|

|

市場調査レポート

商品コード

1455826

建築用断熱材の世界市場:材料別、用途別、建築物の種類別、地域別 - 予測(~2028年)Building Thermal Insulation Market by Material (Glass Wool, Stone Wool, Plastic Foam), Application (Roof Insulation, Floor Insulation, Wall Insulation), Building Type (Residential, Non-Residential) & Region - Global Forecast to 2028 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 建築用断熱材の世界市場:材料別、用途別、建築物の種類別、地域別 - 予測(~2028年) |

|

出版日: 2024年03月21日

発行: MarketsandMarkets

ページ情報: 英文 263 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

建築用断熱材市場は、2023年の292億米ドルからCAGR 4.8%と堅調な伸びを示し、2028年には370億米ドルに達すると予測され、着実な成長が見込まれています。

建物居住者の快適性は、近代建築における優先事項です。適切な断熱材を使用することで、一年中均一で快適な室内温度を維持することができます。グリーンビルディングは環境に優しい方法に焦点を当てています。さらに、建築用断熱材はエネルギー使用量を削減することで、温室効果ガスの排出量も削減します。

| 調査範囲 | |

|---|---|

| 調査期間 | 2017~2028年 |

| 基準年 | 2022年 |

| 予測期間 | 2023~2028年 |

| 単位 | 金額 (100万米ドル) および数量 (キロトン) |

| セグメント | 材料別、用途別、建築物の種類別、地域別 |

| 対象地域 | アジア太平洋、北米、欧州、中東・アフリカ、南米 |

"材料別に見ると、発泡プラスチックのセグメントが予測期間中、金額ベースで最も急成長する"

発泡プラスチックセグメントは、2022年の建築用断熱材市場において、金額ベースで最大の用途です。発泡プラスチックは軽量で柔軟性があるため、様々な建築要件に合わせて成型や成形が可能です。耐火性と熱特性を改善した発泡プラスチック組成物は、メーカーにより継続的に開発されています。発泡プラスチックは、他の断熱材と比較した場合、競争力のある価格帯と強い耐熱性 (R値) を持っています。

"予測期間中、用途別では壁面断熱材が金額ベースで最も急成長する"

壁面断熱材のセグメントは、その汎用性の高い特性により、2022年に金額ベースで世界の建築用断熱材市場をリードしました。耐候性と防音性の向上、建物の熱性能の向上とCO2排出量の削減は、建築用断熱材市場における壁面断熱材の需要を促進する特性の一部です。

"予測期間中、建築物の種類別では住宅分野が金額ベースで最も急成長する"

住宅は、多くの要因により建築用断熱材市場を独占しています。この優位性は、住宅建設における建築用断熱材の広範な用途によるものです。住宅の壁、床、屋根、地下室の断熱に幅広く使用されています。これは、その優れた断熱性、耐湿性、構造的支持性から、エネルギー効率、快適な室内環境、建築基準法の遵守に貢献する材料として好んで選ばれています。建築用断熱材市場は、業界基準の変化や規制の圧力から、住宅用建物でもますます人気が高まっています。

"2022年の建築用断熱材市場は金額ベースで欧州が最大となった"

Kingspan Group PLC、BASF SE、Saint-Gobain SAなど、この業界におけるこの地域の地位を強化した大手企業の存在により、欧州は2022年の建築用断熱材市場で支配的な地位を占めました。欧州は、建築用断熱材市場として重要な位置を占めていますが、その主な理由は、同地域全体の建築慣行におけるエネルギー効率と断熱基準を強調する厳しい建築規制によるものです。これらの規制は、住宅、非住宅、その他を含む様々な建物タイプにおける建築用断熱材の広範な採用を推進しています。

当レポートに掲載されている主要企業は、Kingspan Group PLC (英国)、Knauf Gips KG (ドイツ)、Owens Corning (米国)、Rockwool A/S (デンマーク)、Saint-Gobain SA (フランス)、BASF SE (ドイツ)、Dow Inc. (米国)、Johns Manville Corporation (米国)、GAF Materials Corporation (米国)、CNBM Group (中国)、Aspen Aerogels, Inc. (米国) などです。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- ポーターのファイブフォース分析

- マクロ経済指標

- 主要国のGDP動向と予測

第6章 業界の動向

- サプライチェーン分析

- 原材料

- 製造業

- 流通網

- 活用領域

- 主要な利害関係者と購入基準

- 購入プロセスにおける主要な利害関係者

- 購入基準

- 顧客のビジネスに影響を与える動向/ディスラプション

- エコシステム分析

- ケーススタディ

- 地域社会の福祉の向上:WILMCOTE HOUSEの熱効率の改善

- 技術分析

- 主要技術

- 補完技術

- 価格分析

- 主要企業の平均販売価格の傾向:用途別

- 平均販売価格の傾向:地域別

- 貿易分析

- 建築用断熱材の輸入シナリオ

- 建築用断熱材の輸出シナリオ

- 規制状況

- 主要な会議とイベント (2024~2025年)

- 投資と資金調達のシナリオ

- 特許分析

第7章 建築用断熱材市場:材料別

- イントロダクション

- 発泡プラスチック

- 発泡ポリスチレン

- ポリウレタン (PUR)・ポリイソシアヌレート (PIR) フォーム

- その他の発泡プラスチック

- グラスウール

- ストーンウール

- その他の材料

- エアロゲル

- セルロース

- セルラーガラス

第8章 建築用断熱材市場:建築物の種類別

- イントロダクション

- 非住宅用建物

- 工業用建物

- 商業ビル

- その他

- 住宅

第9章 建築用断熱材市場:用途別

- イントロダクション

- 壁面断熱材

- 外壁断熱材

- 内壁断熱材

- 空洞壁断熱材

- 屋根断熱材

- 平屋根断熱材

- 傾斜屋根断熱材

- 床面断熱材

第10章 建築用断熱材市場:地域別

- イントロダクション

- 欧州

- アジア太平洋

- 北米

- 中東・アフリカ

- 南米

第11章 競合情勢

- イントロダクション

- 主要企業の戦略

- 市場シェア分析

- 収益分析

- 企業評価と財務指標

- ブランド/製品の比較

- 企業評価マトリックス:主要企業

- 企業評価マトリックス:スタートアップ/中小企業

- 競合シナリオと動向

- 製品の発売

- 資本取引

- 拡張

第12章 企業プロファイル

- 主要企業 (事業概要、主要製品、近年の動向、MnMの見解)

- KINGSPAN GROUP PLC

- KNAUF GIPS KG

- OWENS CORNING

- ROCKWOOL A/S

- SAINT-GOBAIN SA

- BASF SE

- DOW INC.

- JOHNS MANVILLE CORPORATION

- GAF MATERIALS CORPORATION

- CNBM GROUP CO., LTD.

- ASPEN AEROGELS, INC.

- その他の企業

- ATLAS ROOFING CORPORATION

- HOLCIM LIMITED

- HUNTSMAN INTERNATIONAL LLC

- KCC CORPORATION

- LAPOLLA INDUSTRIES, INC.

- NICHIAS CORPORATION

- RECTICEL SA

- ODE INSULATION

- TROCELLEN GMBH

- URSA INSULATION SA

- SIKA GROUP

- CELLOFOAM NORTH AMERICA, INC.

- NEO THERMAL INSULATION (INDIA) PVT. LTD.

- LLOYD INSULATIONS (INDIA) LIMITED

第13章 隣接市場および関連市場

- イントロダクション

- 制限

- 断熱製品市場

- 断熱製品市場:地域別

第14章 付録

The building thermal insulation market is poised for steady growth, with a projected value of USD 37.0 billion by 2028, exhibiting a robust CAGR of 4.8% from its 2023 value of USD 29.2 billion. The comfort of building residents is a priority in modern construction. An even and comfortable interior temperature can be sustained all year round with the aid of proper thermal insulation. Green building focuses on eco-friendly methods. Moreover, building thermal insulation subsequently reduces greenhouse gas emissions by lowering energy usage.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2017-2028 |

| Base Year | 2022 |

| Forecast Period | 2023-2028 |

| Units Considered | Value (USD Million) and Volume (Kiloton) |

| Segments | Material, Application, Building type and Region |

| Regions covered | Asia Pacific, North America, Europe, Middle East & Africa, and South America |

"Plastic foam segment is projected to be the fastest growing material of building thermal insulation, in terms of value, during the forecast period."

The plastic foam segment is the largest application in the building thermal insulation market in terms of value, in 2022. Plastic foam is lightweight and flexible enough to be molded and sculpted to meet a variety of construction requirements. Improved plastic foam compositions with improved fire resistance and thermal characteristics are continuously being developed by manufacturers. Plastic foam has a competitive price point and strong thermal resistance (R-value) when compared to certain other insulation materials.

"Wall Insulation to be the fastest growing application for building thermal insulation market, in terms of value, during the forecast period"

The building thermal insulation market is segmented into wall insulation, floor insulation, and roof insulation based on application. The wall insulation application segment led the global building thermal insulation market, in terms of value, in 2022 due to its versatile properties. Enhanced weatherproofing and soundproofing, improved building's thermal performance while reducing its CO2 emission are some of the properties that fuel the demand for wall insulation in building thermal insulation market.

"Residential segment to be the fastest growing building type for building thermal insulation market, in terms of value, during the forecast period"

The residential building type dominates the building thermal insulation market due to many factors. The dominance is due to the extensive applications of building thermal insulation in residential construction. It finds wide use in residential buildings for insulating walls, floors, roofs, and basements. This is a favorably chosen material that contributes to energy efficiency, comfortable indoor conditions, and adherence to building codes because of its outstanding thermal insulating qualities, moisture resistance, and structural support. The building thermal insulation market is also becoming increasingly popular in the residential buildings because of changing industry standards and regulatory pressure.

"Europe was the largest building thermal insulation market in 2022, in terms of value."

Europe held a dominant position in the building thermal insulation market in 2022, owing to the presence of significant players such as Kingspan Group PLC, BASF SE, Saint-Gobain SA, who have strengthened the region's standing in this industry. Europe has a significant market for building thermal insulation, primarily due to stringent building regulations emphasizing energy efficiency and insulation standards in construction practices across the region. These regulations have driven the widespread adoption of building thermal insulation in various building types, including residential, non-residential, and others.

In the meticulous process of determining and verifying market sizes for multiple segments and subsegments, extensive primary interviews were conducted. A breakdown of the profiles of the primary interviewees are as follows:

- By Company Type: Tier 1 - 69%, Tier 2 - 23%, and Tier 3 - 8%

- By Designation: - C-Level - 23%, Director Level - 37%, and Others - 40%

- By Region: North America - 32%, Europe - 21%, Asia Pacific - 28%, South America - 7%, and Middle East & Africa - 12%,

The key market players illustrated in the report include Kingspan Group PLC (UK), Knauf Gips KG (Germany), Owens Corning (US), Rockwool A/S (Denmark), Saint-Gobain SA (France), BASF SE (Germany), Dow Inc. (US), Johns Manville Corporation (US), GAF Materials Corporation (US), CNBM Group Co., Ltd. (China), and Aspen Aerogels, Inc. (US).

Research Coverage

This report segments the market for building thermal insulation on the basis of material, application, building type, and region, and provides estimations for the overall value (USD Million) of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products & services, key strategies, new product launches, expansions, and mergers & acquisition associated with the market for building thermal insulation.

Reasons to buy this report

This research report is focused on various levels of analysis - industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view on the competitive landscape; emerging and high-growth segments of the building thermal insulation market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of key drivers (Stringent regulations to reduce green house gas emissions, Development of green buildings, Reduction in energy consumption and related cost, Rebates and tax credits, Stringent building energy codes), restraints (Fluctuation in prices of plastic foams, Availability of green insulation material), opportunities (High energy requirements), and challenges (Lack of awareness on building thermal insulation)

- Market Penetration: Comprehensive information on building thermal insulation offered by top players in the global building thermal insulation market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the building thermal insulation

- Market Development: Comprehensive information about lucrative emerging markets - the report analyzes the markets for building thermal insulation across regions

- Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global building thermal insulation market

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the building thermal insulation market

- Impact of recession on building thermal insulation

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 BUILDING THERMAL INSULATION MARKET: INCLUSIONS AND EXCLUSIONS

- 1.2.2 BUILDING THERMAL INSULATION MARKET: DEFINITION AND INCLUSIONS, BY MATERIAL

- 1.2.3 BUILDING THERMAL INSULATION MARKET: DEFINITION AND INCLUSIONS, BY APPLICATION

- 1.2.4 BUILDING THERMAL INSULATION MARKET: DEFINITION AND INCLUSIONS, BY BUILDING TYPE

- 1.3 MARKET SCOPE

- 1.3.1 BUILDING THERMAL INSULATION MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

- 1.7.1 IMPACT OF RECESSION

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 BUILDING THERMAL INSULATION MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Interviews with experts-demand and supply sides

- 2.1.2.2 Key industry insights

- 2.1.2.3 Breakdown of primary interviews

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- FIGURE 2 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 1 (SUPPLY SIDE)-COLLECTIVE SHARE OF KEY PLAYERS

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 2 (SUPPLY SIDE)-COLLECTIVE REVENUE OF ALL PRODUCTS

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 3 (DEMAND SIDE)-PRODUCTS SOLD

- 2.2.2 TOP-DOWN APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 4 (TOP-DOWN)

- 2.3 DATA TRIANGULATION

- FIGURE 6 BUILDING THERMAL INSULATION MARKET: DATA TRIANGULATION

- 2.4 GROWTH FORECAST

- 2.4.1 SUPPLY-SIDE ANALYSIS

- FIGURE 7 MARKET GROWTH PROJECTION FROM SUPPLY SIDE

- 2.4.2 DEMAND-SIDE ANALYSIS

- FIGURE 8 MARKET GROWTH PROJECTION FROM DEMAND-SIDE DRIVERS AND OPPORTUNITIES

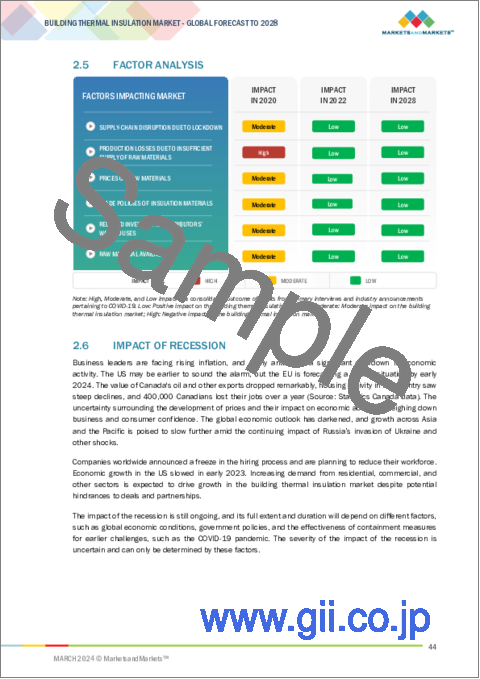

- 2.5 FACTOR ANALYSIS

- 2.6 IMPACT OF RECESSION

- 2.7 ASSUMPTIONS

- 2.8 LIMITATIONS

- 2.9 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- FIGURE 9 PLASTIC FOAM ACCOUNTED FOR LARGEST MARKET SHARE IN 2022

- FIGURE 10 WALL INSULATION TO LEAD BUILDING THERMAL INSULATION MARKET DURING FORECAST PERIOD

- FIGURE 11 RESIDENTIAL SEGMENT TO LEAD BUILDING THERMAL INSULATION MARKET DURING FORECAST PERIOD

- FIGURE 12 ASIA PACIFIC TO WITNESS HIGHEST CAGR DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN BUILDING THERMAL INSULATION MARKET

- FIGURE 13 NON-RESIDENTIAL SEGMENT TO DRIVE MARKET DURING FORECAST PERIOD

- 4.2 BUILDING THERMAL INSULATION MARKET, BY REGION

- FIGURE 14 ASIA PACIFIC TO WITNESS FASTEST GROWTH DURING FORECAST PERIOD

- 4.3 EUROPE BUILDING THERMAL INSULATION MARKET, BY COUNTRY AND MATERIAL

- FIGURE 15 GERMANY ACCOUNTED FOR LARGEST MARKET SHARE IN 2022

- 4.4 BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE AND REGION

- FIGURE 16 RESIDENTIAL SEGMENT ACCOUNTED FOR LARGER MARKET SHARE IN MOST REGIONS

- 4.5 BUILDING THERMAL INSULATION MARKET, BY KEY COUNTRIES

- FIGURE 17 UAE TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 18 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN BUILDING THERMAL INSULATION MARKET

- 5.2.1 DRIVERS

- 5.2.1.1 Stringent regulations to reduce greenhouse gas emissions

- TABLE 1 REGION-WISE REGULATIONS TO REDUCE GREENHOUSE GAS EMISSIONS

- 5.2.1.2 Development of green buildings

- TABLE 2 LEED GREEN BUILDING CERTIFICATIONS, BY COUNTRY (2022)

- 5.2.1.3 Reduction in energy consumption and related costs

- 5.2.1.4 Rebates and tax credits

- 5.2.1.5 Stringent building energy codes

- 5.2.2 RESTRAINTS

- 5.2.2.1 Fluctuation in prices of plastic foam

- 5.2.2.2 Availability of green insulation materials

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 High energy requirements

- 5.2.4 CHALLENGES

- 5.2.4.1 Lack of awareness about building thermal insulation

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 19 BUILDING THERMAL INSULATION MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 THREAT OF NEW ENTRANTS

- 5.3.2 THREAT OF SUBSTITUTES

- 5.3.3 BARGAINING POWER OF SUPPLIERS

- 5.3.4 BARGAINING POWER OF BUYERS

- 5.3.5 INTENSITY OF COMPETITIVE RIVALRY

- TABLE 3 BUILDING THERMAL INSULATION MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.4 MACROECONOMIC INDICATORS

- 5.4.1 GDP TRENDS AND FORECASTS OF MAJOR ECONOMIES

- TABLE 4 GDP TRENDS AND FORECAST, BY MAJOR ECONOMIES, 2020-2028 (USD BILLION)

6 INDUSTRY TRENDS

- 6.1 SUPPLY CHAIN ANALYSIS

- FIGURE 20 BUILDING THERMAL INSULATION: SUPPLY CHAIN

- 6.1.1 RAW MATERIALS

- 6.1.2 MANUFACTURING

- 6.1.3 DISTRIBUTION NETWORK

- 6.1.4 APPLICATION

- 6.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 21 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS IN TOP THREE APPLICATIONS

- TABLE 5 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS IN TOP THREE APPLICATIONS (%)

- 6.2.2 BUYING CRITERIA

- FIGURE 22 KEY BUYING CRITERIA FOR TOP THREE APPLICATIONS

- TABLE 6 KEY BUYING CRITERIA FOR TOP THREE APPLICATIONS

- 6.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 23 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.4 ECOSYSTEM ANALYSIS

- FIGURE 24 ECOSYSTEM OF BUILDING THERMAL INSULATION MARKET

- TABLE 7 BUILDING THERMAL INSULATION MARKET: ROLE IN ECOSYSTEM

- 6.5 CASE STUDIES

- 6.5.1 ENHANCING COMMUNITY WELL-BEING: WILMCOTE HOUSE'S THERMAL EFFICIENCY UPGRADE

- 6.6 TECHNOLOGY ANALYSIS

- 6.6.1 KEY TECHNOLOGIES

- 6.6.1.1 XPS foam technology

- TABLE 8 ADVANTAGES OF XPS FOAM TECHNOLOGY

- 6.6.1.2 ECOSE technology

- TABLE 9 BENEFITS OF ECOSE TECHNOLOGY

- 6.6.2 COMPLEMENTARY TECHNOLOGIES

- 6.6.2.1 Air sealing

- 6.6.2.2 Reflective roofing materials

- 6.6.1 KEY TECHNOLOGIES

- 6.7 PRICING ANALYSIS

- 6.7.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY APPLICATION

- FIGURE 25 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY APPLICATION

- TABLE 10 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY APPLICATION (USD/KG)

- 6.7.2 AVERAGE SELLING PRICE TREND, BY REGION

- FIGURE 26 AVERAGE SELLING PRICE TREND OF BUILDING THERMAL INSULATION, BY REGION (USD/KG)

- TABLE 11 AVERAGE SELLING PRICE TREND OF BUILDING THERMAL INSULATION, BY REGION (USD/KG)

- 6.8 TRADE ANALYSIS

- 6.8.1 IMPORT SCENARIO OF BUILDING THERMAL INSULATION

- FIGURE 27 IMPORT OF BUILDING THERMAL INSULATION, BY KEY COUNTRIES (2017-2022)

- TABLE 12 IMPORT OF BUILDING THERMAL INSULATION, BY REGION, 2017-2022 (USD MILLION)

- 6.8.2 EXPORT SCENARIO OF BUILDING THERMAL INSULATION

- FIGURE 28 EXPORT OF BUILDING THERMAL INSULATION, BY KEY COUNTRIES (2017-2022)

- TABLE 13 EXPORT OF BUILDING THERMAL INSULATION, BY REGION, 2017-2022 (USD MILLION)

- 6.9 REGULATORY LANDSCAPE

- TABLE 14 NORTH AMERICA: REGULATIONS FOR BUILDING THERMAL INSULATION

- TABLE 15 EUROPE: REGULATIONS FOR BUILDING THERMAL INSULATION

- TABLE 16 ASIA PACIFIC: REGULATIONS FOR BUILDING THERMAL INSULATION

- 6.9.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.10 KEY CONFERENCES AND EVENTS IN 2024-2025

- TABLE 17 BUILDING THERMAL INSULATION MARKET: KEY CONFERENCES AND EVENTS

- 6.11 INVESTMENT AND FUNDING SCENARIO

- 6.12 PATENT ANALYSIS

- 6.12.1 APPROACH

- 6.12.2 DOCUMENT TYPE

- TABLE 18 PATENT STATUS: PATENT APPLICATIONS, LIMITED PATENTS, AND GRANTED PATENTS

- FIGURE 29 PATENTS REGISTERED IN BUILDING THERMAL INSULATION, 2012-2023

- FIGURE 30 LIST OF MAJOR PATENTS FOR BUILDING THERMAL INSULATION

- 6.12.3 TOP APPLICANTS

- TABLE 19 LIST OF MAJOR PATENTS OF BUILDING THERMAL INSULATION

- TABLE 20 PATENTS BY INEOS STATE GRID CORPORATION OF CHINA

- TABLE 21 PATENTS BY BASF SE

- TABLE 22 PATENTS BY SAMSUNG ELECTRONICS CO., LTD.

- TABLE 23 TOP 10 PATENT OWNERS IN CHINA, 2012-2023

- FIGURE 31 LEGAL STATUS OF PATENTS FILED IN BUILDING THERMAL INSULATION MARKET

- 6.12.4 JURISDICTION ANALYSIS

- FIGURE 32 MAXIMUM PATENTS FILED IN JURISDICTION OF CHINA

7 BUILDING THERMAL INSULATION MARKET, BY MATERIAL

- 7.1 INTRODUCTION

- TABLE 24 MATERIALS AND THEIR APPLICATIONS

- TABLE 25 OPERATIONAL TEMPERATURE RANGES OF DIFFERENT MATERIALS

- TABLE 26 R-VALUE OF DIFFERENT MATERIALS

- FIGURE 33 PLASTIC FOAM TO ACCOUNT FOR LARGEST SHARE OF BUILDING THERMAL INSULATION MARKET

- TABLE 27 BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 28 BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 29 BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 30 BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 7.2 PLASTIC FOAM

- 7.2.1 GROWTH IN BUILDING & CONSTRUCTION INDUSTRY TO INCREASED DEMAND FOR PLASTIC FOAM

- FIGURE 34 ASIA PACIFIC TO BE LARGEST MARKET FOR PLASTIC FOAM SEGMENT DURING FORECAST PERIOD

- TABLE 31 PLASTIC FOAM: BUILDING THERMAL INSULATION MARKET, BY REGION, 2017-2022 (USD MILLION)

- TABLE 32 PLASTIC FOAM: BUILDING THERMAL INSULATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 33 PLASTIC FOAM: BUILDING THERMAL INSULATION MARKET, BY REGION, 2017-2022 (KILOTON)

- TABLE 34 PLASTIC FOAM: BUILDING THERMAL INSULATION MARKET, BY REGION, 2023-2028 (KILOTON)

- TABLE 35 PLASTIC FOAM: BUILDING THERMAL INSULATION MARKET, BY SUB-TYPE, 2017-2022 (USD MILLION)

- TABLE 36 PLASTIC FOAM: BUILDING THERMAL INSULATION MARKET, BY SUB-TYPE, 2023-2028 (USD MILLION)

- TABLE 37 PLASTIC FOAM: BUILDING THERMAL INSULATION MARKET, BY SUB-TYPE, 2017-2022 (KILOTON)

- TABLE 38 PLASTIC FOAM: BUILDING THERMAL INSULATION MARKET, BY SUB-TYPE, 2023-2028 (KILOTON)

- 7.2.2 POLYSTYRENE FOAM

- 7.2.2.1 Expanded polystyrene (EPS) foam

- 7.2.2.2 Extruded polystyrene (XPS) foam

- TABLE 39 POLYSTYRENE FOAM: BUILDING THERMAL INSULATION MARKET, BY REGION, 2017-2022 (USD MILLION)

- TABLE 40 POLYSTYRENE FOAM: BUILDING THERMAL INSULATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 41 POLYSTYRENE FOAM: BUILDING THERMAL INSULATION MARKET, BY REGION, 2017-2022 (KILOTON)

- TABLE 42 POLYSTYRENE FOAM: BUILDING THERMAL INSULATION MARKET, BY REGION, 2023-2028 (KILOTON)

- 7.2.3 POLYURETHANE (PUR) & POLYISOCYANURATE (PIR) FOAM

- TABLE 43 PUR & PIR FOAM: BUILDING THERMAL INSULATION MARKET, BY REGION, 2017-2022 (USD MILLION)

- TABLE 44 PUR & PIR FOAM: BUILDING THERMAL INSULATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 45 PUR & PIR FOAM: BUILDING THERMAL INSULATION MARKET, BY REGION, 2017-2022 (KILOTON)

- TABLE 46 PUR & PIR FOAM: BUILDING THERMAL INSULATION MARKET, BY REGION, 2023-2028 (KILOTON)

- 7.2.4 OTHER PLASTIC FOAMS

- 7.2.4.1 Phenolic foam

- 7.2.4.2 Elastomeric foam

- TABLE 47 OTHER PLASTIC FOAMS: BUILDING THERMAL INSULATION MARKET, BY REGION, 2017-2022 (USD MILLION)

- TABLE 48 OTHER PLASTIC FOAMS: BUILDING THERMAL INSULATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 49 OTHER PLASTIC FOAMS: BUILDING THERMAL INSULATION MARKET, BY REGION, 2017-2022 (KILOTON)

- TABLE 50 OTHER PLASTIC FOAMS: BUILDING THERMAL INSULATION MARKET, BY REGION, 2023-2028 (KILOTON)

- 7.3 GLASS WOOL

- 7.3.1 LIGHTWEIGHT, NON-COMBUSTIBLE, HIGH TEAR STRENGTH, AND CORROSION-RESISTANT PROPERTIES TO DRIVE DEMAND

- FIGURE 35 NORTH AMERICA TO LEAD GLASS WOOL SEGMENT DURING FORECAST PERIOD

- TABLE 51 GLASS WOOL: BUILDING THERMAL INSULATION MARKET, BY REGION, 2017-2022 (USD MILLION)

- TABLE 52 GLASS WOOL: BUILDING THERMAL INSULATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 53 GLASS WOOL: BUILDING THERMAL INSULATION MARKET, BY REGION, 2017-2022 (KILOTON)

- TABLE 54 GLASS WOOL: BUILDING THERMAL INSULATION MARKET, BY REGION, 2023-2028 (KILOTON)

- 7.4 STONE WOOL

- 7.4.1 GROWTH OF CONSTRUCTION & ARCHITECTURAL SECTORS FUELING MARKET GROWTH

- FIGURE 36 EUROPE TO LEAD STONE WOOL SEGMENT DURING FORECAST PERIOD

- TABLE 55 STONE WOOL: BUILDING THERMAL INSULATION MARKET, BY REGION, 2017-2022 (USD MILLION)

- TABLE 56 STONE WOOL: BUILDING THERMAL INSULATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 57 STONE WOOL: BUILDING THERMAL INSULATION MARKET, BY REGION, 2017-2022 (KILOTON)

- TABLE 58 STONE WOOL: BUILDING THERMAL INSULATION MARKET, BY REGION, 2023-2028 (KILOTON)

- 7.5 OTHER MATERIALS

- 7.5.1 AEROGEL

- 7.5.2 CELLULOSE

- 7.5.3 CELLULAR GLASS

- FIGURE 37 EUROPE TO LEAD OTHER MATERIALS SEGMENT DURING FORECAST PERIOD

- TABLE 59 OTHER MATERIALS: BUILDING THERMAL INSULATION MARKET, BY REGION, 2017-2022 (USD MILLION)

- TABLE 60 OTHER MATERIALS: BUILDING THERMAL INSULATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 61 OTHER MATERIALS: BUILDING THERMAL INSULATION MARKET, BY REGION, 2017-2022 (KILOTON)

- TABLE 62 OTHER MATERIALS: BUILDING THERMAL INSULATION MARKET, BY REGION, 2023-2028 (KILOTON)

8 BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE

- 8.1 INTRODUCTION

- FIGURE 38 RESIDENTIAL SEGMENT TO ACCOUNT FOR LARGER SHARE OF BUILDING THERMAL INSULATION MARKET DURING FORECAST PERIOD

- TABLE 63 BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2017-2022 (USD MILLION)

- TABLE 64 BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2023-2028 (USD MILLION)

- TABLE 65 BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2017-2022 (KILOTON)

- TABLE 66 BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2023-2028 (KILOTON)

- 8.2 NON-RESIDENTIAL BUILDING

- 8.2.1 ROBUST MANUFACTURING AND INCREASE IN INDUSTRIAL ACTIVITIES TO DRIVE MARKET

- 8.2.2 INDUSTRIAL BUILDINGS

- 8.2.3 COMMERCIAL BUILDINGS

- 8.2.4 OTHERS

- FIGURE 39 ASIA PACIFIC TO WITNESS HIGHEST CAGR IN NON-RESIDENTIAL BUILDING SEGMENT DURING FORECAST PERIOD

- TABLE 67 BUILDING THERMAL INSULATION MARKET IN NON-RESIDENTIAL BUILDING, BY REGION, 2017-2022 (USD MILLION)

- TABLE 68 BUILDING THERMAL INSULATION MARKET IN NON-RESIDENTIAL BUILDING, BY REGION, 2023-2028 (USD MILLION)

- TABLE 69 BUILDING THERMAL INSULATION MARKET IN NON-RESIDENTIAL BUILDING, BY REGION, 2017-2022 (KILOTON)

- TABLE 70 BUILDING THERMAL INSULATION MARKET IN NON-RESIDENTIAL BUILDING, BY REGION, 2023-2028 (KILOTON)

- 8.3 RESIDENTIAL BUILDING

- 8.3.1 URBANIZATION AND GOVERNMENT REGULATIONS ON ENERGY-EFFICIENT BUILDINGS TO FUEL DEMAND

- FIGURE 40 EUROPE TO LEAD MARKET IN RESIDENTIAL SEGMENT DURING FORECAST PERIOD

- TABLE 71 BUILDING THERMAL INSULATION MARKET IN RESIDENTIAL BUILDING, BY REGION, 2017-2022 (USD MILLION)

- TABLE 72 BUILDING THERMAL INSULATION MARKET IN RESIDENTIAL BUILDING, BY REGION, 2023-2028 (USD MILLION)

- TABLE 73 BUILDING THERMAL INSULATION MARKET IN RESIDENTIAL BUILDING, BY REGION, 2017-2022 (KILOTON)

- TABLE 74 BUILDING THERMAL INSULATION MARKET IN RESIDENTIAL BUILDING, BY REGION, 2023-2028 (KILOTON)

9 BUILDING THERMAL INSULATION MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- FIGURE 41 PERCENTAGE OF ENERGY LOSS IN BUILDINGS

- FIGURE 42 ROOF INSULATION TO BE FASTEST-GROWING APPLICATION OF BUILDING THERMAL INSULATION

- TABLE 75 BUILDING THERMAL INSULATION MARKET, BY APPLICATION, 2017-2022 (USD MILLION)

- TABLE 76 BUILDING THERMAL INSULATION MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 77 BUILDING THERMAL INSULATION MARKET, BY APPLICATION, 2017-2022 (KILOTON)

- TABLE 78 BUILDING THERMAL INSULATION MARKET, BY APPLICATION, 2023-2028 (KILOTON)

- 9.2 WALL INSULATION

- 9.2.1 EXTERNAL WALLS TO DOMINATE MARKET IN WALL INSULATION SEGMENT

- FIGURE 43 EXTERNAL WALL TO ACCOUNT FOR LARGEST SHARE IN WALL INSULATION APPLICATION DURING FORECAST PERIOD

- 9.2.2 EXTERNAL WALL INSULATION

- 9.2.3 INTERNAL WALL INSULATION

- 9.2.4 CAVITY WALL INSULATION

- TABLE 79 BUILDING THERMAL INSULATION MARKET IN WALL INSULATION, BY SUB-APPLICATION, 2017-2022 (USD MILLION)

- TABLE 80 BUILDING THERMAL INSULATION MARKET IN WALL INSULATION, BY SUB-APPLICATION, 2023-2028 (USD MILLION)

- TABLE 81 BUILDING THERMAL INSULATION MARKET IN WALL INSULATION, BY SUB-APPLICATION, 2017-2022 (KILOTON)

- TABLE 82 BUILDING THERMAL INSULATION MARKET IN WALL INSULATION, BY SUB-APPLICATION, 2023-2028 (KILOTON)

- 9.3 ROOF INSULATION

- 9.3.1 INCREASE IN CONSTRUCTION ACTIVITIES TO DRIVE MARKET

- FIGURE 44 FLAT ROOF TO ACCOUNT FOR LARGER SHARE IN ROOF INSULATION APPLICATION DURING FORECAST PERIOD

- 9.3.2 FLAT ROOF INSULATION

- 9.3.3 PITCHED ROOF INSULATION

- TABLE 83 BUILDING THERMAL INSULATION MARKET IN ROOF INSULATION, BY SUB-APPLICATION, 2017-2022 (USD MILLION)

- TABLE 84 BUILDING THERMAL INSULATION MARKET IN ROOF INSULATION, BY SUB-APPLICATION, 2023-2028 (USD MILLION)

- TABLE 85 BUILDING THERMAL INSULATION MARKET IN ROOF INSULATION, BY SUB-APPLICATION, 2017-2022 (KILOTON)

- TABLE 86 BUILDING THERMAL INSULATION MARKET IN ROOF INSULATION, BY SUB-APPLICATION, 2023-2028 (KILOTON)

- 9.4 FLOOR INSULATION

- 9.4.1 HIGH QUALITY AND TECHNOLOGICAL ADVANCEMENTS DRIVING DEMAND

10 BUILDING THERMAL INSULATION MARKET, BY REGION

- 10.1 INTRODUCTION

- FIGURE 45 ASIA PACIFIC TO BE FASTEST-GROWING BUILDING THERMAL INSULATION MARKET BETWEEN 2023 AND 2028

- TABLE 87 BUILDING THERMAL INSULATION MARKET, BY REGION, 2017-2022 (USD MILLION)

- TABLE 88 BUILDING THERMAL INSULATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 89 BUILDING THERMAL INSULATION MARKET, BY REGION, 2017-2022 (KILOTON)

- TABLE 90 BUILDING THERMAL INSULATION MARKET, BY REGION, 2023-2028 (KILOTON)

- 10.2 EUROPE

- FIGURE 46 EUROPE: BUILDING THERMAL INSULATION MARKET SNAPSHOT

- 10.2.1 IMPACT OF RECESSION ON EUROPE

- 10.2.2 EUROPE BUILDING THERMAL INSULATION MARKET, BY MATERIAL

- TABLE 91 EUROPE: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 92 EUROPE: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 93 EUROPE: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 94 EUROPE: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.2.3 EUROPE BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE

- TABLE 95 EUROPE: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2017-2022 (USD MILLION)

- TABLE 96 EUROPE: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2023-2028 (USD MILLION)

- TABLE 97 EUROPE: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2017-2022 (KILOTON)

- TABLE 98 EUROPE: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2023-2028 (KILOTON)

- 10.2.4 EUROPE BUILDING THERMAL INSULATION MARKET, BY COUNTRY

- TABLE 99 EUROPE: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2017-2022 (USD MILLION)

- TABLE 100 EUROPE: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 101 EUROPE: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2017-2022 (KILOTON)

- TABLE 102 EUROPE: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- 10.2.4.1 Germany

- 10.2.4.1.1 Investments in residential segment and green building labeling systems to drive market

- 10.2.4.1 Germany

- TABLE 103 GERMANY: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 104 GERMANY: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 105 GERMANY: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 106 GERMANY: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.2.4.2 France

- 10.2.4.2.1 Government regulations and presence of established companies to support market growth

- 10.2.4.2 France

- TABLE 107 FRANCE: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 108 FRANCE: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 109 FRANCE: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 110 FRANCE: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.2.4.3 Poland

- 10.2.4.3.1 Stringent building codes and increasing construction activities to drive demand

- 10.2.4.3 Poland

- TABLE 111 POLAND: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 112 POLAND: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 113 POLAND: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 114 POLAND: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.2.4.4 UK

- 10.2.4.4.1 Green building council and investments in construction to fuel demand

- 10.2.4.4 UK

- TABLE 115 UK: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 116 UK: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 117 UK: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 118 UK: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.2.4.5 Italy

- 10.2.4.5.1 New project finance rules and investment policies to support market growth

- 10.2.4.5 Italy

- TABLE 119 ITALY: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 120 ITALY: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 121 ITALY: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 122 ITALY: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.2.4.6 Russia

- 10.2.4.6.1 Glass wool to be fastest-growing segment during forecast period

- 10.2.4.6 Russia

- TABLE 123 RUSSIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 124 RUSSIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 125 RUSSIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 126 RUSSIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.2.4.7 Spain

- 10.2.4.7.1 Strict building codes and increased consumer spending to drive demand

- 10.2.4.7 Spain

- TABLE 127 SPAIN: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 128 SPAIN: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 129 SPAIN: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 130 SPAIN: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.3 ASIA PACIFIC

- FIGURE 47 ASIA PACIFIC: BUILDING THERMAL INSULATION MARKET SNAPSHOT

- 10.3.1 IMPACT OF RECESSION ON ASIA PACIFIC

- 10.3.2 ASIA PACIFIC BUILDING THERMAL INSULATION MARKET, BY MATERIAL

- TABLE 131 ASIA PACIFIC: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 132 ASIA PACIFIC: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 133 ASIA PACIFIC: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 134 ASIA PACIFIC: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.3.3 ASIA PACIFIC BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE

- TABLE 135 ASIA PACIFIC: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2017-2022 (USD MILLION)

- TABLE 136 ASIA PACIFIC: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2023-2028 (USD MILLION)

- TABLE 137 ASIA PACIFIC: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2017-2022 (KILOTON)

- TABLE 138 ASIA PACIFIC: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2023-2028 (KILOTON)

- 10.3.4 ASIA PACIFIC BUILDING THERMAL INSULATION MARKET, BY COUNTRY

- TABLE 139 ASIA PACIFIC: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2017-2022 (USD MILLION)

- TABLE 140 ASIA PACIFIC: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 141 ASIA PACIFIC: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2017-2022 (KILOTON)

- TABLE 142 ASIA PACIFIC: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- 10.3.4.1 China

- 10.3.4.1.1 Mandatory building energy codes for commercial and residential buildings to drive demand

- 10.3.4.1 China

- TABLE 143 CHINA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 144 CHINA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 145 CHINA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 146 CHINA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.3.4.2 Japan

- 10.3.4.2.1 Plastic foam to dominate market during forecast period

- 10.3.4.2 Japan

- TABLE 147 JAPAN: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 148 JAPAN: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 149 JAPAN: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 150 JAPAN: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.3.4.3 India

- 10.3.4.3.1 Economic growth and government initiatives to support market growth

- 10.3.4.3 India

- TABLE 151 INDIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 152 INDIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 153 INDIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 154 INDIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.3.4.4 South Korea

- 10.3.4.4.1 Green building certification rating and certification systems to support market growth

- 10.3.4.4 South Korea

- TABLE 155 SOUTH KOREA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 156 SOUTH KOREA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 157 SOUTH KOREA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 158 SOUTH KOREA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.3.4.5 Thailand

- 10.3.4.5.1 Growth in tourism sector fueling demand

- 10.3.4.5 Thailand

- TABLE 159 THAILAND: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 160 THAILAND: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 161 THAILAND: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 162 THAILAND: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.3.4.6 Malaysia

- 10.3.4.6.1 Government's approach to green features in buildings to support market

- 10.3.4.6 Malaysia

- TABLE 163 MALAYSIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 164 MALAYSIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 165 MALAYSIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 166 MALAYSIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.3.4.7 Indonesia

- 10.3.4.7.1 Implementation of building energy codes to drive market

- 10.3.4.7 Indonesia

- TABLE 167 INDONESIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 168 INDONESIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 169 INDONESIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 170 INDONESIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.4 NORTH AMERICA

- FIGURE 48 NORTH AMERICA: BUILDING THERMAL INSULATION MARKET SNAPSHOT

- 10.4.1 IMPACT OF RECESSION ON NORTH AMERICA

- 10.4.2 NORTH AMERICA BUILDING THERMAL INSULATION MARKET, BY MATERIAL

- TABLE 171 NORTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 172 NORTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 173 NORTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 174 NORTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.4.3 NORTH AMERICA BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE

- TABLE 175 NORTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2017-2022 (USD MILLION)

- TABLE 176 NORTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2023-2028 (USD MILLION)

- TABLE 177 NORTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2017-2022 (KILOTON)

- TABLE 178 NORTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2023-2028 (KILOTON)

- 10.4.4 NORTH AMERICA BUILDING THERMAL INSULATION MARKET, BY COUNTRY

- TABLE 179 NORTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2017-2022 (USD MILLION)

- TABLE 180 NORTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 181 NORTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2017-2022 (KILOTON)

- TABLE 182 NORTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- 10.4.4.1 US

- 10.4.4.1.1 Increased private construction and energy-efficient codes to fuel demand

- 10.4.4.1 US

- TABLE 183 US: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 184 US: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 185 US: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 186 US: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.4.4.2 Canada

- 10.4.4.2.1 Growing commercial and residential constructions to drive demand

- 10.4.4.2 Canada

- TABLE 187 CANADA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 188 CANADA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 189 CANADA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 190 CANADA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.4.4.3 Mexico

- 10.4.4.3.1 Stone wool to be fastest-growing segment during forecast period

- 10.4.4.3 Mexico

- TABLE 191 MEXICO: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 192 MEXICO: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 193 MEXICO: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 194 MEXICO: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.5 MIDDLE EAST & AFRICA

- 10.5.1 IMPACT OF RECESSION ON MIDDLE EAST & AFRICA

- 10.5.2 MIDDLE EAST & AFRICA BUILDING THERMAL INSULATION MARKET, BY MATERIAL

- TABLE 195 MIDDLE EAST & AFRICA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 196 MIDDLE EAST & AFRICA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 197 MIDDLE EAST & AFRICA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 198 MIDDLE EAST & AFRICA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.5.3 MIDDLE EAST & AFRICA BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE

- TABLE 199 MIDDLE EAST & AFRICA: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2017-2022 (USD MILLION)

- TABLE 200 MIDDLE EAST & AFRICA: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2023-2028 (USD MILLION)

- TABLE 201 MIDDLE EAST & AFRICA: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2017-2022 (KILOTON)

- TABLE 202 MIDDLE EAST & AFRICA: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2023-2028 (KILOTON)

- 10.5.4 MIDDLE EAST & AFRICA BUILDING THERMAL INSULATION MARKET, BY COUNTRY

- TABLE 203 MIDDLE EAST & AFRICA: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2017-2022 (USD MILLION)

- TABLE 204 MIDDLE EAST & AFRICA: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 205 MIDDLE EAST & AFRICA: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2017-2022 (KILOTON)

- TABLE 206 MIDDLE EAST & AFRICA: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- 10.5.4.1 GCC

- 10.5.4.1.1 Saudi Arabia

- 10.5.4.1.1.1 Energy efficiency programs and increased government spending to drive market

- 10.5.4.1.1 Saudi Arabia

- 10.5.4.1 GCC

- TABLE 207 SAUDI ARABIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 208 SAUDI ARABIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 209 SAUDI ARABIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 210 SAUDI ARABIA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.5.4.1.2 UAE

- 10.5.4.1.2.1 Implementation of mandatory building codes to fuel demand

- 10.5.4.1.2 UAE

- TABLE 211 UAE: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 212 UAE: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 213 UAE: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 214 UAE: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.5.4.1.3 Qatar

- 10.5.4.1.3.1 High infrastructure and general construction spending to fuel demand

- 10.5.4.1.3 Qatar

- TABLE 215 QATAR: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 216 QATAR: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 217 QATAR: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 218 QATAR: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.5.4.2 South Africa

- 10.5.4.2.1 Stringent regulations to drive demand

- 10.5.4.2 South Africa

- TABLE 219 SOUTH AFRICA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 220 SOUTH AFRICA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 221 SOUTH AFRICA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 222 SOUTH AFRICA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.6 SOUTH AMERICA

- 10.6.1 IMPACT OF RECESSION ON SOUTH AMERICA

- 10.6.2 SOUTH AMERICA BUILDING THERMAL INSULATION MARKET, BY MATERIAL

- TABLE 223 SOUTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 224 SOUTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 225 SOUTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 226 SOUTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.6.3 SOUTH AMERICA BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE

- TABLE 227 SOUTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2017-2022 (USD MILLION)

- TABLE 228 SOUTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2023-2028 (USD MILLION)

- TABLE 229 SOUTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2017-2022 (KILOTON)

- TABLE 230 SOUTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY BUILDING TYPE, 2023-2028 (KILOTON)

- 10.6.4 SOUTH AMERICA BUILDING THERMAL INSULATION MARKET, BY COUNTRY

- TABLE 231 SOUTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2017-2022 (USD MILLION)

- TABLE 232 SOUTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 233 SOUTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2017-2022 (KILOTON)

- TABLE 234 SOUTH AMERICA: BUILDING THERMAL INSULATION MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- 10.6.4.1 Brazil

- 10.6.4.1.1 Energy efficiency labeling systems to fuel demand for building thermal insulation

- 10.6.4.1 Brazil

- TABLE 235 BRAZIL: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 236 BRAZIL: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 237 BRAZIL: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 238 BRAZIL: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

- 10.6.4.2 Argentina

- 10.6.4.2.1 Standards regarding building envelope design and heating efficiency on building rules to drive market

- 10.6.4.2 Argentina

- TABLE 239 ARGENTINA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (USD MILLION)

- TABLE 240 ARGENTINA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (USD MILLION)

- TABLE 241 ARGENTINA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2017-2022 (KILOTON)

- TABLE 242 ARGENTINA: BUILDING THERMAL INSULATION MARKET, BY MATERIAL, 2023-2028 (KILOTON)

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 KEY PLAYER STRATEGIES

- TABLE 243 OVERVIEW OF STRATEGIES ADOPTED BY MAJOR COMPANIES

- 11.3 MARKET SHARE ANALYSIS

- TABLE 244 DEGREE OF COMPETITION

- FIGURE 49 BUILDING THERMAL INSULATION: MARKET SHARE ANALYSIS, 2023

- 11.3.1 RANKING OF KEY MARKET PLAYERS

- FIGURE 50 RANKING OF KEY PLAYERS IN BUILDING THERMAL INSULATION MARKET, 2023

- 11.4 REVENUE ANALYSIS

- FIGURE 51 REVENUE ANALYSIS OF KEY COMPANIES (2018-2023)

- 11.5 COMPANY VALUATION AND FINANCIAL METRICS

- FIGURE 52 VALUATION OF KEY COMPANIES

- FIGURE 53 ENTERPRISE VALUE/EBITDA OF KEY COMPANIES

- 11.6 BRAND/PRODUCT COMPARISON

- 11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- FIGURE 54 BUILDING THERMAL INSULATION MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

- 11.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023

- 11.7.5.1 Company footprint

- FIGURE 55 COMPANY OVERALL FOOTPRINT (25 COMPANIES)

- 11.7.5.2 Region footprint

- TABLE 245 COMPANY REGION FOOTPRINT (25 COMPANIES)

- 11.7.5.3 Material footprint

- TABLE 246 COMPANY MATERIAL FOOTPRINT (25 COMPANIES)

- 11.7.5.4 Application footprint

- TABLE 247 COMPANY APPLICATION FOOTPRINT (25 COMPANIES)

- 11.7.5.5 Building type footprint

- TABLE 248 COMPANY BUILDING TYPE FOOTPRINT (25 COMPANIES)

- 11.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES

- 11.8.1 PROGRESSIVE COMPANIES

- 11.8.2 RESPONSIVE COMPANIES

- 11.8.3 DYNAMIC COMPANIES

- 11.8.4 STARTING BLOCKS

- FIGURE 56 BUILDING THERMAL INSULATION MARKET: STARTUP/SMES EVALUATION MATRIX, 2023

- 11.8.5 COMPETITIVE BENCHMARKING, STARTUP/SMES, 2023

- 11.8.5.1 Building thermal insulation market: Key startups/SMEs

- TABLE 249 BUILDING THERMAL INSULATION MARKET: KEY STARTUPS/SMES

- 11.8.5.2 Building thermal insulation market: competitive benchmarking of key startups/SMEs

- TABLE 250 BUILDING THERMAL INSULATION MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 11.9 COMPETITIVE SCENARIO AND TRENDS

- 11.9.1 PRODUCT LAUNCHES

- TABLE 251 BUILDING THERMAL INSULATION MARKET: PRODUCT LAUNCHES, JANUARY 2018-JANUARY 2023

- 11.9.2 DEALS

- TABLE 252 BUILDING THERMAL INSULATION MARKET: DEALS, JANUARY 2018-JANUARY 2023

- 11.9.3 EXPANSIONS

- TABLE 253 BUILDING THERMAL INSULATION MARKET: EXPANSIONS, JANUARY 2018-JANUARY 2023

12 COMPANY PROFILES

- (Business overview, Products offered, Recent developments & MnM View)**

- 12.1 KEY PLAYERS

- 12.1.1 KINGSPAN GROUP PLC

- TABLE 254 KINGSPAN GROUP PLC: COMPANY OVERVIEW

- FIGURE 57 KINGSPAN GROUP PLC: COMPANY SNAPSHOT

- TABLE 255 KINGSPAN GROUP PLC: PRODUCTS OFFERED

- TABLE 256 KINGSPAN GROUP PLC: DEALS, JANUARY 2018-JANUARY 2023

- TABLE 257 KINGSPAN GROUP PLC: EXPANSIONS, JANUARY 2018-JANUARY 2023

- 12.1.2 KNAUF GIPS KG

- TABLE 258 KNAUF GIPS KG: COMPANY OVERVIEW

- TABLE 259 KNAUF GIPS KG: PRODUCTS OFFERED

- TABLE 260 KNAUF GIPS KG: EXPANSIONS, JANUARY 2018-JANUARY 2023

- 12.1.3 OWENS CORNING

- TABLE 261 OWENS CORNING: COMPANY OVERVIEW

- FIGURE 58 OWENS CORNING: COMPANY SNAPSHOT

- TABLE 262 OWENS CORNING: PRODUCTS OFFERED

- TABLE 263 OWENS CORNING: EXPANSIONS, JANUARY 2018-JANUARY 2023

- 12.1.4 ROCKWOOL A/S

- TABLE 264 ROCKWOOL A/S: COMPANY OVERVIEW

- FIGURE 59 ROCKWOOL A/S: COMPANY SNAPSHOT

- TABLE 265 ROCKWOOL A/S: PRODUCTS OFFERED

- TABLE 266 ROCKWOOL A/S: DEALS, JANUARY 2018-JANUARY 2023

- TABLE 267 ROCKWOOL A/S: EXPANSIONS, JANUARY 2018-JANUARY 2023

- 12.1.5 SAINT-GOBAIN SA

- TABLE 268 SAINT-GOBAIN SA: COMPANY OVERVIEW

- FIGURE 60 SAINT-GOBAIN SA: COMPANY SNAPSHOT

- TABLE 269 SAINT-GOBAIN SA: PRODUCTS OFFERED

- TABLE 270 SAINT-GOBAIN SA: DEALS, JANUARY 2018-JANUARY 2023

- TABLE 271 SAINT-GOBAIN SA: EXPANSIONS, JANUARY 2018-JANUARY 2023

- 12.1.6 BASF SE

- TABLE 272 BASF SE: COMPANY OVERVIEW

- FIGURE 61 BASF SE: COMPANY SNAPSHOT

- TABLE 273 BASF SE: PRODUCTS OFFERED

- TABLE 274 BASF SE: PRODUCT LAUNCHES, JANUARY 2018-JANUARY 2023

- TABLE 275 BASF SE: DEALS, JANUARY 2018-JANUARY 2023

- TABLE 276 BASF SE: EXPANSIONS, JANUARY 2018-JANUARY 2023

- 12.1.7 DOW INC.

- TABLE 277 DOW INC.: COMPANY OVERVIEW

- FIGURE 62 DOW INC.: COMPANY SNAPSHOT

- TABLE 278 DOW INC.: PRODUCTS OFFERED

- 12.1.8 JOHNS MANVILLE CORPORATION

- TABLE 279 JOHNS MANVILLE CORPORATION: COMPANY OVERVIEW

- TABLE 280 JOHNS MANVILLE CORPORATION: PRODUCTS OFFERED

- 12.1.9 GAF MATERIALS CORPORATION

- TABLE 281 GAF MATERIALS CORPORATION: COMPANY OVERVIEW

- TABLE 282 GAF MATERIALS CORPORATION: PRODUCTS OFFERED

- 12.1.10 CNBM GROUP CO., LTD.

- TABLE 283 CNBM GROUP CO., LTD.: COMPANY OVERVIEW

- FIGURE 63 CNBM GROUP CO., LTD.: COMPANY SNAPSHOT

- TABLE 284 CNBM GROUP CO., LTD.: PRODUCTS OFFERED

- 12.1.11 ASPEN AEROGELS, INC.

- TABLE 285 ASPEN AEROGELS, INC.: COMPANY OVERVIEW

- FIGURE 64 ASPEN AEROGELS, INC.: COMPANY SNAPSHOT

- TABLE 286 ASPEN AEROGELS, INC.: PRODUCTS OFFERED

- TABLE 287 ASPEN AEROGELS, INC.: DEALS, JANUARY 2018-JANUARY 2023

- *Details on Business overview, Products offered, Recent developments & MnM View might not be captured in case of unlisted companies.

- 12.2 OTHER PLAYERS

- 12.2.1 ATLAS ROOFING CORPORATION

- TABLE 288 ATLAS ROOFING CORPORATION: COMPANY OVERVIEW

- 12.2.2 HOLCIM LIMITED

- TABLE 289 HOLCIM LIMITED: COMPANY OVERVIEW

- 12.2.3 HUNTSMAN INTERNATIONAL LLC

- TABLE 290 HUNTSMAN INTERNATIONAL LLC: COMPANY OVERVIEW

- 12.2.4 KCC CORPORATION

- TABLE 291 KCC CORPORATION: COMPANY OVERVIEW

- 12.2.5 LAPOLLA INDUSTRIES, INC.

- TABLE 292 LAPOLLA INDUSTRIES, INC.: COMPANY OVERVIEW

- 12.2.6 NICHIAS CORPORATION

- TABLE 293 NICHIAS CORPORATION: COMPANY OVERVIEW

- 12.2.7 RECTICEL SA

- TABLE 294 RECTICEL SA: COMPANY OVERVIEW

- 12.2.8 ODE INSULATION

- TABLE 295 ODE INSULATION: COMPANY OVERVIEW

- 12.2.9 TROCELLEN GMBH

- TABLE 296 TROCELLEN GMBH: COMPANY OVERVIEW

- 12.2.10 URSA INSULATION SA

- TABLE 297 URSA INSULATION SA: COMPANY OVERVIEW

- 12.2.11 SIKA GROUP

- TABLE 298 SIKA GROUP: COMPANY OVERVIEW

- 12.2.12 CELLOFOAM NORTH AMERICA, INC.

- TABLE 299 CELLOFOAM NORTH AMERICA, INC.: COMPANY OVERVIEW

- 12.2.13 NEO THERMAL INSULATION (INDIA) PVT. LTD.

- TABLE 300 NEO THERMAL INSULATION (INDIA) PVT. LTD.: COMPANY OVERVIEW

- 12.2.14 LLOYD INSULATIONS (INDIA) LIMITED

- TABLE 301 LLOYD INSULATIONS (INDIA) LIMITED: COMPANY OVERVIEW

13 ADJACENT & RELATED MARKETS

- 13.1 INTRODUCTION

- 13.2 LIMITATION

- 13.3 INSULATION PRODUCTS MARKET

- 13.3.1 MARKET DEFINITION

- 13.3.2 MARKET OVERVIEW

- 13.4 INSULATION PRODUCTS MARKET, BY REGION

- TABLE 302 INSULATION PRODUCTS MARKET SIZE, BY REGION, 2016-2019 (USD MILLION)

- TABLE 303 INSULATION PRODUCTS MARKET SIZE, BY REGION, 2020-2026 (USD MILLION)

- 13.4.1 NORTH AMERICA

- TABLE 304 NORTH AMERICA: INSULATION PRODUCTS MARKET SIZE, BY COUNTRY, 2016-2019 (USD MILLION)

- TABLE 305 NORTH AMERICA: INSULATION PRODUCTS MARKET SIZE, BY COUNTRY, 2020-2026 (USD MILLION)

- 13.4.2 EUROPE

- TABLE 306 EUROPE: INSULATION PRODUCTS MARKET SIZE, BY COUNTRY, 2016-2019 (USD MILLION)

- TABLE 307 EUROPE: INSULATION PRODUCTS MARKET SIZE, BY COUNTRY, 2020-2026 (USD MILLION)

- 13.4.3 ASIA PACIFIC

- TABLE 308 ASIA PACIFIC: INSULATION PRODUCTS MARKET SIZE, BY COUNTRY, 2016-2019 (USD MILLION)

- TABLE 309 ASIA PACIFIC: INSULATION PRODUCTS MARKET SIZE, BY COUNTRY, 2020-2026 (USD MILLION)

- 13.4.4 REST OF THE WORLD

- TABLE 310 ROW: INSULATION PRODUCTS MARKET SIZE, BY COUNTRY, 2016-2019 (USD MILLION)

- TABLE 311 ROW: INSULATION PRODUCTS MARKET SIZE, BY COUNTRY, 2020-2026 (USD MILLION)

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS