, QSFP-DD, QSFP28, AND QSFP56, BY FIBER TYPE, 2020-2023 (USD MILLION)

- FIGURE 42 MULTIMODE FIBER TYPE FOR QSFP, QSFP+, QSFP-DD, QSFP28, AND QSFP56 SEGMENT TO HOLD LARGER SHARE DURING FORECAST PERIOD

- TABLE 41 OPTICAL TRANSCEIVER MARKET FOR QSFP, QSFP+, QSFP-DD, QSFP28, AND QSFP56, BY FIBER TYPE, 2024-2029 (USD MILLION)

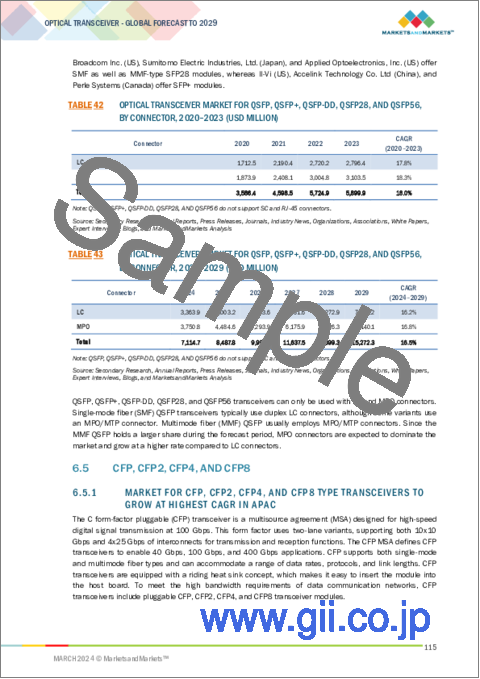

- TABLE 42 OPTICAL TRANSCEIVER MARKET FOR QSFP, QSFP+, QSFP-DD, QSFP28, AND QSFP56, BY CONNECTOR, 2020-2023 (USD MILLION)

- TABLE 43 OPTICAL TRANSCEIVER MARKET FOR QSFP, QSFP+, QSFP-DD, QSFP28, AND QSFP56, BY CONNECTOR, 2024-2029 (USD MILLION)

- 6.5 CFP, CFP2, CFP4, AND CFP8

- 6.5.1 MARKET FOR CFP, CFP2, CFP4, AND CFP8 TYPE TRANSCEIVERS TO GROW AT HIGHEST CAGR IN APAC

- TABLE 44 OPTICAL TRANSCEIVER MARKET FOR CFP, CFP2, CFP4, AND CFP8, BY WAVELENGTH, 2020-2023 (USD MILLION)

- FIGURE 43 1310 NM BAND WAVELENGTH FOR CFP, CFP2, CFP4, AND CFP8 OPTICAL TRANSCEIVERS TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 45 OPTICAL TRANSCEIVER MARKET FOR CFP, CFP2, CFP4, AND CFP8, BY WAVELENGTH, 2024-2029 (USD MILLION)

- TABLE 46 OPTICAL TRANSCEIVER MARKET FOR CFP, CFP2, CFP4, AND CFP8, BY FIBER TYPE, 2020-2023 (USD MILLION)

- FIGURE 44 SINGLE-MODE FIBER TYPE FOR CFP, CFP2, CFP4, AND CFP8 SEGMENT TO HOLD LARGER SHARE DURING FORECAST PERIOD

- TABLE 47 OPTICAL TRANSCEIVER MARKET FOR CFP, CFP2, CFP4, AND CFP8, BY FIBER TYPE, 2024-2029 (USD MILLION)

- TABLE 48 OPTICAL TRANSCEIVER MARKET FOR CFP, CFP2, CFP4, AND CFP8, BY CONNECTOR, 2020-2023 (USD MILLION)

- TABLE 49 OPTICAL TRANSCEIVER MARKET FOR CFP, CFP2, CFP4, AND CFP8, BY CONNECTOR, 2024-2029 (USD MILLION)

- 6.6 XFP

- 6.6.1 ABILITY TO SUPPORT ETHERNET, FIBER CHANNEL, AND SONET STANDARDS TO BOOST DEMAND

- TABLE 50 OPTICAL TRANSCEIVER MARKET FOR XFP, BY WAVELENGTH, 2020-2023 (USD MILLION)

- FIGURE 45 1550 NM BAND WAVELENGTH FOR XFP OPTICAL TRANSCEIVERS TO HOLD LARGEST SHARE DURING FORECAST PERIOD

- TABLE 51 OPTICAL TRANSCEIVER MARKET FOR XFP, BY WAVELENGTH, 2024-2029 (USD MILLION)

- 6.7 CXP

- 6.7.1 GROWING USE OF CXP TRANSCEIVERS FOR HIGH-DENSITY APPLICATIONS TO FAVOR MARKET GROWTH

- TABLE 52 OPTICAL TRANSCEIVER MARKET FOR CXP, BY WAVELENGTH, 2020-2023 (USD MILLION)

- TABLE 53 OPTICAL TRANSCEIVER MARKET FOR CXP, BY WAVELENGTH, 2024-2029 (USD MILLION)

- TABLE 54 OPTICAL TRANSCEIVER MARKET FOR CXP, BY FIBER TYPE, 2020-2023 (USD MILLION)

- TABLE 55 OPTICAL TRANSCEIVER MARKET FOR CXP, BY FIBER TYPE, 2024-2029 (USD MILLION)

7 OPTICAL TRANSCEIVER MARKET, BY DATA RATE

- 7.1 INTRODUCTION

- TABLE 56 OPTICAL TRANSCEIVER MARKET, BY DATA RATE, 2020-2023 (USD MILLION)

- FIGURE 46 OPTICAL TRANSCEIVERS SUPPORTING DATA RATES OF 41 GBPS TO 100 GBPS TO REGISTER HIGHEST GROWTH RATE FROM 2024 TO 2029

- TABLE 57 OPTICAL TRANSCEIVER MARKET, BY DATA RATE, 2024-2029 (USD MILLION)

- TABLE 58 OPTICAL TRANSCEIVER MARKET, BY DATA RATE, 2020-2023 (THOUSAND UNITS)

- TABLE 59 OPTICAL TRANSCEIVER MARKET, BY DATA RATE, 2024-2029 (THOUSAND UNITS)

- 7.2 LESS THAN 10 GBPS

- 7.2.1 ABILITY TO OPERATE THROUGH SINGLE-MODE AS WELL AS MULTIMODE FIBERS TO BOOST DEMAND

- TABLE 60 LIST OF OPTICAL TRANSCEIVERS WITH DATA RATES OF LESS THAN 10 GBPS

- TABLE 61 OPTICAL TRANSCEIVER MARKET FOR LESS THAN 10 GBPS DATA RATES, BY FORM FACTOR, 2020-2023 (USD MILLION)

- TABLE 62 OPTICAL TRANSCEIVER MARKET FOR LESS THAN 10 GBPS DATA RATES, BY FORM FACTOR, 2024-2029 (USD MILLION)

- TABLE 63 OPTICAL TRANSCEIVER MARKET FOR LESS THAN 10 GBPS DATA RATES, BY REGION, 2020-2023 (USD MILLION)

- TABLE 64 OPTICAL TRANSCEIVER MARKET FOR LESS THAN 10 GBPS DATA RATES, BY REGION, 2024-2029 (USD MILLION)

- 7.3 10 GBPS TO 40 GBPS

- 7.3.1 GROWING USE OF 10 GBPS TO 40 GBPS DATA RATE MODULES FOR SWITCHING AND ROUTING APPLICATIONS TO BOOST GROWTH

- TABLE 65 LIST OF OPTICAL TRANSCEIVERS WITH DATA RATES OF 10 GBPS TO 40 GBPS

- TABLE 66 OPTICAL TRANSCEIVER MARKET FOR 10 GBPS TO 40 GBPS DATA RATES, BY FORM FACTOR, 2020-2023 (USD MILLION)

- TABLE 67 OPTICAL TRANSCEIVER MARKET FOR 10 GBPS TO 40 GBPS DATA RATES, BY FORM FACTOR, 2024-2029 (USD MILLION)

- TABLE 68 OPTICAL TRANSCEIVER MARKET FOR 10 GBPS TO 40 GBPS DATA RATES, BY REGION, 2020-2023 (USD MILLION)

- TABLE 69 OPTICAL TRANSCEIVER MARKET FOR 10 GBPS TO 40 GBPS DATA RATES, BY REGION, 2024-2029 (USD MILLION)

- 7.4 41 GBPS TO 100 GBPS

- 7.4.1 MARKET TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 70 LIST OF OPTICAL TRANSCEIVERS WITH DATA RATES OF 41 GBPS TO 100 GBPS

- TABLE 71 OPTICAL TRANSCEIVER MARKET FOR 41 GBPS TO 100 GBPS DATA RATES, BY FORM FACTOR, 2020-2023 (USD MILLION)

- TABLE 72 OPTICAL TRANSCEIVER MARKET FOR 41 GBPS TO 100 GBPS DATA RATES, BY FORM FACTOR, 2024-2029 (USD MILLION)

- TABLE 73 OPTICAL TRANSCEIVER MARKET FOR 41 GBPS TO 100 GBPS DATA RATES, BY REGION, 2020-2023 (USD MILLION)

- TABLE 74 OPTICAL TRANSCEIVER MARKET FOR 41 GBPS TO 100 GBPS DATA RATES, BY REGION, 2024-2029 (USD MILLION)

- 7.5 MORE THAN 100 GBPS

- 7.5.1 WIDE USAGE OF MORE THAN 100 GBPS DATA RATE MODULES FOR SHORT-REACH COMMUNICATIONS TO FUEL GROWTH

- TABLE 75 LIST OF OPTICAL TRANSCEIVERS WITH DATA RATES OF MORE THAN 100 GBPS

- TABLE 76 OPTICAL TRANSCEIVER MARKET FOR MORE THAN 100 GBPS DATA RATES, BY FORM FACTOR, 2020-2023 (USD MILLION)

- TABLE 77 OPTICAL TRANSCEIVER MARKET FOR MORE THAN 100 GBPS DATA RATES, BY FORM FACTOR, 2024-2029 (USD MILLION)

- TABLE 78 OPTICAL TRANSCEIVER MARKET FOR MORE THAN 100 GBPS DATA RATES, BY REGION, 2020-2023 (USD MILLION)

- TABLE 79 OPTICAL TRANSCEIVER MARKET FOR MORE THAN 100 GBPS DATA RATES, BY REGION, 2024-2029 (USD MILLION)

8 OPTICAL TRANSCEIVER MARKET, BY FIBER TYPE

- 8.1 INTRODUCTION

- TABLE 80 OPTICAL TRANSCEIVER MARKET, BY FIBER TYPE, 2020-2023 (USD MILLION)

- FIGURE 47 MULTIMODE OPTICAL TRANSCEIVERS TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- TABLE 81 OPTICAL TRANSCEIVER MARKET, BY FIBER TYPE, 2024-2029 (USD MILLION)

- 8.2 SINGLE-MODE FIBER (SMF)

- 8.2.1 ADVANTAGES SUCH AS LONG-DISTANCE TRANSMISSION DUE TO LOWER ATTENUATION TO BOOST MARKET GROWTH

- TABLE 82 LIST OF PLAYERS OFFERING SINGLE-MODE TRANSCEIVERS

- TABLE 83 OPTICAL TRANSCEIVER MARKET FOR SINGLE-MODE FIBERS, BY FORM FACTOR, 2020-2023 (USD MILLION)

- TABLE 84 OPTICAL TRANSCEIVER MARKET FOR SINGLE-MODE FIBERS, BY FORM FACTOR, 2024-2029 (USD MILLION)

- TABLE 85 OPTICAL TRANSCEIVER MARKET FOR SINGLE-MODE FIBERS, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 86 OPTICAL TRANSCEIVER MARKET FOR SINGLE-MODE FIBERS, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 87 OPTICAL TRANSCEIVER MARKET FOR SINGLE-MODE FIBERS, BY REGION, 2020-2023 (USD MILLION)

- TABLE 88 OPTICAL TRANSCEIVER MARKET FOR SINGLE-MODE FIBERS, BY REGION, 2024-2029 (USD MILLION)

- 8.3 MULTIMODE FIBER (MMF)

- 8.3.1 ABILITY OF MULTIMODE FIBERS TO CONSUME LESS POWER TO DRIVE GROWTH

- TABLE 89 LIST OF PLAYERS OFFERING MULTIMODE TRANSCEIVERS

- TABLE 90 OPTICAL TRANSCEIVER MARKET FOR MULTIMODE FIBERS, BY FORM FACTOR, 2020-2023 (USD MILLION)

- TABLE 91 OPTICAL TRANSCEIVER MARKET FOR MULTIMODE FIBERS, BY FORM FACTOR, 2024-2029 (USD MILLION)

- TABLE 92 OPTICAL TRANSCEIVER MARKET FOR MULTIMODE FIBERS, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 93 OPTICAL TRANSCEIVER MARKET FOR MULTIMODE FIBERS, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 94 OPTICAL TRANSCEIVER MARKET FOR MULTIMODE FIBERS, BY REGION, 2020-2023 (USD MILLION)

- FIGURE 48 MULTIMODE OPTICAL TRANSCEIVER MARKET TO GROW AT HIGHEST CAGR IN ASIA PACIFIC DURING FORECAST PERIOD

- TABLE 95 OPTICAL TRANSCEIVER MARKET FOR MULTIMODE FIBERS, BY REGION, 2024-2029 (USD MILLION)

9 OPTICAL TRANSCEIVER MARKET, BY DISTANCE

- 9.1 INTRODUCTION

- TABLE 96 OPTICAL TRANSCEIVER MARKET, BY DISTANCE, 2020-2023 (USD MILLION)

- FIGURE 49 LESS THAN 1 KM MARKET SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- TABLE 97 OPTICAL TRANSCEIVER MARKET, BY DISTANCE, 2024-2029 (USD MILLION)

- 9.2 LESS THAN 1 KM

- 9.2.1 GROWING PREFERENCE FOR MULTIMODE FIBER TRANSCEIVERS FOR LESS THAN 1 KM DISTANCE CONNECTIVITY TO BOOST MARKET

- TABLE 98 LIST OF OPTICAL TRANSCEIVERS WITH LESS THAN 1 KM REACH

- TABLE 99 OPTICAL TRANSCEIVER MARKET FOR LESS THAN 1 KM RANGE MODULES, BY REGION, 2020-2023 (USD MILLION)

- FIGURE 50 NORTH AMERICA TO DOMINATE MARKET FOR LESS THAN 1 KM RANGE MODULES DURING FORECAST PERIOD

- TABLE 100 OPTICAL TRANSCEIVER MARKET FOR LESS THAN 1 KM RANGE MODULES, BY REGION, 2024-2029 (USD MILLION)

- 9.3 1 TO 10 KM

- 9.3.1 GROWING USE FOR INTRA-DATA CENTER CONNECTION APPLICATIONS TO SUPPORT MARKET GROWTH

- TABLE 101 LIST OF OPTICAL TRANSCEIVERS WITH 1 TO 10 KM REACH

- TABLE 102 OPTICAL TRANSCEIVER MARKET FOR 1 TO 10 KM RANGE MODULES, BY REGION, 2020-2023 (USD MILLION)

- FIGURE 51 ASIA PACIFIC MARKET FOR 1 TO 10 KM RANGE MODULES TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 103 OPTICAL TRANSCEIVER MARKET FOR 1 TO 10 KM RANGE MODULES, BY REGION, 2024-2029 (USD MILLION)

- 9.4 11 TO 100 KM

- 9.4.1 GROWING USE ON SINGLE-MODE FIBERS TO FAVOR MARKET GROWTH

- TABLE 104 LIST OF OPTICAL TRANSCEIVERS WITH 11 TO 100 KM REACH

- TABLE 105 OPTICAL TRANSCEIVER MARKET FOR 11 TO 100 KM RANGE MODULES, BY REGION, 2020-2023 (USD MILLION)

- FIGURE 52 MARKET FOR 11 TO 100 KM RANGE MODULES IN ASIA PACIFIC TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- TABLE 106 OPTICAL TRANSCEIVER MARKET FOR 11 TO 100 KM RANGE MODULES, BY REGION, 2024-2029 (USD MILLION)

- 9.5 MORE THAN 100 KM

- 9.5.1 GROWING USE FOR LONG-DISTANCE TELECOMMUNICATION NETWORKS TO PROPEL GROWTH

- TABLE 107 LIST OF OPTICAL TRANSCEIVERS WITH MORE THAN 100 KM REACH

- TABLE 108 OPTICAL TRANSCEIVER MARKET FOR MORE THAN 100 KM RANGE MODULES, BY REGION, 2020-2023 (USD MILLION)

- FIGURE 53 MARKET FOR MORE THAN 100 KM RANGE MODULES IN ASIA PACIFIC TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- TABLE 109 OPTICAL TRANSCEIVER MARKET FOR MORE THAN 100 KM RANGE MODULES, BY REGION, 2024-2029 (USD MILLION)

10 OPTICAL TRANSCEIVER MARKET, BY WAVELENGTH

- 10.1 INTRODUCTION

- TABLE 110 OPTICAL TRANSCEIVER MARKET, BY WAVELENGTH, 2020-2023 (USD MILLION)

- FIGURE 54 OPTICAL TRANSCEIVERS OPERATING IN 1310 NM BAND TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 111 OPTICAL TRANSCEIVER MARKET, BY WAVELENGTH, 2024-2029 (USD MILLION)

- 10.2 850 NM BAND

- 10.2.1 GROWING USE FOR SHORT-DISTANCE COMMUNICATION TO BOOST MARKET DEMAND

- TABLE 112 LIST OF OPTICAL TRANSCEIVERS OPERATING AT 850 NM BAND

- TABLE 113 OPTICAL TRANSCEIVER MARKET FOR 850 NM BAND, BY FORM FACTOR, 2020-2023 (USD MILLION)

- TABLE 114 OPTICAL TRANSCEIVER MARKET FOR 850 NM BAND, BY FORM FACTOR, 2024-2029 (USD MILLION)

- TABLE 115 OPTICAL TRANSCEIVER MARKET FOR 850 NM BAND, BY REGION, 2020-2023 (USD MILLION)

- TABLE 116 OPTICAL TRANSCEIVER MARKET FOR 850 NM BAND, BY REGION, 2024-2029 (USD MILLION)

- 10.3 1310 NM BAND

- 10.3.1 GROWING USE FOR DATA TRANSFER THROUGH SINGLE-MODE AND MULTIMODE FIBERS TO DRIVE MARKET GROWTH

- TABLE 117 LIST OF OPTICAL TRANSCEIVERS OPERATING AT 1310 NM BAND

- TABLE 118 OPTICAL TRANSCEIVER MARKET FOR 1310 NM BAND, BY FORM FACTOR, 2020-2023 (USD MILLION)

- TABLE 119 OPTICAL TRANSCEIVER MARKET FOR 1310 NM BAND, BY FORM FACTOR, 2024-2029 (USD MILLION)

- TABLE 120 OPTICAL TRANSCEIVER MARKET FOR 1310 NM BAND, BY REGION, 2020-2023 (USD MILLION)

- FIGURE 55 NORTH AMERICA TO LEAD OPTICAL TRANSCEIVER MARKET FOR 1310 NM BAND

- TABLE 121 OPTICAL TRANSCEIVER MARKET FOR 1310 NM BAND, BY REGION, 2024-2029 (USD MILLION)

- 10.4 1550 NM BAND

- 10.4.1 EXTENSIVE USE OF 1150 NM BAND TRANSCEIVERS FOR LONG-DISTANCE COMMUNICATION TO SUPPORT MARKET GROWTH

- TABLE 122 LIST OF OPTICAL TRANSCEIVERS OPERATING AT 1550 NM BAND

- TABLE 123 OPTICAL TRANSCEIVER MARKET FOR 1550 NM BAND, BY FORM FACTOR, 2020-2023 (USD MILLION)

- TABLE 124 OPTICAL TRANSCEIVER MARKET FOR 1550 NM BAND, BY FORM FACTOR, 2024-2029 (USD MILLION)

- TABLE 125 OPTICAL TRANSCEIVER MARKET FOR 1550 NM BAND, BY REGION, 2020-2023 (USD MILLION)

- TABLE 126 OPTICAL TRANSCEIVER MARKET FOR 1550 NM BAND, BY REGION, 2024-2029 (USD MILLION)

- 10.5 OTHER WAVELENGTHS

- TABLE 127 OPTICAL TRANSCEIVER MARKET FOR OTHER WAVELENGTHS, BY FORM FACTOR, 2020-2023 (USD MILLION)

- TABLE 128 OPTICAL TRANSCEIVER MARKET FOR OTHER WAVELENGTHS, BY FORM FACTOR, 2024-2029 (USD MILLION)

- TABLE 129 OPTICAL TRANSCEIVER MARKET FOR OTHER WAVELENGTHS, BY REGION, 2020-2023 (USD MILLION)

- TABLE 130 OPTICAL TRANSCEIVER MARKET FOR OTHER WAVELENGTHS, BY REGION, 2024-2029 (USD MILLION)

11 OPTICAL TRANSCEIVER MARKET, BY CONNECTOR

- 11.1 INTRODUCTION

- TABLE 131 OPTICAL TRANSCEIVER MARKET, BY CONNECTOR, 2020-2023 (USD MILLION)

- FIGURE 56 MPO CONNECTOR-BASED OPTICAL TRANSCEIVERS TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 132 OPTICAL TRANSCEIVER MARKET, BY CONNECTOR, 2024-2029 (USD MILLION)

- 11.2 LC

- 11.2.1 GROWING USE OF LC CONNECTORS FOR COHERENT POINT-TO-POINT AND METRO APPLICATIONS TO BOOST MARKET

- TABLE 133 LIST OF OPTICAL TRANSCEIVERS WITH LC CONNECTORS

- TABLE 134 OPTICAL TRANSCEIVER MARKET FOR LC CONNECTORS, BY FORM FACTOR, 2020-2023 (USD MILLION)

- TABLE 135 OPTICAL TRANSCEIVER MARKET FOR LC CONNECTORS, BY FORM FACTOR, 2024-2029 (USD MILLION)

- TABLE 136 OPTICAL TRANSCEIVER MARKET FOR LC CONNECTORS, BY REGION, 2020-2023 (USD MILLION)

- TABLE 137 OPTICAL TRANSCEIVER MARKET FOR LC CONNECTORS, BY REGION, 2024-2029 (USD MILLION)

- 11.3 SC

- 11.3.1 SC CONNECTOR-BASED OPTICAL TRANSCEIVERS SEGMENT TO GROW AT HIGHEST CAGR IN ASIA PACIFIC

- TABLE 138 LIST OF OPTICAL TRANSCEIVERS WITH SC CONNECTORS

- TABLE 139 OPTICAL TRANSCEIVER MARKET FOR SC CONNECTORS, BY FORM FACTOR, 2020-2023 (USD MILLION)

- TABLE 140 OPTICAL TRANSCEIVER MARKET FOR SC CONNECTORS, BY FORM FACTOR, 2024-2029 (USD MILLION)

- TABLE 141 OPTICAL TRANSCEIVER MARKET FOR SC CONNECTORS, BY REGION, 2020-2023 (USD MILLION)

- TABLE 142 OPTICAL TRANSCEIVER MARKET FOR SC CONNECTORS, BY REGION, 2024-2029 (USD MILLION)

- 11.4 MPO

- 11.4.1 GROWING USE OF MPO CONNECTORS FOR HIGH-SPEED OPTICAL TRANSCEIVERS TO DRIVE MARKET GROWTH

- TABLE 143 LIST OF OPTICAL TRANSCEIVERS WITH MPO CONNECTORS

- TABLE 144 OPTICAL TRANSCEIVER MARKET FOR MPO CONNECTORS, BY FORM FACTOR, 2020-2023 (USD MILLION)

- TABLE 145 OPTICAL TRANSCEIVER MARKET FOR MPO CONNECTORS, BY FORM FACTOR, 2024-2029 (USD MILLION)

- TABLE 146 OPTICAL TRANSCEIVER MARKET FOR MPO CONNECTORS, BY REGION, 2020-2023 (USD MILLION)

- FIGURE 57 MPO CONNECTORS MARKET TO GROW AT HIGHEST CAGR IN ASIA PACIFIC DURING FORECAST PERIOD

- TABLE 147 OPTICAL TRANSCEIVER MARKET FOR MPO CONNECTORS, BY REGION, 2024-2029 (USD MILLION)

- 11.5 RJ-45

- 11.5.1 LOWEST DATA RATE CAPABILITY ASSOCIATED WITH RJ-45 CONNECTORS TO BOOST DEMAND

- TABLE 148 LIST OF OPTICAL TRANSCEIVERS WITH RJ-45 CONNECTORS

- TABLE 149 OPTICAL TRANSCEIVER MARKET FOR RJ-45 CONNECTORS, BY FORM FACTOR, 2020-2023 (USD MILLION)

- TABLE 150 OPTICAL TRANSCEIVER MARKET FOR RJ-45 CONNECTORS, BY FORM FACTOR, 2024-2029 (USD MILLION)

- TABLE 151 OPTICAL TRANSCEIVER MARKET FOR RJ-45 CONNECTORS, BY REGION, 2020-2023 (USD MILLION)

- FIGURE 58 ASIA PACIFIC REGION FOR MODULES BASED ON RJ-45 CONNECTORS TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 152 OPTICAL TRANSCEIVER MARKET FOR RJ-45 CONNECTORS, BY REGION, 2024-2029 (USD MILLION)

12 OPTICAL TRANSCEIVER MARKET, BY PROTOCOL

- 12.1 INTRODUCTION

- TABLE 153 OPTICAL TRANSCEIVER MARKET, BY PROTOCOL, 2020-2023 (USD MILLION)

- FIGURE 59 MARKET FOR FTTX TO WITNESS HIGHEST GROWTH DURING FORECAST PERIOD

- TABLE 154 OPTICAL TRANSCEIVER MARKET, BY PROTOCOL, 2024-2029 (USD MILLION)

- 12.2 ETHERNET

- 12.2.1 ABILITY TO SUPPORT WIDE RANGE OF TRANSMISSION SPEEDS TO BOOST ADOPTION OF ETHERNET OPTICAL TRANSCEIVERS

- TABLE 155 LIST OF ETHERNET-BASED OPTICAL TRANSCEIVERS

- 12.3 FIBER CHANNELS

- 12.3.1 GROWING ADOPTION OF FIBER CHANNEL OPTICAL TRANSCEIVERS IN DATA CENTERS TO SUPPORT MARKET GROWTH

- TABLE 156 LIST OF FIBER CHANNEL OPTICAL TRANSCEIVERS

- 12.4 CWDM/DWDM

- 12.4.1 ABILITY OF WDM PROTOCOLS TO INCREASE DATA CARRYING CAPACITY WITHOUT INCREASING DATA RATES TO DRIVE MARKET GROWTH

- TABLE 157 LIST OF CWDM/DWDM OPTICAL TRANSCEIVERS

- 12.5 FTTX

- 12.5.1 GROWING ADOPTION OF FTTH TO FAVOR MARKET GROWTH

- TABLE 158 LIST OF FTTX OPTICAL TRANSCEIVERS

- 12.6 OTHER PROTOCOLS

- TABLE 159 LIST OF OPTICAL TRANSCEIVERS COMPATIBLE WITH OTHER PROTOCOLS

13 OPTICAL TRANSCEIVER MARKET, BY APPLICATION

- 13.1 INTRODUCTION

- TABLE 160 OPTICAL TRANSCEIVER MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- FIGURE 60 OPTICAL TRANSCEIVER MARKET FOR DATA CENTER APPLICATIONS TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 161 OPTICAL TRANSCEIVER MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- 13.2 TELECOMMUNICATION

- 13.2.1 ULTRA-LONG-HAUL NETWORKS

- 13.2.1.1 Growing use of DWDM technology for ultra-long-haul network communication to boost market

- 13.2.2 LONG-HAUL NETWORKS

- 13.2.2.1 Growing use of single-mode fibers for long distances to favor market growth

- 13.2.3 METRO NETWORKS

- 13.2.3.1 Expansion of 4G and rising adoption of 5G to present opportunities for market growth

- TABLE 162 LIST OF OPTICAL TRANSCEIVERS FOR TELECOMMUNICATION APPLICATIONS

- TABLE 163 OPTICAL TRANSCEIVER MARKET FOR TELECOMMUNICATION APPLICATIONS, BY FIBER TYPE, 2020-2023 (USD MILLION)

- FIGURE 61 SINGLE-MODE FIBER OPTICAL TRANSCEIVERS TO LEAD MARKET FOR TELECOMMUNICATION APPLICATIONS DURING FORECAST PERIOD

- TABLE 164 OPTICAL TRANSCEIVER MARKET FOR TELECOMMUNICATION APPLICATIONS, BY FIBER TYPE, 2024-2029 (USD MILLION)

- TABLE 165 OPTICAL TRANSCEIVER MARKET FOR TELECOMMUNICATION APPLICATIONS, BY REGION, 2020-2023 (USD MILLION)

- TABLE 166 OPTICAL TRANSCEIVER MARKET FOR TELECOMMUNICATION APPLICATIONS, BY REGION, 2024-2029 (USD MILLION)

- 13.2.1 ULTRA-LONG-HAUL NETWORKS

- 13.3 DATA CENTER

- 13.3.1 DATA CENTER INTERCONNECTS

- 13.3.1.1 Increasing data traffic and demand for higher data rates to create opportunities for 400G transceivers in market

- 13.3.2 INTRA-DATA CENTER CONNECTIONS

- 13.3.2.1 Growing demand for cloud-based services to drive growth of energy-efficient and high-speed transceivers

- TABLE 167 LIST OF OPTICAL TRANSCEIVERS FOR DATA CENTER APPLICATIONS

- TABLE 168 OPTICAL TRANSCEIVER MARKET FOR DATA CENTER APPLICATIONS, BY FIBER TYPE, 2020-2023 (USD MILLION)

- FIGURE 62 MULTIMODE FIBER OPTICAL TRANSCEIVERS TO HOLD LARGER MARKET SHARE FOR DATA CENTER APPLICATIONS DURING FORECAST PERIOD

- TABLE 169 OPTICAL TRANSCEIVER MARKET FOR DATA CENTER APPLICATIONS, BY FIBER TYPE, 2024-2029 (USD MILLION)

- TABLE 170 OPTICAL TRANSCEIVER MARKET FOR DATA CENTER APPLICATIONS, BY REGION, 2020-2023 (USD MILLION)

- TABLE 171 OPTICAL TRANSCEIVER MARKET FOR DATA CENTER APPLICATIONS, BY REGION, 2024-2029 (USD MILLION)

- 13.3.1 DATA CENTER INTERCONNECTS

- 13.4 ENTERPRISE

- 13.4.1 INCREASING NEED FOR HIGH DATA RATES FOR VARIOUS ENTERPRISE APPLICATIONS TO DRIVE MARKET GROWTH

- TABLE 172 LIST OF OPTICAL TRANSCEIVERS FOR ENTERPRISE APPLICATIONS

- TABLE 173 OPTICAL TRANSCEIVER MARKET FOR ENTERPRISE APPLICATIONS, BY FIBER TYPE, 2020-2023 (USD MILLION)

- FIGURE 63 MULTIMODE FIBER OPTICAL TRANSCEIVERS TO HOLD LARGER MARKET SHARE FOR ENTERPRISE APPLICATIONS DURING FORECAST PERIOD

- TABLE 174 OPTICAL TRANSCEIVER MARKET FOR ENTERPRISE APPLICATIONS, BY FIBER TYPE, 2024-2029 (USD MILLION)

- TABLE 175 OPTICAL TRANSCEIVER MARKET FOR ENTERPRISE APPLICATIONS, BY REGION, 2020-2023 (USD MILLION)

- TABLE 176 OPTICAL TRANSCEIVER MARKET FOR ENTERPRISE APPLICATIONS, BY REGION, 2024-2029 (USD MILLION)

14 OPTICAL TRANSCEIVERS MARKET, BY REGION

- 14.1 INTRODUCTION

- FIGURE 64 OPTICAL TRANSCEIVER MARKET IN CHINA TO GROW AT THE HIGHEST CAGR

- TABLE 177 OPTICAL TRANSCEIVER MARKET, BY REGION, 2020-2023 (USD MILLION)

- FIGURE 65 OPTICAL TRANSCEIVER MARKET IN ASIA PACIFIC TO GROW AT THE HIGHEST CAGR DURING THE FORECAST PERIOD

- TABLE 178 OPTICAL TRANSCEIVER MARKET, BY REGION, 2024-2029 (USD MILLION)

- 14.2 NORTH AMERICA

- 14.2.1 RECESSION IMPACT ON MARKET IN NORTH AMERICA

- FIGURE 66 SNAPSHOT: NORTH AMERICAN OPTICAL TRANSCEIVER MARKET

- TABLE 179 NORTH AMERICA: OPTICAL TRANSCEIVER MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 180 NORTH AMERICA: OPTICAL TRANSCEIVER MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 181 NORTH AMERICA: OPTICAL TRANSCEIVER MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 182 NORTH AMERICA: OPTICAL TRANSCEIVER MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 183 NORTH AMERICA: OPTICAL TRANSCEIVER MARKET, BY FIBER TYPE, 2020-2023 (USD MILLION)

- TABLE 184 NORTH AMERICA: OPTICAL TRANSCEIVER MARKET, BY FIBER TYPE, 2024-2029 (USD MILLION)

- TABLE 185 NORTH AMERICA: OPTICAL TRANSCEIVER MARKET, BY DATA RATE, 2020-2023 (USD MILLION)

- TABLE 186 NORTH AMERICA: OPTICAL TRANSCEIVER MARKET, BY DATA RATE, 2024-2029 (USD MILLION)

- TABLE 187 NORTH AMERICA: OPTICAL TRANSCEIVER MARKET, BY WAVELENGTH, 2020-2023 (USD MILLION)

- TABLE 188 NORTH AMERICA: OPTICAL TRANSCEIVER MARKET, BY WAVELENGTH, 2024-2029 (USD MILLION)

- TABLE 189 NORTH AMERICA: OPTICAL TRANSCEIVER MARKET, BY CONNECTOR, 2020-2023 (USD MILLION)

- TABLE 190 NORTH AMERICA: OPTICAL TRANSCEIVER MARKET, BY CONNECTOR, 2024-2029 (USD MILLION)

- TABLE 191 NORTH AMERICA: OPTICAL TRANSCEIVER MARKET, BY DISTANCE, 2020-2023 (USD MILLION)

- TABLE 192 NORTH AMERICA: OPTICAL TRANSCEIVER MARKET, BY DISTANCE, 2024-2029 (USD MILLION)

- TABLE 193 NORTH AMERICA: OPTICAL TRANSCEIVER MARKET, BY PROTOCOL, 2020-2023 (USD MILLION)

- TABLE 194 NORTH AMERICA: OPTICAL TRANSCEIVER MARKET, BY PROTOCOL, 2024-2029 (USD MILLION)

- 14.2.2 US

- 14.2.2.1 Data centers and cloud-based services to fuel market growth

- 14.2.3 CANADA

- 14.2.3.1 Emerging hotspot for data center application and 5G networking to boost market

- 14.2.4 MEXICO

- 14.2.4.1 5G expansion in Mexico to fuel market growth

- 14.3 EUROPE

- 14.3.1 RECESSION IMPACT ON MARKET IN EUROPE

- FIGURE 67 SNAPSHOT: EUROPEAN OPTICAL TRANSCEIVER MARKET

- TABLE 195 EUROPE: OPTICAL TRANSCEIVER MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 196 EUROPE: OPTICAL TRANSCEIVER MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 197 EUROPE: OPTICAL TRANSCEIVER MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 198 EUROPE: OPTICAL TRANSCEIVER MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 199 EUROPE: OPTICAL TRANSCEIVER MARKET, BY FIBER TYPE, 2020-2023 (USD MILLION)

- TABLE 200 EUROPE: OPTICAL TRANSCEIVER MARKET, BY FIBER TYPE, 2024-2029 (USD MILLION)

- TABLE 201 EUROPE: OPTICAL TRANSCEIVER MARKET, BY DATA RATE, 2020-2023 (USD MILLION)

- TABLE 202 EUROPE: OPTICAL TRANSCEIVER MARKET, BY DATA RATE, 2024-2029 (USD MILLION)

- TABLE 203 EUROPE: OPTICAL TRANSCEIVER MARKET, BY WAVELENGTH, 2020-2023 (USD MILLION)

- TABLE 204 EUROPE: OPTICAL TRANSCEIVER MARKET, BY WAVELENGTH, 2024-2029 (USD MILLION)

- TABLE 205 EUROPE: OPTICAL TRANSCEIVER MARKET, BY CONNECTOR, 2020-2023 (USD MILLION)

- TABLE 206 EUROPE: OPTICAL TRANSCEIVER MARKET, BY CONNECTOR, 2024-2029 (USD MILLION)

- TABLE 207 EUROPE: OPTICAL TRANSCEIVER MARKET, BY DISTANCE, 2020-2023 (USD MILLION)

- TABLE 208 EUROPE: OPTICAL TRANSCEIVER MARKET, BY DISTANCE, 2024-2029 (USD MILLION)

- TABLE 209 EUROPE: OPTICAL TRANSCEIVER MARKET, BY PROTOCOL, 2020-2023 (USD MILLION)

- TABLE 210 EUROPE: OPTICAL TRANSCEIVER MARKET, BY PROTOCOL, 2024-2029 (USD MILLION)

- 14.3.2 GERMANY

- 14.3.2.1 Strong infrastructure and cloud-based services integrated with big data, AI, and IoT to boost market in Germany

- 14.3.3 UK

- 14.3.3.1 Increasing number of data center applications to favor market growth

- 14.3.4 FRANCE

- 14.3.4.1 Presence of several big telecom operators to support market

- 14.3.5 REST OF EUROPE (ROE)

- 14.4 ASIA PACIFIC

- 14.4.1 RECESSION IMPACT ON MARKET IN ASIA PACIFIC

- FIGURE 68 SNAPSHOT: APAC OPTICAL TRANSCEIVER MARKET

- TABLE 211 ASIA PACIFIC: OPTICAL TRANSCEIVER MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 212 ASIA PACIFIC: OPTICAL TRANSCEIVER MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 213 ASIA PACIFIC: OPTICAL TRANSCEIVER MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 214 ASIA PACIFIC: OPTICAL TRANSCEIVER MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 215 ASIA PACIFIC: OPTICAL TRANSCEIVER MARKET, BY FIBER TYPE, 2020-2023 (USD MILLION)

- TABLE 216 ASIA PACIFIC: OPTICAL TRANSCEIVER MARKET, BY FIBER TYPE, 2024-2029 (USD MILLION)

- TABLE 217 ASIA PACIFIC: OPTICAL TRANSCEIVER MARKET, BY DATA RATE, 2020-2023 (USD MILLION)

- TABLE 218 ASIA PACIFIC: OPTICAL TRANSCEIVER MARKET, BY DATA RATE, 2024-2029 (USD MILLION)

- TABLE 219 ASIA PACIFIC: OPTICAL TRANSCEIVER MARKET, BY WAVELENGTH, 2020-2023 (USD MILLION)

- TABLE 220 ASIA PACIFIC: OPTICAL TRANSCEIVER MARKET, BY WAVELENGTH, 2024-2029 (USD MILLION)

- TABLE 221 ASIA PACIFIC: OPTICAL TRANSCEIVER MARKET, BY CONNECTOR, 2020-2023 (USD MILLION)

- TABLE 222 ASIA PACIFIC: OPTICAL TRANSCEIVER MARKET, BY CONNECTOR, 2024-2029 (USD MILLION)

- TABLE 223 ASIA PACIFIC: OPTICAL TRANSCEIVER MARKET, BY DISTANCE, 2020-2023 (USD MILLION)

- TABLE 224 ASIA PACIFIC: OPTICAL TRANSCEIVER MARKET, BY DISTANCE, 2024-2029 (USD MILLION)

- TABLE 225 ASIA PACIFIC: OPTICAL TRANSCEIVER MARKET, BY PROTOCOL, 2020-2023 (USD MILLION)

- TABLE 226 ASIA PACIFIC: OPTICAL TRANSCEIVER MARKET, BY PROTOCOL, 2024-2029 (USD MILLION)

- 14.4.2 CHINA

- 14.4.2.1 Advancement of 5G networks with higher bandwidths to drive market opportunities in China

- 14.4.3 JAPAN

- 14.4.3.1 Technological advancements in fiber optics networks to boost market

- 14.4.4 SOUTH KOREA

- 14.4.4.1 Rising communication infrastructure development to drive market in South Korea

- 14.4.5 REST OF ASIA PACIFIC

- 14.5 REST OF THE WORLD (ROW)

- 14.5.1 RECESSION IMPACT ON MARKET IN ROW

- TABLE 227 ROW: OPTICAL TRANSCEIVER MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 228 ROW: OPTICAL TRANSCEIVER MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 229 ROW: OPTICAL TRANSCEIVER MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 230 ROW: OPTICAL TRANSCEIVER MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 231 ROW: OPTICAL TRANSCEIVER MARKET, BY FIBER TYPE, 2020-2023 (USD MILLION)

- TABLE 232 ROW: OPTICAL TRANSCEIVER MARKET, BY FIBER TYPE, 2024-2029 (USD MILLION)

- TABLE 233 ROW: OPTICAL TRANSCEIVER MARKET, BY DATA RATE, 2020-2023 (USD MILLION)

- TABLE 234 ROW: OPTICAL TRANSCEIVER MARKET, BY DATA RATE, 2024-2029 (USD MILLION)

- TABLE 235 ROW: OPTICAL TRANSCEIVER MARKET, BY WAVELENGTH, 2020-2023 (USD MILLION)

- TABLE 236 ROW: OPTICAL TRANSCEIVER MARKET, BY WAVELENGTH, 2024-2029 (USD MILLION)

- TABLE 237 ROW: OPTICAL TRANSCEIVER MARKET, BY CONNECTOR, 2020-2023 (USD MILLION)

- TABLE 238 ROW: OPTICAL TRANSCEIVER MARKET, BY CONNECTOR, 2024-2029 (USD MILLION)

- TABLE 239 ROW: OPTICAL TRANSCEIVER MARKET, BY DISTANCE, 2020-2023 (USD MILLION)

- TABLE 240 ROW: OPTICAL TRANSCEIVER MARKET, BY DISTANCE, 2024-2029 (USD MILLION)

- TABLE 241 ROW: OPTICAL TRANSCEIVER MARKET, BY PROTOCOL, 2020-2023 (USD MILLION)

- TABLE 242 ROW: OPTICAL TRANSCEIVER MARKET, BY PROTOCOL, 2024-2029 (USD MILLION)

- 14.5.2 SOUTH AMERICA

- 14.5.2.1 Increasing data traffic growth to support market

- 14.5.3 GCC

- 14.5.3.1 Advancements in 5G technology to boost market growth

- 14.5.4 REST OF MIDDLE EAST & AFRICA (MEA)

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- TABLE 243 OVERVIEW OF STRATEGIES DEPLOYED BY OPTICAL TRANSCEIVER COMPANIES

- 15.2.1 PRODUCT PORTFOLIO

- 15.2.2 REGIONAL FOCUS

- 15.2.3 MANUFACTURING FOOTPRINT

- 15.2.4 ORGANIC/INORGANIC PLAY

- 15.3 REVENUE ANALYSIS

- FIGURE 69 REVENUE ANALYSIS OF KEY PLAYERS IN OPTICAL TRANSCEIVER MARKET

- 15.4 MARKET SHARE ANALYSIS

- TABLE 244 DEGREE OF COMPETITION IN OPTICAL TRANSCEIVER MARKET, 2023

- FIGURE 70 OPTICAL TRANSCEIVER MARKET: MARKET SHARE ANALYSIS, 2023

- 15.5 COMPANY VALUATION AND FINANCIAL METRICS

- FIGURE 71 OPTICAL TRANSCEIVER MARKET: COMPANY VALUATION

- FIGURE 72 OPTICAL TRANSCEIVER MARKET: FINANCIAL METRICS

- 15.6 BRAND/PRODUCT COMPARISON

- 15.7 COMPANY EVALUATION MATRIX: KEY PLAYERS

- 15.7.1 STARS

- 15.7.2 EMERGING LEADERS

- 15.7.3 PERVASIVE PLAYERS

- 15.7.4 PARTICIPANTS

- FIGURE 73 OPTICAL TRANSCEIVER MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

- 15.7.5 COMPANY FOOTPRINT ANALYSIS

- FIGURE 74 OVERALL COMPANY FOOTPRINT (25 KEY PLAYERS)

- TABLE 245 COMPANY APPLICATION FOOTPRINT

- TABLE 246 COMPANY DATA RATE FOOTPRINT (25 COMPANIES)

- TABLE 247 COMPANY FORM FACTOR FOOTPRINT (25 COMPANIES)

- TABLE 248 COMPANY REGIONAL FOOTPRINT (25 COMPANIES)

- 15.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES

- 15.8.1 PROGRESSIVE COMPANIES

- 15.8.2 RESPONSIVE COMPANIES

- 15.8.3 DYNAMIC COMPANIES

- 15.8.4 STARTING BLOCKS

- FIGURE 75 OPTICAL TRANSCEIVER MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2023

- 15.8.5 COMPETITIVE BENCHMARKING

- TABLE 249 OPTICAL TRANSCEIVER MARKET: LIST OF KEY STARTUPS/SMES

- TABLE 250 OPTICAL TRANSCEIVER MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES

- TABLE 251 OPTICAL TRANSCEIVER MARKET: PRODUCT LAUNCHES, JANUARY 2020- FEBRUARY 2024

- 15.9.2 DEALS

- TABLE 252 OPTICAL TRANSCEIVER MARKET: DEALS, JANUARY 2020- JANUARY 2024

- 15.9.3 OTHER DEVELOPMENTS

- TABLE 253 OPTICAL TRANSCEIVER MARKET: OTHER DEVELOPMENTS, JANUARY 2020- JANUARY 2024

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- (Business Overview, Products Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats))**

- 16.1.1 COHERENT CORP.

- TABLE 254 COHERENT CORP.: COMPANY OVERVIEW

- FIGURE 76 COHERENT CORP.: COMPANY SNAPSHOT (2023)

- TABLE 255 COHERENT CORP.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 256 COHERENT CORP.: PRODUCT LAUNCHES

- TABLE 257 COHERENT CORP.: DEALS

- TABLE 258 COHERENT CORP.: OTHER DEVELOPMENTS

- 16.1.2 INNOLIGHT

- TABLE 259 INNOLIGHT: BUSINESS OVERVIEW

- TABLE 260 INNOLIGHT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 261 INNOLIGHT: PRODUCT LAUNCHES

- TABLE 262 INNOLIGHT: DEALS

- TABLE 263 INNOLIGHT: OTHER DEVELOPMENTS

- 16.1.3 ACCELINK TECHNOLOGY CO. LTD.

- TABLE 264 ACCELINK TECHNOLOGY CO. LTD.: BUSINESS OVERVIEW

- FIGURE 77 ACCELINK TECHNOLOGY CO. LTD.: COMPANY SNAPSHOT (2022)

- TABLE 265 ACCELINK TECHNOLOGY CO. LTD.: EXPANSIONS

- 16.1.4 HISENSE BROADBAND, INC.

- TABLE 266 HISENSE BROADBAND, INC.: BUSINESS OVERVIEW

- TABLE 267 HISENSE BROADBAND, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 268 HISENSE BROADBAND, INC.: PRODUCT LAUNCHES

- 16.1.5 CISCO SYSTEMS, INC.

- TABLE 269 CISCO SYSTEMS, INC.: COMPANY OVERVIEW

- FIGURE 78 CISCO SYSTEMS, INC.: COMPANY SNAPSHOT (2023)

- TABLE 270 CISCO SYSTEMS, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 271 CISCO SYSTEMS, INC.: DEALS

- 16.1.6 BROADCOM INC.

- TABLE 272 BROADCOM INC.: COMPANY OVERVIEW

- FIGURE 79 BROADCOM INC.: COMPANY SNAPSHOT (2023)

- TABLE 273 BROADCOM INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 274 BROADCOM INC.: PRODUCT LAUNCHES

- 16.1.7 LUMENTUM OPERATIONS LLC

- TABLE 275 LUMENTUM OPERATIONS LLC: BUSINESS OVERVIEW

- FIGURE 80 LUMENTUM OPERATIONS LLC: COMPANY SNAPSHOT (2023)

- TABLE 276 LUMENTUM OPERATIONS LLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 277 LUMENTUM OPERATIONS LLC: PRODUCT LAUNCHES

- TABLE 278 LUMENTUM OPERATIONS LLC: DEALS

- 16.1.8 SUMITOMO ELECTRIC INDUSTRIES, LTD.

- TABLE 279 SUMITOMO ELECTRIC INDUSTRIES, LTD.: BUSINESS OVERVIEW

- FIGURE 81 SUMITOMO ELECTRIC INDUSTRIES, LTD.: COMPANY SNAPSHOT (2022)

- TABLE 280 SUMITOMO ELECTRIC INDUSTRIES, LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 281 SUMITOMO ELECTRIC INDUSTRIES, LTD.: DEALS

- 16.1.9 INTEL CORPORATION

- TABLE 282 INTEL CORPORATION: BUSINESS OVERVIEW

- FIGURE 82 INTEL CORPORATION: COMPANY SNAPSHOT (2023)

- TABLE 283 INTEL CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 284 INTEL CORPORATION: PRODUCT LAUNCHES

- TABLE 285 INTEL CORPORATION: DEALS

- 16.1.10 FUJITSU OPTICAL COMPONENTS LIMITED

- TABLE 286 FUJITSU OPTICAL COMPONENTS LIMITED: BUSINESS OVERVIEW

- TABLE 287 FUJITSU OPTICAL COMPONENTS LIMITED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 288 FUJITSU OPTICAL COMPONENTS LIMITED: PRODUCT LAUNCHES

- 16.2 OTHER KEY PLAYERS

- 16.2.1 CIENA CORPORATION

- 16.2.2 NVIDIA CORPORATION

- 16.2.3 APPLIED OPTOELECTRONICS, INC.

- 16.2.4 HUAGONG ZHENGYUAN

- 16.2.5 NEC CORPORATION

- 16.2.6 PERLE SYSTEMS

- 16.2.7 SMITHS INTERCONNECT

- 16.2.8 SMARTOPTICS

- 16.2.9 SOLID OPTICS

- 16.2.10 SOURCE PHOTONICS

- 16.2.11 HUAWEI TECHNOLOGIES CO., LTD.

- 16.2.12 EOPTOLINK TECHNOLOGY INC.

- 16.2.13 INFINERA

- 16.2.14 FOCI

- 16.2.15 AMPHENOL COMMUNICATIONS SOLUTIONS

- *Details on Business Overview, Products Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats) might not be captured in case of unlisted companies.

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS