|

|

市場調査レポート

商品コード

1270838

デジタル教育の世界市場:タイプ別(自習型、インストラクター主導型)、コースタイプ別、エンドユーザー別(学術機関、企業・公共部門)、地域別 - 2028年までの予測Digital Education Market by Type (Self-paced Online Education and Instructor-led Online Education), Course Type, End User (Academic Institutions and Enterprises & Public Sector) and Region - Global Forecast to 2028 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| デジタル教育の世界市場:タイプ別(自習型、インストラクター主導型)、コースタイプ別、エンドユーザー別(学術機関、企業・公共部門)、地域別 - 2028年までの予測 |

|

出版日: 2023年05月03日

発行: MarketsandMarkets

ページ情報: 英文 222 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界のデジタル教育の市場規模は、2023年の194億米ドルから、2028年までに667億米ドルまで拡大し、予測期間中にCAGRで28.0%の成長が予測されています。

従来の学習に対するデジタル学習の主な利点は、その手頃な価格です。オンライン学習では、学習者/学生は大学の単位やブロードバンド料金を支払うだけでよいため、教科書、学生の交通費、食事、正装、分割払いや授業ごとに支払うことができる幅広い支払い方法の利用、不動産(地元に住んでいない人は宿泊施設を探す)などに費やしたお金を大幅に節約することができます。さらに、すべての教材がオンラインで利用できるため、ペーパーレスの学習環境を実現し、より低価格で環境に優しい学習が可能です。

"タイプ別では、自習型のオンライン教育セグメントが予測期間中に大きな市場規模を保持する"

自習型のオンライン教育セグメントがより大きな市場規模を保持すると予想されています。自習型のオンラインコースでは、コース全体を通して講師と生徒が同時に対応する必要はありません。講師はビデオを録画したり、生徒が講師の関与なしに学習できるコンテンツを提供することができます。学習者は、いつでもどこでも自分のペースで知識を習得できるため、長期的な知識の定着に大きな効果を発揮します。

"コースタイプ別では、起業家精神・経営管理コースセグメントが予測期間中に2番目に高いCAGRを保持する"

起業家精神・経営管理コースセグメントは、予測期間中に2番目に高いCAGRを保持すると予測されています。経営管理コースは、一般経営、事業開発、金融・銀行、マーケティング、旅行・観光、教養、ビジネス関連科目など、さまざまな分野の学習で構成されています。欧州の大学や教育機関はデジタル教育ソリューションを導入し、国際的な移動と多言語教育を可能にしています。その結果、TshinguaXやFederica Web Learningなど、さまざまな地域のデジタル教育プロバイダーが、世界で活躍する複数のデジタル教育プロバイダーと協力するようになりました。オンライン教育サービスプロバイダーがビジネス志向のコースを開始したことも、デジタル教育市場の成長に拍車をかけています。デジタル教育プロバイダーは、既存の経営に特化したコースを強化し、イノベーション・起業家精神における世界のMBAや修士号など、大学付属の複数のコースで、高等教育に特化した学習者をターゲットにしています。

"エンドユーザー別では、学術機関セグメントが予測期間中に高いCAGRで成長する"

エンドユーザー別では、学術機関セグメントが予測期間中により高いCAGRで成長すると予想されています。学術分野におけるデジタル教育ソリューションは、時間や距離にとらわれずに知識を共有するための新たな扉を開いています。教育機関は、学生にオンライン教育を提供することで、コースの効果を大幅に向上させることができます。多くの大学や教育機関ではまだ伝統的な教育モデルを採用していますが、他のほとんどの大学や教育機関では、デジタル教育の近代化に向けてこの変化を採用しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要と業界動向

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- ケーススタディ分析

- エコシステム分析

- サプライチェーン分析

- ポーターのファイブフォース分析

- 主要な利害関係者と購入基準

- 技術分析

- 価格分析

- 特許分析

- 規制状況

- 購入者に影響を与える動向/混乱

- 主な会議とイベント(2023年~2024年)

第6章 デジタル教育市場:タイプ別

- イントロダクション

- 自習型

- インストラクター主導型

第7章 デジタル教育市場:コースタイプ別

- イントロダクション

- 科学・技術コース

- 起業家精神・経営管理コース

- その他

第8章 デジタル教育市場:エンドユーザー別

- イントロダクション

- 学術機関

- 企業・公共部門

第9章 デジタル教育市場:地域別

- イントロダクション

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他の欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- その他のアジア太平洋地域

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- その他の中東・アフリカ

- ラテンアメリカ

- ブラジル

- メキシコ

- その他のラテンアメリカ

第10章 競合情勢

- イントロダクション

- 上位ベンダーの市場シェア

- 上位ベンダー5社の収益分析

- 企業評価象限(2022年)

- スタートアップ/中小企業向けの企業評価象限(2022年)

- スタートアップ/中小企業向けの競合ベンチマーキング

- 企業の財務指標

- 世界の主要な市場参入企業のスナップショット

- 競合シナリオ

第11章 企業プロファイル

- 主要企業

- COURSERA

- EDX

- PLURALSIGHT

- UDEMY

- UDACITY

- EDUREKA

- ALISON

- LINKEDIN LEARNING

- JIGSAW ACADEMY

- IVERSITY

- その他の企業

- MIRIADAX

- INTELLIPAAT

- FUTURELEARN

- EDMODO

- SWAYAM

- NOVOED

- XUETANGX

- LINKSTREET LEARNING(RAPL)

- KHAN ACADEMY

- KADENZE

- FEDERICA WEB LEARNING

- MY MOOC

- TREEHOUSE

- SKILLSHARE

- CREATIVELIVE

- CXL

- GO1

- BYJU'S

- DATACAMP

- PLATZI

- THINKFUL

第12章 隣接・関連市場

- イントロダクション

- 学習管理システム市場

- スマートラーニング市場

第13章 付録

The Global Digital Education Market size to grow from USD 19.4 billion in 2023 to USD 66.7 billion by 2028, at a Compound Annual Growth Rate (CAGR) of 28.0% during the forecast period. A major advantage of digital learning over traditional learning is its affordability. With online learning, learners/students only need to pay for university credits, broadband bills, thereby saving a lot of money which would have been spent otherwise on textbooks, student transportation, meals, formal attire, availability of a wide range of payment options that let learners pay in installments or per class basis, real estate (those who are non-localite, seek accommodation). Moreover, all study materials are available online, thus creating a paperless learning environment that is more affordable while also being eco-friendly.

"By Type, the Self-paced Online Education segment to hold the larger market size during the forecast period."

The Self-paced Online Education segment is expected to hold the larger market size. Self-paced online courses do not require instructors and students to be available at the same time during the entire course. Instructors can record videos or provide content that students can learn from without the instructor's involvement. Learners get the flexibility of taking the course anywhere anytime at their own pace of grasping the knowledge and hence it becomes effective in long-term knowledge retention significantly.

"By Course Type, Entrepreneurship and business management courses segment to have second highest CAGR during the forecast period"

The Entrepreneurship and business management courses segment is projected to hold the second highest CAGR during the forecast period. Business management courses consist of various areas of study, such as general management, business development, finance and banking, marketing, travel and tourism, liberal arts, and business-related subjects. Universities and educational organizations in Europe have adopted digital education solutions, enabling international mobility and multiple-language training. As a result, various regional digital education providers, such as TshinguaX and Federica Web Learning, have collaborated with several globally active digital education providers. The initiation of business-oriented courses by online education service providers has added to the growth of the digital education market. Digital education providers have enhanced existing management-specific courses to target higher-education-focused learners with several university-affiliated courses, such as Global MBA and Masters in Innovation and Entrepreneurship.

"By End User, the Academic Institutions segment to grow at higher CAGR during the forecast period"

By End User, the Academic Institutions segment is expected to grow at a higher CAGR during the forecast period. Digital education solutions in the academic sector has opened new doors for sharing knowledge without the boundaries of time and distance. Education institutions can greatly improve the effectiveness of their courses by availing online education to their students. Although many universities and institutions still use traditional educational models, most others are adopting this change towards the digital education modernization.

The breakup of the profiles of the primary participants is given below:

- By Company: Tier 1 - 20%, Tier 2 - 25%, and Tier 3 - 55%

- By Designation: C-Level Executives - 40%, Directors- 33%, Managers-27%

- By Region: North America - 32%, Europe - 38%, Asia Pacific - 18%, and Rest of the World* - 12%

Note: Others include sales managers, marketing managers, and product managers

Note: Rest of the World includes the Middle East & Africa and Latin America

Note: Tier 1 companies have revenues more than USD 100 million; tier 2 companies' revenue ranges from USD 10 million to USD 100 million; and tier 3 companies' revenue is less than 10 million

Source: Secondary Literature, Expert Interviews, and MarketsandMarkets Analysis

The following key Digital Education vendors are profiled in the report:

- Coursera (US)

- edX (US)

- Pluralsight (US)

- Udemy (US)

- Udacity (US)

- Edureka (India)

- Alison (Ireland)

- LinkedIn Learning (US)

- Jigsaw Academy (India)

- Iversity (Germany)

- Miriadax (Spain)

- Intellipaat (India)

- Edmodo (UK)

- NovoEd (US)

- XuetangX (China)

- Linkstreet Learning (India)

- Khan Academy (US)

- Kadenze (US)

- Federica Web Learning (Italy)

- My Mooc (France)

- Treehouse (US)

- Skillshare (US)

- CreativeLive (US)

- CXL (US)

- GO1 (Australia)

- BYJU'S (India)

- DataCamp (US)

- Platzi (US)

- Thinkful (US)

Research Coverage

The Digital Education Market is segmented by Type, Course Type, End User, and Region. A detailed analysis of the key industry players has been undertaken to provide insights into their business overviews; solutions and services; key strategies; new product launches and product enhancements; partnerships, acquisitions, and collaborations; agreements and business expansions; and competitive landscape associated within the Digital Education Market.

Reasons to Buy the Report

The report would help the market leaders and new entrants in the following ways:

- The report comprehensively and exhaustively segments the Digital Education Market and provides the closest approximations of the revenue numbers for the overall market and its subsegments across different regions.

- It provides impact of recession on the market, among top vendors worldwide along with figures which are the closest approximations, estimated and projected.

- It would help stakeholders understand the pulse of the market as analyzed information is provided basis the key market drivers, restraints, challenges, and opportunities in the market.

- It would help stakeholders understand the market dynamics better, their competitors better and gain more insights to uplift their positions in the market. The competitive landscape section includes a competitor ecosystem, market diversification parameters such as new product launch, product enhancement, partnerships, agreement, integration, collaborations, and acquisitions.

- Market quadrant of digital education vendors have been precisely incorporated as a figure which helps readers understand market players categorization and their performance.

- In-depth exhaustive assessment of market shares, growth strategies and service offerings of leading players such as Coursera (US), edX (US), Udemy (US), Udacity (US), Alison (Ireland), Edureka (India), LinkedIn Learning (US), Byju's (India), among others in the Digital education market strategies.

- The report also helps stakeholders understand the competitive analysis by these market players via competitive benchmarking, heat map.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- TABLE 1 USD EXCHANGE RATES, 2019-2022

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 DIGITAL EDUCATION MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakup of primary profiles

- FIGURE 2 BREAKUP OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

- 2.1.2.2 Primary respondents

- TABLE 2 PRIMARY RESPONDENTS: DIGITAL EDUCATION MARKET

- 2.1.2.3 Key industry insights

- 2.2 DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- FIGURE 3 DIGITAL EDUCATION MARKET: TOP-DOWN AND BOTTOM-UP APPROACHES

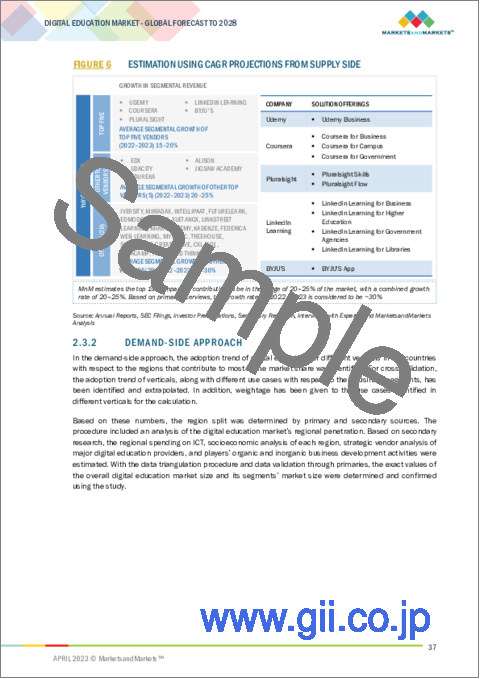

- 2.3.1 SUPPLY-SIDE APPROACH

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY APPROACH 1 (SUPPLY SIDE): REVENUE OF SERVICES FROM VENDORS

- FIGURE 5 BOTTOM-UP APPROACH (SUPPLY SIDE): COLLECTIVE REVENUE OF DIGITAL EDUCATION VENDORS

- FIGURE 6 ESTIMATION USING CAGR PROJECTIONS FROM SUPPLY SIDE

- 2.3.2 DEMAND-SIDE APPROACH

- FIGURE 7 MARKET SIZE ESTIMATION METHODOLOGY APPROACH 2 (BOTTOM-UP): REVENUE GENERATED BY VENDORS FROM EACH APPLICATION

- FIGURE 8 MARKET PROJECTIONS FROM DEMAND SIDE

- 2.4 MARKET FORECAST: FACTOR IMPACT ANALYSIS

- TABLE 3 FACTOR ANALYSIS

- 2.4.1 RECESSION IMPACT ANALYSIS

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- FIGURE 9 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

- FIGURE 10 GLOBAL DIGITAL EDUCATION MARKET, 2020-2028 (USD MILLION)

- 3.1 DIGITAL EDUCATION MARKET: OVERVIEW OF RECESSION IMPACT

- FIGURE 11 FASTEST-GROWING SEGMENTS IN DIGITAL EDUCATION MARKET, 2023-2028

- FIGURE 12 ACADEMIC INSTITUTIONS SEGMENT TO HOLD LARGER MARKET SIZE DURING FORECAST PERIOD

- FIGURE 13 SELF-PACED ONLINE EDUCATION SEGMENT TO HOLD LARGER MARKET SIZE DURING FORECAST PERIOD

- FIGURE 14 SCIENCE & TECHNOLOGY COURSES SEGMENT TO DOMINATE COURSE TYPE MARKET TILL 2028

- FIGURE 15 DIGITAL EDUCATION MARKET: REGIONAL SNAPSHOT

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE MARKET OPPORTUNITIES IN DIGITAL EDUCATION

- FIGURE 16 INCREASED INTERNET PENETRATION AND REDUCED INFRASTRUCTURE COST TO DRIVE DIGITAL EDUCATION MARKET

- 4.2 DIGITAL EDUCATION MARKET, BY END USER, 2023 VS. 2028

- FIGURE 17 ACADEMIC INSTITUTIONS SEGMENT TO HOLD LARGER MARKET SHARE DURING FORECAST PERIOD

- 4.3 DIGITAL EDUCATION MARKET, BY TYPE, 2023 VS. 2028

- FIGURE 18 SELF-PACED ONLINE EDUCATION SEGMENT TO HOLD LARGER MARKET SHARE DURING FORECAST PERIOD

- 4.4 DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023 VS. 2028

- FIGURE 19 SCIENCE & TECHNOLOGY COURSES SEGMENT TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- 4.5 DIGITAL EDUCATION MARKET: REGIONAL SCENARIO, 2023-2028

- FIGURE 20 ASIA PACIFIC TO EMERGE AS BEST MARKET FOR INVESTMENTS IN NEXT FIVE YEARS

- FIGURE 21 DIGITAL EDUCATION MARKET IN JAPAN TO GROW AT HIGHEST RATE DURING FORECAST PERIOD

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 22 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES: DIGITAL EDUCATION MARKET

- 5.2.1 DRIVERS

- 5.2.1.1 Growing internet penetration

- FIGURE 23 GLOBAL INTERNET PENETRATION: PERCENTAGE OF POPULATION

- 5.2.1.2 Reduced infrastructure cost and increased scalability using online learning

- 5.2.1.3 Increased self-efficacy, greater convenience, and more flexibility

- 5.2.1.4 Rising demand for microlearning

- 5.2.1.5 Remote access anytime, anywhere

- 5.2.2 RESTRAINTS

- 5.2.2.1 Lack of face-to-face interaction and direct monitoring

- 5.2.2.2 Health concerns due to more screen time

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rising demand for game-based learning

- 5.2.3.2 Growing inclination toward adaptive learning

- 5.2.4 CHALLENGES

- 5.2.4.1 Unreliable infrastructure in developing countries

- 5.2.4.2 Need for additional training

- 5.3 CASE STUDY ANALYSIS

- 5.3.1 CASE STUDY 1: ADOBE PARTNERED WITH COURSERA TO OFFER AI AND ML EDUCATION TO ENGINEERS

- 5.3.2 CASE STUDY 2: NTT DATA LEVERAGED UDEMY BUSINESS TO ELEVATE TECHNICAL AND PROFESSIONAL KNOWLEDGE OF EMPLOYEES

- 5.3.3 CASE STUDY 3: LEGO GROUP LEVERAGED LINKEDIN LEARNING FOR BUSINESS

- 5.3.4 CASE STUDY 4: TEAMHEALTH PARTNERED WITH PLURALSIGHT TO DEVELOP FIRST-EVER INNOVATION LAB WITH PLURALSIGHT SKILLS

- 5.3.5 CASE STUDY 5: REINVENTING AND SIMPLIFYING ELEARNING FOR FRONTLINE WORKERS

- 5.3.6 CASE STUDY 6: IT TEAM TRAINED ON RECENT UPGRADES AND TRENDS WITH UDEMY BUSINESS

- 5.4 ECOSYSTEM ANALYSIS

- FIGURE 24 DIGITAL EDUCATION MARKET: ECOSYSTEM

- TABLE 4 DIGITAL EDUCATION MARKET: ECOSYSTEM

- 5.5 SUPPLY CHAIN ANALYSIS

- FIGURE 25 SUPPLY CHAIN ANALYSIS: DIGITAL EDUCATION MARKET

- 5.5.1 CONTENT CREATORS

- 5.5.2 PLATFORM PROVIDERS

- 5.5.3 END USERS

- 5.6 PORTER'S FIVE FORCES ANALYSIS

- TABLE 5 PORTER'S FIVE FORCES ANALYSIS: DIGITAL EDUCATION MARKET

- FIGURE 26 PORTER'S FIVE FORCES ANALYSIS: DIGITAL EDUCATION MARKET

- 5.6.1 THREAT OF NEW ENTRANTS

- 5.6.2 THREAT OF SUBSTITUTES

- 5.6.3 BARGAINING POWER OF SUPPLIERS

- 5.6.4 BARGAINING POWER OF BUYERS

- 5.6.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.7 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.7.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 27 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP END USERS

- TABLE 6 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP END USERS (%)

- 5.7.2 BUYING CRITERIA

- FIGURE 28 KEY BUYING CRITERIA FOR TOP END USERS

- TABLE 7 KEY BUYING CRITERIA FOR TOP END USERS

- 5.8 TECHNOLOGY ANALYSIS

- 5.8.1 CLOUD/SOFTWARE AS A SERVICE

- 5.8.2 AI

- 5.8.3 ML

- 5.8.4 INTERNET OF THINGS TECHNOLOGY

- 5.9 PRICING ANALYSIS

- TABLE 8 DIGITAL EDUCATION MARKET: PRICING LEVELS

- 5.9.1 AVERAGE SELLING PRICE TREND

- 5.10 PATENT ANALYSIS

- FIGURE 29 NUMBER OF PATENT DOCUMENTS PUBLISHED, 2012-2022

- FIGURE 30 TOP FIVE PATENT OWNERS (GLOBAL)

- TABLE 9 TOP 10 PATENT APPLICANTS

- 5.11 REGULATORY LANDSCAPE

- 5.11.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.11.2 REGULATIONS, BY REGION

- 5.11.2.1 North America

- 5.11.2.2 Europe

- 5.11.2.3 Asia Pacific

- 5.11.2.4 Middle East & South Africa

- 5.11.2.5 Latin America

- 5.12 TRENDS/DISRUPTIONS IMPACTING BUYERS

- FIGURE 31 TRENDS/DISRUPTIONS IMPACTING BUYERS

- 5.13 KEY CONFERENCES AND EVENTS IN 2023-2024

- TABLE 14 DIGITAL EDUCATION MARKET: DETAILED LIST OF CONFERENCES AND EVENTS

6 DIGITAL EDUCATION MARKET, BY TYPE

- 6.1 INTRODUCTION

- FIGURE 32 INSTRUCTOR-LED ONLINE EDUCATION SEGMENT TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- 6.1.1 DRIVERS: DIGITAL EDUCATION MARKET, BY TYPE

- 6.1.1.1 Self-paced online education

- 6.1.1.2 Instructor-led online education

- TABLE 15 DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 16 DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 6.1.2 SELF-PACED ONLINE EDUCATION

- 6.1.2.1 Convenience and customization to draw end users

- TABLE 17 SELF-PACED ONLINE EDUCATION MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 18 SELF-PACED ONLINE EDUCATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 6.1.3 INSTRUCTOR-LED ONLINE EDUCATION

- 6.1.3.1 Availability of one-to-one interactions, Q&A sessions, and doubt clearance to foster adoption

- TABLE 19 INSTRUCTOR-LED ONLINE EDUCATION MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 20 INSTRUCTOR-LED ONLINE EDUCATION MARKET, BY REGION, 2023-2028 (USD MILLION)

7 DIGITAL EDUCATION MARKET, BY COURSE TYPE

- 7.1 INTRODUCTION

- FIGURE 33 SCIENCE & TECHNOLOGY COURSES TO GROW AT HIGHEST CAGR

- 7.1.1 DRIVERS: DIGITAL EDUCATION MARKET, BY COURSE TYPE

- 7.1.1.1 Science and technology courses

- 7.1.1.2 Entrepreneurship & business management courses

- 7.1.1.3 Other courses

- TABLE 21 DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 22 DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- 7.1.2 SCIENCE & TECHNOLOGY COURSES

- 7.1.2.1 Higher demand for technical courses to ensure market growth

- TABLE 23 DIGITAL EDUCATION MARKET FOR SCIENCE & TECHNOLOGY COURSES, BY REGION, 2019-2022 (USD MILLION)

- TABLE 24 DIGITAL EDUCATION MARKET FOR SCIENCE & TECHNOLOGY COURSES, BY REGION, 2023-2028 (USD MILLION)

- 7.1.3 ENTREPRENEURSHIP & BUSINESS MANAGEMENT COURSES

- 7.1.3.1 Growing demand from individuals to upgrade management skills to boost market

- TABLE 25 DIGITAL EDUCATION MARKET FOR ENTREPRENEURSHIP & BUSINESS MANAGEMENT COURSES, BY REGION, 2019-2022 (USD MILLION)

- TABLE 26 DIGITAL EDUCATION MARKET FOR ENTREPRENEURSHIP & BUSINESS MANAGEMENT COURSES, BY REGION, 2023-2028 (USD MILLION)

- 7.1.4 OTHER COURSES

- TABLE 27 DIGITAL EDUCATION MARKET FOR OTHER COURSES, BY REGION, 2019-2022 (USD MILLION)

- TABLE 28 DIGITAL EDUCATION MARKET FOR OTHER COURSES, BY REGION, 2023-2028 (USD MILLION)

8 DIGITAL EDUCATION MARKET, BY END USER

- 8.1 INTRODUCTION

- FIGURE 34 ACADEMIC INSTITUTIONS TO SHOW HIGHEST GROWTH

- 8.1.1 DRIVERS: DIGITAL EDUCATION MARKET, BY END USER

- 8.1.1.1 Academic institutions

- 8.1.1.2 Enterprises and public sector

- TABLE 29 DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 30 DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- 8.1.2 ACADEMIC INSTITUTIONS

- 8.1.2.1 Adoption of virtual learning to significantly boost market growth

- TABLE 31 DIGITAL EDUCATION MARKET FOR ACADEMIC INSTITUTIONS, BY REGION, 2019-2022 (USD MILLION)

- TABLE 32 DIGITAL EDUCATION MARKET FOR ACADEMIC INSTITUTIONS, BY REGION, 2023-2028 (USD MILLION)

- 8.1.3 ENTERPRISES & PUBLIC SECTOR

- 8.1.3.1 Need to upgrade employee skills/upskill employees to propel adoption

- TABLE 33 DIGITAL EDUCATION MARKET FOR ENTERPRISES & PUBLIC SECTOR, BY REGION, 2019-2022 (USD MILLION)

- TABLE 34 DIGITAL EDUCATION MARKET FOR ENTERPRISES & PUBLIC SECTOR, BY REGION, 2023-2028 (USD MILLION)

9 DIGITAL EDUCATION MARKET, BY REGION

- 9.1 INTRODUCTION

- FIGURE 35 NORTH AMERICA TO LEAD DIGITAL EDUCATION MARKET DURING FORECAST PERIOD

- TABLE 35 DIGITAL EDUCATION MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 36 DIGITAL EDUCATION MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.2 NORTH AMERICA

- 9.2.1 NORTH AMERICA: DIGITAL EDUCATION MARKET DRIVERS

- 9.2.2 NORTH AMERICA: RECESSION IMPACT

- FIGURE 36 NORTH AMERICA: MARKET SNAPSHOT

- TABLE 37 NORTH AMERICA: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 38 NORTH AMERICA: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 39 NORTH AMERICA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 40 NORTH AMERICA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 41 NORTH AMERICA: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 42 NORTH AMERICA: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- TABLE 43 NORTH AMERICA: DIGITAL EDUCATION MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 44 NORTH AMERICA: DIGITAL EDUCATION MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 9.2.3 US

- 9.2.3.1 Advanced IT infrastructure, presence of many enterprises, and availability of technical expertise to boost market

- TABLE 45 US: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 46 US: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 47 US: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 48 US: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 49 US: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 50 US: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- 9.2.4 CANADA

- 9.2.4.1 Low cost of university education in Canada to attract large student population

- TABLE 51 CANADA: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 52 CANADA: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 53 CANADA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 54 CANADA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 55 CANADA: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 56 CANADA: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- 9.3 EUROPE

- 9.3.1 EUROPE: DIGITAL EDUCATION MARKET DRIVERS

- 9.3.2 EUROPE: RECESSION IMPACT

- TABLE 57 EUROPE: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 58 EUROPE: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 59 EUROPE: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 60 EUROPE: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 61 EUROPE: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 62 EUROPE: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- TABLE 63 EUROPE: DIGITAL EDUCATION MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 64 EUROPE: DIGITAL EDUCATION MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 9.3.3 UK

- 9.3.3.1 Growing adoption of cloud and AI technologies to increase interest in digital education solutions

- TABLE 65 UK: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 66 UK: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 67 UK: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 68 UK: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 69 UK: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 70 UK: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- 9.3.4 GERMANY

- 9.3.4.1 Early adoption of 5G and well-established infrastructure to favor market

- TABLE 71 GERMANY: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 72 GERMANY: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 73 GERMANY: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 74 GERMANY: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 75 GERMANY: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 76 GERMANY: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- 9.3.5 FRANCE

- 9.3.5.1 Strong innovation environment and high internet penetration to boost growth

- TABLE 77 FRANCE: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 78 FRANCE: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 79 FRANCE: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 80 FRANCE: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 81 FRANCE: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 82 FRANCE: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- 9.3.6 REST OF EUROPE

- TABLE 83 REST OF EUROPE: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 84 REST OF EUROPE: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 85 REST OF EUROPE: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 86 REST OF EUROPE: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 87 REST OF EUROPE: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 88 REST OF EUROPE: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- 9.4 ASIA PACIFIC

- 9.4.1 ASIA PACIFIC: DIGITAL EDUCATION MARKET DRIVERS

- 9.4.2 ASIA PACIFIC: RECESSION IMPACT

- FIGURE 37 ASIA PACIFIC: MARKET SNAPSHOT

- TABLE 89 ASIA PACIFIC: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 90 ASIA PACIFIC: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 91 ASIA PACIFIC: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 92 ASIA PACIFIC: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 93 ASIA PACIFIC: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 94 ASIA PACIFIC: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- TABLE 95 ASIA PACIFIC: DIGITAL EDUCATION MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 96 ASIA PACIFIC: DIGITAL EDUCATION MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 9.4.3 JAPAN

- 9.4.3.1 Advanced ICT capabilities to bolster market

- TABLE 97 JAPAN: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 98 JAPAN: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 99 JAPAN: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 100 JAPAN: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 101 JAPAN: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 102 JAPAN: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- 9.4.4 CHINA

- 9.4.4.1 China to dominate digital education market

- TABLE 103 CHINA: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 104 CHINA: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 105 CHINA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 106 CHINA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 107 CHINA: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 108 CHINA: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- 9.4.5 INDIA

- 9.4.5.1 Digital India initiative to support digital education sector

- TABLE 109 INDIA: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 110 INDIA: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 111 INDIA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 112 INDIA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 113 INDIA: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 114 INDIA: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- 9.4.6 AUSTRALIA

- 9.4.6.1 Shift to advanced digital education solutions to boost digital education requirements among large enterprises

- TABLE 115 AUSTRALIA: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 116 AUSTRALIA: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 117 AUSTRALIA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 118 AUSTRALIA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 119 AUSTRALIA: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 120 AUSTRALIA: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- 9.4.7 REST OF ASIA PACIFIC

- TABLE 121 REST OF ASIA PACIFIC: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 122 REST OF ASIA PACIFIC: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 123 REST OF ASIA PACIFIC: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 124 REST OF ASIA PACIFIC: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 125 REST OF ASIA PACIFIC: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 126 REST OF ASIA PACIFIC: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- 9.5 MIDDLE EAST & AFRICA

- 9.5.1 MIDDLE EAST AND AFRICA: DIGITAL EDUCATION MARKET DRIVERS

- 9.5.2 MIDDLE EAST AND AFRICA: RECESSION IMPACT

- TABLE 127 MIDDLE EAST & AFRICA: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 128 MIDDLE EAST & AFRICA: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 129 MIDDLE EAST & AFRICA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 130 MIDDLE EAST & AFRICA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 131 MIDDLE EAST & AFRICA: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 132 MIDDLE EAST & AFRICA: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- TABLE 133 MIDDLE EAST & AFRICA: DIGITAL EDUCATION MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 134 MIDDLE EAST & AFRICA: DIGITAL EDUCATION MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 9.5.3 UAE

- 9.5.3.1 UAE market to show highest CAGR over forecast period

- TABLE 135 UAE: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 136 UAE: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 137 UAE: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 138 UAE: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 139 UAE: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 140 UAE: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- 9.5.4 KSA

- 9.5.4.1 Saudi Arabia to hold largest market share in Middle East & Africa

- TABLE 141 KSA: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 142 KSA: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 143 KSA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 144 KSA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 145 KSA: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 146 KSA: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- 9.5.5 REST OF MIDDLE EAST & AFRICA

- TABLE 147 REST OF MIDDLE EAST & AFRICA: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 148 REST OF MIDDLE EAST & AFRICA: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 149 REST OF MIDDLE EAST & AFRICA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 150 REST OF MIDDLE EAST & AFRICA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 151 REST OF MIDDLE EAST & AFRICA: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 152 REST OF MIDDLE EAST & AFRICA: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- 9.6 LATIN AMERICA

- 9.6.1 LATIN AMERICA: DIGITAL EDUCATION MARKET DRIVERS

- 9.6.2 LATIN AMERICA: RECESSION IMPACT

- TABLE 153 LATIN AMERICA: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 154 LATIN AMERICA: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 155 LATIN AMERICA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 156 LATIN AMERICA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 157 LATIN AMERICA: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 158 LATIN AMERICA: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- TABLE 159 LATIN AMERICA: DIGITAL EDUCATION MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 160 LATIN AMERICA: DIGITAL EDUCATION MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 9.6.3 BRAZIL

- 9.6.3.1 High FDI and presence of large enterprises to drive digital education market

- TABLE 161 BRAZIL: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 162 BRAZIL: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 163 BRAZIL: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 164 BRAZIL: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 165 BRAZIL: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 166 BRAZIL: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- 9.6.4 MEXICO

- 9.6.4.1 Advancements in mobile communications and high internet penetration to boost growth of digital education

- TABLE 167 MEXICO: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 168 MEXICO: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 169 MEXICO: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 170 MEXICO: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 171 MEXICO: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 172 MEXICO: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

- 9.6.5 REST OF LATIN AMERICA

- TABLE 173 REST OF LATIN AMERICA: DIGITAL EDUCATION MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 174 REST OF LATIN AMERICA: DIGITAL EDUCATION MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 175 REST OF LATIN AMERICA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2019-2022 (USD MILLION)

- TABLE 176 REST OF LATIN AMERICA: DIGITAL EDUCATION MARKET, BY COURSE TYPE, 2023-2028 (USD MILLION)

- TABLE 177 REST OF LATIN AMERICA: DIGITAL EDUCATION MARKET, BY END USER, 2019-2022 (USD MILLION)

- TABLE 178 REST OF LATIN AMERICA: DIGITAL EDUCATION MARKET, BY END USER, 2023-2028 (USD MILLION)

10 COMPETITIVE LANDSCAPE

- 10.1 INTRODUCTION

- 10.2 MARKET SHARE OF TOP VENDORS

- TABLE 179 INTENSITY OF COMPETITIVE RIVALRY

- FIGURE 38 MARKET SHARE ANALYSIS, 2022

- 10.3 REVENUE ANALYSIS OF TOP FIVE VENDORS

- FIGURE 39 REVENUE ANALYSIS OF TOP FIVE VENDORS, 2018-2022 (USD MILLION)

- 10.4 COMPANY EVALUATION QUADRANT, 2022

- 10.4.1 DEFINITIONS AND METHODOLOGY

- FIGURE 40 KEY PLAYER EVALUATION QUADRANT: CRITERIA WEIGHTAGE

- 10.4.2 STARS

- 10.4.3 EMERGING LEADERS

- 10.4.4 PERVASIVE PLAYERS

- 10.4.5 PARTICIPANTS

- FIGURE 41 COMPANY EVALUATION QUADRANT, 2022

- TABLE 180 COMPANY FOOTPRINT (TOP 10 PLAYERS)

- 10.5 COMPANY EVALUATION QUADRANT FOR STARTUPS/SMES, 2022

- 10.5.1 DEFINITION AND METHODOLOGY

- FIGURE 42 COMPANY EVALUATION QUADRANT FOR STARTUPS/SMES: CRITERIA WEIGHTAGE

- 10.5.2 PROGRESSIVE COMPANIES

- 10.5.3 RESPONSIVE COMPANIES

- 10.5.4 DYNAMIC COMPANIES

- 10.5.5 STARTING BLOCKS

- FIGURE 43 COMPANY EVALUATION QUADRANT FOR STARTUPS/SMES, 2022

- 10.6 COMPETITIVE BENCHMARKING FOR STARTUPS/SMES

- TABLE 181 COMPETITIVE BENCHMARKING FOR STARTUPS/SMES

- TABLE 182 ANALYSIS OF KEY STARTUPS/SMES

- 10.7 COMPANY FINANCIAL METRICS

- FIGURE 44 COMPANY FINANCIAL METRICS, 2022

- 10.8 GLOBAL SNAPSHOT OF KEY MARKET PARTICIPANTS

- FIGURE 45 DIGITAL EDUCATION: GLOBAL SNAPSHOT OF KEY MARKET PARTICIPANTS, 2022

- 10.9 COMPETITIVE SCENARIO

- 10.9.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 183 DIGITAL EDUCATION MARKET: PRODUCT LAUNCHES AND ENHANCEMENTS, JANUARY 2020-FEBRUARY 2023

- 10.9.2 DEALS

- TABLE 184 DIGITAL EDUCATION MARKET: DEALS, FEBRUARY 2020-MARCH 2023

11 COMPANY PROFILES

- 11.1 KEY COMPANIES

- (Business overview, Products offered, Recent Developments, MNM view)**

- 11.1.1 COURSERA

- TABLE 185 COURSERA: BUSINESS OVERVIEW

- FIGURE 46 COURSERA: COMPANY SNAPSHOT

- TABLE 186 COURSERA: PRODUCTS/SOLUTIONS OFFERED

- TABLE 187 COURSERA: PRODUCT LAUNCHES

- TABLE 188 COURSERA: DEALS

- 11.1.2 EDX

- TABLE 189 EDX: BUSINESS OVERVIEW

- TABLE 190 EDX: PRODUCTS/SOLUTIONS OFFERED

- TABLE 191 EDX: PRODUCT LAUNCHES

- TABLE 192 EDX: DEALS

- 11.1.3 PLURALSIGHT

- TABLE 193 PLURALSIGHT: BUSINESS OVERVIEW

- TABLE 194 PLURALSIGHT: PRODUCTS/SOLUTIONS OFFERED

- TABLE 195 PLURALSIGHT: PRODUCT LAUNCHES

- TABLE 196 PLURALSIGHT: DEALS

- 11.1.4 UDEMY

- TABLE 197 UDEMY: BUSINESS OVERVIEW

- FIGURE 47 UDEMY: COMPANY SNAPSHOT

- TABLE 198 UDEMY: PRODUCTS/SOLUTIONS OFFERED

- TABLE 199 UDEMY: PRODUCT LAUNCHES

- TABLE 200 UDEMY: DEALS

- 11.1.5 UDACITY

- TABLE 201 UDACITY: BUSINESS OVERVIEW

- TABLE 202 UDACITY: PRODUCTS/SOLUTIONS OFFERED

- TABLE 203 UDACITY: PRODUCT LAUNCHES

- TABLE 204 UDACITY: DEALS

- 11.1.6 EDUREKA

- TABLE 205 EDUREKA: BUSINESS OVERVIEW

- TABLE 206 EDUREKA: PRODUCTS/SOLUTIONS OFFERED

- 11.1.7 ALISON

- TABLE 207 ALISON: BUSINESS OVERVIEW

- TABLE 208 ALISON: PRODUCTS/SOLUTIONS OFFERED

- TABLE 209 ALISON: PRODUCT LAUNCHES

- TABLE 210 ALISON: DEALS

- 11.1.8 LINKEDIN LEARNING

- TABLE 211 LINKEDIN LEARNING: BUSINESS OVERVIEW

- TABLE 212 LINKEDIN LEARNING: PRODUCTS/SOLUTIONS OFFERED

- TABLE 213 LINKEDIN LEARNING: DEALS

- 11.1.9 JIGSAW ACADEMY

- TABLE 214 JIGSAW ACADEMY: BUSINESS OVERVIEW

- TABLE 215 JIGSAW ACADEMY: PRODUCTS/SOLUTIONS OFFERED

- 11.1.10 IVERSITY

- TABLE 216 IVERSITY: BUSINESS OVERVIEW

- TABLE 217 IVERSITY: PRODUCTS/SOLUTIONS OFFERED

- *Details on Business overview, Products offered, Recent Developments, MNM view might not be captured in case of unlisted companies.

- 11.2 OTHER PLAYERS

- 11.2.1 MIRIADAX

- 11.2.2 INTELLIPAAT

- 11.2.3 FUTURELEARN

- 11.2.4 EDMODO

- 11.2.5 SWAYAM

- 11.2.6 NOVOED

- 11.2.7 XUETANGX

- 11.2.8 LINKSTREET LEARNING (RAPL)

- 11.2.9 KHAN ACADEMY

- 11.2.10 KADENZE

- 11.2.11 FEDERICA WEB LEARNING

- 11.2.12 MY MOOC

- 11.2.13 TREEHOUSE

- 11.2.14 SKILLSHARE

- 11.2.15 CREATIVELIVE

- 11.2.16 CXL

- 11.2.17 GO1

- 11.2.18 BYJU'S

- 11.2.19 DATACAMP

- 11.2.20 PLATZI

- 11.2.21 THINKFUL

12 ADJACENT & RELATED MARKETS

- 12.1 INTRODUCTION

- 12.2 LEARNING MANAGEMENT SYSTEM MARKET

- TABLE 218 LEARNING MANAGEMENT SYSTEM MARKET, BY COMPONENT, 2017-2021 (USD MILLION)

- TABLE 219 LEARNING MANAGEMENT SYSTEM MARKET, BY COMPONENT, 2022-2027 (USD MILLION)

- TABLE 220 LEARNING MANAGEMENT SYSTEM MARKET, BY DELIVERY MODE, 2017-2021 (USD MILLION)

- TABLE 221 LEARNING MANAGEMENT SYSTEM MARKET, BY DELIVERY MODE, 2022-2027 (USD MILLION)

- TABLE 222 LEARNING MANAGEMENT SYSTEM MARKET, BY USER TYPE, 2017-2021 (USD MILLION)

- TABLE 223 LEARNING MANAGEMENT SYSTEM MARKET, BY USER TYPE, 2022-2027 (USD MILLION)

- TABLE 224 LEARNING MANAGEMENT SYSTEM MARKET FOR CORPORATE USERS, BY TYPE, 2017-2021 (USD MILLION)

- TABLE 225 LEARNING MANAGEMENT SYSTEM MARKET FOR CORPORATE USERS, BY TYPE, 2022-2027 (USD MILLION)

- TABLE 226 LEARNING MANAGEMENT SYSTEM MARKET, BY DEPLOYMENT TYPE, 2017-2021 (USD MILLION)

- TABLE 227 LEARNING MANAGEMENT SYSTEM MARKET, BY DEPLOYMENT TYPE, 2022-2027 (USD MILLION)

- TABLE 228 LEARNING MANAGEMENT SYSTEM MARKET, BY REGION, 2017-2021 (USD MILLION)

- TABLE 229 LEARNING MANAGEMENT SYSTEM MARKET, BY REGION, 2022-2027 (USD MILLION)

- 12.3 SMART LEARNING MARKET

- TABLE 230 SMART LEARNING MARKET, BY COMPONENT, 2017-2020 (USD MILLION)

- TABLE 231 SMART LEARNING MARKET, BY COMPONENT, 2021-2026 (USD MILLION)

- TABLE 232 SMART LEARNING MARKET, BY SERVICE, 2017-2020 (USD MILLION)

- TABLE 233 SMART LEARNING MARKET, BY SERVICE, 2021-2026 (USD MILLION)

- TABLE 234 SMART LEARNING MARKET, BY LEARNING TYPE, 2017-2020 (USD MILLION)

- TABLE 235 SMART LEARNING MARKET, BY LEARNING TYPE, 2021-2026 (USD MILLION)

- TABLE 236 SMART LEARNING MARKET, BY END USER, 2017-2020 (USD MILLION)

- TABLE 237 SMART LEARNING MARKET, BY END USER, 2021-2026 (USD MILLION)

- TABLE 238 SMART LEARNING MARKET, BY REGION, 2017-2020 (USD MILLION)

- TABLE 239 SMART LEARNING MARKET, BY REGION, 2021-2026 (USD MILLION)

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS