|

|

市場調査レポート

商品コード

1374758

ポリエステルフィルムの世界市場:タイプ別、用途別、厚さ別、最終用途産業別、地域別-2028年までの予測Polyester Film Market by Type (Biaxially oriented, thermal film, metalized film, holographic film, UV stabilized, matte film, barrier film), Application (packaging, electrical insulation, imaging), End Use Industry, and Region - Global forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| ポリエステルフィルムの世界市場:タイプ別、用途別、厚さ別、最終用途産業別、地域別-2028年までの予測 |

|

出版日: 2023年10月25日

発行: MarketsandMarkets

ページ情報: 英文 247 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

| 調査範囲 | |

|---|---|

| 調査対象年 | 2023年~2028年 |

| 基準年 | 2022 |

| 予測期間 | 2023年~2028年 |

| 対象単位 | 金額(10億米ドル/100万米ドル) |

| セグメント | タイプ別、用途別、厚さ別、最終用途産業別、地域別 |

| 対象地域 | アジア太平洋、北米、欧州、中東・アフリカ、南米 |

ポリエステルフィルムの市場規模は、2023年の327億米ドルから6.2%のCAGRで拡大し、2028年には442億米ドルに達すると予測されています。

ポリエステルフィルムは汎用性が高く軽量な包装材料であり、食品・飲料、医薬品、消費財など様々な産業で使用されるようになってきています。フレキシブルパッケージングソリューションに対する需要の高まりが、今後数年間のポリエステルフィルム市場の成長を促進すると予想されます。フレキシブル包装は消費者にとって使用や保管に便利で、軽量で輸送も容易なため、メーカーや小売業者にとって良い選択肢となります。フレキシブル包装はリサイクル可能な材料から作られることが多く、製造や輸送にかかるエネルギーも少なくて済むため、ガラスや金属などの硬質包装材料よりも持続可能な包装ソリューションとなる可能性があります。フレキシブルパッケージング業界は、新しく改良されたパッケージングソリューションを開発するために常に革新的であり、ポリエステルフィルムは、その多用途性、耐久性、優れたバリア特性により、フレキシブル・パッケージング用途に人気のある選択肢となっています。

ポリエステルフィルムは、その軽量性、耐久性、汎用性、優れたバリア性により、食品・飲料包装業界で好まれている素材です。スナック菓子、キャンディ、パン、肉、チーズ、冷凍食品の包装など、幅広い用途に使用されています。湿気、酸素、汚染からこれらの製品を守るその能力は、製品の鮮度と品質に貢献しています。さらに、ポリエステルフィルムはさまざまな包装形態に適応し、高品質のグラフィックを印刷することができるため、訴求力が高まります。こうした用途にとどまらず、ポリエステルフィルムは多様な食品・飲料包装のニーズに対応する汎用性と信頼性の高い選択肢であり続けるとともに、持続可能性への取り組みやアクティブでスマートな包装システムの開発など、革新的な包装ソリューションの一翼を担っています。

ポリエステルフィルム業界におけるUV安定化フィルムの著しい成長は、いくつかの説得力のある要因に起因しています。これらのフィルムは、有害な紫外線への長時間の曝露に耐える能力により、屋外用途で脚光を浴びており、屋外看板、バナー、農業、保護カバーに不可欠なものとなっています。黄変や脆化に耐える優れた耐久性は、建設、自動車、包装など、長期的な性能が最重要視される産業に対応しています。

北米がポリエステルフィルムの第2位の市場として機能しているのにはいくつかの重要な理由があります。第一に、北米には多様で確立された産業基盤があり、パッケージング、エレクトロニクス、自動車、建設など幅広い産業が含まれます。これらの分野では、さまざまな用途でポリエステルフィルムに頼ることが多いです。第二に、北米市場ではフレキシブルで持続可能なパッケージング・ソリューションに対する需要が高まっており、これがパッケージング用途でのポリエステルフィルムの使用を後押ししています。さらに、ポリエステルフィルムが部品や断熱材に使用されているエレクトロニクス産業や自動車産業における技術革新が、市場の成長に寄与しています。さらに、同地域が持続可能性とリサイクル性に重点を置いていることが、ポリエステルフィルムの環境に優しい性質と合致し、様々な用途での使用を促進しています。最後に、技術の進歩と研究開発の取り組みが北米のポリエステルフィルム市場の拡大につながり、北米はこの多用途素材の第2位の市場となっています。

当レポートでは、世界のポリエステルフィルム市場について調査し、タイプ別、用途別、厚さ別、最終用途産業別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

第6章 業界の動向

- イントロダクション

- 顧客のビジネスに影響を与える動向/混乱

- バリューチェーン分析

- 価格分析

- 生態系マッピング

- 技術分析

- 特許分析

- 貿易分析

- 2023年から2024年の主要な会議とイベント

- 関税と規制状況

- ポーターのファイブフォース分析

- 主要な利害関係者と購入基準

- マクロ経済指標

- ケーススタディ

第7章 ポリエステルフィルム市場、タイプ別

- イントロダクション

- 二軸配向フィルム

- サーマルフィルム

- 金属化フィルム

- ホログラフィックフィルム

- UV安定化フィルム

- マットフィルム

- バリアフィルム

- その他

第8章 ポリエステルフィルム市場、用途別

- イントロダクション

- 梱包

- 工業用ラミネート

- イメージングと印刷

- 電気絶縁

- ソーラーパネル

- その他

第9章 ポリエステルフィルム市場、厚さ別

- イントロダクション

- 50ミクロン未満

- 51~100ミクロン

- 101~200ミクロン

- 201~300ミクロン

- 300ミクロン超

第10章 ポリエステルフィルム市場、最終用途産業別

- イントロダクション

- 食品・飲料

- 電気・電子

- 医薬品

- 繊維

- 医療

- モビリティ・輸送

- その他

第11章 ポリエステルフィルム市場、地域別

- イントロダクション

- アジア太平洋

- 北米

- 欧州

- 中東・アフリカ

- 南米

第12章 競合情勢

- イントロダクション

- 主要参入企業が採用した戦略

- 市場シェア分析

- 収益分析

- 企業評価マトリックス(Tier 1)

- 新興企業/中小企業の評価マトリックス

- 競争シナリオと動向

第13章 企業プロファイル

- 主要参入企業

- TORAY INDUSTRIES, INC.

- KOLON INDUSTRIES, INC.

- TOYOBO CO., LTD.

- POLYPLEX

- ESTER INDUSTRIES LIMITED

- DUPONT TEIJIN FILMS

- MITSUBISHI POLYESTER FILM GMBH

- POLIFILM EXTRUSION GMBH.

- TERPHANE

- JINDAL POLY FILMS LTD.

- その他の企業

- SEALED AIR CORPORATION

- OBEN HOLDING GROUP

- RADICI PARTECIPAZIONI SPA

- AEP INDUSTRIES

- UFLEX LIMITED

- AMCOR PLC

- BERRY GLOBAL GROUP, INC.

- DOW

- EASTMAN CHEMICAL COMPANY

- IMPAK FILMS US LLC

- POLINAS

- FUTAMURA CHEMICAL CO. LTD.

- SUMILON POLYESTER LTD.

- AMERPLAST

- ZHEJIANG WUZHOU POLYESTER FILM CO., LTD.

第14章 付録

Report Description

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2028 |

| Base Year | 2022 |

| Forecast Period | 2023-2028 |

| Units Considered | Value (USD Billion/Million) |

| Segments | type, application, end use industry and Region |

| Regions covered | Asia Pacific, North America, Europe, Middle East & Africa, and South America |

The Polyester Film Market is projected to reach USD 44.2 Billion by 2028, at a CAGR of 6.2% from USD 32.7 Billion in 2023. Polyester film is a versatile and lightweight packaging material that is increasingly being used in a variety of industries, including food and beverage, pharmaceuticals, and consumer goods. The growing demand for flexible packaging solutions is expected to fuel the growth of the polyester film market in the coming years. Flexible packaging is convenient for consumers to use and store, and it is also lightweight and easy to transport, making it a good choice for manufacturers and retailers. Flexible packaging can be a more sustainable packaging solution than rigid packaging materials, such as glass and metal, as it is often made from recyclable materials and takes less energy to produce and transport. The flexible packaging industry is constantly innovating to develop new and improved packaging solutions, and polyester film is a popular choice for flexible packaging applications due to its versatility, durability, and good barrier properties.

"Food and beverage, by End use industry, accounts for the second-largest market share in 2022."

Polyester film is a favored material in the food and beverage packaging industry due to its lightweight, durability, versatility, and excellent barrier properties. It serves a wide range of applications, including packaging for snacks, candy, bread, meat, cheese, and frozen foods. Its ability to protect these products from moisture, oxygen, and contamination contributes to their freshness and quality. Moreover, polyester film is adaptable to various packaging formats and can be printed with high-quality graphics, enhancing its appeal. Beyond these applications, it remains a versatile and reliable choice for diverse food and beverage packaging needs, while also playing a role in innovative packaging solutions, including sustainability initiatives and the development of active and smart packaging systems.

"UV Stabilized film is expected to be the fastest growing at CAGR 5.7% for polyester film market during the forecast period, in terms of value."

The remarkable growth of UV stabilized films within the polyester films industry can be attributed to several compelling factors. These films have found prominence in outdoor applications due to their ability to withstand prolonged exposure to damaging UV radiation, making them indispensable for outdoor signage, banners, agriculture, and protective coverings. Their outstanding durability, resisting yellowing and embrittlement, caters to industries where long-term performance is paramount, such as construction, automotive, and packaging.

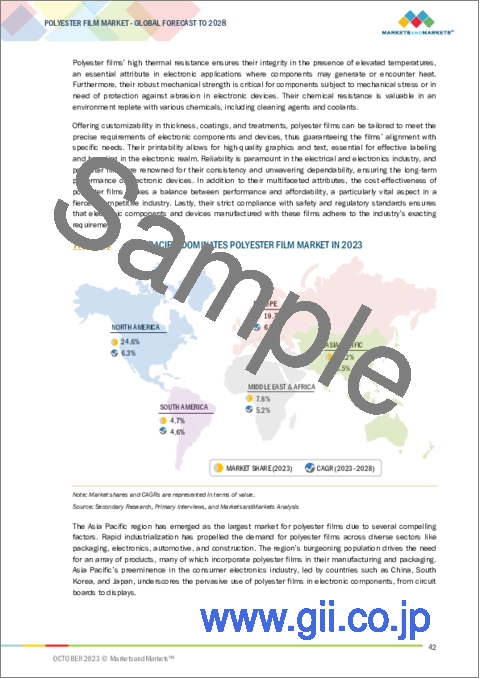

"Based on region, North America was the second largest market for polyester film market in 2022."

North America serves as the second-largest market for polyester films for several key reasons. Firstly, North America has a diverse and established industrial base, which encompasses a wide range of industries such as packaging, electronics, automotive, and construction. These sectors often rely on polyester films for their various applications. Secondly, there's a growing demand for flexible and sustainable packaging solutions in the North American market, which has bolstered the use of polyester films in packaging applications. Moreover, innovations in the electronics and automotive industries, where polyester films are used in components and insulation, have contributed to market growth. Additionally, the region's focus on sustainability and recyclability aligns well with the eco-friendly nature of polyester films, driving their usage in various applications. Finally, technological advancements and research and development initiatives have led to the expansion of the polyester film market in North America, making it the second-largest market for this versatile material.

In the process of determining and verifying the market size for several segments and subsegments identified through secondary research, extensive primary interviews were conducted. A breakdown of the profiles of the primary interviewees is as follows:

- By Company Type: Tier 1 - 40%, Tier 2 - 30%, and Tier 3 - 30%

- By Designation: C-Level - 20%, Director Level - 10%, and Others - 70%

- By Region: North America - 20%, Europe -30%, Asia Pacific - 30%, Middle East & Africa - 10%, and South America-10%

The key players in this market include DuPont Teijin Films (US), TORAY INDUSTRIES, INC. (Japan), Mitsubishi Polyester Film GmbH (Germany), Kolon Industries, Inc. (South Korea), Ester Industries Limited (India), Jindal Films Limited (India), Terphane LLC (US), TOYOBO CO. LTD.,(Japan), Polyplex Corporation Limited (India).

Research Coverage

This report segments the market for the thermoplastic polyolefin material market on the basis of type, application, and region. It provides estimations for the overall value of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products & services, key strategies, new product launches, expansions, and mergers & acquisitions associated with the market for the thermoplastic polyolefin material market.

Key benefits of buying this report

This research report is focused on various levels of analysis - industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape, emerging and high-growth segments of the thermoplastic polyolefin material market; high-growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of key drivers: Increasing demand for advanced technologies, Energy Efficiency and Sustainability.

- Market Penetration: Comprehensive information on the Polyurethane catalyst market offered by top players in the global Polyurethane catalyst market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the Polyurethane catalyst market.

- Market Development: Comprehensive information about lucrative emerging markets - the report analyzes the markets for the Polyurethane catalyst market across regions.

- Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global Polyurethane catalyst market.

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the Polyurethane catalyst market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS & EXCLUSIONS

- 1.3 MARKET SCOPE

- FIGURE 1 POLYESTER FILM MARKET SEGMENTATION

- 1.3.1 REGIONS COVERED

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 POLYESTER FILM MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary interviews - Top polyester film manufacturers

- 2.1.2.2 Breakdown of primary interviews

- 2.1.2.3 Key industry insights

- 2.2 BASE NUMBER CALCULATION

- 2.2.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 2.2.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 2.3 FORECAST NUMBER CALCULATION

- 2.3.1 SUPPLY SIDE

- 2.3.2 DEMAND SIDE

- 2.4 MARKET SIZE ESTIMATION

- 2.4.1 BOTTOM-UP APPROACH

- 2.4.2 TOP-DOWN APPROACH

- 2.5 DATA TRIANGULATION

- FIGURE 3 POLYESTER FILM MARKET: DATA TRIANGULATION

- 2.6 ASSUMPTIONS

- 2.7 IMPACT OF RECESSION

3 EXECUTIVE SUMMARY

- FIGURE 4 BIAXIALLY-ORIENTED FILMS TO LEAD POLYESTER FILM MARKET BETWEEN 2023 AND 2028

- FIGURE 5 <50 MICRONS THICKNESS SEGMENT TO LEAD POLYESTER FILM MARKET BETWEEN 2023 AND 2028

- FIGURE 6 PACKAGING APPLICATION TO LEAD POLYESTER FILM MARKET DURING FORECAST PERIOD

- FIGURE 7 ELECTRICAL & ELECTRONICS SEGMENT TO LEAD POLYESTER FILM MARKET DURING FORECAST PERIOD

- FIGURE 8 ASIA PACIFIC DOMINATES POLYESTER FILM MARKET IN 2023

4 PREMIUM INSIGHTS

- 4.1 SIGNIFICANT OPPORTUNITIES FOR PLAYERS IN POLYESTER FILM MARKET

- FIGURE 9 EXPANSION OF PACKAGING INDUSTRY COUPLED WITH GROWTH OF PHARMACEUTICAL & HEALTHCARE SECTORS TO DRIVE MARKET

- 4.2 POLYESTER FILM MARKET, BY TYPE

- FIGURE 10 BIAXIALLY-ORIENTED FILMS TO BE FASTEST-GROWING TYPE SEGMENT DURING FORECAST PERIOD

- 4.3 POLYESTER FILM MARKET, BY REGION

- FIGURE 11 ASIA PACIFIC TO BE FASTEST-GROWING POLYESTER FILM MARKET DURING FORECAST PERIOD

- 4.4 POLYESTER FILM MARKET, BY THICKNESS

- FIGURE 12 <50 MICRONS THICKNESS TO BE FASTEST-GROWING SEGMENT DURING FORECAST PERIOD

- 4.5 POLYESTER FILM MARKET, BY APPLICATION

- FIGURE 13 PACKAGING TO BE FASTEST-GROWING APPLICATION DURING FORECAST PERIOD

- 4.6 POLYESTER FILM MARKET, BY END-USE INDUSTRY

- FIGURE 14 ELECTRICAL & ELECTRONICS TO BE FASTEST-GROWING END-USE INDUSTRY SEGMENT DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 15 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN POLYESTER FILM MARKET

- 5.2.1 DRIVERS

- 5.2.1.1 Growing packaging industry

- 5.2.1.2 E-commerce boom in recent years

- 5.2.1.3 Expanding landscape of pharmaceutical and healthcare industries

- 5.2.2 RESTRAINTS

- 5.2.2.1 Growing environmental concerns about plastic waste

- 5.2.2.2 Availability of alternatives

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Recycling and circular economy

- 5.2.3.2 Sustainable packaging

- 5.2.4 CHALLENGES

- 5.2.4.1 Overcoming recycling-related issues

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

- 6.2.1 REVENUE SHIFT AND NEW REVENUE POCKETS FOR POLYESTER FILM MANUFACTURERS

- FIGURE 16 REVENUE SHIFT OF POLYESTER FILM MARKET

- 6.3 VALUE CHAIN ANALYSIS

- FIGURE 17 OVERVIEW OF POLYESTER FILM MARKET VALUE CHAIN

- 6.3.1 RAW MATERIAL SUPPLIERS

- 6.3.2 POLYESTER RESIN MANUFACTURING

- 6.3.3 POLYESTER FILM MANUFACTURING

- 6.3.4 DISTRIBUTION

- 6.3.5 END-USE INDUSTRIES

- 6.4 PRICING ANALYSIS

- 6.4.1 AVERAGE SELLING PRICE TREND, BY REGION

- TABLE 1 AVERAGE SELLING PRICE, BY REGION, 2019-2028 (USD/TON)

- FIGURE 18 POLYESTER FILM MARKET: AVERAGE SELLING PRICE TREND, BY REGION

- 6.4.2 AVERAGE SELLING PRICE TREND, BY TYPE

- TABLE 2 AVERAGE SELLING PRICE, BY TYPE, 2019-2028 (USD/TON)

- 6.4.3 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY TOP 3 TYPES

- TABLE 3 AVERAGE SELLING PRICE, BY TOP 3 TYPES, 2019-2028 (USD/TON)

- FIGURE 19 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY TOP 3 TYPES

- 6.5 ECOSYSTEM MAPPING

- TABLE 4 POLYESTER FILM MARKET: ECOSYSTEM

- 6.6 TECHNOLOGY ANALYSIS

- TABLE 5 KEY TECHNOLOGIES OFFERED IN POLYESTER FILM MARKET

- TABLE 6 COMPLEMENTARY TECHNOLOGIES OFFERED IN POLYESTER FILM MARKET

- TABLE 7 ADJACENT TECHNOLOGIES OFFERED FOR POLYESTER FILM

- 6.7 PATENT ANALYSIS

- 6.7.1 METHODOLOGY

- 6.7.2 PATENTS GRANTED WORLDWIDE, 2014-2023

- TABLE 8 TOTAL NUMBER OF PATENTS

- 6.7.2.1 Publication trends over last ten years

- FIGURE 20 NUMBER OF PATENTS GRANTED OVER LAST 10 YEARS

- 6.7.3 INSIGHTS

- 6.7.4 LEGAL STATUS OF PATENTS

- FIGURE 21 PATENT ANALYSIS, BY LEGAL STATUS

- 6.7.5 JURISDICTION ANALYSIS

- FIGURE 22 REGIONAL ANALYSIS OF PATENT GRANTED FOR POLYESTER FILM MARKET, 2023

- 6.7.6 TOP COMPANIES/APPLICANTS

- FIGURE 23 TOP 10 COMPANIES WITH HIGHEST NUMBER OF PATENTS IN LAST TEN YEARS

- TABLE 9 LIST OF MAJOR PATENT OWNERS FOR POLYESTER FILM

- 6.7.7 LIST OF MAJOR PATENTS

- TABLE 10 MAJOR PATENTS FOR POLYESTER FILM

- 6.8 TRADE ANALYSIS

- 6.8.1 IMPORT SCENARIO

- FIGURE 24 IMPORT OF POLYESTER FILM, BY COUNTRY, 2019-2022 (USD MILLION)

- 6.8.2 EXPORT SCENARIO

- FIGURE 25 EXPORT OF POLYESTER FILM, BY COUNTRY, 2019-2022 (USD MILLION)

- 6.9 KEY CONFERENCES & EVENTS, 2023-2024

- TABLE 11 POLYESTER FILM MARKET: DETAILED LIST OF CONFERENCES AND EVENTS

- 6.10 TARIFF & REGULATORY LANDSCAPE

- 6.10.1 TARIFF AND REGULATIONS RELATED TO POLYESTER FILM

- TABLE 12 TARIFFS RELATED TO POLYESTER FILM MARKET

- 6.10.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 MIDDLE EAST & AFRICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 SOUTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.10.3 REGULATIONS RELATED TO POLYESTER FILM MARKET

- TABLE 18 NORTH AMERICA: LIST OF REGULATIONS FOR POLYESTER FILM MARKET

- TABLE 19 EUROPE: LIST OF REGULATIONS FOR POLYESTER FILM MARKET

- TABLE 20 ASIA PACIFIC: LIST OF REGULATIONS FOR POLYESTER FILM MARKET

- 6.11 PORTER'S FIVE FORCES ANALYSIS

- TABLE 21 IMPACT OF PORTER'S FIVE FORCES ON POLYESTER FILM MARKET

- FIGURE 26 PORTER'S FIVE FORCES ANALYSIS: POLYESTER FILM MARKET

- 6.11.1 THREAT OF NEW ENTRANTS

- 6.11.2 THREAT OF SUBSTITUTES

- 6.11.3 BARGAINING POWER OF SUPPLIERS

- 6.11.4 BARGAINING POWER OF BUYERS

- 6.11.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.12 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 27 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP FIVE APPLICATIONS

- TABLE 22 INFLUENCE OF INSTITUTIONAL BUYERS ON BUYING PROCESS FOR TOP FIVE APPLICATIONS

- 6.12.2 BUYING CRITERIA

- FIGURE 28 KEY BUYING CRITERIA FOR APPLICATIONS

- TABLE 23 KEY BUYING CRITERIA FOR APPLICATIONS

- 6.13 MACROECONOMIC INDICATORS

- 6.13.1 GDP TRENDS AND FORECASTS OF MAJOR ECONOMIES

- TABLE 24 GDP TRENDS AND FORECASTS, BY KEY COUNTRY, 2019-2028 (USD MILLION)

- 6.14 CASE STUDY

- 6.14.1 USE OF RECYCLED POLYESTER IN DIFFERENT APPLICATIONS

- 6.14.2 DETERMINING PURITY OF POLYESTER FILMS FOR USE IN ENCAPSULATION OF COLLECTION MATERIALS

- 6.14.3 EVALUATION OF INDIGENOUSLY MANUFACTURED GARFILM-EM-250 µM THICK POLYESTER FILM AS DOSIMETER FOR HIGH DOSE APPLICATIONS

7 POLYESTER FILM MARKET, BY TYPE

- 7.1 INTRODUCTION

- FIGURE 29 BIAXIALLY-ORIENTED FILMS TO LEAD MARKET DURING FORECAST PERIOD

- TABLE 25 POLYESTER FILM MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 26 POLYESTER FILM MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 27 POLYESTER FILM MARKET, BY TYPE, 2019-2022 (KILOTON)

- TABLE 28 POLYESTER FILM MARKET, BY TYPE, 2023-2028 (KILOTON)

- 7.2 BIAXIALLY-ORIENTED FILMS

- 7.2.1 SUPERIOR DIMENSIONAL STABILITY, TENSILE STRENGTH, AND OPTICAL CLARITY

- 7.3 THERMAL FILMS

- 7.3.1 ENGINEERED TO WITHSTAND HIGH TEMPERATURES

- 7.4 METALIZED FILMS

- 7.4.1 VERSATILE FILMS WITH REFLECTIVE, BARRIER, AND INSULATING PROPERTIES

- 7.5 HOLOGRAPHIC FILMS

- 7.5.1 ENGINEERED TO PRODUCE DYNAMIC AND THREE-DIMENSIONAL VISUAL EFFECTS WHEN EXPOSED TO LIGHT

- 7.6 UV STABILIZED FILMS

- 7.6.1 ENGINEERED TO PROVIDE EXCEPTIONAL PROTECTION AGAINST UV RADIATION

- 7.7 MATTE FILMS

- 7.7.1 DESIGNED TO REDUCE GLARE, MINIMIZE REFLECTION, AND PROVIDE SOFT DIFFUSED APPEARANCE

- 7.8 BARRIER FILMS

- 7.8.1 SUPERIOR PROTECTION AGAINST PENETRATION OF GASES, MOISTURE, AND OTHER ENVIRONMENTAL FACTORS

- 7.9 OTHER FILMS

- 7.9.1 CONDUCTIVE FILMS

- 7.9.1.1 Engineered to provide electrical conductivity while retaining flexibility and durability

- 7.9.2 RELEASE FILMS

- 7.9.2.1 Prevent adhesion between adhesive materials and various surfaces during manufacturing process

- 7.9.3 ANTI-STATIC FILMS

- 7.9.3.1 Engineered to control and dissipate static electricity

- 7.9.1 CONDUCTIVE FILMS

8 POLYESTER FILM MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- FIGURE 30 PACKAGING TO LEAD POLYESTER FILM MARKET DURING FORECAST PERIOD

- TABLE 29 POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 30 POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.2 PACKAGING

- 8.2.1 ENHANCED BARRIER PROPERTIES, COUPLED WITH TRANSPARENCY, DURABILITY, AND RECYCLABILITY

- 8.3 INDUSTRIAL LAMINATES

- 8.3.1 ABILITY TO COMBINE WITH OTHER MATERIALS FOR SPECIFIC PERFORMANCE CHARACTERISTICS

- 8.4 IMAGING & PRINTING

- 8.4.1 ENHANCED OPTICAL CLARITY, DIMENSIONAL STABILITY, AND PRINTABILITY

- 8.5 ELECTRICAL INSULATION

- 8.5.1 EXCEPTIONAL DIELECTRIC PROPERTIES, THERMAL RESISTANCE, AND DURABILITY

- 8.6 SOLAR PANELS

- 8.6.1 UV RESISTANCE, MOISTURE RESISTANCE, AND THERMAL STABILITY

- 8.7 OTHER APPLICATIONS

- 8.7.1 AGRICULTURE & HORTICULTURE

- 8.7.1.1 Enhancing crop protection, optimizing growth conditions, and managing environmental influences

- 8.7.2 AUTOMATED CUTTING & ENGRAVING

- 8.7.2.1 Enhanced accuracy, efficiency, and customization allow precise replication of designs on various surfaces

- 8.7.1 AGRICULTURE & HORTICULTURE

9 POLYESTER FILM MARKET, BY THICKNESS

- 9.1 INTRODUCTION

- FIGURE 31 <50 MICRONS FILM SEGMENT TO DOMINATE POLYESTER FILM MARKET DURING FORECAST PERIOD

- TABLE 31 POLYESTER FILM MARKET, BY THICKNESS, 2019-2022 (USD MILLION)

- TABLE 32 POLYESTER FILM MARKET, BY THICKNESS, 2023-2028 (USD MILLION)

- 9.2 <50 MICRONS

- 9.2.1 THINNESS, FLEXIBILITY, AND VERSATILITY FOR VARIOUS INNOVATIVE APPLICATIONS

- 9.3 51-100 MICRONS

- 9.3.1 BALANCE BETWEEN FLEXIBILITY, STRENGTH, AND DURABILITY

- 9.4 101-200 MICRONS

- 9.4.1 VERSATILITY AND ROBUSTNESS MAKE THEM PREFERABLE CHOICE

- 9.5 201-300 MICRONS

- 9.5.1 ENHANCED COMBINATION OF STRENGTH, RIGIDITY, AND LONGEVITY

- 9.6 >300 MICRONS

- 9.6.1 SUPERIOR STRENGTH, DURABILITY, AND RIGIDITY

10 POLYESTER FILM MARKET, BY END-USE INDUSTRY

- 10.1 INTRODUCTION

- FIGURE 32 ELECTRICAL & ELECTRONICS END-USE INDUSTRY TO DOMINATE MARKET DURING FORECAST PERIOD

- TABLE 33 POLYESTER FILM MARKET, BY END-USE INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 34 POLYESTER FILM MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- 10.2 FOOD & BEVERAGE

- 10.2.1 VERSATILITY, PRINTABILITY, AND BARRIER PROPERTIES TO DRIVE DEMAND

- 10.3 ELECTRICAL & ELECTRONICS

- 10.3.1 VERSATILE MATERIAL FOR WIDE RANGE OF APPLICATIONS

- 10.4 PHARMACEUTICAL

- 10.4.1 SUITABLE FOR STERILE AND MOISTURE-SENSITIVE APPLICATIONS

- 10.5 TEXTILE

- 10.5.1 CREATION OF FUNCTIONAL, DECORATIVE, AND HIGH-PERFORMANCE TEXTILES

- 10.6 MEDICAL

- 10.6.1 BIOCOMPATIBILITY, RESISTANCE TO STERILIZATION PROCESSES, AND CLARITY

- 10.7 MOBILITY & TRANSPORTATION

- 10.7.1 ENHANCEMENT OF SAFETY, COMFORT, AND AESTHETICS OF VEHICLES AND TRANSPORTATION INFRASTRUCTURE

- 10.8 OTHER END-USE INDUSTRIES

- 10.8.1 BUILDING & CONSTRUCTION

- 10.8.1.1 Improved safety, security, aesthetics, and energy efficiency of buildings

- 10.8.2 SPORTS & RECREATION

- 10.8.2.1 Strength, durability, and resistance to environmental factors

- 10.8.1 BUILDING & CONSTRUCTION

11 POLYESTER FILM MARKET, BY REGION

- 11.1 INTRODUCTION

- FIGURE 33 ASIA PACIFIC TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

- TABLE 35 POLYESTER FILM MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 36 POLYESTER FILM MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 37 POLYESTER FILM MARKET, BY REGION, 2019-2022 (KILOTON)

- TABLE 38 POLYESTER FILM MARKET, BY REGION, 2023-2028 (KILOTON)

- TABLE 39 POLYESTER FILM MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 40 POLYESTER FILM MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 41 POLYESTER FILM MARKET, BY TYPE, 2019-2022 (KILOTON)

- TABLE 42 POLYESTER FILM MARKET, BY TYPE, 2023-2028 (KILOTON)

- TABLE 43 POLYESTER FILM MARKET, BY THICKNESS, 2019-2022 (USD MILLION)

- TABLE 44 POLYESTER FILM MARKET, BY THICKNESS, 2023-2028 (USD MILLION)

- TABLE 45 POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 46 POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 47 POLYESTER FILM MARKET, BY END-USE INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 48 POLYESTER FILM MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- 11.2 ASIA PACIFIC

- 11.2.1 RECESSION IMPACT

- FIGURE 34 ASIA PACIFIC: POLYESTER FILM MARKET SNAPSHOT

- TABLE 49 ASIA PACIFIC: POLYESTER FILM MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 50 ASIA PACIFIC: POLYESTER FILM MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 51 ASIA PACIFIC: POLYESTER FILM MARKET, BY COUNTRY, 2019-2022 (KILOTON)

- TABLE 52 ASIA PACIFIC: POLYESTER FILM MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- TABLE 53 ASIA PACIFIC: POLYESTER FILM MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 54 ASIA PACIFIC: POLYESTER FILM MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 55 ASIA PACIFIC: POLYESTER FILM MARKET, BY TYPE, 2019-2022 (KILOTON)

- TABLE 56 ASIA PACIFIC: POLYESTER FILM MARKET, BY TYPE, 2023-2028 (KILOTON)

- TABLE 57 ASIA PACIFIC: POLYESTER FILM MARKET, BY THICKNESS, 2019-2022 (USD MILLION)

- TABLE 58 ASIA PACIFIC: POLYESTER FILM MARKET, BY THICKNESS, 2023-2028 (USD MILLION)

- TABLE 59 ASIA PACIFIC: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 60 ASIA PACIFIC: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 61 ASIA PACIFIC: POLYESTER FILM MARKET, BY END-USE INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 62 ASIA PACIFIC: POLYESTER FILM MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- 11.2.2 CHINA

- 11.2.2.1 Heavy capital investment in packaging material to drive market

- TABLE 63 CHINA: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 64 CHINA: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.2.3 JAPAN

- 11.2.3.1 Largest market for polyester film products

- TABLE 65 JAPAN: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 66 JAPAN: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.2.4 SOUTH KOREA

- 11.2.4.1 Dynamic private sector and investment by public companies to drive industrial growth

- TABLE 67 SOUTH KOREA: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 68 SOUTH KOREA: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.2.5 INDIA

- 11.2.5.1 Investment by major players to drive growth

- TABLE 69 INDIA: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 70 INDIA: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.2.6 REST OF ASIA PACIFIC

- TABLE 71 REST OF ASIA PACIFIC: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 72 REST OF ASIA PACIFIC: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.3 NORTH AMERICA

- 11.3.1 RECESSION IMPACT

- FIGURE 35 NORTH AMERICA: POLYESTER FILM MARKET SNAPSHOT

- TABLE 73 NORTH AMERICA: POLYESTER FILM MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 74 NORTH AMERICA: POLYESTER FILM MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 75 NORTH AMERICA: POLYESTER FILM MARKET, BY COUNTRY, 2019-2022 (KILOTON)

- TABLE 76 NORTH AMERICA: POLYESTER FILM MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- TABLE 77 NORTH AMERICA: POLYESTER FILM MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 78 NORTH AMERICA: POLYESTER FILM MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 79 NORTH AMERICA: POLYESTER FILM MARKET, BY TYPE, 2019-2022 (KILOTON)

- TABLE 80 NORTH AMERICA: POLYESTER FILM MARKET, BY TYPE, 2023-2028 (KILOTON)

- TABLE 81 NORTH AMERICA: POLYESTER FILM MARKET, BY THICKNESS, 2019-2022 (USD MILLION)

- TABLE 82 NORTH AMERICA: POLYESTER FILM MARKET, BY THICKNESS, 2023-2028 (USD MILLION)

- TABLE 83 NORTH AMERICA: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 84 NORTH AMERICA: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 85 NORTH AMERICA: POLYESTER FILM MARKET, BY END-USE INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 86 NORTH AMERICA: POLYESTER FILM MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- 11.3.1.1 US

- 11.3.1.1.1 Expansion of construction, automotive, furniture, and packaging industries to drive demand

- 11.3.1.1 US

- TABLE 87 US: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 88 US: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.3.2 CANADA

- 11.3.2.1 Plastic and packaging industry to drive demand

- TABLE 89 CANADA: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 90 CANADA: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.3.3 MEXICO

- 11.3.3.1 Evolving food & beverage industry to drive demand

- TABLE 91 MEXICO: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 92 MEXICO: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.4 EUROPE

- 11.4.1 RECESSION IMPACT

- FIGURE 36 EUROPE: POLYESTER FILM MARKET SNAPSHOT

- TABLE 93 EUROPE: POLYESTER FILM MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 94 EUROPE: POLYESTER FILM MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 95 EUROPE: POLYESTER FILM MARKET, BY COUNTRY, 2019-2022 (KILOTON)

- TABLE 96 EUROPE: POLYESTER FILM MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- TABLE 97 EUROPE: POLYESTER FILM MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 98 EUROPE: POLYESTER FILM MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 99 EUROPE: POLYESTER FILM MARKET, BY TYPE, 2019-2022 (KILOTON)

- TABLE 100 EUROPE: POLYESTER FILM MARKET, BY TYPE, 2023-2028 (KILOTON)

- TABLE 101 EUROPE: POLYESTER FILM MARKET, BY THICKNESS, 2019-2022 (USD MILLION)

- TABLE 102 EUROPE: POLYESTER FILM MARKET, BY THICKNESS, 2023-2028 (USD MILLION)

- TABLE 103 EUROPE: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 104 EUROPE: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 105 EUROPE: POLYESTER FILM MARKET, BY END-USE INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 106 EUROPE: POLYESTER FILM MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- 11.4.2 GERMANY

- 11.4.2.1 Largest potential market for big industries such as automotive and construction

- TABLE 107 GERMANY: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 108 GERMANY: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.4.3 ITALY

- 11.4.3.1 Largest economy in Europe with well-developed petrochemical industry

- TABLE 109 ITALY: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 110 ITALY: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.4.4 FRANCE

- 11.4.4.1 Presence of many established players to drive market

- TABLE 111 FRANCE: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 112 FRANCE: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.4.5 UK

- 11.4.5.1 Rapid growth in construction sector to drive market

- TABLE 113 UK: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 114 UK: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.4.6 RUSSIA

- 11.4.6.1 High versatility of polyester films to drive demand

- TABLE 115 RUSSIA: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 116 RUSSIA: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.4.7 SPAIN

- 11.4.7.1 Increased demand for safe vehicles to drive market

- TABLE 117 SPAIN: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 118 SPAIN: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.4.8 REST OF EUROPE

- TABLE 119 REST OF EUROPE: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 120 REST OF EUROPE: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 RECESSION IMPACT

- FIGURE 37 MIDDLE EAST & AFRICA: POLYESTER FILM MARKET SNAPSHOT

- TABLE 121 MIDDLE EAST & AFRICA: POLYESTER FILM MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 122 MIDDLE EAST & AFRICA: POLYESTER FILM MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 123 MIDDLE EAST & AFRICA: POLYESTER FILM MARKET, BY COUNTRY, 2019-2022 (KILOTON)

- TABLE 124 MIDDLE EAST & AFRICA: POLYESTER FILM MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- TABLE 125 MIDDLE EAST & AFRICA: POLYESTER FILM MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 126 MIDDLE EAST & AFRICA: POLYESTER FILM MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 127 MIDDLE EAST & AFRICA: POLYESTER FILM MARKET, BY TYPE, 2019-2022 (KILOTON)

- TABLE 128 MIDDLE EAST & AFRICA: POLYESTER FILM MARKET, BY TYPE, 2023-2028 (KILOTON)

- TABLE 129 MIDDLE EAST & AFRICA: POLYESTER FILM MARKET, BY THICKNESS, 2019-2022 (USD MILLION)

- TABLE 130 MIDDLE EAST & AFRICA: POLYESTER FILM MARKET, BY THICKNESS, 2023-2028 (USD MILLION)

- TABLE 131 MIDDLE EAST & AFRICA: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 132 MIDDLE EAST & AFRICA: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 133 MIDDLE EAST & AFRICA: POLYESTER FILM MARKET, BY END-USE INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 134 MIDDLE EAST & AFRICA: POLYESTER FILM MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- 11.5.2 SAUDI ARABIA

- 11.5.2.1 Industrial growth to drive polyester film market

- TABLE 135 SAUDI ARABIA: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 136 SAUDI ARABIA: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.5.3 SOUTH AFRICA

- 11.5.3.1 Rapid growth in manufacturing industry to drive demand

- TABLE 137 SOUTH AFRICA: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 138 SOUTH AFRICA: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.5.4 REST OF MIDDLE EAST & AFRICA

- TABLE 139 REST OF MIDDLE EAST & AFRICA: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 140 REST OF MIDDLE EAST & AFRICA: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.6 SOUTH AMERICA

- 11.6.1 RECESSION IMPACT

- FIGURE 38 SOUTH AMERICA: POLYESTER FILM MARKET SNAPSHOT

- TABLE 141 SOUTH AMERICA: POLYESTER FILM MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 142 SOUTH AMERICA: POLYESTER FILM MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 143 SOUTH AMERICA: POLYESTER FILM MARKET, BY COUNTRY, 2019-2022 (KILOTON)

- TABLE 144 SOUTH AMERICA: POLYESTER FILM MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- TABLE 145 SOUTH AMERICA: POLYESTER FILM MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 146 SOUTH AMERICA: POLYESTER FILM MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 147 SOUTH AMERICA: POLYESTER FILM MARKET, BY TYPE, 2019-2022 (KILOTON)

- TABLE 148 SOUTH AMERICA: POLYESTER FILM MARKET, BY TYPE, 2023-2028 (KILOTON)

- TABLE 149 SOUTH AMERICA: POLYESTER FILM MARKET, BY THICKNESS, 2019-2022 (USD MILLION)

- TABLE 150 SOUTH AMERICA: POLYESTER FILM MARKET, BY THICKNESS, 2023-2028 (USD MILLION)

- TABLE 151 SOUTH AMERICA: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 152 SOUTH AMERICA: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 153 SOUTH AMERICA: POLYESTER FILM MARKET, BY END-USE INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 154 SOUTH AMERICA: POLYESTER FILM MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- 11.6.2 BRAZIL

- 11.6.2.1 Largest share in GDP of South America

- TABLE 155 BRAZIL: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 156 BRAZIL: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.6.3 ARGENTINA

- 11.6.3.1 Industrial sector of Argentina to drive demand

- TABLE 157 ARGENTINA: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 158 ARGENTINA: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.6.4 REST OF SOUTH AMERICA

- TABLE 159 REST OF SOUTH AMERICA: POLYESTER FILM MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 160 REST OF SOUTH AMERICA: POLYESTER FILM MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 STRATEGIES ADOPTED BY KEY PLAYERS

- TABLE 161 OVERVIEW OF STRATEGIES ADOPTED BY KEY POLYESTER FILM MANUFACTURERS

- 12.3 MARKET SHARE ANALYSIS

- 12.3.1 RANKING OF KEY MARKET PLAYERS, 2022

- FIGURE 39 RANKING OF TOP FIVE PLAYERS IN POLYESTER FILM MARKET, 2022

- 12.3.2 MARKET SHARE OF KEY PLAYERS

- TABLE 162 POLYESTER FILM MARKET: DEGREE OF COMPETITION

- FIGURE 40 POLYESTER FILM MARKET IN 2022

- 12.3.2.1 Toyobo Co., Ltd.

- 12.3.2.2 Polyplex Corporation Ltd.

- 12.3.2.3 Kolon Industries Inc.

- 12.3.2.4 Toray Industries Inc.

- 12.3.2.5 Polifilm Extrusion GmbH

- 12.4 REVENUE ANALYSIS

- FIGURE 41 REVENUE OF KEY PLAYERS, 2020-2024

- 12.5 COMPANY EVALUATION MATRIX (TIER 1)

- 12.5.1 STARS

- 12.5.2 EMERGING LEADERS

- 12.5.3 PERVASIVE PLAYERS

- 12.5.4 PARTICIPANTS

- FIGURE 42 POLYESTER FILM MARKET: COMPANY EVALUATION MATRIX, 2022 (TIER 1)

- 12.5.5 COMPANY FOOTPRINT

- TABLE 163 POLYESTER FILM MARKET: KEY COMPANY APPLICATION FOOTPRINT

- TABLE 164 POLYESTER FILM MARKET: KEY COMPANY END-USE INDUSTRY FOOTPRINT

- TABLE 165 POLYESTER FILM MARKET: KEY COMPANY TYPE FOOTPRINT

- TABLE 166 POLYESTER FILM MARKET: KEY COMPANY REGION FOOTPRINT

- 12.6 START-UP/SME EVALUATION MATRIX

- 12.6.1 PROGRESSIVE COMPANIES

- 12.6.2 RESPONSIVE COMPANIES

- 12.6.3 DYNAMIC COMPANIES

- 12.6.4 STARTING BLOCKS

- FIGURE 43 POLYESTER FILM MARKET: START-UP/SME EVALUATION MATRIX, 2022

- 12.6.5 COMPETITIVE BENCHMARKING

- TABLE 167 POLYESTER FILM MARKET: DETAILED LIST OF KEY START-UPS/SMES

- TABLE 168 POLYESTER FILMS MARKET: COMPETITIVE BENCHMARKING OF KEY PLAYERS [START-UPS/SMES], BY APPLICATION

- TABLE 169 POLYESTER FILMS MARKET: COMPETITIVE BENCHMARKING OF KEY PLAYERS [START-UPS/SMES], BY TYPE

- TABLE 170 POLYESTER FILM MARKET: COMPETITIVE BENCHMARKING OF KEY PLAYERS [START-UPS/SMES], BY END-USE INDUSTRY

- TABLE 171 POLYESTER FILM MARKET: COMPETITIVE BENCHMARKING OF KEY PLAYERS [START-UPS/SMES], BY REGION

- 12.7 COMPETITIVE SCENARIOS AND TRENDS

- 12.7.1 PRODUCT LAUNCHES

- TABLE 172 POLYESTER FILM MARKET: PRODUCT LAUNCHES (2019-2023)

- 12.7.2 DEALS

- TABLE 173 POLYESTER FILM MARKET: DEALS (2019-2023)

- 12.7.3 OTHER DEVELOPMENTS

- TABLE 174 POLYESTER FILM: OTHER DEVELOPMENTS (2019-2023)

13 COMPANY PROFILES

- (Business Overview, Products/Solutions/Services Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats))**

- 13.1 KEY PLAYERS

- 13.1.1 TORAY INDUSTRIES, INC.

- TABLE 175 TORAY INDUSTRIES, INC.: COMPANY OVERVIEW

- FIGURE 44 TORAY INDUSTRIES, INC.: COMPANY SNAPSHOT

- TABLE 176 TORAY INDUSTRIES, INC.: PRODUCT OFFERINGS

- TABLE 177 TORAY INDUSTRIES, INC.: PRODUCT LAUNCHES

- TABLE 178 TORAY INDUSTRIES, INC.: OTHER DEVELOPMENTS

- 13.1.2 KOLON INDUSTRIES, INC.

- TABLE 179 KOLON INDUSTRIES, INC.: COMPANY OVERVIEW

- FIGURE 45 KOLON INDUSTRIES, INC.: COMPANY SNAPSHOT

- TABLE 180 KOLON INDUSTRIES, INC.: PRODUCT OFFERINGS

- TABLE 181 KOLON INDUSTRIES, INC.: PRODUCT LAUNCHES

- 13.1.3 TOYOBO CO., LTD.

- TABLE 182 TOYOBO CO., LTD.: COMPANY OVERVIEW

- FIGURE 46 TOYOBO CO., LTD.: COMPANY SNAPSHOT

- TABLE 183 TOYOBO CO. LTD.: PRODUCT OFFERINGS

- TABLE 184 TOYOBO CO. LTD.: DEALS

- TABLE 185 TOYOBO CO. LTD.: OTHER DEVELOPMENTS

- 13.1.4 POLYPLEX

- TABLE 186 POLYPLEX: COMPANY OVERVIEW

- FIGURE 47 POLYPLEX: COMPANY SNAPSHOT

- TABLE 187 POLYPLEX: PRODUCT OFFERINGS

- TABLE 188 POLYPLEX: OTHER DEVELOPMENTS

- 13.1.5 ESTER INDUSTRIES LIMITED

- TABLE 189 ESTER INDUSTRIES LIMITED: COMPANY OVERVIEW

- FIGURE 48 ESTER INDUSTRIES LIMITED: COMPANY SNAPSHOT

- TABLE 190 ESTER INDUSTRIES LIMITED: PRODUCT OFFERINGS

- TABLE 191 ESTER INDUSTRIES LIMITED: OTHER DEVELOPMENTS

- 13.1.6 DUPONT TEIJIN FILMS

- TABLE 192 DUPONT TEIJIN FILMS: COMPANY OVERVIEW

- TABLE 193 DUPONT TEIJIN FILMS: PRODUCT OFFERINGS

- TABLE 194 DUPONT TEIJIN FILMS: PRODUCT LAUNCHES

- TABLE 195 DUPONT TEIJIN FILMS: DEALS

- 13.1.7 MITSUBISHI POLYESTER FILM GMBH

- TABLE 196 MITSUBISHI POLYESTER FILM GMBH: COMPANY OVERVIEW

- TABLE 197 MITSUBISHI POLYESTER FILM GMBH: PRODUCT OFFERINGS

- TABLE 198 MITSUBISHI POLYESTER FILM GMBH: OTHER DEVELOPMENTS

- 13.1.8 POLIFILM EXTRUSION GMBH.

- TABLE 199 POLIFILM EXTRUSION GMBH: COMPANY OVERVIEW

- TABLE 200 POLIFILM EXTRUSION GMBH: PRODUCT OFFERINGS

- TABLE 201 POLIFILM EXTRUSION GMBH: DEALS

- TABLE 202 POLIFILM EXTRUSION GMBH: OTHER DEVELOPMENTS

- 13.1.9 TERPHANE

- TABLE 203 TERPHANE: COMPANY OVERVIEW

- TABLE 204 TERPHANE: PRODUCT OFFERINGS

- TABLE 205 TERPHANE: PRODUCT LAUNCHES

- TABLE 206 TERPHANE: DEALS

- TABLE 207 TERPHANE: OTHER DEVELOPMENTS

- 13.1.10 JINDAL POLY FILMS LTD.

- TABLE 208 JINDAL POLY FILMS LTD.: COMPANY OVERVIEW

- FIGURE 49 JINDAL POLY FILMS LTD.: COMPANY SNAPSHOT

- TABLE 209 JINDAL POLY FILMS LTD.: PRODUCT OFFERINGS

- TABLE 210 JINDAL POLY FILMS LTD.: DEALS

- TABLE 211 JINDAL POLY FILMS LTD.: OTHER DEVELOPMENTS

- 13.2 OTHER PLAYERS

- 13.2.1 SEALED AIR CORPORATION

- TABLE 212 SEALED AIR CORPORATION: COMPANY OVERVIEW

- 13.2.2 OBEN HOLDING GROUP

- TABLE 213 OBEN HOLDING GROUP: COMPANY OVERVIEW

- 13.2.3 RADICI PARTECIPAZIONI SPA

- TABLE 214 RADICI PARTECIPAZIONI SPA: COMPANY OVERVIEW

- 13.2.4 AEP INDUSTRIES

- TABLE 215 AEP INDUSTRIES: COMPANY OVERVIEW

- 13.2.5 UFLEX LIMITED

- TABLE 216 UFLEX LIMITED: COMPANY OVERVIEW

- 13.2.6 AMCOR PLC

- TABLE 217 AMCOR PLC: COMPANY OVERVIEW

- 13.2.7 BERRY GLOBAL GROUP, INC.

- TABLE 218 BERRY GLOBAL GROUP, INC.: COMPANY OVERVIEW

- 13.2.8 DOW

- TABLE 219 DOW: COMPANY OVERVIEW

- 13.2.9 EASTMAN CHEMICAL COMPANY

- TABLE 220 EASTMAN CHEMICAL COMPANY: COMPANY OVERVIEW

- 13.2.10 IMPAK FILMS US LLC

- TABLE 221 IMPAK FILMS US LLC : COMPANY OVERVIEW

- 13.2.11 POLINAS

- TABLE 222 POLINAS: COMPANY OVERVIEW

- 13.2.12 FUTAMURA CHEMICAL CO. LTD.

- TABLE 223 FUTAMURA CHEMICAL CO. LTD.: COMPANY OVERVIEW

- 13.2.13 SUMILON POLYESTER LTD.

- TABLE 224 SUMILON POLYESTER LTD.: COMPANY OVERVIEW

- 13.2.14 AMERPLAST

- TABLE 225 AMERPLAST: COMPANY OVERVIEW

- 13.2.15 ZHEJIANG WUZHOU POLYESTER FILM CO., LTD.

- TABLE 226 ZHEJIANG WUZHOU POLYESTER FILM CO., LTD.: COMPANY OVERVIEW

- *Details on Business Overview, Products/Solutions/Services Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats) might not be captured in case of unlisted companies.

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS