|

|

市場調査レポート

商品コード

1557266

ファクトリーオートメーション市場-2024年から2029年までの予測Factory Automation Market - Forecasts from 2024 to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| ファクトリーオートメーション市場-2024年から2029年までの予測 |

|

出版日: 2024年08月23日

発行: Knowledge Sourcing Intelligence

ページ情報: 英文 145 Pages

納期: 即日から翌営業日

|

全表示

- 概要

- 目次

ファクトリーオートメーション市場は、2024年の3,370億6,000万米ドルから2029年には5,204億800万米ドルへと、CAGR9.08%で成長すると予測されています。

この成長は主に、生産性の向上と生産コストの削減に貢献する先端技術と自動制御装置の採用が拡大していることに起因します。さらに、米国や欧州などの新興経済諸国では、熟練労働者の確保が重要な課題となっており、ファクトリーオートメーションがその目的に効果的に役立っています。人工知能やロボットなどの先端技術の浸透が進むにつれ、オートメーションによってマテリアルハンドリングや迅速な生産作業などの活動が促進されるからです。

さらに、5Gワイヤレス技術の発展とインダストリー4.0の導入の高まりが相まって、製薬、自動車、製造などの主要産業において、ファクトリーオートメーションソリューションの需要が予測期間まで高まると予想されています。例えば、世界経済フォーラムによると、サウジアラビアにおける先進製造ハブ戦略の採用は、工場の数を2023年の約1万から2035年までに3万6,000に増やすことを目標としており、その中には今後数年間で完全にオートメーションされる4,000の工場も含まれます。これには、産業部門の多様化を目的とした約2,730億米ドルの投資も含まれます。

さらに、オートメーション機器の貿易の増加は、長期的に市場の成長を大きく押し上げると考えられます。例えば、国際貿易局によると、米国はオートメーション産業にとって重要な技術革新の源であり、2022年には約130億米ドルのオートメーション機器を輸出します。

さらに、企業はファクトリーオートメーションの需要拡大に対応するため、製造能力の増強と新製品ラインの立ち上げに注力しています。例えば、2022年にエマソンは、PACSystems(TM)RSTi-EP CPE 200として知られるプログラマブルオートメーションコントローラ(PAC)の発売を発表しました。この製品はコスト効率に優れ、すぐに使える分析機能を提供し、長期的に効率を高めてユーザーに競争上の優位性をもたらします。

ファクトリーオートメーション市場促進要因

- 世界の産業オートメーション導入の拡大が市場成長を促進すると予想されます。

この市場の成長を支える主要理由の1つは、世界の産業オートメーションの拡大です。産業オートメーションは、産業における人間の介入を最小限に抑え、制御システムと情報技術を組み込んであらゆる産業プロセスを処理します。

さらに、産業用モノのインターネット(IIoT)とインダストリアル4.0の開発は、ロジスティクス・チェーン全体の生産と管理を促進する最新の技術的アプローチであり、それによって産業セグメントのスマートファクトリーオートメーションを生み出しています。さらに、自動車セクターにおけるオートメーションも、今後数年間の主要な促進要因になると予測されています。これには、単調な作業のオートメーションを可能にするロボティック・プロセス・オートメーション(RPA)や、その他の協働目的のためのロボティクスへの拡大における組立ロボットの応用が組み込まれています。さらに、従来の自動車をEVに置き換える流れが強まっていることも、自動車業界における需要増にさらなる原動力を与えると考えられます。

また、Manufacturing Institute(MI)の推定によると、熟練労働力不足の結果、製造部門の未就職者数は全体で210万人に達すると予想されています。このことは、ファクトリーオートメーションの成長と拡大にとって有利な展望を浮き彫りにしており、今後数年間は主要な産業部門に先進技術を取り入れることになります。

さらに、市場における主要開発が予測期間中の市場成長を促進すると予想されます。例えば、2023年にABBは、電力と水産業におけるデジタル変革をサポートすることを対象としたABB Ability(TM)Symphony(R)Plus分散制御システムを発売しました。この製品は、他のオートメーション機能やコア制御システムに干渉することなく、クラウドやエッジへの安全なOPC UA1接続を顧客に記載しています。

ファクトリーオートメーション市場ケーススタディ:

- Xiaomiのケーススタディ

最近の製造業では、技術の進歩が大きな役割を果たしています。企業はポテンシャルを最大限に発揮するために、新しいオートメーション技術に切り替えています。このような状況の中、Xiaomiはスマート生産のコンセプトを取り入れ、際立った革新的な製品でファクトリーオートメーションに向けて重要な一歩を踏み出しました。2023年、Xiaomiの曽学中(Zeng Xuezhong)研究開発・製造責任者は、世界ロボット会議でXiaomiスマートファクトリーの第2段階が完成したことを発表しました。このステップは、技術を利用したスマート製造と産業オートメーションへの飛躍を意味します。

第2段階の範囲はかなり広範で、表面実装技術(SMT)やパッチから、カードテスト、組み立て、完全な機械テスト、そして最終的に完成品のパッケージングに至る方法を網羅しています。このプロセスは生産工程を容易に増やし、生産工程をより速くします。同社の第2段階は第1段階の10倍の規模です。この成長は、スマート製造とファクトリーオートメーションに対するXiaomiの自信とコミットメントを反映したものと考えられます。同社は2024年にスマート生産能力を使った生産を開始する準備が整っています。

Xiaomi・スマート・ファクトリーの第2フェーズの実施は、スマートオートメーションと産業オートメーションのセグメントでの拡大の具体的な証拠です。さらに、このセグメントでのXiaomiのリーダーシップと革新的なアプローチは、新技術の世界を形成し、製造業に技術を含めるための重要な一歩です。この開発は、スマート製造システムが生産プロセスに影響を与え、産業オートメーションとイノベーションを形成するという観点から極めて重要です。

Xiaomiは、スマート製造であり、可能な限り労働力を使わない無人の次世代スマート工場の建設を計画しています。同社はまた、生産ラインを拡大するために中国政府と協定を結んでいます。Xiaomi初の電気自動車工場は北京郊外に建設される予定です。新しいファクトリーオートメーション技術を使い、Xiaomiは電気自動車セグメントで最大の飛躍を遂げる計画です。Xiaomiは北京経済技術開発区委員会(BDA)と提携し、製造工場を建設します。

したがって、ケーススタディの結論として、同社は電気自動車の製造と新技術ソリューションの開発に重点を置いています。これは、ファクトリーオートメーションのような新進気鋭の新技術の主要セグメントとして期待されています。

ファクトリーオートメーション市場の主要開発:

- 2024年4月-FANUC Americaはシカゴで開催された「Automate 2024」において、コボット、ロボット、AI、モーションコントロールのイノベーションの新製品群を展示しました。

- 2023年4月-Okuma America Corporationは、米国ノースカロライナ州に本社を置く新しいファクトリーオートメーション部門を立ち上げました。この部門は、労働力不足に対処するためにオートメーションシステムの導入を求める製造業者の需要に対応します。

主要市場セグメンテーション:

ファクトリーオートメーション市場は以下のようにセグメント化され、分析されています。

製品タイプ別

- センサー

- モーション&ドライブ

- 産業用制御システム

- 製造実行システム

- ソフトウェア

- その他

オートメーションタイプ別

- 定置型

- プログラム可能

- フレキシブル

業界別

- 石油・ガス

- 製薬

- 自動車

- エネルギー・電力

- 印刷・包装

- 化学

- 製造

- その他

地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他

- 中東中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- イスラエル

- その他

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- インドネシア

- タイ

- その他

目次

第1章 イントロダクション

- 市場概要

- 市場の定義

- 調査範囲

- 市場セグメンテーション

- 通貨

- 前提条件

- 基準年と予測年のタイムライン

- 利害関係者にとっての主要メリット

第2章 調査手法

- 調査デザイン

- 調査プロセス

第3章 エグゼクティブサマリー

- 主要調査結果

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 業界バリューチェーン分析

- アナリストビュー

- ケーススタディ

- Xiaomiのケーススタディ

- Mitsubishi Electric(Mahindra & Mahindra)のケーススタディ

- Mitsubishi Electric(JR Machine)の事例

- Parker Hannifin PneumaticsとL&T Technology Servicesのケーススタディ

- Rockwell Automationのケーススタディ

第5章 ファクトリーオートメーション市場:製品タイプ別

- イントロダクション

- センサー

- モーション&ドライブ

- 産業用制御システム

- 製造実行システム

- ソフトウェア

- その他

第6章 ファクトリーオートメーション市場:オートメーションタイプ別

- イントロダクション

- 定置型

- プログラム可能

- フレキシブル

第7章 ファクトリーオートメーション市場:業界別

- イントロダクション

- 石油・ガス

- 製薬

- 自動車

- エネルギーと電力

- 印刷と包装

- 化学薬品

- 製造業

- その他

第8章 ファクトリーオートメーション市場:地域別

- イントロダクション

- 北米

- 製品タイプ別

- オートメーションタイプ別

- 業界別

- 国別

- 南米

- 製品タイプ別

- オートメーションタイプ別

- 業界別

- 国別

- 欧州

- 製品タイプ別

- オートメーションタイプ別

- 業界別

- 国別

- 中東・アフリカ

- 製品タイプ別

- オートメーションタイプ別

- 業界別

- 国別

- アジア太平洋

- 製品タイプ別

- オートメーションタイプ別

- 業界別

- 国別

第9章 競合環境と分析

- 主要企業と戦略分析

- 市場シェア分析

- 合併、買収、合意とコラボレーション

- 競合ダッシュボード

第10章 企業プロファイル

- Siemens AG

- Honeywell International

- Rockwell Automation

- Schneider Electric

- Ametek Inc

- Emerson Process Management

- Bosch Automation

- General Electric

- Johnson Controls

- ABB Ltd

The factory automation market is expected to grow at a compound annual growth rate (CAGR) of 9.08%, from US$337.060 billion in 2024 to US$520.408 billion in 2029.

This growth is mainly attributed to the growing adoption of advanced technologies and automatic control devices that contribute to enhanced productivity and reduced production costs. Additionally, in developed economies such as the United States and Europe, the availability of skilled labor is a significant issue where factory automation effectively serves the purpose. This is because, with the rising penetration of advanced technologies such as artificial intelligence and robots, among others, automation facilitates activities such as material handling and quick production tasks.

Furthermore, the development of 5G wireless technology coupled with the rising adoption of Industry 4.0 is anticipated to drive the demand for factory automation solutions until the forecast period in key industries such as pharmaceutical, automotive, and manufacturing. For instance, according to the World Economic Forum, the adoption of the Advanced Manufacturing Hub Strategy in Saudi Arabia targets to increase the number of factories to 36,000 by 2035 from around 10,000 in 2023, including 4000 factories to be fully automated in upcoming years. This also includes an investment of around US$273 billion aimed at diversification of the industrial sector.

Moreover, the rising trade in automation equipment will significantly boost market growth in the long term. For instance, as per the International Trade Administration, the United States is a key source of innovation for the automation industry, exporting around $13 billion of automation equipment in 2022.

Furthermore, companies focus on augmenting their manufacturing capabilities and launching new product lines to meet the growing demand for factory automation. For instance, in 2022, Emerson announced the launch of its programmable automation controllers (PAC) known as PACSystems(TM) RSTi-EP CPE 200. The product is cost-effective, provides ready-to-support analytics, and provides users with a competitive advantage with enhanced efficiency in the long term.

FACTORY AUTOMATION MARKET DRIVERS:

- The growing adoption of industrial automation worldwide is expected to propel the market growth.

One of the prime reasons supporting this market's growth is the growing industrial automation worldwide. Industrial automation minimizes human intervention in industry and incorporates control systems and information technologies to handle all industrial processes.

Moreover, the development of the Industrial Internet of Things (IIoT) and Industrial 4.0 are the latest technological approaches that foster the production and management of the entire logistics chain, thereby giving rise to smart factory automation in the industrial sector. Moreover, automation in the automotive sector is also anticipated to be a major driving factor in the upcoming years. This incorporates the application of assembly robots in expansion to robotic process automation (RPA) that empowers automation of monotonous tasks, and robotics for other collaborative purposes. Moreover, the increasing drift of replacing traditional vehicles with EVs will give additional driving force to the rising demand within the automotive industry.

Besides, according to estimates from the Manufacturing Institute (MI), the overall number of unfulfilled occupations in the manufacturing division is anticipated to reach 2.1 million, a result of the lack of a skilled labor force. This highlights favorable prospects for factory automation's growth and expansion, incorporating advanced technologies in major industrial sectors in the upcoming years.

Additionally, key developments in the market are expected to propel market growth during the forecast period. For instance, in 2023, ABB launched its ABB Ability(TM) Symphony(R) Plus distributed control system, which targets to support digital transformation in the power and water industries. The product provides customers with a secure OPC UA1 connection to the cloud and edge without interference with other automation functionalities and core control systems.

Factory Automation Market Case Study:

- Xiaomi case study

Technological advancements are playing a huge role in manufacturing these days. Companies are switching towards new automation techniques to reach their maximum potential. In this context, Xiaomi took an important step towards factory automation with innovative products that stand out and embrace the concept of smart production. In 2023, Xiaomi's Zeng Xuezhong, responsible for research, development, and manufacturing, announced at the World Robot Conference that the company had completed the second phase of Xiaomi Smart Factory. This step signifies the leap toward smart manufacturing and industrial automation using technology.

The scope of the second phase was quite extensive, and it encompasses a method spanning from Surface Mount Technology (SMT) and patches to card testing, assembly, complete machine testing, and finally, finished product packaging. This process will increase the production process easily and will make the production process faster. The company's phase two was 10 times the size of phase one. This growth will reflect Xiaomi's confidence and commitment to smart manufacturing and factory automation. The company is ready to start its production using smart production capacity in 2024.

The implementation of Xiaomi Smart Factory's second phase is concrete evidence of the expansion in the field of smart automation and industrial automation. Additionally, Xiaomi's leadership and innovative approach in this area is a significant step in shaping the world for new technology and including technology in manufacturing. This development is pivotal from the point of view that smart manufacturing systems influence the production process and also shape industrial automation and innovation.

Xiaomi plans to build unmanned next-generation smart factories that are smart manufacturing and involve as little labor as possible. The company has also signed agreements with the Chinese government to expand its production line. Xiaomi's first electric car factory will be built in the suburbs of Beijing. Using its new factory automation technology, Xiaomi plans to take the biggest leap in the electronics vehicle segment. Xiaomi has partnered with the Beijing Economic-Technological Development Area Committee (BDA) to build a manufacturing plant.

Hence, to conclude the case study, the company is heavily focused on manufacturing and developing new technological solutions for electric vehicles. This is expected to be the major area of focus with new up-and-coming technology like factory automation.

Factory Automation Market Key Developments:

- April 2024- FANUC America showcased its new range of cobots, robots, AI, and motion control innovation at the "Automate 2024" in Chicago. Through its new offerings, the company aims to help start-ups and OEMs enhance their productivity and reduce labor restraints.

- April 2023- Okuma America Corporation launched its new factory automation division, headquartered in North Carolina, USA. This division will cater to the demand for manufacturers seeking automation system adoption to address labor shortages.

Key Market Segmentation:

The Factory Automation Market is segmented and analyzed as below:

By Product Type

- Sensors

- Motion & Drives

- Industrial Control System

- Manufacturing Execution Systems

- Software

- Others

By Automation Type

- Fixed

- Programmable

- Flexible

By Industry Vertical

- Oil and Gas

- Pharmaceutical

- Automotive

- Energy and Power

- Printing and Packaging

- Chemical

- Manufacturing

- Others

By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- UAE

- Israel

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Indonesia

- Thailand

- Others

TABLE OF CONTENTS

1. INTRODUCTION

- 1.1. Market Overview

- 1.2. Market Definition

- 1.3. Scope of the Study

- 1.4. Market Segmentation

- 1.5. Currency

- 1.6. Assumptions

- 1.7. Base and Forecast Years Timeline

- 1.8. Key benefits for the stakeholders

2. RESEARCH METHODOLOGY

- 2.1. Research Design

- 2.2. Research Process

3. EXECUTIVE SUMMARY

- 3.1. Key Findings

4. MARKET DYNAMICS

- 4.1. Market Drivers

- 4.2. Market Restraints

- 4.3. Porter's Five Forces Analysis

- 4.3.1. Bargaining Power of Suppliers

- 4.3.2. Bargaining Power of Buyers

- 4.3.3. Threat of New Entrants

- 4.3.4. Threat of Substitutes

- 4.3.5. Competitive Rivalry in the Industry

- 4.4. Industry Value Chain Analysis

- 4.5. Analyst view

- 4.6. Case Studies

- 4.6.1. Xiaomi case study

- 4.6.2. Mitsubishi Electric (Mahindra & Mahindra) case study

- 4.6.3. Mitsubishi Electric (JR Machine) case study

- 4.6.4. Parker Hannifin Pneumatics and L&T Technology Services case study

- 4.6.5. Rockwell Automation case study

5. FACTORY AUTOMATION MARKET BY PRODUCT TYPE

- 5.1. Introduction

- 5.2. Sensors

- 5.3. Motion & Drives

- 5.4. Industrial Control System

- 5.5. Manufacturing Execution Systems

- 5.6. Software

- 5.7. Others

6. FACTORY AUTOMATION MARKET BY AUTOMATION TYPE

- 6.1. Introduction

- 6.2. Fixed

- 6.3. Programmable

- 6.4. Flexible

7. FACTORY AUTOMATION MARKET BY INDUSTRY VERTICAL

- 7.1. Introduction

- 7.2. Oil and Gas

- 7.3. Pharmaceutical

- 7.4. Automotive

- 7.5. Energy and Power

- 7.6. Printing and Packaging

- 7.7. Chemical

- 7.8. Manufacturing

- 7.9. Others

8. FACTORY AUTOMATION MARKET BY GEOGRAPHY

- 8.1. Introduction

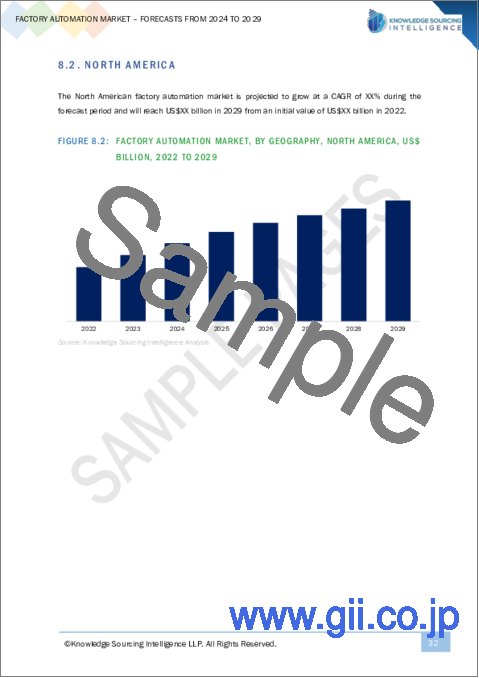

- 8.2. North America

- 8.2.1. By Product Type

- 8.2.2. By Automation Type

- 8.2.3. By Industry Vertical

- 8.2.4. By Country

- 8.2.4.1. United States

- 8.2.4.2. Canada

- 8.2.4.3. Mexico

- 8.3. South America

- 8.3.1. By Product Type

- 8.3.2. By Automation Type

- 8.3.3. By Industry Vertical

- 8.3.4. By Country

- 8.3.4.1. Brazil

- 8.3.4.2. Argentina

- 8.3.4.3. Others

- 8.4. Europe

- 8.4.1. By Product Type

- 8.4.2. By Automation Type

- 8.4.3. By Industry Vertical

- 8.4.4. By Country

- 8.4.4.1. United Kingdom

- 8.4.4.2. Germany

- 8.4.4.3. France

- 8.4.4.4. Italy

- 8.4.4.5. Spain

- 8.4.4.6. Others

- 8.5. Middle East and Africa

- 8.5.1. By Product Type

- 8.5.2. By Automation Type

- 8.5.3. By Industry Vertical

- 8.5.4. By Country

- 8.5.4.1. Saudi Arabia

- 8.5.4.2. UAE

- 8.5.4.3. Israel

- 8.5.4.4. Others

- 8.6. Asia Pacific

- 8.6.1. By Product Type

- 8.6.2. By Automation Type

- 8.6.3. By Industry Vertical

- 8.6.4. By Country

- 8.6.4.1. China

- 8.6.4.2. Japan

- 8.6.4.3. India

- 8.6.4.4. South Korea

- 8.6.4.5. Indonesia

- 8.6.4.6. Thailand

- 8.6.4.7. Others

9. COMPETITIVE ENVIRONMENT AND ANALYSIS

- 9.1. Major Players and Strategy Analysis

- 9.2. Market Share Analysis

- 9.3. Mergers, Acquisitions, Agreements, and Collaborations

- 9.4. Competitive Dashboard

10. COMPANY PROFILES

- 10.1. Siemens AG

- 10.2. Honeywell International

- 10.3. Rockwell Automation

- 10.4. Schneider Electric

- 10.5. Ametek Inc

- 10.6. Emerson Process Management

- 10.7. Bosch Automation

- 10.8. General Electric

- 10.9. Johnson Controls

- 10.10. ABB Ltd