|

市場調査レポート

商品コード

1851114

BOPPフィルム:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)BOPP Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| BOPPフィルム:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月24日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

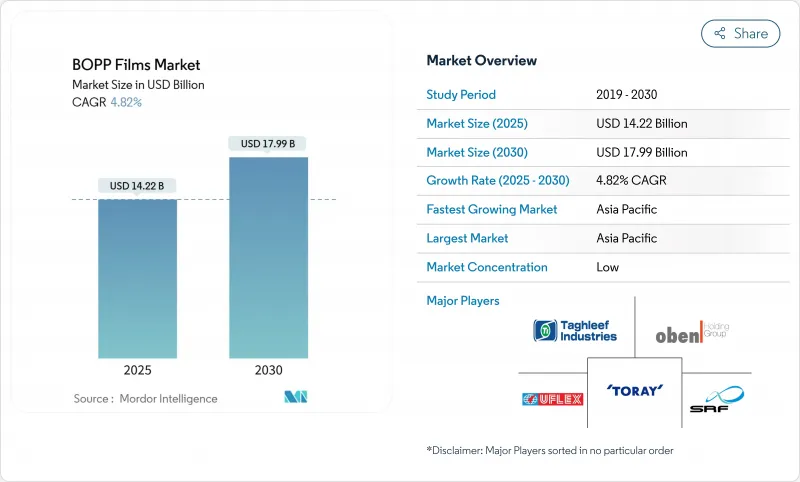

BOPPフィルムの世界市場規模は2025年に142億2,000万米ドル、2030年には179億9,000万米ドルに拡大し、予測期間のCAGRは4.82%になると予測されています。

成長の背景には、規制の合理化によって食品接触承認サイクルが短縮され、スナック、医薬品、eコマース包装向けの新規二軸延伸ポリプロピレン(BOPP)配合の採用が加速していることがあります。デジタル小売の増加により、ブランドオーナーは軽量でヒートシール可能なメーラーフィルムを好むようになっています。一方、ポリプロピレン樹脂の価格変動(北米では2025年初頭に1ポンド当たり4~5セント上昇)は、コンバーターのマージンを圧迫し続けており、垂直統合とヘッジ手段を奨励しています。政策面では、欧州連合(EU)の包装・包装廃棄物規制(PPWR)が2030年までにすべての包装材をリサイクル可能にすることを要求しており、世界のサプライチェーン全体で単一素材のBOPP構造に対する需要を喚起しています。

世界のBOPPフィルム市場動向と洞察

発展途上国における高密着性スナック包装の需要急増

都市部での食料品の拡大と地域スナックブランドのプレミアム化が、BOPPフィルム市場を透明で高光沢グレードへと押し上げています。Haldiram社のようなインドのスナックメーカーは現在、透明BOPPを活用して賞味期限を最大20%延長し、近代的な小売店の陳列で製品の視認性を高めています。東南アジアでも、検査が容易なシースルーパックを好む食品安全規則によって、同様のシフトが進んでいます。この動きは、改ざん防止シールによって廃棄物を減らしながら、コスト効率の良いバリア性能を実現します。PETに比べて低い変換コストに後押しされた新興企業は、2030年まで持続的な需要を確保するため、引き続き主要な採用企業であり続ける。

ブランドオーナーが持続可能性目標のためにPVCラップからBOPPに切り替える

ハロゲン基材を排除する規制圧力は、PVCラップからBOPPへの世界的な軸足を加速させています。ユニリーバは、2026年までにポリ塩化ビニールを全廃するという2024年のコミットメントにより、食品およびパーソナルケア製品ラインのフレキシブルパックの素材としてBOPPフィルムを選択することになりました。ネスレ社では、この移行によりリサイクル物流が簡素化され、10~15%のコスト削減が実現しました。また、菓子類のラップをBOPPに移行したことで、リサイクル率は23%から87%に急上昇しました。コンバーターは新しいシーリング・ジョーや設備の改修に投資しているが、コンプライアンス費用の低下とブランド・エクイティの向上が設備投資のハードルを打ち消しています。

ポリプロピレン樹脂価格の変動

北米のポリプロピレン価格は2025年初頭にポンド当たり4~5セント上昇し、2024年からの同様の上昇に呼応しました。インドのBOPP価格は1トン当たり1,020米ドルに達したが、20%の新規生産能力に対して国内需要は11%の増加にとどまり、業界の収益性は10年間で最低の8%になりました。コンバーターはキャッシュフローのひっ迫に直面し、規模の経済を得るためにM&Aを加速させています。

セグメント分析

メタライズドフィルムは2030年までCAGR 8.36%の見通しを確保しました。透明フィルムは2024年に金額ベースでBOPPフィルム市場の51.32%を占め、製品の鮮度を強調するスナックやベーカリーのウィンドウに不可欠であることが証明されました。高真空メタライザーへのコンバーター投資は、より軽量でプレミアム箔と同等の性能をサポートします。これと並行して、ブリスターオーバーラップ用のメタライズドグレードに関連するBOPPフィルム市場規模は、厳格な安定性要件に後押しされ、2030年までに30億米ドルを超えると予測されます。

白色、不透明、真珠光沢の各グレードは、ラベルストック、テープ、高級ラップに使用され、美的コントラストとUV不透明性を提供します。しかし、そのシェアは汎用クリアグレードに比べニッチです。AluBondやAlOxのような特殊コーティングは、金属との接着性や光学的透明性を向上させることで用途の幅を広げ、規制対象の医薬品カートンの中でPVdCコーティングPVCの代替品としてBOPPフィルム市場を強化しています。

45µm以上のフィルムは、機械的剛性を必要とする工業用テープ、肥料袋、スタンドアップパウチのおかげでCAGR 7.54%で成長しています。それでも15~30µm分野は市場セグメンテーションの36.34%を占め、コストバランスの取れたスナック菓子用ラップやラベルの主流を維持しています。逐次二軸延伸技術は現在、機械方向配向度を12まで引き上げ、かつてはより重いゲージに限定されていた性能を、より薄いフィルムにもたらします。この技術シフトは、非重要パッケージングにおけるヘビーゲージの優位性を徐々に侵食する可能性があります。

15µm以下のニッチは、巻き取りやパンクの懸念に直面しているが、ポリマー核剤と制御された冷却により、プロセスの安定性が向上しています。ミドルウェイトの30~45µmフィルムは、医薬品のオーバーラップやプレミアムコーヒーライナーの定番であり続け、剛性とバリア要求のバランスを保っています。このような多様性は、BOPPフィルム市場の根底にある多層的な成長プロファイルを示しています。

本レポートは二軸延伸ポリプロピレンフィルムの市場分析をカバーし、フィルムタイプ(透明、メタライズド、その他)、厚さ(15mm未満、15~30mm、その他)、用途(包装、ラベリング、ラップアラウンド、その他)、エンドユーザーバーティカル(食品、飲食品、その他)、地域(北米、欧州、アジア太平洋、南米、中東アフリカ)で区分しています。

地域分析

アジア太平洋地域は2024年の収益の45.21%を占め、8.43%という最も速い年平均成長率(CAGR)を記録しており、特にインドにおける2024年度から2025年度にかけてのポリマー消費量の8.5%の成長がこれを裏付けています。一貫生産、低い人件費、スナックや医薬品需要への近接性が構造的な優位性を生み出しています。とはいえ、オレフィンの供給過剰とレガシー資産の未稼働がマージンの重荷となっており、選択的な操業停止と輸出のリバランスを促しています。

北米では、eコマースが地方への配送を拡大し、メーラーフィルムの消費に拍車をかけているため、需要は着実に伸びています。しかし、樹脂のボラティリティはコンバーターの収益性に課題をもたらし、垂直統合とリサイクル・コンテンツの革新に拍車をかけています。欧州では、PPWR規制を満たすための高バリア性リサイクル対応ラミネートが中心となっており、現地ブランドオーナーの間でモノマテリアルBOPPへの投資が促進されています。

中東・アフリカは、インフラ整備の恩恵を受けています。UFlexのエジプト工場は、消費者市場の近くに位置し、欧州への貿易アクセスを活用しています。南米では、現地の食品加工業者がブランド化された保存可能なスナック菓子を目指しているが、通貨変動と樹脂の輸入依存が成長を抑制しています。これらの地域別の物語は、BOPPフィルム市場が地理的に多様な軌道を描いていることを裏付けています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 発展途上国における高透明度スナック菓子包装への需要急増

- ブランドオーナーが持続可能性を目標にPVCラップからBOPPに変更

- eコマースブームがヒートシール可能なBOPPメーラーフィルムを牽引

- ポリオレフィン総合メーカーによる急速な生産能力増強

- リサイクル対応モノマテリアル積層板の商品化

- 市場抑制要因

- ポリプロピレン樹脂価格の変動

- 中国のレガシーラインの未稼働が世界のマージンを押し下げる

- プレミアムニッチにおけるバイオベースバリアフィルムとの競合

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 主要マクロ経済動向の市場への影響

第5章 市場規模と成長予測

- フィルムタイプ別

- 透明

- メタライズド

- 不透明/白

- 真珠光沢

- その他のフィルムタイプ

- 厚さ別

- 15μm未満

- 15-30µm

- 30-45µm

- 45μm以上

- 用途別

- パッケージ

- ラベリングとラップアラウンド

- ラミネート加工

- 感圧テープ

- その他のアプリケーション

- エンドユーザー業界別

- 食品

- 飲料

- 製薬・医療

- パーソナルケアと化粧品

- 産業

- その他のエンドユーザー業界別

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ケニア

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Taghleef Industries

- Jindal Poly Films

- Toray Industries

- SRF Limited

- Uflex Ltd

- Cosmo Films

- Polyplex Corp

- Oben Holding Group

- Treofan Group

- Vacmet India

- NAN YA Plastics

- Mitsui Chemicals Tohcello

- Futamura Chemical

- Innovia Films

- Irplast S.p.A

- Inteplast Group

- Biofilm SA

- Manucor Spa

- Dunmore Corp

- Tatrafan SRO