|

|

市場調査レポート

商品コード

1761501

工業用コーティング剤の世界市場:機能別、技術別、樹脂タイプ別、最終用途業界別、地域別 - 2030年までの予測Industrial Coatings Market by type (Acrylic, Alkyd, Polyester, Polyurethane, Epoxy, Fluoropolymer), Technology (Solventborne Coatings, Waterborne Coatings, Powder Coatings), End-use Industry (General Industrial), and Region - Global Forecast to 2030 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 工業用コーティング剤の世界市場:機能別、技術別、樹脂タイプ別、最終用途業界別、地域別 - 2030年までの予測 |

|

出版日: 2025年06月30日

発行: MarketsandMarkets

ページ情報: 英文 346 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

金額ベースでは、工業用コーティング剤の市場規模は、2024年の1,120億4,000万米ドルから2030年には1,423億5,000万米ドルに成長し、2025年~2030年のCAGRは4.12%になると予測されています。

自動車産業における需要の拡大が、工業用コーティング剤市場開拓の主な理由です。防錆、表面耐久性の向上、魅力的な外観といった要因が、自動車にコーティングを施すことの重要性を際立たせています。特に新興産業では、自動車の生産台数が世界的に増加するにつれて、あらゆる必須要件を満たす高度なコーティングの必要性が高まっています。さらに、軽量素材へのシフトと電気自動車への関心の高まりが、最先端コーティングの採用を市場に促しています。自動車セクターの継続的な成長は、工業用コーティング剤の進歩に大きく貢献すると予想されます。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2021年~2030年 |

| 基準年 | 2024年 |

| 予測期間 | 2025年~2030年 |

| 検討単位 | 金額(100万米ドル)および数量(キロトン) |

| セグメント | 機能別、技術別、樹脂タイプ別、最終用途業界別、地域別 |

| 対象地域 | アジア太平洋、欧州、北米、中東・アフリカ、南米 |

工業用コーティング剤市場は粉体塗料への移行が進んでおり、その優れた性能と環境に優しい性質から最も速い成長を記録すると予測されています。粉体塗料は、揮発性有機化合物(VOC)の排出量が非常に少ないため、これらのガスに関する規制が厳しくなるにつれ、人気の高い選択肢となっています。その耐久性、錆びにくさ、印象的な仕上げにより、粉体塗料は自動車、家電製品、家具、工業用途など、さまざまな業界で広く使用されています。さらに、革新的な方法と余った塗料の再利用が可能なため、廃棄物が少なく、コスト効率が向上します。その結果、粉体塗料は予測期間中に急成長を遂げています。

アクリル樹脂は、その汎用性、手頃な価格、多様な塗布方法により、工業用コーティング剤市場で最大のシェアを占めています。主に工業用や自動車用に使用されるアクリル樹脂塗料は、耐候性、鮮やかな発色、速乾性が評価されています。アクリル樹脂は水と溶剤の両方の形態があり、環境および規制当局が定める要件を満たしています。アクリル樹脂は取り扱いが容易であり、様々な産業で利用されていることから、その使用量は世界的に高い水準を維持しています。

工業用コーティング剤の需要が最も急速に増加しているのは、製造業の増加、建築の増加、様々な製品への強力な保護塗料の使用の高まりによる一般工業分野です。この分野には、機械、金属加工、消費財、機器製造が含まれます。これらの産業はすべて、製品を腐食から守ると同時に外観を向上させるコーティングに依存しています。世界的に、特に経済成長国において工業生産が増加していることから、この市場セグメントにおけるコーティング剤の需要は今後数年間で増加すると予想されます。

欧州は、成熟した塗料産業、厳しい環境規制、自動車、一般産業、海洋、建設などの主要な最終用途分野での旺盛な需要により、工業用コーティング剤の金額ベースで第2位の市場となっています。ドイツ、フランス、イタリア、英国は、製造施設やコーティング技術が発達しています。また、同地域は持続可能性に重点を置いており、水系塗料や粉体塗料のような環境にやさしい塗料へのシフトを推進しています。

世界最大の産業の一つである欧州の自動車産業は、高性能工業用コーティング剤、特に耐食性に優れた魅力的な塗料の需要を引き続き牽引しています。さらに、老朽化したインフラの再建と、土木・事業建設への投資の増加が同時に進行しているため、保護塗料の需要も伸びています。しかし、VOCの排出や化学物質の使用に関する厳しい環境規制は、従来の溶剤を使用するコーティングの課題となっており、低VOCや高度な配合へのシフトが進んでいます。欧州は、成熟期にもかかわらず、コーティング市場における技術革新と持続可能な実践の中心地です。これらの要因は、この地域が世界の工業用コーティング剤市場において重要な地位を維持することを保証しています。

当レポートでは、世界の工業用コーティング剤市場について調査し、機能別、技術別、樹脂タイプ別、最終用途業界別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- ポーターのファイブフォース分析

- 主要な利害関係者と購入基準

- 価格分析

- マクロ経済指標

第6章 業界動向

- サプライチェーン分析

- 顧客のビジネスに影響を与える動向と混乱

- エコシステム分析

- 貿易分析

- 技術分析

- ケーススタディ分析

- 規制状況

- 2025年~2027年の主な会議とイベント

- 投資と資金調達のシナリオ

- 特許分析

- AI/生成AIが工業用コーティング剤市場に与える影響

- 2025年の米国関税の影響:工業用コーティング剤市場

第7章 工業用コーティング剤市場(機能別)

- イントロダクション

- 耐食性

- 耐火性

- 耐薬品性

- 耐熱性

- 紫外線耐性

- 防汚

- 静電気防止

- 装飾コーティング

第8章 工業用コーティング剤市場(技術別)

- イントロダクション

- 水性コーティング

- 溶剤系コーティング

- 粉体塗料

- その他

第9章 工業用コーティング剤市場(樹脂タイプ別)

- イントロダクション

- アクリル樹脂

- アルキド樹脂

- エポキシ樹脂

- ポリエステル樹脂

- ポリウレタン樹脂

- フッ素ポリマー樹脂

- その他

第10章 工業用コーティング剤市場(最終用途業界別)

- イントロダクション

- 一般産業

- 保護

- 自動車OEM

- 工業用木材

- 自動車補修

- コイル

- 包装

- 船舶

- 航空宇宙

- 鉄道

第11章 工業用コーティング剤市場(地域別)

- イントロダクション

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- ロシア

- 英国

- フランス

- イタリア

- スペイン

- トルコ

- アジア太平洋

- 中国

- インド

- 日本

- インドネシア

- タイ

- 中東・アフリカ

- GCC

- 南アフリカ

- エジプト

- 南米

- ブラジル

- アルゼンチン

第12章 競合情勢

- イントロダクション

- 主要参入企業の戦略/強み

- 市場シェア分析、2024年

- 2021年~2024年におけるトップ5社の収益分析

- 企業評価マトリックス:主要参入企業、2024年

- 企業評価マトリックス:スタートアップ/中小企業、2024年

- ブランド/製品比較分析

- 企業評価と財務指標

- 競合シナリオ

第13章 企業プロファイル

- 主要参入企業

- AKZO NOBEL N.V.

- AXALTA COATING SYSTEMS LTD.

- JOTUN A/S

- PPG INDUSTRIES, INC.

- THE SHERWIN-WILLIAMS COMPANY

- NIPPON PAINT HOLDINGS CO., LTD

- KANSAI PAINT CO., LTD.

- RPM INTERNATIONAL INC.

- HEMPEL A/S

- THE CHEMOURS COMPANY

- その他の企業

- NOROO PAINT & COATINGS CO., LTD.

- SK KAKEN CO., LTD.

- DAW SE

- TEKNOS GROUP

- TIGER COATINGS GMBH & CO. KG

- ASIAN PAINTS LIMITED

- DIAMOND VOGEL

- ADVANCED NANOTECH LAB

- IGP PULVERTECHNIK AG

- NANOVERE TECHNOLOGIES, LLC.

- NYCOTE

- TEKNOVACE COATINGS PVT LTD

- GRAND POLYCOATS COMPANY PVT. LTD.

- ENDURA COATINGS, LLC

- CHUGOKU MARINE PAINTS, LTD.

第14章 隣接市場と関連市場

第15章 付録

List of Tables

- TABLE 1 INDUSTRIAL COATINGS MARKET: RISK ASSESSMENT

- TABLE 2 INDUSTRIAL COATINGS MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 3 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE MAJOR END-USE SEGMENTS

- TABLE 4 KEY BUYING CRITERIA TOP THREE END-USE INDUSTRIES OF INDUSTRIAL COATINGS

- TABLE 5 AVERAGE SELLING PRICE OF INDUSTRIAL COATINGS OFFERED BY KEY PLAYERS, BY END-USE INDUSTRY, 2024 (USD/KG)

- TABLE 6 GDP TRENDS AND FORECAST OF MAJOR ECONOMIES, 2021-2030 (USD BILLION)

- TABLE 7 INDUSTRIAL COATINGS MARKET: ROLE IN ECOSYSTEM

- TABLE 8 IMPORT DATA OF INDUSTRIAL COATINGS, BY REGION, 2019-2024 (USD MILLION)

- TABLE 9 EXPORT DATA OF INDUSTRIAL COATINGS, BY REGION, 2019-2024 (USD MILLION)

- TABLE 10 GLOBAL: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 SOUTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 MIDDLE EAST & AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 INDUSTRIAL COATINGS MARKET: DETAILED LIST OF CONFERENCES & EVENTS

- TABLE 17 INDUSTRIAL COATINGS MARKET: FUNDING/INVESTMENT SCENARIO, 2020-2024

- TABLE 18 INDUSTRIAL COATING MATERIALS MARKET: PATENT STATUS, 2014-2024

- TABLE 19 INDUSTRIAL COATINGS MARKET: LIST OF MAJOR PATENTS, 2014-2024

- TABLE 20 PATENTS BY BASF SE, 2024

- TABLE 21 TOP 10 PATENT OWNERS IN US, 2014-2024

- TABLE 22 US ADJUSTED RECIPROCAL TARIFF RATES

- TABLE 23 INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 24 INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 25 INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 26 INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 27 WATERBORNE: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 28 WATERBORNE: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 29 WATERBORNE: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 30 WATERBORNE: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 31 SOLVENTBORNE: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 32 SOLVENTBORNE: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 33 SOLVENTBORNE: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 34 SOLVENTBORNE: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 35 POWDER COATINGS: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 36 POWDER COATINGS: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 37 POWDER COATINGS: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 38 POWDER COATINGS: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 39 OTHERS: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 40 OTHERS: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 41 OTHERS: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 42 OTHERS: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 43 INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2020-2024 (USD MILLION)

- TABLE 44 INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2025-2030 (USD MILLION)

- TABLE 45 INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2020-2024 (KILOTON)

- TABLE 46 INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2025-2030 (KILOTON)

- TABLE 47 ACRYLIC: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 48 ACRYLIC: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 49 ACRYLIC: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 50 ACRYLIC: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 51 ALKYD: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 52 ALKYD: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 53 ALKYD: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 54 ALKYD: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 55 EPOXY: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 56 EPOXY: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 57 EPOXY: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 58 EPOXY: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 59 POLYESTER: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 60 POLYESTER: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 61 POLYESTER: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 62 POLYESTER: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 63 POLYURETHANE: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 64 POLYURETHANE: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 65 POLYURETHANE: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 66 POLYURETHANE: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 67 FLUOROPOLYMER: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 68 FLUOROPOLYMER: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 69 FLUOROPOLYMER: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 70 FLUOROPOLYMER: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 71 OTHER RESIN TYPES: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 72 OTHER RESIN TYPES: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 73 OTHER RESIN TYPES: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 74 OTHER RESIN TYPES: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 75 INDUSTRIAL COATINGS: END-USE INDUSTRY AND APPLICATION

- TABLE 76 INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2020-2024 (USD MILLION)

- TABLE 77 INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 78 INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2020-2024 (KILOTON)

- TABLE 79 INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 80 GENERAL INDUSTRIAL: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 81 GENERAL INDUSTRIAL: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 82 GENERAL INDUSTRIAL: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 83 GENERAL INDUSTRIAL: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 84 PROTECTIVE: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 85 PROTECTIVE: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 86 PROTECTIVE: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 87 PROTECTIVE: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 88 AUTOMOTIVE OEM: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 89 AUTOMOTIVE OEM: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 90 AUTOMOTIVE OEM: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 91 AUTOMOTIVE OEM: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 92 INDUSTRIAL WOOD: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 93 INDUSTRIAL WOOD: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 94 INDUSTRIAL WOOD: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 95 INDUSTRIAL WOOD: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 96 KEY PLAYERS IN AUTOMOTIVE REFINISH COATINGS MARKET

- TABLE 97 AUTOMOTIVE REFINISH: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 98 AUTOMOTIVE REFINISH: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 99 AUTOMOTIVE REFINISH: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 100 AUTOMOTIVE REFINISH: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 101 COIL: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 102 COIL: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 103 COIL: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 104 COIL: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 105 PACKAGING: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 106 PACKAGING: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 107 PACKAGING: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 108 PACKAGING: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 109 MARINE: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 110 MARINE: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 111 MARINE: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 112 MARINE: INDUSTRIAL COATINGS MARKET, BY REGION, 2023-2028 (KILOTON)

- TABLE 113 AEROSPACE: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 114 AEROSPACE: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 115 AEROSPACE: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 116 AEROSPACE: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 117 RAIL: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 118 RAIL: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 119 RAIL: INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 120 RAIL: INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 121 INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 122 INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 123 INDUSTRIAL COATINGS MARKET, BY REGION, 2020-2024 (KILOTON)

- TABLE 124 INDUSTRIAL COATINGS MARKET, BY REGION, 2025-2030 (KILOTON)

- TABLE 125 NORTH AMERICA: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2020-2024 (USD MILLION)

- TABLE 126 NORTH AMERICA: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2025-2030 (USD MILLION)

- TABLE 127 NORTH AMERICA: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2020-2024 (KILOTON)

- TABLE 128 NORTH AMERICA: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2025-2030 (KILOTON)

- TABLE 129 NORTH AMERICA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 130 NORTH AMERICA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 131 NORTH AMERICA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 132 NORTH AMERICA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 133 NORTH AMERICA: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2020-2024 (USD MILLION)

- TABLE 134 NORTH AMERICA: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 135 NORTH AMERICA: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2020-2024 (KILOTON)

- TABLE 136 NORTH AMERICA: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 137 NORTH AMERICA: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 138 NORTH AMERICA: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 139 NORTH AMERICA: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2020-2024 (KILOTON)

- TABLE 140 NORTH AMERICA: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 141 US: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 142 US: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 143 US: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 144 US: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 145 CANADA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 146 CANADA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 147 CANADA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 148 CANADA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 149 MEXICO: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 150 MEXICO: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 151 MEXICO: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 152 MEXICO: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 153 EUROPE: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2020-2024 (USD MILLION)

- TABLE 154 EUROPE: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2025-2030 (USD MILLION)

- TABLE 155 EUROPE: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2020-2024 (KILOTON)

- TABLE 156 EUROPE: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2025-2030 (KILOTON)

- TABLE 157 EUROPE: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 158 EUROPE: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 159 EUROPE: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 160 EUROPE: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 161 EUROPE: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2020-2024 (USD MILLION)

- TABLE 162 EUROPE: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 163 EUROPE: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2020-2024 (KILOTON)

- TABLE 164 EUROPE: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 165 EUROPE: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 166 EUROPE: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 167 EUROPE: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2020-2024 (KILOTON)

- TABLE 168 EUROPE: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 169 GERMANY: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 170 GERMANY: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 171 GERMANY: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 172 GERMANY: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 173 RUSSIA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 174 RUSSIA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 175 RUSSIA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 176 RUSSIA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 177 UK: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 178 UK: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 179 UK: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 180 UK: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 181 FRANCE: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 182 FRANCE: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 183 FRANCE: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 184 FRANCE: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 185 ITALY: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 186 ITALY: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 187 ITALY: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 188 ITALY: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 189 SPAIN: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 190 SPAIN: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 191 SPAIN: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 192 SPAIN: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 193 TURKEY: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 194 TURKEY: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 195 TURKEY: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 196 TURKEY: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 197 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2020-2024 (USD MILLION)

- TABLE 198 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2025-2030 (USD MILLION)

- TABLE 199 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2020-2024 (KILOTON)

- TABLE 200 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2025-2030 (KILOTON)

- TABLE 201 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 202 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 203 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 204 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 205 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2020-2024 (USD MILLION)

- TABLE 206 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 207 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2020-2024 (KILOTON)

- TABLE 208 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 209 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 210 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 211 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2020-2024 (KILOTON)

- TABLE 212 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 213 CHINA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 214 CHINA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 215 CHINA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 216 CHINA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 217 INDIA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 218 INDIA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 219 INDIA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 220 INDIA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 221 JAPAN: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 222 JAPAN: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 223 JAPAN: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 224 JAPAN: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 225 INDONESIA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 226 INDONESIA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 227 INDONESIA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 228 INDONESIA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 229 THAILAND: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 230 THAILAND: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 231 THAILAND: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 232 THAILAND: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 233 MIDDLE EAST & AFRICA: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2020-2024 (USD MILLION)

- TABLE 234 MIDDLE EAST & AFRICA: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2025-2030 (USD MILLION)

- TABLE 235 MIDDLE EAST & AFRICA: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2020-2024 (KILOTON)

- TABLE 236 MIDDLE EAST & AFRICA: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2025-2030 (KILOTON)

- TABLE 237 MIDDLE EAST & AFRICA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 238 MIDDLE EAST & AFRICA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 239 MIDDLE EAST & AFRICA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 240 MIDDLE EAST & AFRICA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 241 MIDDLE EAST & AFRICA: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2020-2024 (USD MILLION)

- TABLE 242 MIDDLE EAST & AFRICA: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 243 MIDDLE EAST & AFRICA: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2020-2024 (KILOTON)

- TABLE 244 MIDDLE EAST & AFRICA: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 245 MIDDLE EAST & AFRICA: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 246 MIDDLE EAST & AFRICA: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 247 MIDDLE EAST & AFRICA: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2020-2024 (KILOTON)

- TABLE 248 MIDDLE EAST & AFRICA: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 249 SAUDI ARABIA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 250 SAUDI ARABIA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 251 SAUDI ARABIA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 252 SAUDI ARABIA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 253 UAE: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 254 UAE: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 255 UAE: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 256 UAE: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 257 SOUTH AFRICA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 258 SOUTH AFRICA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 259 SOUTH AFRICA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 260 SOUTH AFRICA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 261 EGYPT: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 262 EGYPT: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 263 EGYPT: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 264 EGYPT: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 265 SOUTH AMERICA: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2020-2024 (USD MILLION)

- TABLE 266 SOUTH AMERICA: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2025-2030 (USD MILLION)

- TABLE 267 SOUTH AMERICA: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2020-2024 (KILOTON)

- TABLE 268 SOUTH AMERICA: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE, 2025-2030 (KILOTON)

- TABLE 269 SOUTH AMERICA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 270 SOUTH AMERICA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 271 SOUTH AMERICA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 272 SOUTH AMERICA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 273 SOUTH AMERICA: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2020-2024 (USD MILLION)

- TABLE 274 SOUTH AMERICA: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 275 SOUTH AMERICA: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2020-2024 (KILOTON)

- TABLE 276 SOUTH AMERICA: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY, 2025-2030 (KILOTON)

- TABLE 277 SOUTH AMERICA: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 278 SOUTH AMERICA: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 279 SOUTH AMERICA: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2020-2024 (KILOTON)

- TABLE 280 SOUTH AMERICA: INDUSTRIAL COATINGS MARKET, BY COUNTRY, 2025-2030 (KILOTON)

- TABLE 281 BRAZIL: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 282 BRAZIL: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 283 BRAZIL: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 284 BRAZIL: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 285 ARGENTINA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (USD MILLION)

- TABLE 286 ARGENTINA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 287 ARGENTINA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2020-2024 (KILOTON)

- TABLE 288 ARGENTINA: INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY, 2025-2030 (KILOTON)

- TABLE 289 STRATEGIES ADOPTED BY KEY INDUSTRIAL COATING MANUFACTURERS, JANUARY 2019-JANUARY 2025

- TABLE 290 INDUSTRIAL COATINGS MARKET: DEGREE OF COMPETITION

- TABLE 291 INDUSTRIAL COATINGS MARKET: REGION FOOTPRINT

- TABLE 292 INDUSTRIAL COATINGS MARKET: RESIN TYPE FOOTPRINT

- TABLE 293 INDUSTRIAL COATINGS MARKET: TECHNOLOGY FOOTPRINT

- TABLE 294 INDUSTRIAL COATINGS MARKET: END-USE INDUSTRY FOOTPRINT

- TABLE 295 INDUSTRIAL COATINGS MARKET: KEY STARTUPS/SMES

- TABLE 296 INDUSTRIAL COATINGS MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 297 INDUSTRIAL COATINGS MARKET: PRODUCT LAUNCHES, JANUARY 2019-JANUARY 2025

- TABLE 298 INDUSTRIAL COATINGS MARKET: DEALS, JANUARY 2019-JANUARY 2025

- TABLE 299 INDUSTRIAL COATINGS MARKET: EXPANSIONS, JANUARY 2019-JANUARY 2025

- TABLE 300 INDUSTRIAL COATINGS MARKET: OTHER DEVELOPMENTS, JANUARY 2019-JANUARY 2025

- TABLE 301 AKZONOBEL N.V.: COMPANY OVERVIEW

- TABLE 302 AKZO NOBEL N.V.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 303 AKZO NOBEL N.V.: PRODUCT LAUNCHES, JANUARY 2029-JANUARY 2025

- TABLE 304 AKZO NOBEL N.V.: DEALS, JANUARY 2029-JANUARY 2025

- TABLE 305 AKZO NOBEL N.V.: EXPANSIONS, JANUARY 2029-JANUARY 2025

- TABLE 306 AKZO NOBEL N.V.: OTHER DEVELOPMENTS, JANUARY 2029-JANUARY 2025

- TABLE 307 AXALTA COATING SYSTEMS LTD.: COMPANY OVERVIEW

- TABLE 308 AXALTA COATING SYSTEMS LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 309 AXALTA COATING SYSTEMS LTD.: PRODUCT LAUNCHES, JANUARY 2029-JANUARY 2025

- TABLE 310 AXALTA COATING SYSTEMS LTD.: DEALS, JANUARY 2029-JANUARY 2025

- TABLE 311 AXALTA COATING SYSTEMS LTD.: EXPANSIONS, JANUARY 2029-JANUARY 2025

- TABLE 312 AXALTA COATING SYSTEMS LTD.: OTHER DEVELOPMENTS, JANUARY 2029-JANUARY 2025

- TABLE 313 JOTUN A/S: COMPANY OVERVIEW

- TABLE 314 JOTUN A/S: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 315 JOTUN A/S: PRODUCT LAUNCHES, JANUARY 2029-JANUARY 2025

- TABLE 316 JOTUN A/S: DEALS, JANUARY 2029-JANUARY 2025

- TABLE 317 JOTUN A/S: EXPANSIONS, JANUARY 2029-JANUARY 2025

- TABLE 318 JOTUN A/S: OTHER DEVELOPMENTS, JANUARY 2029-JANUARY 2025

- TABLE 319 PPG INDUSTRIES, INC.: COMPANY OVERVIEW

- TABLE 320 PPG INDUSTRIES, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 321 PPG INDUSTRIES, INC.: PRODUCT LAUNCHES, JANUARY 2029-JANUARY 2025

- TABLE 322 PPG INDUSTRIES, INC.: DEALS, JANUARY 2029-JANUARY 2025

- TABLE 323 PPG INDUSTRIES, INC.: EXPANSIONS, JANUARY 2029-JANUARY 2025

- TABLE 324 PPG INDUSTRIES, INC.: OTHER DEVELOPMENTS, JANUARY 2029-JANUARY 2025

- TABLE 325 THE SHERWIN-WILLIAMS COMPANY: COMPANY OVERVIEW

- TABLE 326 THE SHERWIN-WILLIAMS COMPANY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 327 THE SHERWIN-WILLIAMS COMPANY: PRODUCT LAUNCHES, JANUARY 2029-JANUARY 2025

- TABLE 328 THE SHERWIN-WILLIAMS COMPANY: DEALS, JANUARY 2029-JANUARY 2025

- TABLE 329 NIPPON PAINT HOLDINGS CO., LTD: COMPANY OVERVIEW

- TABLE 330 NIPPON PAINT HOLDINGS CO., LTD: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 331 NIPPON PAINT HOLDINGS CO., LTD: PRODUCT LAUNCHES, JANUARY 2029-JANUARY 2025

- TABLE 332 NIPPON PAINT HOLDINGS CO., LTD: DEALS, JANUARY 2029-JANUARY 2025

- TABLE 333 NIPPON PAINTS HOLDINGS CO., LTD.: EXPANSIONS, JANUARY 2029-JANUARY 2025

- TABLE 334 KANSAI PAINT CO., LTD.: COMPANY OVERVIEW

- TABLE 335 KANSAI PAINT CO., LTD.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 336 KANSAI PAINT CO., LTD.: DEALS, JANUARY 2029-JANUARY 2025

- TABLE 337 RPM INTERNATIONAL INC.: COMPANY OVERVIEW

- TABLE 338 RPM INTERNATIONAL INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 339 RPM INTERNATIONAL INC.: EXPANSIONS, JANUARY 2029-JANUARY 2025

- TABLE 340 HEMPEL A/S: COMPANY OVERVIEW

- TABLE 341 HEMPEL A/S: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 342 HEMPEL A/S: PRODUCT LAUNCHES, JANUARY 2029-JANUARY 2025

- TABLE 343 HEMPEL A/S: DEALS, JANUARY 2029-JANUARY 2025

- TABLE 344 HEMPEL A/S: EXPANSIONS, JANUARY 2029-JANUARY 2025

- TABLE 345 HEMPEL A/S: OTHER DEVELOPMENTS, JANUARY 2029-JANUARY 2025

- TABLE 346 THE CHEMOURS COMPANY: COMPANY OVERVIEW

- TABLE 347 THE CHEMOURS COMPANY: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 348 NOROO PAINT & COATINGS CO., LTD.: COMPANY OVERVIEW

- TABLE 349 SK KAKEN CO., LTD.: COMPANY OVERVIEW

- TABLE 350 DAW SE: COMPANY OVERVIEW, JANUARY 2029-JANUARY 2025

- TABLE 351 TEKNOS GROUP: COMPANY OVERVIEW

- TABLE 352 TIGER COATINGS GMBH & CO. KG: COMPANY OVERVIEW

- TABLE 353 ASIAN PAINTS LIMITED: COMPANY OVERVIEW

- TABLE 354 DIAMOND VOGEL: COMPANY OVERVIEW

- TABLE 355 ADVANCED NANOTECH LAB: COMPANY OVERVIEW

- TABLE 356 IGP PULVERTECHNIK AG: COMPANY OVERVIEW

- TABLE 357 NANOVERE TECHNOLOGIES, LLC.: COMPANY OVERVIEW

- TABLE 358 NYCOTE: COMPANY OVERVIEW

- TABLE 359 TEKNOVACE COATINGS PVT LTD: COMPANY OVERVIEW

- TABLE 360 GRAND POLYCOATS COMPANY PVT. LTD.: COMPANY OVERVIEW

- TABLE 361 ENDURA COATINGS, LLC: COMPANY OVERVIEW

- TABLE 362 CHUGOKU MARINE PAINTS, LTD.: COMPANY OVERVIEW

- TABLE 363 ARCHITECTURAL COATINGS MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 364 ARCHITECTURAL COATINGS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 365 ARCHITECTURAL COATINGS MARKET, BY REGION, 2019-2022 (KILOTON)

- TABLE 366 ARCHITECTURAL COATINGS MARKET, BY REGION, 2023-2028 (KILOTON)

- TABLE 367 ASIA PACIFIC: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 368 ASIA PACIFIC: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 369 ASIA PACIFIC: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2019-2022 (KILOTON)

- TABLE 370 ASIA PACIFIC: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- TABLE 371 EUROPE: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 372 EUROPE: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 373 EUROPE: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2019-2022 (KILOTON)

- TABLE 374 EUROPE: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- TABLE 375 NORTH AMERICA: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 376 NORTH AMERICA: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 377 NORTH AMERICA: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2019-2022 (KILOTON)

- TABLE 378 NORTH AMERICA: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- TABLE 379 MIDDLE EAST & AFRICA: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 380 MIDDLE EAST & AFRICA: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 381 MIDDLE EAST & AFRICA: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2019-2022 (KILOTON)

- TABLE 382 MIDDLE EAST & AFRICA: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- TABLE 383 SOUTH AMERICA: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 384 SOUTH AMERICA: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 385 SOUTH AMERICA: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2019-2022 (KILOTON)

- TABLE 386 SOUTH AMERICA: ARCHITECTURAL COATINGS MARKET, BY COUNTRY, 2023-2028 (KILOTON)

List of Figures

- FIGURE 1 INDUSTRIAL COATINGS MARKET SEGMENTATION AND REGIONAL SCOPE

- FIGURE 2 INDUSTRIAL COATINGS MARKET: RESEARCH DESIGN

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY - APPROACH 1 (SUPPLY SIDE): COLLECTIVE REVENUE OF KEY PLAYERS

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 1 (SUPPLY SIDE): COLLECTIVE MARKET SHARE OF KEY PLAYERS

- FIGURE 5 MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- FIGURE 6 INDUSTRIAL COATINGS MARKET SIZE ESTIMATION, BY VALUE AND VOLUME

- FIGURE 7 INDUSTRIAL COATINGS MARKET SIZE ESTIMATION, BY REGION

- FIGURE 8 INDUSTRIAL COATINGS MARKET: DATA TRIANGULATION

- FIGURE 9 MARKET CAGR PROJECTIONS FROM SUPPLY SIDE

- FIGURE 10 MARKET GROWTH PROJECTIONS FROM DEMAND-SIDE DRIVERS AND OPPORTUNITIES

- FIGURE 11 EPOXY RESIN SEGMENT ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

- FIGURE 12 SOLVENTBORNE COATINGS TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 13 GENERAL INDUSTRIAL SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 14 ASIA PACIFIC ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

- FIGURE 15 RAPID URBANIZATION TO CREATE GROWTH OPPORTUNITIES FOR MARKET PLAYERS

- FIGURE 16 ASIA PACIFIC TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 17 CHINA AND GENERAL INDUSTRIAL SEGMENT ACCOUNTED FOR LARGEST SHARE OF ASIA PACIFIC MARKET IN 2024

- FIGURE 18 ACRYLIC RESIN SEGMENT LED INDUSTRIAL COATINGS MARKET IN MOST REGIONS

- FIGURE 19 INDIA TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- FIGURE 20 INDUSTRIAL COATINGS MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 21 PORTER'S FIVE FORCES ANALYSIS: INDUSTRIAL COATINGS MARKET

- FIGURE 22 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END-USE INDUSTRIES

- FIGURE 23 KEY BUYING CRITERIA FOR TOP THREE END-USE INDUSTRIES IN INDUSTRIAL COATINGS

- FIGURE 24 AVERAGE SELLING PRICE OF INDUSTRIAL COATINGS OFFERED BY KEY PLAYERS, BY END-USE INDUSTRY, 2024 (USD/KG)

- FIGURE 25 AVERAGE SELLING PRICE TREND OF INDUSTRIAL COATINGS, BY REGION, 2022-2030

- FIGURE 26 INDUSTRIAL COATINGS MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 27 TRENDS IN END-USE INDUSTRIES IMPACTING BUSINESS OF INDUSTRIAL COATING MANUFACTURERS

- FIGURE 28 INDUSTRIAL COATINGS MARKET: KEY PLAYERS IN ECOSYSTEM

- FIGURE 29 IMPORT DATA OF INDUSTRIAL COATINGS, BY KEY COUNTRY, 2019-2024

- FIGURE 30 EXPORT DATA OF INDUSTRIAL COATINGS, BY KEY COUNTRY, 2020-2024

- FIGURE 31 PATENTS REGISTERED RELATED TO INDUSTRIAL COATINGS MATERIALS, 2014-2024

- FIGURE 32 TOP PATENT OWNERS, 2014-2024

- FIGURE 33 LEGAL STATUS OF PATENTS FILED FOR INDUSTRIAL COATINGS, 2014-2024

- FIGURE 34 MAJOR PATENTS FILED IN JURISDICTION OF US, 2014-2024

- FIGURE 35 INDUSTRIAL COATINGS MARKET: IMPACT OF AI/GEN AI

- FIGURE 36 SOLVENTBORNE TECHNOLOGY TO LEAD INDUSTRIAL COATINGS MARKET BETWEEN 2025 AND 2030

- FIGURE 37 EPOXY TO BE LARGEST RESIN TYPE FOR INDUSTRIAL COATINGS DURING FORECAST PERIOD

- FIGURE 38 GENERAL INDUSTRIAL TO BE LARGEST END USER OF INDUSTRIAL COATINGS DURING FORECAST PERIOD

- FIGURE 39 ASIA PACIFIC TO BE FASTEST-GROWING INDUSTRIAL COATINGS MARKET DURING FORECAST PERIOD

- FIGURE 40 NORTH AMERICA: INDUSTRIAL COATINGS MARKET SNAPSHOT

- FIGURE 41 EUROPE: INDUSTRIAL COATINGS MARKET SNAPSHOT

- FIGURE 42 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET SNAPSHOT

- FIGURE 43 MARKET SHARE ANALYSIS OF TOP FIVE PLAYERS, 2024

- FIGURE 44 REVENUE ANALYSIS OF KEY COMPANIES OF INDUSTRIAL COATINGS, 2021-2024

- FIGURE 45 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- FIGURE 46 INDUSTRIAL COATINGS MARKET: COMPANY FOOTPRINT

- FIGURE 47 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- FIGURE 48 BRAND/PRODUCT COMPARISON

- FIGURE 49 INDUSTRIAL COATINGS MARKET: EV/EBITDA OF KEY MANUFACTURERS

- FIGURE 50 INDUSTRIAL COATINGS MARKET: ENTERPRISE VALUATION (EV) OF KEY PLAYERS

- FIGURE 51 AKZO NOBEL N.V.: COMPANY SNAPSHOT

- FIGURE 52 AXALTA COATING SYSTEMS LTD.: COMPANY SNAPSHOT

- FIGURE 53 JOTUN A/S: COMPANY SNAPSHOT

- FIGURE 54 PPG INDUSTRIES, INC.: COMPANY SNAPSHOT

- FIGURE 55 THE SHERWIN-WILLIAMS COMPANY: COMPANY SNAPSHOT

- FIGURE 56 NIPPON PAINT HOLDINGS CO., LTD: COMPANY SNAPSHOT

- FIGURE 57 KANSAI PAINT CO., LTD.: COMPANY SNAPSHOT

- FIGURE 58 RPM INTERNATIONAL INC.: COMPANY SNAPSHOT

- FIGURE 59 HEMPEL A/S: COMPANY SNAPSHOT

- FIGURE 60 THE CHEMOURS COMPANY: COMPANY SNAPSHOT

In terms of value, the industrial coatings market is estimated to grow from USD 112.04 billion in 2024 to USD 142.35 billion by 2030, at a CAGR of 4.12% between 2025 and 2030. The growing demand in the automotive industry is a primary reason for the increased development of the industrial coatings market. Factors such as rust protection, more durable surfaces, and attractive appearances highlight the importance of applying coatings in automobiles. As vehicle production rises globally, particularly in emerging industries, there is a greater need for advanced coatings that fulfill all essential requirements. Additionally, the shift toward lighter materials and a heightened interest in electric vehicles are driving the market to adopt cutting-edge coatings. Continued growth in the automotive sector is expected to significantly contribute to the advancement of industrial coatings.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Million) and Volume (Kiloton) |

| Segments | Resin Type, Technology, End-use Industry, and Region |

| Regions covered | Asia Pacific, Europe, North America, Middle East & Africa, and South America |

"Powder coating technology segment is projected to register the highest CAGR in the industrial coatings market, in terms of value, during the forecast period."

The industrial coatings market is increasingly shifting towards powder coatings, which are projected to register the fastest growth due to their excellent performance and environmentally friendly nature. Powder coatings emit very low levels of volatile organic compounds (VOCs), making them a popular choice as regulations on these gases become stricter. Their durability, resistance to rust, and impressive finishes make powder coatings widely used in various industries, including automotive, appliances, furniture, and industrial applications. Additionally, innovative methods and the ability to reuse leftover paint result in less waste and enhanced cost-efficiency. As a result, powder coatings are experiencing rapid growth during the forecast period.

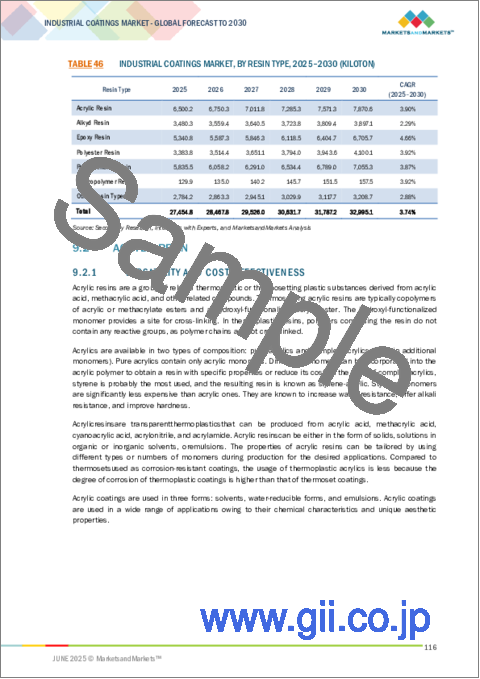

"Acrylic resin segment accounted for the largest market share, in terms of volume, in 2024."

Acrylic resin holds the largest share of the industrial coatings market due to its versatility, affordability, and various application methods. Primarily used for industrial and automotive purposes, acrylic coatings are praised for their weather resistance, vibrant colors, and quick drying times. They can exist in both water and solvent forms, meeting the requirements set by environmental and regulatory authorities. Given that acrylic resins are easy to handle and utilized across multiple industries, their usage remains significantly high across the market world.

"General Industrial segment accounted for the largest market share, in terms of volume, in 2024."

The fastest rise in demand for industrial coatings is observed in the general industrial sector due to increased manufacturing, more construction, and a heightened use of strong, protective coatings for various products. This segment encompasses machinery, metal fabrication, consumer goods, and equipment manufacturing. All these industries rely on coatings that protect their products from corrosion while enhancing their appearance. With industrial production rising globally, particularly in economically growing countries, the demand for coatings in this market segment is expected to increase in the coming years.

"Europe accounted for the second-largest share of the overall industrial coatings market, in terms of value, in 2024."

Europe is the second-largest market in terms of value for industrial coatings due to its mature coating industry, strict environmental regulations, and strong demand in major end-use segments such as automotive, general industrial, marine, and construction. Leading countries in demand include Germany, France, Italy, and the UK, which have well-developed manufacturing facilities and coating technologies. The region is also highly focused on sustainability, driving the shift toward environmentally friendly coating systems like waterborne coatings and powder coatings, which is boosting investments in R&D and the development of environmentally compliant products.

The European automotive industry, one of the largest industries worldwide, continues to drive demand for high-performance industrial coatings, particularly those that are corrosion-resistant and attractive. Moreover, the demand for protective coatings is growing because of the simultaneous reconstruction of outdated infrastructure and the growth of investments in civil and business construction. Strict environmental rules regarding VOC emissions and the use of chemicals have, however, challenged conventional solvent-borne coating, and the shift has been toward low-VOC and advanced formulations. Europe is a center for innovation and sustainable practices in the coatings market despite the latter's maturity. These factors guarantee that the region will remain a significant force in the global industrial coatings market.

- By Company Type: Tier 1 - 55%, Tier 2 - 25%, and Tier 3 - 20%

- By Designation: Directors - 50%, Managers - 30%, and Others - 20%

- By Region: North America - 40%, Europe - 35%, Asia Pacific - 20%, and the Rest of the World - 5%

The key players profiled in the report include The Sherwin-Willaims Company (US), PPG Industries Inc. (US), AkzoNobel N.V. (Netherlands), Axalta Coating Systems LLC (US), Jotun A/S (Norway), Nippon Paint Holdings Co., Ltd. (Japan), Kansai Paint Co., Ltd. (Japan), RPM International Inc. (US), Hempel A/S (Denmark), and BASF Coatings GmbH (Germany).

Research Coverage

This report segments the market for industrial coatings based on resin type, technology, end-use industry, and region, and provides estimations of value (USD million) for the overall market size across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, services, and key strategies associated with the market for water-based barrier coatings.

Reasons to Buy this Report

This research report is focused on various levels of analysis-industry analysis (industry trends), market share analysis of top players, and company profiles. Together, these provide an overall view of the competitive landscape, emerging and high-growth segments of the industrial coatings market, high-growth regions, and market drivers, restraints, and opportunities.

The report provides insights on the following pointers:

- Market Penetration: Comprehensive information on industrial coatings offered by top players in the global market.

- Analysis of key drivers (increasing demand from the automotive industry, environmental regulations boosting the demand for VOC-free coatings, technological advancements in powder coatings, and the growing demand from Asia), restraints (high drying time for waterborne coatings and difficulty in obtaining thin films in powder coatings), opportunities (increasing use of nanocoatings and attractive prospects for powder coatings in the shipbuilding and pipeline sector), and challenges (stringent regulatory policies) influencing the growth of the industrial coatings market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the industrial coatings market

- Market Development: Comprehensive information about lucrative emerging markets - the report analyzes the markets for industrial coatings across regions.

- Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global industrial coatings market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the industrial coatings market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 MARKET DEFINITION AND INCLUSIONS, BY RESIN TYPE

- 1.3.4 MARKET DEFINITION AND INCLUSIONS, BY TECHNOLOGY

- 1.3.5 MARKET DEFINITION AND INCLUSIONS, BY END-USE INDUSTRY

- 1.3.6 YEARS CONSIDERED

- 1.3.7 CURRENCY CONSIDERED

- 1.3.8 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key primary participants

- 2.1.2.2 Key industry insights

- 2.1.2.3 Breakdown of primary interviews

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- 2.4 GROWTH FORECAST

- 2.4.1 SUPPLY-SIDE ANALYSIS

- 2.4.2 DEMAND-SIDE ANALYSIS

- 2.5 ASSUMPTIONS

- 2.6 LIMITATIONS

- 2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN INDUSTRIAL COATINGS MARKET

- 4.2 INDUSTRIAL COATINGS MARKET, BY REGION

- 4.3 ASIA PACIFIC: INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY AND COUNTRY

- 4.4 REGIONAL ANALYSIS: INDUSTRIAL COATINGS MARKET, BY RESIN TYPE

- 4.5 INDUSTRIAL COATINGS MARKET ATTRACTIVENESS

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Stringent environmental regulations boosting demand for VOC-free coatings

- 5.2.1.2 Increasing demand from automotive industry

- 5.2.1.3 Advancements in performance of industrial coatings

- 5.2.1.4 Rapid industrialization in Asia Pacific

- 5.2.1.5 High demand for extended product lifetime and reduced maintenance

- 5.2.2 RESTRAINTS

- 5.2.2.1 Difficulty in achieving thin films with powder coatings

- 5.2.2.2 Longer drying time of waterborne coatings

- 5.2.2.3 Volatility in raw material prices of specialty additives and advanced coatings

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increasing demand for powder coatings in shipbuilding and pipeline sectors

- 5.2.3.2 Increasing use of nano-coatings

- 5.2.4 CHALLENGES

- 5.2.4.1 Stringent regulatory policies

- 5.2.1 DRIVERS

- 5.3 PORTER'S FIVE FORCES ANALYSIS

- 5.3.1 THREAT OF NEW ENTRANTS

- 5.3.2 THREAT OF SUBSTITUTES

- 5.3.3 BARGAINING POWER OF SUPPLIERS

- 5.3.4 BARGAINING POWER OF BUYERS

- 5.3.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.4 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.4.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.4.2 BUYING CRITERIA

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF INDUSTRIAL COATINGS OFFERED BY KEY PLAYERS, BY END-USE INDUSTRY, 2024

- 5.5.2 AVERAGE SELLING PRICE TREND OF INDUSTRIAL COATINGS, BY REGION, 2022-2030

- 5.6 MACROECONOMIC INDICATORS

- 5.6.1 GDP TRENDS AND FORECAST

6 INDUSTRY TRENDS

- 6.1 SUPPLY CHAIN ANALYSIS

- 6.2 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 6.3 ECOSYSTEM ANALYSIS

- 6.4 TRADE ANALYSIS

- 6.4.1 IMPORT SCENARIO (HS CODE 3209)

- 6.4.2 EXPORT SCENARIO

- 6.5 TECHNOLOGY ANALYSIS

- 6.5.1 KEY TECHNOLOGIES

- 6.5.1.1 Innovation in coatings

- 6.5.2 COMPLEMENTARY TECHNOLOGIES

- 6.5.2.1 Self-healing materials

- 6.5.2.2 High-performance thin-film composites

- 6.5.1 KEY TECHNOLOGIES

- 6.6 CASE STUDY ANALYSIS

- 6.6.1 HIGH-QUALITY POWDER COATING FOR ENERGY SECTOR

- 6.6.2 POWDER COATING PARTS ECONOMICALLY IN AUTOMOTIVE QUALITY

- 6.7 REGULATORY LANDSCAPE

- 6.7.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.7.2 MAJOR REGULATORY BODIES

- 6.7.3 REGULATORY FRAMEWORK

- 6.7.3.1 REACH: Ensuring safe use of chemicals

- 6.7.3.2 Global Automotive Declarable Substance List (GADSL)

- 6.7.3.3 End-of-Life Vehicle (ELV) directive

- 6.7.3.4 International Material Data System (IMDS)

- 6.8 KEY CONFERENCES & EVENTS IN 2025-2027

- 6.9 INVESTMENT AND FUNDING SCENARIO

- 6.10 PATENT ANALYSIS

- 6.10.1 APPROACH

- 6.10.2 PATENT TYPES

- 6.10.3 TOP APPLICANTS

- 6.10.4 JURISDICTION ANALYSIS

- 6.11 IMPACT OF AI/GEN AI ON INDUSTRIAL COATINGS MARKET

- 6.12 IMPACT OF 2025 US TARIFF: INDUSTRIAL COATINGS MARKET

- 6.12.1 INTRODUCTION

- 6.12.2 KEY TARIFF RATES

- 6.12.3 PRICE IMPACT ANALYSIS

- 6.12.4 IMPACT ON COUNTRY/REGION

- 6.12.4.1 US

- 6.12.4.2 Europe

- 6.12.4.3 Asia Pacific

- 6.12.5 IMPACT ON END-USE INDUSTRY

7 INDUSTRIAL COATINGS MARKET, BY FUNCTIONALITY

- 7.1 INTRODUCTION

- 7.2 CORROSION RESISTANCE

- 7.3 FIRE RESISTANCE

- 7.4 CHEMICAL RESISTANCE

- 7.5 HEAT RESISTANCE

- 7.6 UV RESISTANCE

- 7.7 ANTI-FOULING

- 7.8 ANTI-STATIC

- 7.9 DECORATIVE COATINGS

8 INDUSTRIAL COATINGS MARKET, BY TECHNOLOGY

- 8.1 INTRODUCTION

- 8.2 WATERBORNE COATINGS

- 8.2.1 INCREASING DEMAND DUE TO EXCELLENT ADHESION AND LOW VOC EMISSION

- 8.3 SOLVENTBORNE COATINGS

- 8.3.1 SOLVENTBORNE FORMULATIONS CONTINUE TO DOMINATE MARKET DUE TO THEIR HIGH PERFORMANCE

- 8.4 POWDER COATINGS

- 8.4.1 OFFER SUPERIOR PERFORMANCE, COST EFFICIENCY, AND LOW VOC EMISSION

- 8.5 OTHERS

9 INDUSTRIAL COATINGS MARKET, BY RESIN TYPE

- 9.1 INTRODUCTION

- 9.2 ACRYLIC RESIN

- 9.2.1 VERSATILITY AND COST-EFFECTIVENESS

- 9.3 ALKYD RESIN

- 9.3.1 EXCELLENT MECHANICAL PROPERTIES, SUPERIOR DRYING SPEED, HIGH GLOSS, AND LOWER COST THAN ACRYLIC BINDERS

- 9.4 EPOXY RESIN

- 9.4.1 GOOD ADHESION, HIGH CHEMICAL RESISTANCE, AND EXCELLENT PHYSICAL PROPERTIES

- 9.5 POLYESTER RESIN

- 9.5.1 WIDELY USED RESIN TYPE IN HIGH-PERFORMANCE COATINGS

- 9.6 POLYURETHANE RESIN

- 9.6.1 INCREASING DEMAND FOR WATERBORNE POLYURETHANE COATINGS

- 9.7 FLUOROPOLYMER RESIN

- 9.7.1 SUITABLE FOR NON-STICK SURFACES DUE TO GOOD THERMAL STABILITY

- 9.8 OTHER RESIN TYPES

10 INDUSTRIAL COATINGS MARKET, BY END-USE INDUSTRY

- 10.1 INTRODUCTION

- 10.2 GENERAL INDUSTRIAL

- 10.2.1 POPULATION GROWTH, INFRASTRUCTURE GROWTH, AND IMPROVED STANDARD OF LIVING TO DRIVE DEMAND

- 10.3 PROTECTIVE

- 10.3.1 ASIA PACIFIC EMERGING AS STRATEGIC LOCATION FOR PROTECTIVE COATING MANUFACTURERS

- 10.4 AUTOMOTIVE OEM

- 10.4.1 GROWING DEMAND FOR ELECTRIC VEHICLES

- 10.5 INDUSTRIAL WOOD

- 10.5.1 INCREASING CONSTRUCTION AND INFRASTRUCTURAL ACTIVITIES TO DRIVE DEMAND

- 10.6 AUTOMOTIVE REFINISH

- 10.6.1 INCREASING NUMBER OF ACCIDENTS PROPELLING DEMAND

- 10.7 COIL

- 10.7.1 DURABLE SURFACE, GREEN BENEFITS, AND COST BENEFITS TO DRIVE MARKET

- 10.8 PACKAGING

- 10.8.1 IMPROVING LIFESTYLE AND CHANGING FOOD HABITS FUELING DEMAND FOR PACKAGING COATINGS

- 10.9 MARINE

- 10.9.1 SLOW GROWTH OF SHIPBUILDING SECTOR HAMPERING DEMAND FOR MARINE COATINGS

- 10.10 AEROSPACE

- 10.10.1 DEVELOPMENT OF CHROME-FREE COATING TECHNOLOGY AUGMENTING MARKET GROWTH

- 10.11 RAIL

- 10.11.1 ADVANCEMENT IN HIGH-SPEED TRAIN INDUSTRY BOOSTING RAIL COATINGS MARKET

11 INDUSTRIAL COATINGS MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 US

- 11.2.1.1 Presence of major manufacturers to drive market growth

- 11.2.2 CANADA

- 11.2.2.1 High export of furniture to boost demand

- 11.2.3 MEXICO

- 11.2.3.1 High export of electronic products to drive market

- 11.2.1 US

- 11.3 EUROPE

- 11.3.1 GERMANY

- 11.3.1.1 Growing economy and rising appliances industry to drive growth

- 11.3.2 RUSSIA

- 11.3.2.1 Growing population leading to rise in demand for automotive industrial coatings

- 11.3.3 UK

- 11.3.3.1 Growing automotive industry and rising investment in R&D to boost demand

- 11.3.4 FRANCE

- 11.3.4.1 Adoption of innovative technologies to drive demand

- 11.3.5 ITALY

- 11.3.5.1 Growing demand from end-use industries to boost market growth

- 11.3.6 SPAIN

- 11.3.6.1 Growing automotive industry to drive demand

- 11.3.7 TURKEY

- 11.3.7.1 Rapid urbanization and diversification in consumer goods to impact market positively

- 11.3.1 GERMANY

- 11.4 ASIA PACIFIC

- 11.4.1 CHINA

- 11.4.1.1 Foreign investments to drive market

- 11.4.2 INDIA

- 11.4.2.1 Government initiatives to help industries grow

- 11.4.3 JAPAN

- 11.4.3.1 Automotive and marine industries to drive demand

- 11.4.4 INDONESIA

- 11.4.4.1 Increasing penetration of Japanese car manufacturers to drive market

- 11.4.5 THAILAND

- 11.4.5.1 Automotive industry to contribute significantly to market growth

- 11.4.1 CHINA

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 GCC

- 11.5.1.1 Saudi Arabia

- 11.5.1.1.1 Significant government investments in infrastructure development

- 11.5.1.2 UAE

- 11.5.1.2.1 Increasing focus on developing regulatory mechanisms and R&D capabilities to drive market

- 11.5.1.1 Saudi Arabia

- 11.5.2 SOUTH AFRICA

- 11.5.2.1 Significant demand for automobiles to boost market

- 11.5.3 EGYPT

- 11.5.3.1 Automotive industry to drive market

- 11.5.1 GCC

- 11.6 SOUTH AMERICA

- 11.6.1 BRAZIL

- 11.6.1.1 Investment partnership program to promote private sector participation in infrastructure development to drive market

- 11.6.2 ARGENTINA

- 11.6.2.1 Increase in population and improved economic conditions to drive demand

- 11.6.1 BRAZIL

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.3 MARKET SHARE ANALYSIS, 2024

- 12.4 REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2021-2024

- 12.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 12.5.1 STARS

- 12.5.2 EMERGING LEADERS

- 12.5.3 PERVASIVE PLAYERS

- 12.5.4 PARTICIPANTS

- 12.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 12.5.5.1 Company footprint

- 12.5.5.2 Region footprint

- 12.5.5.3 Resin type footprint

- 12.5.5.4 Technology footprint

- 12.5.5.5 End-use industry footprint

- 12.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 12.6.1 PROGRESSIVE COMPANIES

- 12.6.2 RESPONSIVE COMPANIES

- 12.6.3 DYNAMIC COMPANIES

- 12.6.4 STARTING BLOCKS

- 12.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 12.6.5.1 Detailed list of key startups/SMES

- 12.6.5.2 Competitive benchmarking of key startups/SMEs

- 12.7 BRAND/PRODUCT COMPARISON ANALYSIS

- 12.8 COMPANY VALUATION AND FINANCIAL METRICS

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES

- 12.9.2 DEALS

- 12.9.3 EXPANSIONS

- 12.9.4 OTHER DEVELOPMENTS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 AKZO NOBEL N.V.

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Expansions

- 13.1.1.3.4 Other developments

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 AXALTA COATING SYSTEMS LTD.

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches

- 13.1.2.3.2 Deals

- 13.1.2.3.3 Expansions

- 13.1.2.3.4 Other developments

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 JOTUN A/S

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.3.2 Deals

- 13.1.3.3.3 Expansions

- 13.1.3.3.4 Other developments

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 PPG INDUSTRIES, INC.

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches

- 13.1.4.3.2 Deals

- 13.1.4.3.3 Expansions

- 13.1.4.3.4 Other developments

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 THE SHERWIN-WILLIAMS COMPANY

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product launches

- 13.1.5.3.2 Deals

- 13.1.5.4 MnM view

- 13.1.5.4.1 Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses and competitive threats

- 13.1.6 NIPPON PAINT HOLDINGS CO., LTD

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product launches

- 13.1.6.3.2 Deals

- 13.1.6.3.3 Expansions

- 13.1.7 KANSAI PAINT CO., LTD.

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Deals

- 13.1.8 RPM INTERNATIONAL INC.

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Expansions

- 13.1.9 HEMPEL A/S

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Product launches

- 13.1.9.3.2 Deals

- 13.1.9.3.3 Expansions

- 13.1.9.3.4 Other developments

- 13.1.10 THE CHEMOURS COMPANY

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.1 AKZO NOBEL N.V.

- 13.2 OTHER PLAYERS

- 13.2.1 NOROO PAINT & COATINGS CO., LTD.

- 13.2.2 SK KAKEN CO., LTD.

- 13.2.3 DAW SE

- 13.2.4 TEKNOS GROUP

- 13.2.5 TIGER COATINGS GMBH & CO. KG

- 13.2.6 ASIAN PAINTS LIMITED

- 13.2.7 DIAMOND VOGEL

- 13.2.8 ADVANCED NANOTECH LAB

- 13.2.9 IGP PULVERTECHNIK AG

- 13.2.10 NANOVERE TECHNOLOGIES, LLC.

- 13.2.11 NYCOTE

- 13.2.12 TEKNOVACE COATINGS PVT LTD

- 13.2.13 GRAND POLYCOATS COMPANY PVT. LTD.

- 13.2.14 ENDURA COATINGS, LLC

- 13.2.15 CHUGOKU MARINE PAINTS, LTD.

14 ADJACENT & RELATED MARKETS

- 14.1 INTRODUCTION

- 14.2 LIMITATIONS

- 14.3 ARCHITECTURAL COATINGS

- 14.3.1 MARKET DEFINITION

- 14.3.2 MARKET OVERVIEW

- 14.4 ARCHITECTURAL COATINGS MARKET, BY REGION

- 14.4.1 ASIA PACIFIC

- 14.4.2 EUROPE

- 14.4.3 NORTH AMERICA

- 14.4.4 MIDDLE EAST & AFRICA

- 14.4.5 SOUTH AMERICA

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 AVAILABLE CUSTOMIZATIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS