|

|

市場調査レポート

商品コード

1785249

医療機器試験・検査・認証アウトソーシングの世界市場規模、シェア、業界分析レポート(サービス別、デバイスクラス別、最終用途別、地域別展望・予測、2025年~2032年)Global Medical Device Testing, Inspection And Certification Outsourcing Market Size, Share & Industry Analysis Report By Service, By Device Class, By End Use, By Regional Outlook and Forecast, 2025 - 2032 |

||||||

|

|||||||

|

|||||||

| 医療機器試験・検査・認証アウトソーシングの世界市場規模、シェア、業界分析レポート(サービス別、デバイスクラス別、最終用途別、地域別展望・予測、2025年~2032年) |

|

出版日: 2025年07月08日

発行: KBV Research

ページ情報: 英文 438 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

医療機器試験・検査・認証アウトソーシング市場規模は、予測期間中に8.3%のCAGRで市場成長し、2032年までに54億8,000万米ドルに達すると予想されています。

主なハイライト:

- 2024年には欧州市場が世界市場を独占し、2024年には収益シェアの39%を占めました。

- 米国の医療機器試験、検査および認証アウトソーシング市場は、北米地域で優位性を維持し、2032年までに市場規模が11億米ドルに達すると予想されています。

- さまざまなデバイスクラスタイプセグメントの中で、クラスIIが世界市場を独占し、2024年には収益シェアの53.4%を占めました。

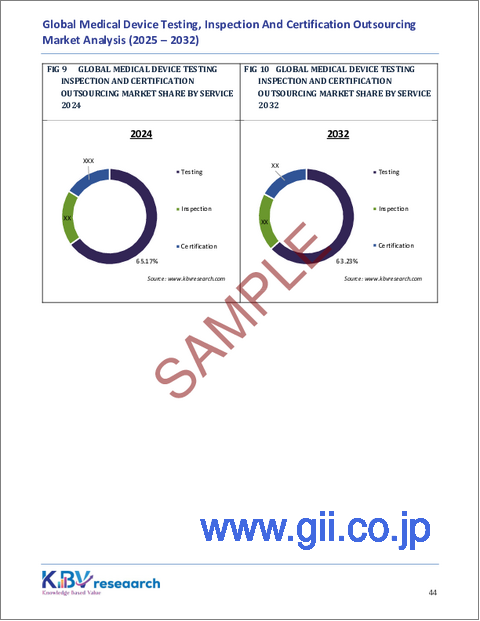

- テストセグメントは2032年にサービスセグメントをリードし、63.2%の収益シェアを獲得し、予測期間中もその優位性を維持すると予測されています。

- さまざまなエンドユーザー分野の中で、2024年に22億9,000万米ドルの収益貢献が見込まれる医療機器企業セグメントが、引き続き優位に立つと予測されています。

医療機器の試験・検査・認証(TIC)アウトソーシング市場は、医療技術の急速な進歩、規制当局の監視強化、そしてヘルスケア製品流通の世界化を背景に、過去数十年間で大きく進化してきました。当初、多くの医療機器メーカーは品質保証と規制遵守のプロセスを社内で管理していました。しかし、機器の複雑性と多様性が増大し、米国食品医薬品局(FDA)、欧州医薬品庁(EMA)、日本のPMDAといった世界の保健当局が厳格なコンプライアンスフレームワークを導入するにつれ、アウトソーシングは戦略的な必要性として浮上しました。

医療機器企業は、国内外の規格への準拠、製品品質の向上、市場投入までの期間短縮を実現するために、サードパーティのTICサービスプロバイダーへの依存度を高め始めました。この傾向は、医療機器の需要が地域間で高まったことにも影響され、メーカーは多様な規制要件を満たす必要が生じ、複数の管轄区域に精通した専門プロバイダーに頼るようになりました。

時間の経過とともに、TIC機能のアウトソーシングは、企業のコスト削減、リスク軽減、そしてイノベーションや製品開発といったコアコンピテンシーへの注力維持に役立ってきました。EUおよび北米の政府保健機関や認証機関は、安全基準や試験プロトコルの策定において重要な役割を果たし、独立した検証と妥当性確認の必要性を改めて認識させています。新興国におけるヘルスケアインフラの拡大と医療機器のデジタル化が進むにつれ、TICアウトソーシングへの依存はさらに高まり、堅調で進化を続ける世界市場が形成されています。

医療機器TICアウトソーシング市場を形成する主要な動向の一つは、デバイスへの先進技術の統合であり、新たな試験能力への切迫したニーズを生み出しています。診断用AIアルゴリズム、遠隔監視用IoTセンサー、ソフトウェア駆動型治療介入を組み込んだデバイスは、サイバーセキュリティ、データ精度、リアルタイム機能について試験する必要があります。従来の試験方法ではこれらの新しいコンポーネントを評価するには不十分であり、TICプロバイダーは競争力を維持するためにハイテクラボとデジタル機能への投資を迫られています。

もう一つの大きなトレンドは、製品リコールや患者の安全への懸念といった世界の出来事を背景に、規制コンプライアンスの重要性が高まっていることです。規制当局は品質保証の基準を引き上げており、FDA 510(k)、CEマーキング、ISO 13485などの認証の取得・維持を目指す企業にとって、独立したTICサービスは不可欠なものとなっています。コンプライアンスはもはや一度きりの活動ではなく、継続的な要件であり、製品ライフサイクル全体を通じてTICプロバイダーとの継続的な連携が求められています。

市場統合分析

世界の医療機器TIC市場は、規制の厳格化、ヘルスケアサプライチェーンの世界化、そして医療機器技術の急速な進歩によって、大きな変革期を迎えています。試験・検査・認証(TIC)サービスは、メーカーと規制当局の双方にとって、製品の安全性、コンプライアンス、そして信頼性を確保するためのものです。これらのサービスが専門化していくにつれ、市場は統合へと向かいつつあり、少数の多国籍TICプロバイダーが、統合型で拡張性に優れ、世界的に調和のとれたソリューションを提供することで市場を独占しています。市場統合は、イノベーション、規制負担、参入障壁、国際的なパートナーシップなど、様々な要因によって形作られており、これら全てが市場力の配分と将来の成長軌道を決定づけます。

1.革新性のレベル- ★★★★☆(4/5)

医療機器TIC市場におけるイノベーションは、試験の自動化、AIを活用した診断、デジタル検査システムを中心に展開しています。TUV SUD、SGS、Intertekなどの企業は、予測検証のための機械学習ベースの試験フレームワークとデジタルツインを導入し、試験範囲を大幅に拡大し、サイクルタイムを短縮しています。

根拠:

イノベーションはダイナミックですが、破壊的というよりは進化的な側面が強いです。コアとなるテスト手法は国際標準に縛られているため、抜本的なイノベーションの余地は限られています。しかしながら、プロセスのデジタル化とAI統合におけるイノベーションは、適度な競争上の差別化をもたらし、中堅・大規模企業に優位性を与えると同時に、ティア2企業には地域に根ざしたイノベーションの余地を残します。

製品ライフサイクル分析:

製品ライフサイクル(PLC)フレームワークは、特定の業界における成熟度、競争動向、投資の焦点、そして戦略計画の理解に役立ちます。世界の医療機器TIC(試験・検査・認証)市場において、PLC分析は、市場の現状、各段階における課題と機会、そして主要企業が変化する規制、技術、そして顧客環境にどのように適応しているかを利害関係者が把握する上で役立ちます。この分析は、過去の発展、現在の動向、そして主要なTIC企業の戦略的動向を統合しています。

1.イントロダクション段階

2000年代初頭、米国FDA、欧州医薬品庁(EMA)、日本のPMDAといった規制当局がコンプライアンスと品質基準の厳格化を開始したことで、医療機器のTICアウトソーシング市場が勢いを増し始めました。第三者によるバリデーションの需要が急増しました。この時期、TICは依然としてメーカー各社が社内で主に処理していました。例えば、TUV SUDやSGSは独立したサービスを提供する数少ない世界企業でしたが、データの機密性に関する懸念やアウトソーシング・エコシステムの未整備により、導入は慎重な姿勢でした。

この段階では、市場は認知度の低さ、カスタマイズ性の高さ、サービスコストの高さ、そして契約交渉サイクルの長さといった特徴がありました。TIC企業は、OEMに対し、独立した検証のメリットを啓蒙する必要がありました。

2.成長段階

2010年から2020年頃にかけて、市場は急成長期に入りました。その要因としては、世界の医療機器輸出の拡大、複数国にまたがる複雑な規制遵守のニーズ(例:欧州におけるMDR)、そしてインプラントやウェアラブルといった新しい機器の急増が挙げられます。転機となったのは、2017年に施行された欧州連合医療機器規則(EU MDR)です。これにより、堅牢な試験と文書化の必要性が高まりました。

インターテック、ビューローベリタス、ULソリューションズといった大手企業は、世界市場へのアクセスを求めるOEMの需要に応えるため、アジア太平洋および中東でサービスを拡大しました。例えば、2019年にはSGSが上海のライフサイエンス研究所を拡張し、国際認証取得に向けたクラスIIおよびIII機器の生体適合性試験能力を強化しました。

3.成熟段階

世界の医療機器TICアウトソーシング市場は現在、成熟期にあります。2024年までに市場は大幅に統合され、TUV Rheinland、Eurofins Scientific、SGSなどの企業が製品安全性、サイバーセキュリティ認証、ソフトウェア検証などに関するエンドツーエンドのサービスを提供するようになるでしょう。

2024年にはテストが市場シェアの約65.1%を占め、特に規制コンプライアンスの更新や接続デバイスのサイバーセキュリティ評価において、より標準化され反復的なサービス需要への移行が見込まれています。

最近の例としては、UL Solutionsが2023年に日本のNTTデータと提携してAI駆動型診断ツール向けの安全な認証プロトコルを開発したことや、Intertekが2022年にSAI Global Assuranceを買収して北米の医療機器部門を強化したことなどが挙げられます。

4.飽和と早期衰退

中核的なTICサービスは成熟しているものの、先進国では従来型デバイス分野は飽和状態になると予想されています。しかしながら、AI統合デバイス、ロボット手術システム、パーソナライズ診断には依然として成長の余地があります。例えば、ビューローベリタスは2023年に、AIベースの画像診断ツールとウェアラブルセンサーを対象としたスマートヘルスTICイニシアチブを立ち上げました。

TICがコモディティ化するにつれ、デジタルテスト、リモート検査、リアルタイムコンプライアンス分析といった付加価値サービスが将来の差別化を決定づけるでしょう。しかし、イノベーションがなければ、サービスマージンは徐々に低下していくでしょう。

5.結論と市場の現状

上記の分析に基づき、世界の医療機器TICアウトソーシング市場は、製品ライフサイクルの成熟期に確実に入っています。この市場は、堅調な需要、高度なサービス標準化、主要企業による積極的な世界展開、そしてコモディティ化を回避するための新たなイノベーションを特徴としています。しかしながら、規制の追い風、機器の技術進化、そして国境を越えた貿易の増加により、専門分野のニッチやサービスが不足している地域において、依然として成長の余地が残されています。

COVID-19の影響分析

COVID-19パンデミックは、医療機器の試験・検査・認証(TIC)アウトソーシング市場に悪影響を及ぼしました。感染拡大当初は、世界のロックダウンとサプライチェーンの混乱により、製造および試験業務に遅延が生じました。多くの非必須医療機器や選択的医療機器の生産が減少し、TICサービスの需要も減少しました。さらに、実地監査や現地査察への制限により、認証プロセスにも支障が生じました。このように、COVID-19パンデミックは、市場の初期段階において悪影響を及ぼしました。

市場成長要因

このトレンドを最も顕著に表す例の一つは、北米市場へのAI対応医療機器の急増です。2024年8月時点で、FDAはAIまたは機械学習対応医療機器を950台承認しており、2020年初頭のわずか数十台から大幅に増加しています。この急激な増加は、ヘルスケアにおけるデジタル技術の役割の拡大と、自律型および半自律型の意思決定支援ツールに対するFDAの規制アプローチの進化を反映しています。これにより、市販後調査、リアルワールドエビデンス(RWE)収集、ソフトウェアライフサイクル監査を提供するTICベンダーへの新たな需要が生まれています。

さらに、急速な技術進歩は北米の医療機器情勢を大きく変革し、イノベーションを推進し、患者ケアを再構築しています。これらの進歩は、診断・治療能力の向上だけでなく、安全性と有効性を確保するための厳格な試験・検査・認証(TIC)プロセスを必要としています。医療機器業界が進化を続ける中で、基準を維持し、患者の健康を守るためには、堅牢なTICフレームワークが不可欠となります。

市場抑制要因

しかし、この地域の医療機器業界は、主に米国食品医薬品局(FDA)とカナダ保健省によって施行される、厳格かつ多面的な規制に縛られています。これらの規制枠組みは、医療機器の安全性、有効性、品質を確保するために設計されていますが、同時にメーカーやTICサービスプロバイダーにとって大きなコンプライアンス負担を生じさせています。こうした複雑さに対応するため、ストライカー社のような企業は、重要なコンプライアンス機能を社内で維持しつつ、標準化された試験手順をFDAおよびMDSAPの実績を持つ信頼できるベンダーにアウトソーシングするという、ハイブリッドTIC戦略を採用しています。このアプローチはリスクの軽減に役立ちますが、完全なアウトソーシングモデルに伴う規模と効率性のメリットは限定的になります。

バリューチェーン分析

医療機器試験・検査・認証アウトソーシング市場のバリューチェーンは、市場・規制情報提供から始まります。ここでは、進化する規格やコンプライアンス要件に関する重要なデータが収集されます。次に、試験・検査サービスが提供され、機器の安全性、品質、機能性を厳密に評価します。次に、認証エンゲージメントが、規制当局による機器の市場参入の正式な承認を確実にします。アドバイザリーおよびプロジェクトマネジメントは、コンプライアンスライフサイクル全体を通じて戦略的なサポートを提供します。発売後は、レポート作成およびデータ分析によってパフォーマンスに関する洞察が得られ、市販後調査および再認証に反映され、継続的な安全性が確保されます。最後に、継続的なイノベーションとトレーニングによって製品の改善が促進され、市場・規制情報提供にフィードバックされます。

サービスの見通し

サービスに基づいて、市場はテスト、検査、および認証に分類されます。

1.テストセグメント

テストセグメントでは、医療機器が市場に投入される前に、適用される安全性、性能、品質基準を満たしていることを確認するための厳格な評価を実施します。これには、生体適合性試験、電磁両立性(EMC)試験、電気安全性試験、機械試験、無菌試験、そしてソフトウェア駆動型デバイスのソフトウェア検証が含まれます。インプラントやウェアラブルといった複雑で小型化されたデバイスの普及に伴い、広範な第三者機関による試験の必要性が高まっています。

例えば、Intertek Group plcは、ウェアラブルバイオセンサーや医療機器向けソフトウェア(SaMD)の高度な試験をサービスポートフォリオに組み込み、特にIEC 62304およびISO 14971への準拠に重点を置いています。同様に、Eurofins Scientific SEは、新しいインプラント製品の前臨床安全性評価に不可欠な、ISO 10993ガイドラインに基づく微生物学および化学特性試験の需要増加に対応しています。

2.検査セグメント

検査サービスでは、デバイスとその製造プロセスが事前に定義された仕様と規制要件を満たしていることを確認するための、物理的および手順的な検証を行います。これには、品質管理検査、工程内監査、そして市場投入前に逸脱、欠陥、または安全性に関する懸念を検出するための最終製品検証が含まれます。検査サービスは、アウトソーシングや世界製造に伴うリスク管理において不可欠です。

TUV SUDやUL Solutionsといった主要企業は、特に輸出向けクラスIIおよびクラスIII機器を製造するアジアの施設向けに、オンサイト検査とリモート検査の両方を提供しています。2023年には、ビューローベリタスが欧州の複数のOEMと提携し、リモート工場検査プロトコルを導入しました。これにより、サプライチェーンの不足やパンデミックに伴う渡航制限といった混乱時においても事業継続が可能になりました。このイノベーションは、リモート検査技術がますます普及していることを浮き彫りにしています。

デバイスクラスの見通し

デバイスクラスに基づいて、市場はクラスII、クラスIII、クラスIに分類されます。

クラスIデバイス

クラスI医療機器は低リスクとみなされ、一般的に規制当局による審査が最も緩やかです。例としては、舌圧子、体温計、包帯、手動手術器具などが挙げられます。これらの機器は通常、市販前承認や第三者機関による広範な試験を必要としませんが、品質検査と基本的なコンプライアンス認証(例:ISO 13485)は、特に輸出においては依然として不可欠です。

TICサービスの範囲は狭いもの、IntertekやSGSといった大手TIC企業は、クラスI機器メーカー向けにバッチ検査、ラベル検証、適正製造基準(GMP)監査を提供しています。UL Solutionsは2023年の開発において、EUおよびラテンアメリカ市場への参入を目指す小規模なクラスI機器メーカー向けに、迅速なコンプライアンスサービスを開始しました。これらの市場では、言語固有のラベルおよびパッケージの審査が厳格化しています。

クラスIIデバイス

クラスII機器は中程度のリスクを伴い、より厳格な監督が必要です。これには、輸液ポンプ、電動車椅子、妊娠検査キット、血圧計などの機器が含まれます。クラスII機器は通常、米国では510(k)市販前届出、EUでは技術文書の提出と適合性評価が必要です。

このカテゴリーは、デバイスの数が多いことに加え、性能試験、電磁両立性、生体適合性、ソフトウェア検証に関する厳格な要件が求められることから、TICアウトソーシング情勢において大きなシェアを占めています。Eurofins Scientific、TUV SUD、BSI GroupなどのTICプロバイダーは、この需要に応えるためにインフラを拡張しています。

最終用途の見通し

最終用途に基づいて、市場は医療機器会社、製薬およびバイオテクノロジー会社、およびその他の最終用途に分類されます。

医療機器企業

医療機器メーカーはTICアウトソーシング情勢圧倒的なシェアを占めており、2024年には市場全体の約77.6%を占めています。この優位性は、進化する国際規制への準拠、製品の安全性と性能の確保、そしてますます複雑化する機器の市場投入までの期間短縮という、極めて重要なニーズによって支えられています。米国FDAの21 CFR Part 820、EU MDR、ISO 13485などの規格は、広範な検証、文書化、そして試験を必要としており、これらを社内で管理するには多くのリソースを要することがよくあります。

メドトロニックのような主要企業は、機器試験の円滑化と世界の規制承認取得の効率化を目指し、インターテックと提携しています。同様に、ボストン・サイエンティフィックは、クラスIIおよびIII機器のエンドツーエンドの品質保証試験をSGSと提携して実施しています。テュフ・ラインランドはシーメンス・ヘルスシナーズとの連携を拡大し、EU MDR制度に基づく包括的な適合性評価をサポートしています。これらの例は、大手メーカーがコンプライアンス維持のために外部のTIC(医療機器製造業者協会)の専門知識にますます依存する一方で、社内リソースをイノベーションに集中させていることを反映しています。

医療機器の試験は、革新的な設計を信頼性と市場性のある製品へと変革するプロセスにおいて重要なステップです。TUV SUDでは、医療製品試験に関する専門知識と、国際的に認定された研究所および施設の世界ネットワークを組み合わせ、ワンストップソリューションを提供しています。

TUV SUD-医療機器および体外診断用医療機器部門

日付:2025年

製薬およびバイオテクノロジー企業

このセグメントには、医薬品規制と医療機器規制の両方を満たす必要がある、オートインジェクターや薬剤溶出インプラントなどの複合製品を開発する企業が含まれます。TIC支出額では純粋な医療機器メーカーよりも規模は小さいものの、製薬企業とバイオテクノロジー企業は市場全体にとって重要な貢献者です。

例えば、ファイザーは、バイオ医薬品デリバリーシステムの分析試験と規制コンサルティングをSGSに委託することで、コンプライアンスへの取り組みを強化しました。さらに、ユーロフィン・サイエンティフィックは、開発から市販後調査段階まで、バイオテクノロジー企業向けに統合的なTICサービスを提供しています。これらの製品は二重の規制監督に直面しているため、TICのアウトソーシングは世界的な対応力を確保するための魅力的な戦略となっています。

「臨床試験で専門パートナーと協力することで、医療機器開発の複雑さを効率的に乗り越え、コンプライアンスを確保し、市場投入までの時間を短縮することができ米国。」

シーラ・マティアス博士- ヴィルパックス・ファーマシューティカルズ最高科学責任者

日付:2025年1月31日

地域の見通し

本レポートに含まれる地域は、北米、欧州、アジア太平洋、ラテンアメリカ、中東・アフリカです。欧州セグメントは、2024年の医療機器試験・検査・認証アウトソーシング市場において39%の収益シェアを獲得しました。この地域の国々は、厳格な適合性評価と市販後調査を重視しており、これがアウトソーシングによるコンプライアンスサービスの需要に大きく貢献しています。多くの欧州企業は、自社製品が統一規格を満たしていることを確認するために、独立した試験機関との連携を好んでいます。この地域では、患者の安全、イノベーション、医療機器の越境取引への関心が高まっており、専門的な第三者認証・検査サービスへの需要がさらに高まっています。

目次

第1章 市場範囲と調査手法

- 市場の定義

- 目的

- 市場範囲

- セグメンテーション

- 調査手法

第2章 市場要覧

- 主なハイライト

第3章 市場概要

- イントロダクション

- 概要

- 市場に影響を与える主な要因

- 市場促進要因

- 市場抑制要因

- 市場機会

- 市場の課題

第4章 競合分析- 世界

- 市場シェア分析 2024年

- 医療機器の試験、検査、認証アウトソーシング市場における最近の戦略

- ポーターファイブフォース分析

第5章 市場動向:医療機器の試験・検査・認証アウトソーシング市場

第6章 競合の現状:医療機器の試験、検査、認証アウトソーシング市場

第7章 市場統合分析- 世界の医療機器TIC市場

第8章 製品ライフサイクル- 世界の医療機器TIC市場

第9章 医療機器の試験・検査・認証アウトソーシング市場のバリューチェーン分析

- 市場および規制情報

- 試験・検査サービスの提供

- 認定契約

- アドバイザリー&プロジェクトマネジメント

- レポートとデータ分析

- 市販後調査と再認証

- 継続的なイノベーションとトレーニング

第10章 主要顧客基準 - 医療機器の試験、検査、認証アウトソーシング市場

- 規制能力と世界な対応範囲

- 先端医療技術における技術的専門知識

- サービス提供のスピードと柔軟性

- コストの透明性と運用効率

- データセキュリティと知的財産(IP)保護

- 評判、経験、そして市販後のサポート

第11章 世界市場:サービス別

- 世界の試験市場:地域別

- 世界の検査市場:地域別

- 世界の認証市場:地域別

第12章 世界市場:デバイスクラス別

- 世界のクラスII市場:地域別

- 世界のクラスIII市場:地域別

- 世界のクラスI市場:地域別

第13章 世界市場:最終用途別

- 世界の医療機器企業市場:地域別

- 世界の製薬・バイオテクノロジー企業市場:地域別

- 世界のその他の最終用途市場:地域別

第14章 世界市場:地域別

- 北米

- 主な影響要因

- 北米市場動向:

- 北米における競合の現状

- 北米の市場:国別

- 米国

- カナダ

- メキシコ

- その他北米地域

- 北米の市場:国別

- 欧州

- 主な影響要因

- 市場促進要因

- 欧州市場動向

- 欧州市場における競合の現状

- 欧州の市場:国別

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- イタリア

- その他欧州地域

- 欧州の市場:国別

- アジア太平洋地域

- 主な影響要因

- 市場動向-アジア太平洋地域

- 競合状況:

- アジア太平洋の市場:国別

- 中国

- 日本

- インド

- 韓国

- マレーシア

- その他アジア太平洋地域

- アジア太平洋の市場:国別

- ラテンアメリカ・中東・アフリカ

- 主な影響要因

- 市場動向-LAMEA

- 競合の現状-LAMEA

- ラテンアメリカ・中東・アフリカの市場:国別

- ブラジル

- アルゼンチン

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- その他ラテンアメリカ・中東・アフリカ地域

- ラテンアメリカ・中東・アフリカの市場:国別

第15章 企業プロファイル

- SGS SA

- Intertek Group PLC

- Eurofins Scientific SE

- TUV SUD

- ALS Limited

- Bureau Veritas SA

- Element Materials Technology(Temasek Holdings)

- DNV AS

- Pace Analytical Services, LLC

- Nelson Laboratories, LLC(Sotera Health Company)

第16章 医療機器の試験、検査、認証アウトソーシング市場の成功必須条件

LIST OF TABLES

- TABLE 1 Global Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 2 Global Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 3 Key Customer Criteria: Medical Device Testing, Inspection And Certification Outsourcing Market

- TABLE 4 Global Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 5 Global Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 6 Global Testing Market by Region, 2021 - 2024, USD Million

- TABLE 7 Global Testing Market by Region, 2025 - 2032, USD Million

- TABLE 8 Global Inspection Market by Region, 2021 - 2024, USD Million

- TABLE 9 Global Inspection Market by Region, 2025 - 2032, USD Million

- TABLE 10 Global Certification Market by Region, 2021 - 2024, USD Million

- TABLE 11 Global Certification Market by Region, 2025 - 2032, USD Million

- TABLE 12 Global Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 13 Global Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 14 Global Class II Market by Region, 2021 - 2024, USD Million

- TABLE 15 Global Class II Market by Region, 2025 - 2032, USD Million

- TABLE 16 Global Class III Market by Region, 2021 - 2024, USD Million

- TABLE 17 Global Class III Market by Region, 2025 - 2032, USD Million

- TABLE 18 Global Class I Market by Region, 2021 - 2024, USD Million

- TABLE 19 Global Class I Market by Region, 2025 - 2032, USD Million

- TABLE 20 Global Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 21 Global Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 22 Global Medical Device Companies Market by Region, 2021 - 2024, USD Million

- TABLE 23 Global Medical Device Companies Market by Region, 2025 - 2032, USD Million

- TABLE 24 Global Pharmaceutical and Biotech Companies Market by Region, 2021 - 2024, USD Million

- TABLE 25 Global Pharmaceutical and Biotech Companies Market by Region, 2025 - 2032, USD Million

- TABLE 26 Global Other End Use Market by Region, 2021 - 2024, USD Million

- TABLE 27 Global Other End Use Market by Region, 2025 - 2032, USD Million

- TABLE 28 Global Medical Device Testing, Inspection And Certification Outsourcing Market by Region, 2021 - 2024, USD Million

- TABLE 29 Global Medical Device Testing, Inspection And Certification Outsourcing Market by Region, 2025 - 2032, USD Million

- TABLE 30 North America Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 31 North America Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 32 North America Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 33 North America Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 34 North America Testing Market by Country, 2021 - 2024, USD Million

- TABLE 35 North America Testing Market by Country, 2025 - 2032, USD Million

- TABLE 36 North America Inspection Market by Country, 2021 - 2024, USD Million

- TABLE 37 North America Inspection Market by Country, 2025 - 2032, USD Million

- TABLE 38 North America Certification Market by Country, 2021 - 2024, USD Million

- TABLE 39 North America Certification Market by Country, 2025 - 2032, USD Million

- TABLE 40 North America Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 41 North America Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 42 North America Class II Market by Country, 2021 - 2024, USD Million

- TABLE 43 North America Class II Market by Country, 2025 - 2032, USD Million

- TABLE 44 North America Class III Market by Country, 2021 - 2024, USD Million

- TABLE 45 North America Class III Market by Country, 2025 - 2032, USD Million

- TABLE 46 North America Class I Market by Country, 2021 - 2024, USD Million

- TABLE 47 North America Class I Market by Country, 2025 - 2032, USD Million

- TABLE 48 North America Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 49 North America Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 50 North America Medical Device Companies Market by Country, 2021 - 2024, USD Million

- TABLE 51 North America Medical Device Companies Market by Country, 2025 - 2032, USD Million

- TABLE 52 North America Pharmaceutical and Biotech Companies Market by Country, 2021 - 2024, USD Million

- TABLE 53 North America Pharmaceutical and Biotech Companies Market by Country, 2025 - 2032, USD Million

- TABLE 54 North America Other End Use Market by Country, 2021 - 2024, USD Million

- TABLE 55 North America Other End Use Market by Country, 2025 - 2032, USD Million

- TABLE 56 North America Medical Device Testing, Inspection And Certification Outsourcing Market by Country, 2021 - 2024, USD Million

- TABLE 57 North America Medical Device Testing, Inspection And Certification Outsourcing Market by Country, 2025 - 2032, USD Million

- TABLE 58 US Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 59 US Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 60 US Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 61 US Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 62 US Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 63 US Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 64 US Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 65 US Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 66 Canada Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 67 Canada Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 68 Canada Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 69 Canada Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 70 Canada Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 71 Canada Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 72 Canada Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 73 Canada Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 74 Mexico Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 75 Mexico Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 76 Mexico Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 77 Mexico Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 78 Mexico Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 79 Mexico Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 80 Mexico Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 81 Mexico Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 82 Rest of North America Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 83 Rest of North America Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 84 Rest of North America Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 85 Rest of North America Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 86 Rest of North America Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 87 Rest of North America Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 88 Rest of North America Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 89 Rest of North America Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 90 Europe Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 91 Europe Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 92 Europe Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 93 Europe Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 94 Europe Testing Market by Country, 2021 - 2024, USD Million

- TABLE 95 Europe Testing Market by Country, 2025 - 2032, USD Million

- TABLE 96 Europe Inspection Market by Country, 2021 - 2024, USD Million

- TABLE 97 Europe Inspection Market by Country, 2025 - 2032, USD Million

- TABLE 98 Europe Certification Market by Country, 2021 - 2024, USD Million

- TABLE 99 Europe Certification Market by Country, 2025 - 2032, USD Million

- TABLE 100 Europe Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 101 Europe Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 102 Europe Class II Market by Country, 2021 - 2024, USD Million

- TABLE 103 Europe Class II Market by Country, 2025 - 2032, USD Million

- TABLE 104 Europe Class III Market by Country, 2021 - 2024, USD Million

- TABLE 105 Europe Class III Market by Country, 2025 - 2032, USD Million

- TABLE 106 Europe Class I Market by Country, 2021 - 2024, USD Million

- TABLE 107 Europe Class I Market by Country, 2025 - 2032, USD Million

- TABLE 108 Europe Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 109 Europe Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 110 Europe Medical Device Companies Market by Country, 2021 - 2024, USD Million

- TABLE 111 Europe Medical Device Companies Market by Country, 2025 - 2032, USD Million

- TABLE 112 Europe Pharmaceutical and Biotech Companies Market by Country, 2021 - 2024, USD Million

- TABLE 113 Europe Pharmaceutical and Biotech Companies Market by Country, 2025 - 2032, USD Million

- TABLE 114 Europe Other End Use Market by Country, 2021 - 2024, USD Million

- TABLE 115 Europe Other End Use Market by Country, 2025 - 2032, USD Million

- TABLE 116 Europe Medical Device Testing, Inspection And Certification Outsourcing Market by Country, 2021 - 2024, USD Million

- TABLE 117 Europe Medical Device Testing, Inspection And Certification Outsourcing Market by Country, 2025 - 2032, USD Million

- TABLE 118 Germany Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 119 Germany Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 120 Germany Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 121 Germany Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 122 Germany Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 123 Germany Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 124 Germany Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 125 Germany Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 126 UK Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 127 UK Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 128 UK Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 129 UK Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 130 UK Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 131 UK Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 132 UK Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 133 UK Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 134 France Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 135 France Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 136 France Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 137 France Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 138 France Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 139 France Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 140 France Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 141 France Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 142 Russia Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 143 Russia Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 144 Russia Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 145 Russia Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 146 Russia Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 147 Russia Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 148 Russia Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 149 Russia Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 150 Spain Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 151 Spain Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 152 Spain Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 153 Spain Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 154 Spain Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 155 Spain Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 156 Spain Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 157 Spain Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 158 Italy Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 159 Italy Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 160 Italy Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 161 Italy Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 162 Italy Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 163 Italy Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 164 Italy Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 165 Italy Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 166 Rest of Europe Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 167 Rest of Europe Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 168 Rest of Europe Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 169 Rest of Europe Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 170 Rest of Europe Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 171 Rest of Europe Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 172 Rest of Europe Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 173 Rest of Europe Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 174 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 175 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 176 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 177 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 178 Asia Pacific Testing Market by Country, 2021 - 2024, USD Million

- TABLE 179 Asia Pacific Testing Market by Country, 2025 - 2032, USD Million

- TABLE 180 Asia Pacific Inspection Market by Country, 2021 - 2024, USD Million

- TABLE 181 Asia Pacific Inspection Market by Country, 2025 - 2032, USD Million

- TABLE 182 Asia Pacific Certification Market by Country, 2021 - 2024, USD Million

- TABLE 183 Asia Pacific Certification Market by Country, 2025 - 2032, USD Million

- TABLE 184 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 185 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 186 Asia Pacific Class II Market by Country, 2021 - 2024, USD Million

- TABLE 187 Asia Pacific Class II Market by Country, 2025 - 2032, USD Million

- TABLE 188 Asia Pacific Class III Market by Country, 2021 - 2024, USD Million

- TABLE 189 Asia Pacific Class III Market by Country, 2025 - 2032, USD Million

- TABLE 190 Asia Pacific Class I Market by Country, 2021 - 2024, USD Million

- TABLE 191 Asia Pacific Class I Market by Country, 2025 - 2032, USD Million

- TABLE 192 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 193 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 194 Asia Pacific Medical Device Companies Market by Country, 2021 - 2024, USD Million

- TABLE 195 Asia Pacific Medical Device Companies Market by Country, 2025 - 2032, USD Million

- TABLE 196 Asia Pacific Pharmaceutical and Biotech Companies Market by Country, 2021 - 2024, USD Million

- TABLE 197 Asia Pacific Pharmaceutical and Biotech Companies Market by Country, 2025 - 2032, USD Million

- TABLE 198 Asia Pacific Other End Use Market by Country, 2021 - 2024, USD Million

- TABLE 199 Asia Pacific Other End Use Market by Country, 2025 - 2032, USD Million

- TABLE 200 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by Country, 2021 - 2024, USD Million

- TABLE 201 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by Country, 2025 - 2032, USD Million

- TABLE 202 China Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 203 China Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 204 China Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 205 China Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 206 China Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 207 China Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 208 China Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 209 China Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 210 Japan Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 211 Japan Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 212 Japan Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 213 Japan Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 214 Japan Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 215 Japan Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 216 Japan Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 217 Japan Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 218 India Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 219 India Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 220 India Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 221 India Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 222 India Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 223 India Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 224 India Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 225 India Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 226 South Korea Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 227 South Korea Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 228 South Korea Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 229 South Korea Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 230 South Korea Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 231 South Korea Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 232 South Korea Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 233 South Korea Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 234 Singapore Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 235 Singapore Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 236 Singapore Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 237 Singapore Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 238 Singapore Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 239 Singapore Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 240 Singapore Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 241 Singapore Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 242 Malaysia Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 243 Malaysia Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 244 Malaysia Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 245 Malaysia Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 246 Malaysia Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 247 Malaysia Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 248 Malaysia Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 249 Malaysia Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 250 Rest of Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 251 Rest of Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 252 Rest of Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 253 Rest of Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 254 Rest of Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 255 Rest of Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 256 Rest of Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 257 Rest of Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 258 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 259 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 260 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 261 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 262 LAMEA Testing Market by Country, 2021 - 2024, USD Million

- TABLE 263 LAMEA Testing Market by Country, 2025 - 2032, USD Million

- TABLE 264 LAMEA Inspection Market by Country, 2021 - 2024, USD Million

- TABLE 265 LAMEA Inspection Market by Country, 2025 - 2032, USD Million

- TABLE 266 LAMEA Certification Market by Country, 2021 - 2024, USD Million

- TABLE 267 LAMEA Certification Market by Country, 2025 - 2032, USD Million

- TABLE 268 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 269 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 270 LAMEA Class II Market by Country, 2021 - 2024, USD Million

- TABLE 271 LAMEA Class II Market by Country, 2025 - 2032, USD Million

- TABLE 272 LAMEA Class III Market by Country, 2021 - 2024, USD Million

- TABLE 273 LAMEA Class III Market by Country, 2025 - 2032, USD Million

- TABLE 274 LAMEA Class I Market by Country, 2021 - 2024, USD Million

- TABLE 275 LAMEA Class I Market by Country, 2025 - 2032, USD Million

- TABLE 276 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 277 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 278 LAMEA Medical Device Companies Market by Country, 2021 - 2024, USD Million

- TABLE 279 LAMEA Medical Device Companies Market by Country, 2025 - 2032, USD Million

- TABLE 280 LAMEA Pharmaceutical and Biotech Companies Market by Country, 2021 - 2024, USD Million

- TABLE 281 LAMEA Pharmaceutical and Biotech Companies Market by Country, 2025 - 2032, USD Million

- TABLE 282 LAMEA Other End Use Market by Country, 2021 - 2024, USD Million

- TABLE 283 LAMEA Other End Use Market by Country, 2025 - 2032, USD Million

- TABLE 284 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by Country, 2021 - 2024, USD Million

- TABLE 285 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by Country, 2025 - 2032, USD Million

- TABLE 286 Brazil Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 287 Brazil Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 288 Brazil Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 289 Brazil Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 290 Brazil Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 291 Brazil Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 292 Brazil Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 293 Brazil Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 294 Argentina Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 295 Argentina Medical Device Testing

- TABLE 318 UAE Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 319 UAE Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 320 UAE Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 321 UAE Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 322 UAE Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 323 UAE Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 324 UAE Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 325 UAE Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 326 Nigeria Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 327 Nigeria Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 328 Nigeria Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 329 Nigeria Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 330 Nigeria Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 331 Nigeria Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 332 Nigeria Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 333 Nigeria Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 334 Rest of LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2024, USD Million

- TABLE 335 Rest of LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market, 2025 - 2032, USD Million

- TABLE 336 Rest of LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2024, USD Million

- TABLE 337 Rest of LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2025 - 2032, USD Million

- TABLE 338 Rest of LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2024, USD Million

- TABLE 339 Rest of LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2025 - 2032, USD Million

- TABLE 340 Rest of LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2024, USD Million

- TABLE 341 Rest of LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2025 - 2032, USD Million

- TABLE 342 Key Information - SGS S.A.

- TABLE 343 Key Information - Intertek Group PLC

- TABLE 344 Key Information - Eurofins Scientific SE

- TABLE 345 Key Information - Tuv sud

- TABLE 346 Key Information - ALS Limited

- TABLE 347 Key Information - Bureau Veritas S.A.

- TABLE 348 Key Information - Element Materials Technology

- TABLE 349 Key Information - DNV AS

- TABLE 350 Key Information - Pace Analytical Services, LLC

- TABLE 351 Key Information - Nelson Laboratories, LLC

LIST OF FIGURES

- FIG 1 Methodology for the research

- FIG 2 Global Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2032, USD Million

- FIG 3 Key Factors Impacting Medical Device Testing, Inspection And Certification Outsourcing Market

- FIG 4 Market Share Analysis, 2024

- FIG 5 Porter's Five Forces Analysis - Medical Device Testing, Inspection And Certification Outsourcing Market

- FIG 6 Market Consolidation Analysis - Global Medical Device TIC Market

- FIG 7 Product Life Cycle - Global Medical Device TIC Market

- FIG 8 Value Chain Analysis of Medical Device Testing, Inspection And Certification Outsourcing Market

- FIG 9 Global Medical Device Testing, Inspection And Certification Outsourcing Market share by Service, 2024

- FIG 10 Global Medical Device Testing, Inspection And Certification Outsourcing Market share by Service, 2032

- FIG 11 Global Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2032, USD Million

- FIG 12 Global Medical Device Testing, Inspection And Certification Outsourcing Market share by Device Class, 2024

- FIG 13 Global Medical Device Testing, Inspection And Certification Outsourcing Market share by Device Class, 2032

- FIG 14 Global Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2032, USD Million

- FIG 15 Global Medical Device Testing, Inspection And Certification Outsourcing Market share by End Use, 2024

- FIG 16 Global Medical Device Testing, Inspection And Certification Outsourcing Market share by End Use, 2032

- FIG 17 Global Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2032, USD Million

- FIG 18 Global Medical Device Testing, Inspection And Certification Outsourcing Market by Region, 2021

- FIG 19 Global Medical Device Testing, Inspection And Certification Outsourcing Market by Region, 2021

- FIG 20 Global Medical Device Testing, Inspection And Certification Outsourcing Market by Region, 2025 - 2032, USD Million

- FIG 21 Key Factors Impacting North America Medical Device Testing, Inspection And Certification Outsourcing Market

- FIG 22 North America Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2032, USD Million

- FIG 23 North America Medical Device Testing, Inspection And Certification Outsourcing Market share by Service, 2024

- FIG 24 North America Medical Device Testing, Inspection And Certification Outsourcing Market share by Service, 2032

- FIG 25 North America Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2032, USD Million

- FIG 26 North America Medical Device Testing, Inspection And Certification Outsourcing Market share by Device Class, 2024

- FIG 27 North America Medical Device Testing, Inspection And Certification Outsourcing Market share by Device Class, 2032

- FIG 28 North America Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2032, USD Million

- FIG 29 North America Medical Device Testing, Inspection And Certification Outsourcing Market share by End Use, 2024

- FIG 30 North America Medical Device Testing, Inspection And Certification Outsourcing Market share by End Use, 2032

- FIG 31 North America Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2032, USD Million

- FIG 32 North America Medical Device Testing, Inspection And Certification Outsourcing Market share by Country, 2024

- FIG 33 North America Medical Device Testing, Inspection And Certification Outsourcing Market share by Country, 2032

- FIG 34 North America Medical Device Testing, Inspection And Certification Outsourcing Market by Country, 2025 - 2032, USD Million

- FIG 35 Key Factors Impacting Europe Medical Device Testing, Inspection And Certification Outsourcing Market

- FIG 36 Europe Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2032, USD Million

- FIG 37 Europe Medical Device Testing, Inspection And Certification Outsourcing Market share by Service, 2024

- FIG 38 Europe Medical Device Testing, Inspection And Certification Outsourcing Market share by Service, 2032

- FIG 39 Europe Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2032, USD Million

- FIG 40 Europe Medical Device Testing, Inspection And Certification Outsourcing Market share by Device Class, 2024

- FIG 41 Europe Medical Device Testing, Inspection And Certification Outsourcing Market share by Device Class, 2032

- FIG 42 Europe Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2032, USD Million

- FIG 43 Europe Medical Device Testing, Inspection And Certification Outsourcing Market share by End Use, 2024

- FIG 44 Europe Medical Device Testing, Inspection And Certification Outsourcing Market share by End Use, 2032

- FIG 45 Europe Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2032, USD Million

- FIG 46 Europe Medical Device Testing, Inspection And Certification Outsourcing Market by Country, 2021

- FIG 47 Europe Medical Device Testing, Inspection And Certification Outsourcing Market by Country, 2021

- FIG 48 Europe Medical Device Testing, Inspection And Certification Outsourcing Market by Country, 2025 - 2032, USD Million

- FIG 49 Key Factors Impacting Europe Medical Device Testing, Inspection And Certification Outsourcing Market

- FIG 50 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2032, USD Million

- FIG 51 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market share by Service, 2024

- FIG 52 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market share by Service, 2032

- FIG 53 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2032, USD Million

- FIG 54 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market share by Device Class, 2024

- FIG 55 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market share by Device Class, 2032

- FIG 56 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2032, USD Million

- FIG 57 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market share by End Use, 2024

- FIG 58 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market share by End Use, 2032

- FIG 59 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2032, USD Million

- FIG 60 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market share by Country, 2024

- FIG 61 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market share by Country, 2032

- FIG 62 Asia Pacific Medical Device Testing, Inspection And Certification Outsourcing Market by Country, 2025 - 2032, USD Million

- FIG 63 Key Factors Impacting Europe Medical Device Testing, Inspection And Certification Outsourcing Market

- FIG 64 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market, 2021 - 2032, USD Million

- FIG 65 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market share by Service, 2024

- FIG 66 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market share by Service, 2032

- FIG 67 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by Service, 2021 - 2032, USD Million

- FIG 68 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market share by Device Class, 2024

- FIG 69 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market share by Device Class, 2032

- FIG 70 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by Device Class, 2021 - 2032, USD Million

- FIG 71 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market share by End Use, 2024

- FIG 72 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market share by End Use, 2032

- FIG 73 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by End Use, 2021 - 2032, USD Million

- FIG 74 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market share by Country, 2024

- FIG 75 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market share by Country, 2032

- FIG 76 LAMEA Medical Device Testing, Inspection And Certification Outsourcing Market by Country, 2025 - 2032, USD Million

- FIG 77 Swot Analysis: SGS S.A.

- FIG 78 Swot Analysis: Intertek Group PLC

- FIG 79 SWOT Analysis: Eurofins Scientific SE

- FIG 80 Swot Analysis: TUV SUD

- FIG 81 Swot Analysis: ALS LIMITED

- FIG 82 Swot Analysis: Bureau Veritas S.A.

- FIG 83 SWOT Analysis: Element Materials Technology

- FIG 84 Swot Analysis: DNV AS

- FIG 85 Swot Analysis: Pace Analytical Services, LLC

The Global Medical Device Testing, Inspection And Certification Outsourcing Market size is expected to reach $5.48 billion by 2032, rising at a market growth of 8.3% CAGR during the forecast period.

Key Highlights:

- The Europe market dominated the Global Market in 2024, accounting for a 39% revenue share in 2024.

- The US Medical Device Testing, Inspection And Certification Outsourcing Market is expected to continue its dominance in North America region thereby reaching a market size of 1.1 billion by 2032.

- Among the various device class type segments, Class II dominated the global market, contributing a revenue share of 53.4% in 2024.

- Testing segment led the services segments in 2032, capturing a 63.2% revenue share and is projected to continue its dominance during projected period.

- Among different end user verticals, Medical Device Companies segment with a revenue contribution of 2.29 billion in 2024 is projected to continue its dominance.

The global medical device testing, inspection, and certification (TIC) outsourcing market has evolved significantly over the past few decades, driven by the rapid advancement of medical technologies, heightened regulatory scrutiny, and the globalization of healthcare product distribution. Initially, many medical device manufacturers managed quality assurance and regulatory compliance processes internally. However, as the complexity and diversity of devices increased, and global health authorities like the U.S. Food and Drug Administration (FDA), European Medicines Agency (EMA), and Japan's PMDA implemented stringent compliance frameworks, outsourcing emerged as a strategic necessity.

Medical device companies began relying on third-party TIC service providers to ensure compliance with national and international standards, improve product quality, and accelerate time-to-market. This trend was also influenced by the growing demand for medical devices across geographies, which required manufacturers to meet varied regulatory requirements, thus turning to specialized providers with multi-jurisdictional expertise.

Over time, outsourcing TIC functions helped companies reduce costs, mitigate risk, and maintain focus on core competencies such as innovation and product development. Government health departments and notified bodies across the EU and North America have played pivotal roles in defining safety standards and testing protocols, reinforcing the need for independent verification and validation. As healthcare infrastructure expands in emerging economies and the digitization of medical devices continues, the reliance on TIC outsourcing has further intensified, creating a robust and evolving global market.

One of the dominant trends shaping the medical device TIC outsourcing market is the integration of advanced technologies into devices, which has created a pressing need for new testing capabilities. Devices incorporating AI algorithms for diagnostics, IoT sensors for remote monitoring, and software-driven therapeutic interventions must be tested for cybersecurity, data accuracy, and real-time functionality. Traditional testing methods fall short in evaluating these novel components, pushing TIC providers to invest in high-tech labs and digital capabilities to remain relevant.

Another major trend is the increasing importance of regulatory compliance, driven by global events such as product recalls and patient safety concerns. Regulatory bodies have raised the bar for quality assurance, making independent TIC services indispensable for companies aiming to secure and retain certifications such as FDA 510(k), CE marking, and ISO 13485. Compliance is no longer a one-time activity but an ongoing requirement, prompting continuous engagement with TIC providers throughout the product lifecycle.

Market Consolidation Analysis

The Global Medical Device TIC Market is undergoing notable transformation driven by regulatory stringency, globalization of healthcare supply chains, and rapid advancements in medical device technology. Testing, Inspection, and Certification (TIC) services ensure product safety, compliance, and reliability for both manufacturers and regulators. As these services become increasingly specialized, the market is gravitating toward consolidation, where a few multinational TIC providers dominate by offering integrated, scalable, and globally harmonized solutions. Market consolidation is shaped by various factors including innovation, regulatory burden, entry barriers, and international partnerships-all of which determine the distribution of market power and future growth trajectories.

1. Level of Innovation - ★★★★☆ (4/5)

Innovation in the medical device TIC market revolves around automation in testing, AI-driven diagnostics, and digital inspection systems. Companies like TUV SUD, SGS, and Intertek are introducing machine learning-based testing frameworks and digital twins for predictive validation, significantly enhancing test coverage and reducing cycle time.

Justification:

Innovation is dynamic but still primarily evolutionary rather than disruptive. Since core testing methodologies are tied to international standards, room for radical innovation is limited. However, innovations in process digitization and AI integration offer moderate competitive differentiation, giving mid-to-large players an edge while allowing room for tier-2 players to innovate locally.

Product Life Cycle Analysis:

The Product Life Cycle (PLC) framework helps in understanding the maturity, competitive dynamics, investment focus, and strategic planning of a particular industry. In the context of the Global Medical Device TIC (Testing, Inspection, and Certification) Market, the PLC analysis is instrumental for stakeholders to determine where the market currently stands, what challenges and opportunities exist at each stage, and how key players adapt to evolving regulatory, technological, and customer landscapes. This analysis combines historical evolution, present dynamics, and strategic movements by major TIC firms.

1. Introduction Stage

In the early 2000s, the medical device TIC outsourcing market began gaining traction as regulatory bodies like the U.S. FDA, the European Medicines Agency (EMA), and Japan's PMDA started tightening compliance and quality standards. The demand for third-party validation surged. During this period, TIC was still largely handled in-house by manufacturers. For example, TUV SUD and SGS were among the few global players offering independent services, but adoption was cautious due to data confidentiality concerns and underdeveloped outsourcing ecosystems.

During this stage, the market was characterized by low awareness, high customization, high service cost, and longer contract negotiation cycles. TIC companies had to educate OEMs about the benefits of independent validation.

2. Growth Stage

From around 2010 to 2020, the market entered a high-growth phase driven by several factors: expansion of global medical device exports, complex multi-country regulatory compliance needs (e.g., MDR in Europe), and the surge in novel devices such as implantables and wearables. A turning point was the implementation of the European Union Medical Device Regulation (EU MDR) in 2017, which heightened the need for robust testing and documentation.

Major players including Intertek, Bureau Veritas, and UL Solutions expanded services in Asia-Pacific and the Middle East to meet demand from OEMs seeking global market access. For instance, in 2019, SGS expanded its life sciences laboratory in Shanghai, enhancing its capacity for biocompatibility testing of Class II and III devices targeting international certification.

3. Maturity Stage

The Global Medical Device TIC Outsourcing Market is currently in the maturity stage. By 2024, the market has consolidated significantly, with companies such as TUV Rheinland, Eurofins Scientific, and SGS providing end-to-end services for product safety, cybersecurity certification, software validation, and more.

Testing accounted for approximately 65.1% of the market share in 2024, indicating a shift towards more standardized and repetitive service demand, particularly for regulatory compliance renewals and cybersecurity assessments for connected devices.

Recent examples include UL Solutions' 2023 partnership with Japan's NTT Data to develop a secure certification protocol for AI-driven diagnostic tools, and Intertek's 2022 acquisition of SAI Global Assurance to enhance its medical device vertical in North America.

4. Saturation and Early Decline

While the core TIC services are mature, saturation is expected in developed economies for traditional device segments. However, growth pockets remain in AI-integrated devices, robotic surgery systems, and personalized diagnostics. For instance, Bureau Veritas launched a smart health TIC initiative in 2023 targeting AI-based imaging tools and wearable sensors.

As TIC becomes commoditized, value-added services such as digital testing, remote inspections, and real-time compliance analytics will define future differentiation. But without innovation, service margins are likely to decline gradually.

5.Conclusion & Current Stage of the Market

Based on the above analysis, the Global Medical Device TIC Outsourcing Market is firmly in its maturity stage of the product life cycle. The market is characterized by strong demand, high service standardization, aggressive global expansion by leading players, and emerging innovations to avoid commoditization. Yet, due to regulatory tailwinds, technological evolution in devices, and rising cross-border trade, it still offers growth avenues in specialized service niches and underserved geographies.

COVID 19 Impact Analysis

The COVID-19 pandemic had a negative impact on the Medical Device Testing, Inspection, and Certification (TIC) Outsourcing Market. During the initial outbreak, global lockdowns and supply chain disruptions delayed manufacturing and testing operations. Many non-essential and elective medical devices saw reduced production, leading to a decline in demand for TIC services. Additionally, restrictions on physical audits and site inspections hampered certification processes. Thus, the COVID-19 pandemic had a negative impact on the market during its early phases.

Market Growth Factors

One of the most prominent examples of this trend is the surge in AI-enabled medical devices entering the North American market. As of August 2024, the FDA had authorized 950 AI- or machine learning-enabled medical devices, up from only a few dozen in early 2020. This exponential increase reflects both the growing role of digital technologies in healthcare and the FDA's evolving regulatory approach to autonomous and semi-autonomous decision-support tools. This has created new demand for TIC vendors that offer post-market surveillance, real-world evidence (RWE) collection, and software lifecycle auditing.

Additionally, Rapid technological advancements are significantly transforming the medical device landscape in North America, driving innovation and reshaping patient care. These developments are not only enhancing diagnostic and therapeutic capabilities but also necessitating rigorous Testing, Inspection, and Certification (TIC) processes to ensure safety and efficacy. As the medical device industry continues to evolve, robust TIC frameworks will be essential to uphold standards and protect patient well-being.

Market Restraining Factors

However, the medical device industry in this region is bound by rigorous and multifaceted regulations, primarily enforced by the U.S. Food and Drug Administration (FDA) and Health Canada. These regulatory frameworks are designed to ensure the safety, efficacy, and quality of medical devices but also create a substantial compliance burden for manufacturers and TIC service providers. In response to these complexities, companies like Stryker Corporation have adopted hybrid TIC strategies-keeping critical compliance functions in-house while outsourcing standardized testing procedures to trusted vendors with proven FDA and MDSAP experience. While this approach helps mitigate risks, it limits the scale and efficiency benefits typically associated with full outsourcing models.

Value Chain Analysis

The value chain of the Medical Device Testing, Inspection, and Certification Outsourcing Market begins with Market & Regulatory Intelligence, where critical data on evolving standards and compliance requirements is gathered. This is followed by Test & Inspection Services, which involve rigorous evaluation of device safety, quality, and functionality. Next, Certification Engagement ensures regulatory bodies formally approve devices for market access. Advisory & Project Management provides strategic support throughout the compliance lifecycle. Post-launch, Reporting & Data Analytics delivers performance insights, feeding into Post-Market Surveillance & Recertification to ensure ongoing safety. Finally, Continuous Innovation & Training fosters product improvements, feeding back into Market & Regulatory Intelligence.

Service Outlook

Based on Service, the market is segmented into Testing, Inspection, and Certification.

1. Testing Segment

The Testing segment involves rigorous evaluations of medical devices to ensure they meet applicable safety, performance, and quality standards before they are launched in the market. This includes biocompatibility tests, electromagnetic compatibility (EMC) tests, electrical safety testing, mechanical testing, sterility testing, and software validation for software-driven devices. The increasing prevalence of complex and miniaturized devices, such as implantables and wearables, has driven the need for extensive third-party testing.

For instance, Intertek Group plc has expanded its service portfolio to include advanced testing for wearable biosensors and software as a medical device (SaMD), particularly focusing on IEC 62304 and ISO 14971 compliance. Similarly, Eurofins Scientific SE has seen increasing demand for microbiology and chemical characterization testing under ISO 10993 guidelines, critical for preclinical safety assessments of new implantable products.

2. Inspection Segment

The Inspection service involves physical and procedural verification of devices and their production processes to ensure they meet predefined specifications and regulatory requirements. These include quality control inspections, in-process audits, and final product verification to detect deviations, defects, or safety concerns before market release. Inspection services are vital in managing risks associated with outsourced and global manufacturing.

Key players like TUV SUD and UL Solutions offer both onsite and remote inspections, particularly for facilities in Asia that manufacture Class II and Class III devices for export. In 2023, Bureau Veritas partnered with multiple OEMs across Europe to implement remote factory inspection protocols, enabling business continuity during disruptions like supply chain shortages and pandemic-related travel restrictions. This innovation underscores how remote inspection technology is becoming more mainstream.

Device Class Outlook

Based on Device Class, the market is segmented into Class II, Class III, and Class I.

Class I Devices

Class I medical devices are considered low-risk and generally subject to the least regulatory scrutiny. Examples include tongue depressors, thermometers, bandages, and manual surgical instruments. These devices typically do not require premarket approval or extensive third-party testing, but quality inspections and basic compliance certification (e.g., ISO 13485) are still critical, especially for export.

Although the scope of TIC services is narrower, leading TIC players like Intertek and SGS provide batch inspection, label verification, and good manufacturing practice (GMP) audits for Class I device producers. In a 2023 development, UL Solutions launched a fast-track compliance service aimed at small-scale Class I device manufacturers looking to enter EU and Latin American markets, where language-specific labeling and packaging reviews are becoming more stringent.

Class II Devices

Class II devices pose moderate risk and require more robust oversight. These include devices such as infusion pumps, powered wheelchairs, pregnancy test kits, and blood pressure monitors. Class II devices typically require 510(k) premarket notification in the U.S. or technical documentation and conformity assessments in the EU.

This category dominates the TIC outsourcing landscape due to the volume of devices, coupled with stringent requirements around performance testing, electromagnetic compatibility, biocompatibility, and software validation. TIC providers like Eurofins Scientific, TUV SUD, and BSI Group have expanded their infrastructure to meet this demand.

End Use Outlook

Based on End Use, the market is segmented into Medical Device Companies, Pharmaceutical and Biotech Companies, and Other End Use.

Medical Device Companies

Medical device manufacturers dominate the TIC outsourcing landscape, accounting for approximately 77.6% of the total market share in 2024. This prominence is driven by their critical need to align with evolving international regulations, ensure safety and performance of products, and speed up time-to-market for increasingly complex devices. Standards like the U.S. FDA's 21 CFR Part 820, EU MDR, and ISO 13485 require extensive validation, documentation, and testing-activities which are often resource-intensive to manage internally.

Leading companies like Medtronic have partnered with Intertek to facilitate device testing and meet global regulatory approvals more efficiently. Similarly, Boston Scientific engages with SGS for end-to-end quality assurance testing for its Class II and III devices. TUV Rheinland has expanded its collaboration with Siemens Healthineers, supporting full-scope conformity assessments under the EU MDR regime. These examples reflect how large manufacturers increasingly rely on external TIC expertise to maintain compliance while focusing internal resources on innovation.

"Medical device testing is a critical step in the process of transforming an innovative design into a reliable and marketable product. At TUV SUD, we combine expert medical product testing knowledge with a global network of internationally accredited laboratories and facilities, providing you with a one-stop solution."

TUV SUD - Medical Devices and IVD Division

Date: 2025

Pharmaceutical and Biotech Companies