水処理薬品の世界市場:タイプ別、原料別、エンドユーザー別、地域別 - 予測(~2030年)

Water Treatment Chemicals Market by Type (Flocculants & Coagulants, Corrosion Inhibitors, Scale Inhibitors, Biocides & Disinfectants, Chelating Agents), Source, End User (Residential, Commercial & Industrial), And Region - Global Forecast to 2030- 発行日

- ページ情報

- 英文 316 Pages

- 納期

-

即納可能

営業時間内にお支払方法などの確認が取れ次第、Eメールにて納品となります。営業時間: 9:00am - 6:00pm (土日祝除く)。

- 商品コード

- 1984861

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

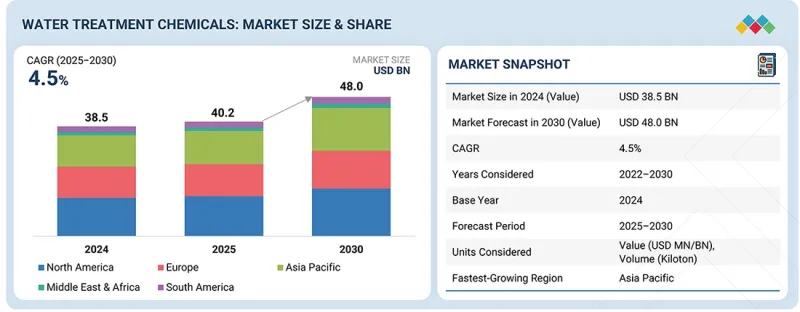

世界の水処理薬品の市場規模は、2025年の402億米ドルから2030年までに480億米ドルに達すると予測され、予測期間にCAGRで4.5%の成長が見込まれています。

| 調査範囲 | |

|---|---|

| 調査対象期間 | 2022年~2031年 |

| 基準年 | 2025年 |

| 予測期間 | 2026年~2031年 |

| 単位 | 100万米ドル、個 |

| セグメント | タイプ、原料、エンドユーザー、用途、地域 |

| 対象地域 | 北米、欧州、アジア太平洋、南米、その他の地域 |

冷却水処理は、複数の高成長業界における幅広い適用性と継続的な運用需要により、水処理薬品市場において用途別で第2位の市場シェアを占めると予測されます。発電所、製油所、石油化学コンビナート、製造施設、商業ビル、データセンターはすべて、主な熱負荷に対応するために、継続的な熱除去能力を維持する冷却システムを必要としています。これらのシステムは水の連続循環によって稼働するため、スケール、腐食、バイオファウリング、微生物の増殖といった継続的な問題が生じ、化学的処理が必要となります。環境規制を満たすために水消費を削減する高循環冷却システムの採用が増加していることから、溶解固形物の濃度が高まり、システムあたりの化学品需要も増加しています。

「エンドユーザー別では、住宅セグメントが予測期間に金額ベースで第2位の市場シェアを占める見込みです。」

住宅エンドユーザーセグメントは、家庭用水の消費と水質管理に関連する、大規模かつ継続的な需要基盤により、水処理薬品市場において2番目に大きなシェアを占めると予測されます。新興市場における住宅開発と都市化は、都市水道システムへの需要の増加をもたらし、結果として、飲料水処理、配水システムの保全、廃水処理に用いる薬品の需要が高まっています。各地における老朽化した配管と不安定な給水の組み合わせは、汚染、腐食、バイオフィルムの発生リスクを高める状況を生み出しており、消毒剤、腐食防止剤、pH調整剤による処理が必要とされています。飲料水の安全性に対する一般市民の理解の高まりに加え、衛生習慣や水性感染症の伝播への懸念から、自治体は水処理規制を厳格化しており、結果として、住宅用化学品の要求が高まっています。

「地域別では、中東・アフリカが予測期間に金額ベースで水処理化学品市場において2番目に高い成長率を示すと予測されます。」

市場予測によると、中東・アフリカの水処理薬品市場は、構造的な水不足や急速な処理能力の拡大、投資政策により、既存市場とは異なる成長条件が形成されることから、地域別で2番目に高い成長率を記録する見込みです。同地域は、海水淡水化、汽水処理、処理済み廃水の再使用といった非在来型の水源に依存しています。これらのプロセスは化学品を多用するため、スケール防止剤、腐食防止剤、特殊添加剤が必要となります。新都市、産業回廊、製油所、発電所の建設においては、設計の初期段階から水処理システムが組み込まれており、プロジェクト全体での化学品消費の増加につながっています。アフリカにおける都市人口の増加と電化プログラムは、化学品の採用レベルが低い都市給水と廃水処理への投資を後押しし、結果として化学品の使用に対する強い需要を生み出すとみられます。

当レポートでは、世界の水処理薬品市場について調査分析し、主な促進要因と抑制要因、製品開発とイノベーション、競合情勢に関する知見を提供しています。

よくあるご質問

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

第3章 重要な知見

- 水処理薬品市場における企業にとって魅力的な機会

- 水処理薬品市場:原料別

- 水処理薬品市場:用途別

- 水処理薬品市場:タイプ別

- 水処理薬品市場:エンドユーザー別

- 水処理薬品市場:国別

第4章 市場の概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- アンメットニーズと未開発部門

- 水処理薬品市場におけるアンメットニーズ

- ホワイトスペースの機会

- 相互接続された市場と部門横断的な機会

- 相互接続された市場

- 部門横断的な機会

- Tier 1/2/3企業の戦略的な動き

- ポーターの5つの競争要因の分析

- バリューチェーン分析

- エコシステム

- 価格設定の分析

- 平均販売価格:主要企業別

- 平均販売価格:地域別

- 平均販売価格:用途別

- マクロ経済指標

- 水処理薬品市場に対する2025年の米国関税の影響

- 主な関税率

- 価格の影響の分析

- 国/地域への影響

- 最終用途産業への影響

- 貿易分析

- 輸入シナリオ(HSコード842121)

- 輸出シナリオ(HSコード842121)

- 輸入シナリオ(HSコード382499)

- 輸出シナリオ(HSコード382499)

- カスタマービジネスに影響を与える動向/混乱

- 投資と資金調達のシナリオ

- ケーススタディ

- 主な会議・イベント(2026年~2027年)

第5章 技術の進歩、AIによる影響、特許、イノベーション、将来の用途

- 技術分析

- 主要技術

- 補完技術

- 隣接技術

- 技術/製品ロードマップ

- 上流技術ロードマップ:原料、配合、生産

- 燃料、水、排出管理製品ロードマップ

- 生産、水、排出管理製品ロードマップ

- 特許分析

- 特許の法的地位

- 管轄権分析

- 将来の用途

- 先進の水再使用・水循環システム

- 海水淡水化・汽水処理

- 新規汚染物質と残留汚染物質の処理

- 膜ろ過と先進ろ過技術への支援

- 産業施設における冷却水とプロセス水の管理

- 水処理薬品市場に対するAI/汎用AIの影響

- 主なユースケースと市場の将来性

- 水処理薬品処理におけるベストプラクティス

- 水処理薬品市場におけるAI導入のケーススタディ研究

- 相互接続された隣接エコシステムと市場参入企業への影響

- 水処理市場における生成AIの採用に対する顧客の準備状況

第6章 規制情勢と持続可能性への取り組み

- 地域の規制と遵守事項

- 規制機関、政府機関、その他の組織

- 業界標準

- 持続可能性への取り組み

- 規制政策と持続可能性への取り組みの影響

- 認証、ラベル表示、環境基準

第7章 顧客情勢と購買行動

- 意思決定プロセス

- 主なステークホルダーと購入基準

- 採用障壁・内部課題

- さまざまな最終用途産業におけるアンメットニーズ

- 市場の収益性

- 潜在的な収益

- コスト動向

- 主要最終用途産業における利益率の機会

第8章 水処理薬品市場:原料別

- バイオベース

- 合成

第9章 水処理薬品市場:用途別

- ボイラー水処理

- 冷却水処理

- 原水処理

- 海水淡水化

- その他の用途

第10章 水処理薬品市場:タイプ別

- 凝固剤・凝集剤

- 腐食防止剤

- スケール抑制剤

- 殺生物剤・消毒剤

- キレート剤

- 消泡剤

- pH調整剤・安定剤

- その他のタイプ

第11章 水処理薬品市場:エンドユーザー別

- 住宅

- 商業

- 工業

第12章 水処理薬品市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- イタリア

- フランス

- スペイン

- 英国

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- インドネシア

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- エジプト

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

第13章 競合情勢

- 収益分析(2022年~2024年)

- 市場シェア分析(2024年)

- 企業の評価と財務指標

- 製品の比較

- 企業の評価マトリクス:主要企業(2024年)

- 企業の評価マトリクス:スタートアップ/中小企業(2024年)

- 競合シナリオ

第14章 企業プロファイル

- 主要企業

- ECOLAB

- VEOLIA

- BASF

- DOW INC.

- KEMIRA

- SOLENIS

- SOLVAY

- NOURYON

- KURITA WATER INDUSTRIES LTD.

- SNF FLOERGER

- SYENSQO

- ARXADA

- CORTEC CORPORATION

- その他の企業

- ARIES CHEMICAL, INC.

- BUCKMAN

- DORF KETAL

- FERALCO AB

- GEO SPECIALTY CHEMICALS

- HYDRITE CHEMICAL

- INNOSPEC INC.

- ION EXCHANGE(INDIA)LTD.

- ITALMATCH CHEMICALS S.P.A.

- IXOM

- MCC CHEMICALS, INC.

- ROEMEX LIMITED

- THERMAX LIMITED

- UNIPHOS CHEMICALS

第15章 調査手法

第16章 付録

- 発行日

- 発行

- MarketsandMarkets

- ページ情報

- 英文 316 Pages

- 納期

- 即納可能