ドイツの工業用コーティング:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Germany Industrial Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1685904

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

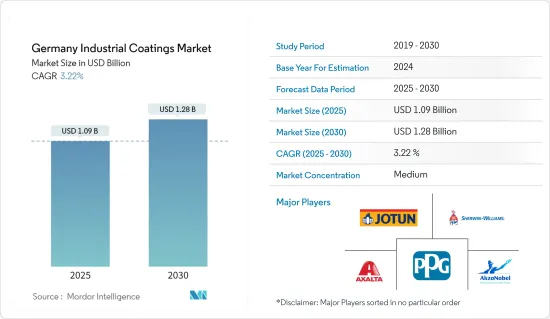

ドイツの工業用コーティング市場規模は2025年に10億9,000万米ドルと推定され、2030年には12億8,000万米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは3.22%です。

COVID-19の発生により、工業用コーティングセクターはマイナスの影響を受けました。GDPの変動により売上が影響を受けました。操業停止と人材不足のため、ほとんどの生産設備が停止しました。その結果、さまざまな生産者の間に不安が生じた。さらに、サプライチェーンの制約が業界の拡大を大きく妨げました。自動車業界は、2019年から2020年にかけて、販売不振、構造的な減速、景気の低迷を示しました。しかし、景気回復を支援するインセンティブ・パッケージとともに、ロックダウンの緩和が地域の自動車産業に恩恵をもたらしました。市場は2021年に回復し、今後数年間は大幅な成長が見込まれます。

主なハイライト

- 短期的には、産業インフラ建設の増加と石油・ガスおよび石油化学産業からの需要増加が市場成長を押し上げると予想されます。

- しかし、揮発性有機化合物(VOC)排出に関する厳しい規制が市場成長の妨げになると予想されます。

- とはいえ、環境に優しいコーティング製品に対する需要の高まりは、調査対象市場に有利な成長機会をもたらす可能性が高いです。

ドイツの工業用コーティング市場動向

繁栄する石油・ガスセクターが保護コーティングの需要を高める

- 石油・ガス産業は、保護塗料の主要なエンドユーザーのひとつです。同業界は高温環境での事業運営を行うため、耐熱性コーティングを必要としています。また、湿った環境にさらされる金属や鉄骨構造物を腐食から守るためにも使用されます。石油・ガス産業では、タンク、パイプ、バルブ、ポンプなどに使用されています。

- 石油・ガス産業では、精製所への石油・ガス輸送中の腐食を防ぐため、上流と下流の両方に保護塗料を使用しています。業界は、資本コストを削減する方法を見つけようとしています。厳しい環境規制を遵守する必要性とともに、資産保護に効果的な長寿命のコーティング・システムの需要につながっています。

- 石油・ガスの海洋生産は、最も厳しい条件のひとつです。そのため、使用されるコーティング・システムは、このような条件に対応できるものでなければならないです。浸透性の紫外線に長時間さらされ、荒い海水と常に接触しているため、工業用コーティングの必要性が高まっています。

- しかし、ロシアとウクライナの戦争に伴い、ドイツはウクライナを支援するため、他の制裁措置に加えて、ロシアからのガスパイプライン「ノルド・ストリーム2」の認証プロセスを停止する措置をとりました。ロシアからの石油および関連製品の一時的な輸入停止は、国内の市場調査に影響を与えそうです。

- BP統計によると、2021年のドイツの石油総消費量は日量204万5,000バレルで、2020年の204万9,000バレルに比べ0.2%減少しました。

- 同じ出典によると、2021年の天然ガス総消費量は905億立方メートルで、2020年の871億立方メートルから4.2%の伸びを記録しました。

- 以上のような動きから、予測期間中、石油・ガス産業向け保護塗料の需要は増加すると予想されます。

エポキシ樹脂の使用量の増加

- エポキシ樹脂は石油由来の強化ポリマー複合材料です。エポキシド単位を含む反応プロセスの結果です。これらの樹脂は、床や金属用途のコーティングの耐久性を高めるために、コーティング用途のバインダーとして使用されます。

- エポキシ・コーティングは、耐腐食性、耐摩耗性、耐候性に優れているため、過酷な使用環境にある鉄鋼用途に適しています。また、高温にも強いため、高温の製品を貯蔵し、極端な熱にさらされるタンクにも適しています。

- 工業用エポキシ・コーティングは一般的に3層で使用されます。まず、亜鉛プライマーなどのプライマーを塗布します。その後、エポキシ樹脂をスプレーします。エポキシ・バインダーまたはポリウレタン・トップコートを塗布してコーティングを完了します。

- エポキシ・ポリアミド・コーティングは耐湿性に優れ、エポキシ・マスティック・コーティングは膜厚に優れ、フェノール・エポキシ・コーティングは耐薬品性に優れています。用途に応じて、エポキシ樹脂は下塗り、中塗り、あるいは上塗りとして使用することができます。

- エポキシ樹脂は工業用コーティングのバインダーとして頻繁に使用されます。これらのコーティングは、船舶や化学薬品貯蔵タンクで使用される高い接着性、高い耐薬品性(耐腐食性)、耐物理性を提供します。

- エポキシ塗料は、その入手のしやすさから、数多くの工業用途に使用されています。エポキシ粉体塗料は、洗濯機、乾燥機、白物家電、石油・ガス産業で使用される鋼管や継手、送水パイプライン、コンクリート補強用鉄筋などに、その柔軟な適用性から使用されています。

- エポキシ・コーティングの利点はいくつかある:

- エポキシ・コーティングは長持ちし、費用対効果が高く、防水性があり、衝撃に強いです。

- 研磨されたコンクリートのように滑りにくいため、作業の安全性を高めるために使用されます。

- エポキシ樹脂は光沢があるため視認性が高く、光源を反射して安全な作業環境を実現します。

- 以上のような要因が、予測期間中に調査された市場におけるエポキシ樹脂の需要を増大させる可能性があります。

ドイツの工業用コーティング産業の概要

ドイツの工業用コーティング市場は、その性質上、部分的に統合されています。同市場の主要企業には、PPGインダストリーズ社、シャーウィン・ウィリアムズ社、アクゾノーベルNV社、アクサルタ・コーティング・システムズ社、ヨーツン社などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 産業インフラ建設の増加

- 石油・ガスおよび石油化学産業からの需要増加

- 抑制要因

- VOC排出に関する厳しい規制

- その他の阻害要因

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 樹脂タイプ

- エポキシ

- アクリル

- アルキド

- ポリウレタン

- その他の樹脂タイプ

- コーティング技術

- 水性コーティング

- 溶剤型コーティング

- 放射線硬化型コーティング

- 粉体塗料

- タイプ

- 一般工業用

- 保護

- 石油・ガス

- 鉱業

- 電力

- インフラ

- その他の保護

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- AkzoNobel NV

- Axalta Coating Systems

- Beckers group

- Hempel AS

- Jotun

- MIPA SE

- PPG Industries Inc.

- RPM International Inc.

- The Sherwin-Williams Company

第7章 市場機会と今後の動向

- 環境に優しい塗料への需要の高まり

目次

The Germany Industrial Coatings Market size is estimated at USD 1.09 billion in 2025, and is expected to reach USD 1.28 billion by 2030, at a CAGR of 3.22% during the forecast period (2025-2030).

Due to the outbreak of COVID-19, the industrial coatings sector was negatively impacted. Sales were affected due to GDP movement. Most production units were shut down due to the lockdowns and shortage of human resources. This resulted in uncertainty among various producers. Furthermore, supply chain constraints significantly obstructed the expansion of the industry. The automotive industry showed sluggish sales, a structural slowdown, and a sputtering economy in 2019-2020. However, the easing of lockdowns, along with incentive packages to support economic revival, benefited the regional automotive industry. The market recovered in 2021 and is expected to grow at a significant rate in the coming years.

Key Highlights

- Over the short term, the increasing construction of industrial infrastructure and the growing demand from oil and gas and petrochemical industries are expected to boost the market growth.

- However, the stringent regulations for volatile organic compound (VOC) emissions are expected to hinder the market's growth.

- Nevertheless, the rising demand for eco-friendly coating products is likely to create lucrative growth opportunities for the studied market.

German Industrial Coatings Market Trends

Flourishing Oil and Gas Sector to Rise the Demand for Protective Coatings

- The oil and gas sector is one of the major end users of protective coatings. The industry requires heat-resistant coatings due to the high-temperature environment of its business operations. The coatings are also used to protect metal and steel structures from corrosion when exposed to moist and damp conditions. They are used in the oil and gas industry for tanks, pipes, valves, pumps, etc.

- The oil and gas industry uses protective coatings for both upstream and downstream segments to prevent corrosion during oil and gas transportation toward refineries. The industry has been trying to find ways to cut capital charges. Along with the need to adhere to strict environmental regulations, this has led to the demand for a coating system with a long life, which may be effective in protecting assets.

- Offshore oil and gas production has some of the most demanding conditions. Therefore, the coating systems used must be equipped for these conditions. Prolonged exposure to penetrating UV rays and constant contact with rough seawater increases the need for industrial coatings.

- However, with the Russia-Ukraine war, Germany has taken steps to halt the process of certifying the Nord Stream Two gas pipeline from Russia, besides other sanctions, in support of Ukraine. The temporary halts on the imports of petroleum and allied products from Russia are likely to affect the market studied in the country.

- According to BP Stats, the total oil consumption in Germany was 2,045 thousand barrels per day in 2021, registering a decline rate of 0.2% compared to 2,049 thousand barrels per day in 2020.

- As per the same source, the total natural gas consumption in the country was 90.5 billion cubic meters in 2021, registering a growth rate of 4.2% from 87.1 billion cubic meters in 2020.

- All the above-motioned factors are expected to augment the demand for protective coatings for the oil and gas industry during the forecast period.

Rising Usage of Epoxy Resins

- Epoxy resins are reinforced polymer composites derived from petroleum sources. They are the result of a reactive process involving epoxide units. These resins are used as binders for coating applications to enhance the durability of coatings for floor and metal applications.

- Epoxy coatings are suitable for steel applications in harsh operating environments because of their resistance to corrosion, abrasion, and weathering. These coatings are also resistant to extremely high temperatures, making them suitable for use on tanks that store hot products and are exposed to extreme heat.

- Industrial epoxy coatings are commonly used in three layers. Firstly, a primer, such as zinc primer, is applied. The epoxy is then sprayed on. An epoxy binder or polyurethane topcoat is applied to complete the coating process.

- Epoxy polyamide coatings are ideal for moisture resistance, epoxy mastic coatings are used for film thickness, and phenolic epoxy coatings are excellent for chemical resistance. Depending on the application, epoxies can be used as a priming, intermediate coat, or even a topcoat.

- Epoxy resins are frequently used as binders in industrial coatings. Those coatings provide high adhesion and high chemical (corrosion) and physical resistance for use on ships and chemical storage tanks.

- Due to their availability, epoxy coatings find numerous industrial applications. Epoxy powder coatings are used on washers, dryers, white goods, steel pipes, and fittings used in the oil and gas industry, water transmission pipelines, and concrete reinforcing rebar due to their flexible applicability.

- Several advantages of epoxy coatings are:

- Epoxy coatings are long-lasting, cost-effective, waterproof, and shock-resistant.

- They are used to improve operational safety since they are not slippery like polished concrete.

- Epoxy increases visibility with its high sheen, reflecting light sources and improving visibility making for a safer working environment.

- All the above-mentioned factors may augment the demand for epoxy resins for the market studied during the forecast period.

German Industrial Coatings Industry Overview

The Germany industrial coatings market is partially consolidated in nature. Some of the major key playersin the market include PPG Industries Inc., The Sherwin-Williams Company, AkzoNobel NV, Axalta Coating Systems and Jotun.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Industrial Infrastructure Construction

- 4.1.2 Growing Demand from Oil and Gas and Petrochemical Industries

- 4.2 Restraints

- 4.2.1 Stringent Regulations for VOC Emissions

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size by Value)

- 5.1 Resin Type

- 5.1.1 Epoxy

- 5.1.2 Acrylic

- 5.1.3 Alkyd

- 5.1.4 Polyurethane

- 5.1.5 Other Resin Types

- 5.2 Technology

- 5.2.1 Water-borne Coatings

- 5.2.2 Solvent-borne Coatings

- 5.2.3 Radiation-cured Coatings

- 5.2.4 Powder Coatings

- 5.3 Type

- 5.3.1 General Industrial

- 5.3.2 Protective

- 5.3.2.1 Oil and Gas

- 5.3.2.2 Mining

- 5.3.2.3 Power

- 5.3.2.4 Infrastructure

- 5.3.2.5 Other Protectives

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AkzoNobel NV

- 6.4.2 Axalta Coating Systems

- 6.4.3 Beckers group

- 6.4.4 Hempel AS

- 6.4.5 Jotun

- 6.4.6 MIPA SE

- 6.4.7 PPG Industries Inc.

- 6.4.8 RPM International Inc.

- 6.4.9 The Sherwin-Williams Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Demand for Eco-friendly Coatings

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日