|

|

市場調査レポート

商品コード

1789277

C4ISRの世界市場規模、シェア、動向分析:タイプ別、業界別、最終用途別、用途別、コンポーネント別、地域別、展望と予測、2025~2032年Global C4ISR Market Size, Share & Industry Analysis Report By Type, By Vertical, By End Use, By Application, By Component, By Regional Outlook and Forecast, 2025 - 2032 |

||||||

|

|||||||

|

|||||||

| C4ISRの世界市場規模、シェア、動向分析:タイプ別、業界別、最終用途別、用途別、コンポーネント別、地域別、展望と予測、2025~2032年 |

|

出版日: 2025年07月18日

発行: KBV Research

ページ情報: 英文 561 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

C4ISRの市場規模は、予測期間中に4.7%のCAGRで市場成長し、2032年までに1,814億9,000万米ドルに達すると予想されています。

主なハイライト:

- 北米市場は2024年にC4ISR市場を独占し、2024年には38.00%の収益シェアを占めました。

- 米国市場は北米におけるリーダーシップを維持し、2032年までに512億7,000万米ドルの市場規模に達すると予測されています。

- タイプ別では、新規設置が世界市場を独占し、2024年には56.57%の収益シェアを占めました。

- 業界別では、防衛・軍事が2032年までに収益シェア71.68%と予測され、世界市場をリードすると予想されています。

- 航空セグメントは2024年に主要な最終用途として浮上し、35.56%の収益シェアを獲得し、予測期間中その優位性を維持すると予測されています。

- 用途別では、情報・監視・偵察は、2032年に425億9,000万米ドルの市場規模で成長する見込みで、予測期間を通じてその優位な地位を維持すると予測されています。

- コンポーネント別では、ハードウェアが2024年に979億8,000万米ドルの市場規模を獲得し、このセグメントは予測期間中その地位を維持すると思われます。

近年、市場は大きな変化を経験し、防衛計画や技術面の見直しに影響を与えてきました。通信・指揮システムの改善を目的として、その起源は冷戦時代にまで遡ります。設計面では、初期のC4ISRシステムはハードウェアをベースとしており、各要素は独立して機能していました。実際、これらの要素は以前は無線通信とシンプルなデータ処理ツールを使用していました。

C4ISRの現代的な変化

- C4ISRの現代段階は、衛星通信、GPU、ネットワーク操作の使用によって特徴づけられました。

- 現代のシナリオでは、C4ISRシステムは軍隊がさまざまな状況を理解し、それに応じて戦略的な行動を計画するのに役立ちます。

- 緊張と紛争が高まっている現在の状況では、統合C4ISRが各国の焦点の不可欠な部分になりつつあり、それによってより適切かつ迅速な意思決定を支援しています。

人工知能と機械学習の役割

- 軍事情報管理は、AIと機械学習テクノロジーを搭載したC4ISRシステムから大きな恩恵を受けました。

- このようなツールは、活動を計画するのに役立つだけでなく、兵士や将校の物理的な作業負荷を軽減するのにも役立ちます。

- これらのシステムは、さまざまな不利な状況に関する予測的な脅威警告を提供することで警報メカニズムを強化し、最小限の人間の介入でシステムが自ら判断を下して機能できるようにします。

サイバー防衛と電子戦への焦点

- C4ISRシステムは本質的にデジタルネットワークに大きく依存しているため、サイバー攻撃を受けやすくなります。

- サイバーリスクに対処するため、防衛グループは指揮システムを保護するための強力なサイバーセキュリティ機能を追加しており、現在ではサイバー防御はC4ISRシステムの不可欠な部分となっています。

大手防衛企業の戦略

- Northrop Grumman、Lockheed Martin、BAE Systems、Thales Groupなどの大手防衛企業にとって、研究開発は重要な投資重点分野です。

- AIを活用した信号インテリジェンス、センサー融合、量子通信などの新技術は、これらの企業の中心的な焦点であり、それによって大きな改善がもたらされます。

軍事力への影響

- こうした進歩により、軍隊に新たな強みと能力がもたらされています。

- この分野への一連の投資により、各国に防衛・安全保障分野の最先端技術が提供されています。

大手防衛企業間の統合と、新規参入企業による破壊的技術の投入により、この市場における競合は熾烈になっています。 Raytheon Technologies、Saab、Leonardoといった企業は、技術力だけでなく、相互運用性、費用対効果、そして導入後のサポートにも力を入れています。主要企業は防衛関連の契約を強力に掌握していますが、アジア太平洋地域や中東の様々な国々が、官民連携を通じて自国開発に取り組んでいます。

様々な戦略的ルートの中でも、パートナーシップ契約は主要な開発戦略であり、市場シナリオを形成し、エンドユーザーのダイナミックな需要に対応しています。2025年5月、L3Harris Technologies, Inc.はAirbusと提携し、同社の先進システムをMQ-72C無人補給ヘリコプターに統合しました。この協業は、米国海兵隊の柔軟な指揮統制能力をサポートし、航空補給コネクタプログラムに基づくラピッドプロトタイピングの支援により、戦闘中の即応性を高め、ミッションの柔軟性を高めます。

KBV Cardinal matrix - C4ISR市場の競争分析

KBV Cardinal matrixに示された分析によると、Lockheed Martin Corporation、RTX Corporation、Northrop Grumman Corporation、General Dynamics Corporation、BAE Systems PLCがC4ISR市場の先駆者です。2025年6月、Northrop Grumman Corporationは航空宇宙・防衛企業であるHanwha Systemsとの提携を発表し、統合防空ミサイル防衛(IAMD)指揮統制(C2)技術の強化を目指します。NorthropのIBCSシステムとHanwhaの韓国製IAMD C2ソリューションを組み合わせることで、韓国におけるセンサー統合、脅威への対応、そして適応性の高いミッション能力の向上を目指します。L3Harris Technologies, Inc.、Thales Group S.A.、Leonardo SpAなどは、C4ISR市場における主要なイノベーターです。

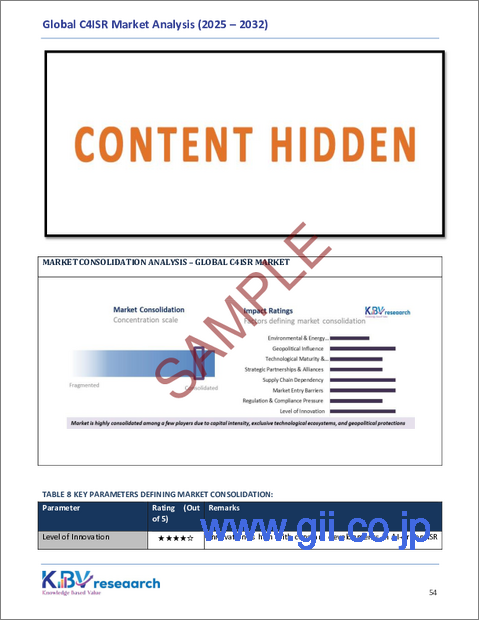

市場統合分析:

世界中のC4ISR市場は、現代の防衛・諜報活動を技術的に強化する上で重要な役割を担っています。政府の深い関与、複雑な調達サイクル、多額の研究開発投資、そして厳格な規制が、C4ISR市場の特徴を形成しています。このエコシステムは、国際的な合弁事業を含む大手防衛関連企業とシステムインテグレーター、防衛専用プラットフォーム、そして長期的な軍事契約を通じて、主に主要な防衛関連請負業者とシステムインテグレーターによって支配されています。C4ISR市場は、多額の資本投資と複雑な規制により、市場統合が急速に進んでいます。市場は、Lockheed Martin、Thales Group、Northrop Grumman、BAE Systems、Raytheon Technologiesなど、数少ない世界のリーディングカンパニーによって支配されています。

パラメータごとの統合評価

革新性

C4ISR宇宙分野は、特に宇宙ベースの監視、AIおよびMLを活用したISR、そして戦略通信システムにおいて、イノベーションを中核としています。主要企業は、自律システム、エッジコンピューティング、そしてマルチドメイン作戦(MDO)統合の分野に多額の投資を行っています。C4ISRシステムにおけるイノベーションは、各国の防衛契約と直接結びついており、閉鎖的なエコシステムの構築につながっています。

根拠:

各国政府からの資金提供と優れた調査プロジェクトは、関連するイノベーションサイクルに影響を与え、方向づけています。こうしたイノベーションは防衛大手企業に集中しており、中小企業やスタートアップ企業による介入は最小限に抑えられています。

主な市場動向:

製品ライフサイクル分析:

技術の進歩、OEM戦略、調達パターン、そして数々のデジタル化の取り組みに支えられ、C4ISR市場は現在、製品ライフサイクル(PLC)の成熟期を迎えています。北米と欧州地域はC4ISRシステムの導入が成熟期にあるのに対し、アジア太平洋地域やラテンアメリカ、中東・アフリカの一部といった新興地域は成長後期から成熟初期への移行期にあります。安定した競合、継続的なイノベーション、高い相互運用性、そしてレガシーシステムの変革が求められています。

C4ISR市場の製品ライフサイクル分析は、利害関係者が市場の現在のライフサイクル段階を理解し、研究開発への投資やその他の戦略的動きに関するより適切な意思決定を行うのに役立ちます。本章では、C4ISR市場の様々な段階について、タイムラインと業界の実例を用いて解説しました。

導入段階

冷戦時代の導入段階では、C4ISRシステムは各国の軍事組織によって独自に開発されました。サイロ化された指揮統制に重点が置かれていたため、初期のシステムでは、初歩的なレーダーシステム、アナログ無線、基本的な信号システムが使用されていました。この段階は、相互運用性が限られており、研究開発投資が高額であったことが特徴でした。

たとえば、1960年代の米国軍の初期のC2ネットワークやNATOの最初の統合防空システムは、この段階の技術を代表しています。

COVID-19の影響分析

COVID-19パンデミックの期間は、世界中で困難な課題をもたらしました。サプライチェーンに混乱が生じ、多くの地域で生産停止に至りました。完全または部分的なロックダウンにより、原材料や完成品の供給が大幅に制限され、多くの配送問題も発生しました。さらに、世界中で健康への懸念が高まったため、企業は人員不足に陥り、生産性が大幅に低下しました。このように、COVID-19は市場に悪影響を及ぼしました。

市場成長要因

C4ISR市場が世界中で成長している主な理由は、先進国と発展途上国の両方が軍事予算を増額し、防衛システムを変革していることです。各国政府は、戦場をインテリジェントに把握する上での最新技術の利点と重要性を認識しており、これにより軍隊は共同作戦においてもより適切かつ迅速な意思決定を行えるようになっています。つまり、より厳格でインテリジェントなセキュリティの必要性、政府の投資意欲、そして防衛力の変革に向けた取り組みが、市場成長の原動力となっているのです。

さらに、AIとMLの軍事指揮統制システムへの導入と影響力の拡大は、C4ISR市場の変革を象徴しています。現代の戦闘はますます複雑化、高速化しており、人々が大量の情報を効率的に管理することは困難になっています。

市場抑制要因

C4ISRは、衛星通信、リアルタイムデータ管理、高度なセンサー、セキュアネットワークといったスマートテクノロジーを基盤としています。C4ISRシステムの設置と運用維持にかかる高額なコストは、C4ISRシステムの市場成長を阻害する大きな要因となっています。新興諸国は、高額なコストという観点から、システムの調達と維持管理において大きな投資課題に直面しています。

バリューチェーン分析

この画像は、技術または防衛システム開発の一般的なバリューチェーンを示しており、研究開発からエンドユーザーサービスとフィードバックループへの明確な進展が示されています。これは研究開発から始まります。ここでは、新しいアイデアとソリューションが概念化され、テストされます。次に、コンポーネント製造がこれらのアイデアを具体的な部品に変換します。これらのコンポーネントはシステム統合中にまとめられ、全体としてまとまった機能を確実にします。次に、統合されたシステムは展開を通じてインストールされ、運用可能になります。展開後、運用と保守のフェーズで、システムがライフサイクル全体にわたってスムーズかつ効率的に実行されるようにします。最後に、エンドユーザーサービスとフィードバックループでユーザーフィードバックを収集してチェーンを閉じます。このフィードバックはさらなる改善に役立ち、バリューチェーン全体にわたって継続的なイノベーションと改良を推進します。

市場シェア分析

タイプ別の展望

タイプ別に、市場は新規設置と改修に分類されます。

新規設置セグメント

新規設置セグメントは、2024年に市場における収益シェアの56.57%を獲得しました。このセグメントは、防衛およびその他の治安部隊向けの全く新しいシステムとインフラの導入を中心に展開されます。こうした展開には、高度な指揮センター、通信ネットワーク、統合監視システムの導入が含まれます。

米国国防総省の統合全ドメイン指揮統制(JADC2)イニシアチブの下、Lockheed Martinは、各軍種を含む統合ソフトウェア定義C4ISRエコシステムの提供において中核的な役割を担っています。

改修セグメント

改修セグメントは、2024年の市場において43.43%という大きな収益シェアを記録しました。このセグメントは、既存のC4ISRシステムのアップグレードと近代化を担い、システムの寿命と有効性の向上に貢献します。世界中で、多くの軍隊がコストを抑え、高度な技術と能力を備えるために、C4ISRシステムの改修を実施しています。

BAE Systemsはこの分野の主要企業の一つであり、強化されたソフトウェア定義無線やデジタルネットワークのインターフェイスなど、高度な指揮統制コンポーネントを英国の装甲車両に搭載する改修を担当しています。

業界別の展望

業界別に、市場は防衛・軍事、政府、および商業に分類されます。

防衛・軍事部門

防衛・軍事分野は2024年に市場収益シェアの73.61%を獲得し、C4ISR市場を牽引しています。軍隊の近代化と国家安全保障への投資増加により、最大の収益源となっています。この分野には、リアルタイム監視ネットワーク、高度な戦場管理ソリューション、軍隊向け戦略的通信などが含まれます。

例えば、Lockheed Martinは、米国国防総省への統合C4ISRソリューションの供給において優位性を維持しています。同社は2024年に戦術情報標的アクセスノード(TITAN)プログラムの展開範囲をさらに拡大し、宇宙基地と地上のセンサーを連携させることで、部隊間で迅速に情報共有することを目指しています。

地域別の展望

地域別に見ると、市場は北米、欧州、アジア太平洋、ラテンアメリカ、中東・アフリカに分割されています。

北米は、2024年に市場収益シェアの38%を記録しました。このセグメントは、潤沢な国防予算と継続的な技術革新に牽引され、C4ISR市場において支配的な地位を占めています。米国は、世界の軍事的優位性を維持するために、指揮統制および監視能力の近代化に多額の投資を行っています。

市場競争と特性

C4ISR市場における競合は依然として激しく、多くの地域企業やニッチ企業が専門的なソリューションを提供していることが背景にあります。新興の防衛関連請負業者、地元のテクノロジー企業、そして革新的なスタートアップ企業は、能力不足を補い、政府との契約を獲得するために絶えず競争を繰り広げています。このダイナミックな情勢は急速な技術進歩を促し、情報収集、監視、指揮システムにおける激しい競争と多様なサービス提供を促進しています。

目次

第1章 市場範囲と調査手法

- 市場の定義

- 目的

- 市場範囲

- セグメンテーション

- 調査手法

第2章 市場要覧

- 主なハイライト

第3章 市場概要

- イントロダクション

- 概要

- 市場に影響を与える主な要因

- 市場促進要因

- 市場抑制要因

- 市場機会

- 市場の課題

第4章 市場動向-世界市場

第5章 競合状況- 世界市場

第6章 競合分析

- KBV Cardinal Matrix

- 最近の業界全体の戦略的展開

- パートナーシップ、コラボレーション、および契約

- 製品の発売と製品の拡大

- 買収と合併

- 地理的拡大

- 市場シェア分析、2024年

- 主要成功戦略

- 主な戦略

- 主要な戦略的動き

- ポーターファイブフォース分析

第7章 C4ISR市場のバリューチェーン分析

- 研究開発(R&D)

- コンポーネント製造

- システム統合

- 展開・インストール

- 運用・保守

- エンドユーザーサービス・フィードバックループ

第8章 主な顧客基準:C4ISR市場

第9章 市場統合分析:世界市場

第10章 世界市場:タイプ別

- 世界の新規設置市場:地域別

- 世界の改修市場:地域別

第11章 世界市場:業界別

- 世界の防衛・軍事市場:地域別

- 世界の政府市場:地域別

- 世界の商業市場:地域別

第12章 世界市場:最終用途別

- 世界の航空市場:地域別

- 世界の海軍市場:地域別

- 世界の陸上市場:地域別

- 世界の宇宙市場:地域別

第13章 世界市場:用途別

- 世界の情報・監視・偵察(ISR)市場:地域別

- 世界の指揮統制市場:地域別

- 世界の通信市場:地域別

- 世界の電子戦市場:地域別

- 世界のコンピュータ市場:地域別

第14章 世界市場:コンポーネント別

- 世界のハードウェア市場:地域別

- 世界のソフトウェア市場:地域別

- 世界のサービス市場:地域別

第15章 世界市場:地域別

- 北米

- 市場動向

- 競合状況

- 主な影響要因

- 北米の市場:国別

- 米国

- カナダ

- メキシコ

- その他北米地域

- 北米の市場:国別

- 欧州

- 市場動向

- 競合状況

- 主な影響要因

- 欧州の市場:国別

- 英国

- ドイツ

- フランス

- ロシア

- スペイン

- イタリア

- その他欧州地域

- 欧州の市場:国別

- アジア太平洋地域

- 市場動向

- 競合状況

- 主な影響要因

- アジア太平洋の市場:国別

- 中国

- 日本

- インド

- 韓国

- シンガポール

- マレーシア

- その他アジア太平洋地域

- アジア太平洋の市場:国別

- ラテンアメリカ・中東・アフリカ

- 市場動向

- 競合状況

- 主な影響要因

- ラテンアメリカ・中東・アフリカの市場:コンポーネント別

- ラテンアメリカ・中東・アフリカの市場:国別

- サウジアラビア

- アルゼンチン

- アラブ首長国連邦

- ブラジル

- 南アフリカ

- ナイジェリア

- その他ラテンアメリカ・中東・アフリカ地域

- ラテンアメリカ・中東・アフリカの市場:国別

第16章 企業プロファイル

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- RTX Corporation

- BAE Systems PLC

- General Dynamics Corporation

- Thales Group SA

- The Boeing Company

- Leonardo SpA(Leonardo DRS, Inc)

- L3Harris Technologies, Inc

- Elbit Systems Ltd

第17章 成功の必須条件

LIST OF TABLES

- TABLE 1 Global C4ISR Market, 2021 - 2024, USD Million

- TABLE 2 Global C4ISR Market, 2025 - 2032, USD Million

- TABLE 3 Partnerships, Collaborations and Agreements- C4ISR Market

- TABLE 4 Product Launches And Product Expansions- C4ISR Market

- TABLE 5 Acquisition and Mergers- C4ISR Market

- TABLE 6 Geographical Expansion- C4ISR Market

- TABLE 7 Key Customer Criteria: C4ISR Market

- TABLE 8 Key Parameters defining Market Consolidation:

- TABLE 9 Global C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 10 Global C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 11 Global New Installation Market by Region, 2021 - 2024, USD Million

- TABLE 12 Global New Installation Market by Region, 2025 - 2032, USD Million

- TABLE 13 Global Retrofit Market by Region, 2021 - 2024, USD Million

- TABLE 14 Global Retrofit Market by Region, 2025 - 2032, USD Million

- TABLE 15 Global C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 16 Global C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 17 Global Defense & Military Market by Region, 2021 - 2024, USD Million

- TABLE 18 Global Defense & Military Market by Region, 2025 - 2032, USD Million

- TABLE 19 Global Government Market by Region, 2021 - 2024, USD Million

- TABLE 20 Global Government Market by Region, 2025 - 2032, USD Million

- TABLE 21 Global Commercial Market by Region, 2021 - 2024, USD Million

- TABLE 22 Global Commercial Market by Region, 2025 - 2032, USD Million

- TABLE 23 Global C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 24 Global C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 25 Global Air Market by Region, 2021 - 2024, USD Million

- TABLE 26 Global Air Market by Region, 2025 - 2032, USD Million

- TABLE 27 Global Naval Market by Region, 2021 - 2024, USD Million

- TABLE 28 Global Naval Market by Region, 2025 - 2032, USD Million

- TABLE 29 Global Ground Market by Region, 2021 - 2024, USD Million

- TABLE 30 Global Ground Market by Region, 2025 - 2032, USD Million

- TABLE 31 Global Space Market by Region, 2021 - 2024, USD Million

- TABLE 32 Global Space Market by Region, 2025 - 2032, USD Million

- TABLE 33 Global C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 34 Global C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 35 Global Intelligence, Surveillance and Reconnaissance (ISR) Market by Region, 2021 - 2024, USD Million

- TABLE 36 Global Intelligence, Surveillance and Reconnaissance (ISR) Market by Region, 2025 - 2032, USD Million

- TABLE 37 Global Command & Control Market by Region, 2021 - 2024, USD Million

- TABLE 38 Global Command & Control Market by Region, 2025 - 2032, USD Million

- TABLE 39 Global Communications Market by Region, 2021 - 2024, USD Million

- TABLE 40 Global Communications Market by Region, 2025 - 2032, USD Million

- TABLE 41 Global Electronic Warfare Market by Region, 2021 - 2024, USD Million

- TABLE 42 Global Electronic Warfare Market by Region, 2025 - 2032, USD Million

- TABLE 43 Global Computers Market by Region, 2021 - 2024, USD Million

- TABLE 44 Global Computers Market by Region, 2025 - 2032, USD Million

- TABLE 45 Global C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 46 Global C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 47 Global Hardware Market by Region, 2021 - 2024, USD Million

- TABLE 48 Global Hardware Market by Region, 2025 - 2032, USD Million

- TABLE 49 Global Software Market by Region, 2021 - 2024, USD Million

- TABLE 50 Global Software Market by Region, 2025 - 2032, USD Million

- TABLE 51 Global Services Market by Region, 2021 - 2024, USD Million

- TABLE 52 Global Services Market by Region, 2025 - 2032, USD Million

- TABLE 53 Global C4ISR Market by Region, 2021 - 2024, USD Million

- TABLE 54 Global C4ISR Market by Region, 2025 - 2032, USD Million

- TABLE 55 North America C4ISR Market, 2021 - 2024, USD Million

- TABLE 56 North America C4ISR Market, 2025 - 2032, USD Million

- TABLE 57 North America C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 58 North America C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 59 North America New Installation Market by Region, 2021 - 2024, USD Million

- TABLE 60 North America New Installation Market by Region, 2025 - 2032, USD Million

- TABLE 61 North America Retrofit Market by Region, 2021 - 2024, USD Million

- TABLE 62 North America Retrofit Market by Region, 2025 - 2032, USD Million

- TABLE 63 North America C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 64 North America C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 65 North America Defense & Military Market by Country, 2021 - 2024, USD Million

- TABLE 66 North America Defense & Military Market by Country, 2025 - 2032, USD Million

- TABLE 67 North America Government Market by Country, 2021 - 2024, USD Million

- TABLE 68 North America Government Market by Country, 2025 - 2032, USD Million

- TABLE 69 North America Commercial Market by Country, 2021 - 2024, USD Million

- TABLE 70 North America Commercial Market by Country, 2025 - 2032, USD Million

- TABLE 71 North America C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 72 North America C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 73 North America Air Market by Country, 2021 - 2024, USD Million

- TABLE 74 North America Air Market by Country, 2025 - 2032, USD Million

- TABLE 75 North America Naval Market by Country, 2021 - 2024, USD Million

- TABLE 76 North America Naval Market by Country, 2025 - 2032, USD Million

- TABLE 77 North America Ground Market by Country, 2021 - 2024, USD Million

- TABLE 78 North America Ground Market by Country, 2025 - 2032, USD Million

- TABLE 79 North America Space Market by Country, 2021 - 2024, USD Million

- TABLE 80 North America Space Market by Country, 2025 - 2032, USD Million

- TABLE 81 North America C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 82 North America C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 83 North America Intelligence, Surveillance and Reconnaissance (ISR) Market by Country, 2021 - 2024, USD Million

- TABLE 84 North America Intelligence, Surveillance and Reconnaissance (ISR) Market by Country, 2025 - 2032, USD Million

- TABLE 85 North America Command & Control Market by Country, 2021 - 2024, USD Million

- TABLE 86 North America Command & Control Market by Country, 2025 - 2032, USD Million

- TABLE 87 North America Communications Market by Country, 2021 - 2024, USD Million

- TABLE 88 North America Communications Market by Country, 2025 - 2032, USD Million

- TABLE 89 North America Electronic Warfare Market by Country, 2021 - 2024, USD Million

- TABLE 90 North America Electronic Warfare Market by Country, 2025 - 2032, USD Million

- TABLE 91 North America Computers Market by Country, 2021 - 2024, USD Million

- TABLE 92 North America Computers Market by Country, 2025 - 2032, USD Million

- TABLE 93 North America C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 94 North America C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 95 North America Hardware Market by Country, 2021 - 2024, USD Million

- TABLE 96 North America Hardware Market by Country, 2025 - 2032, USD Million

- TABLE 97 North America Software Market by Country, 2021 - 2024, USD Million

- TABLE 98 North America Software Market by Country, 2025 - 2032, USD Million

- TABLE 99 North America Services Market by Country, 2021 - 2024, USD Million

- TABLE 100 North America Services Market by Country, 2025 - 2032, USD Million

- TABLE 101 North America C4ISR Market by Country, 2021 - 2024, USD Million

- TABLE 102 North America C4ISR Market by Country, 2025 - 2032, USD Million

- TABLE 103 US C4ISR Market, 2021 - 2024, USD Million

- TABLE 104 US C4ISR Market, 2025 - 2032, USD Million

- TABLE 105 US C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 106 US C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 107 US C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 108 US C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 109 US C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 110 US C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 111 US C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 112 US C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 113 US C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 114 US C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 115 Canada C4ISR Market, 2021 - 2024, USD Million

- TABLE 116 Canada C4ISR Market, 2025 - 2032, USD Million

- TABLE 117 Canada C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 118 Canada C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 119 Canada C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 120 Canada C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 121 Canada C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 122 Canada C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 123 Canada C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 124 Canada C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 125 Canada C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 126 Canada C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 127 Mexico C4ISR Market, 2021 - 2024, USD Million

- TABLE 128 Mexico C4ISR Market, 2025 - 2032, USD Million

- TABLE 129 Mexico C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 130 Mexico C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 131 Mexico C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 132 Mexico C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 133 Mexico C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 134 Mexico C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 135 Mexico C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 136 Mexico C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 137 Mexico C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 138 Mexico C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 139 Rest of North America C4ISR Market, 2021 - 2024, USD Million

- TABLE 140 Rest of North America C4ISR Market, 2025 - 2032, USD Million

- TABLE 141 Rest of North America C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 142 Rest of North America C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 143 Rest of North America C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 144 Rest of North America C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 145 Rest of North America C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 146 Rest of North America C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 147 Rest of North America C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 148 Rest of North America C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 149 Rest of North America C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 150 Rest of North America C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 151 Europe C4ISR Market, 2021 - 2024, USD Million

- TABLE 152 Europe C4ISR Market, 2025 - 2032, USD Million

- TABLE 153 Europe C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 154 Europe C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 155 Europe New Installation Market by Country, 2021 - 2024, USD Million

- TABLE 156 Europe New Installation Market by Country, 2025 - 2032, USD Million

- TABLE 157 Europe Retrofit Market by Country, 2021 - 2024, USD Million

- TABLE 158 Europe Retrofit Market by Country, 2025 - 2032, USD Million

- TABLE 159 Europe C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 160 Europe C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 161 Europe Defense & Military Market by Country, 2021 - 2024, USD Million

- TABLE 162 Europe Defense & Military Market by Country, 2025 - 2032, USD Million

- TABLE 163 Europe Government Market by Country, 2021 - 2024, USD Million

- TABLE 164 Europe Government Market by Country, 2025 - 2032, USD Million

- TABLE 165 Europe Commercial Market by Country, 2021 - 2024, USD Million

- TABLE 166 Europe Commercial Market by Country, 2025 - 2032, USD Million

- TABLE 167 Europe C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 168 Europe C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 169 Europe Air Market by Country, 2021 - 2024, USD Million

- TABLE 170 Europe Air Market by Country, 2025 - 2032, USD Million

- TABLE 171 Europe Naval Market by Country, 2021 - 2024, USD Million

- TABLE 172 Europe Naval Market by Country, 2025 - 2032, USD Million

- TABLE 173 Europe Ground Market by Country, 2021 - 2024, USD Million

- TABLE 174 Europe Ground Market by Country, 2025 - 2032, USD Million

- TABLE 175 Europe Space Market by Country, 2021 - 2024, USD Million

- TABLE 176 Europe Space Market by Country, 2025 - 2032, USD Million

- TABLE 177 Europe C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 178 Europe C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 179 Europe Intelligence, Surveillance and Reconnaissance (ISR) Market by Country, 2021 - 2024, USD Million

- TABLE 180 Europe Intelligence, Surveillance and Reconnaissance (ISR) Market by Country, 2025 - 2032, USD Million

- TABLE 181 Europe Command & Control Market by Country, 2021 - 2024, USD Million

- TABLE 182 Europe Command & Control Market by Country, 2025 - 2032, USD Million

- TABLE 183 Europe Communications Market by Country, 2021 - 2024, USD Million

- TABLE 184 Europe Communications Market by Country, 2025 - 2032, USD Million

- TABLE 185 Europe Electronic Warfare Market by Country, 2021 - 2024, USD Million

- TABLE 186 Europe Electronic Warfare Market by Country, 2025 - 2032, USD Million

- TABLE 187 Europe Computers Market by Country, 2021 - 2024, USD Million

- TABLE 188 Europe Computers Market by Country, 2025 - 2032, USD Million

- TABLE 189 Europe C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 190 Europe C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 191 Europe Hardware Market by Country, 2021 - 2024, USD Million

- TABLE 192 Europe Hardware Market by Country, 2025 - 2032, USD Million

- TABLE 193 Europe Software Market by Country, 2021 - 2024, USD Million

- TABLE 194 Europe Software Market by Country, 2025 - 2032, USD Million

- TABLE 195 Europe Services Market by Country, 2021 - 2024, USD Million

- TABLE 196 Europe Services Market by Country, 2025 - 2032, USD Million

- TABLE 197 Europe C4ISR Market by Country, 2021 - 2024, USD Million

- TABLE 198 Europe C4ISR Market by Country, 2025 - 2032, USD Million

- TABLE 199 UK C4ISR Market, 2021 - 2024, USD Million

- TABLE 200 UK C4ISR Market, 2025 - 2032, USD Million

- TABLE 201 UK C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 202 UK C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 203 UK C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 204 UK C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 205 UK C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 206 UK C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 207 UK C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 208 UK C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 209 UK C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 210 UK C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 211 Germany C4ISR Market, 2021 - 2024, USD Million

- TABLE 212 Germany C4ISR Market, 2025 - 2032, USD Million

- TABLE 213 Germany C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 214 Germany C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 215 Germany C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 216 Germany C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 217 Germany C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 218 Germany C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 219 Germany C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 220 Germany C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 221 Germany C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 222 Germany C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 223 France C4ISR Market, 2021 - 2024, USD Million

- TABLE 224 France C4ISR Market, 2025 - 2032, USD Million

- TABLE 225 France C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 226 France C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 227 France C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 228 France C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 229 France C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 230 France C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 231 France C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 232 France C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 233 France C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 234 France C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 235 Russia C4ISR Market, 2021 - 2024, USD Million

- TABLE 236 Russia C4ISR Market, 2025 - 2032, USD Million

- TABLE 237 Russia C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 238 Russia C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 239 Russia C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 240 Russia C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 241 Russia C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 242 Russia C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 243 Russia C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 244 Russia C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 245 Russia C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 246 Russia C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 247 Spain C4ISR Market, 2021 - 2024, USD Million

- TABLE 248 Spain C4ISR Market, 2025 - 2032, USD Million

- TABLE 249 Spain C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 250 Spain C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 251 Spain C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 252 Spain C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 253 Spain C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 254 Spain C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 255 Spain C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 256 Spain C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 257 Spain C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 258 Spain C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 259 Italy C4ISR Market, 2021 - 2024, USD Million

- TABLE 260 Italy C4ISR Market, 2025 - 2032, USD Million

- TABLE 261 Italy C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 262 Italy C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 263 Italy C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 264 Italy C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 265 Italy C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 266 Italy C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 267 Italy C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 268 Italy C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 269 Italy C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 270 Italy C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 271 Rest of Europe C4ISR Market, 2021 - 2024, USD Million

- TABLE 272 Rest of Europe C4ISR Market, 2025 - 2032, USD Million

- TABLE 273 Rest of Europe C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 274 Rest of Europe C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 275 Rest of Europe C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 276 Rest of Europe C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 277 Rest of Europe C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 278 Rest of Europe C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 279 Rest of Europe C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 280 Rest of Europe C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 281 Rest of Europe C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 282 Rest of Europe C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 283 Asia Pacific C4ISR Market, 2021 - 2024, USD Million

- TABLE 284 Asia Pacific C4ISR Market, 2025 - 2032, USD Million

- TABLE 285 Asia Pacific C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 286 Asia Pacific C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 287 Asia Pacific New Installation Market by Country, 2021 - 2024, USD Million

- TABLE 288 Asia Pacific New Installation Market by Country, 2025 - 2032, USD Million

- TABLE 289 Asia Pacific Retrofit Market by Country, 2021 - 2024, USD Million

- TABLE 290 Asia Pacific Retrofit Market by Country, 2025 - 2032, USD Million

- TABLE 291 Asia Pacific C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 292 Asia Pacific C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 293 Asia Pacific Defense & Military Market by Country, 2021 - 2024, USD Million

- TABLE 294 Asia Pacific Defense & Military Market by Country, 2025 - 2032, USD Million

- TABLE 295 Asia Pacific Government Market by Country, 2021 - 2024, USD Million

- TABLE 296 Asia Pacific Government Market by Country, 2025 - 2032, USD Million

- TABLE 297 Asia Pacific Commercial Market by Country, 2021 - 2024, USD Million

- TABLE 298 Asia Pacific Commercial Market by Country, 2025 - 2032, USD Million

- TABLE 299 Asia Pacific C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 300 Asia Pacific C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 301 Asia Pacific Air Market by Country, 2021 - 2024, USD Million

- TABLE 302 Asia Pacific Air Market by Country, 2025 - 2032, USD Million

- TABLE 303 Asia Pacific Naval Market by Country, 2021 - 2024, USD Million

- TABLE 304 Asia Pacific Naval Market by Country, 2025 - 2032, USD Million

- TABLE 305 Asia Pacific Ground Market by Country, 2021 - 2024, USD Million

- TABLE 306 Asia Pacific Ground Market by Country, 2025 - 2032, USD Million

- TABLE 307 Asia Pacific Space Market by Country, 2021 - 2024, USD Million

- TABLE 308 Asia Pacific Space Market by Country, 2025 - 2032, USD Million

- TABLE 309 Asia Pacific C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 310 Asia Pacific C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 311 Asia Pacific Intelligence, Surveillance and Reconnaissance (ISR) Market by Country, 2021 - 2024, USD Million

- TABLE 312 Asia Pacific Intelligence, Surveillance and Reconnaissance (ISR) Market by Country, 2025 - 2032, USD Million

- TABLE 313 Asia Pacific Command & Control Market by Country, 2021 - 2024, USD Million

- TABLE 314 Asia Pacific Command & Control Market by Country, 2025 - 2032, USD Million

- TABLE 315 Asia Pacific Communications Market by Country, 2021 - 2024, USD Million

- TABLE 316 Asia Pacific Communications Market by Country, 2025 - 2032, USD Million

- TABLE 317 Asia Pacific Electronic Warfare Market by Country, 2021 - 2024, USD Million

- TABLE 318 Asia Pacific Electronic Warfare Market by Country, 2025 - 2032, USD Million

- TABLE 319 Asia Pacific Computers Market by Country, 2021 - 2024, USD Million

- TABLE 320 Asia Pacific Computers Market by Country, 2025 - 2032, USD Million

- TABLE 321 Asia Pacific C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 322 Asia Pacific C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 323 Asia Pacific Hardware Market by Country, 2021 - 2024, USD Million

- TABLE 324 Asia Pacific Hardware Market by Country, 2025 - 2032, USD Million

- TABLE 325 Asia Pacific Software Market by Country, 2021 - 2024, USD Million

- TABLE 326 Asia Pacific Software Market by Country, 2025 - 2032, USD Million

- TABLE 327 Asia Pacific Services Market by Country, 2021 - 2024, USD Million

- TABLE 328 Asia Pacific Services Market by Country, 2025 - 2032, USD Million

- TABLE 329 Asia Pacific C4ISR Market by Country, 2021 - 2024, USD Million

- TABLE 330 Asia Pacific C4ISR Market by Country, 2025 - 2032, USD Million

- TABLE 331 China C4ISR Market, 2021 - 2024, USD Million

- TABLE 332 China C4ISR Market, 2025 - 2032, USD Million

- TABLE 333 China C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 334 China C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 335 China C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 336 China C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 337 China C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 338 China C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 339 China C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 340 China C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 341 China C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 342 China C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 343 Japan C4ISR Market, 2021 - 2024, USD Million

- TABLE 344 Japan C4ISR Market, 2025 - 2032, USD Million

- TABLE 345 Japan C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 346 Japan C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 347 Japan C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 348 Japan C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 349 Japan C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 350 Japan C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 351 Japan C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 352 Japan C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 353 Japan C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 354 Japan C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 355 India C4ISR Market, 2021 - 2024, USD Million

- TABLE 356 India C4ISR Market, 2025 - 2032, USD Million

- TABLE 357 India C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 358 India C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 359 India C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 360 India C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 361 India C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 362 India C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 363 India C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 364 India C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 365 India C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 366 India C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 367 South Korea C4ISR Market, 2021 - 2024, USD Million

- TABLE 368 South Korea C4ISR Market, 2025 - 2032, USD Million

- TABLE 369 South Korea C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 370 South Korea C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 371 South Korea C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 372 South Korea C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 373 South Korea C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 374 South Korea C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 375 South Korea C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 376 South Korea C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 377 South Korea C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 378 South Korea C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 379 Singapore C4ISR Market, 2021 - 2024, USD Million

- TABLE 380 Singapore C4ISR Market, 2025 - 2032, USD Million

- TABLE 381 Singapore C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 382 Singapore C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 383 Singapore C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 384 Singapore C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 385 Singapore C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 386 Singapore C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 387 Singapore C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 388 Singapore C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 389 Singapore C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 390 Singapore C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 391 Malaysia C4ISR Market, 2021 - 2024, USD Million

- TABLE 392 Malaysia C4ISR Market, 2025 - 2032, USD Million

- TABLE 393 Malaysia C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 394 Malaysia C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 395 Malaysia C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 396 Malaysia C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 397 Malaysia C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 398 Malaysia C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 399 Malaysia C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 400 Malaysia C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 401 Malaysia C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 402 Malaysia C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 403 Rest of Asia Pacific C4ISR Market, 2021 - 2024, USD Million

- TABLE 404 Rest of Asia Pacific C4ISR Market, 2025 - 2032, USD Million

- TABLE 405 Rest of Asia Pacific C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 406 Rest of Asia Pacific C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 407 Rest of Asia Pacific C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 408 Rest of Asia Pacific C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 409 Rest of Asia Pacific C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 410 Rest of Asia Pacific C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 411 Rest of Asia Pacific C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 412 Rest of Asia Pacific C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 413 Rest of Asia Pacific C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 414 Rest of Asia Pacific C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 415 LAMEA C4ISR Market, 2021 - 2024, USD Million

- TABLE 416 LAMEA C4ISR Market, 2025 - 2032, USD Million

- TABLE 417 LAMEA C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 418 LAMEA C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 419 LAMEA New Installation Market by Country, 2021 - 2024, USD Million

- TABLE 420 LAMEA New Installation Market by Country, 2025 - 2032, USD Million

- TABLE 421 LAMEA Retrofit Market by Country, 2021 - 2024, USD Million

- TABLE 422 LAMEA Retrofit Market by Country, 2025 - 2032, USD Million

- TABLE 423 LAMEA C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 424 LAMEA C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 425 LAMEA Defense & Military Market by Country, 2021 - 2024, USD Million

- TABLE 426 LAMEA Defense & Military Market by Country, 2025 - 2032, USD Million

- TABLE 427 LAMEA Government Market by Country, 2021 - 2024, USD Million

- TABLE 428 LAMEA Government Market by Country, 2025 - 2032, USD Million

- TABLE 429 LAMEA Commercial Market by Country, 2021 - 2024, USD Million

- TABLE 430 LAMEA Commercial Market by Country, 2025 - 2032, USD Million

- TABLE 431 LAMEA C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 432 LAMEA C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 433 LAMEA Air Market by Country, 2021 - 2024, USD Million

- TABLE 434 LAMEA Air Market by Country, 2025 - 2032, USD Million

- TABLE 435 LAMEA Naval Market by Country, 2021 - 2024, USD Million

- TABLE 436 LAMEA Naval Market by Country, 2025 - 2032, USD Million

- TABLE 437 LAMEA Ground Market by Country, 2021 - 2024, USD Million

- TABLE 438 LAMEA Ground Market by Country, 2025 - 2032, USD Million

- TABLE 439 LAMEA Space Market by Country, 2021 - 2024, USD Million

- TABLE 440 LAMEA Space Market by Country, 2025 - 2032, USD Million

- TABLE 441 LAMEA C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 442 LAMEA C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 443 LAMEA Intelligence, Surveillance and Reconnaissance (ISR) Market by Country, 2021 - 2024, USD Million

- TABLE 444 LAMEA Intelligence, Surveillance and Reconnaissance (ISR) Market by Country, 2025 - 2032, USD Million

- TABLE 445 LAMEA Command & Control Market by Country, 2021 - 2024, USD Million

- TABLE 446 LAMEA Command & Control Market by Country, 2025 - 2032, USD Million

- TABLE 447 LAMEA Communications Market by Country, 2021 - 2024, USD Million

- TABLE 448 LAMEA Communications Market by Country, 2025 - 2032, USD Million

- TABLE 449 LAMEA Electronic Warfare Market by Country, 2021 - 2024, USD Million

- TABLE 450 LAMEA Electronic Warfare Market by Country, 2025 - 2032, USD Million

- TABLE 451 LAMEA Computers Market by Country, 2021 - 2024, USD Million

- TABLE 452 LAMEA Computers Market by Country, 2025 - 2032, USD Million

- TABLE 453 LAMEA C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 454 LAMEA C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 455 LAMEA Hardware Market by Country, 2021 - 2024, USD Million

- TABLE 456 LAMEA Hardware Market by Country, 2025 - 2032, USD Million

- TABLE 457 LAMEA Software Market by Country, 2021 - 2024, USD Million

- TABLE 458 LAMEA Software Market by Country, 2025 - 2032, USD Million

- TABLE 459 LAMEA Services Market by Country, 2021 - 2024, USD Million

- TABLE 460 LAMEA Services Market by Country, 2025 - 2032, USD Million

- TABLE 461 LAMEA C4ISR Market by Country, 2021 - 2024, USD Million

- TABLE 462 LAMEA C4ISR Market by Country, 2025 - 2032, USD Million

- TABLE 463 Saudi Arabia C4ISR Market, 2021 - 2024, USD Million

- TABLE 464 Saudi Arabia C4ISR Market, 2025 - 2032, USD Million

- TABLE 465 Saudi Arabia C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 466 Saudi Arabia C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 467 Saudi Arabia C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 468 Saudi Arabia C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 469 Saudi Arabia C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 470 Saudi Arabia C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 471 Saudi Arabia C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 472 Saudi Arabia C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 473 Saudi Arabia C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 474 Saudi Arabia C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 475 Argentina C4ISR Market, 2021 - 2024, USD Million

- TABLE 476 Argentina C4ISR Market, 2025 - 2032, USD Million

- TABLE 477 Argentina C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 478 Argentina C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 479 Argentina C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 480 Argentina C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 481 Argentina C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 482 Argentina C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 483 Argentina C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 484 Argentina C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 485 Argentina C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 486 Argentina C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 487 UAE C4ISR Market, 2021 - 2024, USD Million

- TABLE 488 UAE C4ISR Market, 2025 - 2032, USD Million

- TABLE 489 UAE C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 490 UAE C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 491 UAE C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 492 UAE C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 493 UAE C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 494 UAE C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 495 UAE C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 496 UAE C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 497 UAE C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 498 UAE C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 499 Brazil C4ISR Market, 2021 - 2024, USD Million

- TABLE 500 Brazil C4ISR Market, 2025 - 2032, USD Million

- TABLE 501 Brazil C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 502 Brazil C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 503 Brazil C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 504 Brazil C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 505 Brazil C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 506 Brazil C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 507 Brazil C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 508 Brazil C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 509 Brazil C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 510 Brazil C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 511 South Africa C4ISR Market, 2021 - 2024, USD Million

- TABLE 512 South Africa C4ISR Market, 2025 - 2032, USD Million

- TABLE 513 South Africa C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 514 South Africa C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 515 South Africa C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 516 South Africa C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 517 South Africa C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 518 South Africa C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 519 South Africa C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 520 South Africa C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 521 South Africa C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 522 South Africa C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 523 Nigeria C4ISR Market, 2021 - 2024, USD Million

- TABLE 524 Nigeria C4ISR Market, 2025 - 2032, USD Million

- TABLE 525 Nigeria C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 526 Nigeria C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 527 Nigeria C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 528 Nigeria C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 529 Nigeria C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 530 Nigeria C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 531 Nigeria C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 532 Nigeria C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 533 Nigeria C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 534 Nigeria C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 535 Rest of LAMEA C4ISR Market, 2021 - 2024, USD Million

- TABLE 536 Rest of LAMEA C4ISR Market, 2025 - 2032, USD Million

- TABLE 537 Rest of LAMEA C4ISR Market by Type, 2021 - 2024, USD Million

- TABLE 538 Rest of LAMEA C4ISR Market by Type, 2025 - 2032, USD Million

- TABLE 539 Rest of LAMEA C4ISR Market by Vertical, 2021 - 2024, USD Million

- TABLE 540 Rest of LAMEA C4ISR Market by Vertical, 2025 - 2032, USD Million

- TABLE 541 Rest of LAMEA C4ISR Market by End Use, 2021 - 2024, USD Million

- TABLE 542 Rest of LAMEA C4ISR Market by End Use, 2025 - 2032, USD Million

- TABLE 543 Rest of LAMEA C4ISR Market by Application, 2021 - 2024, USD Million

- TABLE 544 Rest of LAMEA C4ISR Market by Application, 2025 - 2032, USD Million

- TABLE 545 Rest of LAMEA C4ISR Market by Component, 2021 - 2024, USD Million

- TABLE 546 Rest of LAMEA C4ISR Market by Component, 2025 - 2032, USD Million

- TABLE 547 Key Information - Lockheed Martin Corporation

- TABLE 548 Key Information - Northrop Grumman Corporation

- TABLE 549 Key Information - RTX Corporation

- TABLE 550 Key Information - BAE Systems PLC

- TABLE 551 Key Information - General Dynamics Corporation

- TABLE 552 Key Information - Thales Group S.A.

- TABLE 553 Key Information - The Boeing Company

- TABLE 554 Key information - Leonardo SpA

- TABLE 555 Key information - L3Harris Technologies, Inc.

- TABLE 556 Key Information - Elbit Systems Ltd.

LIST OF FIGURES

- FIG 1 Methodology for the research

- FIG 2 C4ISR Market Evolution

- FIG 3 Global C4ISR Market, 2021 - 2032, USD Million

- FIG 4 Key Factors Impacting C4ISR Market

- FIG 5 Trends in C4ISR Market

- FIG 6 Global C4ISR Market Dynamics

- FIG 7 KBV Cardinal Matrix

- FIG 8 Market Share Analysis, 2024

- FIG 9 Key Leading Strategies: Percentage Distribution (2021-2025)

- FIG 10 Key Strategic Move: (Partnerships, Collaborations & Agreements: 2021, sep - 2025, Jun) Leading Players

- FIG 11 Porter's Five Forces Analysis - C4ISR Market

- FIG 12 Value Chain Analysis of C4ISR Market

- FIG 13 Key Customer Criteria: C4ISR Market

- FIG 14 Market Consolidation Analysis - Global C4ISR Market

- FIG 15 Global C4ISR Market share by Type, 2024

- FIG 16 Global C4ISR Market share by Type, 2032

- FIG 17 Global C4ISR Market by Type, 2021 - 2032, USD Million

- FIG 18 Global C4ISR Market by Vertical, 2024

- FIG 19 Global C4ISR Market by Vertical, 2032

- FIG 20 Global C4ISR Market by Vertical, 2021 - 2032, USD Million

- FIG 21 Global C4ISR Market share by End Use, 2024

- FIG 22 Global C4ISR Market share by End Use, 2032

- FIG 23 Global C4ISR Market by End Use, 2021 - 2032, USD Million

- FIG 24 Global C4ISR Market share by Application, 2024

- FIG 25 Global C4ISR Market share by Application, 2032

- FIG 26 Global C4ISR Market by Application, 2021 - 2032, USD Million

- FIG 27 Global C4ISR Market share by Component, 2024

- FIG 28 Global C4ISR Market by Component, 2032

- FIG 29 Global C4ISR Market by Component, 2021 - 2032, USD Million

- FIG 30 Global C4ISR Market share by Region, 2024

- FIG 31 Global C4ISR Market share by Region, 2032

- FIG 32 Global C4ISR Market by Region, 2021 - 2032, USD Million

- FIG 33 Evolution of North America C4ISR Market

- FIG 34 Key Factors Impacting North America C4ISR Market

- FIG 35 North America C4ISR Market, 2021 - 2032, USD Million

- FIG 36 North America C4ISR Market share by Type, 2024

- FIG 37 North America C4ISR Market share by Type, 2032

- FIG 38 North America C4ISR Market by Type, 2021 - 2032, USD Million

- FIG 39 North America C4ISR Market by Vertical, 2024

- FIG 40 North America C4ISR Market by Vertical, 2032

- FIG 41 North America C4ISR Market by Vertical, 2021 - 2032, USD Million

- FIG 42 North America C4ISR Market share by End Use, 2024

- FIG 43 North America C4ISR Market share by End Use, 2032

- FIG 44 North America C4ISR Market by End Use, 2021 - 2032, USD Million

- FIG 45 North America C4ISR Market share by Application, 2024

- FIG 46 North America C4ISR Market share by Application, 2032

- FIG 47 North America C4ISR Market by Application, 2021 - 2032, USD Million

- FIG 48 North America C4ISR Market share by Component, 2024

- FIG 49 North America C4ISR Market by Component, 2032

- FIG 50 North America C4ISR Market by Component, 2021 - 2032, USD Million

- FIG 51 North America C4ISR Market share by Country, 2024

- FIG 52 North America C4ISR Market share by Country, 2032

- FIG 53 North America C4ISR Market by Country, 2021 - 2032, USD Million

- FIG 54 Key Factors Impacting Europe C4ISR Market

- FIG 55 Europe C4ISR Market, 2021 - 2032, USD Million

- FIG 56 Europe C4ISR Market share by Type, 2024

- FIG 57 Europe C4ISR Market share by Type, 2032

- FIG 58 Europe C4ISR Market by Type, 2021 - 2032, USD Million

- FIG 59 Europe C4ISR Market by Vertical, 2024

- FIG 60 Europe C4ISR Market by Vertical, 2032

- FIG 61 Europe C4ISR Market by Vertical, 2021 - 2032, USD Million

- FIG 62 Europe C4ISR Market share by End Use, 2024

- FIG 63 Europe C4ISR Market share by End Use, 2032

- FIG 64 Europe C4ISR Market by End Use, 2021- 2032, USD Million

- FIG 65 Europe C4ISR Market share by Application, 2024

- FIG 66 Europe C4ISR Market share by Application, 2032

- FIG 67 Europe C4ISR Market by Application, 2021 - 2032, USD Million

- FIG 68 Europe C4ISR Market share by Component, 2024

- FIG 69 Europe C4ISR Market by Component, 2032

- FIG 70 Europe C4ISR Market by Component, 2021 - 2032, USD Million

- FIG 71 Europe C4ISR Market share by Country, 2024

- FIG 72 Europe C4ISR Market share by Country, 2032

- FIG 73 Europe C4ISR Market by Country, 2021 - 2032, USD Million

- FIG 74 Key Factors Impacting Asia Pacific C4ISR Market

- FIG 75 Asia Pacific C4ISR Market, 2021 - 2032, USD Million

- FIG 76 Asia Pacific C4ISR Market share by Type, 2024

- FIG 77 Asia Pacific C4ISR Market share by Type, 2032

- FIG 78 Asia Pacific C4ISR Market by Type, 2021 - 2032, USD Million

- FIG 79 Asia Pacific C4ISR Market by Vertical, 2024

- FIG 80 Asia Pacific C4ISR Market by Vertical, 2032

- FIG 81 Asia Pacific C4ISR Market by Vertical, 2021 - 2032, USD Million

- FIG 82 Asia Pacific C4ISR Market share by End Use, 2024

- FIG 83 Asia Pacific C4ISR Market share by End Use, 2032

- FIG 84 Asia Pacific C4ISR Market by End Use, 2021 - 2032, USD Million

- FIG 85 Asia Pacific C4ISR Market share by Application, 2024

- FIG 86 Asia Pacific C4ISR Market share by Application, 2032

- FIG 87 Asia Pacific C4ISR Market by Application, 2021 - 2032, USD Million

- FIG 88 Asia Pacific C4ISR Market share by Component, 2024

- FIG 89 Asia Pacific C4ISR Market by Component, 2032

- FIG 90 Asia Pacific C4ISR Market by Component, 2021 - 2032, USD Million

- FIG 91 Asia Pacific C4ISR Market share by Country, 2024

- FIG 92 Asia Pacific C4ISR Market share by Country, 2032

- FIG 93 Asia Pacific C4ISR Market by Country, 2021 - 2032, USD Million

- FIG 94 Key Factors Impacting LAMEA C4ISR Market

- FIG 95 LAMEA C4ISR Market, 2021 - 2032, USD Million

- FIG 96 LAMEA C4ISR Market share by Type, 2024

- FIG 97 LAMEA C4ISR Market share by Type, 2032

- FIG 98 LAMEA C4ISR Market by Type, 2021 - 2032, USD Million

- FIG 99 LAMEA C4ISR Market by Vertical, 2024

- FIG 100 LAMEA C4ISR Market by Vertical, 2032

- FIG 101 LAMEA C4ISR Market by Vertical, 2021 - 2032, USD Million

- FIG 102 LAMEA C4ISR Market share by End Use, 2024

- FIG 103 LAMEA C4ISR Market share by End Use, 2032

- FIG 104 LAMEA C4ISR Market by End Use, 2021 - 2032, USD Million

- FIG 105 LAMEA C4ISR Market share by Application, 2024

- FIG 106 LAMEA C4ISR Market share by Application, 2032

- FIG 107 LAMEA C4ISR Market by Application, 2021 - 2032, USD Million

- FIG 108 LAMEA C4ISR Market share by Component, 2024

- FIG 109 LAMEA C4ISR Market by Component, 2032

- FIG 110 LAMEA C4ISR Market by Component, 2021 - 2032, USD Million

- FIG 111 LAMEA C4ISR Market share by Country, 2024

- FIG 112 LAMEA C4ISR Market share by Country, 2032

- FIG 113 LAMEA C4ISR Market by Country, 2021 - 2032, USD Million

- FIG 114 Recent strategies and developments: Lockheed Martin Corporation

- FIG 115 SWOT Analysis: Lockheed Martin Corporation

- FIG 116 SWOT Analysis: Northrop Grumman Corporation

- FIG 117 SWOT Analysis: RTX Corporation

- FIG 118 SWOT Analysis: BAE SYSTEMS PLC

- FIG 119 SWOT Analysis: General Dynamics Corporation

- FIG 120 Recent strategies and developments: Thales Group S.A.

- FIG 121 SWOT Analysis: Thales Group S.A.

- FIG 122 SWOT Analysis: The Boeing Company

- FIG 123 Recent strategies and developments: Leonardo SpA

- FIG 124 SWOT Analysis: Leonardo SpA

- FIG 125 Recent strategies and developments: L3Harris Technologies, Inc.

- FIG 126 SWOT Analysis: L3Harris Technologies, Inc.

- FIG 127 SWOT Analysis: Elbit Systems Ltd.

The Global C4ISR Market size is expected to reach $181.49 billion by 2032, rising at a market growth of 4.7% CAGR during the forecast period.

Key Highlights:

- The North America market dominated Global C4ISR Market in 2024, accounting for a 38.00% revenue share in 2024.

- The U.S. market is projected to maintain its leadership in North America, reaching a market size of USD 51.27 billion by 2032.

- Among the various Type, the New Installation segment dominated the global market, contributing a revenue share of 56.57% in 2024.

- In terms of Vertical, Defense & Military segment are expected to lead the global market, with a projected revenue share of 71.68% by 2032.

- The Air market emerged as the leading End Use in 2024, capturing a 35.56% revenue share, and is projected to retain its dominance during the forecast period.

- The Intelligence, Surveillance and Reconnaissance Market in Application is poised to grow at the market in 2032 with a market size of USD 42.59 billion and is projected to maintain its dominant position throughout the forecast period.

- By Component the Hardware Segment captured the market size of USD 97.98 billion in 2024 and this segment will maintain its position during the forecast period.

The market has experienced a significant change over these years influencing the modifications in the defense plan and on the technology fronts. Its inception dates way back to the cold war to improve communication and command systems. From the design point of view the early C4ISR systems were based on hardware and were quite separate from each other. As a fact these factors previously used radio communication along with simple data processing tools.

Modern Changes in C4ISR

- The modern phase of C4ISR was marked with the use of Satellite communications, GPU and networked operations.

- In the modern scenario, the C4ISR systems assist the military forces in understanding the different situations and accordingly plan their strategic actions.

- In current conditions, with the rising tensions and conflicts, the integrated C4ISR is becoming an integral part of the countries' focus thereby supporting in taking better and faster decisions.

Role of Artificial Intelligence and Machine Learning

- The military intelligence management largely benefited from the C4ISR systems powered by AI and Machine learning technologies.

- Such tools are helpful not only to plan the activities rather also assist in reducing the soldiers and officers' metal workload.

- These systems enhance the alarm mechanisms by providing predictive threat warnings about different unfavorable conditions and allow systems to take decisions and function on their own with minimal human interventions.

Focus on Cyber Defense and Electronic Warfare

- Since by nature, the C4ISR systems are dependent on digital networks majorly, hence are prone to cyber-attacks.

- To deal with the cyber risks, the defense group are adding strong features for cybersecurity to safeguard the command systems and now the cyber defense is an integral part of C4ISR systems.

Strategies for Major Defense Companies

- Research and development is a key investment focus area for the leading defense companies such as Northrop Grumman, Lockheed Martin, BAE Systems and Thales Group.

- New technologies including AI powered signal intelligence, sensor fusion and quantum communication are among the core focus of these companies thereby bringing significant improvements.

Impact on Military Capabilities

- Such advancements are bringing in new strengths and abilities to the military.

- The series of investments in this area is providing cutting edge technology in defense and security sector to various nations.

Consolidation among the leading defense giants and disruptive technologies from the entrants in this market makes the competition in this market intense in its nature. Companies such as Raytheon Technologies, Saab and Leonardo make endeavors not only on the technological prowess but rather on interoperability, cost effectiveness and post-deployment support also. Though, the leading companies are having strong hold on the defense contracts however, various nations in Asia Pacific and Middle East are working through public-private partnerships for indigenous developments.

Among various strategic routes, the Partnerships deal as the key development strategy are shaping the market scenarios thereby catering to the dynamic demands from the end users. In May, 2025, L3Harris Technologies, Inc. partnered with Airbus for the integration of advanced systems from the former onto the MQ-72C unmanned logistics helicopter. This collaboration supports the adaptable command and control capabilities for the U.S Marines thereby enabling the readiness and enhancing the mission flexibility during the contests with the help of rapid prototyping under the Aerial Logistics connector program.

KBV Cardinal Matrix - C4ISR Market Competition Analysis

Based on the Analysis presented in the KBV Cardinal matrix; Lockheed Martin Corporation, RTX Corporation, Northrop Grumman Corporation, General Dynamics Corporation, and BAE Systems PLC are the forerunners in the C4ISR Market. In June, 2025, Northrop Grumman Corporation announced the partnership with Hanwha Systems, an Aerospace and defense company to enhance integrated air and missile defense (IAMD) command-and-control (C2) technologies. They will combine Northrop's IBCS system with Hanwha's Korean IAMD C2 solutions to improve sensor integration, threat engagement, and adaptable mission capabilities in South Korea. Companies such as L3Harris Technologies, Inc., Thales Group S.A., and Leonardo SpA are some of the key innovators in C4ISR Market.

Market Consolidation Analysis:

The C4ISR market worldwide holds a high importance in strengthening the modern defense and intelligence operations technologically. The deep government involvement, complex procurement cycles, high R&D investments and strict regulations shape the characteristics of the C4ISR market. The ecosystem is majorly dominated by the major defense contractors and system integrators via joint ventures including the international ones too, defense exclusive platforms and long-term military contracts. The C4ISR market experience a strong market consolidation owing to the high capital investment requirements and complex regulations. The market is dominated by few global leading players namely Lockheed Martin, Thales Group, Northrop Grumman, BAE Systems and Raytheon Technologies among others.

Parameter-wise Consolidation Evaluation

1. Level of Innovation - ★★★★☆ (4/5)

C4ISR space has innovation at its core especially in space-based surveillance, AI and ML-enabled ISR and strategic communication systems. The key companies are making big investments in the fields of autonomous systems, edge computing and multi-domain operations (MDO) integration. The innovation in C4ISR systems is directly linked with the defense contract from the countries, thereby leading to the closed ecosystems.

Justification:

The funding from the governments across countries and the distinguished research projects influence and direct the related innovation cycles. Such innovations are centralized to the defense primes leading to the minimal intervention from smaller companies and startups.

Key Market Trends:

Product Life Cycle Analysis:

Backed up on the technological advancements, OEM strategies, procurement patterns, and a number of digital initiatives, the global C4ISR market is presently experiencing the maturity stage of Product Life Cycle (PLC). The North America and Europe regions are witnessing the maturity stage of the adoption of C4ISR systems unlike the emerging regions such as Asia Pacific and parts of LAMEA, experiencing transitions between late growth to early maturity phase. Stable competition, regular innovation, high interoperability and transformation of legacy systems.

The Product Life Cycle Analysis of Global C4ISR market assists the stakeholders in understanding the prevailing lifecycle phase of the market thereby taking better decisions pertaining to the investments in R&D and other strategic moves. The chapter discussed various phases of the C4ISR market with timelines and real examples from the industry.

1. Introduction Stage

During the introduction phase, C4ISR systems were developed by military organizations across countries in-house during the Cold War. With the focus on the siloed command and control, such initial systems used rudimentary radar systems, analog radios and basic signal systems. This phase was characterized by limited interoperability and high R&D investments.

For e.g. Early C2 networks of U.S. military in 1960s and the first integrated air defense systems of NATO represented the technologies of this phase.

COVID 19 Impact Analysis

The period of COVID-19 pandemic posed difficult challenges across the world. It disturbed the supply chains and even suspended production in several places. Complete and partial lockdowns heavily restricted the supply of raw materials and finished products, also leading to numerous delivery issues. Further, with health concerns all over, the companies had a very limited workforce leading to the significant reduction in productivity. So, the COVID-19 had a negative influence on the market.

Market Growth Factors

The key reason for the growth of the C4ISR market growth worldwide is that both the developed and developing nations are increasing their military budgets and transforming their defense systems. The governments are acknowledging the benefits and importance of modern age technologies in having an intelligent understanding of battlefield thereby enabling the military to take better and fast decisions while working in joint venture modes also. Conclusively, the requirement of stringer and intelligent security, government intentions for investment and mission to transform the defense forces are the fuel to the market growth.

In addition, the inclusion of AI and ML and its growing influence in military command and control systems marks a transformation in the global C4ISR market. Battles, in the current modern times, are getting more complex and faster, making it difficult for the people to manage the rush of information in an efficient manner.

Market Restraining Factors

The C4ISR is based on smart technologies including satellite communication, real time data management, advanced sensors and secure networks. The high cost involved in installations and maintaining the operations of C4ISR systems poses a major restraint to the market growth of C4ISR systems. Developing countries face huge investment challenges in procuring and maintaining the systems from the point of view of the expensive costs.

Value Chain Analysis

The image illustrates a typical value chain for technology or defense system development, depicting a clear progression from Research & Development to End-User Services & Feedback Loop. It begins with R&D, where new ideas and solutions are conceptualized and tested. Next, Component Manufacturing transforms these ideas into tangible parts. These components are brought together during System Integration, ensuring they work as a cohesive whole. The integrated system is then installed and made operational through Deployment & Installation. After deployment, the Operation & Maintenance phase ensures the system runs smoothly and efficiently over its lifecycle. Finally, End-User Services & Feedback Loop closes the chain by gathering user feedback, which informs further improvements, driving continuous innovation and refinement throughout the value chain.

Market Share Analysis

Type Outlook

Based on Type, the market is segmented into New Installation and Retrofit.

New Installation Segment

The New Installation segment garnered 56.57% revenue share in the market in 2024. The New installation segment revolves around the deployment of completely new systems and infrastructure for defense as well other security forces. Such deployment includes the installation of advanced command centers, communication networks and integrated surveillance systems from the start.

Under the U.S. Department of Defense's Joint All-Domain Command and Control (JADC2) initiative, Lockheed Martin contribute a core role in delivering the integrated software-defined C4ISR ecosystems including service branches.

Retrofit Segment

The Retrofit segment registered a considerable 43.43% revenue share in the market in 2024. This segment takes care of the upgradation and modernization of existing C4ISR systems which helps in enhancing longevity and its effectiveness. Globally, several armed forces get their C4ISR systems retrofitted in order to control costs and to get equipped with advanced technologies and capabilities.

BAE Systems is among the key players in this segment and is responsible for the British armored vehicles' retrofitting with the advanced command and control components such as enhanced software defined radios and interfaces for digital networks.

Vertical Outlook

Based on Vertical, the market is segmented into Defense & Military, Government, and Commercial.

Defense & Military Segment

The Defense & Military segment acquired 73.61% revenue share in the market in 2024 and dominates the C4ISR market in this segment. It accounts for the largest revenue owing to the increased investments in modernization of forces and national security. It includes the real-time surveillance networks, advanced battlefield management solutions and strategic communications for the forces.

For instance, Lockheed Martin maintains its dominance in the supply of integrated C4ISR solutions to the U.S Department of Defense. The company further expanded footprints of its Tactical Intelligence Targeting Access Node (TITAN) program in 2024, to share the intelligence fast across the units via linking space-based and terrestrial sensors.

Regional Outlook

Region-wise, the market is segmented into North America, Europe, Asia Pacific, LAMEA.

The North America segment recorded 38% revenue share in the market in 2024. This segment holds a dominant position in the C4ISR market, driven by substantial defense budgets and continuous technological innovation. The United States invests heavily in modernizing its command, control, and surveillance capabilities to maintain global military superiority.

Market Competition and Attributes

The competition in the C4ISR market remains high, driven by numerous regional and niche companies offering specialized solutions. Emerging defense contractors, local technology firms, and innovative startups constantly compete to fill capability gaps and secure government contracts. This dynamic landscape encourages rapid technological advancements, fostering strong rivalry and diverse offerings across intelligence, surveillance, and command systems.

Recent Strategies Deployed in the Market

- May-2025: Thales Group S.A. unveiled TRAC SIGMA, an L-band radar for military and civilian air traffic control and surveillance with 300 km range, 3D detection, and anti-jamming features, supporting dual-use data sharing.

- Mar-2025: Thales Group S.A. launched the Vehicle Mounted SquadNet Radio (VMSR) to expand secure communications for vehicles, integrating voice and data for dismounted troops and platforms, with MANET, anti-jamming, and dual voice nets.

- Feb-2025: L3Harris Technologies, Inc. introduced Amorphous, a scalable, open-architecture software for coordinating drone swarms autonomously across domains, supporting Pentagon programs like Replicator for resilient uncrewed operations.

- Oct-2024: Leonardo SpA established a new facility at Aberdeen Proving Ground to support U.S. Army programs with labs and integration bays for C4ISR, electronic warfare, and force protection systems, strengthening Army collaboration.

- Oct-2024: Northrop Grumman Corporation partnered with Terma to cooperate on advanced defense technologies including the F-35 fighter, UAVs, EW, radar, and missile defense, enhancing Denmark's defense base and SME collaboration.

- Sep-2024: Leonardo SpA partnered with BAE Systems to develop a demonstrator for the Future Combat Air System (FCAS), boosting UK-Italy ties and complementing ongoing next-gen fighter collaboration discussions with Japan.

List of Key Companies Profiled

- Axis Communications AB (Canon, Inc.)

- Motorola Solutions, Inc.

- Hangzhou Hikvision Digital Technology Co., Ltd.

- Bosch Sicherheitssysteme GmbH (Robert Bosch GmbH)

- Zhejiang Dahua Technology Co., Ltd.

- Sony Semiconductor Solutions Corporation (Sony Corporation)

- Honeywell International Inc.

- Johnson Controls International PLC

- OmniVision Technologies, Inc.

- i-PRO Co., Ltd.

Global C4ISR Market Report Segmentation

By Type

- New Installation

- Retrofit

By Vertical

- Defense & Military

- Government

- Commercial

By End Use

- Air

- Naval

- Ground

- Space

By Application

- Intelligence, Surveillance and Reconnaissance (ISR)

- Command & Control

- Communications

- Electronic Warfare

- Computers

By Component

- Hardware

- Software

- Services

By Geography

- North America

- US

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- UK

- France

- Russia

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Singapore

- Malaysia

- Rest of Asia Pacific

- LAMEA

- Brazil

- Argentina

- UAE

- Saudi Arabia

- South Africa

- Nigeria

- Rest of LAMEA

Table of Contents

Chapter 1. Market Scope & Methodology

- 1.1 Market Definition

- 1.2 Objectives

- 1.3 Market Scope

- 1.4 Segmentation

- 1.4.1 Global C4ISR Market, by Type

- 1.4.2 Global C4ISR Market, by Vertical

- 1.4.3 Global C4ISR Market, by End Use

- 1.4.4 Global C4ISR Market, by Application

- 1.4.5 Global C4ISR Market, by Component

- 1.4.6 Global C4ISR Market, by Geography

- 1.5 Methodology for the research

Chapter 2. Market at a Glance

- 2.1 Key Highlights

Chapter 3. Market Overview

- 3.1 Introduction

- 3.1.1 Overview