|

|

市場調査レポート

商品コード

1261567

ロボットエンドエフェクターの世界市場規模、シェア、産業動向分析レポートタイプ別(グリッパー、溶接ガン、ツールチェンジャー、クランプ、サクションカップ、その他)、業界別、ロボットタイプ別、用途別、地域別展望と予測、2022-2028年Global Robot End Effector Market Size, Share & Industry Trends Analysis Report By Type (Grippers, Welding Guns, Tool Changers, Clamps, Suction Cups, and Others), By Vertical, By Robot Type, By Application, By Regional Outlook and Forecast, 2022 - 2028 |

||||||

|

|

|||||||

| ロボットエンドエフェクターの世界市場規模、シェア、産業動向分析レポートタイプ別(グリッパー、溶接ガン、ツールチェンジャー、クランプ、サクションカップ、その他)、業界別、ロボットタイプ別、用途別、地域別展望と予測、2022-2028年 |

|

出版日: 2023年03月31日

発行: KBV Research

ページ情報: 英文 335 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

ロボットエンドエフェクター市場規模は、2028年には42億米ドルに達し、予測期間中にCAGR12.6%の市場成長率で上昇すると予測されています。

例えば、調整可能なロボットアームは、作業場の特定の場所にセットすることができますが、エンドエフェクターがなければ、操作を実行することができません。協働ロボットの使用は、ロボットエンドエフェクター市場を推進する主な要因です。これらのロボットは、周囲の環境と関わり、適切に反応します。作業環境の変化に応じて、行動や操作の方向性を調整するのです。また、より迅速に作業を完了するために、さまざまな分野で自動化が進んでいることも、ロボットエンドエフェクターの需要を高めています。

COVID-19の影響度分析

COVID-19のパンデミックは、建築、ホテル、工業、観光の各分野に大きな影響を与えました。その結果、多くの国で生産が停止したり、深刻な制約を受けたりしました。また、建設業や運輸業などのサプライチェーンにも支障をきたし、世界の大流行となりました。その結果、ロボット用エンドエフェクターの生産量と需要が減少し、市場の拡大が抑制されました。また、パンデミック時には、自動車産業の操業が制約されました。ロボット用エンドエフェクターの主要な最終顧客は、自動車メーカーです。したがって、この業界の減少は、ロボット型エンドエフェクターの市場に影響を与えました。

市場成長要因

多くの産業でロボットエンドエフェクターの導入が進む

自動化、AI・ML、IIoTなどの新技術により、ロボットの使用事例が大きく広がり、近年、ロボットの需要は大幅に増加しています。また、ロボットビジネスは技術開発の影響を受けており、独創的で手頃な価格のロボットを作ることができるようになっています。ロボティクスへの投資は、商業、住宅、工業の各エンドユーザー部門におけるデジタル技術の導入が進んでいることが、さらに後押ししています。また、「インダストリー4.0」や「スマートシティ」のような政府の支援政策やプログラムにより、ロボットやエンドエフェクターの市場開拓に有利な市場環境が整いつつあります。したがって、予測期間中、ロボット用エンドエフェクターの需要は増加し、市場の成長が促進されると予想されます。

自動化および作業効率向上のための需要拡大

ロボットのエンドエフェクターは、機械の生産性を向上させながら、労働生産性を効果的に高めることができます。製造工程を自動化することで、生産がスピードアップし、作業者の生産性が向上します。その結果、1時間当たりの生産量が増加します。近年、世界の先進国では人件費が高騰しているため、労働生産性の向上はビジネスに大きなプラスの影響を与えます。また、以前は人間が行っていた単調な仕事のほとんどが機械に取って代わられ、ロボットの利用が求められています。ロボット技術は、人手不足の影響も同時に軽減することができます。

市場の抑制要因

特に中小企業にとっては高い導入・維持コスト

産業用ロボットやオートメーションへの投資は、まだ法外に高価です。ロボットのエンドエフェクターを設置するための費用が、商業的な制約になっています。企業は新規投資への支出が少ないです。自動車や他の主要部門に比べて資本が少ないのです。ガラス研磨事業者のように、作業の自動化を求められる中小企業は現在ほとんどないです。さらに、ロボットのエンドエフェクターは、修理やメンテナンスに費用がかかる重厚な分野で使用される場合、損傷に対して極めて脆弱です。これらすべての要因が、市場の成長を大きく妨げています。

タイプの展望

ロボットエンドエフェクター市場は、タイプ別に、溶接ガン、グリッパー、ツールチェンジャー、クランプ、吸引カップ、その他に分類されます。2021年のロボットエンドエフェクター市場では、グリッパーセグメントが最も高い収益シェアを獲得しています。ロボットにすぐに追加できる把持ツールには、エンドエフェクターやエリアグラッピングシステムがあります。これらは、特に梱包を伴う作業に適しています。多様なワークの形状や大きさを考慮したハンドリング利用が、グリッパーセグメントの大きな推進力となっています。

ロボットタイプの展望

ロボットタイプに基づいて、ロボットエンドエフェクター市場は、従来型産業用ロボットと協働型産業用ロボットに分けられます。2021年のロボットエンドエフェクター市場では、従来型産業用ロボット分野が最大の収益シェアを記録しました。従来の産業用ロボットは、産業環境における自動化操作に実装するために、固定または移動ベースに取り付けることができる3軸以上の自動制御、再プログラム可能な多目的マニピュレータです。

アプリケーションの展望

用途に基づき、ロボットエンドエフェクター市場はハンドリング、溶接、アセンブリ、加工、ディスペンシング、その他に区分されます。2021年のロボットエンドエフェクター市場では、組立部門が顕著な成長率を調達しました。組立ロボットは、人間の労働力よりも迅速かつ正確に高度な反復作業を行うため、このセグメントの拡大を支えています。組立・分解工程でロボットを使用することで、人間は労働災害のリスクのない他の作業に従事することができます。ワークセルには、ロボット組立システムによる1つまたは複数の組立作業を収容することができます。ロボットはビジョンシステムを使って、複雑なピックアンドプレース作業や品質管理を行うことができます。

業界別展望

ロボットエンドエフェクター市場は、業種別では、自動車、電気・電子、金属・機械、プラスチック・ゴム・化学、食品・飲料、精密工学・光学、医薬品・化粧品、eコマース、その他に分類されます。2021年のロボットエンドエフェクター市場では、電気・電子分野がかなりの収益シェアを示しています。ロボットは、人間にとって危険な作業を行うことができます。ロボットは、電気・電子産業における高電圧機器や危険物を扱うことができ、作業員の損傷や死亡の危険性を低減することができます。自動化されたロボットは、生産サイクル全体の実質的にどの時点でも使用することができ、今日のエレクトロニクスの製造において大きな可能性を持っています。

地域別展望

地域別に見ると、ロボットエンドエフェクター市場は、北米、欧州、アジア太平洋、LAMEAで分析されています。アジア太平洋地域は、2021年にロボットエンドエフェクター市場で最大の収益シェアを獲得しました。最小限の生産コスト、手頃な労働力の容易な入手、緩い排気ガスと安全基準、外国直接投資に対する政府の介入により、この地域のロボットエンドエフェクター市場は過去10年間でより急速に成長しました。また、この地域は自動車産業や半導体産業も盛んで、ロボットエンドエフェクターが多く使用されています。

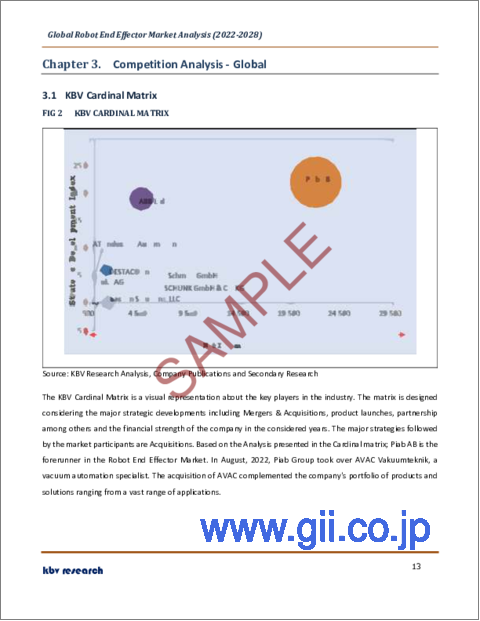

市場参入企業がとる主な戦略は買収です。カーディナルマトリックスで示された分析によると、Piab ABはロボットエンドエフェクター市場の先駆者です。ABB Ltd.、DESTACO, Inc.、Kuka AGなどの企業は、ロボットエンドエフェクター市場における主要な革新的企業の一部です。

目次

第1章 市場範囲と調査手法

- 市場の定義

- 目的

- 市場範囲

- セグメンテーション

- 世界のロボットエンドエフェクター市場:タイプ別

- 世界のロボットエンドエフェクター市場:業界別

- 世界のロボットエンドエフェクター市場:ロボットタイプ別

- 世界のロボットエンドエフェクター市場:用途別

- 世界のロボットエンドエフェクター市場:地域別

- 調査手法

第2章 市場概要

- イントロダクション

- 概要

- 市場構成とシナリオ

- 概要

- 市場に影響を与える主な要因

- 市場促進要因

- 市場抑制要因

第3章 競合分析- 世界

- KBVカーディナルマトリックス

- 最近の業界全体の戦略的展開

- パートナーシップ、コラボレーション、および契約

- 製品の発売と製品の拡大

- 買収と合併

- 地理的拡大

- 主要成功戦略

- 主要なリーディングストラテジー

- 主要な戦略的動き

第4章 世界のロボットエンドエフェクター市場:タイプ別

- 世界グリッパー市場:地域別

- 世界の溶接ガン市場:地域別

- 世界ツールチェンジャー市場:地域別

- 世界クランプ市場:地域別

- 世界の吸盤市場:地域別

- 世界のその他の市場:地域別

第5章 世界のロボットエンドエフェクター市場:業界別

- 世界の自動車市場:地域別

- 世界の金属および機械市場:地域別

- 世界の飲食品市場:地域別

- 世界の電気・電子市場:地域別

- 世界のプラスチック、ゴム、化学市場:地域別

- 世界の精密工学および光学市場:地域別

- 世界の医薬品および化粧品市場:地域別

- 世界のeコマース市場:地域別

- 世界なその他の垂直市場:地域別

第6章 世界のロボットエンドエフェクター市場:ロボットの種類別

- 世界の伝統的な産業用ロボット市場:地域別

- 世界の協働型産業用ロボット市場:地域別

第7章 世界のロボットエンドエフェクター市場:用途別

- 世界ハンドリング市場:地域別

- 世界の溶接市場:地域別

- 世界の組立市場:地域別

- 世界の加工市場:地域別

- 世界の調剤市場:地域別

- 世界のその他の市場:地域別

第8章 世界のロボットエンドエフェクター市場:地域別

- 北米

- 北米の市場:国別

- 米国

- カナダ

- メキシコ

- その他北米地域

- 北米の市場:国別

- 欧州

- 欧州の市場:国別

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- イタリア

- その他欧州地域

- 欧州の市場:国別

- アジア太平洋

- アジア太平洋の市場:国別

- 中国

- 日本

- インド

- 韓国

- シンガポール

- マレーシア

- その他アジア太平洋地域

- アジア太平洋の市場:国別

- ラテンアメリカ・中東・アフリカ

- ラテンアメリカ・中東・アフリカの市場:国別

- ブラジル

- アルゼンチン

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- ナイジェリア

- その他ラテンアメリカ・中東・アフリカ地域

- ラテンアメリカ・中東・アフリカの市場:国別

第9章 企業プロファイル

- ABB Ltd

- Piab AB(Patricia Industries)(Investor AB)

- DESTACO, Inc(Dover Corporation)

- ATI Industrial Automation, Inc(Novanta, Inc.)

- Kuka AG(Midea Investment Holding Co, Ltd.)

- Bastian Solutions, LLC(Toyota Advanced Logistics Group)(Toyota Industries Corporation)

- SCHUNK GmbH & Co KG

- J Schmalz GmbH

- Zimmer Group

- Robotiq, Inc

LIST OF TABLES

- TABLE 1 Global Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 2 Global Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 3 Partnerships, Collaborations and Agreements- Robot End Effector Market

- TABLE 4 Product Launches And Product Expansions- Robot End Effector Market

- TABLE 5 Acquisition and Mergers- Robot End Effector Market

- TABLE 6 Geographical expansions - Robot End Effector Market

- TABLE 7 Global Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 8 Global Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 9 Global Grippers Market by Region, 2018 - 2021, USD Million

- TABLE 10 Global Grippers Market by Region, 2022 - 2028, USD Million

- TABLE 11 Global Welding Guns Market by Region, 2018 - 2021, USD Million

- TABLE 12 Global Welding Guns Market by Region, 2022 - 2028, USD Million

- TABLE 13 Global Tool Changers Market by Region, 2018 - 2021, USD Million

- TABLE 14 Global Tool Changers Market by Region, 2022 - 2028, USD Million

- TABLE 15 Global Clamps Market by Region, 2018 - 2021, USD Million

- TABLE 16 Global Clamps Market by Region, 2022 - 2028, USD Million

- TABLE 17 Global Suction Cups Market by Region, 2018 - 2021, USD Million

- TABLE 18 Global Suction Cups Market by Region, 2022 - 2028, USD Million

- TABLE 19 Global Others Market by Region, 2018 - 2021, USD Million

- TABLE 20 Global Others Market by Region, 2022 - 2028, USD Million

- TABLE 21 Global Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 22 Global Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 23 Global Automotive Market by Region, 2018 - 2021, USD Million

- TABLE 24 Global Automotive Market by Region, 2022 - 2028, USD Million

- TABLE 25 Global Metal & Machinery Market by Region, 2018 - 2021, USD Million

- TABLE 26 Global Metal & Machinery Market by Region, 2022 - 2028, USD Million

- TABLE 27 Global Food & Beverage Market by Region, 2018 - 2021, USD Million

- TABLE 28 Global Food & Beverage Market by Region, 2022 - 2028, USD Million

- TABLE 29 Global Electrical & Electronics Market by Region, 2018 - 2021, USD Million

- TABLE 30 Global Electrical & Electronics Market by Region, 2022 - 2028, USD Million

- TABLE 31 Global Plastic, Rubber, & Chemical Market by Region, 2018 - 2021, USD Million

- TABLE 32 Global Plastic, Rubber, & Chemical Market by Region, 2022 - 2028, USD Million

- TABLE 33 Global Precision Engineering & Optics Market by Region, 2018 - 2021, USD Million

- TABLE 34 Global Precision Engineering & Optics Market by Region, 2022 - 2028, USD Million

- TABLE 35 Global Pharmaceutical & Cosmetics Market by Region, 2018 - 2021, USD Million

- TABLE 36 Global Pharmaceutical & Cosmetics Market by Region, 2022 - 2028, USD Million

- TABLE 37 Global E-Commerce Market by Region, 2018 - 2021, USD Million

- TABLE 38 Global E-Commerce Market by Region, 2022 - 2028, USD Million

- TABLE 39 Global Other Vertical Market by Region, 2018 - 2021, USD Million

- TABLE 40 Global Other Vertical Market by Region, 2022 - 2028, USD Million

- TABLE 41 Global Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 42 Global Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 43 Global Traditional Industrial Robots Market by Region, 2018 - 2021, USD Million

- TABLE 44 Global Traditional Industrial Robots Market by Region, 2022 - 2028, USD Million

- TABLE 45 Global Collaborative Industrial Robots Market by Region, 2018 - 2021, USD Million

- TABLE 46 Global Collaborative Industrial Robots Market by Region, 2022 - 2028, USD Million

- TABLE 47 Global Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 48 Global Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 49 Global Handling Market by Region, 2018 - 2021, USD Million

- TABLE 50 Global Handling Market by Region, 2022 - 2028, USD Million

- TABLE 51 Global Welding Market by Region, 2018 - 2021, USD Million

- TABLE 52 Global Welding Market by Region, 2022 - 2028, USD Million

- TABLE 53 Global Assembly Market by Region, 2018 - 2021, USD Million

- TABLE 54 Global Assembly Market by Region, 2022 - 2028, USD Million

- TABLE 55 Global Processing Market by Region, 2018 - 2021, USD Million

- TABLE 56 Global Processing Market by Region, 2022 - 2028, USD Million

- TABLE 57 Global Dispensing Market by Region, 2018 - 2021, USD Million

- TABLE 58 Global Dispensing Market by Region, 2022 - 2028, USD Million

- TABLE 59 Global Others Market by Region, 2018 - 2021, USD Million

- TABLE 60 Global Others Market by Region, 2022 - 2028, USD Million

- TABLE 61 Global Robot End Effector Market by Region, 2018 - 2021, USD Million

- TABLE 62 Global Robot End Effector Market by Region, 2022 - 2028, USD Million

- TABLE 63 North America Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 64 North America Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 65 North America Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 66 North America Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 67 North America Grippers Market by Country, 2018 - 2021, USD Million

- TABLE 68 North America Grippers Market by Country, 2022 - 2028, USD Million

- TABLE 69 North America Welding Guns Market by Country, 2018 - 2021, USD Million

- TABLE 70 North America Welding Guns Market by Country, 2022 - 2028, USD Million

- TABLE 71 North America Tool Changers Market by Country, 2018 - 2021, USD Million

- TABLE 72 North America Tool Changers Market by Country, 2022 - 2028, USD Million

- TABLE 73 North America Clamps Market by Country, 2018 - 2021, USD Million

- TABLE 74 North America Clamps Market by Country, 2022 - 2028, USD Million

- TABLE 75 North America Suction Cups Market by Country, 2018 - 2021, USD Million

- TABLE 76 North America Suction Cups Market by Country, 2022 - 2028, USD Million

- TABLE 77 North America Others Market by Country, 2018 - 2021, USD Million

- TABLE 78 North America Others Market by Country, 2022 - 2028, USD Million

- TABLE 79 North America Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 80 North America Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 81 North America Automotive Market by Country, 2018 - 2021, USD Million

- TABLE 82 North America Automotive Market by Country, 2022 - 2028, USD Million

- TABLE 83 North America Metal & Machinery Market by Country, 2018 - 2021, USD Million

- TABLE 84 North America Metal & Machinery Market by Country, 2022 - 2028, USD Million

- TABLE 85 North America Food & Beverage Market by Country, 2018 - 2021, USD Million

- TABLE 86 North America Food & Beverage Market by Country, 2022 - 2028, USD Million

- TABLE 87 North America Electrical & Electronics Market by Country, 2018 - 2021, USD Million

- TABLE 88 North America Electrical & Electronics Market by Country, 2022 - 2028, USD Million

- TABLE 89 North America Plastic, Rubber, & Chemical Market by Country, 2018 - 2021, USD Million

- TABLE 90 North America Plastic, Rubber, & Chemical Market by Country, 2022 - 2028, USD Million

- TABLE 91 North America Precision Engineering & Optics Market by Country, 2018 - 2021, USD Million

- TABLE 92 North America Precision Engineering & Optics Market by Country, 2022 - 2028, USD Million

- TABLE 93 North America Pharmaceutical & Cosmetics Market by Country, 2018 - 2021, USD Million

- TABLE 94 North America Pharmaceutical & Cosmetics Market by Country, 2022 - 2028, USD Million

- TABLE 95 North America E-Commerce Market by Country, 2018 - 2021, USD Million

- TABLE 96 North America E-Commerce Market by Country, 2022 - 2028, USD Million

- TABLE 97 North America Other Vertical Market by Country, 2018 - 2021, USD Million

- TABLE 98 North America Other Vertical Market by Country, 2022 - 2028, USD Million

- TABLE 99 North America Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 100 North America Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 101 North America Traditional Industrial Robots Market by Country, 2018 - 2021, USD Million

- TABLE 102 North America Traditional Industrial Robots Market by Country, 2022 - 2028, USD Million

- TABLE 103 North America Collaborative Industrial Robots Market by Country, 2018 - 2021, USD Million

- TABLE 104 North America Collaborative Industrial Robots Market by Country, 2022 - 2028, USD Million

- TABLE 105 North America Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 106 North America Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 107 North America Handling Market by Country, 2018 - 2021, USD Million

- TABLE 108 North America Handling Market by Country, 2022 - 2028, USD Million

- TABLE 109 North America Welding Market by Country, 2018 - 2021, USD Million

- TABLE 110 North America Welding Market by Country, 2022 - 2028, USD Million

- TABLE 111 North America Assembly Market by Country, 2018 - 2021, USD Million

- TABLE 112 North America Assembly Market by Country, 2022 - 2028, USD Million

- TABLE 113 North America Processing Market by Country, 2018 - 2021, USD Million

- TABLE 114 North America Processing Market by Country, 2022 - 2028, USD Million

- TABLE 115 North America Dispensing Market by Country, 2018 - 2021, USD Million

- TABLE 116 North America Dispensing Market by Country, 2022 - 2028, USD Million

- TABLE 117 North America Others Market by Country, 2018 - 2021, USD Million

- TABLE 118 North America Others Market by Country, 2022 - 2028, USD Million

- TABLE 119 North America Robot End Effector Market by Country, 2018 - 2021, USD Million

- TABLE 120 North America Robot End Effector Market by Country, 2022 - 2028, USD Million

- TABLE 121 US Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 122 US Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 123 US Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 124 US Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 125 US Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 126 US Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 127 US Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 128 US Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 129 US Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 130 US Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 131 Canada Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 132 Canada Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 133 Canada Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 134 Canada Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 135 Canada Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 136 Canada Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 137 Canada Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 138 Canada Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 139 Canada Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 140 Canada Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 141 Mexico Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 142 Mexico Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 143 Mexico Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 144 Mexico Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 145 Mexico Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 146 Mexico Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 147 Mexico Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 148 Mexico Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 149 Mexico Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 150 Mexico Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 151 Rest of North America Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 152 Rest of North America Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 153 Rest of North America Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 154 Rest of North America Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 155 Rest of North America Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 156 Rest of North America Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 157 Rest of North America Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 158 Rest of North America Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 159 Rest of North America Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 160 Rest of North America Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 161 Europe Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 162 Europe Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 163 Europe Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 164 Europe Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 165 Europe Grippers Market by Country, 2018 - 2021, USD Million

- TABLE 166 Europe Grippers Market by Country, 2022 - 2028, USD Million

- TABLE 167 Europe Welding Guns Market by Country, 2018 - 2021, USD Million

- TABLE 168 Europe Welding Guns Market by Country, 2022 - 2028, USD Million

- TABLE 169 Europe Tool Changers Market by Country, 2018 - 2021, USD Million

- TABLE 170 Europe Tool Changers Market by Country, 2022 - 2028, USD Million

- TABLE 171 Europe Clamps Market by Country, 2018 - 2021, USD Million

- TABLE 172 Europe Clamps Market by Country, 2022 - 2028, USD Million

- TABLE 173 Europe Suction Cups Market by Country, 2018 - 2021, USD Million

- TABLE 174 Europe Suction Cups Market by Country, 2022 - 2028, USD Million

- TABLE 175 Europe Others Market by Country, 2018 - 2021, USD Million

- TABLE 176 Europe Others Market by Country, 2022 - 2028, USD Million

- TABLE 177 Europe Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 178 Europe Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 179 Europe Automotive Market by Country, 2018 - 2021, USD Million

- TABLE 180 Europe Automotive Market by Country, 2022 - 2028, USD Million

- TABLE 181 Europe Metal & Machinery Market by Country, 2018 - 2021, USD Million

- TABLE 182 Europe Metal & Machinery Market by Country, 2022 - 2028, USD Million

- TABLE 183 Europe Food & Beverage Market by Country, 2018 - 2021, USD Million

- TABLE 184 Europe Food & Beverage Market by Country, 2022 - 2028, USD Million

- TABLE 185 Europe Electrical & Electronics Market by Country, 2018 - 2021, USD Million

- TABLE 186 Europe Electrical & Electronics Market by Country, 2022 - 2028, USD Million

- TABLE 187 Europe Plastic, Rubber, & Chemical Market by Country, 2018 - 2021, USD Million

- TABLE 188 Europe Plastic, Rubber, & Chemical Market by Country, 2022 - 2028, USD Million

- TABLE 189 Europe Precision Engineering & Optics Market by Country, 2018 - 2021, USD Million

- TABLE 190 Europe Precision Engineering & Optics Market by Country, 2022 - 2028, USD Million

- TABLE 191 Europe Pharmaceutical & Cosmetics Market by Country, 2018 - 2021, USD Million

- TABLE 192 Europe Pharmaceutical & Cosmetics Market by Country, 2022 - 2028, USD Million

- TABLE 193 Europe E-Commerce Market by Country, 2018 - 2021, USD Million

- TABLE 194 Europe E-Commerce Market by Country, 2022 - 2028, USD Million

- TABLE 195 Europe Other Vertical Market by Country, 2018 - 2021, USD Million

- TABLE 196 Europe Other Vertical Market by Country, 2022 - 2028, USD Million

- TABLE 197 Europe Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 198 Europe Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 199 Europe Traditional Industrial Robots Market by Country, 2018 - 2021, USD Million

- TABLE 200 Europe Traditional Industrial Robots Market by Country, 2022 - 2028, USD Million

- TABLE 201 Europe Collaborative Industrial Robots Market by Country, 2018 - 2021, USD Million

- TABLE 202 Europe Collaborative Industrial Robots Market by Country, 2022 - 2028, USD Million

- TABLE 203 Europe Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 204 Europe Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 205 Europe Handling Market by Country, 2018 - 2021, USD Million

- TABLE 206 Europe Handling Market by Country, 2022 - 2028, USD Million

- TABLE 207 Europe Welding Market by Country, 2018 - 2021, USD Million

- TABLE 208 Europe Welding Market by Country, 2022 - 2028, USD Million

- TABLE 209 Europe Assembly Market by Country, 2018 - 2021, USD Million

- TABLE 210 Europe Assembly Market by Country, 2022 - 2028, USD Million

- TABLE 211 Europe Processing Market by Country, 2018 - 2021, USD Million

- TABLE 212 Europe Processing Market by Country, 2022 - 2028, USD Million

- TABLE 213 Europe Dispensing Market by Country, 2018 - 2021, USD Million

- TABLE 214 Europe Dispensing Market by Country, 2022 - 2028, USD Million

- TABLE 215 Europe Others Market by Country, 2018 - 2021, USD Million

- TABLE 216 Europe Others Market by Country, 2022 - 2028, USD Million

- TABLE 217 Europe Robot End Effector Market by Country, 2018 - 2021, USD Million

- TABLE 218 Europe Robot End Effector Market by Country, 2022 - 2028, USD Million

- TABLE 219 Germany Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 220 Germany Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 221 Germany Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 222 Germany Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 223 Germany Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 224 Germany Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 225 Germany Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 226 Germany Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 227 Germany Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 228 Germany Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 229 UK Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 230 UK Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 231 UK Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 232 UK Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 233 UK Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 234 UK Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 235 UK Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 236 UK Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 237 UK Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 238 UK Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 239 France Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 240 France Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 241 France Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 242 France Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 243 France Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 244 France Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 245 France Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 246 France Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 247 France Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 248 France Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 249 Russia Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 250 Russia Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 251 Russia Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 252 Russia Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 253 Russia Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 254 Russia Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 255 Russia Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 256 Russia Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 257 Russia Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 258 Russia Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 259 Spain Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 260 Spain Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 261 Spain Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 262 Spain Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 263 Spain Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 264 Spain Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 265 Spain Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 266 Spain Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 267 Spain Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 268 Spain Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 269 Italy Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 270 Italy Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 271 Italy Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 272 Italy Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 273 Italy Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 274 Italy Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 275 Italy Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 276 Italy Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 277 Italy Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 278 Italy Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 279 Rest of Europe Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 280 Rest of Europe Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 281 Rest of Europe Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 282 Rest of Europe Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 283 Rest of Europe Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 284 Rest of Europe Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 285 Rest of Europe Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 286 Rest of Europe Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 287 Rest of Europe Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 288 Rest of Europe Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 289 Asia Pacific Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 290 Asia Pacific Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 291 Asia Pacific Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 292 Asia Pacific Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 293 Asia Pacific Grippers Market by Country, 2018 - 2021, USD Million

- TABLE 294 Asia Pacific Grippers Market by Country, 2022 - 2028, USD Million

- TABLE 295 Asia Pacific Welding Guns Market by Country, 2018 - 2021, USD Million

- TABLE 296 Asia Pacific Welding Guns Market by Country, 2022 - 2028, USD Million

- TABLE 297 Asia Pacific Tool Changers Market by Country, 2018 - 2021, USD Million

- TABLE 298 Asia Pacific Tool Changers Market by Country, 2022 - 2028, USD Million

- TABLE 299 Asia Pacific Clamps Market by Country, 2018 - 2021, USD Million

- TABLE 300 Asia Pacific Clamps Market by Country, 2022 - 2028, USD Million

- TABLE 301 Asia Pacific Suction Cups Market by Country, 2018 - 2021, USD Million

- TABLE 302 Asia Pacific Suction Cups Market by Country, 2022 - 2028, USD Million

- TABLE 303 Asia Pacific Others Market by Country, 2018 - 2021, USD Million

- TABLE 304 Asia Pacific Others Market by Country, 2022 - 2028, USD Million

- TABLE 305 Asia Pacific Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 306 Asia Pacific Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 307 Asia Pacific Automotive Market by Country, 2018 - 2021, USD Million

- TABLE 308 Asia Pacific Automotive Market by Country, 2022 - 2028, USD Million

- TABLE 309 Asia Pacific Metal & Machinery Market by Country, 2018 - 2021, USD Million

- TABLE 310 Asia Pacific Metal & Machinery Market by Country, 2022 - 2028, USD Million

- TABLE 311 Asia Pacific Food & Beverage Market by Country, 2018 - 2021, USD Million

- TABLE 312 Asia Pacific Food & Beverage Market by Country, 2022 - 2028, USD Million

- TABLE 313 Asia Pacific Electrical & Electronics Market by Country, 2018 - 2021, USD Million

- TABLE 314 Asia Pacific Electrical & Electronics Market by Country, 2022 - 2028, USD Million

- TABLE 315 Asia Pacific Plastic, Rubber, & Chemical Market by Country, 2018 - 2021, USD Million

- TABLE 316 Asia Pacific Plastic, Rubber, & Chemical Market by Country, 2022 - 2028, USD Million

- TABLE 317 Asia Pacific Precision Engineering & Optics Market by Country, 2018 - 2021, USD Million

- TABLE 318 Asia Pacific Precision Engineering & Optics Market by Country, 2022 - 2028, USD Million

- TABLE 319 Asia Pacific Pharmaceutical & Cosmetics Market by Country, 2018 - 2021, USD Million

- TABLE 320 Asia Pacific Pharmaceutical & Cosmetics Market by Country, 2022 - 2028, USD Million

- TABLE 321 Asia Pacific E-Commerce Market by Country, 2018 - 2021, USD Million

- TABLE 322 Asia Pacific E-Commerce Market by Country, 2022 - 2028, USD Million

- TABLE 323 Asia Pacific Other Vertical Market by Country, 2018 - 2021, USD Million

- TABLE 324 Asia Pacific Other Vertical Market by Country, 2022 - 2028, USD Million

- TABLE 325 Asia Pacific Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 326 Asia Pacific Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 327 Asia Pacific Traditional Industrial Robots Market by Country, 2018 - 2021, USD Million

- TABLE 328 Asia Pacific Traditional Industrial Robots Market by Country, 2022 - 2028, USD Million

- TABLE 329 Asia Pacific Collaborative Industrial Robots Market by Country, 2018 - 2021, USD Million

- TABLE 330 Asia Pacific Collaborative Industrial Robots Market by Country, 2022 - 2028, USD Million

- TABLE 331 Asia Pacific Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 332 Asia Pacific Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 333 Asia Pacific Handling Market by Country, 2018 - 2021, USD Million

- TABLE 334 Asia Pacific Handling Market by Country, 2022 - 2028, USD Million

- TABLE 335 Asia Pacific Welding Market by Country, 2018 - 2021, USD Million

- TABLE 336 Asia Pacific Welding Market by Country, 2022 - 2028, USD Million

- TABLE 337 Asia Pacific Assembly Market by Country, 2018 - 2021, USD Million

- TABLE 338 Asia Pacific Assembly Market by Country, 2022 - 2028, USD Million

- TABLE 339 Asia Pacific Processing Market by Country, 2018 - 2021, USD Million

- TABLE 340 Asia Pacific Processing Market by Country, 2022 - 2028, USD Million

- TABLE 341 Asia Pacific Dispensing Market by Country, 2018 - 2021, USD Million

- TABLE 342 Asia Pacific Dispensing Market by Country, 2022 - 2028, USD Million

- TABLE 343 Asia Pacific Others Market by Country, 2018 - 2021, USD Million

- TABLE 344 Asia Pacific Others Market by Country, 2022 - 2028, USD Million

- TABLE 345 Asia Pacific Robot End Effector Market by Country, 2018 - 2021, USD Million

- TABLE 346 Asia Pacific Robot End Effector Market by Country, 2022 - 2028, USD Million

- TABLE 347 China Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 348 China Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 349 China Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 350 China Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 351 China Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 352 China Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 353 China Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 354 China Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 355 China Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 356 China Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 357 Japan Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 358 Japan Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 359 Japan Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 360 Japan Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 361 Japan Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 362 Japan Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 363 Japan Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 364 Japan Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 365 Japan Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 366 Japan Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 367 India Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 368 India Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 369 India Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 370 India Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 371 India Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 372 India Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 373 India Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 374 India Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 375 India Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 376 India Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 377 South Korea Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 378 South Korea Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 379 South Korea Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 380 South Korea Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 381 South Korea Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 382 South Korea Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 383 South Korea Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 384 South Korea Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 385 South Korea Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 386 South Korea Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 387 Singapore Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 388 Singapore Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 389 Singapore Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 390 Singapore Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 391 Singapore Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 392 Singapore Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 393 Singapore Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 394 Singapore Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 395 Singapore Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 396 Singapore Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 397 Malaysia Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 398 Malaysia Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 399 Malaysia Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 400 Malaysia Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 401 Malaysia Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 402 Malaysia Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 403 Malaysia Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 404 Malaysia Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 405 Malaysia Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 406 Malaysia Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 407 Rest of Asia Pacific Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 408 Rest of Asia Pacific Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 409 Rest of Asia Pacific Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 410 Rest of Asia Pacific Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 411 Rest of Asia Pacific Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 412 Rest of Asia Pacific Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 413 Rest of Asia Pacific Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 414 Rest of Asia Pacific Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 415 Rest of Asia Pacific Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 416 Rest of Asia Pacific Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 417 LAMEA Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 418 LAMEA Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 419 LAMEA Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 420 LAMEA Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 421 LAMEA Grippers Market by Country, 2018 - 2021, USD Million

- TABLE 422 LAMEA Grippers Market by Country, 2022 - 2028, USD Million

- TABLE 423 LAMEA Welding Guns Market by Country, 2018 - 2021, USD Million

- TABLE 424 LAMEA Welding Guns Market by Country, 2022 - 2028, USD Million

- TABLE 425 LAMEA Tool Changers Market by Country, 2018 - 2021, USD Million

- TABLE 426 LAMEA Tool Changers Market by Country, 2022 - 2028, USD Million

- TABLE 427 LAMEA Clamps Market by Country, 2018 - 2021, USD Million

- TABLE 428 LAMEA Clamps Market by Country, 2022 - 2028, USD Million

- TABLE 429 LAMEA Suction Cups Market by Country, 2018 - 2021, USD Million

- TABLE 430 LAMEA Suction Cups Market by Country, 2022 - 2028, USD Million

- TABLE 431 LAMEA Others Market by Country, 2018 - 2021, USD Million

- TABLE 432 LAMEA Others Market by Country, 2022 - 2028, USD Million

- TABLE 433 LAMEA Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 434 LAMEA Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 435 LAMEA Automotive Market by Country, 2018 - 2021, USD Million

- TABLE 436 LAMEA Automotive Market by Country, 2022 - 2028, USD Million

- TABLE 437 LAMEA Metal & Machinery Market by Country, 2018 - 2021, USD Million

- TABLE 438 LAMEA Metal & Machinery Market by Country, 2022 - 2028, USD Million

- TABLE 439 LAMEA Food & Beverage Market by Country, 2018 - 2021, USD Million

- TABLE 440 LAMEA Food & Beverage Market by Country, 2022 - 2028, USD Million

- TABLE 441 LAMEA Electrical & Electronics Market by Country, 2018 - 2021, USD Million

- TABLE 442 LAMEA Electrical & Electronics Market by Country, 2022 - 2028, USD Million

- TABLE 443 LAMEA Plastic, Rubber, & Chemical Market by Country, 2018 - 2021, USD Million

- TABLE 444 LAMEA Plastic, Rubber, & Chemical Market by Country, 2022 - 2028, USD Million

- TABLE 445 LAMEA Precision Engineering & Optics Market by Country, 2018 - 2021, USD Million

- TABLE 446 LAMEA Precision Engineering & Optics Market by Country, 2022 - 2028, USD Million

- TABLE 447 LAMEA Pharmaceutical & Cosmetics Market by Country, 2018 - 2021, USD Million

- TABLE 448 LAMEA Pharmaceutical & Cosmetics Market by Country, 2022 - 2028, USD Million

- TABLE 449 LAMEA E-Commerce Market by Country, 2018 - 2021, USD Million

- TABLE 450 LAMEA E-Commerce Market by Country, 2022 - 2028, USD Million

- TABLE 451 LAMEA Other Vertical Market by Country, 2018 - 2021, USD Million

- TABLE 452 LAMEA Other Vertical Market by Country, 2022 - 2028, USD Million

- TABLE 453 LAMEA Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 454 LAMEA Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 455 LAMEA Traditional Industrial Robots Market by Country, 2018 - 2021, USD Million

- TABLE 456 LAMEA Traditional Industrial Robots Market by Country, 2022 - 2028, USD Million

- TABLE 457 LAMEA Collaborative Industrial Robots Market by Country, 2018 - 2021, USD Million

- TABLE 458 LAMEA Collaborative Industrial Robots Market by Country, 2022 - 2028, USD Million

- TABLE 459 LAMEA Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 460 LAMEA Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 461 LAMEA Handling Market by Country, 2018 - 2021, USD Million

- TABLE 462 LAMEA Handling Market by Country, 2022 - 2028, USD Million

- TABLE 463 LAMEA Welding Market by Country, 2018 - 2021, USD Million

- TABLE 464 LAMEA Welding Market by Country, 2022 - 2028, USD Million

- TABLE 465 LAMEA Assembly Market by Country, 2018 - 2021, USD Million

- TABLE 466 LAMEA Assembly Market by Country, 2022 - 2028, USD Million

- TABLE 467 LAMEA Processing Market by Country, 2018 - 2021, USD Million

- TABLE 468 LAMEA Processing Market by Country, 2022 - 2028, USD Million

- TABLE 469 LAMEA Dispensing Market by Country, 2018 - 2021, USD Million

- TABLE 470 LAMEA Dispensing Market by Country, 2022 - 2028, USD Million

- TABLE 471 LAMEA Others Market by Country, 2018 - 2021, USD Million

- TABLE 472 LAMEA Others Market by Country, 2022 - 2028, USD Million

- TABLE 473 LAMEA Robot End Effector Market by Country, 2018 - 2021, USD Million

- TABLE 474 LAMEA Robot End Effector Market by Country, 2022 - 2028, USD Million

- TABLE 475 Brazil Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 476 Brazil Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 477 Brazil Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 478 Brazil Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 479 Brazil Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 480 Brazil Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 481 Brazil Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 482 Brazil Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 483 Brazil Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 484 Brazil Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 485 Argentina Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 486 Argentina Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 487 Argentina Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 488 Argentina Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 489 Argentina Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 490 Argentina Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 491 Argentina Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 492 Argentina Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 493 Argentina Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 494 Argentina Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 495 UAE Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 496 UAE Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 497 UAE Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 498 UAE Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 499 UAE Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 500 UAE Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 501 UAE Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 502 UAE Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 503 UAE Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 504 UAE Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 505 Saudi Arabia Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 506 Saudi Arabia Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 507 Saudi Arabia Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 508 Saudi Arabia Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 509 Saudi Arabia Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 510 Saudi Arabia Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 511 Saudi Arabia Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 512 Saudi Arabia Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 513 Saudi Arabia Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 514 Saudi Arabia Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 515 South Africa Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 516 South Africa Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 517 South Africa Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 518 South Africa Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 519 South Africa Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 520 South Africa Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 521 South Africa Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 522 South Africa Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 523 South Africa Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 524 South Africa Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 525 Nigeria Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 526 Nigeria Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 527 Nigeria Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 528 Nigeria Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 529 Nigeria Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 530 Nigeria Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 531 Nigeria Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 532 Nigeria Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 533 Nigeria Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 534 Nigeria Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 535 Rest of LAMEA Robot End Effector Market, 2018 - 2021, USD Million

- TABLE 536 Rest of LAMEA Robot End Effector Market, 2022 - 2028, USD Million

- TABLE 537 Rest of LAMEA Robot End Effector Market by Type, 2018 - 2021, USD Million

- TABLE 538 Rest of LAMEA Robot End Effector Market by Type, 2022 - 2028, USD Million

- TABLE 539 Rest of LAMEA Robot End Effector Market by Vertical, 2018 - 2021, USD Million

- TABLE 540 Rest of LAMEA Robot End Effector Market by Vertical, 2022 - 2028, USD Million

- TABLE 541 Rest of LAMEA Robot End Effector Market by Robot Type, 2018 - 2021, USD Million

- TABLE 542 Rest of LAMEA Robot End Effector Market by Robot Type, 2022 - 2028, USD Million

- TABLE 543 Rest of LAMEA Robot End Effector Market by Application, 2018 - 2021, USD Million

- TABLE 544 Rest of LAMEA Robot End Effector Market by Application, 2022 - 2028, USD Million

- TABLE 545 Key Information - ABB Ltd

- TABLE 546 Key Information - Piab AB

- TABLE 547 Key Information - DESTACO, inc.

- TABLE 548 Key Information - ATI Industrial Automation, Inc.

- TABLE 549 Key Information - Kuka AG

- TABLE 550 Key Information - Bastian Solutions, LLC

- TABLE 551 Key Information - SCHUNK GmbH & Co. KG

- TABLE 552 Key Information - J. Schmalz GmbH

- TABLE 553 Key Information - Zimmer Group

- TABLE 554 Key Information - Robotiq, Inc.

List of Figures

- FIG 1 Methodology for the research

- FIG 2 KBV Cardinal Matrix

- FIG 3 Key Leading Strategies: Percentage Distribution (2018-2022)

- FIG 4 Key Strategic Move: (Acquisitions and Mergers : 2018, Feb - 2022, Aug) Leading Players

- FIG 5 Global Robot End Effector Market share by Type, 2021

- FIG 6 Global Robot End Effector Market share by Type, 2028

- FIG 7 Global Robot End Effector Market by Type, 2018 - 2028, USD Million

- FIG 8 Global Robot End Effector Market share by Vertical, 2021

- FIG 9 Global Robot End Effector Market share by Vertical, 2028

- FIG 10 Global Robot End Effector Market by Vertical, 2018 - 2028, USD Million

- FIG 11 Global Robot End Effector Market share by Robot Type, 2021

- FIG 12 Global Robot End Effector Market share by Robot Type, 2028

- FIG 13 Global Robot End Effector Market by Robot Type, 2018 - 2028, USD Million

- FIG 14 Global Robot End Effector Market share by Application, 2021

- FIG 15 Global Robot End Effector Market share by Application, 2028

- FIG 16 Global Robot End Effector Market by Application, 2018 - 2028, USD Million

- FIG 17 Global Robot End Effector Market share by Region, 2021

- FIG 18 Global Robot End Effector Market share by Region, 2028

- FIG 19 Global Robot End Effector Market by Region, 2018 - 2028, USD Million

- FIG 20 Recent strategies and developments: ABB Ltd.

- FIG 21 SWOT Analysis: ABB Ltd

- FIG 22 Recent strategies and developments: Piab AB

The Global Robot End Effector Market size is expected to reach $4.2 billion by 2028, rising at a market growth of 12.6% CAGR during the forecast period.

Robot end effectors are mechanical devices attached to the end of robotic arms that respond to the robot's environment. It includes selecting and positioning objects, putting product components together, and stacking boxes and packages. The process tools, grippers, and sensors work with the robot end effectors fixed to the robot arm. Robot end effectors are sometimes called end-of-arm tooling (EOA), robot tools, end-of-arm devices, robotic peripherals, robotic tooltips, and robot tools.

An end effector enables the robot to engage with the task at hand. The majority of end effectors are electromechanical or mechanical. They can be as basic as two-finger grippers for pick-and-place activities or as sophisticated as extensive sensor networks for robotic inspection. Sometimes the phrase "End Of Arm Tool" (EOAT) is also used to denote robotic end effector. A robot end effector is essentially the business end of the robot. Most robots are virtually useless without an end effector.

For example, an adjustable robotic arm can be set to a specific spot in its workplace, but without an end effector, it cannot carry out any operations. The use of collaborative robotics is the main driver propelling the robot end effector market. These robots engage with their surroundings and respond appropriately. They adjust their course of action or operation direction in response to alterations in the working environment. Also, the advent of automation in various sectors to complete tasks more quickly has increased the demand for robot end effectors.

COVID-19 Impact Analysis

The COVID-19 pandemic significantly impacted the building, hotel, industrial, and tourism sectors. As a result, production ceased or was severely constrained in many nations. Globally, supply chains for the construction and transportation industries as well as those industries themselves, were hindered. This resulted in a decrease in both the production and the demand for robot end effectors, which restrained the market's expansion. In addition, the automotive industry's operations were constrained during the pandemic. The primary end customers of the robotic end effectors are automotive manufacturers. Therefore, the decrease in this industry impacted the market for robotic end effectors.

Market Growth Factors

Rising installation of the robot end effectors across numerous industries

Automation, AI & ML, IIoT, and other emerging technologies have greatly broadened the use cases for robots, which has resulted in a considerable increase in demand for robotics in recent years. The robotics business has also been impacted by technological development, which has made it possible to create creative, affordable robots. Investment in robotics is further fueled by the growing adoption of digital technologies in commercial, residential, and industrial end-user sectors. Also, advantageous market conditions are being created for the development of the robotics and end-effector markets by supportive government policies and programs like "Industry 4.0" as well as Smart Cities. Hence, throughout the projection period, the demand for robot end effectors is expected to rise, which will promote market growth.

Growing demand for increased automation as well as worker efficiency

Robot end effectors effectively boost labor productivity while improving machine productivity. Automating a manufacturing process speeds up output and increases worker productivity. As a result, more is produced per hour of work. An increase in worker productivity has a substantial positive impact on the business because labor costs have been steadily growing in industrialized nations worldwide recently. In addition, most of the monotonous jobs that humans formerly performed are now being replaced by machines, demanding the use of robots. Robotic technology also aids in reducing the effects of a labor shortage concurrently.

Market Restraining Factors

High implementation and maintenance costs, particularly for SMEs

Investing in industrial robotics and automation is still prohibitively expensive. The expense of installing robotic end effectors is a commercial restraint. The businesses spend less on new investments. They have less capital than the automotive and other major sectors. Few SMEs nowadays, like glass polishing businesses, are required to automate their operation. Additionally, robot end effectors are extremely vulnerable to damage when used in heavy sectors, where repair or maintenance can be expensive. All these factors significantly hinder the growth of the market.

Type Outlook

Based on type, the robot end effector market is categorized into welding guns, grippers, tool changers, clamps, suction cups, and others. The grippers segment garnered the highest revenue share in the robot end effector market in 2021. Gripping tools that can be added to the robot immediately include end effectors and area grasping systems. They are especially well suited to operations that involve packing. The handling use of grippers in a variety of workpieces, taking into account their diverse shapes and sizes, is a major driving force of the gripper segment.

Robot Type Outlook

On the basis of robot type, the robot end effector market is divided into traditional industrial robots and collaborative industrial robots. The traditional industrial robots segment recorded the largest revenue share in the robot end effector market in 2021. Traditional industrial robots are multipurpose manipulator that are automatically controlled, reprogrammable, and programmable in three or more axes that can be fixed or attached to a mobile base for implementation in automation operations in an industrial setting.

Application Outlook

Based on application, the robot end effector market is segmented into handling, welding, assembly, processing, dispensing, and others. The assembly segment procured a remarkable growth rate in the robot end effector market in 2021. Assembly robots perform highly repetitive tasks more rapidly and accurately than human labor, which supports the segment's expansion. The employment of robotics in assembly and disassembly processes frees humans to take on other tasks that don't put them at risk for workplace accidents. A work cell may house one or more assembly tasks in robotic assembly systems. Robots can use vision systems to do complex pick-and-place tasks and quality control.

Vertical Outlook

On the basis of vertical, the robot end effector market is classified into automotive, electrical & electronics, metal & machinery, plastic, rubber, & chemical, food & beverage, precision engineering & optics, pharmaceutical & cosmetics, e-commerce, and others. The electrical and electronics segment witnessed a substantial revenue share in the robot end effector market in 2021. Robots are capable of performing hazardous tasks that are risky for humans. Robots can work with high-voltage equipment and hazardous materials in the electrical and electronics industries, lowering the danger of worker damage or even death. Automated robots can be used at practically any point of the whole production cycle and have great potential in the manufacturing of electronics today.

Regional Outlook

Region wise, the robot end effector market is analyzed across North America, Europe, Asia Pacific, and LAMEA. The Asia Pacific region acquired the largest revenue share in the robot end effector market in 2021. Due to minimal production costs, easy availability of affordable labor, lax emission and safety standards, and government interventions for foreign direct investments, the robot end effector market in the region has grown more rapidly over the past ten years. In addition, the region also has a robust automotive and semiconductor industry, which uses robot end effectors significantly.

The major strategies followed by the market participants are Acquisitions. Based on the Analysis presented in the Cardinal matrix; Piab AB is the forerunner in the Robot End Effector Market. Companies such as ABB Ltd., DESTACO, Inc., and Kuka AG are some of the key innovators in Robot End Effector Market.

The market research report covers the analysis of key stake holders of the market. Key companies profiled in the report include ABB Ltd., ATI Industrial Automation, Inc. (Novanta, Inc.), DESTACO, Inc. (Dover Corporation), Kuka AG (Midea Investment Holding Co., Ltd.), Bastian Solutions, LLC (Toyota Advanced Logistics Group) (Toyota Industries Corporation), Piab AB (Patricia Industries)(Investor AB), Robotiq, Inc., SCHUNK GmbH & Co. KG, J. Schmalz GmbH and Zimmer Group.

Recent Strategies Deployed in Robot End Effector Market

Partnerships, Collaborations and Agreements:

Jul-2022: ABB extended its collaboration with SKF for identifying and evaluating solutions for supporting clients' increased production efficiency and improving manufacturing capabilities. The expansion strengthened the company's technical leadership and its focus on industrial automation.

Feb-2022: ATI Industrial Automation and Celera Motion, the business units of Novanta, partnered with MassRobotics, for developing and scaling the next generation of successful robotics startups. Following this partnership, the companies would create advanced innovations in surgical/medical robotics and would increase robotic productivity.

Nov-2021: ABB announced a partnership with Sevensense Robotics, a provider of 3D visual technology and artificial intelligence, for driving next-generation autonomous mobile robots. The partnership is yet another crucial step in ABB's strategy to advance flexible automation's next generation and broaden its robotics and automation product offerings.

Nov-2020: KUKA Robotics extended its partnership with AutomaTech Robotik, the Canadian provider of robotic automation solutions, to North America. The partnership's main focus is to spread awareness of AutomaTech's KUKA robot-based woodworking machine tending solutions throughout North America. With the help of AutomaTech's software and robotics integration expertise, KUKA's robot technology will enable manufacturers to develop their businesses.

Jul-2020: KUKA came into partnership with T-Systems for creating a solution for digitalized production in order to help the manufacturing industry in reaping benefits from digitization immediately.

Feb-2020: ABB came into partnership with Covariant, for bringing AI-enabled robotics solutions, starting from a completely autonomous warehouse order fulfillment solution. With Covariant AI technology, ABB expedites its entry into the distribution and e-commerce fulfillment sectors. Together, the companies will work towards a robotics-enabled AI future in which intelligent robots collaborate with people in dynamic surroundings, learning from and developing as a group with each task accomplished.

Acquisitions and Mergers:

Aug-2022: Piab Group took over AVAC Vakuumteknik, a vacuum automation specialist. The acquisition of AVAC complemented the company's portfolio of products and solutions ranging from a vast range of applications.

Apr-2022: Piab signed an agreement to acquire Joulin, a provider of vacuum gripping solutions. The acquisition complemented Piab's business in the rising material handling solutions market.

Oct-2020: ABB completed the acquisition of Codian Robotics, a company that provides delta robots. The acquisition enabled ABB to assist its clients in realizing the full potential of automation and enhance their flexibility in a business environment that is undergoing rapid change.

Geographical and Business Expansions:

Mar-2023: ABB announced the expansion of its North American Robotics headquarters and manufacturing facility in Michigan by increasing its production capacity in response to the rising automation demand. With this expansion, the company would enhance its leadership in the development and manufacturing of cutting-edge robotic solutions in the U.S.

Mar-2023: Schmalz announced the expansion of its facility in the Raleigh area for robotics tooling production. New product lines, such as workstation cranes and end-of-arm robotic palletizer and de-palletizer equipment, will be accommodated following the expansion. Moreover, Schmaltz will add new product lines for material handling systems and collaborative robot end-of-arm equipment. Schmalz Inc. would be able to accommodate high-demand products that must be delivered quickly to distributors and consumers because of the expanded assembly warehouse, which will also give the company much-needed additional capacity for value-added assembly work. Our growth in the North American market will be aided even further by the additional office space.

Dec-2022: ABB announced the opening of its state-of-the-art, flexible, and fully automated robotics factory in Shanghai, China. The 67,000m2 manufacturing and research facility, in which ABB invested $150 million (1.1 billion RMB), will use its digital and automation technologies to produce next-generation robots, strengthening its position as a leader in robotics and automation in China.

Dec-2021: Schunk opened new CoLabs in the USA and China for providing local customers with automation. The experts on-site can test and improve industrial applications for the automotive industry, aerospace industry, or medical technology in live operation, across a total of 215 square meters.

Product Launches and Expansions:

Mar-2023: Destaco released a new line of cobot tooling solutions that would support customers who use cobots and small payload robots in their operations. The tools are suitable for tasks such as grasping, palletizing, machine tending, tool change, and tool extension. The tooling solutions are suitable for cobots with an ISO 9409-1-50-4-M6 end-of-arm attachment pattern.

Dec-2021: ATI Industrial Automation introduced the QC-29 robotic tool changer for opening up the productivity for smaller robots. The changer features the rugged and powerful technology of ATI's heavy-duty tool changers for robots in the 25-35 kg payload class. The QC-29 is the first standard ATI Tool Changer created with a rectangular body that attaches quickly to robot wrists with a diameter of 40 mm and 50 mm. Connecting utilities is made simple with built-in airports and three module mounting flats, and the Zero-Freeplay design assures maximum repeatability for high-efficiency tool changes.

Apr-2021: Piab AB announced the launch of new suction end effectors for industrial robots. In particular, for the logistics, warehousing, e-commerce, and recycling industries, the MX suction cup family of Piab, is remarkable for scooping up various things. Applications for the MX suction cup include bin picking, order fulfillment, box depalletizing, and parcel sorting. The five sizes of MX suction cups-35, 42, 50, 57, and 65 mm in diameter-are all compatible with its comprehensive piGRIP fitting programme, providing a variety of fitting choices that may be customized to your requirements.

Mar-2021: Destaco unveiled TCI manual tool changer for cobots. With the TC1 Series manual tool changer, Destaco increased the scope of its end-of-arm tooling offering. The TC1 tool changer is pre-assembled and ready to install for collaborative robots used for loading and unloading, picking and placing, and other applications. The TC1 tool changer's small weight of 330 grams (11.6 ounces) and low-profile height of 25 mm (1 inch) have little effect on the payload capacity of cobots. The TC1's push-button release enables a tool change in under three seconds. The TC1 has inbuilt safety features, such as a visible red signal when the tool is not securely coupled or locked into place, and positional coupling repeatability of 0.025 mm (0.001 inches).

Jan-2021: Piab introduced a soft gripper, or end effector, for industrial robots. Piab's piSoftGrip line was created for the automation of the chocolate and food industries. The vacuum-based soft gripper can hold onto delicate, lightweight oblong items with unique geometries and/or surfaces. PiSoftGrip is a straightforward and reliable tool with two grasping fingers and a sealed hoover cavity that are both constructed in one piece. The product is not sensitive to dust, and the degree of hoover applied allows for simple adjustment and control of the gripping force. To facilitate the picking of extended items, it is simple to arrange the gripper in rows (multiple modes).

Scope of the Study

Market Segments covered in the Report:

By Type

- Grippers

- Welding Guns

- Tool Changers

- Clamps

- Suction Cups

- Others

By Vertical

- Automotive

- Metal & Machinery

- Food & Beverage

- Electrical & Electronics

- Plastic, Rubber, & Chemical

- Precision Engineering & Optics

- Pharmaceutical & Cosmetics

- E-Commerce

- Others

By Robot Type

- Traditional Industrial Robots

- Collaborative Industrial Robots

By Application

- Handling

- Welding

- Assembly

- Processing

- Dispensing

- Others

By Geography

- North America

- US

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- UK

- France

- Russia

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Singapore

- Malaysia

- Rest of Asia Pacific

- LAMEA

- Brazil

- Argentina

- UAE

- Saudi Arabia

- South Africa

- Nigeria

- Rest of LAMEA

Companies Profiled

- ABB Ltd.

- ATI Industrial Automation, Inc. (Novanta, Inc.)

- DESTACO, Inc. (Dover Corporation)

- Kuka AG (Midea Investment Holding Co., Ltd.)

- Bastian Solutions, LLC (Toyota Advanced Logistics Group) (Toyota Industries Corporation)

- Piab AB (Patricia Industries)(Investor AB)

- Robotiq, Inc.

- SCHUNK GmbH & Co. KG

- J. Schmalz GmbH

- Zimmer Group

Unique Offerings from KBV Research

- Exhaustive coverage

- Highest number of market tables and figures

- Subscription based model available

- Guaranteed best price

- Assured post sales research support with 10% customization free

Table of Contents

Chapter 1. Market Scope & Methodology

- 1.1 Market Definition

- 1.2 Objectives

- 1.3 Market Scope

- 1.4 Segmentation

- 1.4.1 Global Robot End Effector Market, by Type

- 1.4.2 Global Robot End Effector Market, by Vertical

- 1.4.3 Global Robot End Effector Market, by Robot Type

- 1.4.4 Global Robot End Effector Market, by Application

- 1.4.5 Global Robot End Effector Market, by Geography

- 1.5 Methodology for the research

Chapter 2. Market Overview

- 2.1 Introduction

- 2.1.1 Overview

- 2.1.1.1 Market Composition & Scenario

- 2.1.1 Overview

- 2.2 Key Factors Impacting the Market

- 2.2.1 Market Drivers

- 2.2.2 Market Restraints

Chapter 3. Competition Analysis - Global

- 3.1 KBV Cardinal Matrix

- 3.2 Recent Industry Wide Strategic Developments

- 3.2.1 Partnerships, Collaborations and Agreements

- 3.2.2 Product Launches and Product Expansions

- 3.2.3 Acquisition and Mergers

- 3.2.4 Geographical Expansions

- 3.3 Top Winning Strategies

- 3.3.1 Key Leading Strategies: Percentage Distribution (2018-2022)

- 3.3.2 Key Strategic Move: (Acquisitions and Mergers : 2018, Feb - 2022, Aug) Leading Players

Chapter 4. Global Robot End Effector Market by Type

- 4.1 Global Grippers Market by Region

- 4.2 Global Welding Guns Market by Region

- 4.3 Global Tool Changers Market by Region

- 4.4 Global Clamps Market by Region

- 4.5 Global Suction Cups Market by Region

- 4.6 Global Others Market by Region

Chapter 5. Global Robot End Effector Market by Vertical

- 5.1 Global Automotive Market by Region

- 5.2 Global Metal & Machinery Market by Region

- 5.3 Global Food & Beverage Market by Region

- 5.4 Global Electrical & Electronics Market by Region

- 5.5 Global Plastic, Rubber, & Chemical Market by Region

- 5.6 Global Precision Engineering & Optics Market by Region

- 5.7 Global Pharmaceutical & Cosmetics Market by Region

- 5.8 Global E-Commerce Market by Region

- 5.9 Global Other Vertical Market by Region

Chapter 6. Global Robot End Effector Market by Robot Type

- 6.1 Global Traditional Industrial Robots Market by Region

- 6.2 Global Collaborative Industrial Robots Market by Region

Chapter 7. Global Robot End Effector Market by Application

- 7.1 Global Handling Market by Region

- 7.2 Global Welding Market by Region

- 7.3 Global Assembly Market by Region

- 7.4 Global Processing Market by Region

- 7.5 Global Dispensing Market by Region

- 7.6 Global Others Market by Region

Chapter 8. Global Robot End Effector Market by Region

- 8.1 North America Robot End Effector Market

- 8.1.1 North America Robot End Effector Market by Type

- 8.1.1.1 North America Grippers Market by Country

- 8.1.1.2 North America Welding Guns Market by Country

- 8.1.1.3 North America Tool Changers Market by Country

- 8.1.1.4 North America Clamps Market by Country

- 8.1.1.5 North America Suction Cups Market by Country

- 8.1.1.6 North America Others Market by Country

- 8.1.2 North America Robot End Effector Market by Vertical

- 8.1.2.1 North America Automotive Market by Country

- 8.1.2.2 North America Metal & Machinery Market by Country

- 8.1.2.3 North America Food & Beverage Market by Country

- 8.1.2.4 North America Electrical & Electronics Market by Country

- 8.1.2.5 North America Plastic, Rubber, & Chemical Market by Country

- 8.1.2.6 North America Precision Engineering & Optics Market by Country

- 8.1.2.7 North America Pharmaceutical & Cosmetics Market by Country

- 8.1.2.8 North America E-Commerce Market by Country

- 8.1.2.9 North America Other Vertical Market by Country

- 8.1.3 North America Robot End Effector Market by Robot Type

- 8.1.3.1 North America Traditional Industrial Robots Market by Country

- 8.1.3.2 North America Collaborative Industrial Robots Market by Country

- 8.1.4 North America Robot End Effector Market by Application

- 8.1.4.1 North America Handling Market by Country

- 8.1.4.2 North America Welding Market by Country

- 8.1.4.3 North America Assembly Market by Country

- 8.1.4.4 North America Processing Market by Country

- 8.1.4.5 North America Dispensing Market by Country

- 8.1.4.6 North America Others Market by Country

- 8.1.5 North America Robot End Effector Market by Country

- 8.1.5.1 US Robot End Effector Market

- 8.1.5.1.1 US Robot End Effector Market by Type

- 8.1.5.1.2 US Robot End Effector Market by Vertical

- 8.1.5.1.3 US Robot End Effector Market by Robot Type

- 8.1.5.1.4 US Robot End Effector Market by Application

- 8.1.5.2 Canada Robot End Effector Market

- 8.1.5.2.1 Canada Robot End Effector Market by Type

- 8.1.5.2.2 Canada Robot End Effector Market by Vertical

- 8.1.5.2.3 Canada Robot End Effector Market by Robot Type

- 8.1.5.2.4 Canada Robot End Effector Market by Application