|

|

市場調査レポート

商品コード

1323876

コネクテッド航空機の世界市場:タイプ別、プラットフォーム別、コネクティビティ別、地域別-2028年までの予測Connected Aircraft Market by Type, Platform, Connectivity & Region - Global Forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| コネクテッド航空機の世界市場:タイプ別、プラットフォーム別、コネクティビティ別、地域別-2028年までの予測 |

|

出版日: 2023年07月28日

発行: MarketsandMarkets

ページ情報: 英文 235 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

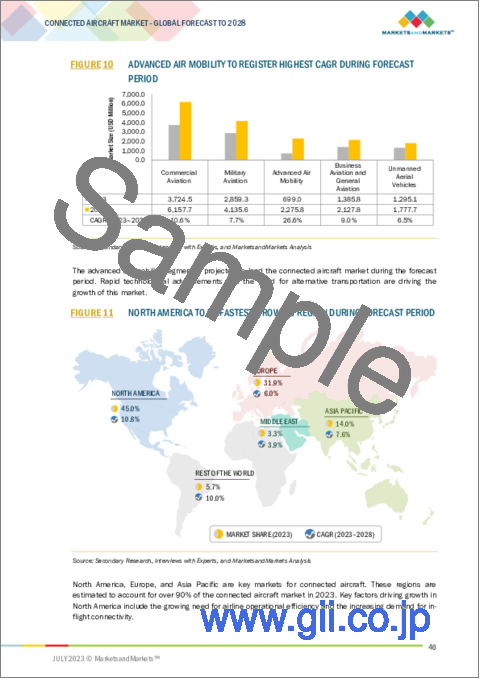

コネクテッド航空機の市場規模は、2023年の100億米ドルから2028年には165億米ドルに成長すると予測され、2023年から2028年までのCAGRは10.6%と見込まれています。

コネクテッド航空機は、航空機と地上システム間のリアルタイムデータ伝送を容易にし、航空会社がフライトオペレーションをモニターし最適化することを可能にします。これにより、燃費効率の向上、メンテナンス費用の最小化、全体的な運航効率の向上が期待できます。

タイプ別では、ソフトウェア分野が予測期間中にコネクテッド航空機市場で最も高い成長を遂げると予測されています。航空機のコネクテッド化が進むにつれ、サイバーセキュリティが重要な関心事となっています。航空会社やメーカーが航空機システムを潜在的なサイバー脅威や攻撃から守るために強固なサイバーセキュリティソリューションに投資しているため、ソフトウェアセグメントは成長を目の当たりにしています。

プラットフォーム別では、Advanced Air Mobility(AAM)セグメントは予測期間中、市場で最も高いCAGRを持つと予測されています。AAMプラットフォームは、自律飛行システム、電気推進、高度通信ネットワークなどの先進技術に大きく依存しています。これらの分野における継続的な開発とイノベーションが、AAMプラットフォームの成長を促進しています。

コネクティビティ別では、予測期間中、機内コネクティビティ分野がコネクテッド航空機市場をリードすると予測されます。技術の進歩により、機内接続はより信頼性が高く、より高速で、コスト効率に優れています。先進的な衛星通信システムおよび空対地通信システムの開発により、機内インターネットサービスの品質が大幅に向上しています。

コネクテッド航空機市場は、北米が強い経済力を誇り、研究開発への投資もかなりの水準に達しています。この資金力により、航空会社や航空宇宙企業は先進的なコネクテッド航空機技術に投資することができます。この地域は、技術企業、航空会社、航空宇宙メーカー間の連携を促進しています。こうしたパートナーシップにより、革新的なコネクテッド航空機ソリューションの開発と展開が促進されます。北米の民間航空業界はまた、大手航空会社、航空機リース会社、および相当数の運航航空機を擁する強固で広範な業界です。このような大規模な事業は、コネクテッド航空機ソリューションにとって重要な市場となっています。

当レポートでは、世界のコネクテッド航空機市場について調査し、市場の概要とともに、タイプ別、プラットフォーム別、コネクティビティ別、地域別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- コネクテッド航空機市場に対する景気後退の影響

- バリューチェーン分析

- 顧客のビジネスに影響を与える動向/混乱

- 生態系マッピング

- ポーターのファイブフォース分析

- 価格分析

- プラットフォーム別のボリュームデータ

- 関税と規制状況

- 貿易分析

- 主要な利害関係者と購入基準

- 2023年~2024年の主要な会議とイベント

- 技術分析

- 使用事例分析

第6章 業界の動向

- イントロダクション

- 技術動向

- メガトレンドの影響

- イノベーションと特許分析

- 技術ロードマップ

第7章 コネクテッド航空機市場、タイプ別

- イントロダクション

- ハードウェア

- ソフトウェア

第8章 コネクテッド航空機市場、プラットフォーム別

- イントロダクション

- 民間航空

- ビジネス航空および一般航空

- 軍用航空

- 無人航空機

- AAM

第9章 コネクテッド航空機市場、コネクティビティ別

- イントロダクション

- 機内

- 空対空

- 空対地

第10章 コネクテッド航空機市場、地域別

- イントロダクション

- 北米

- 欧州

- アジア太平洋

- 中東

- その他の地域

第11章 競合情勢

第12章 企業プロファイル

- 主要参入企業

- GOGO INC.

- HONEYWELL INTERNATIONAL INC.

- RAYTHEON TECHNOLOGIES CORPORATION

- THALES GROUP

- VIASAT INC.

- TE CONNECTIVITY LTD.

- COBHAM PLC

- BAE SYSTEMS

- PANASONIC AVIONICS CORPORATION

- ANUVU

- KONTRON AG

- ASTRONICS

- IRIDIUM COMMUNICATIONS INC.

- RAMCO SYSTEMS

- GARMIN

- その他の企業

- BROTECS

- APIJET LLC

- EXSYN AVIATION SOLUTIONS

- FLIGHT DATA SYSTEMS

- JEPPESEN

- FLEETPLAN.NET

- BYTRON AVIATION SYSTEMS

- ULTRAMAIN

- FLIGHTMAN

- DONICA INTERNATIONAL INC.

第13章 付録

The Connected Aircraft Market size is projected to grow from USD 10.0 billion in 2023 to USD 16.5 billion by 2028, at a CAGR of 10.6% from 2023 to 2028. Connected aircraft facilitate real-time data transmission between the aircraft and ground systems, enabling airlines to monitor and optimize flight operations. This, in turn, can result in enhanced fuel efficiency, minimized maintenance expenses, and overall improved operational efficiency.

The Software segment is expected to grow the highest during the forecast period.

Based on type, the software segment is projected to grow the highest in the Connected Aircraft Market during the forecast period. As aircraft become more connected, cybersecurity becomes a crucial concern. The software segment is witnessing growth as airlines and manufacturers invest in robust cybersecurity solutions to protect aircraft systems from potential cyber threats and attacks.

The Advanced Air Mobility segment is projected to have the highest CAGR in the market during the forecast period.

Based on the platform, the Advanced Air Mobility (AAM) segment is expected to have the highest CAGR in the market during the forecast period. AAM platforms heavily rely on advanced technologies, such as autonomous flight systems, electric propulsion, and advanced communication networks. Ongoing developments and innovations in these areas are driving the growth of AAM platforms.

In-flight connectivity is projected to lead the Connected Aircraft Market during the forecast period.

Based on connectivity, the in-flight connectivity segment is projected to lead the Connected Aircraft Market during the forecast period. Technological advancements have made in-flight connectivity more reliable, faster, and cost-effective. The development of advanced satellite and air-to-ground communication systems has significantly improved the quality of in-flight internet services.

North America is expected to account for the largest market share in 2023.

The Connected Aircraft market has been studied for the regions North America, Europe, Asia Pacific, and Rest of the World. North America boasts a strong economy and a significant level of investment in research and development. This financial capacity allows airlines and aerospace companies to invest in advanced connected aircraft technologies. The region fosters collaborations between technology companies, airlines, and aerospace manufacturers. These partnerships facilitate the development and deployment of innovative connected aircraft solutions. The commercial aviation industry in North America is also robust and extensive, with major airlines, aircraft leasing companies, and a substantial fleet of operational aircraft. This sizable scale of operations presents a significant market for connected aircraft solutions.

The break-up of the profile of primary participants in the Connected Aircraft Market:

- By Company Type: Tier 1 - 55%, Tier 2 - 25%, and Tier 3 - 20%

- By Designation: C Level - 50%, Director Level - 25%, Others-25%

- By Region: North America - 47%, Europe - 21%, Asia Pacific - 21%, Rest of the World - 11%.

Prominent companies include Honeywell International (US), Raytheon Technologies Corporation (US), Thales Group (France), Viasat Inc (US), and Gogo Inc (US) are some of the major players.

Research Coverage:

The report segments the Connected Aircraft Market based on Type (Hardware, Software), By Platform (Commercial Aviation, Military Aviation, Business Aviation and General Aviation, Unmanned Aerial Vehicles,

Advanced Air Mobility), By Connectivity (In-Flight Connectivity, Air-to-Air Connectivity, Air-to-Ground Connectivity), and Region. The Connected Aircraft Market has been studied in North America, Europe, Asia Pacific, the Middle East, and the Rest of the World. The scope of the report covers extensive information covering market overviews, such as drivers, restraints, challenges, and opportunities, that drive the growth in the market. Analysis of key players in the industry providing business overviews, products, solutions, and services, key strategies, recent developments, and new product & service launches associated with the Connected Aircraft market is also covered in the report. An extensive competitive analysis of the key players and the up-and-coming startups in the Connected Aircraft Ecosystem is also covered in the report.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall Connected Aircraft Market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Growing demand to increase airline operational efficiency; Increasing demand for in-flight connectivity; Rising demand for enhanced airline and passenger safety; Advancements in communication technologies), restraints (Limited bandwidth for connected aircraft; Cybersecurity risks), opportunities (Enhancing aircraft maintenance with connected aircraft solutions; Increased focus on predictive maintenance), and challenges (Lack of skilled labor; Software updates and maintenance challenges in connected aircraft) influencing the growth of the connected aircraft market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the Connected Aircraft Market

- Market Development: Comprehensive information about lucrative markets - the report analyses the Connected Aircraft Market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the Connected Aircraft Market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players in the Connected Aircraft Market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- FIGURE 1 CONNECTED AIRCRAFT MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- 1.3.3 YEARS CONSIDERED

- 1.4 INCLUSIONS AND EXCLUSIONS

- TABLE 1 INCLUSIONS AND EXCLUSIONS

- 1.5 CURRENCY CONSIDERED

- TABLE 2 USD EXCHANGE RATES

- 1.6 LIMITATIONS

- 1.7 MARKET STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

- 1.8.1 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 RESEARCH PROCESS FLOW

- FIGURE 3 RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary sources

- 2.1.2.2 Key data from primary sources

- FIGURE 4 BREAKDOWN OF PRIMARY INTERVIEWS

- 2.2 FACTOR ANALYSIS

- 2.2.1 INTRODUCTION

- 2.2.2 DEMAND-SIDE INDICATORS

- 2.2.3 SUPPLY-SIDE INDICATORS

- 2.2.4 RECESSION IMPACT ANALYSIS

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 BOTTOM-UP APPROACH

- 2.3.1.1 Market size estimation and methodology

- FIGURE 5 BOTTOM-UP APPROACH

- 2.3.2 TOP-DOWN APPROACH

- FIGURE 6 TOP-DOWN APPROACH

- 2.3.1 BOTTOM-UP APPROACH

- 2.4 DATA TRIANGULATION

- FIGURE 7 DATA TRIANGULATION

- 2.5 RESEARCH ASSUMPTIONS

3 EXECUTIVE SUMMARY

- FIGURE 8 SOFTWARE TO BE LARGEST SEGMENT DURING FORECAST PERIOD

- FIGURE 9 AIR-TO-GROUND CONNECTIVITY TO SURPASS OTHER SEGMENTS DURING FORECAST PERIOD

- FIGURE 10 ADVANCED AIR MOBILITY TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 11 NORTH AMERICA TO BE FASTEST-GROWING REGION DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CONNECTED AIRCRAFT MARKET

- FIGURE 12 INCREASING DEMAND FOR ENHANCED PASSENGER EXPERIENCE

- 4.2 CONNECTED AIRCRAFT MARKET, BY TYPE

- FIGURE 13 COMMERCIAL AVIATION TO SECURE MAXIMUM MARKET SHARE IN 2023

- 4.3 CONNECTED AIRCRAFT MARKET, BY HARDWARE TYPE

- FIGURE 14 SATELLITE COMMUNICATIONS SYSTEMS TO RECORD HIGHEST CAGR BETWEEN 2023 AND 2028

- 4.4 CONNECTED AIRCRAFT MARKET, BY COUNTRY

- FIGURE 15 GERMANY TO BE FASTEST-GROWING COUNTRY DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 16 CONNECTED AIRCRAFT MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Need for optimum airline operations

- 5.2.1.2 Increased demand for in-flight connectivity

- 5.2.1.3 Improved airline and passenger safety

- 5.2.1.4 Advancements in communications technologies

- 5.2.2 RESTRAINTS

- 5.2.2.1 Limited availability of bandwidth

- 5.2.2.2 Cybersecurity risks

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Integration of advanced aircraft solutions

- 5.2.3.2 Emphasis on predictive maintenance

- 5.2.4 CHALLENGES

- 5.2.4.1 Lack of skilled labor

- 5.2.4.2 Challenges associated with software updates and maintenance

- 5.3 IMPACT OF RECESSION ON CONNECTED AIRCRAFT MARKET

- 5.4 VALUE CHAIN ANALYSIS

- FIGURE 17 VALUE CHAIN ANALYSIS

- 5.4.1 RAW MATERIALS

- 5.4.2 R&D

- 5.4.3 COMPONENT MANUFACTURING

- 5.4.4 ASSEMBLERS AND INTEGRATORS

- 5.4.5 END USERS

- 5.5 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 18 REVENUE SHIFT CURVE

- 5.6 ECOSYSTEM MAPPING

- 5.6.1 PROMINENT COMPANIES

- 5.6.2 PRIVATE AND SMALL ENTERPRISES

- 5.6.3 END USERS

- FIGURE 19 CONNECTED AIRCRAFT MARKET ECOSYSTEM MAP

- TABLE 3 CONNECTED AIRCRAFT MARKET ECOSYSTEM

- 5.7 PORTER'S FIVE FORCES ANALYSIS

- TABLE 4 PORTER'S FIVE FORCE ANALYSIS

- 5.7.1 THREAT OF NEW ENTRANTS

- 5.7.2 THREAT OF SUBSTITUTES

- 5.7.3 BARGAINING POWER OF SUPPLIERS

- 5.7.4 BARGAINING POWER OF BUYERS

- 5.7.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.8 PRICING ANALYSIS

- TABLE 5 AVERAGE PRICE ANALYSIS OF CONNECTED AIRCRAFT SOLUTIONS

- 5.9 VOLUME DATA, BY PLATFORM

- TABLE 6 VOLUME DATA, BY PLATFORM, 2023-2028 (UNITS)

- 5.10 TARIFF AND REGULATORY LANDSCAPE

- TABLE 7 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER AGENCIES

- TABLE 8 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER AGENCIES

- TABLE 9 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER AGENCIES

- 5.11 TRADE ANALYSIS

- TABLE 10 COUNTRY-WISE IMPORTS, 2019-2022 (USD THOUSAND)

- TABLE 11 COUNTRY-WISE EXPORTS, 2019-2022 (USD THOUSAND)

- 5.12 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 20 INFLUENCE OF STAKEHOLDERS ON BUYING CONNECTED AIRCRAFT, BY TYPE

- TABLE 12 INFLUENCE OF STAKEHOLDERS ON BUYING CONNECTED AIRCRAFT, BY TYPE (%)

- 5.12.2 BUYING CRITERIA

- FIGURE 21 KEY BUYING CRITERIA FOR CONNECTED AIRCRAFT, BY TYPE

- TABLE 13 KEY BUYING CRITERIA FOR CONNECTED AIRCRAFT, BY TYPE

- 5.13 KEY CONFERENCES AND EVENTS, 2023-2024

- TABLE 14 KEY CONFERENCES AND EVENTS, 2023-2024

- 5.14 TECHNOLOGY ANALYSIS

- 5.14.1 ROBOTICS

- 5.14.2 DATA ANALYTICS

- 5.15 USE CASE ANALYSIS

- 5.15.1 CONNECTED AIRCRAFT SYSTEMS FOR MILITARY OPERATIONS

- 5.15.2 COMMUNICATIONS SYSTEMS FOR AIRCRAFT

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 TECHNOLOGY TRENDS

- 6.2.1 5G

- 6.2.2 ARTIFICIAL INTELLIGENCE (AI) AND MACHINE LEARNING (ML)

- 6.2.3 ADVANCED SENSORS AND INTERNET OF THINGS (IOT)

- 6.2.4 AUGMENTED REALITY (AR) AND VIRTUAL REALITY (VR)

- 6.2.5 BLOCKCHAIN TECHNOLOGY

- 6.3 IMPACT OF MEGATRENDS

- 6.3.1 CLOUD COMPUTING

- 6.3.2 QUANTUM COMPUTING

- 6.3.3 SUSTAINABLE TECHNOLOGIES

- 6.4 INNOVATIONS AND PATENT ANALYSIS

- TABLE 15 PATENTS FOR CONNECTED AIRCRAFT

- 6.5 TECHNOLOGICAL ROADMAP

- FIGURE 22 TECHNOLOGICAL ADVANCEMENTS IN CONNECTED AIRCRAFT

7 CONNECTED AIRCRAFT MARKET, BY TYPE

- 7.1 INTRODUCTION

- FIGURE 23 CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028

- TABLE 16 CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 17 CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 7.2 HARDWARE

- TABLE 18 HARDWARE: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 19 HARDWARE: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 7.2.1 SATELLITE COMMUNICATIONS SYSTEMS

- 7.2.1.1 Need for connectivity in adverse weather conditions to drive growth

- 7.2.2 DATA MANAGEMENT SYSTEMS

- 7.2.2.1 Improved operational efficiency to drive growth

- 7.2.3 INTERFACING DEVICES

- 7.2.3.1 Demand for enhanced passenger experience to drive growth

- 7.2.4 OTHERS

- 7.3 SOFTWARE

- TABLE 20 SOFTWARE: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 21 SOFTWARE: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

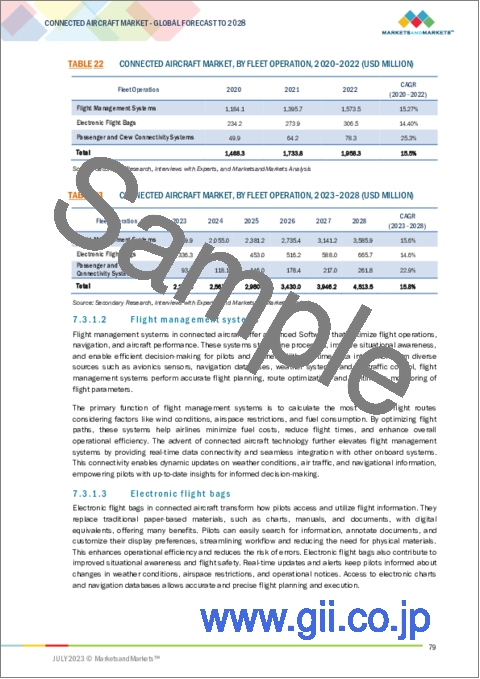

- 7.3.1 FLEET OPERATIONS

- 7.3.1.1 Optimum management and performance to drive growth

- TABLE 22 CONNECTED AIRCRAFT MARKET, BY FLEET OPERATION, 2020-2022 (USD MILLION)

- TABLE 23 CONNECTED AIRCRAFT MARKET, BY FLEET OPERATION, 2023-2028 (USD MILLION)

- 7.3.1.2 Flight management systems

- 7.3.1.3 Electronic flight bags

- 7.3.1.4 Passenger and crew connectivity systems

- 7.3.2 FLEET MONITORING

- 7.3.2.1 Predictive maintenance and real-time monitoring to drive growth

- TABLE 24 CONNECTED AIRCRAFT MARKET, BY FLEET MONITORING, 2020-2022 (USD MILLION)

- TABLE 25 CONNECTED AIRCRAFT MARKET, BY FLEET MONITORING, 2023-2028 (USD MILLION)

- 7.3.2.2 Fuel and engine monitoring systems

- 7.3.2.3 Structure monitoring systems

- 7.3.2.4 Component monitoring systems

8 CONNECTED AIRCRAFT MARKET, BY PLATFORM

- 8.1 INTRODUCTION

- FIGURE 24 CONNECTED AIRCRAFT MARKET, BY PLATFORM, 2023-2028

- TABLE 26 CONNECTED AIRCRAFT MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 27 CONNECTED AIRCRAFT MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- 8.2 COMMERCIAL AVIATION

- TABLE 28 COMMERCIAL AVIATION: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 29 COMMERCIAL AVIATION: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 8.2.1 NARROW-BODY AIRCRAFT

- 8.2.1.1 Increased passenger demand to drive growth

- 8.2.2 WIDE-BODY AIRCRAFT

- 8.2.2.1 Improved performance and safety to drive growth

- 8.2.3 REGIONAL JETS

- 8.2.3.1 Better passenger connectivity to drive growth

- 8.2.4 COMMERCIAL HELICOPTERS

- 8.2.4.1 Widespread use in emergency services to drive growth

- 8.3 BUSINESS AVIATION AND GENERAL AVIATION

- TABLE 30 BUSINESS AVIATION AND GENERAL AVIATION: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 31 BUSINESS AVIATION AND GENERAL AVIATION: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 8.3.1 BUSINESS JETS

- 8.3.1.1 Emphasis on privacy and comfort to drive growth

- 8.3.2 LIGHT AND ULTRALIGHT AIRCRAFT

- 8.3.2.1 Improved flying experience to drive growth

- 8.4 MILITARY AVIATION

- TABLE 32 MILITARY AVIATION: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 33 MILITARY AVIATION: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 8.4.1 FIGHTER AIRCRAFT

- 8.4.1.1 increased operational agility to drive growth

- 8.4.2 TRANSPORT AIRCRAFT

- 8.4.2.1 Logistics management and fuel efficiency to drive growth

- 8.4.3 SPECIAL MISSION AIRCRAFT

- 8.4.3.1 Need for enhanced mission capabilities to drive growth

- 8.4.4 MILITARY HELICOPTERS

- 8.4.4.1 Ability to support critical missions to drive growth

- 8.5 UNMANNED AERIAL VEHICLES

- TABLE 34 UNMANNED AERIAL VEHICLES: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 35 UNMANNED AERIAL VEHICLES: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 8.5.1 MILITARY

- 8.5.1.1 Rising defense investments to drive growth

- 8.5.2 COMMERCIAL

- 8.5.2.1 Advanced sensor and flight capabilities to drive growth

- 8.5.3 GOVERNMENT AND LAW

- 8.5.3.1 Efficient monitoring and surveillance to drive growth

- 8.6 ADVANCED AIR MOBILITY

- TABLE 36 ADVANCED AIR MOBILITY: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 37 ADVANCED AIR MOBILITY: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 8.6.1 AIR TAXIS

- 8.6.1.1 Expanding urban population to drive growth

- 8.6.2 AIR SHUTTLES AND AIR METROS

- 8.6.2.1 Development of cutting-edge technologies to drive growth

- 8.6.3 PERSONAL AIR VEHICLES

- 8.6.3.1 Demand for safe and convenient transportation to drive growth

- 8.6.4 CARGO AIR VEHICLES

- 8.6.4.1 Rapid deployment in commercial logistics industry to drive growth

- 8.6.5 AIR AMBULANCES AND MEDICAL EMERGENCY VEHICLES

- 8.6.5.1 Growing demand from health industry to drive growth

9 CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY

- 9.1 INTRODUCTION

- FIGURE 25 CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028

- TABLE 38 CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 39 CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 9.2 IN-FLIGHT CONNECTIVITY

- 9.2.1 DEMAND FOR INTERNET AND OTHER SERVICES TO DRIVE GROWTH

- 9.3 AIR-TO-AIR CONNECTIVITY

- 9.3.1 NEED FOR SAFETY TO DRIVE GROWTH

- 9.4 AIR-TO-GROUND CONNECTIVITY

- 9.4.1 NEED FOR REAL-TIME INFORMATION TO DRIVE GROWTH

10 CONNECTED AIRCRAFT MARKET, BY REGION

- 10.1 INTRODUCTION

- FIGURE 26 CONNECTED AIRCRAFT MARKET, BY REGION, 2023-2028

- TABLE 40 CONNECTED AIRCRAFT MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 41 CONNECTED AIRCRAFT MARKET, BY REGION, 2023-2028 (USD MILLION)

- 10.2 NORTH AMERICA

- 10.2.1 RECESSION IMPACT ANALYSIS

- 10.2.2 PESTLE ANALYSIS

- FIGURE 27 NORTH AMERICA: CONNECTED AIRCRAFT MARKET SNAPSHOT

- TABLE 42 NORTH AMERICA: CONNECTED AIRCRAFT MARKET, BY COUNTRY, 2020-2022 (USD MILLION)

- TABLE 43 NORTH AMERICA: CONNECTED AIRCRAFT MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 44 NORTH AMERICA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 45 NORTH AMERICA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 46 NORTH AMERICA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 47 NORTH AMERICA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.2.3 US

- 10.2.3.1 Increased preference for in-flight connectivity to drive growth

- TABLE 48 US: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 49 US: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 50 US: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 51 US: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.2.4 CANADA

- 10.2.4.1 Demand for real-time data analytics to drive growth

- TABLE 52 CANADA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 53 CANADA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 54 CANADA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 55 CANADA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.3 EUROPE

- 10.3.1 RECESSION IMPACT ANALYSIS

- 10.3.2 PESTLE ANALYSIS

- FIGURE 28 EUROPE: CONNECTED AIRCRAFT MARKET SNAPSHOT

- TABLE 56 EUROPE: CONNECTED AIRCRAFT MARKET, BY COUNTRY, 2020-2022 (USD MILLION)

- TABLE 57 EUROPE: CONNECTED AIRCRAFT MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 58 EUROPE: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 59 EUROPE: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 60 EUROPE: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 61 EUROPE: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.3.3 FRANCE

- 10.3.3.1 Integration of advanced technologies to drive growth

- TABLE 62 FRANCE: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 63 FRANCE: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 64 FRANCE: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 65 FRANCE: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.3.4 GERMANY

- 10.3.4.1 Increased R&D activities to drive growth

- TABLE 66 GERMANY: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 67 GERMANY: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 68 GERMANY: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 69 GERMANY: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.3.5 ITALY

- 10.3.5.1 Demand for real-time connectivity to drive growth

- TABLE 70 ITALY: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 71 ITALY: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 72 ITALY: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 73 ITALY: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.3.6 UK

- 10.3.6.1 Need for better fuel efficiency to drive growth

- TABLE 74 UK: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 75 UK: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 76 UK: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 77 UK: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.3.7 RUSSIA

- 10.3.7.1 Installation of connectivity solutions in existing fleets to drive growth

- TABLE 78 RUSSIA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 79 RUSSIA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 80 RUSSIA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 81 RUSSIA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.3.8 REST OF EUROPE

- TABLE 82 REST OF EUROPE: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 83 REST OF EUROPE: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 84 REST OF EUROPE: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 85 REST OF EUROPE: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.4 ASIA PACIFIC

- 10.4.1 RECESSION IMPACT ANALYSIS

- 10.4.2 PESTLE ANALYSIS

- FIGURE 29 ASIA PACIFIC: CONNECTED AIRCRAFT MARKET SNAPSHOT

- TABLE 86 ASIA PACIFIC: CONNECTED AIRCRAFT MARKET, BY COUNTRY, 2020-2022 (USD MILLION)

- TABLE 87 ASIA PACIFIC: CONNECTED AIRCRAFT MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 88 ASIA PACIFIC: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 89 ASIA PACIFIC: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 90 ASIA PACIFIC: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 91 ASIA PACIFIC: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.4.3 CHINA

- 10.4.3.1 Low maintenance costs to drive growth

- TABLE 92 CHINA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 93 CHINA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 94 CHINA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 95 CHINA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.4.4 INDIA

- 10.4.4.1 Rising technology adoption by airlines to drive growth

- TABLE 96 INDIA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 97 INDIA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 98 INDIA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 99 INDIA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.4.5 JAPAN

- 10.4.5.1 Rapid adoption of advanced connectivity solutions to drive growth

- TABLE 100 JAPAN: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 101 JAPAN: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 102 JAPAN: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 103 JAPAN: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.4.6 AUSTRALIA

- 10.4.6.1 Ongoing technological advancements to drive growth

- TABLE 104 AUSTRALIA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 105 AUSTRALIA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 106 AUSTRALIA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 107 AUSTRALIA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.4.7 SOUTH KOREA

- 10.4.7.1 Emphasis on smart and connected solutions to drive growth

- TABLE 108 SOUTH KOREA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 109 SOUTH KOREA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 110 SOUTH KOREA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 111 SOUTH KOREA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.4.8 REST OF ASIA PACIFIC

- TABLE 112 REST OF ASIA PACIFIC: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 113 REST OF ASIA PACIFIC: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 114 REST OF ASIA PACIFIC: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 115 REST OF ASIA PACIFIC: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.5 MIDDLE EAST

- 10.5.1 RECESSION IMPACT ANALYSIS

- 10.5.2 PESTLE ANALYSIS

- FIGURE 30 MIDDLE EAST: CONNECTED AIRCRAFT MARKET SNAPSHOT

- TABLE 116 MIDDLE EAST: CONNECTED AIRCRAFT MARKET, BY COUNTRY, 2020-2022 (USD MILLION)

- TABLE 117 MIDDLE EAST: CONNECTED AIRCRAFT MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 118 MIDDLE EAST: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 119 MIDDLE EAST: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 120 MIDDLE EAST: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 121 MIDDLE EAST: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.5.3 SAUDI ARABIA

- 10.5.3.1 Demand for improved in-flight experience to drive growth

- TABLE 122 SAUDI ARABIA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 123 SAUDI ARABIA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 124 SAUDI ARABIA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 125 SAUDI ARABIA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.5.4 UAE

- 10.5.4.1 Increased investments in connected aircraft to drive growth

- TABLE 126 UAE: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 127 UAE: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 128 UAE: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 129 UAE: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.5.5 ISRAEL

- 10.5.5.1 Expertise in advanced communications systems and data analytics to drive growth

- TABLE 130 ISRAEL: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 131 ISRAEL: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 132 ISRAEL: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 133 ISRAEL: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.5.6 REST OF MIDDLE EAST

- TABLE 134 REST OF MIDDLE EAST: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 135 REST OF MIDDLE EAST: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 136 REST OF MIDDLE EAST: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 137 REST OF MIDDLE EAST: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.6 REST OF THE WORLD

- 10.6.1 RECESSION IMPACT ANALYSIS

- TABLE 138 REST OF THE WORLD: CONNECTED AIRCRAFT MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 139 REST OF THE WORLD: CONNECTED AIRCRAFT MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 140 REST OF THE WORLD: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 141 REST OF THE WORLD: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 142 REST OF THE WORLD: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 143 REST OF THE WORLD: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.6.2 LATIN AMERICA

- 10.6.2.1 Improved interconnected air travel to drive growth

- TABLE 144 LATIN AMERICA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 145 LATIN AMERICA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 146 LATIN AMERICA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 147 LATIN AMERICA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

- 10.6.3 AFRICA

- 10.6.3.1 Domestic fleet upgrades to drive growth

- TABLE 148 AFRICA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2020-2022 (USD MILLION)

- TABLE 149 AFRICA: CONNECTED AIRCRAFT MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 150 AFRICA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2020-2022 (USD MILLION)

- TABLE 151 AFRICA: CONNECTED AIRCRAFT MARKET, BY CONNECTIVITY, 2023-2028 (USD MILLION)

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- TABLE 152 STRATEGIES ADOPTED BY KEY PLAYERS IN CONNECTED AIRCRAFT MARKET, 2020-2023

- 11.2 MARKET SHARE ANALYSIS, 2022

- FIGURE 31 MARKET SHARE ANALYSIS OF KEY PLAYERS, 2022

- TABLE 153 CONNECTED AIRCRAFT MARKET: DEGREE OF COMPETITION, 2022

- 11.3 MARKET RANKING ANALYSIS, 2022

- FIGURE 32 MARKET RANKING OF KEY PLAYERS, 2022

- 11.4 REVENUE ANALYSIS, 2022

- FIGURE 33 REVENUE ANALYSIS OF KEY PLAYERS, 2022

- 11.5 COMPANY EVALUATION MATRIX, 2022

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- FIGURE 34 COMPANY EVALUATION MATRIX, 2022

- 11.6 COMPANY FOOTPRINT ANALYSIS

- TABLE 154 COMPANY FOOTPRINT

- TABLE 155 SEGMENT FOOTPRINT

- 11.7 START-UP/SME EVALUATION MATRIX, 2022

- 11.7.1 PROGRESSIVE COMPANIES

- 11.7.2 RESPONSIVE COMPANIES

- 11.7.3 DYNAMIC COMPANIES

- 11.7.4 STARTING BLOCKS

- FIGURE 35 START-UP/SME EVALUATION MATRIX, 2022

- TABLE 156 KEY START-UPS/SMES

- TABLE 157 COMPETITIVE BENCHMARKING OF KEY START-UPS/SMES

- 11.8 COMPETITIVE SCENARIO

- 11.8.1 PRODUCT LAUNCHES

- TABLE 158 PRODUCT LAUNCHES, 2020-2023

- 11.8.2 DEALS

- TABLE 159 DEALS, 2020-2023

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- (Business Overview, Products/Services/Solutions Offered, MnM View, Key Strengths and Right to Win, Strategic Choices Made, Weaknesses and Competitive Threats, Recent Developments)**

- 12.1.1 GOGO INC.

- TABLE 160 GOGO INC.: COMPANY OVERVIEW

- TABLE 161 GOGO INC.: PRODUCTS/SOLUTIONS OFFERED

- TABLE 162 GOGO INC.: DEALS

- 12.1.2 HONEYWELL INTERNATIONAL INC.

- TABLE 163 HONEYWELL INTERNATIONAL INC.: COMPANY OVERVIEW

- TABLE 164 HONEYWELL INTERNATIONAL INC.: PRODUCTS/SOLUTIONS OFFERED

- TABLE 165 HONEYWELL INTERNATIONAL INC.: DEALS

- 12.1.3 RAYTHEON TECHNOLOGIES CORPORATION

- TABLE 166 RAYTHEON TECHNOLOGIES CORPORATION: COMPANY OVERVIEW

- FIGURE 38 RAYTHEON TECHNOLOGIES CORPORATION: COMPANY SNAPSHOT

- TABLE 167 RAYTHEON TECHNOLOGIES CORPORATION: PRODUCTS/SOLUTIONS OFFERED

- TABLE 168 RAYTHEON TECHNOLOGIES CORPORATION: DEALS

- 12.1.4 THALES GROUP

- TABLE 169 THALES GROUP: COMPANY OVERVIEW

- FIGURE 39 THALES GROUP: COMPANY SNAPSHOT

- TABLE 170 THALES GROUP: PRODUCTS/SOLUTIONS OFFERED

- TABLE 171 THALES GROUP: DEALS

- 12.1.5 VIASAT INC.

- TABLE 172 VIASAT INC.: COMPANY OVERVIEW

- FIGURE 40 VIASAT INC.: COMPANY SNAPSHOT

- TABLE 173 VIASAT INC.: PRODUCTS/SOLUTIONS OFFERED

- TABLE 174 VIASAT INC.: DEALS

- 12.1.6 TE CONNECTIVITY LTD.

- TABLE 175 TE CONNECTIVITY LTD.: COMPANY OVERVIEW

- FIGURE 41 TE CONNECTIVITY: COMPANY SNAPSHOT

- TABLE 176 TE CONNECTIVITY LTD.: PRODUCTS/SOLUTIONS OFFERED

- 12.1.7 COBHAM PLC

- TABLE 177 COBHAM PLC: COMPANY OVERVIEW

- FIGURE 42 COBHAM PLC: COMPANY SNAPSHOT

- TABLE 178 COBHAM PLC: PRODUCTS/SOLUTIONS OFFERED

- TABLE 179 COBHAM PLC: DEALS

- 12.1.8 BAE SYSTEMS

- TABLE 180 BAE SYSTEMS: COMPANY OVERVIEW

- FIGURE 43 BAE SYSTEMS: COMPANY SNAPSHOT

- TABLE 181 BAE SYSTEMS: PRODUCTS/SOLUTIONS OFFERED

- TABLE 182 BAE SYSTEMS: PRODUCT LAUNCHES

- TABLE 183 BAE SYSTEMS: DEALS

- 12.1.9 PANASONIC AVIONICS CORPORATION

- TABLE 184 PANASONIC AVIONICS CORPORATION: COMPANY OVERVIEW

- TABLE 185 PANASONIC AVIONICS CORPORATION: PRODUCTS/SOLUTIONS OFFERED

- TABLE 186 PANASONIC AVIONICS CORPORATION: DEALS

- 12.1.10 ANUVU

- TABLE 187 ANUVU: COMPANY OVERVIEW

- TABLE 188 ANUVU: PRODUCTS/SOLUTIONS OFFERED

- TABLE 189 ANUVU: DEALS

- 12.1.11 KONTRON AG

- TABLE 190 KONTRON AG: COMPANY OVERVIEW

- FIGURE 44 KONTRON AG: COMPANY SNAPSHOT

- TABLE 191 KONTRON AG: PRODUCTS/SOLUTIONS OFFERED

- 12.1.12 ASTRONICS

- TABLE 192 ASTRONICS: COMPANY OVERVIEW

- FIGURE 45 ASTRONICS: COMPANY SNAPSHOT

- TABLE 193 ASTRONICS: PRODUCTS/SOLUTIONS OFFERED

- TABLE 194 ASTRONICS: DEALS

- 12.1.13 IRIDIUM COMMUNICATIONS INC.

- TABLE 195 IRIDIUM COMMUNICATIONS INC.: COMPANY OVERVIEW

- FIGURE 46 IRIDIUM COMMUNICATIONS INC.: COMPANY SNAPSHOT

- TABLE 196 IRIDIUM COMMUNICATIONS INC.: PRODUCTS/SOLUTIONS OFFERED

- TABLE 197 IRIDIUM COMMUNICATIONS INC.: DEALS

- 12.1.14 RAMCO SYSTEMS

- TABLE 198 RAMCO SYSTEMS: COMPANY OVERVIEW

- FIGURE 47 RAMCO SYSTEMS: COMPANY SNAPSHOT

- TABLE 199 RAMCO SYSTEMS: PRODUCTS/SOLUTIONS OFFERED

- TABLE 200 RAMCO SYSTEMS: DEALS

- 12.1.15 GARMIN

- TABLE 201 GARMIN: COMPANY OVERVIEW

- FIGURE 48 GARMIN: COMPANY SNAPSHOT

- TABLE 202 GARMIN: PRODUCTS/SOLUTIONS OFFERED

- TABLE 203 GARMIN: PRODUCT LAUNCHES

- TABLE 204 GARMIN: DEALS

- *Business Overview, Products/Services/Solutions Offered, MnM View, Key Strengths and Right to Win, Strategic Choices Made, Weaknesses and Competitive Threats, Recent Developments might not be captured in case of unlisted companies.

- 12.2 OTHER PLAYERS

- 12.2.1 BROTECS

- TABLE 205 BROTECS: COMPANY OVERVIEW

- 12.2.2 APIJET LLC

- TABLE 206 APIJET LLC: COMPANY OVERVIEW

- 12.2.3 EXSYN AVIATION SOLUTIONS

- TABLE 207 EXSYN AVIATION SOLUTIONS: COMPANY OVERVIEW

- 12.2.4 FLIGHT DATA SYSTEMS

- TABLE 208 FLIGHT DATA SYSTEMS: COMPANY OVERVIEW

- 12.2.5 JEPPESEN

- TABLE 209 JEPPESEN: COMPANY OVERVIEW

- 12.2.6 FLEETPLAN.NET

- TABLE 210 FLEETPLAN.NET: COMPANY OVERVIEW

- 12.2.7 BYTRON AVIATION SYSTEMS

- TABLE 211 BYTRON AVIATION SYSTEMS: COMPANY OVERVIEW

- 12.2.8 ULTRAMAIN

- TABLE 212 ULTRAMAIN: COMPANY OVERVIEW

- 12.2.9 FLIGHTMAN

- TABLE 213 FLIGHTMAN: COMPANY OVERVIEW

- 12.2.10 DONICA INTERNATIONAL INC.

- TABLE 214 DONICA INTERNATIONAL INC.: COMPANY OVERVIEW

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS