|

|

市場調査レポート

商品コード

1277591

医療向けエッジコンピューティングの世界市場:コンポーネント別(ハードウェア、ソフトウェア、サービス)、アプリケーション別(診断、ロボット手術、テレヘルス・RPM、救急車)、エンドユーザー別(病院、クリニック、外来診療センター)、地域別 - 2028年までの予測Edge Computing in Healthcare Market by Component (Hardware, Software, Services), Application (Diagnostics, Robotic Surgery, Telehealth, RPM, and Ambulances), End User (Hospitals, Clinics, Ambulatory Care Center), & Region - Global Forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 医療向けエッジコンピューティングの世界市場:コンポーネント別(ハードウェア、ソフトウェア、サービス)、アプリケーション別(診断、ロボット手術、テレヘルス・RPM、救急車)、エンドユーザー別(病院、クリニック、外来診療センター)、地域別 - 2028年までの予測 |

|

出版日: 2023年05月16日

発行: MarketsandMarkets

ページ情報: 英文 228 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界の医療向けエッジコンピューティングの市場規模は、2022年の推定41億米ドルから、2028年には129億米ドルまで拡大し、予測期間中にCAGRで26.1%の成長が予測されています。

エッジコンピューティングは、デバイス数の増加に伴い、インターネットサービスの利用が増加し、広帯域幅のアプリケーションに対する需要が高まっていることから、業界全体で人気を集めています。エッジコンピューティングは、低遅延、トラフィック分散、信頼性の向上、コスト削減など、さまざまな利点があるため、世界中の医療組織に急速に受け入れられてきています。

"ハードウェア:ハードウェアセグメントは、2022年に最大の市場シェアを占めると推定される"

ハードウェアによる高い市場シェアは、高いパフォーマンス、スケール、柔軟性を実現するために、医療機関がエッジハードウェアを大規模に導入していることに起因しています。市場のベンダーは、エッジインフラ全体を完成させる包括的なエッジハードウェア(コンピューティング、ストレージ、ネットワーキング用のエッジシステム)とハードウェアコンポーネント(コンピューティングシステム、ゲートウェイ/ルーター、サーバー、物理データセンター)を提供しています。エッジハードウェアは、収集、フィルタリング、処理、伝送、監視、ルーティングといったエッジの中核機能を実現するための通信と接続を確立するバックボーンとして機能します。

"テレヘルス・遠隔患者モニタリング(RPM)のアプリケーションが、予測期間中に最大の市場規模を占める"

アプリケーション別では、市場は診断、テレヘルス・遠隔患者モニタリング(RPM)、ロボット手術、救急車、その他のアプリケーションに区分されます。テレヘルス・遠隔患者モニタリング(RPM)は、予測期間中に最大の市場規模を占めると予想されます。エッジコンピューティングを活用することで、遠隔医療プロバイダーは、よりシームレスで統合された患者体験を提供し、患者の関与と満足度を向上させることができます。患者は、自宅に居ながら、医療専門家との遠隔診療を受け、医療記録にアクセスし、ウェアラブルデバイスを使用して自分の健康状態をモニタリングできます。

"予測期間中、欧州が、医療向けエッジコンピューティング市場で2番目に大きなシェアを占める"

北米は、エッジコンピューティングベンダーが多数存在すること、スマートテクノロジーの早期技術導入、戦略的パートナーシップの高まり、ワークロード中心のITインフラに対する需要などから、エッジコンピューティング市場で最大の市場規模を維持し、次いで欧州が続くと予想されています。政府のさまざまな取り組みや、欧州や北米の企業におけるデータ処理の差し迫ったニーズは、エッジコンピューティングベンダーが現地で事業を拡大する大きなチャンスとなっています。アジア太平洋とラテンアメリカでは、クラウドベースのサービス展開の拡大、ネットワーク接続の改善ニーズ、テクノロジー同化の進展、エッジコンピューティングの利点に対する認識の高まりにより、エッジコンピューティングソリューションの導入が進んでいます。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

第6章 業界動向

- イントロダクション

- 主要な業界動向の概要

- ケーススタディ分析

- エコシステム分析

- 価格分析

- 特許分析

- 技術分析

- サプライチェーン分析

- 主要な利害関係者と購入基準

- 主要な会議とイベント(2023年~2024年)

- ポーターのファイブフォース分析

- 規制状況

- 顧客のビジネスに影響を与える動向/混乱

第7章 医療向けエッジコンピューティング市場:コンポーネント別

- イントロダクション

- ハードウェア

- ソフトウェア

- サービス

第8章 医療向けエッジコンピューティング市場:アプリケーション別

- イントロダクション

- 診断

- ロボット手術

- テレヘルス・遠隔患者モニタリング(RPM)

- 救急車

- その他

第9章 医療向けエッジコンピューティング市場:エンドユーザー別

- イントロダクション

- 病院・クリニック

- 長期ケアセンター・在宅医療環境

- 外来診療センター

- その他

第10章 医療向けエッジコンピューティング市場:地域別

- イントロダクション

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他の欧州

- アジア太平洋地域

- 日本

- 韓国

- その他のアジア太平洋地域

- その他の地域

第11章 競合情勢

- イントロダクション

- 主要企業の戦略

- 上位市場企業の収益分析(2022年)

- 市場シェア分析(2022年)

- 競合ベンチマーキング

- 企業の評価象限

- スタートアップ/中小企業の評価象限

- 競合シナリオと動向

第12章 企業プロファイル

- 主要企業

- CISCO SYSTEMS, INC.

- HUAWEI TECHNOLOGIES CO., LTD.

- DELL TECHNOLOGIES, INC.

- AMAZON WEB SERVICES

- GOOGLE, INC.

- MICROSOFT CORPORATION

- INTEL CORPORATION

- GENERAL ELECTRIC DIGITAL

- HEWLETT PACKARD ENTERPRISE COMPANY

- VMWARE, INC.

- NOKIA

- NVIDIA CORPORATION

- CAPGEMINI

- IEI INTEGRATION CORPORATION

- ADVANTECH CO., LTD.

- その他の企業

- SAGUNA NETWORKS LTD.

- FASTLY, INC.

- STACKPATH, LLC

- ADLINK TECHNOLOGY, INC.

- DIGI INTERNATIONAL, INC.

- SIERRA WIRELESS(A SEMTECH COMPANY)

- JUNIPER NETWORKS, INC.

- EDGECONNEX, INC.

- CLEARBLADE, INC.

- EDGEIQ

第13章 付録

The edge computing in healthcare market is anticipated to grow from an estimated USD 4.1 billion in 2022 to USD 12.9 billion in 2028, at a CAGR of 26.1% during the forecast period. Edge computing is gaining popularity across industries as there is a rise in the number of devices, which has increased the demand for high-bandwidth applications with the growing use of internet services. Edge computing is rapidly gaining acceptance worldwide by healthcare organizations due to various benefits, including low latency, traffic distribution, increased reliability, and reduced costs

"Hardware: The hardware segment is estimated to account for the largest market share in 2022"

The high market share by hardware is owed to high-scale deployment of edge hardware by healthcare organizations to achieve high performance, scale, and flexibility. Vendors in the market offer comprehensive edge hardware (edge systems for computing, storage, and networking) and hardware components (computing systems, gateways/routers, servers, and physical data centers) that complete the entire edge infrastructure. Edge hardware act as a backbone to establish communication and connection for enabling core edge functions, such as collection, filtering, processing, transmission, monitoring, and routing.

" Telehealth & remote patient monitoring application to account for largest market size during forecast period"

Based on application, the market is segmented into diagnosis, telehealth & remote patient monitoring, robotic surgery, ambulances, and other applications. Telehealth and remote patient monitoring is expected to hold the largest market size during the forecast period. By leveraging edge computing, telehealth providers can offer a more seamless and integrated patient experience, improving patient engagement and satisfaction. Patients can receive remote consultations with healthcare professionals, access medical records, and monitor their own health and wellness using wearable devices, all from the comfort of their own homes

"Europe accounted for the second-largest share in the edge computing in healthcare market during the forecast period"

North America is expected to hold the largest market size in the edge computing market, followed by Europe, due to the presence of plenty of edge computing vendors, early technological adoption of smart technologies, rising strategic partnerships, and demand for workload-centric IT infrastructure. Various government initiatives and imminent needs among European and North American enterprises to handle data present a strong opportunity for edge computing vendors to expand locally. The adoption of edge computing solutions is increasing in Asia Pacific and Latin America due to the growing deployment of cloud-based services, the need for improving network connectivity, the rise in technology assimilation, and the increasing awareness of the benefits of edge computing.

Break of primary participants was as mentioned below:

- By Company Type - Tier 1-40%, Tier 2-35%, and Tier 3-25%

- By Designation - C-level-35%, Director-level-40%, Others-25%

- By Region - North America-42%, Europe-25%, Asia Pacific-18%, and Rest of the World-15%

Key Players in the Edge Computing in Healthcare Market

The key players operating in the edge computing in the healthcare market include CISCO Systems, Inc. (US), HUAWEI Technologies Co. Ltd (China), Dell Technologies, Inc. (US), Amazon Web Services (US), Google, Inc. (US), Microsoft Corporation (US), Intel Corporation (US), General Electric Digital (US), Hewlett Packard Enterprise Company (US), VMware, Inc. (US), Nokia Corporation (Finland), NVIDIA Corporation (US), Capgemini (France), Saguna Networks Ltd. (Israel), Fastly, Inc. (US), StackPath, LLC (US), ADLINK Technology, Inc. (Taiwan), Digi International, Inc. (US), Sierra Wireless (A Semtech Company) (Canada), Juniper Networks, Inc. (US), EdgeConneX, Inc. (US), ClearBlade, Inc. (US) and EdgeIQ (US).

Research Coverage:

The report analyzes the edge computing in healthcare market and aims at estimating the market size and future growth potential of this market based on various segments such as component, application, end user, and region. The report also includes a product portfolio matrix of various edge computing in healthcare hardware, software, & services available in the market. The report also provides a competitive analysis of the key players in this market, along with their company profiles, product offerings, and key market strategies.

Reasons to Buy the Report

The report will enrich established firms as well as new entrants/smaller firms to gauge the pulse of the market, which in turn would help them, garner a more significant share of the market. Firms purchasing the report could use one or any combination of the below-mentioned strategies to strengthen their position in the market.

This report provides insights into the following pointers:

- Market Penetration: Comprehensive information on product portfolios offered by the top players in the global edge computing in healthcare market. The report analyzes this market by product & service and end user.

- Product Enhancement/Innovation: Detailed insights on upcoming trends and product launches in the global edge computing in healthcare market

- Market Development: Comprehensive information on the lucrative emerging markets by products & services and end user

- Market Diversification: Exhaustive information about new products or product enhancements, growing geographies, recent developments, and investments in the global edge computing in healthcare market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, competitive leadership mapping, and capabilities of leading players in the global edge computing in healthcare market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 INCLUSIONS AND EXCLUSIONS

- 1.4 MARKET SCOPE

- 1.4.1 MARKET SEGMENTATION

- FIGURE 1 EDGE COMPUTING IN HEALTHCARE MARKET: MARKET SEGMENTATION

- 1.4.2 REGIONAL SCOPE

- 1.5 YEARS CONSIDERED

- 1.6 CURRENCY CONSIDERED

- TABLE 1 EXCHANGE RATES UTILIZED FOR CONVERSION TO USD

- 1.7 LIMITATIONS

- 1.8 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 EDGE COMPUTING IN HEALTHCARE MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakup of primary profiles

- FIGURE 3 BREAKUP OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

- 2.1.2.2 Key industry insights

- 2.2 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 4 DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- FIGURE 5 EDGE COMPUTING IN HEALTHCARE MARKET: TOP-DOWN AND BOTTOM-UP APPROACHES

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY - APPROACH 1 (SUPPLY SIDE): ESTIMATION OF REVENUE GENERATED BY VENDORS FROM EDGE COMPUTING

- FIGURE 7 MARKET SIZE ESTIMATION METHODOLOGY - BOTTOM-UP APPROACH (SUPPLY SIDE): ESTIMATION OF COLLECTIVE REVENUE OF EDGE COMPUTING VENDORS

- FIGURE 8 MARKET SIZE ESTIMATION METHODOLOGY (SUPPLY SIDE): ILLUSTRATION OF VENDOR REVENUE ESTIMATION

- 2.4 MARKET FORECAST

- TABLE 2 FACTOR ANALYSIS

- 2.5 IMPACT OF RECESSION

- 2.6 RISK ASSESSMENT

- TABLE 3 LIMITATIONS AND ASSOCIATED RISKS

- 2.7 LIMITATIONS

3 EXECUTIVE SUMMARY

- FIGURE 9 HARDWARE SEGMENT TO ACCOUNT FOR LARGEST MARKET SIZE DURING FORECAST PERIOD

- FIGURE 10 TELEHEALTH & REMOTE PATIENT MONITORING SEGMENT TO ACCOUNT FOR LARGEST MARKET SIZE DURING FORECAST PERIOD

- FIGURE 11 HOSPITALS & CLINICS SEGMENT TO ACCOUNT FOR LARGEST MARKET SIZE DURING FORECAST PERIOD

- FIGURE 12 NORTH AMERICA TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN EDGE COMPUTING IN HEALTHCARE MARKET

- FIGURE 13 RISING DEMAND FOR LOW-LATENCY PROCESSING AND REAL-TIME, AUTOMATED DECISION-MAKING SOLUTIONS TO DRIVE MARKET GROWTH

- 4.2 EDGE COMPUTING IN HEALTHCARE MARKET, BY REGION

- FIGURE 14 NORTH AMERICA TO DOMINATE EDGE COMPUTING IN HEALTHCARE MARKET DURING FORECAST PERIOD

- 4.3 NORTH AMERICA: EDGE COMPUTING IN HEALTHCARE MARKET, BY END USER AND COUNTRY, 2022

- FIGURE 15 HOSPITALS & CLINICS AND US DOMINATED MARKET IN NORTH AMERICA IN 2022

- 4.4 EDGE COMPUTING IN HEALTHCARE MARKET, BY COMPONENT

- FIGURE 16 SOFTWARE SEGMENT TO HOLD MAJORITY MARKET SHARE IN 2028

- 4.5 EDGE COMPUTING IN HEALTHCARE MARKET, BY END USER

- FIGURE 17 HOSPITALS & CLINICS TO ACCOUNT FOR LARGEST MARKET SHARE IN 2028

- 4.6 EDGE COMPUTING IN HEALTHCARE MARKET, BY APPLICATION

- FIGURE 18 TELEHEALTH & REMOTE PATIENT MONITORING TO BE FASTEST-GROWING SEGMENT DURING FORECAST PERIOD

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 19 EDGE COMPUTING IN HEALTHCARE MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Growing adoption of IoT medical devices

- 5.2.1.2 Exponentially increasing network traffic and volume of healthcare data

- 5.2.1.3 Rising need to curtail healthcare costs

- FIGURE 20 HEALTHCARE EXPENDITURE, BY COUNTRY, 2021 (% OF GDP)

- 5.2.1.4 Rising demand for low-latency processing and real-time, automated decision-making solutions

- 5.2.2 RESTRAINTS

- 5.2.2.1 High CAPEX and OPEX associated with edge computing systems

- 5.2.2.2 Interoperability challenges related to edge computing across different healthcare systems

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Advent of 5G network

- FIGURE 21 PERCENTAGE SHARE OF DIFFERENT MOBILE NETWORK CONNECTIONS, BY REGION, 2023

- 5.2.4 CHALLENGES

- 5.2.4.1 Complexities in integrating edge computing systems with existing cloud architecture

- 5.2.4.2 Susceptibility to cyberattacks and limited authentication capabilities of edge computing architecture

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 OVERVIEW OF KEY INDUSTRY TRENDS

- 6.3 CASE STUDY ANALYSIS

- 6.3.1 SENTARA IMPROVED RESPONSE TIME WITH DELL'S EDGE COMPUTING SOLUTIONS

- 6.3.2 RED HAT HELPED HCA HEALTHCARE IMPROVE SEPSIS DIAGNOSIS

- 6.3.3 AI-ASSISTED HOME-BASED PATIENT MONITORING FACILITATED BY BIOBEAT DURING COVID-19

- 6.3.4 ZELLA DC FACILITATED HOME-BASED PATIENT MONITORING FOR CENTERS FOR DISEASE CONTROL AND PREVENTION (CDC)

- 6.4 ECOSYSTEM ANALYSIS

- FIGURE 22 EDGE COMPUTING IN HEALTHCARE MARKET: ECOSYSTEM

- 6.5 PRICING ANALYSIS

- TABLE 4 PRICING ANALYSIS OF MICROSOFT EDGE COMPUTING SOLUTIONS

- TABLE 5 PRICING ANALYSIS OF AWS EDGE COMPUTING SOLUTIONS

- 6.6 PATENT ANALYSIS

- 6.6.1 PATENT PUBLICATION TRENDS FOR EDGE COMPUTING IN HEALTHCARE MARKET

- FIGURE 23 PATENT PUBLICATION TRENDS, JANUARY 2012-APRIL 2023

- 6.6.2 JURISDICTION AND TOP APPLICANT ANALYSIS

- FIGURE 24 TOP PATENT APPLICANTS & OWNERS (COMPANIES/INSTITUTIONS) FOR HEALTHCARE EDGE COMPUTING SOLUTIONS, JANUARY 2012- APRIL 2023

- FIGURE 25 TOP APPLICANT COUNTRIES/JURISDICTIONS FOR HEALTHCARE EDGE COMPUTING SOLUTIONS PATENTS, JANUARY 2012-APRIL 2023

- TABLE 6 EDGE COMPUTING IN HEALTHCARE MARKET: LIST OF PATENTS/PATENT APPLICATIONS, 2020-2023

- 6.7 TECHNOLOGY ANALYSIS

- 6.7.1 ARTIFICIAL INTELLIGENCE AND MACHINE LEARNING

- 6.7.2 5G

- 6.7.3 INTERNET OF THINGS (IOT)

- 6.7.4 AUGMENTED REALITY (AR) AND VIRTUAL REALITY (VR)

- 6.7.5 SYSTEM ARCHITECTURE FOR HEALTHCARE EDGE COMPUTING SOLUTIONS

- FIGURE 26 EDGE COMPUTING IN HEALTHCARE MARKET: SYSTEM ARCHITECTURE

- 6.8 SUPPLY CHAIN ANALYSIS

- FIGURE 27 EDGE COMPUTING IN HEALTHCARE MARKET: SUPPLY CHAIN

- 6.9 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.9.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 28 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS

- TABLE 7 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS (%)

- 6.9.2 BUYING CRITERIA

- FIGURE 29 KEY BUYING CRITERIA, BY END USER

- TABLE 8 KEY BUYING CRITERIA, BY END USER (%)

- 6.10 KEY CONFERENCES & EVENTS, 2023-2024

- TABLE 9 EDGE COMPUTING IN HEALTHCARE MARKET: DETAILED LIST OF CONFERENCES AND EVENTS

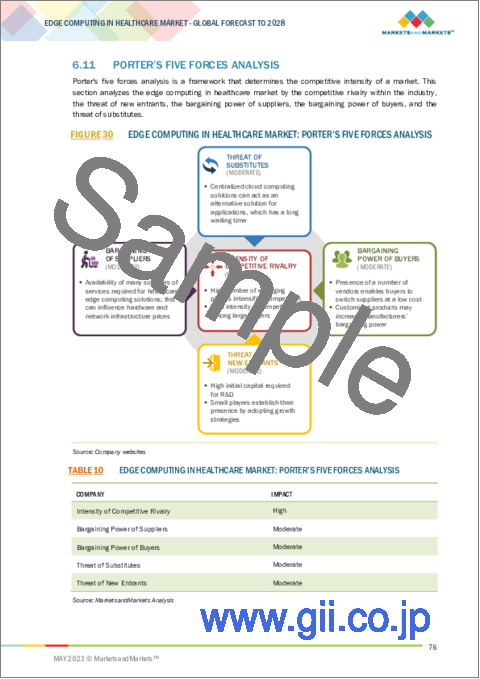

- 6.11 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 30 EDGE COMPUTING IN HEALTHCARE MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 10 EDGE COMPUTING IN HEALTHCARE MARKET: PORTER'S FIVE FORCES ANALYSIS

- 6.11.1 THREAT OF NEW ENTRANTS

- 6.11.2 THREAT OF SUBSTITUTES

- 6.11.3 BARGAINING POWER OF SUPPLIERS

- 6.11.4 BARGAINING POWER OF BUYERS

- 6.11.5 INTENSITY OF COMPETITIVE RIVALRY

- 6.12 REGULATORY LANDSCAPE

- 6.12.1 NORTH AMERICA

- 6.12.2 EUROPE

- 6.12.3 ASIA PACIFIC

- 6.12.4 MIDDLE EAST AND SOUTH AFRICA

- 6.12.5 LATIN AMERICA

- 6.13 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 31 REVENUE SHIFTS AND NEW REVENUE POCKETS FOR EDGE COMPUTING IN HEALTHCARE MARKET

7 EDGE COMPUTING IN HEALTHCARE MARKET, BY COMPONENT

- 7.1 INTRODUCTION

- FIGURE 32 SOFTWARE SEGMENT ACCOUNTED FOR LARGEST MARKET SHARE IN 2022

- TABLE 11 EDGE COMPUTING IN HEALTHCARE MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- 7.2 HARDWARE

- 7.2.1 REFER TO PHYSICAL COMPONENTS REQUIRED TO RUN APPLICATIONS

- TABLE 12 HARDWARE: EDGE COMPUTING IN HEALTHCARE MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 13 HARDWARE: EDGE COMPUTING IN HEALTHCARE MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 14 HARDWARE: EDGE COMPUTING IN HEALTHCARE MARKET IN EUROPE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 15 HARDWARE: EDGE COMPUTING IN HEALTHCARE MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2028 (USD MILLION)

- 7.3 SOFTWARE

- 7.3.1 ENHANCE COMPUTING CAPABILITIES OF EDGE DEVICES AND DATA CENTERS

- TABLE 16 SOFTWARE: EDGE COMPUTING IN HEALTHCARE MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 17 SOFTWARE: EDGE COMPUTING IN HEALTHCARE MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 18 SOFTWARE: EDGE COMPUTING IN HEALTHCARE MARKET IN EUROPE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 19 SOFTWARE: EDGE COMPUTING IN HEALTHCARE MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2028 (USD MILLION)

- 7.4 SERVICES

- 7.4.1 INCLUDE CONSULTING, PRODUCT SUPPORT, INTEGRATION, UPDATES, AND MAINTENANCE OF INTEGRATED EDGE DEVICES AND SOLUTIONS

- TABLE 20 SERVICES: EDGE COMPUTING IN HEALTHCARE MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 21 SERVICES: EDGE COMPUTING IN HEALTHCARE MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 22 SERVICES: EDGE COMPUTING IN HEALTHCARE MARKET IN EUROPE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 23 SERVICES: EDGE COMPUTING IN HEALTHCARE MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2028 (USD MILLION)

8 EDGE COMPUTING IN HEALTHCARE MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- FIGURE 33 TELEHEALTH & REMOTE PATIENT MONITORING SEGMENT HELD LARGEST MARKET SHARE, BY APPLICATION, IN 2022

- TABLE 24 EDGE COMPUTING IN HEALTHCARE MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- 8.2 DIAGNOSTICS

- 8.2.1 GROWING ADOPTION OF TELEHEALTH SERVICES AND REMOTE PATIENT MONITORING TECHNOLOGIES TO AUGMENT MARKET GROWTH

- TABLE 25 DIAGNOSTICS: EDGE COMPUTING IN HEALTHCARE MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 26 DIAGNOSTICS: EDGE COMPUTING IN HEALTHCARE MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 27 DIAGNOSTICS: EDGE COMPUTING IN HEALTHCARE MARKET IN EUROPE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 28 DIAGNOSTICS: EDGE COMPUTING IN HEALTHCARE MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2028 (USD MILLION)

- 8.3 ROBOTIC SURGERY

- 8.3.1 INCREASING ADOPTION OF EDGE AI IN ROBOTIC SURGERIES TO PROPEL MARKET GROWTH

- TABLE 29 ROBOTIC SURGERY: EDGE COMPUTING IN HEALTHCARE MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 30 ROBOTIC SURGERY: EDGE COMPUTING IN HEALTHCARE MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 31 ROBOTIC SURGERY: EDGE COMPUTING IN HEALTHCARE MARKET IN EUROPE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 32 ROBOTIC SURGERY: EDGE COMPUTING IN HEALTHCARE MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2028 (USD MILLION)

- 8.4 TELEHEALTH & REMOTE PATIENT MONITORING

- 8.4.1 INCREASING USE OF INTEGRATED WEARABLES AND PENETRATION OF MEDICAL IOT DEVICES TO SUPPORT MARKET GROWTH

- TABLE 33 CHRONIC DISEASES AND THEIR COST BURDEN ON US

- TABLE 34 TELEHEALTH & REMOTE PATIENT MONITORING: EDGE COMPUTING IN HEALTHCARE MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 35 TELEHEALTH & REMOTE PATIENT MONITORING: EDGE COMPUTING IN HEALTHCARE MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 36 TELEHEALTH & REMOTE PATIENT MONITORING: EDGE COMPUTING IN HEALTHCARE MARKET IN EUROPE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 37 TELEHEALTH & REMOTE PATIENT MONITORING: EDGE COMPUTING IN HEALTHCARE MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2028 (USD MILLION)

- 8.5 AMBULANCES

- 8.5.1 RISING FOCUS ON MINIMIZING RESPONSE TIMES IN EMERGENCY SITUATIONS TO LEAD TO ADOPTION OF EDGE COMPUTING IN AMBULANCES

- TABLE 38 AMBULANCES: EDGE COMPUTING IN HEALTHCARE MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 39 AMBULANCES: EDGE COMPUTING IN HEALTHCARE MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 40 AMBULANCES: EDGE COMPUTING IN HEALTHCARE MARKET IN EUROPE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 41 AMBULANCES: EDGE COMPUTING IN HEALTHCARE MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2028 (USD MILLION)

- 8.6 OTHER APPLICATIONS

- TABLE 42 OTHER APPLICATIONS: EDGE COMPUTING IN HEALTHCARE MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 43 OTHER APPLICATIONS: EDGE COMPUTING IN HEALTHCARE MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 44 OTHER APPLICATIONS: EDGE COMPUTING IN HEALTHCARE MARKET IN EUROPE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 45 OTHER APPLICATIONS: EDGE COMPUTING IN HEALTHCARE MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2028 (USD MILLION)

9 EDGE COMPUTING IN HEALTHCARE MARKET, BY END USER

- 9.1 INTRODUCTION

- FIGURE 34 HOSPITALS & CLINICS SEGMENT CAPTURED LARGEST MARKET SHARE, BY END USER, IN 2022

- TABLE 46 EDGE COMPUTING IN HEALTHCARE MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.2 HOSPITALS & CLINICS

- 9.2.1 ADOPTION OF TELEHEALTH SERVICES AND REMOTE PATIENT MONITORING TECHNOLOGIES TO AUGMENT MARKET GROWTH

- TABLE 47 HOSPITALS & CLINICS: EDGE COMPUTING IN HEALTHCARE MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 48 HOSPITALS & CLINICS: EDGE COMPUTING IN HEALTHCARE MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 49 HOSPITALS & CLINICS: EDGE COMPUTING IN HEALTHCARE MARKET IN EUROPE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 50 HOSPITALS & CLINICS: EDGE COMPUTING IN HEALTHCARE MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2028 (USD MILLION)

- 9.3 LONG-TERM CARE CENTERS AND HOME CARE SETTINGS

- 9.3.1 RISE IN GLOBAL GERIATRIC POPULATION REQUIRING LONG-TERM CARE TO SUPPORT MARKET GROWTH

- TABLE 51 LONG-TERM CARE CENTERS & HOME CARE FACILITIES: EDGE COMPUTING IN HEALTHCARE MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 52 LONG-TERM CARE CENTERS & HOME CARE FACILITIES: EDGE COMPUTING IN HEALTHCARE MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 53 LONG-TERM CARE CENTERS & HOME CARE FACILITIES: EDGE COMPUTING IN HEALTHCARE MARKET IN EUROPE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 54 LONG-TERM CARE CENTERS & HOME CARE FACILITIES: EDGE COMPUTING IN HEALTHCARE MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2028 (USD MILLION)

- 9.4 AMBULATORY CARE CENTERS

- 9.4.1 GRADUAL SHIFT FROM INPATIENT TO OUTPATIENT CARE TO BOOST MARKET

- FIGURE 35 OUTPATIENT APPOINTMENTS AND ATTENDANCES IN UK, 2011-2022

- TABLE 55 AMBULATORY CARE CENTERS: EDGE COMPUTING IN HEALTHCARE MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 56 AMBULATORY CARE CENTERS: EDGE COMPUTING IN HEALTHCARE MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 57 AMBULATORY CARE CENTERS: EDGE COMPUTING IN HEALTHCARE MARKET IN EUROPE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 58 AMBULATORY CARE CENTERS: EDGE COMPUTING IN HEALTHCARE MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2028 (USD MILLION)

- 9.5 OTHER END USERS

- TABLE 59 OTHER END USERS: EDGE COMPUTING IN HEALTHCARE MARKET, BY REGION, 2021-2028 (USD MILLION)

- TABLE 60 OTHER END USERS: EDGE COMPUTING IN HEALTHCARE MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 61 OTHER END USERS: EDGE COMPUTING IN HEALTHCARE MARKET IN EUROPE, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 62 OTHER END USERS: EDGE COMPUTING IN HEALTHCARE MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2028 (USD MILLION)

10 EDGE COMPUTING IN HEALTHCARE MARKET, BY REGION

- 10.1 INTRODUCTION

- FIGURE 36 NORTH AMERICA TO EMERGE AS NEW HOTSPOT DURING FORECAST PERIOD

- FIGURE 37 NORTH AMERICA HELD LARGEST SHARE OF EDGE COMPUTING IN HEALTHCARE MARKET IN 2022

- TABLE 63 EDGE COMPUTING IN HEALTHCARE MARKET, BY REGION, 2021-2028 (USD MILLION)

- 10.2 NORTH AMERICA

- 10.2.1 NORTH AMERICA: RECESSION IMPACT

- FIGURE 38 NORTH AMERICA: EDGE COMPUTING IN HEALTHCARE MARKET SNAPSHOT

- TABLE 64 NORTH AMERICA: EDGE COMPUTING IN HEALTHCARE MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 65 NORTH AMERICA: EDGE COMPUTING IN HEALTHCARE MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 66 NORTH AMERICA: EDGE COMPUTING IN HEALTHCARE MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 67 NORTH AMERICA: EDGE COMPUTING IN HEALTHCARE MARKET, BY END USER, 2021-2028 (USD MILLION)

- 10.2.2 US

- 10.2.2.1 Accounted for largest share of North American market in 2022

- TABLE 68 US: EDGE COMPUTING IN HEALTHCARE MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 69 US: EDGE COMPUTING IN HEALTHCARE MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 70 US: EDGE COMPUTING IN HEALTHCARE MARKET, BY END USER, 2021-2028 (USD MILLION)

- 10.2.3 CANADA

- 10.2.3.1 Increasing collaborations and efforts to promote adoption of edge computing in healthcare to drive market

- TABLE 71 CANADA: EDGE COMPUTING IN HEALTHCARE MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 72 CANADA: EDGE COMPUTING IN HEALTHCARE MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 73 CANADA: EDGE COMPUTING IN HEALTHCARE MARKET, BY END USER, 2021-2028 (USD MILLION)

- 10.3 EUROPE

- 10.3.1 EUROPE: RECESSION IMPACT

- FIGURE 39 EUROPE: EDGE COMPUTING IN HEALTHCARE MARKET SNAPSHOT

- TABLE 74 EUROPE: EDGE COMPUTING IN HEALTHCARE MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 75 EUROPE: EDGE COMPUTING IN HEALTHCARE MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 76 EUROPE: EDGE COMPUTING IN HEALTHCARE MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 77 EUROPE: EDGE COMPUTING IN HEALTHCARE MARKET, BY END USER, 2021-2028 (USD MILLION)

- 10.3.2 UK

- 10.3.2.1 Growing penetration of wearables to fuel market growth

- TABLE 78 UK: EDGE COMPUTING IN HEALTHCARE MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 79 UK: EDGE COMPUTING IN HEALTHCARE MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 80 UK: EDGE COMPUTING IN HEALTHCARE MARKET, BY END USER, 2021-2028 (USD MILLION)

- 10.3.3 GERMANY

- 10.3.3.1 Government initiatives to expedite development of digital healthcare ecosystem to enhance market growth

- TABLE 81 GERMANY: EDGE COMPUTING IN HEALTHCARE MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 82 GERMANY: EDGE COMPUTING IN HEALTHCARE MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 83 GERMANY: EDGE COMPUTING IN HEALTHCARE MARKET, BY END USER, 2021-2028 (USD MILLION)

- 10.3.4 FRANCE

- 10.3.4.1 Government's eHealth 2022 plan to boost market

- TABLE 84 FRANCE: EDGE COMPUTING IN HEALTHCARE MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 85 FRANCE: EDGE COMPUTING IN HEALTHCARE MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 86 FRANCE: EDGE COMPUTING IN HEALTHCARE MARKET, BY END USER, 2021-2028 (USD MILLION)

- 10.3.5 REST OF EUROPE

- TABLE 87 REST OF EUROPE: EDGE COMPUTING IN HEALTHCARE MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 88 REST OF EUROPE: EDGE COMPUTING IN HEALTHCARE MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 89 REST OF EUROPE: EDGE COMPUTING IN HEALTHCARE MARKET, BY END USER, 2021-2028 (USD MILLION)

- 10.4 ASIA PACIFIC

- 10.4.1 ASIA PACIFIC: RECESSION IMPACT

- TABLE 90 ASIA PACIFIC: EDGE COMPUTING IN HEALTHCARE MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 91 ASIA PACIFIC: EDGE COMPUTING IN HEALTHCARE MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 92 ASIA PACIFIC: EDGE COMPUTING IN HEALTHCARE MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 93 ASIA PACIFIC: EDGE COMPUTING IN HEALTHCARE MARKET, BY END USER, 2021-2028 (USD MILLION)

- 10.4.2 JAPAN

- 10.4.2.1 Introduction of cutting-edge edge healthcare computing technologies to induce market growth

- TABLE 94 JAPAN: EDGE COMPUTING IN HEALTHCARE MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 95 JAPAN: EDGE COMPUTING IN HEALTHCARE MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 96 JAPAN: EDGE COMPUTING IN HEALTHCARE MARKET, BY END USER, 2021-2028 (USD MILLION)

- 10.4.3 SOUTH KOREA

- 10.4.3.1 Prevalence of chronic diseases to drive implementation of edge computing in healthcare

- TABLE 97 SOUTH KOREA: EDGE COMPUTING IN HEALTHCARE MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 98 SOUTH KOREA: EDGE COMPUTING IN HEALTHCARE MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 99 SOUTH KOREA: EDGE COMPUTING IN HEALTHCARE MARKET, BY END USER, 2021-2028 (USD MILLION)

- 10.4.4 REST OF ASIA PACIFIC

- TABLE 100 REST OF ASIA PACIFIC: EDGE COMPUTING IN HEALTHCARE MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 101 REST OF ASIA PACIFIC: EDGE COMPUTING IN HEALTHCARE MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 102 REST OF ASIA PACIFIC: EDGE COMPUTING IN HEALTHCARE MARKET, BY END USER, 2021-2028 (USD MILLION)

- 10.5 REST OF THE WORLD

- 10.5.1 REST OF THE WORLD: RECESSION IMPACT

- TABLE 103 REST OF THE WORLD: EDGE COMPUTING IN HEALTHCARE MARKET, BY COMPONENT, 2021-2028 (USD MILLION)

- TABLE 104 REST OF THE WORLD: EDGE COMPUTING IN HEALTHCARE MARKET, BY APPLICATION, 2021-2028 (USD MILLION)

- TABLE 105 REST OF THE WORLD: EDGE COMPUTING IN HEALTHCARE MARKET, BY END USER, 2021-2028 (USD MILLION)

11 COMPETITIVE LANDSCAPE

- 11.1 INTRODUCTION

- 11.2 KEY PLAYER STRATEGIES

- TABLE 106 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN EDGE COMPUTING IN HEALTHCARE MARKET

- FIGURE 40 KEY DEVELOPMENTS UNDERTAKEN BY MAJOR PLAYERS BETWEEN JANUARY 2020 AND MARCH 2023

- 11.3 REVENUE ANALYSIS OF TOP MARKET PLAYERS, 2022

- FIGURE 41 REVENUE ANALYSIS OF KEY PLAYERS

- 11.4 MARKET SHARE ANALYSIS, 2022

- FIGURE 42 EDGE COMPUTING IN HEALTHCARE MARKET: MARKET SHARE ANALYSIS, 2022

- 11.5 COMPETITIVE BENCHMARKING

- TABLE 107 COMPANY FOOTPRINT ANALYSIS

- TABLE 108 PRODUCT FOOTPRINT ANALYSIS (25 COMPANIES)

- TABLE 109 APPLICATION FOOTPRINT ANALYSIS (25 COMPANIES)

- TABLE 110 REGION FOOTPRINT ANALYSIS (25 COMPANIES)

- 11.6 COMPANY EVALUATION QUADRANT

- 11.6.1 STARS

- 11.6.2 PERVASIVE PLAYERS

- 11.6.3 EMERGING LEADERS

- 11.6.4 PARTICIPANTS

- FIGURE 43 EDGE COMPUTING IN HEALTHCARE MARKET: COMPANY EVALUATION QUADRANT, 2022

- 11.7 START-UPS/SMES EVALUATION QUADRANT

- 11.7.1 PROGRESSIVE COMPANIES

- 11.7.2 DYNAMIC COMPANIES

- 11.7.3 STARTING BLOCKS

- 11.7.4 RESPONSIVE COMPANIES

- FIGURE 44 EDGE COMPUTING IN HEALTHCARE MARKET: START-UPS/SMES EVALUATION QUADRANT, 2022

- 11.8 COMPETITIVE SCENARIOS AND TRENDS

- 11.8.1 PRODUCT/SERVICE LAUNCHES

- TABLE 111 EDGE COMPUTING IN HEALTHCARE MARKET: PRODUCT/SERVICE LAUNCHES, 2020-2023

- 11.8.2 DEALS

- TABLE 112 EDGE COMPUTING IN HEALTHCARE MARKET: DEALS, 2020-2023

12 COMPANY PROFILES

- (Business Overview, Products & services Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats))**

- 12.1 KEY PLAYERS

- 12.1.1 CISCO SYSTEMS, INC.

- TABLE 113 CISCO SYSTEMS, INC.: COMPANY OVERVIEW

- FIGURE 45 CISCO SYSTEMS, INC.: COMPANY SNAPSHOT, 2022

- TABLE 114 CISCO SYSTEMS, INC.: PRODUCTS & SERVICES OFFERED

- TABLE 115 CISCO SYSTEMS, INC.: DEALS

- 12.1.2 HUAWEI TECHNOLOGIES CO., LTD.

- TABLE 116 HUAWEI TECHNOLOGIES CO., LTD.: COMPANY OVERVIEW

- TABLE 117 HUAWEI TECHNOLOGIES CO., LTD.: PRODUCTS & SERVICES OFFERED

- TABLE 118 HUAWEI TECHNOLOGIES CO., LTD.: DEALS

- 12.1.3 DELL TECHNOLOGIES, INC.

- TABLE 119 DELL TECHNOLOGIES, INC.: COMPANY OVERVIEW

- FIGURE 46 DELL TECHNOLOGIES, INC.: COMPANY SNAPSHOT, 2022

- TABLE 120 DELL TECHNOLOGIES, INC.: PRODUCTS & SERVICES OFFERED

- TABLE 121 DELL TECHNOLOGIES, INC.: PRODUCT LAUNCHES

- TABLE 122 DELL TECHNOLOGIES, INC.: DEALS

- 12.1.4 AMAZON WEB SERVICES

- TABLE 123 AMAZON WEB SERVICES: COMPANY OVERVIEW

- FIGURE 47 AMAZON WEB SERVICES: COMPANY SNAPSHOT, 2022

- TABLE 124 AMAZON WEB SERVICES: PRODUCTS & SERVICES OFFERED

- TABLE 125 AMAZON WEB SERVICES: PRODUCT LAUNCHES

- TABLE 126 AMAZON WEB SERVICES: DEALS

- 12.1.5 GOOGLE, INC.

- TABLE 127 GOOGLE, INC.: COMPANY OVERVIEW

- FIGURE 48 GOOGLE, INC.: COMPANY SNAPSHOT, 2022

- TABLE 128 GOOGLE, INC.: PRODUCTS & SERVICES OFFERED

- TABLE 129 GOOGLE, INC.: DEALS

- 12.1.6 MICROSOFT CORPORATION

- TABLE 130 MICROSOFT CORPORATION: COMPANY OVERVIEW

- FIGURE 49 MICROSOFT CORPORATION: COMPANY SNAPSHOT, 2022

- TABLE 131 MICROSOFT CORPORATION: PRODUCTS & SERVICES OFFERED

- TABLE 132 MICROSOFT CORPORATION: PRODUCT LAUNCHES

- TABLE 133 MICROSOFT CORPORATION: DEALS

- 12.1.7 INTEL CORPORATION

- TABLE 134 INTEL CORPORATION: COMPANY OVERVIEW

- FIGURE 50 INTEL CORPORATION: COMPANY SNAPSHOT, 2022

- TABLE 135 INTEL CORPORATION: PRODUCTS & SERVICES OFFERED

- TABLE 136 INTEL CORPORATION: PRODUCT LAUNCHES

- TABLE 137 INTEL CORPORATION: DEALS

- 12.1.8 GENERAL ELECTRIC DIGITAL

- TABLE 138 GENERAL ELECTRIC DIGITAL: COMPANY OVERVIEW

- TABLE 139 GENERAL ELECTRIC DIGITAL: PRODUCTS & SERVICES OFFERED

- 12.1.9 HEWLETT PACKARD ENTERPRISE COMPANY

- TABLE 140 HEWLETT PACKARD ENTERPRISE COMPANY: COMPANY OVERVIEW

- FIGURE 51 HEWLETT PACKARD ENTERPRISE COMPANY: COMPANY SNAPSHOT, 2022

- TABLE 141 HEWLETT PACKARD ENTERPRISE COMPANY: PRODUCTS & SERVICES OFFERED

- TABLE 142 HEWLETT PACKARD ENTERPRISE COMPANY: PRODUCT LAUNCHES

- TABLE 143 HEWLETT PACKARD ENTERPRISE COMPANY: DEALS

- 12.1.10 VMWARE, INC.

- TABLE 144 VMWARE, INC.: COMPANY OVERVIEW

- FIGURE 52 VMWARE, INC.: COMPANY SNAPSHOT, 2022

- TABLE 145 VMWARE, INC.: PRODUCTS & SERVICES OFFERED

- TABLE 146 VMWARE, INC.: DEALS

- 12.1.11 NOKIA

- TABLE 147 NOKIA: COMPANY OVERVIEW

- FIGURE 53 NOKIA: COMPANY SNAPSHOT, 2022

- TABLE 148 NOKIA: PRODUCTS & SERVICES OFFERED

- TABLE 149 NOKIA: DEALS

- 12.1.12 NVIDIA CORPORATION

- TABLE 150 NVIDIA CORPORATION: COMPANY OVERVIEW

- FIGURE 54 NVIDIA CORPORATION: COMPANY SNAPSHOT, 2022

- TABLE 151 NVIDIA CORPORATION: PRODUCTS & SERVICES OFFERED

- TABLE 152 NVIDIA CORPORATION: PRODUCT LAUNCHES

- TABLE 153 NVIDIA CORPORATION: DEALS

- 12.1.13 CAPGEMINI

- TABLE 154 CAPGEMINI: COMPANY OVERVIEW

- FIGURE 55 CAPGEMINI: COMPANY SNAPSHOT, 2022

- TABLE 155 CAPGEMINI: PRODUCTS & SERVICES OFFERED

- TABLE 156 CAPGEMINI: DEALS

- TABLE 157 CAPGEMINI: OTHERS

- 12.1.14 IEI INTEGRATION CORPORATION

- TABLE 158 IEI INTEGRATION CORPORATION: COMPANY OVERVIEW

- FIGURE 56 IEI INTEGRATION CORPORATION: COMPANY SNAPSHOT, 2022

- TABLE 159 IEI INTEGRATION CORPORATION: PRODUCTS & SERVICES OFFERED

- TABLE 160 IEI INTEGRATION CORPORATION: DEALS

- 12.1.15 ADVANTECH CO., LTD.

- TABLE 161 ADVANTECH CO., LTD.: COMPANY OVERVIEW

- FIGURE 57 ADVANTECH CO., LTD.: COMPANY SNAPSHOT, 2022

- TABLE 162 ADVANTECH CO., LTD.: PRODUCTS & SERVICES OFFERED

- TABLE 163 ADVANTECH CO., LTD.: PRODUCT LAUNCHES

- TABLE 164 ADVANTECH CO., LTD.: DEALS

- 12.2 OTHER PLAYERS

- 12.2.1 SAGUNA NETWORKS LTD.

- 12.2.2 FASTLY, INC.

- 12.2.3 STACKPATH, LLC

- 12.2.4 ADLINK TECHNOLOGY, INC.

- 12.2.5 DIGI INTERNATIONAL, INC.

- 12.2.6 SIERRA WIRELESS (A SEMTECH COMPANY)

- 12.2.7 JUNIPER NETWORKS, INC.

- 12.2.8 EDGECONNEX, INC.

- 12.2.9 CLEARBLADE, INC.

- 12.2.10 EDGEIQ

- *Details on Business Overview, Products & services Offered, Recent Developments, and MnM View (Key strengths/Right to Win, Strategic Choices Made, and Weaknesses and Competitive Threats) might not be captured in case of unlisted companies.

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS