|

|

市場調査レポート

商品コード

1257392

バイオマス発電の世界市場:技術別 (燃焼、ガス化、嫌気性消化、熱分解)・原料別 (農業廃棄物、森林廃棄物、動物排泄物、都市廃棄物)・燃料別 (固体、液体、気体)・地域別の将来予測 (2028年まで)Biomass Power Generation Market by Technology (Combustion, Gasification, Anaerobic Digestion, Pyrolysis), Feedstock (Agricultural Waste, Forest Waste, Animal Waste, Municipal Waste), Fuel (Solid, Liquid, Gaseous) and Region - Global Forecast to 2028 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| バイオマス発電の世界市場:技術別 (燃焼、ガス化、嫌気性消化、熱分解)・原料別 (農業廃棄物、森林廃棄物、動物排泄物、都市廃棄物)・燃料別 (固体、液体、気体)・地域別の将来予測 (2028年まで) |

|

出版日: 2023年03月30日

発行: MarketsandMarkets

ページ情報: 英文 190 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界のバイオマス発電の市場規模は、2023年の913億米ドルから2028年には1,057億米ドルに達し、予測期間中に3.0%のCAGRで成長する、と予想されます。

産業分野での自家発電用エネルギー需要の増加が、バイオマス発電市場の主な促進要因となっています。

"森林廃棄物:原料別で最大セグメント"

原料別に見ると、2022年には森林廃棄物が最も大きなシェアを占めると推定されます。森林バイオマス廃棄物は、森林伐採の副産物で、木材チップ・樹皮・おがくず・製材スクラップ・倒木などが含まれます。森林廃棄物は、発電に大きく利用されてきました。推定によると、中国は利用可能なエネルギー資源のうち、50%の森林バイオマスを発電とバイオ燃料に使用しています。

"ガス化:技術別で2番目に大きなセグメントとして浮上する"

技術別に見ると、2022年にはガス化が第2位のシェアを占めると予想されています。燃焼と熱分解の価格は近年大幅に低下しているため、ガス化はコスト面での激しい競争に直面しています。一方、こうした状況が、各国にエネルギーの対外依存度を引き下げ、エネルギー安全保障を向上させる機会を提供しています。

"燃料別では、固体燃料分野が予測期間中に最も急成長する"

固形燃料セグメントは、予測期間中に最も急成長するセグメントとなる見込みです。特に木質バイオマスは、発電用固体燃料として広く好まれています。米国エネルギー省は、化石燃料とバイオマス固体燃料の両方が、発電施設のライフサイクルにおいて地球温暖化に与える影響を調査しました。

"欧州が2番目に大きな成長地域となる"

欧州は予測期間中、2番目に急速に成長するバイオマス発電市場になると予想されます。欧州連合は、輸送や電力を中心とした産業全体の用途にクリーンなエネルギー源を効率的に利用するために、欧州グリーンディールを実施しました。このイニシアチブは、2050年までに廃棄物、エネルギー、燃料に関する欧州のネットゼロ目標の一環として、二酸化炭素排出量を削減するために実施されました。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 顧客のビジネスに影響を与える動向/混乱

- バリュー/サプライチェーン分析

- エコシステム分析

- 技術分析

- 価格分析

- 特許分析

- 関税と規制の枠組み

- 主な会議とイベント (2023年)

- 貿易分析

- ケーススタディ分析

- ポーターのファイブフォース分析

- 主な利害関係者と購入基準

- バイオマス原料の需給分析

第6章 バイオマス発電市場:原料別

- イントロダクション

- 農業廃棄物

- 森林廃棄物

- 動物排泄物

- 都市廃棄物

第7章 バイオマス発電市場:技術別

- イントロダクション

- 燃焼

- ガス化

- 嫌気性消化

- 熱分解

第8章 バイオマス発電市場:燃料別

- イントロダクション

- 固形燃料

- 液体燃料

- 気体燃料

第9章 バイオマス発電市場:地域別

- イントロダクション

- 欧州

- ドイツ

- 英国

- フィンランド

- スウェーデン

- イタリア

- フランス

- オランダ

- 他の欧州諸国

- アジア太平洋

- 中国

- 日本

- インド

- インドネシア

- タイ

- 他のアジア太平洋諸国

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- 他の南米諸国

- 中東・アフリカ

- 南アフリカ

- トルコ

- エジプト

- イスラエル

- 他の中東・アフリカ諸国

第10章 競合情勢

- 概要

- 市場シェア分析 (2022年)

- 市場評価フレームワーク (2018年~2021年)

- 上位企業の収益分析:セグメント別

- 近年の動向

- 資本取引

- その他

- 競合リーダーシップマッピング

- スタートアップ/中小企業の評価クアドラント (2021年)

- 競合ベンチマーキング

第11章 企業プロファイル

- 主要企業

- ENGIE

- XCEL ENERGY INC.

- BABCOCK & WILCOX ENTERPRISES, INC.

- ØRSTED A/S

- EPH

- RWE

- RENOVA INC.

- VEOLIA ENERGY HUNGARY CO. LTD.

- ACCIONA

- EDF RENEWABLE ENERGY

- DRAX GROUP

- SALZBURG AG

- LAHTI ENERGIA OY

- VATTENFALL

- STATKRAFT

- その他の企業

- GRETA ENERGY LIMITED

- YONAGO BIOMASS POWER GENERATION LLC

- BELGIAN ECO ENERGY (BEE)

- D.E.S.I. POWER

- ENEXOR ENERGY LLC

第12章 付録

The global biomass power generation market is estimated to grow from USD 91.3 Billion in 2023 to USD 105.7 Billion by 2028; it is expected to record a CAGR of 3.0% during the forecast period. Increase in the energy demand for in-house electricity generation from industrial sector which drives the biomass power generation market.

"Forest Waste: The largest segment of the biomass power generation market, by feedstock "

Based on feedstock, the biomass power generation market has been split into four types: Agriculture Waste, Forest Waste, Animal Waste and Municipal Waste. The forest waste were estimated to have the largest share of the biomass power generation market in 2022. Forest biomass waste is the by-product of forest harvesting, which includes wood chips, bark, sawdust, mill scrap, and timber slash. Forest waste has been used largely for power generation. As per estimates, China uses 50% of the forest biomass among the available energy resources to generate power and biofuel.

"Gasification segment is expected to emerge as the second-largest segment based on technology"

By technology, the biomass power generation market has been segmented into combustion, pyrolysis, gasification and anaerobic digestion. Gasification are expected to be the second largest share of the biomass power generation market in 2022. Gasification is becoming increasingly competitive in terms of cost, with the price of combustion and pyrolysis dropping significantly in recent years. They offer an opportunity for countries to reduce their reliance on improve energy security.

"By fuel, the Solid Fuel segment is expected to be the fastest growing market during the forecast period."

Based on Solid fuel, the biomass power generation market is segmented into solid fuel, liquid fuel and gaseous fuel. The Solid fuel segment is expected to be the fastest-growing segment during the forecast period. Woody biomass is mostly the preferred solid fuel for power generation. The US Department of Energy studied the impact of both fossil fuels and biomass solid fuels on global warming during the life cycle of a power generation facility.

Europe is expected to be the second largest growing region in the biomass power generation market

Europe is expected to be the second fastest biomass power generation market during the forecast period. The European Union implemented the European Green Deal to efficiently use clean energy sources for applications across industries, especially transportation and power. The initiative was implemented to reduce carbon emissions as a part of European net zero goals for waste, energy, and fuel by 2050.

Breakdown of Primaries:

In-depth interviews have been conducted with various key industry participants, subject-matter experts, C-level executives of key market players, and industry consultants, among other experts, to obtain and verify critical qualitative and quantitative information, as well as to assess future market prospects. The distribution of primary interviews is as follows:

By Company Type: Tier 1- 65%, Tier 2- 24%, and Tier 3- 11%

By Designation: C-Level- 30%, Director Levels- 25%, and Others- 45%

By Region: North America- 35%, Asia Pacific- 25%, Europe- 15%, the Middle East & Africa- 15%, and South America- 10%

Note: Others include product engineers, product specialists, and engineering leads.

Note: The tiers of the companies are defined on the basis of their total revenues as of 2021. Tier 1: > USD 1 billion, Tier 2: From USD 500 million to USD 1 billion, and Tier 3: < USD 500 million

The biomass power generation market is dominated by a few major players that have a wide regional presence. The leading players in the biomass power generation market are ENGIE (France), Babcock & Wilcox Enterprises, Inc. (US), Xcel Energy Inc. (US), EPH (Czechia) and Ørsted A/S (Denmark).

Research Coverage:

The report defines, describes, and forecasts the global biomass power generation market, by component, power source, application, and region. It also offers a detailed qualitative and quantitative analysis of the market. The report provides a comprehensive review of the major market drivers, restraints, opportunities, and challenges. It also covers various important aspects of the market. These include an analysis of the competitive landscape, market dynamics, market estimates, in terms of value, and future trends in the biomass power generation market.

Key Benefits of Buying the Report

- Electrification of rural areas and Investments in upgrading and expanding transmission and distribution infrastructure are some of the main factors driving the biomass power generation market. Factors such as high installation costs and lack of common standards for electrification in some countries still restrain the market. Increased government mandates for upgrading electrical infrastructure and reducing power losses provide opportunities for the biomass power generation market to grow. Even though delays in electrical transmission projects are major challenges faced by countries under biomass power plant development.

- Product Development/ Innovation: The future of the biomass power generation market looks bright for renewable energy or bioenergy to reduce the carbon footprints. As investments are increasing in renewable energy sector, technology become less expensive due to improvements in modules and the ability to connect directly to higher voltage systems.

- Market Development: Renewable energy sources are becoming increasingly important in the grid infrastructure for power generation. Renewables include sources such as solar, wind, hydro, geothermal, and biomass, among others. Asia Pacific biomass power generation market is expected to experience significant growth in the coming years, driven by increasing demand for electricity in rural areas.

- Market Diversification: ENGIE signed an agreement with Alier, a paper recycle specialist, to build and commission a new thermal energy generation plant from sustainable forest management in Rosello's factory, specializing in manufacturing paper for the construction and packaging industries (Lleida).

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like ENGIE (France), Babcock & Wilcox Enterprises, Inc. (US), Xcel Energy Inc. (US), EPH (Czechia) and Ørsted A/S (Denmark) among others in the biomass power generation market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 INCLUSIONS AND EXCLUSIONS

- 1.4 STUDY SCOPE

- FIGURE 1 BIOMASS POWER GENERATION MARKET: SEGMENTATION

- 1.4.1 BIOMASS POWER GENERATION MARKET: REGIONAL SCOPE

- 1.4.2 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 BIOMASS POWER GENERATION MARKET: RESEARCH DESIGN

- 2.2 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 3 DATA TRIANGULATION

- 2.2.1 SECONDARY DATA

- 2.2.1.1 Key data from secondary sources

- 2.2.2 PRIMARY DATA

- 2.2.2.1 Key data from primary sources

- 2.2.2.2 Breakdown of primaries

- FIGURE 4 BREAKDOWN OF PRIMARIES

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 BOTTOM-UP APPROACH

- FIGURE 5 BIOMASS POWER GENERATION MARKET: BOTTOM-UP APPROACH

- 2.3.2 TOP-DOWN APPROACH

- FIGURE 6 BIOMASS POWER GENERATION MARKET: TOP-DOWN APPROACH

- 2.3.3 DEMAND-SIDE ANALYSIS

- FIGURE 7 BIOMASS POWER GENERATION MARKET: DEMAND-SIDE ANALYSIS

- FIGURE 8 METRICS CONSIDERED TO ANALYZE AND ASSESS DEMAND FOR BIOMASS POWER GENERATION SYSTEMS

- 2.3.3.1 Assumptions for demand-side analysis

- 2.3.3.2 Calculations to derive market size using demand-side analysis

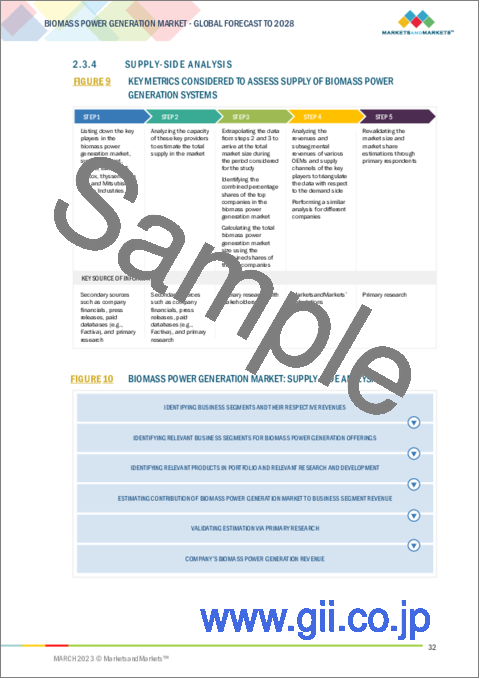

- 2.3.4 SUPPLY-SIDE ANALYSIS

- FIGURE 9 KEY METRICS CONSIDERED TO ASSESS SUPPLY OF BIOMASS POWER GENERATION SYSTEMS

- FIGURE 10 BIOMASS POWER GENERATION MARKET: SUPPLY-SIDE ANALYSIS

- 2.3.4.1 Assumptions for supply-side analysis

- FIGURE 11 COMPANY ANALYSIS, 2022

- 2.4 FORECAST

- 2.5 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- TABLE 1 BIOMASS POWER GENERATION MARKET: SNAPSHOT

- FIGURE 12 ASIA PACIFIC DOMINATED BIOMASS POWER GENERATION MARKET IN 2022

- FIGURE 13 FOREST WASTE SEGMENT TO LEAD BIOMASS POWER GENERATION MARKET DURING FORECAST PERIOD

- FIGURE 14 COMBUSTION SEGMENT TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- FIGURE 15 SOLID FUEL SEGMENT TO DOMINATE BIOMASS POWER GENERATION MARKET DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN BIOMASS POWER GENERATION MARKET

- FIGURE 16 GROWING NEED TO DECARBONIZE INDUSTRIAL SECTOR

- 4.2 BIOMASS POWER GENERATION MARKET, BY REGION

- FIGURE 17 ASIA PACIFIC TO WITNESS HIGHEST GROWTH IN BIOMASS POWER GENERATION MARKET DURING FORECAST PERIOD

- 4.3 ASIA PACIFIC BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK AND COUNTRY

- FIGURE 18 FOREST WASTE SEGMENT AND CHINA DOMINATED ASIA PACIFIC BIOMASS POWER GENERATION MARKET IN 2022

- 4.4 BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK

- FIGURE 19 FOREST WASTE SEGMENT TO WITNESS SIGNIFICANT GROWTH DURING FORECAST PERIOD

- 4.5 BIOMASS POWER GENERATION MARKET, BY TECHNOLOGY

- FIGURE 20 COMBUSTION SEGMENT DOMINATED BIOMASS POWER GENERATION MARKET IN 2022

- 4.6 BIOMASS POWER GENERATION MARKET, BY FUEL

- FIGURE 21 SOLID FUEL SEGMENT ACCOUNTED FOR LARGEST MARKET SHARE IN 2022

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 22 BIOMASS POWER GENERATION MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Abundant availability of biomass feedstocks

- FIGURE 23 CUMULATIVE AGRICULTURAL RESIDUE GENERATION IN SELECTED COUNTRIES

- FIGURE 24 MAJOR FOREST RESIDUE-PRODUCING COUNTRIES

- 5.2.1.2 Government-led initiatives to boost bioenergy production

- FIGURE 25 NUMBER OF POLICIES ISSUED IN CHINA RELATED TO BIOMASS POWER GENERATION, 2006-2021

- 5.2.1.3 Increasing employment in agriculture industry and growing rural development

- FIGURE 26 EMPLOYMENT RATE IN BIOENERGY INDUSTRY

- 5.2.1.4 Rising need to control greenhouse gas (GHG) emissions

- 5.2.1.5 Growing use of biomass for power generation by co-firing in coal-based power plants

- 5.2.2 RESTRAINTS

- 5.2.2.1 Improper supply chain management of biomass

- TABLE 2 CROPS AND THEIR HARVESTING IN INDIA

- 5.2.2.2 Fluctuating and high costs of feedstocks

- TABLE 3 BIOMASS COLLECTION SYSTEMS AND THEIR COSTS IN DIFFERENT COUNTRIES

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 High depletion rate of fossil fuels

- 5.2.3.2 Advancements in biomass power generation techniques

- 5.2.4 CHALLENGES

- 5.2.4.1 Requirement for high initial investments

- 5.2.4.2 Variability in biomass properties

- TABLE 4 PROXIMATE ANALYSIS OF BIOMASS MATERIALS

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.3.1 REVENUE SHIFT AND NEW REVENUE POCKETS FOR BIOMASS POWER GENERATION COMPANIES

- FIGURE 27 REVENUE SHIFT FOR BIOMASS POWER BIOMASS POWER GENERATION COMPANIES

- 5.4 VALUE/SUPPLY CHAIN ANALYSIS

- FIGURE 28 BIOMASS POWER GENERATION MARKET: SUPPLY CHAIN ANALYSIS

- 5.4.1 BIOMASS FEEDSTOCK PROVIDERS

- 5.4.2 BIOMASS TRANSPORTATION PROVIDERS

- 5.4.3 ENGINEERING PROCUREMENT AND CONSTRUCTION (EPC) CONTRACTORS

- 5.4.4 BIOMASS POWER PLANT OWNERS

- TABLE 5 COMPANIES AND THEIR ROLE IN BIOMASS POWER GENERATION ECOSYSTEM

- 5.5 ECOSYSTEM ANALYSIS

- FIGURE 29 BIOMASS POWER GENERATION MARKET MAP

- 5.6 TECHNOLOGY ANALYSIS

- 5.6.1 BIOMASS CO-FIRING

- 5.6.2 PYRO GASIFICATION

- 5.7 PRICING ANALYSIS

- 5.7.1 LEVELIZED COST OF BIOMASS POWER GENERATION, BY TECHNOLOGY

- TABLE 6 LEVELIZED COST OF BIOMASS POWER GENERATION

- 5.8 PATENT ANALYSIS

- 5.8.1 LIST OF MAJOR PATENTS

- TABLE 7 BIOMASS POWER GENERATION MARKET: INNOVATIONS AND PATENT REGISTRATIONS, JUNE 2016-FEBRUARY 2023

- 5.9 TARIFF AND REGULATORY FRAMEWORK

- 5.9.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 8 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 9 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 SOUTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 MIDDLE EAST & AFRICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.9.2 REGULATORY FRAMEWORK

- TABLE 13 BIOMASS POWER GENERATION MARKET: REGULATORY FRAMEWORK, BY REGION

- 5.10 KEY CONFERENCES AND EVENTS, 2023

- TABLE 14 BIOMASS POWER GENERATION MARKET: DETAILED LIST OF CONFERENCES AND EVENTS

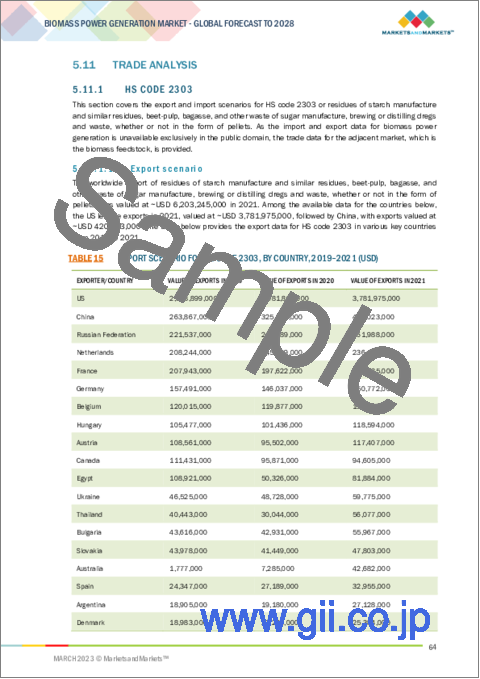

- 5.11 TRADE ANALYSIS

- 5.11.1 HS CODE 2303

- 5.11.1.1 Export scenario

- TABLE 15 EXPORT SCENARIO FOR HS CODE 2303, BY COUNTRY, 2019-2021 (USD)

- FIGURE 30 EXPORT DATA FOR HS CODE 2303 OF TOP FIVE COUNTRIES, 2019-2021 (USD)

- 5.11.1.2 Import scenario

- TABLE 16 IMPORT SCENARIO FOR HS CODE 2303, BY COUNTRY, 2019-2021 (USD)

- FIGURE 31 IMPORT DATA FOR HS CODE 2303 OF TOP FIVE COUNTRIES, 2019-2021 (USD)

- 5.11.2 HS CODE 382510

- 5.11.2.1 Export scenario

- TABLE 17 EXPORT SCENARIO FOR HS CODE: 382510, BY COUNTRY, 2019-2021 (USD)

- FIGURE 32 EXPORT DATA FOR HS CODE 382510 OF TOP FIVE COUNTRIES, 2019-2021 (USD)

- 5.11.2.2 Import scenario

- TABLE 18 IMPORT SCENARIO FOR HS CODE: 382510, BY COUNTRY, 2019-2021 (USD)

- FIGURE 33 IMPORT DATA FOR HS CODE 382510 OF TOP FIVE COUNTRIES, 2019-2021 (USD)

- 5.11.3 HS CODE 382520

- 5.11.3.1 Export scenario

- TABLE 19 EXPORT SCENARIO FOR HS CODE: 382520, BY COUNTRY, 2019-2021 (USD)

- FIGURE 34 EXPORT DATA FOR HS CODE 382520 OF TOP FIVE COUNTRIES, 2019-2021 (USD)

- 5.11.3.2 Import scenario

- TABLE 20 IMPORT SCENARIO FOR HS CODE: 382520, BY COUNTRY, 2019-2021 (USD)

- FIGURE 35 IMPORT DATA FOR HS CODE 382520 OF TOP FIVE COUNTRIES, 2019-2021 (USD)

- 5.11.1 HS CODE 2303

- 5.12 CASE STUDY ANALYSIS

- 5.12.1 DECENTRALIZED ENERGY SYSTEMS OF INDIA (DESI POWER) HELPED COMMUNITIES IN RURAL AREAS HARNESS POWER FOR ECONOMIC PURPOSES

- 5.12.1.1 Problem statement

- 5.12.1.2 Solution

- 5.12.2 VALMET PROVIDED TURNKEY BIOPOWER PLANT TO SALZBURG AG TO GENERATE GREEN ELECTRICITY AND HEAT

- 5.12.2.1 Problem statement

- 5.12.2.2 Solution

- 5.12.1 DECENTRALIZED ENERGY SYSTEMS OF INDIA (DESI POWER) HELPED COMMUNITIES IN RURAL AREAS HARNESS POWER FOR ECONOMIC PURPOSES

- 5.13 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 36 BIOMASS POWER GENERATION MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 21 BIOMASS POWER GENERATION MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.13.1 BARGAINING POWER OF BUYERS

- 5.13.2 BARGAINING POWER OF SUPPLIERS

- 5.13.3 THREAT OF SUBSTITUTES

- 5.13.4 INTENSITY OF COMPETITIVE RIVALRY

- 5.13.5 THREAT OF NEW ENTRANTS

- 5.14 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 37 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY TECHNOLOGY

- TABLE 22 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF TOP TECHNOLOGIES (%)

- 5.14.2 BUYING CRITERIA

- FIGURE 38 KEY BUYING CRITERIA FOR TOP TECHNOLOGY-BASED BIOMASS POWER GENERATION SYSTEMS

- TABLE 23 KEY BUYING CRITERIA, BY TECHNOLOGY

- 5.15 SUPPLY AND DEMAND ANALYSIS OF BIOMASS FEEDSTOCK

6 BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK

- 6.1 INTRODUCTION

- FIGURE 39 FOREST WASTE SEGMENT DOMINATED BIOMASS POWER GENERATION MARKET IN 2022

- TABLE 24 BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 6.2 AGRICULTURAL WASTE

- 6.2.1 GROWING NEED TO MEET ENERGY DEMANDS IN RURAL AREAS

- TABLE 25 AGRICULTURAL WASTE: BIOMASS POWER GENERATION MARKET, BY REGION, 2021-2028 (USD MILLION)

- 6.3 FOREST WASTE

- 6.3.1 RISING DEMAND FOR WOOD BIOMASS

- TABLE 26 FOREST WASTE: BIOMASS POWER GENERATION MARKET, BY REGION, 2021-2028 (USD MILLION)

- 6.4 ANIMAL WASTE

- 6.4.1 GROWING USE OF ANIMAL WASTE TO PRODUCE BIOGAS

- TABLE 27 ANIMAL WASTE: BIOMASS POWER GENERATION MARKET, BY REGION, 2021-2028 (USD MILLION)

- 6.5 MUNICIPAL WASTE

- 6.5.1 STRINGENT GOVERNMENT POLICIES RELATED TO DISPOSAL OF MUNICIPAL WASTE

- TABLE 28 MUNICIPAL WASTE: BIOMASS POWER GENERATION MARKET, BY REGION, 2021-2028 (USD MILLION)

7 BIOMASS POWER GENERATION MARKET, BY TECHNOLOGY

- 7.1 INTRODUCTION

- FIGURE 40 COMBUSTION SEGMENT LED BIOMASS POWER GENERATION MARKET IN 2022

- TABLE 29 BIOMASS POWER GENERATION MARKET, BY TECHNOLOGY, 2021-2028 (TWH)

- TABLE 30 BIOMASS POWER GENERATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- 7.2 COMBUSTION

- 7.2.1 PRESENCE OF FAVORABLE GOVERNMENT POLICIES REGARDING USING BIOMASS BLENDS AND REDUCING COAL USE

- TABLE 31 COMBUSTION: BIOMASS POWER GENERATION MARKET, BY REGION, 2021-2028 (TWH)

- TABLE 32 COMBUSTION: BIOMASS POWER GENERATION MARKET, BY REGION, 2021-2028 (USD MILLION)

- 7.3 GASIFICATION

- 7.3.1 INCREASING NUMBER OF GASIFICATION PROJECTS

- TABLE 33 GASIFICATION: BIOMASS POWER GENERATION MARKET, BY REGION, 2021-2028 (TWH)

- TABLE 34 GASIFICATION: BIOMASS POWER GENERATION MARKET, BY REGION, 2021-2028 (USD MILLION)

- 7.4 ANAEROBIC DIGESTION

- 7.4.1 EXCELLENT PROPERTIES OF ANAEROBIC DIGESTION TECHNOLOGY

- TABLE 35 ANAEROBIC DIGESTION: BIOMASS POWER GENERATION MARKET, BY REGION, 2021-2028 (TWH)

- TABLE 36 ANAEROBIC DIGESTION: BIOMASS POWER GENERATION MARKET, BY REGION, 2021-2028 (USD MILLION)

- 7.5 PYROLYSIS

- 7.5.1 HIGH EFFICIENCY OF PYROLYSIS TECHNOLOGY IN ELECTRICITY GENERATION

- TABLE 37 PYROLYSIS: BIOMASS POWER GENERATION MARKET, BY REGION, 2021-2028 (TWH)

- TABLE 38 PYROLYSIS: BIOMASS POWER GENERATION MARKET, BY REGION, 2021-2028 (USD MILLION)

8 BIOMASS POWER GENERATION MARKET, BY FUEL

- 8.1 INTRODUCTION

- FIGURE 41 SOLID FUEL SEGMENT HELD LARGEST SHARE OF BIOMASS POWER GENERATION MARKET IN 2022

- TABLE 39 BIOMASS POWER GENERATION MARKET, BY FUEL, 2021-2028 (USD MILLION)

- 8.2 SOLID FUEL

- 8.2.1 RISING PREFERENCE FOR WOOD BIOMASS AS SOLID FUEL FOR POWER GENERATION

- TABLE 40 SOLID FUEL: BIOMASS POWER GENERATION MARKET, BY REGION, 2021-2028 (USD MILLION)

- 8.3 LIQUID FUEL

- 8.3.1 ADVANCEMENTS IN TECHNOLOGIES USED TO PRODUCE LIQUID FUEL

- TABLE 41 LIQUID FUEL: BIOMASS POWER GENERATION MARKET, BY REGION, 2021-2028 (USD MILLION)

- 8.4 GASEOUS FUEL

- 8.4.1 PRESENCE OF STRINGENT REGULATIONS RELATED TO LANDFILLS

- TABLE 42 GASEOUS FUEL: BIOMASS POWER GENERATION MARKET, BY REGION, 2021-2028 (USD MILLION)

9 BIOMASS POWER GENERATION MARKET, BY REGION

- 9.1 INTRODUCTION

- FIGURE 42 ASIA PACIFIC HELD LARGEST SHARE OF BIOMASS POWER GENERATION MARKET IN 2022

- FIGURE 43 ASIA PACIFIC BIOMASS POWER GENERATION MARKET TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- TABLE 43 BIOMASS POWER GENERATION MARKET, BY REGION, 2021-2028 (TWH)

- TABLE 44 BIOMASS POWER GENERATION MARKET, BY REGION, 2021-2028 (USD MILLION)

- 9.2 EUROPE

- FIGURE 44 EUROPE: SNAPSHOT OF BIOMASS POWER GENERATION MARKET

- 9.2.1 EUROPE: RECESSION IMPACT

- TABLE 45 EUROPE: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- TABLE 46 EUROPE: BIOMASS POWER GENERATION MARKET, BY FUEL, 2021-2028 (USD MILLION)

- TABLE 47 EUROPE: BIOMASS POWER GENERATION MARKET, BY TECHNOLOGY, 2021-2028 (TWH)

- TABLE 48 EUROPE: BIOMASS POWER GENERATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 49 EUROPE: BIOMASS POWER GENERATION MARKET, BY COUNTRY, 2021-2028 (TWH)

- TABLE 50 EUROPE: BIOMASS POWER GENERATION MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 9.2.2 GERMANY

- 9.2.2.1 Government-led initiatives for energy transition

- TABLE 51 GERMANY: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.2.3 UK

- 9.2.3.1 Advancements in green hydrogen technologies

- TABLE 52 UK: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.2.4 FINLAND

- 9.2.4.1 Increasing renewable electricity generation through forest waste

- TABLE 53 FINLAND: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.2.5 SWEDEN

- 9.2.5.1 Increasing investments in biomass power plants

- TABLE 54 SWEDEN: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.2.6 ITALY

- 9.2.6.1 Government efforts to decarbonize transportation sector

- TABLE 55 ITALY: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.2.7 FRANCE

- 9.2.7.1 Rising use of biofuels for power generation

- TABLE 56 FRANCE: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.2.8 NETHERLANDS

- 9.2.8.1 Government-led incentives for electricity production

- TABLE 57 NETHERLANDS: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.2.9 REST OF EUROPE

- TABLE 58 REST OF EUROPE: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.3 ASIA PACIFIC

- FIGURE 45 ASIA PACIFIC: SNAPSHOT OF BIOMASS POWER GENERATION MARKET

- 9.3.1 ASIA PACIFIC: RECESSION IMPACT

- TABLE 59 ASIA PACIFIC: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- TABLE 60 ASIA PACIFIC: BIOMASS POWER GENERATION MARKET, BY FUEL, 2021-2028 (USD MILLION)

- TABLE 61 ASIA PACIFIC: BIOMASS POWER GENERATION MARKET, BY TECHNOLOGY, 2021-2028 (TWH)

- TABLE 62 ASIA PACIFIC: BIOMASS POWER GENERATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 63 ASIA PACIFIC: BIOMASS POWER GENERATION MARKET, BY COUNTRY, 2021-2028 (TWH)

- TABLE 64 ASIA PACIFIC: BIOMASS POWER GENERATION MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 9.3.2 CHINA

- 9.3.2.1 Rising private investments to decarbonize industrial sector

- TABLE 65 CHINA: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.3.3 JAPAN

- 9.3.3.1 Rising number of waste-to-energy projects

- TABLE 66 JAPAN: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.3.4 INDIA

- 9.3.4.1 Increasing financial assistance from government and rising rural electrification and captive power requirements

- TABLE 67 INDIA: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.3.5 INDONESIA

- 9.3.5.1 Rising investments in setting up waste-to-energy projects

- TABLE 68 INDONESIA: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.3.6 THAILAND

- 9.3.6.1 Increasing foreign investments and ability to transition to clean energy

- TABLE 69 THAILAND: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.3.7 REST OF ASIA PACIFIC

- TABLE 70 REST OF ASIA PACIFIC: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.4 NORTH AMERICA

- 9.4.1 NORTH AMERICA: RECESSION IMPACT

- TABLE 71 NORTH AMERICA: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- TABLE 72 NORTH AMERICA: BIOMASS POWER GENERATION MARKET, BY FUEL, 2021-2028 (USD MILLION)

- TABLE 73 NORTH AMERICA: BIOMASS POWER GENERATION MARKET, BY TECHNOLOGY, 2021-2028 (TWH)

- TABLE 74 NORTH AMERICA: BIOMASS POWER GENERATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 75 NORTH AMERICA: BIOMASS POWER GENERATION MARKET, BY COUNTRY, 2021-2028 (TWH)

- TABLE 76 NORTH AMERICA: BIOMASS POWER GENERATION MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 9.4.2 US

- 9.4.2.1 Increasing in-house electricity production

- TABLE 77 US: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.4.3 CANADA

- 9.4.3.1 Favorable policies promoting installation of power plants

- TABLE 78 CANADA: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.4.4 MEXICO

- 9.4.4.1 Increasing renewable electricity generation using agricultural residue

- TABLE 79 MEXICO: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.5 SOUTH AMERICA

- 9.5.1 SOUTH AMERICA: RECESSION IMPACT

- TABLE 80 SOUTH AMERICA: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- TABLE 81 SOUTH AMERICA: BIOMASS POWER GENERATION MARKET, BY FUEL, 2021-2028 (USD MILLION)

- TABLE 82 SOUTH AMERICA: BIOMASS POWER GENERATION MARKET, BY TECHNOLOGY, 2021-2028 (TWH)

- TABLE 83 SOUTH AMERICA: BIOMASS POWER GENERATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 84 SOUTH AMERICA: BIOMASS POWER GENERATION MARKET, BY COUNTRY, 2021-2028 (TWH)

- TABLE 85 SOUTH AMERICA: BIOMASS POWER GENERATION MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 9.5.2 BRAZIL

- 9.5.2.1 Increasing investments in power plants to decarbonize industrial sector

- TABLE 86 BRAZIL: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.5.3 ARGENTINA

- 9.5.3.1 Growing demand for biofuels

- TABLE 87 ARGENTINA: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.5.4 COLOMBIA

- 9.5.4.1 Increasing investments in waste-to-energy projects to generate green energy

- TABLE 88 COLOMBIA: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.5.5 REST OF SOUTH AMERICA

- TABLE 89 REST OF SOUTH AMERICA: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.6 MIDDLE EAST & AFRICA

- 9.6.1 MIDDLE EAST & AFRICA: RECESSION IMPACT

- TABLE 90 MIDDLE EAST & AFRICA: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- TABLE 91 MIDDLE EAST & AFRICA: BIOMASS POWER GENERATION MARKET, BY FUEL, 2021-2028 (USD MILLION)

- TABLE 92 MIDDLE EAST & AFRICA: BIOMASS POWER GENERATION MARKET, BY TECHNOLOGY, 2021-2028 (TWH)

- TABLE 93 MIDDLE EAST & AFRICA: BIOMASS POWER GENERATION MARKET, BY TECHNOLOGY, 2021-2028 (USD MILLION)

- TABLE 94 MIDDLE EAST & AFRICA: BIOMASS POWER GENERATION MARKET, BY COUNTRY, 2021-2028 (TWH)

- TABLE 95 MIDDLE EAST & AFRICA: BIOMASS POWER GENERATION MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 9.6.2 SOUTH AFRICA

- 9.6.2.1 Rising number of public-private partnerships (PPPs)

- TABLE 96 SOUTH AFRICA: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.6.3 TURKEY

- 9.6.3.1 Increasing use of forest waste to produce sustainable fuel and electricity

- TABLE 97 TURKEY: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.6.4 EGYPT

- 9.6.4.1 Government-led initiatives to increase investments in construction of biomass power plants

- TABLE 98 EGYPT: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.6.5 ISRAEL

- 9.6.5.1 Establishment of new greenhouse gas (GHG) emission target

- TABLE 99 ISRAEL: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

- 9.6.6 REST OF MIDDLE EAST & AFRICA

- TABLE 100 REST OF MIDDLE EAST & AFRICA: BIOMASS POWER GENERATION MARKET, BY FEEDSTOCK, 2021-2028 (USD MILLION)

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- FIGURE 46 KEY DEVELOPMENTS IN BIOMASS POWER GENERATION MARKET, 2018-2022

- 10.2 MARKET SHARE ANALYSIS, 2022

- TABLE 101 BIOMASS POWER GENERATION MARKET: DEGREE OF COMPETITION

- FIGURE 47 INDUSTRY CONCENTRATION OF TOP PLAYERS IN BIOMASS POWER GENERATION MARKET, 2022

- 10.3 MARKET EVALUATION FRAMEWORK, 2018-2021

- TABLE 102 MARKET EVALUATION FRAMEWORK, 2018-2021

- 10.4 SEGMENTAL REVENUE ANALYSIS OF TOP MARKET PLAYERS

- FIGURE 48 SEGMENTAL REVENUE ANALYSIS, 2018-2021

- 10.5 RECENT DEVELOPMENTS

- 10.5.1 DEALS

- TABLE 103 BIOMASS POWER GENERATION: DEALS, 2018-2022

- 10.5.2 OTHERS

- TABLE 104 BIOMASS POWER GENERATION MARKET: OTHERS, 2018-2022

- 10.6 COMPETITIVE LEADERSHIP MAPPING

- 10.6.1 STARS

- 10.6.2 EMERGING LEADERS

- 10.6.3 PERVASIVE PLAYERS

- 10.6.4 PARTICIPANTS

- FIGURE 49 BIOMASS POWER GENERATION MARKET: COMPETITIVE LEADERSHIP MAPPING, 2022

- TABLE 105 FEEDSTOCK: COMPANY FOOTPRINT

- TABLE 106 FUEL: COMPANY FOOTPRINT

- TABLE 107 TECHNOLOGY: COMPANY FOOTPRINT

- TABLE 108 REGION: COMPANY FOOTPRINT

- 10.7 START-UP/SME EVALUATION QUADRANT, 2021

- 10.7.1 PROGRESSIVE COMPANIES

- 10.7.2 RESPONSIVE COMPANIES

- 10.7.3 DYNAMIC COMPANIES

- 10.7.4 STARTING BLOCKS

- FIGURE 50 BIOMASS POWER GENERATION MARKET: START-UP/SME EVALUATION QUADRANT, 2022

- 10.8 COMPETITIVE BENCHMARKING

- TABLE 109 BIOMASS POWER GENERATION MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 110 FEEDSTOCK: COMPANY FOOTPRINT (STARTUPS/SMES)

- TABLE 111 FUEL: COMPANY FOOTPRINT (STARTUPS/SMES)

- TABLE 112 TECHNOLOGY: COMPANY FOOTPRINT (STARTUPS/SMES)

- TABLE 113 REGION: COMPANY FOOTPRINT (STARTUPS/SMES)

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- (Business Overview, Products/Services/Solutions Offered, MnM View, Key Strengths and Right to Win, Strategic Choices Made, Weaknesses and Competitive Threats, Recent Developments)**

- 11.1.1 ENGIE

- TABLE 114 ENGIE: COMPANY OVERVIEW

- FIGURE 51 ENGIE: COMPANY SNAPSHOT

- TABLE 115 ENGIE: DEALS

- 11.1.2 XCEL ENERGY INC.

- TABLE 116 XCEL ENERGY INC.: COMPANY OVERVIEW

- FIGURE 52 XCEL ENERGY INC.: COMPANY SNAPSHOT

- TABLE 117 XCEL ENERGY INC.: DEALS

- 11.1.3 BABCOCK & WILCOX ENTERPRISES, INC.

- TABLE 118 BABCOCK & WILCOX ENTERPRISES, INC.: COMPANY OVERVIEW

- 11.1.4 ØRSTED A/S

- TABLE 119 ØRSTED A/S: COMPANY OVERVIEW

- TABLE 120 ØRSTED A/S: DEALS

- 11.1.5 EPH

- TABLE 121 EPH: COMPANY OVERVIEW

- FIGURE 55 EPH: COMPANY SNAPSHOT

- 11.1.6 RWE

- TABLE 122 RWE: COMPANY OVERVIEW

- 11.1.7 RENOVA INC.

- TABLE 123 RENOVA INC.: COMPANY OVERVIEW

- 11.1.8 VEOLIA ENERGY HUNGARY CO. LTD.

- TABLE 124 VEOLIA ENERGY HUNGARY CO. LTD.: COMPANY OVERVIEW

- 11.1.9 ACCIONA

- TABLE 125 ACCIONA: COMPANY OVERVIEW

- FIGURE 58 ACCIONA: COMPANY SNAPSHOT

- 11.1.10 EDF RENEWABLE ENERGY

- TABLE 126 EDF RENEWABLE ENERGY: COMPANY OVERVIEW

- 11.1.11 DRAX GROUP

- TABLE 127 DRAX GROUP: COMPANY OVERVIEW

- FIGURE 59 DRAX GROUP: COMPANY SNAPSHOT

- 11.1.12 SALZBURG AG

- TABLE 128 SALZBURG AG: COMPANY OVERVIEW

- TABLE 129 SALZBURG AG: DEALS

- 11.1.13 LAHTI ENERGIA OY

- TABLE 130 LAHTI ENERGIA OY: COMPANY OVERVIEW

- 11.1.14 VATTENFALL

- TABLE 131 VATTENFALL: COMPANY OVERVIEW

- 11.1.15 STATKRAFT

- TABLE 132 STATKRAFT: COMPANY OVERVIEW

- TABLE 133 STATKRAFT: DEALS

- *Business Overview, Products/Services/Solutions Offered, MnM View, Key Strengths and Right to Win, Strategic Choices Made, Weaknesses and Competitive Threats, Recent Developments might not be captured in case of unlisted companies.

- 11.2 OTHER PLAYERS

- 11.2.1 GRETA ENERGY LIMITED

- 11.2.2 YONAGO BIOMASS POWER GENERATION LLC

- 11.2.3 BELGIAN ECO ENERGY (BEE)

- 11.2.4 D.E.S.I. POWER

- 11.2.5 ENEXOR ENERGY LLC

12 APPENDIX

- 12.1 INSIGHTS FROM INDUSTRY EXPERTS

- 12.2 DISCUSSION GUIDE

- 12.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.4 CUSTOMIZATION OPTIONS

- 12.5 RELATED REPORTS

- 12.6 AUTHOR DETAILS