|

|

市場調査レポート

商品コード

1505244

ドア用断熱材の世界市場:材料タイプ別、断熱タイプ別、最終用途別、地域別 - 予測(~2029年)Door Insulation Market by Material Type (Traditional Insulation, Foam Insulation, Natural Insulation, Others), Insulation Type (Thermal, Acoustic, Others), End-use (Residential, Commercial, Industrial) and Region - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| ドア用断熱材の世界市場:材料タイプ別、断熱タイプ別、最終用途別、地域別 - 予測(~2029年) |

|

出版日: 2024年07月01日

発行: MarketsandMarkets

ページ情報: 英文 241 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

世界のドア用断熱材の市場規模は、2024年の13億米ドルから2029年までに17億米ドルに達すると予測され、CAGRで5.2%の成長が見込まれます。

市場は、その急成長の促進要因の重なりによって牽引されています。エネルギー効率と持続可能性に対する意識の高まり、熱性能を重視する厳しい建築規制、騒音防止ソリューションに対する需要の高まりは、市場の主な促進要因です。さらに、断熱技術の進歩や、優れた性能を提供する革新的な材料、世界の建設活動の活発化も市場の拡大に寄与しています。これらの促進要因は、熱的快適性の向上、エネルギーコストの削減、環境基準への適合に対するニーズと相まって、ドア用断熱材市場の持続的な成長に好ましい環境を作り出しています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2020年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2030年 |

| 単位 | 金額(100万/10億米ドル)、数量(キロトン) |

| セグメント | 材料タイプ、絶縁タイプ、最終用途、地域 |

| 対象地域 | アジア太平洋、北米、欧州、中東・アフリカ、南米 |

「材料タイプ別では、伝統的な断熱材が2023年に第2位の市場シェアを占めます。」

ガラス繊維やミネラルウールのような伝統的な断熱材は、その確立されたプレゼンス、汎用性、費用対効果により、ポリウレタンやポリスチレンフォーム断熱材に次いでドア用断熱材市場で2番目に大きなセグメントとなっています。細いガラス繊維から作られるガラス繊維断熱材は、優れた熱特性と音響特性を備えているため、新築でも改修でもドア用断熱材としてよく使われます。湿気、火災、害虫に対する耐性がさらにその魅力を高めています。天然または合成鉱物から作られるミネラルウールは、優れた耐火性と吸音性を備えており、これらの要素が重要な用途に最適です。これらの伝統的な材料は、何十年もの間、建設産業で広く使用され、建設業者、請負業者、住宅所有者の間で信頼と信用を得てきました。施工が簡単で入手しやすく、先進の断熱材に比べて比較的安価であるため、特に予算重視のプロジェクトでは魅力的な選択肢となります。さらに、ファイバーグラスとミネラルウールは不燃性であるため、安全性が重要視される環境での使用に適しています。さらに、ファイバーグラスとミネラルウールの製造工程における継続的な改良によって性能が向上し、最新の断熱材に代わる競争力のある選択肢となっています。ポリウレタンフォームとポリスチレンフォームが優れた断熱材を提供する一方で、費用対効果、汎用性、確立された効能の組み合わせにより、ガラス繊維とミネラルウールがドア用断熱材市場で強力な存在であり続けています。

「住宅が予測期間に金額ベースで市場のもっとも急成長する最終用途となる見込みです。」

住宅セグメントは、その拡大を促進する複数の主な要因により、ドア用断熱材市場でもっとも急成長しているセグメントとなっています。第一に、住宅所有者の間でエネルギー効率と持続可能性に対する意識が高まり、重視されるようになっています。エネルギーコストの上昇と環境への関心の高まりにより、エネルギー消費と二酸化炭素排出を削減する方法を求める住宅所有者が増えています。ドア用断熱材は、住宅の熱性能を向上させ、ドアからの熱損失や熱取得を抑え、エネルギー料金を下げる上で重要な役割を果たしています。第二に、エネルギー効率の高い住宅改良を促進することを目的とした政府の取り組みや優遇措置が、住宅部門におけるドア断熱の需要をさらに促進しています。こうした税額控除、リベート、省エネアップグレードに対する補助金などのインセンティブは、住宅所有者が住宅のエネルギー効率を向上させる断熱ソリューションに投資することを奨励します。さらに、住宅の新築や既存住宅の改築は、住宅向けドア用断熱材市場の成長に大きく寄与しています。建設業者、請負業者、住宅所有者は、ドアに高品質の断熱材を施工することで、快適性の向上、騒音伝達の低減、資産価値の上昇など、長期的な利益が得られることを認識しています。さらに、革新的な材料や施工技術の向上といった断熱技術の進歩により、住宅所有者によるドア用断熱材のアップグレードがより簡単かつ費用対効果も高いものとなっています。全体として、消費者の意識、政府の支援、建設活動、技術の進歩の組み合わせが、ドア用断熱材市場における住宅セグメントの急成長を後押ししています。

当レポートでは、世界のドア用断熱材市場について調査分析し、主な促進要因と抑制要因、競合情勢、将来の動向などの情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

- ドア用断熱材市場の企業にとって魅力的な機会

- ドア用断熱材市場:材料別

- ドア用断熱材市場:断熱材タイプ別

- ドア用断熱材市場:最終用途別

- ドア用断熱材市場:主要国別

第5章 市場の概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

第6章 産業の動向

- イントロダクション

- 顧客ビジネスに影響を与える動向/混乱

- バリューチェーン分析

- 原材料サプライヤー

- メーカー

- 販売業者

- エンドユーザー

- 投資情勢と資金調達シナリオ

- 価格分析

- 平均販売価格動向:地域別

- 平均販売価格動向:材料別

- 主要企業の平均販売価格動向:上位3材料タイプ別

- エコシステム

- 技術分析

- 特許分析

- 貿易分析

- 輸入シナリオ

- 輸出シナリオ

- 主な会議とイベント(2024年~2025年)

- 関税と規制情勢

- ドア用断熱材市場に関連する関税と規制

- 規制機関、政府機関、その他の組織

- ドア用断熱材市場に関する規制

- ポーターのファイブフォース分析

- 主なステークホルダーと購入基準

- マクロ経済指標

- ケーススタディ分析

第7章 ドア用断熱材市場:断熱材タイプ別

- イントロダクション

- 熱

- 音響

- その他の断熱材タイプ

第8章 ドア用断熱材市場:材料別

- イントロダクション

- 伝統的な断熱材

- ファイバーグラス

- ウール

- フォーム断熱材

- ポリウレタンフォーム

- ポリスチレンフォーム

- 天然断熱材

- 羊毛

- コットン

- セルロース

- コルク

- 麻

- 木質繊維

- その他の材料タイプ

- エアロゲル断熱材

- 反射断熱材

- ポリイソシアヌレート(PIR)絶縁材

- バーミキュライト断熱材

第9章 ドア用断熱材市場:最終用途別

- イントロダクション

- 住宅

- 商業

- 工業

第10章 ドア用断熱材市場:地域別

- イントロダクション

- アジア太平洋

- 北米

- 欧州

- 中東・アフリカ

- 南米

第11章 競合情勢

- イントロダクション

- 主要企業戦略/有力企業

- 市場シェア分析

- 主要市場企業ランキング(2023年)

- 主要企業の市場シェア

- 収益分析

- ブランド/製品の比較

- 企業の評価マトリクス、主要企業(2023年)

- 企業の評価マトリクス、スタートアップ/中小企業

- 評価と財務指標:ドア用断熱材ベンダー

- 競合シナリオと動向

第12章 企業プロファイル

- 主要企業

- BASF SE

- DUPONT

- COVESTRO AG

- JOHNS MANVILLE

- ROCKWOOL A/S

- SYNTHOS

- OWENS CORNING

- KINGSPAN GROUP

- KNAUF INSULATION

- SOUDAL N.V.

- SAINT-GOBAIN

- HUNTSMAN INTERNATIONAL LLC.

- DOW

- その他の企業

- SELENA GROUP

- PAUL BAUDER GMBH & CO. KG

- HELIOS KEMOSTIK, D.O.O.

- ADFAST

- INSULFOAM

- CELLOFOAM NORTH AMERICA INC.

- ATLAS ROOFING CORPORATION

- ICP BUILDING SOLUTIONS GROUP

- VASMANN

- BOSTIK

- FISCHER GROUP OF COMPANIES

第13章 付録

The Door insulation Market is projected to reach USD 1.7 billion by 2029, at a CAGR of 5.2% from USD 1.3 billion in 2024. The door insulation market is driven by a confluence of factors fueling its rapid growth. Increasing awareness of energy efficiency and sustainability, stringent building regulations emphasizing thermal performance, and rising demand for noise control solutions are key drivers propelling the market forward. Additionally, advancements in insulation technology, innovative materials offering superior performance, and growing construction activities worldwide contribute to the market's expansion. These drivers, coupled with the need for enhanced thermal comfort, reduced energy costs, and compliance with environmental standards, create a favorable environment for sustained growth in the door insulation market.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2030 |

| Units Considered | Value (USD Billion/Million), and Volume (Kiloton) |

| Segments | Material Type, Insulation Type, End-use, and Region |

| Regions covered | Asia Pacific, North America, Europe, Middle East & Africa, South America |

"Traditional insulation, by material type, accounts for the second-largest market share in 2023."

Traditional insulation like fiberglass and mineral wool account for the second largest segment of the door insulation market after polyurethane and polystyrene foam insulation due to their well-established presence, versatility, and cost-effectiveness. Fiberglass insulation, made from fine strands of glass, offers excellent thermal and acoustic properties, making it a popular choice for door insulation in both new constructions and retrofits. Its resistance to moisture, fire, and pests further enhances its appeal. Mineral wool, derived from natural or synthetic minerals, provides superior fire resistance and sound absorption capabilities, making it ideal for applications where these factors are critical. These traditional materials have been extensively used in the construction industry for decades, earning trust and reliability among builders, contractors, and homeowners. Their ease of installation, availability, and relatively lower cost compared to advanced insulation materials make them attractive options, especially in budget-conscious projects. Additionally, fiberglass and mineral wool are non-combustible, contributing to their use in safety-critical environments. Furthermore, ongoing improvements in the manufacturing processes of fiberglass and mineral wool have enhanced their performance, making them competitive alternatives to modern insulation materials. While polyurethane and polystyrene foams offer superior thermal insulation, the combination of cost-effectiveness, versatility, and established efficacy ensures that fiberglass and mineral wool remain significant players in the door insulation market.

"Residential is expected to be the fastest growing end-use for door insulation market during the forecast period, in terms of value."

The residential segment is the fastest-growing sector in the door insulation market due to several key factors driving its expansion. Firstly, there is a growing awareness and emphasis on energy efficiency and sustainability among homeowners. With rising energy costs and increasing environmental concerns, more homeowners are seeking ways to reduce their energy consumption and carbon footprint. Door insulation plays a crucial role in improving the thermal performance of homes, reducing heat loss or gain through doors, and thereby lowering energy bills. Secondly, government initiatives and incentives aimed at promoting energy-efficient home improvements further fuel the demand for door insulation in the residential sector. These incentives, such as tax credits, rebates, and subsidies for energy-saving upgrades, encourage homeowners to invest in insulation solutions that improve their homes' energy efficiency. Additionally, the construction of new residential buildings and the renovation of existing homes contribute significantly to the growth of the residential door insulation market. Builders, contractors, and homeowners recognize the long-term benefits of installing high-quality insulation in doors, including improved comfort, reduced noise transmission, and increased property value. Moreover, advancements in insulation technology, such as innovative materials and improved installation techniques, make it easier and more cost-effective for homeowners to upgrade their door insulation. Overall, the combination of consumer awareness, government support, construction activities, and technological advancements drives the rapid growth of the residential segment in the door insulation market.

"Thermal insulation is expected to be the fastest growing insulation type segment for door insulation market during the forecast period, in terms of value."

Thermal insulation is the fastest-growing type in the door insulation market due to its critical role in enhancing energy efficiency and reducing heating and cooling costs. As energy prices rise and environmental concerns intensify, there is a growing demand for solutions that minimize energy consumption. Thermal insulation effectively prevents heat transfer, maintaining desired indoor temperatures and reducing the load on HVAC systems. This results in significant cost savings and a smaller carbon footprint, aligning with global sustainability goals. Advancements in insulation materials, such as improved foam and aerogel technologies, offer superior thermal performance and easier installation processes. These innovations make thermal insulation more accessible and effective, driving its adoption in both residential and commercial buildings. Moreover, building codes and regulations increasingly mandate higher energy efficiency standards, further propelling the demand for thermal insulation in doors. Additionally, the growing awareness of the long-term benefits of thermal insulation, such as enhanced comfort, reduced noise pollution, and increased property value, contributes to its rapid market growth. As consumers and businesses prioritize energy efficiency and sustainability, thermal insulation's ability to deliver tangible economic and environmental benefits ensures its position as the fastest-growing segment in the door insulation market.

"Based on region, North America was the second largest market for door insulation in 2023."

North America holds the position as the second-largest market for door insulation after Europe due to several significant factors. Firstly, the region's stringent energy efficiency regulations and building codes drive the demand for high-performance insulation solutions, including door insulation, to meet the required thermal performance standards. With a focus on reducing energy consumption and promoting sustainable building practices, there is a growing emphasis on enhancing the thermal efficiency of buildings through effective insulation measures. Secondly, North America's diverse climate conditions, ranging from extreme cold in northern regions to hot and humid climates in the south, create a strong need for insulation materials that can provide year-round thermal comfort. Door insulation plays a critical role in maintaining indoor temperatures, reducing heating and cooling costs, and improving overall energy efficiency, making it a vital component in building construction and renovation projects across the continent. Additionally, the construction industry's robust growth, fueled by residential, commercial, and industrial developments, contributes to the demand for door insulation materials. New construction projects, as well as renovations and retrofitting activities, drive the market for insulation solutions that enhance building performance and meet regulatory requirements. Moreover, technological advancements in insulation materials, such as innovative formulations and improved installation techniques, further boost the adoption of door insulation in North America. These advancements offer enhanced thermal performance, durability, and environmental sustainability, aligning with the region's focus on energy conservation and green building practices.

In the process of determining and verifying the market size for several segments and subsegments identified through secondary research, extensive primary interviews were conducted. A breakdown of the profiles of the primary interviewees is as follows:

- By Company Type: Tier 1 - 45%, Tier 2 - 35%, and Tier 3 - 20%

- By Designation: C-Level - 20%, Director Level - 10%, and Others - 70%

- By Region: North America - 30%, Europe -30%, Asia Pacific - 20%, Middle East & Africa - 10%, and South America-10%

The key players in this market are BASF SE (Germany), DuPont (US), Soudal Holding N.V. (Belgium), Covestro AG (Germany), Owens Corning (US), ROCKWOOL A/S (Denmark), Knauf Insulation (US), Johns Manville (US), Synthos (Poland), Saint-Gobain (France), Kingspan Group (Ireland) etc.

Research Coverage

This report segments the market for the door insulation market on the basis of material type, insulation type, end-use and region. It provides estimations for the overall value of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products & services, key strategies, new product launches, expansions, and mergers & acquisitions associated with the market for the door insulation market.

Key benefits of buying this report

This research report is focused on various levels of analysis - industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape, emerging and high-growth segments of the door insulation market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of key drivers: Energy efficiency regulations and environmental awareness, growing construction industry and technological development bringing innovative and advanced insulating materials and installation methods.

- Market Penetration: Comprehensive information on the door insulation market offered by top players in the global door insulation market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the door insulation market.

- Market Development: Comprehensive information about lucrative emerging markets - the report analyzes the markets for the door insulation across regions.

- Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global door insulation market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the door insulation market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 INCLUSIONS & EXCLUSIONS

- FIGURE 1 DOOR INSULATION MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 LIMITATIONS

- 1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 DOOR INSULATION MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Primary data sources

- 2.1.2.3 Key primary participants

- 2.1.2.4 Breakdown of interviews with experts

- 2.1.2.5 Key industry insights

- 2.2 BASE NUMBER CALCULATION

- 2.2.1 SUPPLY-SIDE APPROACH

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: SUPPLY-SIDE APPROACH

- 2.2.2 DEMAND-SIDE APPROACH

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: DEMAND-SIDE APPROACH

- 2.3 FORECAST NUMBER CALCULATION

- 2.3.1 SUPPLY SIDE

- 2.3.2 DEMAND SIDE

- 2.4 MARKET SIZE ESTIMATION

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: REVENUE OF MARKET PLAYERS

- 2.4.1 BOTTOM-UP APPROACH

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- 2.4.2 TOP-DOWN APPROACH

- FIGURE 7 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- 2.5 DATA TRIANGULATION

- FIGURE 8 DOOR INSULATION MARKET: DATA TRIANGULATION

- 2.6 RESEARCH ASSUMPTIONS

- 2.7 IMPACT OF RECESSION

- 2.8 GROWTH FORECAST

- 2.9 RISK ASSESSMENT

- 2.10 FACTOR ANALYSIS

3 EXECUTIVE SUMMARY

- FIGURE 9 FOAM INSULATION SEGMENT TO DOMINATE MARKET BETWEEN 2024 AND 2029

- FIGURE 10 THERMAL INSULATION SEGMENT TO LEAD MARKET BETWEEN 2024 AND 2029

- FIGURE 11 RESIDENTIAL END USE SEGMENT TO LEAD MARKET BETWEEN 2024 AND 2030

- FIGURE 12 EUROPE TO LEAD MARKET DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DOOR INSULATION MARKET

- FIGURE 13 ENERGY EFFICIENCY REGULATIONS REDUCING ENERGY CONSUMPTION AND GREENHOUSE GAS EMISSIONS TO DRIVE MARKET

- 4.2 DOOR INSULATION MARKET, BY MATERIAL TYPE

- FIGURE 14 FOAM INSULATION TO BE FASTEST-GROWING SEGMENT DURING FORECAST PERIOD

- 4.3 DOOR INSULATION MARKET, BY INSULATION TYPE

- FIGURE 15 THERMAL TO BE FASTEST-GROWING SEGMENT DURING FORECAST PERIOD

- 4.4 DOOR INSULATION MARKET, BY END USE

- FIGURE 16 RESIDENTIAL TO BE FASTEST-GROWING SEGMENT DURING FORECAST PERIOD

- 4.5 DOOR INSULATION MARKET, BY KEY COUNTRY

- FIGURE 17 INDIA TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 18 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN DOOR INSULATION MARKET

- 5.2.1 DRIVERS

- 5.2.1.1 Energy efficiency regulations and environmental awareness

- 5.2.1.2 Growing construction industry

- 5.2.1.3 Technological advancements in insulation materials and installation methods

- 5.2.2 RESTRAINTS

- 5.2.2.1 High initial cost of insulation and installation

- 5.2.2.2 Regulatory hurdles and compliance costs

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Green building initiatives and retrofitting existing buildings

- 5.2.4 CHALLENGES

- 5.2.4.1 Volatility in prices of raw materials

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.2.1 REVENUE SHIFT AND NEW REVENUE POCKETS FOR DOOR INSULATION MANUFACTURERS

- FIGURE 19 REVENUE SHIFT OF DOOR INSULATION MARKET

- 6.3 VALUE CHAIN ANALYSIS

- FIGURE 20 OVERVIEW OF DOOR INSULATION MARKET VALUE CHAIN

- 6.3.1 RAW MATERIAL SUPPLIERS

- 6.3.2 MANUFACTURERS

- 6.3.3 DISTRIBUTORS

- 6.3.4 END USERS

- 6.4 INVESTMENT LANDSCAPE AND FUNDING SCENARIO

- FIGURE 21 DOOR INSULATION MARKET: INVESTMENT AND FUNDING SCENARIO

- 6.5 PRICING ANALYSIS

- 6.5.1 AVERAGE SELLING PRICE TREND, BY REGION

- TABLE 1 AVERAGE SELLING PRICE, BY REGION, 2020-2029 (USD/KG)

- FIGURE 22 DOOR INSULATION MARKET: AVERAGE SELLING PRICE TREND, BY REGION

- 6.5.2 AVERAGE SELLING PRICE TREND, BY MATERIAL TYPE

- TABLE 2 AVERAGE SELLING PRICE, BY MATERIAL TYPE, 2020-2029 (USD/KG)

- 6.5.3 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY TOP 3 MATERIAL TYPES

- TABLE 3 AVERAGE SELLING PRICE OF KEY PLAYERS, BY MATERIAL TYPE, 2020-2029 (USD/KG)

- FIGURE 23 AVERAGE SELLING PRICE TREND OF KEY PLAYERS FOR TOP 3 MATERIAL TYPES

- 6.6 ECOSYSTEM

- TABLE 4 DOOR INSULATION MARKET: ECOSYSTEM

- 6.7 TECHNOLOGY ANALYSIS

- 6.7.1 TECHNOLOGIES OFFERED IN DOOR INSULATION MARKET

- TABLE 5 TECHNOLOGIES OFFERED IN DOOR INSULATION MARKET

- 6.7.2 COMPLEMENTARY TECHNOLOGIES OFFERED IN DOOR INSULATION MARKET

- TABLE 6 COMPLEMENTARY TECHNOLOGIES OFFERED IN DOOR INSULATION MARKET

- 6.7.3 ADJACENT TECHNOLOGIES OFFERED FOR DOOR INSULATION MARKET

- TABLE 7 ADJACENT TECHNOLOGIES OFFERED FOR DOOR INSULATION MARKET

- 6.8 PATENT ANALYSIS

- 6.8.1 METHODOLOGY

- 6.8.2 PATENTS GRANTED WORLDWIDE, 2014-2023

- TABLE 8 DOOR INSULATION MARKET: TOTAL NUMBER OF PATENTS

- 6.8.3 PATENT PUBLICATION TRENDS

- FIGURE 24 NUMBER OF PATENTS GRANTED (2014-2023)

- 6.8.4 INSIGHTS

- 6.8.5 LEGAL STATUS OF PATENTS

- FIGURE 25 DOOR INSULATION MARKET: LEGAL STATUS OF PATENTS

- 6.8.6 JURISDICTION ANALYSIS

- FIGURE 26 PATENT ANALYSIS FOR DOOR INSULATION, BY JURISDICTION, 2014-2023

- 6.8.7 TOP COMPANIES/APPLICANTS

- FIGURE 27 TOP 10 COMPANIES WITH HIGHEST NUMBER OF PATENTS IN LAST 10 YEARS

- TABLE 9 LIST OF MAJOR PATENT OWNERS FOR DOOR INSULATION

- 6.8.8 LIST OF MAJOR PATENTS

- TABLE 10 MAJOR PATENTS FOR DOOR INSULATION

- 6.9 TRADE ANALYSIS

- 6.9.1 IMPORT SCENARIO

- FIGURE 28 IMPORTS OF DOOR INSULATION, BY COUNTRY, 2020-2023 (USD THOUSAND)

- 6.9.2 EXPORT SCENARIO

- FIGURE 29 EXPORTS OF DOOR INSULATION, BY COUNTRY, 2020-2023 (USD THOUSAND)

- 6.10 KEY CONFERENCES & EVENTS, 2024-2025

- TABLE 11 DOOR INSULATION MARKET: DETAILED LIST OF CONFERENCES & EVENTS, 2024-2025

- 6.11 TARIFF AND REGULATORY LANDSCAPE

- 6.11.1 TARIFFS AND REGULATIONS RELATED TO DOOR INSULATION MARKET

- TABLE 12 TARIFFS RELATED TO DOOR INSULATION MARKET

- 6.11.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 MIDDLE EAST & AFRICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 SOUTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.11.3 REGULATIONS RELATED TO DOOR INSULATION MARKET

- TABLE 18 LIST OF REGULATIONS FOR DOOR INSULATION MARKET

- 6.12 PORTER'S FIVE FORCES ANALYSIS

- TABLE 19 DOOR INSULATION MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 30 DOOR INSULATION MARKET: PORTER'S FIVE FORCES ANALYSIS

- 6.12.1 THREAT OF SUBSTITUTES

- 6.12.2 THREAT OF NEW ENTRANTS

- 6.12.3 BARGAINING POWER OF SUPPLIERS

- 6.12.4 BARGAINING POWER OF BUYERS

- 6.12.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.13 KEY STAKEHOLDERS AND BUYING CRITERIA

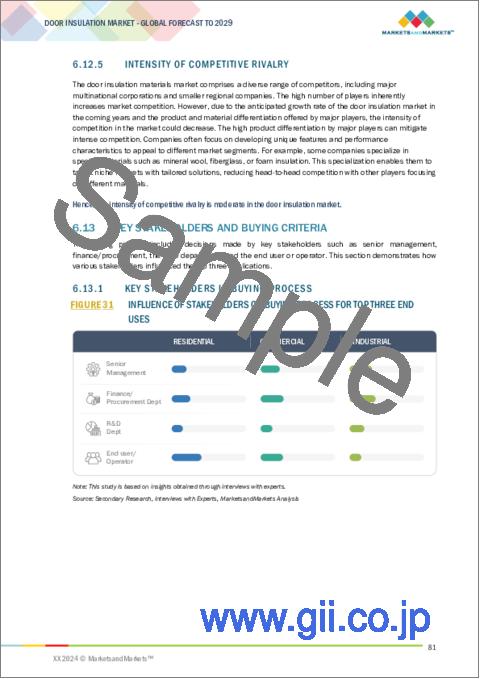

- 6.13.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 31 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USES

- TABLE 20 INFLUENCE OF INSTITUTIONAL BUYERS ON BUYING PROCESS FOR TOP THREE END USES

- 6.13.2 BUYING CRITERIA

- FIGURE 32 KEY BUYING CRITERIA FOR END USERS

- TABLE 21 KEY BUYING CRITERIA FOR END USERS

- 6.14 MACROECONOMIC INDICATORS

- 6.14.1 GDP TRENDS AND FORECASTS OF MAJOR ECONOMIES

- TABLE 22 PROJECTED REAL GDP GROWTH (ANNUAL PERCENTAGE CHANGE) OF KEY COUNTRIES, 2018-2025

- 6.15 CASE STUDY ANALYSIS

- 6.15.1 THERMAL ANALYSIS OF A WOODEN DOOR SYSTEM WITH INTEGRATED VACUUM INSULATION PANELS

- 6.15.2 THERMAL REPLACEMENT

- 6.15.3 PROFESSIONAL RESIDENTIAL INSTALLATION

7 DOOR INSULATION MARKET, BY INSULATION TYPE

- 7.1 INTRODUCTION

- FIGURE 33 THERMAL SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- TABLE 23 DOOR INSULATION MARKET, BY INSULATION TYPE, 2020-2023 (USD MILLION)

- TABLE 24 DOOR INSULATION MARKET, BY INSULATION TYPE, 2024-2029 (USD MILLION)

- 7.2 THERMAL

- 7.2.1 RISING ENERGY COSTS AND STRINGENT ENVIRONMENTAL REGULATIONS TO DRIVE MARKET

- 7.3 ACOUSTIC

- 7.3.1 URBANIZATION, REGULATORY REQUIREMENTS, AND TECHNOLOGICAL ADVANCEMENTS TO DRIVE MARKET

- 7.4 OTHER INSULATION TYPES

8 DOOR INSULATION MARKET, BY MATERIAL TYPE

- 8.1 INTRODUCTION

- FIGURE 34 FOAM INSULATION TO LEAD MARKET DURING FORECAST PERIOD

- TABLE 25 DOOR INSULATION MARKET, BY MATERIAL TYPE, 2020-2023 (USD MILLION)

- TABLE 26 DOOR INSULATION MARKET, BY MATERIAL TYPE, 2024-2029 (USD MILLION)

- TABLE 27 DOOR INSULATION MARKET, BY MATERIAL TYPE, 2020-2023 (KILOTON)

- TABLE 28 DOOR INSULATION MARKET, BY MATERIAL TYPE, 2024-2029( KILOTON)

- 8.2 TRADITIONAL INSULATION

- 8.2.1 FIBERGLASS

- 8.2.1.1 Exceptional acoustic resistance and long term durability to drive market

- 8.2.2 WOOL

- 8.2.2.1 Exceptional fire resistance properties and easy installation to drive market

- 8.2.1 FIBERGLASS

- 8.3 FOAM INSULATION

- 8.3.1 POLYURETHANE FOAM

- 8.3.1.1 Exceptional thermal and moisture resistance along with ease of installation to drive market

- 8.3.2 POLYSTYRENE FOAM

- 8.3.2.1 Durability and ease of installation to drive market

- 8.3.1 POLYURETHANE FOAM

- 8.4 NATURAL INSULATION

- 8.4.1 SHEEP WOOL

- 8.4.1.1 Self-extinguishing properties to drive installation in buildings

- 8.4.2 COTTON

- 8.4.2.1 Pest and mold resistance, along with thermal insulation, to drive market

- 8.4.3 CELLULOSE

- 8.4.3.1 Sustainability due to recycled content and resource conservation along with thermal resistance to drive market

- 8.4.4 CORK

- 8.4.4.1 Unique cellular structure trapping heat and reducing thermal conductivity to drive market

- 8.4.5 HEMP

- 8.4.5.1 High heat regulating capacity, sustainability, and eco-friendliness to drive market

- 8.4.6 WOOD FIBER

- 8.4.6.1 Hygroscopic properties enhancing moisture regulating capabilities to drive market

- 8.4.1 SHEEP WOOL

- 8.5 OTHER MATERIAL TYPES

- 8.5.1 AEROGEL INSULATION

- 8.5.2 REFLECTIVE INSULATION

- 8.5.3 POLYISOCYANURATE (PIR) INSULATION

- 8.5.4 VERMICULITE INSULATION

9 DOOR INSULATION MARKET, BY END USE

- 9.1 INTRODUCTION

- FIGURE 35 RESIDENTIAL SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- TABLE 29 DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 30 DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 9.2 RESIDENTIAL

- 9.2.1 DEMAND FOR ENERGY EFFICIENCY, COMFORT, AND SUSTAINABILITY TO DRIVE MARKET

- 9.3 COMMERCIAL

- 9.3.1 ENERGY EFFICIENCY, REGULATORY COMPLIANCE, COST SAVINGS, AND ENHANCED OCCUPANT COMFORT TO DRIVE MARKET

- 9.4 INDUSTRIAL

- 9.4.1 REGULATORY COMPLIANCE, ENERGY EFFICIENCY, SAFETY, DURABILITY, AND OPERATIONAL EFFICIENCY TO DRIVE MARKET

10 DOOR INSULATION MARKET, BY REGION

- 10.1 INTRODUCTION

- FIGURE 36 ASIA PACIFIC TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

- TABLE 31 DOOR INSULATION MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 32 DOOR INSULATION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 33 DOOR INSULATION MARKET, BY REGION, 2020-2023 (KILOTON)

- TABLE 34 DOOR INSULATION MARKET, BY REGION, 2024-2029 (KILOTON)

- 10.2 ASIA PACIFIC

- 10.2.1 IMPACT OF RECESSION

- FIGURE 37 ASIA PACIFIC: DOOR INSULATION MARKET SNAPSHOT

- TABLE 35 ASIA PACIFIC: DOOR INSULATION MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 36 ASIA PACIFIC: DOOR INSULATION MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 37 ASIA PACIFIC: DOOR INSULATION MARKET, BY COUNTRY, 2020-2023 (KILOTON)

- TABLE 38 ASIA PACIFIC: DOOR INSULATION MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 39 ASIA PACIFIC: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2020-2023 (USD MILLION)

- TABLE 40 ASIA PACIFIC: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2024-2029 (USD MILLION)

- TABLE 41 ASIA PACIFIC: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2020-2023 (KILOTON)

- TABLE 42 ASIA PACIFIC: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2024-2029 (KILOTON)

- TABLE 43 ASIA PACIFIC: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 44 ASIA PACIFIC: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- TABLE 45 ASIA PACIFIC: DOOR INSULATION MARKET, BY INSULATION TYPE, 2020-2023 (USD MILLION)

- TABLE 46 ASIA PACIFIC: DOOR INSULATION MARKET, BY INSULATION TYPE, 2024-2029 (USD MILLION)

- 10.2.1.1 China

- 10.2.1.1.1 Rapid industrialization, urbanization, and growing environmental awareness to drive market

- 10.2.1.1 China

- TABLE 47 CHINA: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 48 CHINA: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.2.1.2 JAPAN

- 10.2.1.2.1 Innovations in building materials and focus on disaster resilience to drive market

- 10.2.1.2 JAPAN

- TABLE 49 JAPAN: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 50 JAPAN: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.2.1.3 India

- 10.2.1.3.1 Rising middle-class income and improved living standards to drive market

- 10.2.1.3 India

- TABLE 51 INDIA: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 52 INDIA: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.2.1.4 South Korea

- 10.2.1.4.1 Adoption of smart building technologies prioritizing energy efficiency to drive market

- 10.2.1.4 South Korea

- TABLE 53 SOUTH KOREA: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 54 SOUTH KOREA: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.2.1.5 Rest of Asia Pacific

- TABLE 55 REST OF ASIA PACIFIC: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 56 REST OF ASIA PACIFIC: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.3 NORTH AMERICA

- 10.3.1 IMPACT OF RECESSION

- FIGURE 38 NORTH AMERICA: DOOR INSULATION MARKET SNAPSHOT

- TABLE 57 NORTH AMERICA: DOOR INSULATION MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 58 NORTH AMERICA: DOOR INSULATION MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 59 NORTH AMERICA: DOOR INSULATION MARKET, BY COUNTRY, 2020-2023 (KILOTON)

- TABLE 60 NORTH AMERICA: DOOR INSULATION MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 61 NORTH AMERICA: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2020-2023 (USD MILLION)

- TABLE 62 NORTH AMERICA: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2024-2029 (USD MILLION)

- TABLE 63 NORTH AMERICA: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2020-2023 (KILOTON)

- TABLE 64 NORTH AMERICA: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2024-2029 (KILOTON)

- TABLE 65 NORTH AMERICA: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 66 NORTH AMERICA: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- TABLE 67 NORTH AMERICA: DOOR INSULATION MARKET, BY INSULATION TYPE, 2020-2023 (USD MILLION)

- TABLE 68 NORTH AMERICA: DOOR INSULATION MARKET, BY INSULATION TYPE, 2024-2029 (USD MILLION)

- 10.3.1.1 US

- 10.3.1.1.1 Growing emphasis on reducing carbon footprint and enhancing energy efficiency to drive market

- 10.3.1.1 US

- TABLE 69 US: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 70 US: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.3.1.2 Canada

- 10.3.1.2.1 Harsh winter climates requiring effective door insulation to drive market

- 10.3.1.2 Canada

- TABLE 71 CANADA: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 72 CANADA: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.3.1.3 Mexico

- 10.3.1.3.1 Rising energy costs and demand for comfortable living and working environments to drive market

- 10.3.1.3 Mexico

- TABLE 73 MEXICO: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 74 MEXICO: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.4 EUROPE

- 10.4.1 IMPACT OF RECESSION

- FIGURE 39 EUROPE: DOOR INSULATION MARKET SNAPSHOT

- TABLE 75 EUROPE: DOOR INSULATION MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 76 EUROPE: DOOR INSULATION MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 77 EUROPE: DOOR INSULATION MARKET, BY COUNTRY, 2020-2023 (KILOTON)

- TABLE 78 EUROPE: DOOR INSULATION MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 79 EUROPE: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2020-2023 (USD MILLION)

- TABLE 80 EUROPE: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2024-2029 (USD MILLION)

- TABLE 81 EUROPE: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2020-2023 (KILOTON)

- TABLE 82 EUROPE: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2024-2029 (KILOTON)

- TABLE 83 EUROPE: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 84 EUROPE: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- TABLE 85 EUROPE: DOOR INSULATION MARKET, BY INSULATION TYPE, 2020-2023 (USD MILLION)

- TABLE 86 EUROPE: DOOR INSULATION MARKET, BY INSULATION TYPE, 2024-2029 (USD MILLION)

- 10.4.1.1 Germany

- 10.4.1.1.1 Advanced insulation technologies and focus on sustainability to drive market

- 10.4.1.1 Germany

- TABLE 87 GERMANY: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 88 GERMANY: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.4.1.2 Italy

- 10.4.1.2.1 Renovation boom fueled by government incentives to drive market

- 10.4.1.2 Italy

- TABLE 89 ITALY: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 90 ITALY: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.4.1.3 France

- 10.4.1.3.1 Environmental regulations for buildings and high energy costs to drive market

- 10.4.1.3 France

- TABLE 91 FRANCE: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 92 FRANCE: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.4.1.4 UK

- 10.4.1.4.1 Stringent building regulations for thermal performance to drive market

- 10.4.1.4 UK

- TABLE 93 UK: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 94 UK: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.4.1.5 Spain

- 10.4.1.5.1 Government incentives and mandates for energy-efficient home renovations to drive market

- 10.4.1.5 Spain

- TABLE 95 SPAIN: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 96 SPAIN: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.4.1.6 Russia

- 10.4.1.6.1 Adverse climatic conditions and energy-saving regulations to drive market

- 10.4.1.6 Russia

- TABLE 97 RUSSIA: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 98 RUSSIA: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.4.1.7 Rest of Europe

- TABLE 99 REST OF EUROPE: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 100 REST OF EUROPE: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.5 MIDDLE EAST & AFRICA

- 10.5.1 IMPACT OF RECESSION

- TABLE 101 MIDDLE EAST & AFRICA: DOOR INSULATION MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 102 MIDDLE EAST & AFRICA: DOOR INSULATION MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 103 MIDDLE EAST & AFRICA: DOOR INSULATION MARKET, BY COUNTRY, 2020-2023 (KILOTON)

- TABLE 104 MIDDLE EAST & AFRICA: DOOR INSULATION MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 105 MIDDLE EAST & AFRICA: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2020-2023 (USD MILLION)

- TABLE 106 MIDDLE EAST & AFRICA: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2024-2029 (USD MILLION)

- TABLE 107 MIDDLE EAST & AFRICA: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2020-2023 (KILOTON)

- TABLE 108 MIDDLE EAST & AFRICA: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2024-2029 (KILOTON)

- TABLE 109 MIDDLE EAST & AFRICA: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 110 MIDDLE EAST & AFRICA: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- TABLE 111 MIDDLE EAST & AFRICA: DOOR INSULATION MARKET, BY INSULATION TYPE, 2020-2023 (USD MILLION)

- TABLE 112 MIDDLE EAST & AFRICA: DOOR INSULATION MARKET, BY INSULATION TYPE, 2024-2029 (USD MILLION)

- 10.5.1.1 GCC Countries

- 10.5.1.1.1 UAE

- 10.5.1.1.1.1 Stringent green building regulations for adoption of energy-saving measures to drive market

- 10.5.1.1.1 UAE

- 10.5.1.1 GCC Countries

- TABLE 113 UAE: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 114 UAE: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.5.1.1.2 Saudi Arabia

- 10.5.1.1.2.1 Intense heat, stringent building codes, and rising energy costs to drive market

- 10.5.1.1.2 Saudi Arabia

- TABLE 115 SAUDI ARABIA: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 116 SAUDI ARABIA: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.5.1.1.3 Rest of GCC countries

- TABLE 117 REST OF GCC: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 118 REST OF GCC: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.5.1.2 South Africa

- 10.5.1.2.1 Strategic efforts to balance cost, awareness, and sustainability to drive market

- 10.5.1.2 South Africa

- TABLE 119 SOUTH AFRICA: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 120 SOUTH AFRICA: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.5.1.3 Rest of Middle East & Africa

- TABLE 121 REST OF MIDDLE EAST & AFRICA: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 122 REST OF MIDDLE EAST & AFRICA: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.6 SOUTH AMERICA

- 10.6.1 IMPACT OF RECESSION

- TABLE 123 SOUTH AMERICA: DOOR INSULATION MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 124 SOUTH AMERICA: DOOR INSULATION MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 125 SOUTH AMERICA: DOOR INSULATION MARKET, BY COUNTRY, 2020-2023 (KILOTON)

- TABLE 126 SOUTH AMERICA: DOOR INSULATION MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 127 SOUTH AMERICA: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2020-2023 (USD MILLION)

- TABLE 128 SOUTH AMERICA: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2024-2029 (USD MILLION)

- TABLE 129 SOUTH AMERICA: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2020-2023 (KILOTON)

- TABLE 130 SOUTH AMERICA: DOOR INSULATION MARKET, BY MATERIAL TYPE, 2024-2029 (KILOTON)

- TABLE 131 SOUTH AMERICA: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 132 SOUTH AMERICA: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- TABLE 133 SOUTH AMERICA: DOOR INSULATION MARKET, BY INSULATION TYPE, 2020-2023 (USD MILLION)

- TABLE 134 SOUTH AMERICA: DOOR INSULATION MARKET, BY INSULATION TYPE, 2024-2029 (USD MILLION)

- 10.6.1.1 Argentina

- 10.6.1.1.1 Economic instability and limited consumer awareness to hinder market growth

- 10.6.1.1 Argentina

- TABLE 135 ARGENTINA: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 136 ARGENTINA: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.6.1.2 Brazil

- 10.6.1.2.1 Diverse climatic landscape and incentives for energy-efficient construction practices to drive market

- 10.6.1.2 Brazil

- TABLE 137 BRAZIL: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 138 BRAZIL: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

- 10.6.1.3 Rest of South America

- TABLE 139 REST OF SOUTH AMERICA: DOOR INSULATION MARKET, BY END USE, 2020-2023 (USD MILLION)

- TABLE 140 REST OF SOUTH AMERICA: DOOR INSULATION MARKET, BY END USE, 2024-2029 (USD MILLION)

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 11.2.1 OVERVIEW OF STRATEGIES ADOPTED BY DOOR INSULATION MANUFACTURERS

- 11.3 MARKET SHARE ANALYSIS

- 11.3.1 RANKING OF KEY MARKET PLAYERS, 2023

- FIGURE 40 RANKING OF TOP FIVE PLAYERS IN DOOR INSULATION MARKET, 2023

- 11.3.2 MARKET SHARE OF KEY PLAYERS

- TABLE 141 DOOR INSULATION MARKET: DEGREE OF COMPETITION

- FIGURE 41 SHARE OF KEY PLAYERS IN DOOR INSULATION MARKET, 2023

- 11.4 REVENUE ANALYSIS

- FIGURE 42 REVENUE ANALYSIS OF KEY PLAYERS, 2020-2024

- 11.5 BRAND/PRODUCT COMPARISON

- FIGURE 43 BRAND/PRODUCT COMPARATIVE ANALYSIS, BY SEGMENT

- 11.6 COMPANY EVALUATION MATRIX, KEY PLAYERS, 2023

- 11.6.1 STARS

- 11.6.2 EMERGING LEADERS

- 11.6.3 PERVASIVE PLAYERS

- 11.6.4 PARTICIPANTS

- FIGURE 44 DOOR INSULATION MARKET: COMPANY EVALUATION MATRIX, 2023

- 11.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2023

- FIGURE 45 DOOR INSULATION MARKET: COMPANY FOOTPRINT

- TABLE 142 INSULATION TYPE: COMPANY FOOTPRINT (13 COMPANIES)

- TABLE 143 MATERIAL TYPE: COMPANY FOOTPRINT (13 COMPANIES)

- TABLE 144 END USE: COMPANY FOOTPRINT (13 COMPANIES)

- TABLE 145 REGION: COMPANY FOOTPRINT (13 COMPANIES)

- 11.7 COMPANY EVALUATION MATRIX, STARTUPS/SMES

- 11.7.1 PROGRESSIVE COMPANIES

- 11.7.2 RESPONSIVE COMPANIES

- 11.7.3 DYNAMIC COMPANIES

- 11.7.4 STARTING BLOCKS

- FIGURE 46 DOOR INSULATION MARKET: STARTUP/SME EVALUATION MATRIX, 2023

- 11.7.5 COMPETITIVE BENCHMARKING, STARTUPS/SMES, 2023

- 11.7.5.1 Detailed list of key startups/SMEs

- TABLE 146 DOOR INSULATION MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- 11.7.5.2 Door insulation market: Competitive benchmarking of key startups/SMEs

- TABLE 147 DOOR INSULATION MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 11.8 VALUATION AND FINANCIAL METRICS: DOOR INSULATION VENDORS

- FIGURE 47 EV/EBITDA OF KEY VENDORS

- FIGURE 48 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY VENDORS

- 11.9 COMPETITIVE SCENARIO AND TRENDS

- 11.9.1 PRODUCT LAUNCHES

- TABLE 148 DOOR INSULATION MARKET: PRODUCT LAUNCHES, JANUARY 2020-MAY 2024

- 11.9.2 DEALS

- TABLE 149 DOOR INSULATION MARKET: DEALS, JANUARY 2020-MAY 2024

- 11.9.3 EXPANSIONS

- TABLE 150 DOOR INSULATION MARKET: EXPANSIONS, JANUARY 2020-MAY 2024

- 11.9.4 OTHERS

- TABLE 151 DOOR INSULATION MARKET: OTHERS, JANUARY 2020-MAY 2024

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- (Business Overview, Products Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats))**

- 12.1.1 BASF SE

- TABLE 152 BASF SE: COMPANY OVERVIEW

- FIGURE 49 BASF SE: COMPANY SNAPSHOT

- TABLE 153 BASF SE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.2 DUPONT

- TABLE 154 DUPONT: COMPANY OVERVIEW

- FIGURE 50 DUPONT: COMPANY SNAPSHOT

- TABLE 155 DUPONT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.3 COVESTRO AG

- TABLE 156 COVESTRO AG: COMPANY OVERVIEW

- FIGURE 51 COVESTRO AG: COMPANY SNAPSHOT

- TABLE 157 COVESTRO AG: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 158 COVESTRO AG: DEALS, JANUARY 2020-MAY 2024

- 12.1.4 JOHNS MANVILLE

- TABLE 159 JOHNS MANVILLE: COMPANY OVERVIEW

- TABLE 160 JOHNS MANVILLE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.5 ROCKWOOL A/S

- TABLE 161 ROCKWOOL A/S: COMPANY OVERVIEW

- FIGURE 52 ROCKWOOL A/S: COMPANY SNAPSHOT

- TABLE 162 ROCKWOOL A/S: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 163 ROCKWOOL A/S: DEALS, JANUARY 2020-MAY 2024

- TABLE 164 ROCKWOOL A/S: EXPANSIONS, JANUARY 2020-MAY 2024

- TABLE 165 ROCKWOOL A/S: OTHERS, JANUARY 2020-MAY 2024

- 12.1.6 SYNTHOS

- TABLE 166 SYNTHOS: COMPANY OVERVIEW

- TABLE 167 SYNTHOS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 168 SYNTHOS: EXPANSIONS, JANUARY 2020-MAY 2024

- 12.1.7 OWENS CORNING

- TABLE 169 OWENS CORNING: COMPANY OVERVIEW

- FIGURE 53 OWENS CORNING: COMPANY SNAPSHOT

- TABLE 170 OWENS CORNING: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 171 OWENS CORNING: DEALS, JANUARY 2020-MAY 2024

- 12.1.8 KINGSPAN GROUP

- TABLE 172 KINGSPAN GROUP: COMPANY OVERVIEW

- FIGURE 54 KINGSPAN GROUP: COMPANY SNAPSHOT

- TABLE 173 KINGSPAN GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 174 KINGSPAN GROUP: DEALS, JANUARY 2020-MAY 2024

- TABLE 175 KINGSPAN GROUP: EXPANSIONS, JANUARY 2020-MAY 2024

- TABLE 176 KINGSPAN GROUP: OTHERS, JANUARY 2020-MAY 2024

- 12.1.9 KNAUF INSULATION

- TABLE 177 KNAUF INSULATION: COMPANY OVERVIEW

- TABLE 178 KNAUF INSULATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 179 KNAUF INSULATION: EXPANSIONS, JANUARY 2020-MAY 2024

- TABLE 180 KNAUF INSULATION: OTHERS, JANUARY 2020-MAY 2024

- 12.1.10 SOUDAL N.V.

- TABLE 181 SOUDAL N.V.: COMPANY OVERVIEW

- FIGURE 55 SOUDAL N.V.: COMPANY SNAPSHOT

- TABLE 182 SOUDAL N.V.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 183 SOUDAL N.V.: PRODUCT LAUNCHES, JANUARY 2020-MAY 2024

- TABLE 184 SOUDAL N.V.: DEALS, JANUARY 2020-MAY 2024

- 12.1.11 SAINT-GOBAIN

- TABLE 185 SAINT-GOBAIN: COMPANY OVERVIEW

- FIGURE 56 SAINT-GOBAIN: COMPANY SNAPSHOT

- TABLE 186 SAINT-GOBAIN: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 187 SAINT-GOBAIN: DEALS, JANUARY 2020-MAY 2024

- 12.1.12 HUNTSMAN INTERNATIONAL LLC.

- TABLE 188 HUNTSMAN INTERNATIONAL LLC.: COMPANY OVERVIEW

- FIGURE 57 HUNTSMAN INTERNATIONAL LLC.: COMPANY SNAPSHOT

- TABLE 189 HUNTSMAN INTERNATIONAL LLC.: PRODUCT/SOLUTIONS/SERVICES OFFERED

- 12.1.13 DOW

- TABLE 190 DOW: COMPANY OVERVIEW

- FIGURE 58 DOW: COMPANY SNAPSHOT

- TABLE 191 DOW: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 192 DOW: PRODUCT LAUNCHES, JANUARY 2020-MAY 2024

- TABLE 193 DOW: OTHERS, JANUARY 2020-MAY 2024

- 12.2 OTHER PLAYERS

- 12.2.1 SELENA GROUP

- TABLE 194 SELENA GROUP: COMPANY OVERVIEW

- 12.2.2 PAUL BAUDER GMBH & CO. KG

- TABLE 195 PAUL BAUDER GMBH & CO. KG: COMPANY OVERVIEW

- 12.2.3 HELIOS KEMOSTIK, D.O.O.

- TABLE 196 HELIOS KEMOSTIK, D.O.O.: COMPANY OVERVIEW

- 12.2.4 ADFAST

- TABLE 197 ADFAST: COMPANY OVERVIEW

- 12.2.5 INSULFOAM

- TABLE 198 INSULFOAM: COMPANY OVERVIEW

- 12.2.6 CELLOFOAM NORTH AMERICA INC.

- TABLE 199 CELLOFOAM NORTH AMERICA INC.: COMPANY OVERVIEW

- 12.2.7 ATLAS ROOFING CORPORATION

- TABLE 200 ATLAS ROOFING CORPORATION: COMPANY OVERVIEW

- 12.2.8 ICP BUILDING SOLUTIONS GROUP

- TABLE 201 ICP BUILDING SOLUTIONS GROUP: COMPANY OVERVIEW

- 12.2.9 VASMANN

- TABLE 202 VASMANN: COMPANY OVERVIEW

- 12.2.10 BOSTIK

- TABLE 203 BOSTIK: COMPANY OVERVIEW

- 12.2.11 FISCHER GROUP OF COMPANIES

- TABLE 204 FISCHER GROUP OF COMPANIES: COMPANY OVERVIEW

- *Details on Business Overview, Products Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats) might not be captured in case of unlisted companies.

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS