光トランシーバ:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Optical Transceiver - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 144 Pages

- 納期

- 2~3営業日

- 商品コード

- 1683460

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

光トランシーバの市場規模は2025年に150億9,000万米ドルと推計され、2030年には279億1,000万米ドルに達すると予測され、市場推計・予測期間(2025~2030年)のCAGRは13.09%です。

光トランシーバは、光ファイバートランシーバとも呼ばれ、光ファイバーネットワークでデータの送受信に使用される相互接続コンポーネントです。トランスミッターとレシーバーの2つの主要部品で構成されます。トランスミッターは電気信号を光信号に変換し、光ファイバーケーブルを通して伝送します。一方、レシーバーは光信号を受信し、電気信号に変換します。

主なハイライト

- 光トランシーバは、長距離の高速データ伝送を可能にします。ビデオストリーミング、クラウドコンピューティング、データセンターなどの高帯域幅アプリケーションをサポートできます。光トランシーバは、信号の大幅な劣化なしに長距離のデータ伝送が可能です。光ファイバーケーブルで何キロものデータ伝送を必要とする通信やネットワーキング・アプリケーションで一般的に使用されています。

- いくつかの要因により、電気通信業界では高度な通信に対するニーズが高まっています。このような要因には、エネルギー効率の要求、高度な接続性の提供への注力、モノのインターネット(IoT)や人工知能(AI)などの新技術の台頭などがあります。通信事業者は、高度な接続性とより高いパフォーマンスを顧客に提供しようと努力しています。これには、5G、エッジコンピューティング、ネットワークインフラの改善といった技術の導入が含まれます。これらの進歩により、より高速で信頼性の高い通信サービスが可能になります。ベアラネットワークの高度な開発とアップグレードにより、5G技術の進展と基地局の展開に伴い、光通信ネットワーク機器の需要が増加すると予測されています。

- クラウドベースのサービスは、近年需要が大幅に増加しています。クラウド・コンピューティングは、オンプレミスのサーバーやハードウェアを不要にすることで、企業のITインフラ・コストを削減することを可能にします。その代わり、企業はオンデマンドでコンピューティング・リソースやサービスにアクセスでき、使用した分だけ料金を支払うことができます。また、クラウド・サービスは、需要に応じてリソースを増減できます。その大きな利点からクラウドサービスの採用が増えれば、高度な通信インフラに対する大規模な需要が生まれ、光トランシーバ市場を牽引することになります。

- データセンターなどの光トランシーバは、大容量データトランスミッションネットワークに不可欠です。近年、光トランシーバのネットワーク複雑化が進んでいます。最新のネットワークでは高いデータレートが要求されるため、1Gから400Gまでの速度でデータを伝送できる光トランシーバが開発されています。データレートが高くなると、信頼性が高く効率的なデータ伝送を確保するため、より高度な設計と技術が必要になります。

- COVID-19の発生はデータの利用を増加させました。中国で革新的なインターネットを利用したエンターテインメント・サービスを提供する大手プラットフォーム、Maoyan Entertainmentによる、COVID-19の流行が中国のエンターテインメント業界に与えた影響に関する報告書によると、映画業界はパンデミックによって深刻な打撃を受けたが、テレビやストリーミング・プラットフォームを含むオンライン・エンターテインメント市場は、人々が家に閉じこもっていたため活況を呈していました。これが市場の成長につながりました。

光トランシーバ市場動向

データセンターが光トランシーバの急成長アプリケーションに

- 現代のデジタルサービスのバックボーンとして機能するデータセンターの急増により、効率的で信頼性の高い接続ソリューションが必要とされています。光トランシーバは、これらのデータセンター内で中断のないデータフローを維持するために必要な速度、容量、拡張性を提供します。

- データセンターは、調査した市場の重要な促進要因として浮上しています。AIやハイパフォーマンスコンピューティング(HPC)のようなデータや技術の普及に伴い、データセンター資産を迅速、確実、コスト効率よく接続する必要性が著しく高まっています。スループット、遅延、運用の簡素化、メンテナンス、インテリジェンス、セキュリティは、データセンター・ベンダーにとって重要な優先事項となりつつあります。

- データセンター・ネットワークは、光ファイバー技術を急速に採用しています。データセンター用のファイバーベースのネットワークは、多数の光ファイバー機器を組み合わせることで構築されます。このような大容量ネットワークでは、光トランシーバが重要な役割を果たします。現在、最新のデータセンター・ネットワークの大半は、大容量のデータ・トランスミッションを必要としています。

- 米国に本社を置くInphiは、データセンター・アプリケーションをますますターゲットにし、シリコンフォトニクスとDSP技術を活用した400Gデータセンター相互接続光モジュールなどの先進的な製品でマーケットプレースを拡大しています。Cloudsceneによると、2023年9月現在、米国には5375のデータセンターがあり、世界のどの国よりも多いです。さらに522ヵ所がドイツに、517ヵ所が英国にあります。

- クラウドアプリケーション、AI、ビッグデータの導入が進むにつれ、さまざまな地域でデータセンター建設の需要が高まっています。より多くの組織が業務をクラウドに移行するにつれて、そのニーズをサポートするためにより高度なデータセンターが必要となります。例えば、メトロエッジは2023年1月、データセンター施設の設計・建設について、クルーン・コンストラクションやその他の建設会社と最終合意しました。このプロジェクトは、今後数カ月以内に完全な権利を取得し、まもなく着工する予定です。

- マイクロソフトは2023年11月、ケベック州でのクラウド・コンピューティングとAIインフラの拡大に今後2年間で5億米ドルを投資すると発表しました。この発表では、L'Ancienne-Lorette、Donnacona、Saint-Augustin-de-Desmaures、Levisにおける将来のデータセンター立地が言及されており、間もなく建設が開始されます。

北米が最大の市場シェアを占める

- 北米は、通信環境の拡大とインターネットの普及により、光トランシーバ市場の開拓に大きく貢献している国の一つです。こうした動向は接続性の向上を要求し、北米の光トランシーバ需要を増大させています。SaaSソリューション企業でオンラインメディアモニタリング企業のMeltwaterによると、2023年10月時点の米国のインターネット普及率は91.8%。

- 米国ではインターネットの普及率が高く、AI、5G、IoT、ハイパフォーマンス・コンピューティングなどの先進技術が導入されているため、高いデータ転送速度が求められており、これが市場の成長を後押ししています。

- データトラフィックの増加は、企業や消費者が生成するデータをサポートする多くのデータセンターを開発する追加需要を生み出しています。米国ではクラウド・コンピューティング・サービスやアプリケーションの利用も拡大する見込みで、大規模なハイパースケール・クラウド・ベース・データセンターの開発につながっています。

- グーグル(米国)、マイクロソフト(米国)、アマゾン(米国)などの主要データセンター企業の存在も、北米の光トランシーバ市場の成長に大きく貢献しています。グーグルやマイクロソフトなどのクラウドサービスプロバイダは、データセンタに高データレート光トランシーバを導入しています。

- データの急増とAIやハイパフォーマンスコンピューティング(HPC)などの技術の拡大に伴い、データセンタ資産を迅速、確実、コスト効率よく接続する必要性が大きく高まっています。スループット、レイテンシー、運用・保守の簡素化、インテリジェンス、セキュリティといった要素は、地域のデータセンター・ベンダーにとって主要な優先事項となりつつあります。米国は、5G展開への投資率が高いことから、5G市場の主要なイノベーターであり投資家の1つです。

光トランシーバ市場の概要

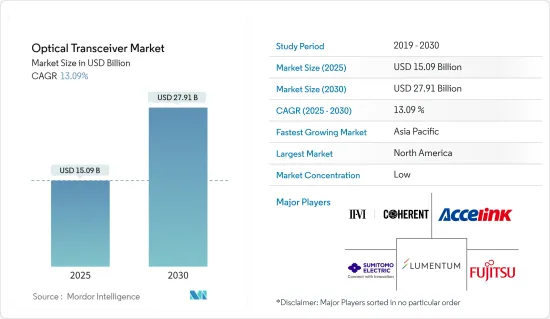

光トランシーバ市場は、コヒレント社(II-VI Incorporated)、アクセルリンク・テクノロジーズ社(Accelink Technologies)、ルメンタム・オペレーションズ社(Lumentum Operations LLC)、住友電気工業社(Sumitomo Electric Industries Ltd)、富士通オプティカルコンポーネンツ社(Fujitsu Optical Components Limited)などの大手企業が存在し、非常に断片化されています。市場のプレーヤーは、製品ラインナップを強化し、持続可能な競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2023年12月II-VI Incorporatedは、光通信ネットワーク向けに超小型QSFP-DDとOSFPフォームファクタの800G ZR/ZR+トランシーバを発表しました。コヒレント社の800G ZR/ZR+トランシーバは、IPルーターのQSFP-DDおよびOSFPトランシーバスロットに直接差し込むことができる世界初のデジタルコヒーレントオプティクス(DCO)です。

- 2023年10月ソースフォトニクスは、スコットランドのグラスゴーで開催されたECOC 2023で、AIクラスタ接続用の800Gbpsショートリーチマルチモード(MMF)トランシーバとアクティブケーブルの提供を発表しました。これは、ショートリーチの光プラガブルモジュールとアクティブケーブルアプリケーションで、AIデータセンターインフラが飛躍的に高速化することを可能にします。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19の影響とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 高度通信へのニーズの高まり

- クラウドベースのサービスに対する需要の増加

- 市場抑制要因

- ネットワークの複雑化

第6章 市場セグメンテーション

- プロトコル別

- イーサネット

- ファイバーチャネル

- CWDM/DWDM

- FTTX

- その他のプロトコル

- データレート別

- 10Gbps未満

- 10 Gbps~40 Gbps

- 100 Gbps

- 100Gbps以上

- 用途別

- データセンター

- 通信

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Coherent Corp.(II-VI Incorporated)

- Accelink Technologies

- Lumentum Operations LLC(Lumentum Holdings)

- Sumitomo Electric Industries Ltd

- Fujitsu Optical Components Limited(Fujitsu Ltd)

- Smiths Interconnect(Reflex Photonics Inc.)

- Source Photonics(Redview Capital)

- Huawei Technologies Co. Ltd

- Broadcom Inc.

- HUBER+SUHNER Cube Optics

第8章 投資分析

第9章 市場機会と今後の動向

目次

The Optical Transceiver Market size is estimated at USD 15.09 billion in 2025, and is expected to reach USD 27.91 billion by 2030, at a CAGR of 13.09% during the forecast period (2025-2030).

An optical transceiver, also known as a fiber optic transceiver, is an interconnect component used to transmit and receive data in a fiber-optic network. It consists of two main parts: a transmitter and a receiver. The transmitter converts electrical signals into light signals, which are transmitted through fiber optic cables. The receiver, on the other hand, receives light signals and converts them back into electrical signals.

Key Highlights

- Optical transceivers enable high-speed data transmission over long distances. They can support high bandwidth applications like video streaming, cloud computing, and data centers. They can transmit data over long distances without significant signal degradation. They are commonly used in telecommunications and networking applications that require data transmission over kilometers of fiber optic cables.

- Due to several factors, the telecom industry is experiencing an increasing need for advanced communication. These factors include the demand for energy efficiency, the focus on delivering advanced connectivity, and the rise of new technologies such as the Internet of Things (IoT) and artificial intelligence (AI). Telecom companies strive to deliver advanced connectivity and higher performance to their customers. This includes deploying technologies like 5G, edge computing, and improved network infrastructure. These advancements enable faster and more reliable communication services. The advanced development and upgrade of the bearer network is anticipated to drive the demand for optical communication network equipment to increase as 5G technology progresses and base stations are deployed.

- Cloud-based services have experienced a significant increase in demand in recent years. Cloud computing allows businesses to reduce their IT infrastructure costs by eliminating the need for on-premises servers and hardware. Instead, companies can access computing resources and services on demand, paying only for what they use. Cloud services also offer the ability to scale resources up or down based on demand. The increasing adoption of cloud services owing to their significant advantages would create massive demand for advanced communication infrastructure, thereby driving the optical transceivers market.

- Optical transceivers, such as data centers, are critical in high-capacity data transmission networks. In recent years, there has been an increase in network complexity in optical transceivers. The demand for high data rates in modern networks has led to the development of optical transceivers capable of transmitting data at speeds ranging from 1G to 400 G. The higher data rates require more sophisticated designs and technologies to ensure reliable and efficient data transmission.

- The outbreak of COVID-19 increased the usage of data. According to a report on the impact of the COVID-19 pandemic on China's entertainment industry by Maoyan Entertainment, a leading platform providing innovative Internet-empowered entertainment services in China, the movie industry was severely hit by the pandemic, whereas the online entertainment market, including TV and streaming platforms, were booming as people were confined to their homes. This has led to the growth of the market.

Optical Transceiver Market Trends

Data Centers to the Fastest Growing Application for Optical Transceivers

- The proliferation of data centers, which serve as the backbone of modern digital services, requires efficient and reliable connectivity solutions. Optical transceivers offer the speed, capacity, and scalability required to maintain the uninterrupted data flow within these data centers.

- Data centers are emerging as significant drivers in the market studied. With the proliferation of data and technologies, like AI and high-performance computing (HPC), the need to connect data center assets quickly, reliably, and cost-effectively is growing significantly. Throughput, latency, simplified operations, maintenance, intelligence, and security are becoming significant priorities for data center vendors.

- Data center networks are rapidly adopting fiber optics technology. A fiber-based network for data centers is built by combining many fiber optic devices. In these high-capacity networks, optical transceivers play a significant role. The majority of modern data center networks currently necessitate high-capacity data transmission.

- US-based Inphi is increasingly targeting data center applications and extending its marketplace with advanced products, including 400G data center interconnect optical modules, which leverage their silicon photonics and DSP technologies. According to Cloudscene, as of September 2023, there were 5,375 data centers in the United States, the most of any country worldwide. A further 522 were in Germany, while 517 were in the United Kingdom.

- The growing adoption of cloud applications, AI, and big data drives the demand for data center construction across various regions. As more organizations shift their operations to the cloud, they require more advanced data centers to support their needs. For instance, in January 2023, Metro Edge finalized agreements with Clune Construction and other construction firms to design and build the data center facility. The project is expected to have full entitlements within the next few months and break ground shortly after.

- In November 2023, Microsoft announced it would invest USD 500 million in expanding its cloud computing and AI infrastructure in Quebec over the next two years. The announcement references future data center locations in L'Ancienne-Lorette, Donnacona, Saint-Augustin-de-Desmaures, and Levis, with construction starting soon.

North America Holds Largest Market Share

- North America is one of the significant contributors to the optical transceiver market's development due to the growing communication landscape and the massive internet penetration. These trends demand improved connectivity, increasing the demand for optical transceivers in North America. According to Meltwater, a software-as-a-service solution company and an online media monitoring company, as of October 2023, the internet penetration rate as of October 2023 in the United States was 91.8%.

- The high adoption of the Internet and advanced technologies like AI, 5G, IoT, and high-performance computing in the United States is driving the need for a high data transmission rate, which drives the market's growth.

- Increasing data traffic has created additional demand for developing many data centers that support data generated by businesses and consumers. The use of cloud-computing services and applications is also expected to grow in the United States, leading to the development of large hyperscale cloud-based data centers.

- The presence of some of the key data center companies like Google (US), Microsoft (US), and Amazon (US) has also contributed significantly to the growth of the optical transceiver market in North America. Cloud service providers like Google and Microsoft are implementing high-data-rate optical transceivers in their data centers.

- With the proliferation of data and expansion of technologies like AI and high-performance computing (HPC), the need to connect data center assets quickly, reliably, and cost-effectively is growing significantly. Factors such as throughput, latency, simplified operations and maintenance, intelligence, and security are becoming major priorities for regional data center vendors. The United States is one of the major innovators and investors in the 5G market, owing to a high investment rate for 5G deployment.

Optical Transceiver Market Overview

The optical transceiver market is highly fragmented, with the presence of major players like Coherent Corp. (II-VI Incorporated), Accelink Technologies, Lumentum Operations LLC (Lumentum Holdings), Sumitomo Electric Industries Ltd, and Fujitsu Optical Components Limited (Fujitsu Ltd). Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- December 2023: II-VI Incorporated introduced its 800G ZR/ZR+ transceiver in ultracompact QSFP-DD and OSFP form factors for optical communications networks. The 800G ZR/ZR+ transceivers from Coherent are the world's first digital coherent optics (DCO) that can plug directly into QSFP-DD and OSFP transceiver slots on IP routers.

- October 2023: Source Photonics announced the availability of 800 Gbps short-reach multimode (MMF) transceivers and active cables for AI cluster connectivity at ECOC 2023 in Glasgow, Scotland, that enables AI data center infrastructure to achieve dramatically higher speeds for short-reach optical pluggable modules and active cable applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Need for Advanced Communication

- 5.1.2 Increasing Demand for Cloud-based Services

- 5.2 Market Restraints

- 5.2.1 Increase in Network Complexity

6 MARKET SEGMENTATION

- 6.1 By Protocol

- 6.1.1 Ethernet

- 6.1.2 Fiber Channel

- 6.1.3 CWDM/DWDM

- 6.1.4 FTTX

- 6.1.5 Other Protocols

- 6.2 By Data Rate

- 6.2.1 Less than 10 Gbps

- 6.2.2 10 Gbps to 40 Gbps

- 6.2.3 100 Gbps

- 6.2.4 Greater than 100 Gbps

- 6.3 By Application

- 6.3.1 Data Center

- 6.3.2 Telecommunication

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Coherent Corp. (II-VI Incorporated)

- 7.1.2 Accelink Technologies

- 7.1.3 Lumentum Operations LLC (Lumentum Holdings)

- 7.1.4 Sumitomo Electric Industries Ltd

- 7.1.5 Fujitsu Optical Components Limited (Fujitsu Ltd)

- 7.1.6 Smiths Interconnect (Reflex Photonics Inc.)

- 7.1.7 Source Photonics (Redview Capital)

- 7.1.8 Huawei Technologies Co. Ltd

- 7.1.9 Broadcom Inc.

- 7.1.10 HUBER+SUHNER Cube Optics

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 144 Pages

- 納期

- 2~3営業日