|

|

市場調査レポート

商品コード

1248050

ロボットエンドエフェクターの世界市場:種類別 (グリッパー、溶接ガン、ツールチェンジャー、クランプ、吸盤、バリ取り、はんだ付け、フライス、塗装ツール)・ロボットの種類別 (従来型、協働型)・用途別・産業別・地域別の将来予測 (2028年まで)Robot End Effector Market by Type (Grippers, Welding Guns, Tool Changer, Clamps, Suction Cups, Deburring, Soldering, Milling, & Painting Tools), Robot Type (Traditional, Collaborative), Application, Industry & Region - Forecast to 2028 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| ロボットエンドエフェクターの世界市場:種類別 (グリッパー、溶接ガン、ツールチェンジャー、クランプ、吸盤、バリ取り、はんだ付け、フライス、塗装ツール)・ロボットの種類別 (従来型、協働型)・用途別・産業別・地域別の将来予測 (2028年まで) |

|

出版日: 2023年03月21日

発行: MarketsandMarkets

ページ情報: 英文 264 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界のロボットエンドエフェクターの市場規模は、2023年の23億米ドルから、2028年には43億米ドルに達し、13.5%のCAGRで成長する、予測されています。

市場拡大の主な要因としては、モジュール式エンドエフェクターの需要増大、コボット (協働ロボット) の急速な普及、中小企業における自動化の浸透、倉庫・医薬品・食品・飲料などの産業における普及浸透などが挙げられます。

"種類別に見ると、2022年にはグリッパーが最大のシェアを占める"

電動グリッパー・協働グリッパー・ソフトグリッパー・カスタム型グリッパーの人気が高まっているため、種類別ではグリッパーが最大のシェアを占め、今後もその傾向が続く見通しです。グリッパー市場の主な促進要因として、様々な形状・サイズのワークピースに対応したハンドリング用途、FDM (Fused Deposition Modeling) 3Dプリントなどの3Dプリント技術の活用、医療産業における利用拡大、などが挙げられます。さらに、医薬品・食品業界におけるソフトグリッパーやバキュームグリッパーの利用拡大も、グリッパー分野で活動する企業に一定の成長機会をもたらすと考えられます。

"ロボットの種類別に見ると、2022年には従来型産業ロボットが最大のシェアを占める"

従来型産業ロボットは、スピードと正確さを念頭に置いて開発されてきました。一般に、高い可搬重量を持ち、単一のタスクを連続的に実行するようにプログラムされています。自動車、電気・電子、金属・機械などの産業において、従来の産業用ロボットが重作業用として採用されており、これらの産業に大きく依存しているため、産業ロボットの売上は増加しています。

"地域別に見ると、2022年にはアジア太平洋が最大の市場規模を占める"

アジア太平洋の市場成長は、域内各国 (特に中国、韓国、インドなど) で、自動車メーカーや電気・電子機器メーカーによる自動化への投資が進んでいることに起因していると思われます。中国と日本では高齢化が進み、人件費が高騰しているため、自動化の導入が進んでいます。この地域は世界の主要な製造拠点と考えられており、エンドエフェクター市場に十分な成長機会をもたらすと期待されています。

当レポートでは、世界のロボットエンドエフェクターの市場について分析し、市場の基本構造や最新情勢、主な市場促進・抑制要因、種類別・ロボットの種類別・用途別・産業別・地域別の市場動向の見通し、市場競争の状態、主要企業のプロファイルなどを調査しております。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- バリューチェーン分析

- エコシステム分析

- 価格分析

- 顧客のビジネスに影響を与える動向/混乱

- 技術分析

- ポーターのファイブフォース分析

- 主な利害関係者と購入基準

- ケーススタディ

- 貿易分析

- 特許分析

- 主な会議とイベント (2022年~2023年)

- 規制状況

第6章 ロボットエンドエフェクター市場:種類別

- イントロダクション

- 溶接ガン

- グリッパー

- 機械式グリッパー

- 電動式グリッパー

- 磁気式グリッパー

- ツールチェンジャー

- クランプ

- 吸盤

- その他

第7章 ロボットエンドエフェクター市場:ロボットの種類別

- イントロダクション

- 従来型産業ロボット

- 協働型産業ロボット

第8章 ロボットエンドエフェクター市場:用途別

- イントロダクション

- ハンドリング

- 組立

- 溶接

- 調剤

- 処理

- その他

第9章 ロボットエンドエフェクター市場:産業別

- イントロダクション

- 自動車

- 電気・電子機器

- 金属・機械

- プラスチック・ゴム・化学製品

- 食品・飲料

- 精密工学・光学

- 医薬品・化粧品

- eコマース

- その他

第10章 ロボットエンドエフェクター市場:地域別

- イントロダクション

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- 他の欧州諸国

- アジア太平洋

- 中国

- 日本

- 韓国

- インド

- 他のアジア太平洋諸国

- 他の国々 (RoW)

- 中東

- アフリカ

- 南米

第11章 競合情勢

- 概要

- 主要企業が採用した戦略

- 市場シェア分析 (2022年)

- 企業評価クアドラント

- スタートアップ/中小企業の評価マトリックス

- 企業の製品フットプリント分析

- 競合シナリオと動向

- 製品の発売

- 資本取引

- その他

第12章 企業プロファイル

- 主要企業

- SCHUNK

- ZIMMER GROUP

- SCHMALZ

- DESTACO

- FESTO

- ABB

- ATI INDUSTRIAL AUTOMATION

- PIAB AB

- ROBOTIQ

- TUNKERS

- その他の企業

- JH ROBOTICS

- EMI CORP

- SOFT ROBOTICS

- WEISS ROBOTICS

- INTELLIGENT ACTUATOR INC.

- BASTIAN SOLUTIONS

- FIPA

- IPR

- SMC

- RAD

- KUKA

- APPLIED ROBOTICS

- ONROBOT

- MILLIBAR ROBOTICS

- WYZO

第13章 隣接市場

- 産業用ロボット市場

- イントロダクション

- 16.00kg以下

- 16.01~60.00kg

- 60.01~225.00kg

- 225.00kg以上

第14章 付録

The global robot end effector market is expected to grow from USD 2.3 billion in 2023 to USD 4.3 billion by 2028, registering a CAGR of 13.5%. The main drivers for the expansion of the robot end effector market include a rising demand for modular end effectors, a surge in cobot adoption, increasing penetration of automation in small and medium-sized enterprises (SMEs), and growing adoption in industries such as warehousing, pharmaceuticals, and food & beverage.

"Grippers accounted for the largest share of robot end-effector market in 2022"

Grippers accounted for the largest share due to the growing popularity of electric grippers, collaborative grippers, soft grippers, and customized grippers. This trend is expected to continue during the forecast period as well. The market for grippers is largely driven by its handling application in a wide range of workpieces considering their various shapes and size, the use of 3D printing technology such as fused deposition modeling (FDM) 3D printing, and their increasing applications in healthcare industries. Additionally, the increasing application of soft grippers and vacuum grippers in the pharmaceutical & food industry would present several growth opportunities to players operating in the gripper segment.

"Traditional industrial robots accounted for the largest share of robot end-effector market in 2022"

Traditional industrial robots are developed with speed and accuracy in mind. They are generally built to carry high payloads and are programmed to perform a single task continuously. The adoption of traditional industrial robots for heavy-duty applications in the industries such as automotive, electrical & electronics, and metal & machinery has increased the sales of industrial robots as it is largely dependent on these industries.

"Asia Pacific to account for the largest market size in 2022"

The market growth in Asia Pacific can be attributed to the investment in automation by automotive and, electrical & electronics companies, especially in countries such as China, South Korea, and India. The aging population in China and Japan has resulted in rising labor costs, leading to the growing adoption of automation. This region is considered a major manufacturing hub in the world, which is expected to provide ample growth opportunities to the end effector market.

Break-up of the profiles of primary participants:

- By Company Type - Tier 1 - 40%, Tier 2 - 30%, and Tier 3 - 30%

- By Designation - C-level Executives - 40%, Directors - 40%, and Others - 20%

- By Region - North America - 40%, Europe - 30%, Asia Pacific - 25%, and RoW - 10%

The major players in the market are Schunk (Germany), Schmalz (Germany), Zimmer Group (Germany), Tunkers (Germany), and Destaco (US).

Research Coverage:

The robot end-effector market has been segmented into type, robot type, application, industry, and region. The robot end-effector market was studied for North America, Europe, Asia Pacific, and the Rest of the World (RoW). The report describes the major drivers, restraints, challenges, and opportunities pertaining to the robot end-effector market and forecasts the same till 2028. Apart from these, the report also consists of leadership mapping and analysis of all the companies included in the robot end-effector ecosystem.

Key Benefits of Buying the Report:

The report offers valuable insights into the robot end effector market, including precise revenue estimates for the overall market and its subsegments. In addition, the report provides a comprehensive analysis of the market's competitive landscape, key players, and value chain, which can aid market leaders and new entrants in making informed decisions. The report is instrumental in helping stakeholders gain a deeper understanding of the competitive landscape and plan effective go-to-market strategies. Moreover, it provides a detailed overview of the market's pulse, highlighting key drivers, restraints, challenges, and opportunities that stakeholders can leverage to their advantage.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 DEFINITION AND SCOPE

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- FIGURE 1 ROBOT END EFFECTOR MARKET SEGMENTATION

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 ROBOT END EFFECTOR MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Major secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Breakdown of primaries

- 2.1.3 SECONDARY AND PRIMARY RESEARCH

- 2.1.3.1 Key industry insights

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- FIGURE 3 ROBOT END EFFECTOR MARKET: BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- FIGURE 4 APPROACH 2 FOR MARKET SIZE ESTIMATION (SUPPLY SIDE): REVENUE GENERATED FROM PRODUCTS IN ROBOT END EFFECTOR MARKET

- FIGURE 5 ROBOT END EFFECTOR MARKET: TOP-DOWN APPROACH

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 6 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS AND LIMITATIONS

- 2.4.1 RESEARCH ASSUMPTIONS

- FIGURE 7 ASSUMPTIONS OF RESEARCH STUDY

- 2.4.2 LIMITATIONS

- 2.5 APPROACH TO IMPACT ON RECESSION

- 2.6 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- FIGURE 8 GRIPPERS TO ACCOUNT FOR LARGEST SHARE OF ROBOT END EFFECTOR MARKET IN 2023

- FIGURE 9 TRADITIONAL INDUSTRIAL ROBOTS EXPECTED TO ACCOUNT FOR LARGER MARKET SHARE IN 2023

- FIGURE 10 AUTOMOTIVE INDUSTRY ACCOUNTED FOR LARGEST MARKET SHARE IN 2022

- FIGURE 11 ASIA PACIFIC TO EXHIBIT HIGHEST CAGR DURING FORECAST PERIOD

- 3.1 IMPACT ANALYSIS OF RECESSION ON ROBOT END EFFECTOR MARKET

- FIGURE 12 GDP GROWTH PROJECTION TILL 2023 FOR MAJOR ECONOMIES (PERCENTAGE CHANGE)

- FIGURE 13 ROBOT END EFFECTOR MARKET SCENARIO: BEFORE RECESSION AND WITH RECESSION

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE GROWTH OPPORTUNITIES FOR ROBOT END EFFECTOR MARKET PLAYERS

- FIGURE 14 INCREASING ADOPTION OF COLLABORATIVE ROBOTS (COBOTS) EXPECTED TO FUEL MARKET GROWTH

- 4.2 ROBOT END EFFECTOR MARKET, BY ROBOT TYPE

- FIGURE 15 TRADITIONAL INDUSTRIAL ROBOTS TO ACCOUNT FOR LARGEST SHARE DURING FORECAST PERIOD

- 4.3 ROBOT END EFFECTOR MARKET, BY TYPE

- FIGURE 16 GRIPPERS HELD LARGEST SHARE OF ROBOT END EFFECTOR MARKET IN 2022

- 4.4 ROBOT END EFFECTOR MARKET, BY INDUSTRY

- FIGURE 17 AUTOMOTIVE INDUSTRY TO DOMINATE MARKET DURING FORECAST PERIOD

- 4.5 ROBOT END EFFECTOR MARKET, BY COUNTRY

- FIGURE 18 CHINA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 19 ROBOT END EFFECTOR MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing demand for modular end effectors among various industries

- 5.2.1.2 Growing demand for collaborative robots (cobots) across various sectors

- FIGURE 20 IMPACT ANALYSIS OF DRIVERS AND OPPORTUNITIES ON ROBOT END EFFECTOR MARKET

- 5.2.2 RESTRAINTS

- 5.2.2.1 High requirement of deployment costs, especially for SMEs

- FIGURE 21 IMPACT ANALYSIS OF RESTRAINTS AND CHALLENGES ON ROBOT END EFFECTOR MARKET

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Surging demand for soft grippers

- 5.2.3.2 Rising adoption of additive manufacturing across industries

- 5.2.3.3 Growing adoption of electric grippers

- 5.2.4 CHALLENGES

- 5.2.4.1 Interoperability and integration issues related to end effectors with existing facilities

- 5.3 VALUE CHAIN ANALYSIS

- FIGURE 22 VALUE CHAIN ANALYSIS

- 5.3.1 MANUFACTURING

- 5.3.2 ASSEMBLY, DISTRIBUTION, AND AFTER-SALES SERVICE

- 5.4 ECOSYSTEM ANALYSIS

- FIGURE 23 ROBOT END EFFECTOR ECOSYSTEM LINKED WITH INDUSTRIAL ROBOTS

- TABLE 1 LIST OF COMPANIES AND THEIR ROLE IN ROBOT END EFFECTOR ECOSYSTEM

- 5.5 PRICING ANALYSIS

- 5.5.1 ASP ANALYSIS OF KEY PLAYERS

- FIGURE 24 ASP OF GRIPPERS BASED ON PAYLOAD

- TABLE 2 KEY PLAYERS: AVERAGE SELLING PRICE OF GRIPPERS BASED ON PAYLOAD (USD)

- 5.5.2 ASP TREND

- TABLE 3 CONTRIBUTION OF VARIOUS END EFFECTORS TO OVERALL COST OF ROBOTIC SYSTEM

- FIGURE 25 ASP TREND FOR VARIOUS ROBOT END EFFECTORS

- 5.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 26 REVENUE SHIFT IN ROBOT END EFFECTOR MARKET

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 KEY TECHNOLOGIES

- 5.7.1.1 Use of 3D printing technology for EOAT manufacturing

- 5.7.1.2 Increase in demand for HRC end effectors

- 5.7.1.3 Development of combination grippers

- 5.7.1.4 Launch of bionic grippers

- 5.7.1.5 Increase in demand for soft and flexible grippers

- 5.7.2 COMPLEMENTARY TECHNOLOGIES

- 5.7.2.1 Integration of Industrial Internet of Things (IIoT) and AI to design systems aligned with Industry 4.0

- 5.7.2.2 Smart and intelligent grippers

- 5.7.3 ADJACENT TECHNOLOGIES

- 5.7.3.1 Grippers in research and conceptual phases

- 5.7.3.2 Innovative components

- 5.7.1 KEY TECHNOLOGIES

- 5.8 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 27 PORTER'S FIVE FORCES ANALYSIS

- TABLE 4 ROBOT END EFFECTOR MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.8.1 THREAT OF NEW ENTRANTS

- 5.8.2 THREAT OF SUBSTITUTES

- 5.8.3 BARGAINING POWER OF BUYERS

- 5.8.4 BARGAINING POWER OF SUPPLIERS

- 5.8.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.9 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.9.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 28 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END-USE INDUSTRIES

- TABLE 5 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END-USE INDUSTRIES (%)

- 5.9.2 BUYING CRITERIA

- FIGURE 29 KEY BUYING CRITERIA FOR TOP THREE END-USE INDUSTRIES

- TABLE 6 KEY BUYING CRITERIA FOR TOP THREE END-USE INDUSTRIES

- 5.10 CASE STUDIES

- 5.10.1 CANADIAN BAKERY BOULANGERIE LA FABRIQUE AUTOMATES USING MGRIP WITH REVTECH SYSTEMS' ROBOTIC PACKAGING SOLUTION

- 5.10.2 SENNHEISER INCREASED NUMBER OF QUALITY TESTS BY 33% WITH ROBOTIQ 2F-85 AND INSIGHTS

- 5.10.3 SAPHO INCREASED PRODUCTION PACE WITH PIAB'S BAG GRIPPERS

- 5.11 TRADE ANALYSIS

- 5.11.1 IMPORT SCENARIO

- FIGURE 30 IMPORT DATA, BY COUNTRY, 2017-2021 (USD MILLION)

- 5.11.2 EXPORT SCENARIO

- FIGURE 31 EXPORT DATA, BY COUNTRY, 2017-2021 (USD MILLION)

- 5.12 PATENT ANALYSIS

- FIGURE 32 TOP 10 COMPANIES WITH HIGHEST NO. OF PATENT APPLICATIONS DURING 2013-2022

- FIGURE 33 NO. OF PATENTS GRANTED PER YEAR OVER LAST 10 YEARS

- TABLE 7 PATENTS FILED FOR VARIOUS TYPES OF ROBOT END EFFECTORS, 2020-2022

- 5.13 KEY CONFERENCES AND EVENTS, 2022-2023

- TABLE 8 ROBOT END EFFECTOR MARKET: CONFERENCES AND EVENTS

- 5.14 REGULATORY LANDSCAPE

- 5.14.1 REGULATIONS

- FIGURE 34 ISO VS ANSI/RIA STANDARDS

- TABLE 9 ISO AND ANSI STANDARDS FOR INDUSTRIAL ROBOTS, END EFFECTORS, AND COBOTS

- 5.14.1.1 North America

- 5.14.1.1.1 US

- 5.14.1.1.2 Canada

- 5.14.1.1 North America

- 5.14.2 STANDARDS

- 5.14.2.1 ISO standards and key regulatory bodies worldwide (excluding North America)

- 5.14.2.2 ISO standards for handling using robots (ISO 14539)

- FIGURE 35 ILLUSTRATION OF VARIOUS STATES AND ACTIONS INVOLVED IN HANDLING APPLICATION

6 ROBOT END EFFECTOR MARKET, BY TYPE

- 6.1 INTRODUCTION

- FIGURE 36 GRIPPERS TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 10 ROBOT END EFFECTOR MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 11 ROBOT END EFFECTOR MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 6.2 WELDING GUNS

- 6.2.1 WELDING GUNS TO ACCOUNT FOR SECOND-LARGEST SHARE OF MARKET DURING FORECAST PERIOD

- TABLE 12 PLAYERS MANUFACTURING ROBOTIC WELDING GUNS

- TABLE 13 WELDING GUNS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- FIGURE 37 WELDING GUNS: COLLABORATIVE INDUSTRIAL ROBOTS TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- TABLE 14 WELDING GUNS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- 6.3 GRIPPERS

- TABLE 15 GRIPPERS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

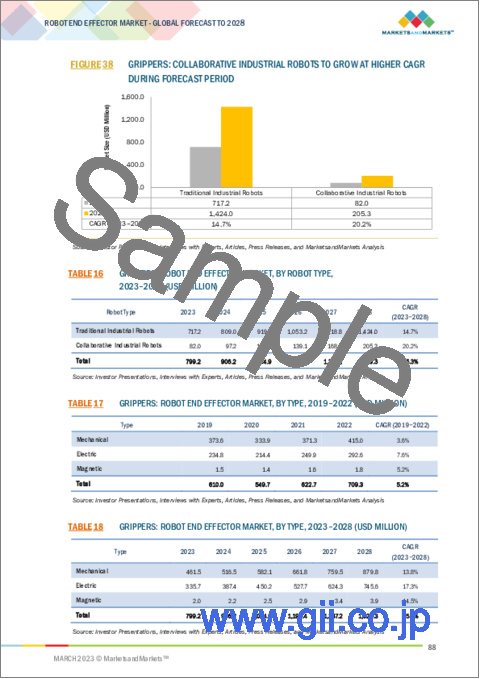

- FIGURE 38 GRIPPERS: COLLABORATIVE INDUSTRIAL ROBOTS TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- TABLE 16 GRIPPERS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- TABLE 17 GRIPPERS: ROBOT END EFFECTOR MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 18 GRIPPERS: ROBOT END EFFECTOR MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 6.3.1 MECHANICAL GRIPPERS

- 6.3.1.1 Mechanical grippers offer advantages such as simplicity and low operating cost

- TABLE 19 PLAYERS MANUFACTURING MECHANICAL GRIPPERS

- 6.3.2 ELECTRIC GRIPPERS

- 6.3.2.1 Electric grippers preferred in applications that require high operational speed

- TABLE 20 PLAYERS MANUFACTURING ELECTRIC GRIPPERS

- TABLE 21 PLAYERS MANUFACTURING DEXTEROUS ROBOTIC HANDS

- 6.3.3 MAGNETIC GRIPPERS

- 6.3.3.1 Magnetic grippers widely used in gripping objects with holes or nets

- TABLE 22 PLAYERS MANUFACTURING MAGNETIC GRIPPERS

- TABLE 23 COMPARISON BETWEEN MECHANICAL, ELECTRIC, AND MAGNETIC GRIPPERS

- 6.4 TOOL CHANGERS

- 6.4.1 TOOL CHANGERS CREATE STRUCTURED INTERFACE BETWEEN ROBOT FLANGE AND TOOL BASE

- TABLE 24 PLAYERS MANUFACTURING TOOL CHANGERS

- TABLE 25 TOOL CHANGERS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- FIGURE 39 TOOL CHANGERS: TRADITIONAL INDUSTRIAL ROBOTS TO ACCOUNT FOR LARGEST SHARE

- TABLE 26 TOOL CHANGERS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- 6.5 CLAMPS

- 6.5.1 CLAMPS USED TO POSITION AND HOLD PRODUCTS WITH LOW GRIP FORCE

- TABLE 27 PLAYERS MANUFACTURING CLAMPS

- TABLE 28 CLAMPS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- TABLE 29 CLAMPS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- 6.6 SUCTION CUPS

- 6.6.1 VACUUM CLAMPS USED FOR VARIOUS MACHINING AND ASSEMBLY OPERATIONS

- TABLE 30 PLAYERS MANUFACTURING VACUUM TECHNOLOGY

- TABLE 31 SUCTION CUPS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- TABLE 32 SUCTION CUPS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- 6.7 OTHERS

- TABLE 33 PLAYERS MANUFACTURING DEBURRING TOOLS

- TABLE 34 PLAYERS MANUFACTURING MILLING TOOLS

- TABLE 35 PLAYERS MANUFACTURING SOLDERING TOOLS

- TABLE 36 PLAYERS MANUFACTURING PAINTING TOOLS

- TABLE 37 PLAYERS MANUFACTURING DISPENSING TOOLS

- TABLE 38 OTHERS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- TABLE 39 OTHERS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

7 ROBOT END EFFECTOR MARKET, BY ROBOT TYPE

- 7.1 INTRODUCTION

- FIGURE 40 COLLABORATIVE INDUSTRIAL ROBOTS MARKET TO GROW AT HIGHER CAGR

- TABLE 40 ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- TABLE 41 ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- 7.2 TRADITIONAL INDUSTRIAL ROBOTS

- 7.2.1 TRADITIONAL INDUSTRIAL ROBOTS SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- TABLE 42 TRADITIONAL INDUSTRIAL ROBOTS: ROBOT END EFFECTOR MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 43 TRADITIONAL INDUSTRIAL ROBOTS: ROBOT END EFFECTOR MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 44 TRADITIONAL INDUSTRIAL ROBOTS: ROBOT END EFFECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 45 TRADITIONAL INDUSTRIAL ROBOTS: ROBOT END EFFECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 7.3 COLLABORATIVE INDUSTRIAL ROBOTS

- 7.3.1 COLLABORATIVE INDUSTRIAL ROBOTS TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 41 GRIPPERS TO DOMINATE COLLABORATIVE INDUSTRIAL ROBOT END EFFECTOR MARKET DURING FORECAST PERIOD

- TABLE 46 COLLABORATIVE INDUSTRIAL ROBOTS: ROBOT END EFFECTOR MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 47 COLLABORATIVE INDUSTRIAL ROBOTS: ROBOT END EFFECTOR MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 48 COLLABORATIVE INDUSTRIAL ROBOTS: ROBOT END EFFECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 49 COLLABORATIVE INDUSTRIAL ROBOTS: ROBOT END EFFECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

8 ROBOT END EFFECTOR MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- FIGURE 42 ROBOT END EFFECTORS HAVE SUBSTANTIAL APPLICATIONS IN HANDLING OPERATIONS

- 8.2 HANDLING

- 8.2.1 USE OF ROBOT END EFFECTORS IN MATERIAL HANDLING IMPROVES SPEED AND PRECISION

- 8.3 ASSEMBLY

- 8.3.1 AUTOMATION TO IMPROVE SPEED AND ACCURACY ACROSS ASSEMBLY LINES

- 8.4 WELDING

- 8.4.1 ROBOT END EFFECTORS USED EXCLUSIVELY IN SPOT AND ARC WELDING

- 8.5 DISPENSING

- 8.5.1 AUTOMOTIVE AND ELECTRONICS INDUSTRIES REQUIRE HIGHLY PRECISE ADHESIVE DISPENSERS

- 8.6 PROCESSING

- 8.6.1 GRINDING AND POLISHING TO IMPROVE CONSISTENCY OF FINISHED PRODUCTS

- 8.7 OTHERS

9 ROBOT END EFFECTOR MARKET, BY INDUSTRY

- 9.1 INTRODUCTION

- FIGURE 43 AUTOMOTIVE INDUSTRY TO ACCOUNT FOR LARGEST MARKET SHARE IN 2023

- TABLE 50 ROBOT END EFFECTOR MARKET, BY INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 51 ROBOT END EFFECTOR MARKET, BY INDUSTRY, 2023-2028 (USD MILLION)

- 9.2 AUTOMOTIVE

- 9.2.1 SUBSTANTIAL USE OF ROBOT END EFFECTORS IN MANUFACTURING AND ASSEMBLY STAGES

- TABLE 52 AUTOMOTIVE: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- TABLE 53 AUTOMOTIVE: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- TABLE 54 AUTOMOTIVE: ROBOT END EFFECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- FIGURE 44 AUTOMOTIVE: EUROPE TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- TABLE 55 AUTOMOTIVE: ROBOT END EFFECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.3 ELECTRICAL & ELECTRONICS

- 9.3.1 ROBOT END EFFECTORS MAINLY USED IN HANDLING AND ASSEMBLY

- TABLE 56 ELECTRICAL & ELECTRONICS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- TABLE 57 ELECTRICAL & ELECTRONICS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- TABLE 58 ELECTRICAL & ELECTRONICS: ROBOT END EFFECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 59 ELECTRICAL & ELECTRONICS: ROBOT END EFFECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.4 METALS & MACHINERY

- 9.4.1 ROBOT END EFFECTORS TO ACHIEVE COST-EFFECTIVE PRODUCTION OF MACHINING METAL COMPONENTS

- TABLE 60 METALS & MACHINERY: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- TABLE 61 METALS & MACHINERY: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- TABLE 62 METALS & MACHINERY: ROBOT END EFFECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- FIGURE 45 METALS & MACHINERY: ASIA PACIFIC TO HOLD LARGEST MARKET SHARE IN 2023

- TABLE 63 METALS & MACHINERY: ROBOT END EFFECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.5 PLASTIC, RUBBER, & CHEMICAL

- 9.5.1 MULTITASKING END EFFECTORS TO FIND SIGNIFICANT USE IN PLASTIC AND RUBBER INDUSTRIES

- TABLE 64 PLASTIC, RUBBER, & CHEMICAL: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- TABLE 65 PLASTIC, RUBBER, & CHEMICAL: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- TABLE 66 PLASTIC, RUBBER, & CHEMICAL: ROBOT END EFFECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 67 PLASTIC, RUBBER, & CHEMICAL: ROBOT END EFFECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.6 FOOD & BEVERAGE

- 9.6.1 SOFT GRIPPERS MAJORLY USED IN FOOD & BEVERAGE INDUSTRY DUE TO HIGH DEGREE OF SANITATION

- TABLE 68 FOOD & BEVERAGE: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- TABLE 69 FOOD & BEVERAGE: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- TABLE 70 FOOD & BEVERAGE: ROBOT END EFFECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- FIGURE 46 FOOD & BEVERAGE: ASIA PACIFIC EXPECTED TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 71 FOOD & BEVERAGE: ROBOT END EFFECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.7 PRECISION ENGINEERING & OPTICS

- 9.7.1 ROBOT END EFFECTORS USED FOR ERROR PROOFING AND VALIDATION

- TABLE 72 PRECISION ENGINEERING & OPTICS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- TABLE 73 PRECISION ENGINEERING & OPTICS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- TABLE 74 PRECISION ENGINEERING & OPTICS: ROBOT END EFFECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 75 PRECISION ENGINEERING & OPTICS: ROBOT END EFFECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.8 PHARMACEUTICAL & COSMETICS

- 9.8.1 ROBOT END EFFECTORS MAINLY USED IN PACKAGING AND SORTING IN PHARMACEUTICAL & COSMETICS INDUSTRIES

- TABLE 76 PHARMACEUTICAL & COSMETICS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- TABLE 77 PHARMACEUTICAL & COSMETICS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- TABLE 78 PHARMACEUTICAL & COSMETICS: ROBOT END EFFECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- FIGURE 47 PHARMACEUTICAL & COSMETICS: ASIA PACIFIC TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 79 PHARMACEUTICAL & COSMETICS: ROBOT END EFFECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.9 E-COMMERCE

- 9.9.1 VACUUM GRIPPERS, PALLETIZERS, AND LARGE CLAMPS SIGNIFICANTLY USED IN WAREHOUSES

- TABLE 80 E-COMMERCE: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- TABLE 81 E-COMMERCE: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- TABLE 82 E-COMMERCE: ROBOT END EFFECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 83 E-COMMERCE: ROBOT END EFFECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 9.10 OTHERS

- TABLE 84 OTHERS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- TABLE 85 OTHERS: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- TABLE 86 OTHERS: ROBOT END EFFECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 87 OTHERS: ROBOT END EFFECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

10 ROBOT END EFFECTOR MARKET, BY REGION

- 10.1 INTRODUCTION

- FIGURE 48 CHINA TO REGISTER HIGHEST GROWTH RATE DURING FORECAST PERIOD

- TABLE 88 ROBOT END EFFECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 89 ROBOT END EFFECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 10.2 NORTH AMERICA

- FIGURE 49 NORTH AMERICA: SNAPSHOT OF ROBOT END EFFECTOR MARKET

- TABLE 90 NORTH AMERICA: ROBOT END EFFECTOR MARKET, BY INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 91 NORTH AMERICA: ROBOT END EFFECTOR MARKET, BY INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 92 NORTH AMERICA: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- TABLE 93 NORTH AMERICA: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- TABLE 94 NORTH AMERICA: ROBOT END EFFECTOR MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 95 NORTH AMERICA: ROBOT END EFFECTOR MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 10.2.1 US

- 10.2.1.1 US to account for largest market share in North America

- 10.2.2 CANADA

- 10.2.2.1 Increased foreign investments in manufacturing sector to drive market

- 10.2.3 MEXICO

- 10.2.3.1 Increasing deployment of industrial robots in automotive industry to foster market growth

- 10.3 EUROPE

- FIGURE 50 EUROPE: SNAPSHOT OF ROBOT END EFFECTOR MARKET

- TABLE 96 EUROPE: ROBOT END EFFECTOR MARKET, BY INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 97 EUROPE: ROBOT END EFFECTOR MARKET, BY INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 98 EUROPE: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- TABLE 99 EUROPE: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- TABLE 100 EUROPE: ROBOT END EFFECTOR MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 101 EUROPE: ROBOT END EFFECTOR MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 10.3.1 UK

- 10.3.1.1 Strong manufacturing industry to boost demand for robot end effectors

- 10.3.2 GERMANY

- 10.3.2.1 Automotive industry to significantly contribute to market growth

- 10.3.3 FRANCE

- 10.3.3.1 Government funding to boost automation and demand for robots

- 10.3.4 REST OF EUROPE

- 10.4 ASIA PACIFIC

- FIGURE 51 ASIA PACIFIC: SNAPSHOT OF ROBOT END EFFECTOR MARKET

- TABLE 102 ASIA PACIFIC: ROBOT END EFFECTOR MARKET, BY INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 103 ASIA PACIFIC: ROBOT END EFFECTOR MARKET, BY INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 104 ASIA PACIFIC: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- TABLE 105 ASIA PACIFIC: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- TABLE 106 ASIA PACIFIC: ROBOT END EFFECTOR MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 107 ASIA PACIFIC: ROBOT END EFFECTOR MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 10.4.1 CHINA

- 10.4.1.1 High-tech manufacturing industries to foster market growth

- 10.4.2 JAPAN

- 10.4.2.1 Growing production of electric vehicles to drive market

- 10.4.3 SOUTH KOREA

- 10.4.3.1 Rise in industrial robots deployed in automotive & electronics industries to drive market

- 10.4.4 INDIA

- 10.4.4.1 Flourishing automotive and electronic industries to boost demand for robot end effectors

- 10.4.5 REST OF ASIA PACIFIC

- 10.5 ROW

- TABLE 108 ROW: ROBOT END EFFECTOR MARKET, BY INDUSTRY, 2019-2022 (USD MILLION)

- TABLE 109 ROW: ROBOT END EFFECTOR MARKET, BY INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 110 ROW: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2019-2022 (USD MILLION)

- TABLE 111 ROW: ROBOT END EFFECTOR MARKET, BY ROBOT TYPE, 2023-2028 (USD MILLION)

- TABLE 112 ROW: ROBOT END EFFECTOR MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 113 ROW: ROBOT END EFFECTOR MARKET, BY REGION, 2023-2028 (USD MILLION)

- 10.5.1 MIDDLE EAST

- 10.5.1.1 Growing adoption of automation in several manufacturing industries to strengthen market

- 10.5.2 AFRICA

- 10.5.2.1 Growing FDI to support market growth

- 10.5.3 SOUTH AMERICA

- 10.5.3.1 Rapid urbanization and increasing focus on manufacturing to boost market

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 STRATEGIES ADOPTED BY KEY PLAYERS

- TABLE 114 OVERVIEW OF STRATEGIES DEPLOYED BY ROBOT END EFFECTOR COMPANIES

- 11.3 MARKET SHARE ANALYSIS, 2022

- FIGURE 52 SHARE OF MAJOR PLAYERS IN ROBOT END EFFECTOR MARKET, 2022

- TABLE 115 DEGREE OF COMPETITION: ROBOT END EFFECTOR MARKET, 2022

- 11.4 COMPANY EVALUATION QUADRANT

- 11.4.1 STARS

- 11.4.2 EMERGING LEADERS

- 11.4.3 PERVASIVE PLAYERS

- 11.4.4 PARTICIPANTS

- FIGURE 53 ROBOT END EFFECTOR MARKET: COMPANY EVALUATION QUADRANT, 2022

- 11.5 STARTUP/SME EVALUATION MATRIX

- 11.5.1 PROGRESSIVE COMPANIES

- 11.5.2 RESPONSIVE COMPANIES

- 11.5.3 DYNAMIC COMPANIES

- 11.5.4 STARTING BLOCKS

- FIGURE 54 ROBOT END EFFECTOR MARKET: STARTUP/SME EVALUATION MATRIX, 2020

- 11.6 PRODUCT FOOTPRINT ANALYSIS OF COMPANIES

- TABLE 116 PRODUCT FOOTPRINT OF COMPANIES

- TABLE 117 END EFFECTOR TYPE FOOTPRINT OF COMPANIES

- TABLE 118 INDUSTRY FOOTPRINT OF COMPANIES (36 COMPANIES)

- TABLE 119 REGIONAL FOOTPRINT OF COMPANIES (36 COMPANIES)

- 11.7 COMPETITIVE SCENARIO AND TRENDS

- 11.7.1 PRODUCT LAUNCHES

- TABLE 120 PRODUCT LAUNCHES, 2020-2022

- 11.7.2 DEALS

- TABLE 121 DEALS, 2020-2022

- 11.7.3 OTHERS

- TABLE 122 EXPANSIONS, 2020-2022

12 COMPANY PROFILES

(Business overview, Products/Solutions/Services offered, Recent Developments, MNM view)*

- 12.1 KEY PLAYERS

- 12.1.1 SCHUNK

- TABLE 123 SCHUNK: BUSINESS OVERVIEW

- TABLE 124 SCHUNK: PRODUCTS OFFERED

- TABLE 125 SCHUNK: PRODUCT LAUNCHES

- TABLE 126 SCHUNK: DEALS

- TABLE 127 SCHUNK: OTHERS

- 12.1.2 ZIMMER GROUP

- TABLE 128 ZIMMER GROUP: BUSINESS OVERVIEW

- TABLE 129 ZIMMER GROUP: PRODUCTS OFFERED

- TABLE 130 ZIMMER GROUP: PRODUCT LAUNCHES

- TABLE 131 ZIMMER GROUP: DEALS

- 12.1.3 SCHMALZ

- TABLE 132 SCHMALZ: BUSINESS OVERVIEW

- TABLE 133 SCHMALZ: PRODUCTS OFFERED

- TABLE 134 SCHMALZ: PRODUCT LAUNCHES

- TABLE 135 SCHMALZ: DEALS

- TABLE 136 SCHMALZ: OTHERS

- 12.1.4 DESTACO

- TABLE 137 DESTACO: BUSINESS OVERVIEW

- TABLE 138 DESTACO: PRODUCTS OFFERED

- TABLE 139 DESTACO: PRODUCT LAUNCHES

- 12.1.5 FESTO

- TABLE 140 FESTO: BUSINESS OVERVIEW

- TABLE 141 FESTO: PRODUCTS OFFERED

- TABLE 142 FESTO: PRODUCT LAUNCHES

- TABLE 143 FESTO: DEALS

- 12.1.6 ABB

- TABLE 144 ABB: BUSINESS OVERVIEW

- FIGURE 55 ABB: COMPANY SNAPSHOT

- TABLE 145 ABB: PRODUCTS OFFERED

- TABLE 146 ABB: PRODUCT LAUNCHES

- TABLE 147 ABB: DEALS

- 12.1.7 ATI INDUSTRIAL AUTOMATION

- TABLE 148 ATI INDUSTRIAL AUTOMATION: BUSINESS OVERVIEW

- TABLE 149 ATI INDUSTRIAL AUTOMATION: PRODUCTS OFFERED

- TABLE 150 ATI INDUSTRIAL AUTOMATION: PRODUCT LAUNCHES

- TABLE 151 ATI INDUSTRIAL AUTOMATION: DEALS

- 12.1.8 PIAB AB

- TABLE 152 PIAB AB: BUSINESS OVERVIEW

- TABLE 153 PIAB AB: PRODUCTS OFFERED

- TABLE 154 PIAB AB: PRODUCT LAUNCHES

- TABLE 155 PIAB AB: DEALS

- 12.1.9 ROBOTIQ

- TABLE 156 ROBOTIQ: BUSINESS OVERVIEW

- TABLE 157 ROBOTIQ: PRODUCTS OFFERED

- TABLE 158 ROBOTIQ: PRODUCT LAUNCHES

- TABLE 159 ROBOTIQ: DEALS

- TABLE 160 ROBOTIQ: OTHERS

- 12.1.10 TUNKERS

- TABLE 161 TUNKERS: BUSINESS OVERVIEW

- FIGURE 56 TUNKERS: COMPANY SNAPSHOT

- TABLE 162 TUNKERS: PRODUCTS OFFERED

- TABLE 163 TUNKERS: PRODUCT LAUNCHES

- TABLE 164 TUNKERS: DEALS

- 12.2 OTHER KEY PLAYERS

- 12.2.1 JH ROBOTICS

- TABLE 165 JH ROBOTICS: COMPANY OVERVIEW

- 12.2.2 EMI CORP

- TABLE 166 EMI CORP: COMPANY OVERVIEW

- 12.2.3 SOFT ROBOTICS

- TABLE 167 SOFT ROBOTICS: COMPANY OVERVIEW

- 12.2.4 WEISS ROBOTICS

- TABLE 168 WEISS ROBOTICS: COMPANY OVERVIEW

- 12.2.5 INTELLIGENT ACTUATOR INC.

- TABLE 169 IAI: COMPANY OVERVIEW

- 12.2.6 BASTIAN SOLUTIONS

- TABLE 170 BASTIAN SOLUTIONS: COMPANY OVERVIEW

- 12.2.7 FIPA

- TABLE 171 FIPA: COMPANY OVERVIEW

- 12.2.8 IPR

- TABLE 172 IPR: COMPANY OVERVIEW

- 12.2.9 SMC

- TABLE 173 SMC: COMPANY OVERVIEW

- 12.2.10 RAD

- TABLE 174 RAD: COMPANY OVERVIEW

- 12.2.11 KUKA

- TABLE 175 KUKA: COMPANY OVERVIEW

- 12.2.12 APPLIED ROBOTICS

- TABLE 176 APPLIED ROBOTICS: COMPANY OVERVIEW

- 12.2.13 ONROBOT

- TABLE 177 ONROBOT: COMPANY OVERVIEW

- 12.2.14 MILLIBAR ROBOTICS

- TABLE 178 MILLIBAR ROBOTICS: BUSINESS OVERVIEW

- 12.2.15 WYZO

- TABLE 179 WYZO: COMPANY OVERVIEW

- Details on Business overview, Products/Solutions/Services offered, Recent Developments, MNM view might not be captured in case of unlisted companies.

13 ADJACENT MARKET

- 13.1 INDUSTRIAL ROBOTICS MARKET

- 13.2 INTRODUCTION

- FIGURE 57 INDUSTRIAL ROBOTS WITH PAYLOAD RANGE OF 16.01 KG-60.00 KG TO WITNESS HIGHEST GROWTH RATE DURING FORECAST PERIOD

- TABLE 180 INDUSTRIAL ROBOTICS MARKET, BY PAYLOAD, 2018-2021 (USD MILLION)

- TABLE 181 INDUSTRIAL ROBOTICS MARKET, BY PAYLOAD, 2022-2027 (USD MILLION)

- TABLE 182 INDUSTRIAL ROBOTICS MARKET, BY PAYLOAD, 2018-2021 (THOUSAND UNITS)

- TABLE 183 INDUSTRIAL ROBOTICS MARKET, BY PAYLOAD, 2022-2027 (THOUSAND UNITS)

- 13.3 UP TO 16.00 KG

- 13.3.1 ROBOTS WITH PAYLOAD UP TO 16.00 KG TO HOLD LARGEST MARKET SHARE IN 2022

- TABLE 184 TYPES OF INDUSTRIAL ROBOTS WITH UP TO 16.00 KG PAYLOAD CAPACITY

- 13.4 16.01-60.00 KG

- 13.4.1 FASTEST GROWTH RATE EXPECTED DURING FORECAST PERIOD

- TABLE 185 TYPES OF INDUSTRIAL ROBOTS WITH 16.01-60.00 KG PAYLOAD CAPACITY

- 13.5 60.01-225.00 KG

- 13.5.1 AUTOMOTIVE AND FOOD & BEVERAGES INDUSTRIES TO DRIVE MARKET

- TABLE 186 TYPES OF INDUSTRIAL ROBOTS WITH 60.01-225.00 KG PAYLOAD CAPACITY

- 13.6 MORE THAN 225.00 KG

- 13.6.1 INCREASING ADOPTION ACROSS INDUSTRIES EXPECTED TO DRIVE MARKET

- TABLE 187 TYPES OF INDUSTRIAL ROBOTS WITH MORE THAN 225.00 KG PAYLOAD CAPACITY

14 APPENDIX

- 14.1 INSIGHTS FROM INDUSTRY EXPERTS

- 14.2 DISCUSSION GUIDE

- 14.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.4 CUSTOMIZATION OPTIONS

- 14.5 RELATED REPORTS

- 14.6 AUTHOR DETAILS