|

|

市場調査レポート

商品コード

1604567

世界のビール市場:2025年~2030年の予測Global Beer Market - Forecasts from 2025 to 2030 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 世界のビール市場:2025年~2030年の予測 |

|

出版日: 2024年11月08日

発行: Knowledge Sourcing Intelligence

ページ情報: 英文 123 Pages

納期: 即日から翌営業日

|

全表示

- 概要

- 目次

世界のビール市場はCAGR4.62%で成長し、2025年の8,320億1,200万米ドルから、2030年には1兆429億3,000万米ドルになると推定されます。

ビールは世界中で広く飲まれているアルコール飲料です。穀類、水、穀物、酵母を一定時間発酵させることによって作られます。独特の味と香りを出すために、ハーブや果物が頻繁に加えられます。ビールのアルコール濃度は3%未満から40%(ABV)まで、スタイルや原料によって異なります。適量を飲めば、ビールは動脈硬化、狭心症、脳卒中、心臓発作などの心臓や循環器系の病気を減らすのに役立つことが実証されています。

他のアルコール飲料と比較すると、ビールは市場シェアが大きく、その多様な配合、フレーバー、味の提供により、ミレニアル世代やZ世代の間で人気が高まっています。当初、フレーバー・ビールは主に欧州と北米で消費されていましたが、近年その需要は世界的に拡大しており、ビール業界全体に大きな利益をもたらしています。発展途上国における革新的な醸造技術の採用も、消費習慣にプラスの影響を与えています。さらに、顧客は斬新でバラエティに富んだおいしい商品を求めるようになっており、ビール市場の拡大を後押ししています。

世界のビール醸造所の増加や世界のビール需要の高まりなど、いくつかの主要な理由が世界のビール市場を牽引しています。また、低アルコール飲料の人気は着実に高まっており、健康志向の消費者からの需要の高まりに伴い、ノンアルコールビールや限定ビールの売上も増加しています。新製品の登場による消費者の選好の変化も、予測期間中の市場拡大を後押しすると予測されます。また、低アルコール・ビールが高アルコール・ビール、特にアルコール度数2.8%以下のものよりも安価になっていることも、市場拡大の原動力となっています。この状況は特にスウェーデンなどの欧州諸国で顕著で、ビールメーカーは低アルコール製品別の改善を試みています。しかし、ビールの宣伝を制限する州法が、市場全体の拡大を妨げています。

世界のビール市場の促進要因

- 世界のビール醸造の増加

世界のビール醸造所の増加は、ビールの生産と需要を促進すると予想されます。ビール醸造所とは、様々な種類のビールを製造する企業やビジネスのことです。The Brewers Association of the USAは、その報告書の中で、国内のビール醸造所の総数は過去数年間で増加したと述べています。同協会によると、2021年、全米のビール醸造所の総数は約9,384で、そのうち約9,210がクラフトビール醸造所でした。2022年には国内の総醸造所数は9,824に増加し、そのうち約9,675がクラフトビール醸造所でした。同協会は2023年、米国では醸造所の総数が前年比約0.8%増の9,906に達し、そのうちクラフトビール醸造所は約9,761に上ると発表しました。

同様に、Brewers of Europeはその報告書の中で、この地域の活動中の醸造所数は2022年に12,879を記録し、2021年の12,738から増加したと述べました。同機関はさらに、2022年にはフランスがこの地域で最も醸造所数が多く、約2,500の醸造所が活動しており、次いで英国とドイツがそれぞれ1,830と1,507の醸造所を有していると述べました。

世界のビール市場の地理的展望

- 欧州が世界のビール市場の主要シェアを占めると予測されます。

最も大きな割合を占めるのは欧州と予測されます。多くの欧州諸国において、ビールは重要な文化の一部です。欧州連合は世界で最も重要なビール生産地域のひとつです。Brewers of Europeによると、2022年には4億194万5,000ヘクトリットルのビールが生産されました。欧州は、ビールやその他のアルコール飲料の最大の生産国と消費国のひとつです。ドイツ、英国、フランス、スペインのような国々は、世界最大のビール生産者の本拠地です。

本レポートを購入する理由:

- 洞察に満ちた分析:顧客セグメント、政府政策と社会経済要因、消費者選好、産業別、その他のサブセグメントに焦点を当て、主要地域および新興地域を網羅した詳細な市場考察を得ることができます。

- 競合情勢:世界の主要企業が採用している戦略的作戦を理解し、適切な戦略による市場浸透の可能性を理解することができます。

- 市場促進要因と将来動向:ダイナミックな要因と極めて重要な市場動向、そしてそれらが今後の市場展開をどのように形成していくかを探ります。

- 行動可能な提言:ダイナミックな環境の中で、新たなビジネスストリームと収益を発掘するための戦略的意思決定に洞察を活用します。

- 幅広い利用者に対応:新興企業、研究機関、コンサルタント、中小企業、大企業にとって有益で費用対効果が高いです。

どのような用途で利用されていますか?

業界および市場考察、事業機会評価、製品需要予測、市場参入戦略、地理的拡大、設備投資決定、規制の枠組みと影響、新製品開拓、競合の影響

調査範囲

- 2022年から2030年までの過去データ・予測

- 成長機会、課題、サプライチェーンの展望、規制枠組み、顧客行動、およびトレンド分析

- 競合のポジショニング、戦略、および市場シェア分析

- セグメントおよび各国を含む地域の収益成長および予測分析

- 企業のプロファイリング(戦略、製品、財務状況、主な発展など)

目次

第1章 イントロダクション

- 市場概要

- 市場の定義

- 調査範囲

- 市場セグメンテーション

- 通貨

- 前提条件

- 基準年と予測年のタイムライン

- 利害関係者にとっての主要なメリット

第2章 調査手法

- 調査デザイン

- 調査プロセス

第3章 エグゼクティブサマリー

- 主要な調査結果

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 業界バリューチェーン分析

- アナリストビュー

第5章 世界のビール市場:タイプ別

- イントロダクション

- ラガー

- エール

- スタウト

- その他

第6章 世界のビール市場:パッケージング別

- イントロダクション

- ボトル

- 缶

第7章 世界のビール市場:流通チャネル別

- イントロダクション

- オントレード

- オフトレード

第8章 世界のビール市場:地域別

- イントロダクション

- 北米

- タイプ別

- パッケージング別

- 流通チャネル別

- 国別

- 南米

- タイプ別

- パッケージング別

- 流通チャネル別

- 国別

- 欧州

- タイプ別

- パッケージング別

- 流通チャネル別

- 国別

- 中東・アフリカ

- タイプ別

- パッケージング別

- 流通チャネル別

- 国別

- アジア太平洋

- タイプ別

- パッケージング別

- 流通チャネル別

- 国別

第9章 競合環境と分析

- 主要企業と戦略分析

- 市場シェア分析

- 合併、買収、合意、コラボレーション

- 競合ダッシュボード

第10章 企業プロファイル

- Anheuser-Busch InBev

- Beijing Enterprises Holdings Limited

- Carlsberg Group

- Diageo PLC

- Dogfish Head Craft Brewery, Inc

- Heineken Holding NV

- Sierra Nevada Brewing Co.

- The Boston Beer Company, Inc

- Som Distilleries and Breweries Ltd.

- B9 Beverages Pvt. Ltd.

- Adie Broswon Group

- Brauerei Aldersbach GmbH

- Privatbrauerei Ayinger

- ABK Beer

- Brimstage Brewery Co. Ltd.

The global beer market is estimated to grow at a CAGR of 4.62%, from US$832.012 billion in 2025 to US$1,042.93 billion in 2030.

Beer is a widely consumed alcoholic beverage around the world. It's made by the fermentation of cereal, water, grains, and yeast for a specific amount of time. Herbs and fruits are frequently added to the drink to give it a distinctive taste and fragrance. Beer has an alcohol concentration that ranges from less than 3% to 40% by volume (ABV), depending on the style and ingredients used in the formulation. When consumed in moderation, beer has been demonstrated to help reduce heart and circulatory system diseases such as atherosclerosis, angina, stroke, and heart attack.

Beer, when compared to other alcoholic beverages, has a significant market share and is growing in popularity among millennials and Gen Z, thanks to its diverse formulations, flavors, and taste offerings. Initially, flavored beer was primarily consumed in Europe and North America, but its demand has been expanding worldwide in recent years, significantly benefiting the total beer industry. The introduction of innovative brewing technologies in developing nations has also positively impacted consumption habits. Furthermore, customers are increasingly seeking novel, varied, and delicious products, driving the beer market's expansion.

Several primary reasons, including an increase in breweries worldwide and the rising global beer demand, are driving the global beer market. Additionally, the popularity of low-alcohol beverages has risen steadily, and revenues of no-alcohol and limited beer have increased in conjunction with the growing demand from health-conscious consumers. Changing consumer tastes as a result of the new products are also predicted to boost market expansion over the forecast period. Another motivator is that low-alcohol beers are now less expensive than their high-alcohol counterparts, particularly those with an ABV of 2.8 percent or less. The situation is particularly prevalent in European countries such as Sweden, where brewers are attempting to improve the low alcohol by-product. However, provincial legislation restricting beer promotion stifles the entire market's expansion.

Global beer market drivers

- Increasing beer brewing across the globe.

The increase in the global breweries of beer is expected to propel the production and demand for beer. A brewery is a company or business which produces various types of beers. The Brewers Association of the USA, in its report, stated that the total count of breweries in the nation witnessed an increase over the past few years. The association stated that in 2021, the total brewery in the nation was recorded at about 9,384, of which about 9,210 were craft brewers. The total brewery count in the country increased to 9,824 in 2022, with about 9,675 craft breweries. In 2023, the association stated that in the USA, the total count of brewers reached 9,906, an increase of about 0.8% over the past year, which included about 9,761 craft breweries.

Similarly, in its report, the Brewers of Europe stated that the region's count of active breweries was recorded at 12,879 in 2022, which increased from 12,738 breweries in 2021. The agency further stated that in 2022, France had the highest number of brewers in the region, with about 2,500 active breweries, followed by the UK and Germany, having 1,830 and 1,507 breweries, respectively.

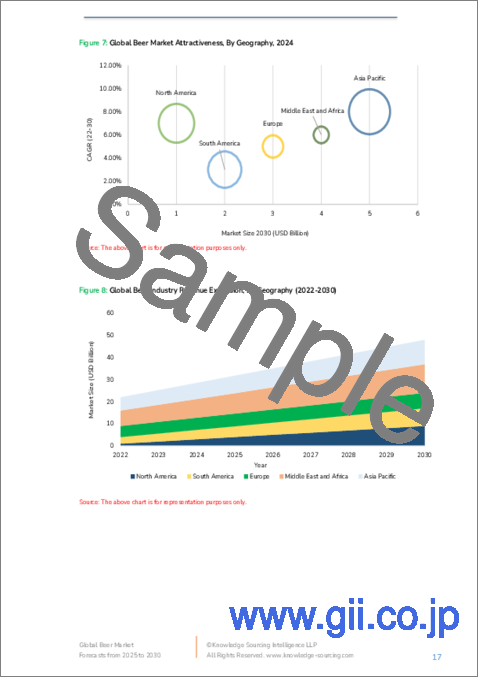

Global beer market geographical outlook

- Europe is forecasted to hold a major share of the global beer market.

The largest proportion is projected to be held by Europe. Beer is an important part of the culture in many European countries. The European Union is one of the world's most important beer-producing regions. As per the Brewers of Europe, 401,945 thousand hectoliters of beer were produced in 2022. Europe is among the biggest producers and consumers of beer and other alcoholic beverages. Countries like Germany, the UK, France, and Spain are home to some of the world's biggest beer producers.

Reasons for buying this report:-

- Insightful Analysis: Gain detailed market insights covering major as well as emerging geographical regions, focusing on customer segments, government policies and socio-economic factors, consumer preferences, industry verticals, other sub- segments.

- Competitive Landscape: Understand the strategic maneuvers employed by key players globally to understand possible market penetration with the correct strategy.

- Market Drivers & Future Trends: Explore the dynamic factors and pivotal market trends and how they will shape up future market developments.

- Actionable Recommendations: Utilize the insights to exercise strategic decision to uncover new business streams and revenues in a dynamic environment.

- Caters to a Wide Audience: Beneficial and cost-effective for startups, research institutions, consultants, SMEs, and large enterprises.

What do businesses use our reports for?

Industry and Market Insights, Opportunity Assessment, Product Demand Forecasting, Market Entry Strategy, Geographical Expansion, Capital Investment Decisions, Regulatory Framework & Implications, New Product Development, Competitive Intelligence

Report Coverage:

- Historical data & forecasts from 2022 to 2030

- Growth Opportunities, Challenges, Supply Chain Outlook, Regulatory Framework, Customer Behaviour, and Trend Analysis

- Competitive Positioning, Strategies, and Market Share Analysis

- Revenue Growth and Forecast Assessment of segments and regions including countries

- Company Profiling (Strategies, Products, Financial Information, and Key Developments among others)

The Global Beer market is segmented and analyzed as follows:

By Type

- Lager

- Ale

- Stouts

- Others

By Packaging

- Bottle

- Can

By Distribution Channel

- On-trade

- Off-trade

By Geography

- North America

- USA

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- Russia

- Germany

- UK

- Spain

- Poland

- France

- Italy

- Others

- Middle East and Africa

- Middle East

- South Africa

- Namibia

- Rest of Africa

- Asia Pacific

- China

- Japan

- India

- South Korea

- Vietnam

- Thailand

- Australia

- Philippines

- Others

TABLE OF CONTENTS

1. INTRODUCTION

- 1.1. Market Overview

- 1.2. Market Definition

- 1.3. Scope of the Study

- 1.4. Market Segmentation

- 1.5. Currency

- 1.6. Assumptions

- 1.7. Base and Forecast Years Timeline

- 1.8. Key benefits for the stakeholders

2. RESEARCH METHODOLOGY

- 2.1. Research Design

- 2.2. Research Process

3. EXECUTIVE SUMMARY

- 3.1. Key Findings

4. MARKET DYNAMICS

- 4.1. Market Drivers

- 4.2. Market Restraints

- 4.3. Porter's Five Forces Analysis

- 4.3.1. Bargaining Power of Suppliers

- 4.3.2. Bargaining Power of Buyers

- 4.3.3. The Threat of New Entrants

- 4.3.4. Threat of Substitutes

- 4.3.5. Competitive Rivalry in the Industry

- 4.4. Industry Value Chain Analysis

- 4.5. Analyst View

5. GLOBAL BEER MARKET BY TYPE

- 5.1. Introduction

- 5.2. Lager

- 5.3. Ale

- 5.4. Stouts

- 5.5. Others

6. GLOBAL BEER MARKET BY PACKAGING

- 6.1. Introduction

- 6.2. Bottle

- 6.3. Can

7. GLOBAL BEER MARKET BY DISTRIBUTION CHANNEL

- 7.1. Introduction

- 7.2. On-trade

- 7.3. Off-trade

8. GLOBAL BEER MARKET BY GEOGRAPHY

- 8.1. Introduction

- 8.2. North America

- 8.2.1. By Type

- 8.2.2. By Packaging

- 8.2.3. By Distribution Channel

- 8.2.4. By Country

- 8.2.4.1. United States

- 8.2.4.2. Canada

- 8.2.4.3. Others

- 8.3. South America

- 8.3.1. By Type

- 8.3.2. By Packaging

- 8.3.3. By Distribution Channel

- 8.3.4. By Country

- 8.3.4.1. Brazil

- 8.3.4.2. Argentina

- 8.3.4.3. Others

- 8.4. Europe

- 8.4.1. By Type

- 8.4.2. By Packaging

- 8.4.3. By Distribution Channel

- 8.4.4. By Country

- 8.4.4.1. Russia

- 8.4.4.2. Germany

- 8.4.4.3. United Kingdom

- 8.4.4.4. Spain

- 8.4.4.5. Poland

- 8.4.4.6. France

- 8.4.4.7. Italy

- 8.4.4.8. Others

- 8.5. Middle East and Africa

- 8.5.1. By Type

- 8.5.2. By Packaging

- 8.5.3. By Distribution Channel

- 8.5.4. By Country

- 8.5.4.1. Middle East

- 8.5.4.2. South Africa

- 8.5.4.3. Namibia

- 8.5.4.4. Others

- 8.6. Asia Pacific

- 8.6.1. By Type

- 8.6.2. By Packaging

- 8.6.3. By Distribution Channel

- 8.6.4. By Country

- 8.6.4.1. China

- 8.6.4.2. Japan

- 8.6.4.3. India

- 8.6.4.4. South Korea

- 8.6.4.5. Vietnam

- 8.6.4.6. Thailand

- 8.6.4.7. Australia

- 8.6.4.8. Philippines

- 8.6.4.9. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

- 9.1. Major Players and Strategy Analysis

- 9.2. Market Share Analysis

- 9.3. Mergers, Acquisitions, Agreements, and Collaborations

- 9.4. Competitive Dashboard

10. COMPANY PROFILES

- 10.1. Anheuser-Busch InBev

- 10.2. Beijing Enterprises Holdings Limited

- 10.3. Carlsberg Group

- 10.4. Diageo PLC

- 10.5. Dogfish Head Craft Brewery, Inc

- 10.6. Heineken Holding NV

- 10.7. Sierra Nevada Brewing Co.

- 10.8. The Boston Beer Company, Inc

- 10.9. Som Distilleries and Breweries Ltd.

- 10.10. B9 Beverages Pvt. Ltd.

- 10.11. Adie Broswon Group

- 10.12. Brauerei Aldersbach GmbH

- 10.13. Privatbrauerei Ayinger

- 10.14. ABK Beer

- 10.15. Brimstage Brewery Co. Ltd.