|

|

市場調査レポート

商品コード

1140426

自動化COE (Center of Excellence) の世界市場:サービス別 (導入支援、ガバナンス、設計・試験)・組織規模別 (中小企業、大企業)・業種別 (BFSI、製造業、医療・ライフサイエンス)・地域別の将来予測 (2027年まで)Automation COE Market by Service (Implementation Support, Governance, Design & Testing), Organization Size (SMEs and Large Enterprises), Vertical (BFSI, Manufacturing, Healthcare & Life Sciences) and Region - Global Forecast to 2027 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 自動化COE (Center of Excellence) の世界市場:サービス別 (導入支援、ガバナンス、設計・試験)・組織規模別 (中小企業、大企業)・業種別 (BFSI、製造業、医療・ライフサイエンス)・地域別の将来予測 (2027年まで) |

|

出版日: 2022年10月12日

発行: MarketsandMarkets

ページ情報: 英文 168 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

自動化COEの市場規模は、2022年の3億米ドルから2027年には15億米ドルへと、予測期間中に36.9%のCAGRで成長すると予測されます。

自動化COE市場の成長を促す要因としては、企業全体のROIの大幅な改善、データ入力エラーの減少、リスクの低減による品質の向上などが挙げられます。

サービス別に見ると、技術評価・コンサルティングサービスの分野が予測期間中に最大の市場規模を記録する見通しです。組織規模別では、大企業が予測期間中に最大の市場規模を占めています。

地域別に見ると、予測期間中は、北米が市場を独占する一方、アジア太平洋が最高のCAGRで成長すると見込まれています。北米市場の成長は、この地域における自動化COEの大手サービスプロバイダーの存在と、研究開発 (R&D) 投資の増加に起因していると考えられます。

当レポートでは、世界の自動化COE (Center of Excellence) の市場について分析し、市場の基本構造や最新情勢、主な市場促進・抑制要因、サービス別・組織規模別・業種別・地域別の市場動向の見通し、市場競争の状態、主要企業のプロファイルなどを調査しております。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要と動向

- イントロダクション

- 市場力学

- 産業動向

- 市場の進化

- 特許分析

- 関税・規制の状況

- 技術分析

- 人工知能 (AI) と機械学習 (ML)

- 自然言語処理 (NLP)

- 光学文字認識 (OCR)

- クラウドコンピューティング

- コンピュータビジョン

- ケーススタディ分析

- エコシステム

- サプライチェーン分析

- ロボットオペレーティングモデル(ROM)の7つの柱

- 自動化COEを達成するための重要な実践

- 主要な事業機能にまたがる自動化COE

- イントロダクション

- 人事

- 財務会計

- 販売・マーケティング

- サプライチェーン・オペレーション

- IT (情報技術)

- 主な会議とイベント (2022年~2023年)

第6章 自動化COE市場:サービス別

- イントロダクション

- 技術評価・コンサルティングサービス

- 設計・試験サービス

- ガバナンスサービス

- 導入支援サービス

第7章 自動化COE市場:組織規模別

- イントロダクション

- 大企業

- 中小企業

第8章 自動化COE市場:業種別

- イントロダクション

- 銀行・金融サービス・保険 (BFSI)

- 製造業

- 小売業・消費財

- 輸送・物流

- IT・ITeS

- 医療・ライフサイエンス

- その他の業種

第9章 自動化COE市場:地域別

- イントロダクション

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- 他の欧州諸国

- アジア太平洋

- インド

- 日本

- 中国

- 他のアジア太平洋諸国

- 他の国々 (RoW)

- 中東・アフリカ

- ラテンアメリカ

第10章 競合情勢

- 概要

- 主要企業の戦略

- 市場評価フレームワーク

- 収益分析

- 過去の収益分析

- 主要企業のランキング (2022年)

- 自動化COE市場における主要ベンダーの比較分析 (2022年)

- 競合シナリオと動向

- 製品の発売

- 資本取引

第11章 企業プロファイル

- イントロダクション

- 主要企業

- SS&C BLUE PRISM

- UIPATH

- AUTOMATION ANYWHERE

- NICE

- DIGITAL WORKFORCE

- HELPSYSTEMS

- その他の企業

- CTRL365

- FASTPATH

- ELECTRONEEK

- ANYROBOT

- NINTEX

- CHAZEY PARTNERS

- SMARTBRIDGE

- BLUEPRINT

- ROBOCLOUD

- VERINT

- CIGNITI

- INNOMINDS

- TESTINGXPERTS

- KIWIQA

- CIGNEX

- ROBOYO

- CALIDAD INFOTECH

- CHOICEWORX

- XENONSTACK

第12章 隣接・関連市場

- イントロダクション

- インテリジェントプロセス自動化市場:世界市場の予測 (2027年まで)

- RPA (ロボットプロセス自動化)・ハイパー自動化市場:世界市場の予測 (2027年まで)

第13章 付録

The automation CoE market size to grow from USD 0.3 billion in 2022 to USD 1.5 billion by 2027, at a Compound Annual Growth Rate (CAGR) of 36.9% during the forecast period. The automation COE market is expected to grow at a significant rate during the forecast period, owing to various business drivers. Some factors driving the growth of the automation COE market are significant improvements in ROIs across businesses, reduced data entry errors, and improved quality with reduced risk.

An automation center of excellence (COE) treats enterprise automation as an ongoing project requiring planning, testing, and regular evaluation. The automation COE framework can be divided into two interrelated pillars: people & processes and systems & infrastructure. In both parts of the framework, it is essential to lay a solid foundation for ongoing enterprise automation projects.

As per UiPath, an automation COE is an internal team that streamlines automation output, provides structure, and helps users scale automation throughout the enterprise. Having a team of automation experts can help users save time and money in developing strategies, ensuring that the company gets the most out of the automation program.

Technology & consulting services to register for the largest market size during the forecast period

Based on services, the automation COE market is segmented into technology assessment & consulting services, design & testing services, governance services, and implementation support services. Automation COE combines multiple technologies to automate complex end-to-end business processes that involve decision-making and continuous learning. Businesses leverage this opportunity by automating small rule-based tasks to complex business processes. To respond to this dynamic trend, organizations need superior automation capabilities.

Large Enterprises to account for the largest market size during the forecast period

Based on organization size, the automation COE market has been segmented into SMEs and large enterprises. SMEs are enterprises with an employee strength of 1-1,000, while large enterprises have an employee strength of more than 1,000. With globalization, organizations have recognized the need to train the internal staff, as well as customers, to attain their business goals. Companies require technologies that can assist them in improving their profit margins and operational efficiencies. Large enterprises are expected to rapidly adopt automation COE in the coming years due to their complex network of channel partners present across the globe.

Asia Pacific to hold highest CAGR during the forecast period

Based on regions, the automation COE market is segmented into North America, Asia Pacific, Europe, and the Rest of the World (RoW). The RoW covers the Middle East & Africa and Latin America. North America is expected to dominate the market during the forecast period. The growth of the North American market can be attributed to the presence of leading service providers for automation COE and increasing investments in R&D in this region.

Enterprises across all regions are increasingly opting for integration and automation technologies for various business operations, such as finance, HR, sales, marketing, and customer support. The Work Automation Index 2022 found that 66% of organizations in North America now use COE platforms in five or more departments, and the number of organizations with seven automated departments has almost tripled since 2019. North America and Europe are expected to hold relatively larger shares of the market, as companies in these regions are early adopters of trending technologies.

Breakdown of primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the frontline workers training market.

- By Company: Tier I: 35%, Tier II: 45%, and Tier III: 20%

- By Designation: C-Level Executives: 35%, D-Level Executives: 25%, and Managers: 40%

- By Region: APAC: 30%, Europe: 20%, North America: 45%, Rest of the World: 5%

The report includes the study of key players offering frontline workers training. It profiles major vendors in the frontline workers training market. The major players in the frontline workers training market include SS&C Blue Prism (UK), UiPath (US), Automation Anywhere (US), NICE (Israel), Digital Workforce (Finland), HelpSystems (US), Ctrl365 (Argentina), FASTPATH (Netherlands), ElectroNeek (US), AnyRobot (US), Roboyo (Germany), Nintex (US), Chazey Partners (US), Smartbridge (US), Blueprint (US), Robocloud (UK), Verint (US), HelpSystems (US), Cigniti (India), Innominds (US), TestingXperts (US), KiwiQA (Australia), Calidad Infotech (India), CIGNEX (US), ChoiceWORX (US), and XenonStack (US).

Research Coverage

The research study for the automation COE market involved extensive use of secondary sources, directories, the Journal of Information Systems & Technology Management, the RPA Journal, and paid databases. Primary sources were mainly industry experts from core and related industries, preferred automation COE solution and service providers, third-party service providers, consulting service providers, end users, and other commercial enterprises. In-depth interviews were conducted with various primary respondents, including key industry participants and subject-matter experts, to obtain and verify critical qualitative and quantitative information, and assess the prospects of the market.

Key Benefits of Buying the Report

The report would provide the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall frontline workers training market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights better to position their business and plan suitable go-to-market strategies. It also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS & EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- TABLE 1 UNITED STATES DOLLAR EXCHANGE RATE, 2019-2021

- 1.5 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 AUTOMATION COE MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- TABLE 2 PRIMARY INTERVIEWS

- 2.1.2.1 Breakup of primary profiles

- 2.1.2.2 Key industry insights

- 2.2 MARKET BREAKUP & DATA TRIANGULATION

- FIGURE 2 DATA TRIANGULATION

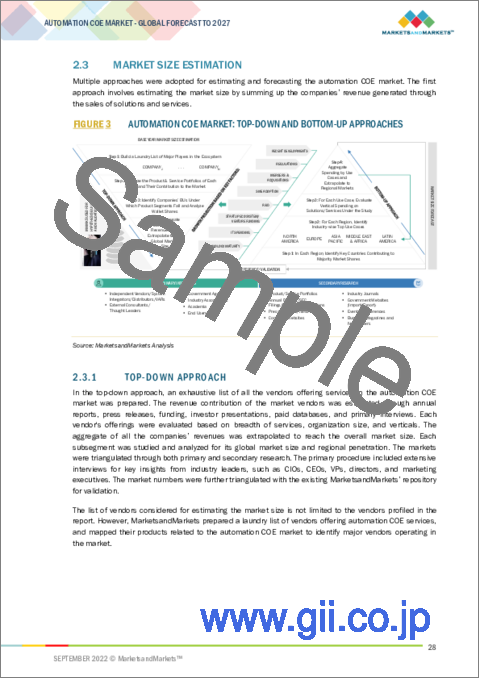

- 2.3 MARKET SIZE ESTIMATION

- FIGURE 3 AUTOMATION COE MARKET: TOP-DOWN AND BOTTOM-UP APPROACHES

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY - BOTTOM-UP APPROACH 1 (SUPPLY SIDE): REVENUE FROM SOLUTIONS/SERVICES

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY - BOTTOM-UP APPROACH 2 (SUPPLY SIDE): COLLECTIVE REVENUE FROM ALL SERVICES

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY - BOTTOM-UP APPROACH 3 (SUPPLY SIDE): COLLECTIVE REVENUE FROM ALL SERVICES

- FIGURE 7 MARKET SIZE ESTIMATION METHODOLOGY - BOTTOM-UP APPROACH 4 (DEMAND SIDE): SHARE OF AUTOMATION COE THROUGH OVERALL SPENDING

- 2.4 MARKET FORECAST

- TABLE 3 FACTOR ANALYSIS

- 2.5 ASSUMPTIONS

- 2.6 LIMITATIONS

3 EXECUTIVE SUMMARY

- TABLE 4 GLOBAL AUTOMATION COE MARKET SIZE AND GROWTH RATE, 2020-2027 (USD MILLION, Y-O-Y%)

- FIGURE 8 TECHNOLOGY ASSESSMENT & CONSULTING SEGMENT TO HOLD LARGER SHARE OF AUTOMATION COE MARKET IN 2022

- FIGURE 9 LARGE ENTERPRISES TO DOMINATE MARKET IN 2022

- FIGURE 10 BFSI VERTICAL TO ACCOUNT FOR LARGEST SHARE OF MARKET IN 2022

- FIGURE 11 NORTH AMERICA TO HOLD HIGHEST SHARE OF AUTOMATION COE MARKET IN 2022

4 PREMIUM INSIGHTS

- 4.1 OPPORTUNITIES IN AUTOMATION COE MARKET

- FIGURE 12 SIGNIFICANT IMPROVEMENTS IN ROI ACROSS BUSINESSES TO DRIVE GROWTH IN MARKET

- 4.2 AUTOMATION COE MARKET: BY TOP 2 SERVICES AND TOP 3 VERTICALS

- FIGURE 13 TECHNOLOGY ASSESSMENT & CONSULTING SEGMENT AND BFSI VERTICAL TO HOLD HIGH MARKET SHARES IN 2022

- 4.3 AUTOMATION COE MARKET: BY REGION

- FIGURE 14 NORTH AMERICA TO HOLD HIGHEST SHARE IN 2022

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 15 AUTOMATION COE MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Significant improvements in ROI across businesses

- 5.2.1.2 Reduced data entry errors

- 5.2.1.3 Improved quality with reduced risk

- 5.2.2 RESTRAINTS

- 5.2.2.1 High development and deployment costs

- 5.2.2.2 Dependence on suppliers and inadequate capabilities to scale automation over time

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Reduced churn

- 5.2.3.2 Continuity of operations using RPA maintenance

- 5.2.3.3 Rise in demand for automation from different industries

- 5.2.4 CHALLENGES

- 5.2.4.1 Employee hesitation and fear of automation due to worries about losing jobs

- 5.2.4.2 Lack of knowledge among departments

- 5.2.4.3 Optimizing business processes prior to automation

- 5.3 INDUSTRY TRENDS

- 5.3.1 MARKET EVOLUTION

- FIGURE 16 EVOLUTION OF AUTOMATION COE MARKET

- 5.3.2 PATENT ANALYSIS

- 5.3.2.1 Methodology

- 5.3.2.2 Document type

- TABLE 5 PATENTS FILED, 2018-2021

- 5.3.2.3 Innovation and patent applications

- FIGURE 17 TOTAL NUMBER OF PATENTS GRANTED IN A YEAR, 2018-2021

- 5.3.2.4 Top applicants

- FIGURE 18 TOP 10 COMPANIES WITH HIGHEST NUMBER OF PATENT APPLICATIONS, 2018-2021

- 5.4 TARIFF AND REGULATORY LANDSCAPE

- 5.4.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 6 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 7 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 8 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 9 MIDDLE EAST & AFRICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 LATIN AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.5 TECHNOLOGY ANALYSIS

- 5.5.1 ARTIFICIAL INTELLIGENCE AND MACHINE LEARNING

- 5.5.2 NATURAL LANGUAGE PROCESSING

- 5.5.3 OPTICAL CHARACTER RECOGNITION

- 5.5.4 CLOUD COMPUTING

- 5.5.5 COMPUTER VISION

- 5.6 CASE STUDY ANALYSIS

- 5.6.1 CASE STUDY: PROSEGUR SECURES USD 12 MILLION IN SAVINGS WITH STRATEGIC INTELLIGENT AUTOMATION PROGRAM

- 5.6.2 CASE STUDY: OHIO'S HOSPICE DELIVERS IMPROVED PATIENT AND EMPLOYEE EXPERIENCE WITH NEW DIGITAL WORKFORCE

- 5.6.3 CASE STUDY: AGCO EMPLOYEES NEGOTIATE CONTRACTS AND LET DIGITAL WORKERS MANAGE PAPERWORK

- 5.6.4 CASE STUDY: AGCO IS FUTURE-PROOFING ITS BUSINESS WITH INTELLIGENT AUTOMATION

- 5.6.5 CASE STUDY: UNIPER TRANSFORMS BUSINESS WITH AUTOMATION

- 5.6.6 CASE STUDY: CUSTODIAL AGENCY AT DUTCH MINISTRY OF JUSTICE USES AUTOMATION TO IMPROVE SERVICES FOR RESIDENTS OF NETHERLANDS

- 5.6.7 CASE STUDY: WALL-TO-WALL AUTOMATION 360 SAVES NEWCASTLE HOSPITALS 7,000 HOURS ANNUALLY, IMPROVING STAFF WORK-LIFE BALANCE

- 5.6.8 CASE STUDY: RAPID ROI FROM RPA - SYNERGY AUTOMATES BILLING TO REALIZE SIGNIFICANT VALUE

- 5.6.9 CASE STUDY: LUMEVITY - FINDING QUICK AUTOMATION WINS WITH FORTRESSIQ

- 5.6.10 CASE STUDY: ARAB NATIONAL BANK SAVED 64K+ HOURS BY SUCCESSFULLY IMPLEMENTING BOTS TO AUTOMATE PROCESSES

- 5.7 ECOSYSTEM

- FIGURE 19 AUTOMATION COE MARKET: ECOSYSTEM

- 5.8 SUPPLY CHAIN ANALYSIS

- FIGURE 20 SUPPLY CHAIN ANALYSIS

- TABLE 11 AUTOMATION COE MARKET: SUPPLY CHAIN

- 5.9 SEVEN PILLARS OF ROBOTIC OPERATING MODEL (ROM)

- FIGURE 21 SEVEN PILLARS OF ROM

- 5.9.1 INTRODUCTION

- 5.10 KEY PRACTICES TO ACHIEVE AUTOMATION COE

- 5.10.1 INTRODUCTION

- 5.11 AUTOMATION COE ACROSS MAJOR BUSINESS FUNCTIONS

- 5.11.1 INTRODUCTION

- 5.11.2 HUMAN RESOURCES

- 5.11.3 FINANCE & ACCOUNTING

- 5.11.4 SALES & MARKETING

- 5.11.5 SUPPLY CHAIN & OPERATIONS

- 5.11.6 INFORMATION TECHNOLOGY

- 5.12 KEY CONFERENCES & EVENTS IN 2022-2023

- TABLE 12 AUTOMATION COE MARKET: DETAILED LIST OF CONFERENCES & EVENTS

6 AUTOMATION COE MARKET, BY SERVICE

- 6.1 INTRODUCTION

- 6.1.1 SERVICES: AUTOMATION COE MARKET DRIVERS

- FIGURE 22 TECHNOLOGY ASSESSMENT & CONSULTING SERVICES TO DOMINATE MARKET DURING FORECAST PERIOD

- TABLE 13 AUTOMATION COE MARKET, BY SERVICE, 2020-2027 (USD MILLION)

- 6.2 TECHNOLOGY ASSESSMENT & CONSULTING SERVICES

- 6.2.1 NEED TO IDENTIFY AND EVALUATE AUTOMATION TO IMPROVE BUSINESS OPERATIONS TO DRIVE MARKET

- TABLE 14 TECHNOLOGY ASSESSMENT & CONSULTING SERVICES: AUTOMATION COE MARKET, BY REGION, 2020-2027 (USD MILLION)

- 6.3 DESIGN & TESTING SERVICES

- 6.3.1 ADVANTAGES SUCH AS REDUCED REDUNDANCIES AND IMPROVED PROCESS QUALITY TO BOOST ADOPTION

- TABLE 15 DESIGN & TESTING SERVICES: AUTOMATION COE MARKET, BY REGION, 2020-2027 (USD MILLION)

- 6.4 GOVERNANCE SERVICES

- 6.4.1 ABILITY OF GOVERNANCE SERVICES TO PROMOTE AND SUPPORT ORGANIZATION-WIDE AUTOMATION TO FUEL DEMAND

- TABLE 16 GOVERNANCE SERVICES: AUTOMATION COE MARKET, BY REGION, 2020-2027 (USD MILLION)

- 6.5 IMPLEMENTATION SUPPORT SERVICES

- 6.5.1 NEED TO EMBED INTELLIGENT DECISION-MAKING CAPABILITIES INTO BUSINESS SOLUTIONS TO DRIVE ADOPTION

- TABLE 17 IMPLEMENTATION SUPPORT SERVICES: AUTOMATION COE MARKET, BY REGION, 2020-2027 (USD MILLION)

7 AUTOMATION COE MARKET, BY ORGANIZATION SIZE

- 7.1 INTRODUCTION

- 7.1.1 ORGANIZATION SIZE: AUTOMATION COE MARKET DRIVERS

- FIGURE 23 SMALL AND MEDIUM-SIZED ENTERPRISES TO REGISTER HIGHER GROWTH RATE DURING FORECAST PERIOD

- TABLE 18 AUTOMATION COE MARKET, BY ORGANIZATION SIZE, 2020-2027 (USD MILLION)

- 7.2 LARGE ENTERPRISES

- 7.2.1 GROWING DEMAND FOR AUTOMATION SOLUTIONS TO SHORTEN TIME SPENT ON ROUTINE TASKS IN LARGE ENTERPRISES TO DRIVE MARKET

- TABLE 19 LARGE ENTERPRISES: AUTOMATION COE MARKET, BY REGION, 2020-2027 (USD MILLION)

- 7.3 SMALL AND MEDIUM-SIZED ENTERPRISES

- 7.3.1 ADVANTAGES SUCH AS COST-EFFECTIVENESS AND INCREASED PRODUCTIVITY TO DRIVE DEMAND FOR AUTOMATION COE AMONG SMES

- TABLE 20 SMALL AND MEDIUM-SIZED ENTERPRISES: AUTOMATION COE MARKET, BY REGION, 2020-2027 (USD MILLION)

8 AUTOMATION COE MARKET, BY VERTICAL

- 8.1 INTRODUCTION

- 8.1.1 VERTICALS: AUTOMATION COE MARKET DRIVERS

- FIGURE 24 HEALTHCARE & LIFE SCIENCES VERTICAL TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 21 AUTOMATION COE MARKET, BY VERTICAL, 2020-2027 (USD MILLION)

- 8.2 BANKING, FINANCIAL SERVICES, AND INSURANCE (BFSI)

- 8.2.1 HIGH ADOPTION OF INTELLIGENT AUTOMATION IN BFSI VERTICAL TO FOSTER GROWTH

- TABLE 22 BANKING, FINANCIAL SERVICES, AND INSURANCE: AUTOMATION COE MARKET, BY REGION, 2020-2027 (USD MILLION)

- 8.3 MANUFACTURING

- 8.3.1 NEED TO ACHIEVE AUTOMATED EFFICIENCY IN AREAS OTHER THAN PRODUCTION LINE TO DRIVE ADOPTION IN MANUFACTURING PLANTS

- TABLE 23 MANUFACTURING: AUTOMATION COE MARKET, BY REGION, 2020-2027 (USD MILLION)

- 8.4 RETAIL & CONSUMER GOODS

- 8.4.1 GROWING ADOPTION OF AUTOMATION IN RETAIL TO SUPPORT INVENTORY, SUPPLY CHAIN, AND INVOICING TO AID GROWTH

- TABLE 24 RETAIL & CONSUMER GOODS: AUTOMATION COE MARKET, BY REGION, 2020-2027 (USD MILLION)

- 8.5 TRANSPORTATION & LOGISTICS

- 8.5.1 GROWING INVESTMENTS BY LOGISTICS & TRANSPORTATION COMPANIES IN INTELLIGENT AUTOMATION TO PROPEL MARKET

- TABLE 25 TRANSPORTATION & LOGISTICS: AUTOMATION COE MARKET, BY REGION, 2020-2027 (USD MILLION)

- 8.6 IT & ITES

- 8.6.1 GROWING USE OF AUTOMATION SOLUTIONS TO AUTOMATE REPETITIVE TASKS TO PROMOTE MARKET

- TABLE 26 IT & ITES: AUTOMATION COE MARKET, BY REGION, 2020-2027 (USD MILLION)

- 8.7 HEALTHCARE & LIFE SCIENCES

- 8.7.1 INCREASING VOLUME OF PATIENT DATA TO INCREASE ADOPTION OF AUTOMATION SOLUTIONS IN HEALTHCARE VERTICAL

- TABLE 27 HEALTHCARE & LIFE SCIENCES: AUTOMATION COE MARKET, BY REGION, 2020-2027 (USD MILLION)

- 8.8 OTHER VERTICALS

- TABLE 28 OTHER VERTICALS: AUTOMATION COE MARKET, BY REGION, 2020-2027 (USD MILLION)

9 AUTOMATION COE MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.1.1 REGION: AUTOMATION COE MARKET DRIVERS

- FIGURE 25 ASIA PACIFIC TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 26 INDIA TO REGISTER HIGHEST GROWTH IN AUTOMATION COE MARKET

- TABLE 29 AUTOMATION COE MARKET, BY REGION, 2020-2027 (USD MILLION)

- 9.2 NORTH AMERICA

- 9.2.1 NORTH AMERICA: REGULATIONS

- 9.2.1.1 Health Insurance Portability and Accountability Act (HIPAA)

- 9.2.1.2 Gramm-Leach-Bliley Act (GLB Act)

- 9.2.1.3 Health Information Technology for Economic and Clinical Health (HITECH) Act

- 9.2.1.4 Sarbanes-Oxley (SOX) Act

- 9.2.1.5 United States Securities and Exchange Commission (SEC)

- 9.2.1.6 California Consumer Privacy Act (CCPA)

- 9.2.1.7 Federal Information Security Management Act (FISMA)

- 9.2.1.8 Federal Information Processing Standards (FIPS)

- FIGURE 27 NORTH AMERICA: MARKET SNAPSHOT

- TABLE 30 NORTH AMERICA: AUTOMATION COE MARKET, BY SERVICE, 2020-2027 (USD MILLION)

- TABLE 31 NORTH AMERICA: AUTOMATION COE MARKET, BY ORGANIZATION SIZE, 2020-2027 (USD MILLION)

- TABLE 32 NORTH AMERICA: AUTOMATION COE MARKET, BY VERTICAL, 2020-2027 (USD MILLION)

- TABLE 33 NORTH AMERICA: AUTOMATION COE MARKET, BY COUNTRY, 2020-2027 (USD MILLION)

- 9.2.2 US

- 9.2.2.1 Rapid growth in technological innovations and rising need to automate business operations to drive market

- 9.2.3 CANADA

- 9.2.3.1 High adoption of automation-based technologies to reduce errors to boost market

- 9.2.1 NORTH AMERICA: REGULATIONS

- 9.3 EUROPE

- 9.3.1 EUROPE: REGULATIONS

- 9.3.1.1 European Market Infrastructure Regulation (EMIR)

- 9.3.1.2 General Data Protection Regulation (GDPR)

- 9.3.1.3 European Committee for Standardization (CEN)

- 9.3.1.4 European Technical Standards Institute (ETSI)

- TABLE 34 EUROPE: AUTOMATION COE MARKET, BY SERVICE, 2020-2027 (USD MILLION)

- TABLE 35 EUROPE: AUTOMATION COE MARKET, BY ORGANIZATION SIZE, 2020-2027 (USD MILLION)

- TABLE 36 EUROPE: AUTOMATION COE MARKET, BY VERTICAL, 2020-2027 (USD MILLION)

- TABLE 37 EUROPE: AUTOMATION COE MARKET, BY COUNTRY, 2020-2027 (USD MILLION)

- 9.3.2 UK

- 9.3.2.1 Increased investments and presence of major automation COE vendors to support growth

- 9.3.3 GERMANY

- 9.3.3.1 Significant demand for automation solutions across various sectors to fuel growth

- 9.3.4 FRANCE

- 9.3.4.1 Rising digital transformation across key verticals to automate business operations to boost growth

- 9.3.5 REST OF EUROPE

- 9.3.1 EUROPE: REGULATIONS

- 9.4 ASIA PACIFIC

- 9.4.1 ASIA PACIFIC: REGULATIONS

- 9.4.1.1 Office of the Privacy Commissioner for Personal Data (PCPD)

- 9.4.1.2 Act on the Protection of Personal Information (APPI)

- 9.4.1.3 Critical Information Infrastructure (CII)

- 9.4.1.4 International Organization for Standardization (ISO) 27001

- 9.4.1.5 Personal Data Protection Act (PDPA)

- FIGURE 28 ASIA PACIFIC: MARKET SNAPSHOT

- TABLE 38 ASIA PACIFIC: AUTOMATION COE MARKET, BY SERVICE, 2020-2027 (USD MILLION)

- TABLE 39 ASIA PACIFIC: AUTOMATION COE MARKET, BY ORGANIZATION SIZE, 2020-2027 (USD MILLION)

- TABLE 40 ASIA PACIFIC: AUTOMATION COE MARKET, BY VERTICAL, 2020-2027 (USD MILLION)

- TABLE 41 ASIA PACIFIC: AUTOMATION COE MARKET, BY COUNTRY, 2020-2027 (USD MILLION)

- 9.4.2 INDIA

- 9.4.2.1 Increased adoption of automation technologies to enhance business processes to build market

- 9.4.3 JAPAN

- 9.4.3.1 Innovative IT infrastructure and rising government investments in innovative technologies to drive growth

- 9.4.4 CHINA

- 9.4.4.1 Growing government investments to leverage innovative technologies to aid growth

- 9.4.5 REST OF ASIA PACIFIC

- 9.4.1 ASIA PACIFIC: REGULATIONS

- 9.5 REST OF THE WORLD

- TABLE 42 REST OF THE WORLD: AUTOMATION COE MARKET, BY SERVICE, 2020-2027 (USD MILLION)

- TABLE 43 REST OF THE WORLD: AUTOMATION COE MARKET, BY ORGANIZATION SIZE, 2020-2027 (USD MILLION)

- TABLE 44 REST OF THE WORLD: AUTOMATION COE MARKET, BY VERTICAL, 2020-2027 (USD MILLION)

- TABLE 45 REST OF THE WORLD: AUTOMATION COE MARKET, BY REGION, 2020-2027 (USD MILLION)

- 9.5.1 MIDDLE EAST & AFRICA

- 9.5.1.1 Growing adoption of RPA by BFSI sector to propel market

- 9.5.2 LATIN AMERICA

- 9.5.2.1 Major shift toward digitalization in recent years to support growth

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- 10.2 KEY PLAYER STRATEGIES

- TABLE 46 OVERVIEW OF STRATEGIES ADOPTED BY KEY AUTOMATION COE VENDORS

- 10.3 MARKET EVALUATION FRAMEWORK

- FIGURE 29 MARKET EVALUATION FRAMEWORK: EXPANSIONS & CONSOLIDATION IN AUTOMATION COE MARKET BETWEEN 2019-2022

- 10.4 REVENUE ANALYSIS

- 10.4.1 HISTORICAL REVENUE ANALYSIS

- FIGURE 30 REVENUE ANALYSIS OF KEY PLAYERS, 2019-2021 (USD MILLION)

- 10.5 RANKING OF KEY MARKET PLAYERS, 2022

- FIGURE 31 RANKING OF KEY PLAYERS, 2022

- 10.6 COMPARATIVE ANALYSIS OF KEY VENDORS IN AUTOMATION COE MARKET, 2022

- FIGURE 32 AUTOMATION COE MARKET: COMPARATIVE ANALYSIS OF KEY PLAYERS

- FIGURE 33 AUTOMATION COE MARKET: COMPARATIVE ANALYSIS OF OTHER KEY PLAYERS

- TABLE 47 AUTOMATION COE MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMES

- TABLE 48 AUTOMATION COE MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- 10.7 COMPETITIVE SCENARIO AND TRENDS

- 10.7.1 PRODUCT LAUNCHES

- TABLE 49 PRODUCT & SERVICE LAUNCHES, 2019-2022

- 10.7.2 DEALS

- TABLE 50 DEALS, 2019-2022

11 COMPANY PROFILES

- 11.1 INTRODUCTION

- (Business Overview, Products/Solutions/Services Offered, Recent Developments, MnM view (Key strengths/Right to win, Strategic choices made, Weakness/competitive threats)**

- 11.2 KEY PLAYERS

- 11.2.1 SS&C BLUE PRISM

- TABLE 51 SS&C BLUE PRISM: BUSINESS OVERVIEW

- FIGURE 34 SS&C BLUE PRISM: COMPANY SNAPSHOT (2021)

- TABLE 52 SS&C BLUE PRISM: PRODUCT LAUNCHES & UPGRADES

- TABLE 53 SS&C BLUE PRISM: DEALS

- 11.2.2 UIPATH

- TABLE 54 UIPATH: BUSINESS OVERVIEW

- FIGURE 35 UIPATH: COMPANY SNAPSHOT (2022)

- TABLE 55 UIPATH: PRODUCT LAUNCHES & UPGRADES

- TABLE 56 UIPATH: DEALS

- 11.2.3 AUTOMATION ANYWHERE

- TABLE 57 AUTOMATION ANYWHERE: BUSINESS OVERVIEW

- TABLE 58 AUTOMATION ANYWHERE: PRODUCT LAUNCHES & UPGRADES

- TABLE 59 AUTOMATION ANYWHERE: DEALS

- 11.2.4 NICE

- TABLE 60 NICE: BUSINESS OVERVIEW

- FIGURE 36 NICE: COMPANY SNAPSHOT (2021)

- TABLE 61 NICE: PRODUCT LAUNCHES & DEALS

- TABLE 62 NICE: DEALS

- 11.2.5 DIGITAL WORKFORCE

- TABLE 63 DIGITAL WORKFORCE: BUSINESS OVERVIEW

- FIGURE 37 DIGITAL WORKFORCE: COMPANY SNAPSHOT (2021)

- TABLE 64 DIGITAL WORKFORCE: DEALS

- 11.2.6 HELPSYSTEMS

- TABLE 65 HELPSYSTEMS: BUSINESS OVERVIEW

- TABLE 66 HELPSYSTEMS: PRODUCT LAUNCHES & UPGRADES

- TABLE 67 HELPSYSTEMS: DEALS

- 11.3 OTHER PLAYERS

- 11.3.1 CTRL365

- 11.3.2 FASTPATH

- 11.3.3 ELECTRONEEK

- 11.3.4 ANYROBOT

- 11.3.5 NINTEX

- 11.3.6 CHAZEY PARTNERS

- 11.3.7 SMARTBRIDGE

- 11.3.8 BLUEPRINT

- 11.3.9 ROBOCLOUD

- 11.3.10 VERINT

- 11.3.11 CIGNITI

- 11.3.12 INNOMINDS

- 11.3.13 TESTINGXPERTS

- 11.3.14 KIWIQA

- 11.3.15 CIGNEX

- 11.3.16 ROBOYO

- 11.3.17 CALIDAD INFOTECH

- 11.3.18 CHOICEWORX

- 11.3.19 XENONSTACK

- *Details on Business Overview, Products/Solutions/Services Offered, Recent Developments, MnM view (Key strengths/Right to win, Strategic choices made, Weakness/competitive threats)** might not be captured in case of unlisted companies.

12 ADJACENT AND RELATED MARKETS

- 12.1 INTRODUCTION

- 12.2 INTELLIGENT PROCESS AUTOMATION MARKET - GLOBAL FORECAST TO 2027

- 12.2.1 MARKET DEFINITION

- 12.2.2 MARKET OVERVIEW

- 12.2.2.1 Intelligent process automation market, by component

- TABLE 68 INTELLIGENT PROCESS AUTOMATION MARKET, BY COMPONENT, 2016-2021 (USD MILLION)

- TABLE 69 INTELLIGENT PROCESS AUTOMATION MARKET, BY COMPONENT, 2022-2027 (USD MILLION)

- 12.2.2.2 Intelligent process automation market, by application

- TABLE 70 INTELLIGENT PROCESS AUTOMATION MARKET, BY APPLICATION, 2016-2021 (USD MILLION)

- TABLE 71 INTELLIGENT PROCESS AUTOMATION MARKET, BY APPLICATION, 2022-2027 (USD MILLION)

- 12.2.2.3 Intelligent process automation market, by business function

- TABLE 72 INTELLIGENT PROCESS AUTOMATION MARKET, BY BUSINESS FUNCTION, 2016-2021 (USD MILLION)

- TABLE 73 INTELLIGENT PROCESS AUTOMATION MARKET, BY BUSINESS FUNCTION, 2022-2027 (USD MILLION)

- 12.2.2.4 Intelligent process automation market, by deployment mode

- TABLE 74 INTELLIGENT PROCESS AUTOMATION MARKET, BY DEPLOYMENT MODE, 2016-2021 (USD MILLION)

- TABLE 75 INTELLIGENT PROCESS AUTOMATION MARKET, BY DEPLOYMENT MODE, 2022-2027 (USD MILLION)

- 12.2.2.5 Intelligent process automation market, by organization size

- TABLE 76 INTELLIGENT PROCESS AUTOMATION MARKET, BY ORGANIZATION SIZE, 2016-2021 (USD MILLION)

- TABLE 77 INTELLIGENT PROCESS AUTOMATION MARKET SIZE, BY ORGANIZATION SIZE, 2022-2027 (USD MILLION)

- 12.2.2.6 Intelligent process automation market, by vertical

- TABLE 78 INTELLIGENT PROCESS AUTOMATION MARKET, BY VERTICAL, 2016-2021 (USD MILLION)

- TABLE 79 INTELLIGENT PROCESS AUTOMATION MARKET, BY VERTICAL, 2022-2027 (USD MILLION)

- 12.2.2.7 Intelligent process automation market, by region

- TABLE 80 INTELLIGENT PROCESS AUTOMATION MARKET, BY REGION, 2016-2021 (USD MILLION)

- TABLE 81 INTELLIGENT PROCESS AUTOMATION MARKET, BY REGION, 2022-2027 (USD MILLION)

- 12.3 RPA AND HYPERAUTOMATION MARKET - GLOBAL FORECAST TO 2027

- 12.3.1 MARKET DEFINITION

- 12.3.2 MARKET OVERVIEW

- 12.3.2.1 RPA and hyperautomation market, by component

- TABLE 82 RPA AND HYPERAUTOMATION MARKET, BY COMPONENT, 2019-2021 (USD MILLION)

- TABLE 83 RPA AND HYPERAUTOMATION MARKET, BY COMPONENT, 2022-2027 (USD MILLION)

- 12.3.2.2 RPA and hyperautomation market, by deployment mode

- TABLE 84 RPA AND HYPERAUTOMATION MARKET, BY DEPLOYMENT MODE, 2019-2021 (USD MILLION)

- TABLE 85 RPA AND HYPERAUTOMATION MARKET, BY DEPLOYMENT MODE, 2022-2027 (USD MILLION)

- 12.3.2.3 RPA and hyperautomation market, by organization size

- TABLE 86 RPA AND HYPERAUTOMATION MARKET, BY ORGANIZATION SIZE, 2019-2021 (USD MILLION)

- TABLE 87 RPA AND HYPERAUTOMATION MARKET, BY ORGANIZATION SIZE, 2022-2027 (USD MILLION)

- 12.3.2.4 RPA and hyperautomation market, by business function

- TABLE 88 RPA AND HYPERAUTOMATION MARKET, BY BUSINESS FUNCTION, 2019-2021 (USD MILLION)

- TABLE 89 RPA AND HYPERAUTOMATION MARKET, BY BUSINESS FUNCTION, 2022-2027 (USD MILLION)

- 12.3.2.5 RPA and hyperautomation market, by vertical

- TABLE 90 RPA AND HYPERAUTOMATION MARKET, BY VERTICAL, 2019-2021 (USD MILLION)

- TABLE 91 RPA AND HYPERAUTOMATION MARKET, BY VERTICAL, 2022-2027 (USD MILLION)

- 12.3.2.6 RPA and hyperautomation market, by region

- TABLE 92 RPA AND HYPERAUTOMATION MARKET, BY REGION, 2019-2021 (USD MILLION)

- TABLE 93 RPA AND HYPERAUTOMATION MARKET, BY REGION, 2022-2027 (USD MILLION)

13 APPENDIX

- 13.1 INSIGHTS FROM INDUSTRY EXPERTS

- 13.2 DISCUSSION GUIDE

- 13.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.4 AVAILABLE CUSTOMIZATIONS

- 13.5 RELATED REPORTS

- 13.6 AUTHOR DETAILS