|

|

市場調査レポート

商品コード

1373599

3Dプリンティングの世界市場規模、シェア、産業動向分析レポート:コンポーネント別、技術別、用途別、業界別、地域別展望と予測、2023年~2030年Global 3D Printing Market Size, Share & Industry Trends Analysis Report By Component (Product, Software, and Services), By Technology, By Application, By Vertical, By Regional Outlook and Forecast, 2023 - 2030 |

||||||

|

|

|||||||

|

|||||||

| 3Dプリンティングの世界市場規模、シェア、産業動向分析レポート:コンポーネント別、技術別、用途別、業界別、地域別展望と予測、2023年~2030年 |

|

出版日: 2023年09月30日

発行: KBV Research

ページ情報: 英文 551 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

3Dプリンティング市場規模は2030年までに864億米ドルに達すると予測され、予測期間中のCAGRは21.4%の市場成長率で上昇します。

KBV Cardinalのマトリックスに示された分析によると、3Dプリンティング市場ではCanon, Inc.が先行しています。Autodesk, Inc.、Stratasys Ltd.、3D Systems Corporationなどの企業は、3Dプリンティング市場の主要なイノベーターです。2022年5月、StratasysはF190 CRおよびF370 CRマシン、FDM 3DプリンターのF123シリーズ、および最終用途のコンポーネントを製造する製造業者および産業機械工向けに開発された新しい炭素繊維強化のFDM Nylon-CF10材料、治具、固定具、ワーク保持ツールを発表しました。

市場成長要因

国や地方自治体による規制支援の高まり

世界各国の政府は、イノベーションを促進し、地域の製造業を後押しし、さまざまな社会的課題に対処する3Dプリンティングの可能性を認識しています。中国は、製造能力の向上を目指す「Made in China 2025」構想の一環として、3Dプリンティングに多額の投資を行っています。ドイツ政府は、特にインダストリー4.0において、さまざまな3Dプリンティングプロジェクトや研究イニシアチブを支援してきました。ドイツの主要研究機関であるフラウンホーファー研究所は、数多くの積層造形プロジェクトに関与しています。政府によっては、製造業や中小企業における3Dプリンティングの導入を奨励するため、税制上の優遇措置や補助金を提供しています。こうした優遇措置は、3Dプリンティング機器や材料に必要な初期投資を抑えるのに役立ちます。このように、政府機関からの支援の高まりが市場の拡大を可能にしています。

世界の製造業の拡大

世界の製造業の拡大は、3Dプリンティング市場に大きな影響を与えています。大きな影響の1つは、さまざまな製造業で3Dプリンティング技術の採用が拡大していることです。製造業が生産プロセスの合理化、リードタイムの短縮、コスト効率の向上を目指す中、3Dプリンティングは魅力的なソリューションを提供しています。さらに、この拡大により、従来の製造工程と3Dプリンティングの連携が進んでいます。企業は3Dプリンティングを統合して金型や試作品を作成し、設計から生産へのシームレスな移行をサポートしています。したがって、世界の製造業の拡大は、採用を促進し、イノベーションを促進し、オンデマンド生産を促進し、3Dプリンティングと従来の製造プロセスとのコラボレーションを促進することによって、3Dプリンティング市場に大きな影響を与えています。

市場抑制要因

高い初期コストと限られた材料選択

3Dプリンティング技術に伴う初期コストの高さは、その広範な採用と成長を大きく妨げる可能性があります。多くの企業や組織、特に中小企業にとって、3Dプリンティング機器と関連インフラストラクチャを取得するために必要な多額の先行投資が抑止力になる可能性があります。これらの費用には、3Dプリンター本体の購入費、材料費、ソフトウェア費、メンテナンス費などが含まれます。その結果、材料の選択が制限されるため、生産ニーズに幅広い材料オプションが必要な業界では、3Dプリンティングの採用が妨げられる可能性があります。このように、高い初期費用と限られた材料選択は、3Dプリンティング市場の成長を大きく阻害しています。

コンポーネントの展望

コンポーネントに基づき、3Dプリンティング市場は製品、ソフトウェア、サービスに分類されます。サービスセグメントは、2022年の3Dプリンティング市場でかなりの成長率を確保しました。サービスセグメントは、印刷技術と材料の進歩の結果、利益を生み出す源として大きな勢いを増しています。3Dプリンティング技術は複雑な形状の製品を製造することを可能にし、従来の製造方法とは対照的に競争力のある価格を提示するため、さまざまな業界の多くの企業が、競争の激しい市場で生き残るために、製品設計から製造まですべてをアウトソーシングすると予想されます。

製品の展望

製品セグメントはさらにプリンターと材料に区分されます。プリンター分野は、2022年の3Dプリンティング市場で最大の収益シェアを獲得しました。3Dプリンターは、ラピッドプロトタイピングを提供する汎用性の高いツールであり、デザイナーが素早くコンセプトを反復し、テストすることを可能にします。これらのプリンターは、少量生産に費用対効果が高く、カスタマイズを促進し、材料の無駄を削減します。また、オンデマンドやローカライズされた製造をサポートし、サプライチェーンを短縮し、教育ツールとしての役割も果たすことができます。

プリンターの展望

プリンター分野は、産業用とデスクトップにさらに二分されます。デスクトップ分野は、2022年の3Dプリンティング市場における収益シェアで顕著な成長率を獲得しました。デスクトップ3Dプリンタは一般的に、産業グレードの同等品よりも予算に優しいため、予算が限られている個人、趣味愛好家、中小企業、教育機関が利用しやすくなっています。多くのデスクトップ3Dプリンタは、ユーザーフレンドリーな設計になっており、最小限のセットアップしか必要としないです。多くの場合、3Dプリントプロセスを簡素化する直感的なソフトウェアインターフェイスが付属しており、初心者でも利用しやすくなっています。

ソフトウェアの展望

ソフトウェアベースで、3Dプリンティング市場は設計ソフトウェア、検査ソフトウェア、プリンターソフトウェア、スキャンソフトウェアに分けられます。設計ソフトウェア分野は、2022年の3Dプリンティング市場で最大の収益シェアを記録しました。3D設計ソフトウェアは多くの利点を提供します。設計者やエンジニアが複雑な3Dモデルを正確かつ簡単に作成できるようになり、迅速なプロトタイプ作成や製品開発が容易になります。多くの場合、設計の検証や分析機能が含まれており、設計プロセスの初期段階で潜在的な問題を特定して対処するのに役立ちます。

技術展望

技術別に見ると、3Dプリンティング市場は、ステレオリソグラフィ、選択的レーザー焼結、電子ビーム溶解、溶融積層造形、その他に区分されます。ステレオリソグラフィセグメントは、2022年の3Dプリンティング市場で最大の収益シェアを獲得しました。ステレオリソグラフィー(SLA)は、その卓越した精度と表面仕上げで知られています。非常に詳細で複雑な部品の製造に優れており、宝飾品、歯科、医療分野の用途に最適です。最小限の支持構造で複雑な形状を作成できるSLAの能力は、後処理の手間を減らし、時間とリソースを節約します。

アプリケーションの展望

用途に基づき、3Dプリンティング市場は教育/調査、視覚補助、プレゼンテーションモデリング、フィット&アセンブリ、プロトタイプツーリング、金属鋳造、機能部品、その他に分類されます。2022年の3Dプリンティング市場では、フィット&アセンブリ分野が著しい成長率を示しました。3Dプリンティングの精度は、正確なフィットとアセンブリ機能を持つパーツを作成する上で非常に貴重です。シームレスに統合された部品の製造を可能にし、加工後の調整の必要性を低減します。これは製品品質の向上、製造の合理化、組み立て時間の短縮につながります。また、この技術はジャスト・イン・タイム生産をサポートし、余剰在庫をなくし、保管コストを削減します。

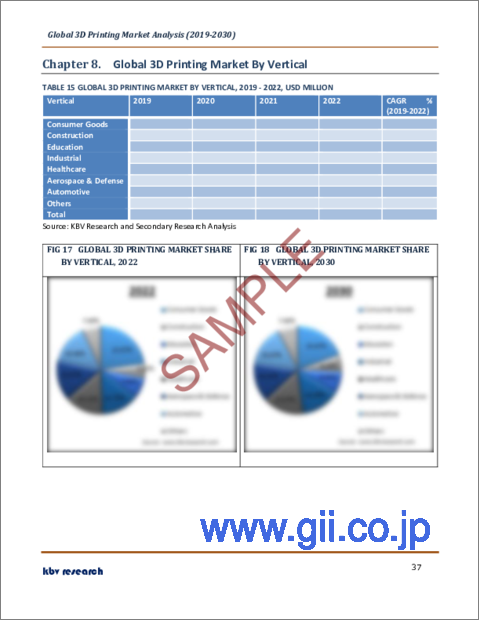

業界別展望

業界別では、3Dプリンティング市場は教育、産業、自動車、航空宇宙・防衛、ヘルスケア、消費財、建設、その他に細分化されます。航空宇宙・防衛セグメントは、2022年の3Dプリンティング市場でかなりの成長率を記録しました。3Dプリンティングは、航空機や宇宙船のコンポーネントの重量を大幅に削減し、燃料効率を高め、生産コストを下げることで、航空宇宙・防衛分野のゲームチェンジャーとなっています。この技術により、複雑で軽量な高強度部品の迅速なプロトタイピングと生産が可能になり、性能の向上、メンテナンスの必要性の低減、技術革新サイクルの短縮につながります。

地域別展望

地域別に見ると、3Dプリンティング市場は北米、欧州、アジア太平洋、LAMEAで分析されています。北米地域は、2022年の3Dプリンティング市場で最大の収益シェアを獲得しました。北米のメーカーは、少量生産、小ロット生産に3Dプリンティングを利用するようになっています。COVID-19パンデミックは、サプライチェーンの回復力の重要性を強調しました。3Dプリンティングは、ローカライズされたオンデマンド製造をサポートし、世界サプライチェーンへの依存を減らし、より弾力的な生産プロセスを保証します。北米のヘルスケア業界は、患者専用のインプラント、手術ガイド、医療機器などの用途に3Dプリントを採用しています。これらのアプリケーションは、患者の転帰を改善し、手術時間を短縮し、医療を強化します。

目次

第1章 市場範囲と調査手法

- 市場の定義

- 目的

- 市場範囲

- セグメンテーション

- 調査手法

第2章 市場の概要

- 主なハイライト

第3章 市場概要

- イントロダクション

- 概要

- 市場構成とシナリオ

- 概要

- 市場に影響を与える主な要因

- 市場促進要因

- 市場抑制要因

第4章 競合分析- 世界

- KBV Cardinal Matrix

- 最近の業界全体の戦略的展開

- パートナーシップ、コラボレーション、および契約

- 製品の発売と製品の拡大

- 買収と合併

- 地理的拡大

- 主要成功戦略

- 主な戦略

- 主要な戦略的動き

- ポーターファイブフォース分析

第5章 世界の3Dプリンティング市場:コンポーネント別

- 世界の製品市場:地域別

- 世界の3Dプリンティング市場:製品タイプ別

- 世界のプリンター市場:地域別

- 世界のプリンター市場:タイプ別

- 世界の産業市場:地域別

- 世界のデスクトップ市場:地域別

- 世界の材料市場:地域別

- 世界の3Dプリンティング市場:材料の種類別

- 世界のポリマー市場:地域別

- 世界の金属および合金市場:地域別

- 世界のセラミック市場:地域別

- 世界のその他の市場:地域別

- 世界のソフトウェア市場:地域別

- 世界の3Dプリンティング市場:ソフトウェア種類別

- 世界の設計ソフトウェア市場:地域別

- 世界の検査ソフトウェア市場:地域別

- 世界のプリンターソフトウェア市場:地域別

- 世界のスキャンソフトウェア市場:地域別

- 世界サービス市場:地域別

第6章 世界の3Dプリンティング市場:技術別

- 世界の光造形市場:地域別

- 世界の溶融蒸着モデリング市場:地域別

- 世界の選択的レーザー焼結市場:地域別

- 世界の積層造形物製造市場:地域別

- 世界の電子ビーム溶解市場:地域別

- 世界のその他の市場:地域別

第7章 世界の3Dプリンティング市場:用途別

- 世界の機能部品市場:地域別

- 世界の嵌合および組立市場:地域別

- 世界の試作工具市場:地域別

- 世界の金属鋳造市場:地域別

- 世界の視覚教材市場:地域別

- 世界のプレゼンテーションモデリング市場:地域別

- 世界の教育・調査市場:地域別

- 世界のその他の市場:地域別

第8章 世界の3Dプリンティング市場:業界別

- 世界の消費財市場:地域別

- 世界の建設市場:地域別

- 世界の教育市場:地域別

- 世界の産業市場:地域別

- 世界のヘルスケア市場:地域別

- 世界の航空宇宙および防衛市場:地域別

- 世界の自動車市場:地域別

- 世界のその他の市場:地域別

第9章 世界の3Dプリンティング市場:地域別

- 北米

- 北米の市場:国別

- 米国

- カナダ

- メキシコ

- その他北米地域

- 北米の市場:国別

- 欧州

- 欧州の市場:国別

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- イタリア

- その他欧州地域

- 欧州の市場:国別

- アジア太平洋

- アジア太平洋の市場:国別

- 中国

- 日本

- インド

- 韓国

- シンガポール

- マレーシア

- その他アジア太平洋地域

- アジア太平洋の市場:国別

- ラテンアメリカ・中東・アフリカ

- ラテンアメリカ・中東・アフリカの市場:国別

- ブラジル

- アルゼンチン

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- ナイジェリア

- その他ラテンアメリカ・中東・アフリカ地域

- ラテンアメリカ・中東・アフリカの市場:国別

第10章 企業プロファイル

- Hoganas AB

- 3D Systems Corporation

- Materialise NV

- General Electric Company

- Stratasys Ltd

- Autodesk, Inc

- The ExOne company(Desktop Metal, Inc)

- Organovo Holdings, Inc

- voxeljet AG

- Canon, Inc

第11章 3Dプリンティング市場の勝利の必須条件

LIST OF TABLES

- TABLE 1 Global 3D Printing Market, 2019 - 2022, USD Million

- TABLE 2 Global 3D Printing Market, 2023 - 2030, USD Million

- TABLE 3 Partnerships, Collaborations and Agreements- 3D Printing Market

- TABLE 4 Product Launches And Product Expansions- 3D Printing Market

- TABLE 5 Acquisition and Mergers- 3D Printing Market

- TABLE 6 Geographical Expansions- 3D Printing Market

- TABLE 7 Global 3D Printing Market By Component, 2019 - 2022, USD Million

- TABLE 8 Global 3D Printing Market By Component, 2023 - 2030, USD Million

- TABLE 9 Global Product Market by Region, 2019 - 2022, USD Million

- TABLE 10 Global Product Market by Region, 2023 - 2030, USD Million

- TABLE 11 Global 3D Printing Market By Product Type, 2019 - 2022, USD Million

- TABLE 12 Global 3D Printing Market By Product Type, 2023 - 2030, USD Million

- TABLE 13 Global Printer Market by Region, 2019 - 2022, USD Million

- TABLE 14 Global Printer Market by Region, 2023 - 2030, USD Million

- TABLE 15 Global Printer Market By Type, 2019 - 2022, USD Million

- TABLE 16 Global Printer Market By Type, 2023 - 2030, USD Million

- TABLE 17 Global Industrial Market by Region, 2019 - 2022, USD Million

- TABLE 18 Global Industrial Market by Region, 2023 - 2030, USD Million

- TABLE 19 Global Desktop Market by Region, 2019 - 2022, USD Million

- TABLE 20 Global Desktop Market by Region, 2023 - 2030, USD Million

- TABLE 21 Global Material Market by Region, 2019 - 2022, USD Million

- TABLE 22 Global Material Market by Region, 2023 - 2030, USD Million

- TABLE 23 Global 3D Printing Market By Material Type, 2019 - 2022, USD Million

- TABLE 24 Global 3D Printing Market By Material Type, 2023 - 2030, USD Million

- TABLE 25 Global Polymer Market by Region, 2019 - 2022, USD Million

- TABLE 26 Global Polymer Market by Region, 2023 - 2030, USD Million

- TABLE 27 Global Metal & Alloys Market by Region, 2019 - 2022, USD Million

- TABLE 28 Global Metal & Alloys Market by Region, 2023 - 2030, USD Million

- TABLE 29 Global Ceramic Market by Region, 2019 - 2022, USD Million

- TABLE 30 Global Ceramic Market by Region, 2023 - 2030, USD Million

- TABLE 31 Global Others Market by Region, 2019 - 2022, USD Million

- TABLE 32 Global Others Market by Region, 2023 - 2030, USD Million

- TABLE 33 Global Software Market by Region, 2019 - 2022, USD Million

- TABLE 34 Global Software Market by Region, 2023 - 2030, USD Million

- TABLE 35 Global 3D Printing Market By Software Type, 2019 - 2022, USD Million

- TABLE 36 Global 3D Printing Market By Software Type, 2023 - 2030, USD Million

- TABLE 37 Global Design Software Market by Region, 2019 - 2022, USD Million

- TABLE 38 Global Design Software Market by Region, 2023 - 2030, USD Million

- TABLE 39 Global Inspection Software Market by Region, 2019 - 2022, USD Million

- TABLE 40 Global Inspection Software Market by Region, 2023 - 2030, USD Million

- TABLE 41 Global Printer Software Market by Region, 2019 - 2022, USD Million

- TABLE 42 Global Printer Software Market by Region, 2023 - 2030, USD Million

- TABLE 43 Global Scanning Software Market by Region, 2019 - 2022, USD Million

- TABLE 44 Global Scanning Software Market by Region, 2023 - 2030, USD Million

- TABLE 45 Global Services Market by Region, 2019 - 2022, USD Million

- TABLE 46 Global Services Market by Region, 2023 - 2030, USD Million

- TABLE 47 Global 3D Printing Market By Technology, 2019 - 2022, USD Million

- TABLE 48 Global 3D Printing Market By Technology, 2023 - 2030, USD Million

- TABLE 49 Global Stereolithography Market by Region, 2019 - 2022, USD Million

- TABLE 50 Global Stereolithography Market by Region, 2023 - 2030, USD Million

- TABLE 51 Global Fused Deposition Modeling Market by Region, 2019 - 2022, USD Million

- TABLE 52 Global Fused Deposition Modeling Market by Region, 2023 - 2030, USD Million

- TABLE 53 Global Selective Laser Sintering Market by Region, 2019 - 2022, USD Million

- TABLE 54 Global Selective Laser Sintering Market by Region, 2023 - 2030, USD Million

- TABLE 55 Global Laminated object Manufacturing Market by Region, 2019 - 2022, USD Million

- TABLE 56 Global Laminated object Manufacturing Market by Region, 2023 - 2030, USD Million

- TABLE 57 Global Electron Beam Melting Market by Region, 2019 - 2022, USD Million

- TABLE 58 Global Electron Beam Melting Market by Region, 2023 - 2030, USD Million

- TABLE 59 Global Others Market by Region, 2019 - 2022, USD Million

- TABLE 60 Global Others Market by Region, 2023 - 2030, USD Million

- TABLE 61 Global 3D Printing Market By Application, 2019 - 2022, USD Million

- TABLE 62 Global 3D Printing Market By Application, 2023 - 2030, USD Million

- TABLE 63 Global Functional Parts Market by Region, 2019 - 2022, USD Million

- TABLE 64 Global Functional Parts Market by Region, 2023 - 2030, USD Million

- TABLE 65 Global Fit & Assembly Market by Region, 2019 - 2022, USD Million

- TABLE 66 Global Fit & Assembly Market by Region, 2023 - 2030, USD Million

- TABLE 67 Global Prototype Tooling Market by Region, 2019 - 2022, USD Million

- TABLE 68 Global Prototype Tooling Market by Region, 2023 - 2030, USD Million

- TABLE 69 Global Metal Casting Market by Region, 2019 - 2022, USD Million

- TABLE 70 Global Metal Casting Market by Region, 2023 - 2030, USD Million

- TABLE 71 Global Visual Aids Market by Region, 2019 - 2022, USD Million

- TABLE 72 Global Visual Aids Market by Region, 2023 - 2030, USD Million

- TABLE 73 Global Presentation Modeling Market by Region, 2019 - 2022, USD Million

- TABLE 74 Global Presentation Modeling Market by Region, 2023 - 2030, USD Million

- TABLE 75 Global Education/Research Market by Region, 2019 - 2022, USD Million

- TABLE 76 Global Education/Research Market by Region, 2023 - 2030, USD Million

- TABLE 77 Global Others Market by Region, 2019 - 2022, USD Million

- TABLE 78 Global Others Market by Region, 2023 - 2030, USD Million

- TABLE 79 Global 3D Printing Market By Vertical, 2019 - 2022, USD Million

- TABLE 80 Global 3D Printing Market By Vertical, 2023 - 2030, USD Million

- TABLE 81 Global Consumer Goods Market by Region, 2019 - 2022, USD Million

- TABLE 82 Global Consumer Goods Market by Region, 2023 - 2030, USD Million

- TABLE 83 Global Construction Market by Region, 2019 - 2022, USD Million

- TABLE 84 Global Construction Market by Region, 2023 - 2030, USD Million

- TABLE 85 Global Education Market by Region, 2019 - 2022, USD Million

- TABLE 86 Global Education Market by Region, 2023 - 2030, USD Million

- TABLE 87 Global Industrial Market by Region, 2019 - 2022, USD Million

- TABLE 88 Global Industrial Market by Region, 2023 - 2030, USD Million

- TABLE 89 Global Healthcare Market by Region, 2019 - 2022, USD Million

- TABLE 90 Global Healthcare Market by Region, 2023 - 2030, USD Million

- TABLE 91 Global Aerospace & Defense Market by Region, 2019 - 2022, USD Million

- TABLE 92 Global Aerospace & Defense Market by Region, 2023 - 2030, USD Million

- TABLE 93 Global Automotive Market by Region, 2019 - 2022, USD Million

- TABLE 94 Global Automotive Market by Region, 2023 - 2030, USD Million

- TABLE 95 Global Others Market by Region, 2019 - 2022, USD Million

- TABLE 96 Global Others Market by Region, 2023 - 2030, USD Million

- TABLE 97 Global 3D Printing Market By Region, 2019 - 2022, USD Million

- TABLE 98 Global 3D Printing Market By Region, 2023 - 2030, USD Million

- TABLE 99 North America 3D Printing Market, 2019 - 2022, USD Million

- TABLE 100 North America 3D Printing Market, 2023 - 2030, USD Million

- TABLE 101 North America 3D Printing Market By Component, 2019 - 2022, USD Million

- TABLE 102 North America 3D Printing Market By Component, 2023 - 2030, USD Million

- TABLE 103 North America Product Market by Country, 2019 - 2022, USD Million

- TABLE 104 North America Product Market by Country, 2023 - 2030, USD Million

- TABLE 105 North America 3D Printing Market By Product Type, 2019 - 2022, USD Million

- TABLE 106 North America 3D Printing Market By Product Type, 2023 - 2030, USD Million

- TABLE 107 North America Printer Market by Region, 2019 - 2022, USD Million

- TABLE 108 North America Printer Market by Region, 2023 - 2030, USD Million

- TABLE 109 North America Printer Market By Type, 2019 - 2022, USD Million

- TABLE 110 North America Printer Market By Type, 2023 - 2030, USD Million

- TABLE 111 North America Industrial Market by Region, 2019 - 2022, USD Million

- TABLE 112 North America Industrial Market by Region, 2023 - 2030, USD Million

- TABLE 113 North America Desktop Market by Region, 2019 - 2022, USD Million

- TABLE 114 North America Desktop Market by Region, 2023 - 2030, USD Million

- TABLE 115 North America Material Market by Region, 2019 - 2022, USD Million

- TABLE 116 North America Material Market by Region, 2023 - 2030, USD Million

- TABLE 117 North America 3D Printing Market By Material Type, 2019 - 2022, USD Million

- TABLE 118 North America 3D Printing Market By Material Type, 2023 - 2030, USD Million

- TABLE 119 North America Polymer Market by Country, 2019 - 2022, USD Million

- TABLE 120 North America Polymer Market by Country, 2023 - 2030, USD Million

- TABLE 121 North America Metal & Alloys Market by Country, 2019 - 2022, USD Million

- TABLE 122 North America Metal & Alloys Market by Country, 2023 - 2030, USD Million

- TABLE 123 North America Ceramic Market by Country, 2019 - 2022, USD Million

- TABLE 124 North America Ceramic Market by Country, 2023 - 2030, USD Million

- TABLE 125 North America Others Market by Country, 2019 - 2022, USD Million

- TABLE 126 North America Others Market by Country, 2023 - 2030, USD Million

- TABLE 127 North America Software Market by Country, 2019 - 2022, USD Million

- TABLE 128 North America Software Market by Country, 2023 - 2030, USD Million

- TABLE 129 North America 3D Printing Market By Software Type, 2019 - 2022, USD Million

- TABLE 130 North America 3D Printing Market By Software Type, 2023 - 2030, USD Million

- TABLE 131 North America Design Software Market by Country, 2019 - 2022, USD Million

- TABLE 132 North America Design Software Market by Country, 2023 - 2030, USD Million

- TABLE 133 North America Inspection Software Market by Country, 2019 - 2022, USD Million

- TABLE 134 North America Inspection Software Market by Country, 2023 - 2030, USD Million

- TABLE 135 North America Printer Software Market by Country, 2019 - 2022, USD Million

- TABLE 136 North America Printer Software Market by Country, 2023 - 2030, USD Million

- TABLE 137 North America Scanning Software Market by Country, 2019 - 2022, USD Million

- TABLE 138 North America Scanning Software Market by Country, 2023 - 2030, USD Million

- TABLE 139 North America Services Market by Country, 2019 - 2022, USD Million

- TABLE 140 North America Services Market by Country, 2023 - 2030, USD Million

- TABLE 141 North America 3D Printing Market By Technology, 2019 - 2022, USD Million

- TABLE 142 North America 3D Printing Market By Technology, 2023 - 2030, USD Million

- TABLE 143 North America Stereolithography Market by Country, 2019 - 2022, USD Million

- TABLE 144 North America Stereolithography Market by Country, 2023 - 2030, USD Million

- TABLE 145 North America Fused Deposition Modeling Market by Country, 2019 - 2022, USD Million

- TABLE 146 North America Fused Deposition Modeling Market by Country, 2023 - 2030, USD Million

- TABLE 147 North America Selective Laser Sintering Market by Country, 2019 - 2022, USD Million

- TABLE 148 North America Selective Laser Sintering Market by Country, 2023 - 2030, USD Million

- TABLE 149 North America Laminated object Manufacturing Market by Country, 2019 - 2022, USD Million

- TABLE 150 North America Laminated object Manufacturing Market by Country, 2023 - 2030, USD Million

- TABLE 151 North America Electron Beam Melting Market by Country, 2019 - 2022, USD Million

- TABLE 152 North America Electron Beam Melting Market by Country, 2023 - 2030, USD Million

- TABLE 153 North America Others Market by Country, 2019 - 2022, USD Million

- TABLE 154 North America Others Market by Country, 2023 - 2030, USD Million

- TABLE 155 North America 3D Printing Market By Application, 2019 - 2022, USD Million

- TABLE 156 North America 3D Printing Market By Application, 2023 - 2030, USD Million

- TABLE 157 North America Functional Parts Market by Country, 2019 - 2022, USD Million

- TABLE 158 North America Functional Parts Market by Country, 2023 - 2030, USD Million

- TABLE 159 North America Fit & Assembly Market by Country, 2019 - 2022, USD Million

- TABLE 160 North America Fit & Assembly Market by Country, 2023 - 2030, USD Million

- TABLE 161 North America Prototype Tooling Market by Country, 2019 - 2022, USD Million

- TABLE 162 North America Prototype Tooling Market by Country, 2023 - 2030, USD Million

- TABLE 163 North America Metal Casting Market by Country, 2019 - 2022, USD Million

- TABLE 164 North America Metal Casting Market by Country, 2023 - 2030, USD Million

- TABLE 165 North America Visual Aids Market by Country, 2019 - 2022, USD Million

- TABLE 166 North America Visual Aids Market by Country, 2023 - 2030, USD Million

- TABLE 167 North America Presentation Modeling Market by Country, 2019 - 2022, USD Million

- TABLE 168 North America Presentation Modeling Market by Country, 2023 - 2030, USD Million

- TABLE 169 North America Education/Research Market by Country, 2019 - 2022, USD Million

- TABLE 170 North America Education/Research Market by Country, 2023 - 2030, USD Million

- TABLE 171 North America Others Market by Country, 2019 - 2022, USD Million

- TABLE 172 North America Others Market by Country, 2023 - 2030, USD Million

- TABLE 173 North America 3D Printing Market By Vertical, 2019 - 2022, USD Million

- TABLE 174 North America 3D Printing Market By Vertical, 2023 - 2030, USD Million

- TABLE 175 North America Consumer Goods Market by Country, 2019 - 2022, USD Million

- TABLE 176 North America Consumer Goods Market by Country, 2023 - 2030, USD Million

- TABLE 177 North America Construction Market by Country, 2019 - 2022, USD Million

- TABLE 178 North America Construction Market by Country, 2023 - 2030, USD Million

- TABLE 179 North America Education Market by Country, 2019 - 2022, USD Million

- TABLE 180 North America Education Market by Country, 2023 - 2030, USD Million

- TABLE 181 North America Industrial Market by Country, 2019 - 2022, USD Million

- TABLE 182 North America Industrial Market by Country, 2023 - 2030, USD Million

- TABLE 183 North America Healthcare Market by Country, 2019 - 2022, USD Million

- TABLE 184 North America Healthcare Market by Country, 2023 - 2030, USD Million

- TABLE 185 North America Aerospace & Defense Market by Country, 2019 - 2022, USD Million

- TABLE 186 North America Aerospace & Defense Market by Country, 2023 - 2030, USD Million

- TABLE 187 North America Automotive Market by Country, 2019 - 2022, USD Million

- TABLE 188 North America Automotive Market by Country, 2023 - 2030, USD Million

- TABLE 189 North America Others Market by Country, 2019 - 2022, USD Million

- TABLE 190 North America Others Market by Country, 2023 - 2030, USD Million

- TABLE 191 North America 3D Printing Market By Country, 2019 - 2022, USD Million

- TABLE 192 North America 3D Printing Market By Country, 2023 - 2030, USD Million

- TABLE 193 US 3D Printing Market, 2019 - 2022, USD Million

- TABLE 194 US 3D Printing Market, 2023 - 2030, USD Million

- TABLE 195 US 3D Printing Market By Component, 2019 - 2022, USD Million

- TABLE 196 US 3D Printing Market By Component, 2023 - 2030, USD Million

- TABLE 197 US 3D Printing Market By Product Type, 2019 - 2022, USD Million

- TABLE 198 US 3D Printing Market By Product Type, 2023 - 2030, USD Million

- TABLE 199 US Printer Market By Type, 2019 - 2022, USD Million

- TABLE 200 US Printer Market By Type, 2023 - 2030, USD Million

- TABLE 201 US 3D Printing Market By Material Type, 2019 - 2022, USD Million

- TABLE 202 US 3D Printing Market By Material Type, 2023 - 2030, USD Million

- TABLE 203 US 3D Printing Market By Software Type, 2019 - 2022, USD Million

- TABLE 204 US 3D Printing Market By Software Type, 2023 - 2030, USD Million

- TABLE 205 US 3D Printing Market By Technology, 2019 - 2022, USD Million

- TABLE 206 US 3D Printing Market By Technology, 2023 - 2030, USD Million

- TABLE 207 US 3D Printing Market By Application, 2019 - 2022, USD Million

- TABLE 208 US 3D Printing Market By Application, 2023 - 2030, USD Million

- TABLE 209 US 3D Printing Market By Vertical, 2019 - 2022, USD Million

- TABLE 210 US 3D Printing Market By Vertical, 2023 - 2030, USD Million

- TABLE 211 Canada 3D Printing Market, 2019 - 2022, USD Million

- TABLE 212 Canada 3D Printing Market, 2023 - 2030, USD Million

- TABLE 213 Canada 3D Printing Market By Component, 2019 - 2022, USD Million

- TABLE 214 Canada 3D Printing Market By Component, 2023 - 2030, USD Million

- TABLE 215 Canada 3D Printing Market By Product Type, 2019 - 2022, USD Million

- TABLE 216 Canada 3D Printing Market By Product Type, 2023 - 2030, USD Million

- TABLE 217 Canada Printer Market By Type, 2019 - 2022, USD Million

- TABLE 218 Canada Printer Market By Type, 2023 - 2030, USD Million

- TABLE 219 Canada 3D Printing Market By Material Type, 2019 - 2022, USD Million

- TABLE 220 Canada 3D Printing Market By Material Type, 2023 - 2030, USD Million

- TABLE 221 Canada 3D Printing Market By Software Type, 2019 - 2022, USD Million

- TABLE 222 Canada 3D Printing Market By Software Type, 2023 - 2030, USD Million

- TABLE 223 Canada 3D Printing Market By Technology, 2019 - 2022, USD Million

- TABLE 224 Canada 3D Printing Market By Technology, 2023 - 2030, USD Million

- TABLE 225 Canada 3D Printing Market By Application, 2019 - 2022, USD Million

- TABLE 226 Canada 3D Printing Market By Application, 2023 - 2030, USD Million

- TABLE 227 Canada 3D Printing Market By Vertical, 2019 - 2022, USD Million

- TABLE 228 Canada 3D Printing Market By Vertical, 2023 - 2030, USD Million

- TABLE 229 Mexico 3D Printing Market, 2019 - 2022, USD Million

- TABLE 230 Mexico 3D Printing Market, 2023 - 2030, USD Million

- TABLE 231 Mexico 3D Printing Market By Component, 2019 - 2022, USD Million

- TABLE 232 Mexico 3D Printing Market By Component, 2023 - 2030, USD Million

- TABLE 233 Mexico 3D Printing Market By Product Type, 2019 - 2022, USD Million

- TABLE 234 Mexico 3D Printing Market By Product Type, 2023 - 2030, USD Million

- TABLE 235 Mexico Printer Market By Type, 2019 - 2022, USD Million

- TABLE 236 Mexico Printer Market By Type, 2023 - 2030, USD Million

- TABLE 237 Mexico 3D Printing Market By Material Type, 2019 - 2022, USD Million

- TABLE 238 Mexico 3D Printing Market By Material Type, 2023 - 2030, USD Million

- TABLE 239 Mexico 3D Printing Market By Software Type, 2019 - 2022, USD Million

- TABLE 240 Mexico 3D Printing Market By Software Type, 2023 - 2030, USD Million

- TABLE 241 Mexico 3D Printing Market By Technology, 2019 - 2022, USD Million

- TABLE 242 Mexico 3D Printing Market By Technology, 2023 - 2030, USD Million

- TABLE 243 Mexico 3D Printing Market By Application, 2019 - 2022, USD Million

- TABLE 244 Mexico 3D Printing Market By Application, 2023 - 2030, USD Million

- TABLE 245 Mexico 3D Printing Market By Vertical, 2019 - 2022, USD Million

- TABLE 246 Mexico 3D Printing Market By Vertical, 2023 - 2030, USD Million

- TABLE 247 Rest of North America 3D Printing Market, 2019 - 2022, USD Million

- TABLE 248 Rest of North America 3D Printing Market, 2023 - 2030, USD Million

- TABLE 249 Rest of North America 3D Printing Market By Component, 2019 - 2022, USD Million

- TABLE 250 Rest of North America 3D Printing Market By Component, 2023 - 2030, USD Million

- TABLE 251 Rest of North America 3D Printing Market By Product Type, 2019 - 2022, USD Million

- TABLE 252 Rest of North America 3D Printing Market By Product Type, 2023 - 2030, USD Million

- TABLE 253 Rest of North America Printer Market By Type, 2019 - 2022, USD Million

- TABLE 254 Rest of North America Printer Market By Type, 2023 - 2030, USD Million

- TABLE 255 Rest of North America 3D Printing Market By Material Type, 2019 - 2022, USD Million

- TABLE 256 Rest of North America 3D Printing Market By Material Type, 2023 - 2030, USD Million

- TABLE 257 Rest of North America 3D Printing Market By Software Type, 2019 - 2022, USD Million

- TABLE 258 Rest of North America 3D Printing Market By Software Type, 2023 - 2030, USD Million

- TABLE 259 Rest of North America 3D Printing Market By Technology, 2019 - 2022, USD Million

- TABLE 260 Rest of North America 3D Printing Market By Technology, 2023 - 2030, USD Million

- TABLE 261 Rest of North America 3D Printing Market By Application, 2019 - 2022, USD Million

- TABLE 262 Rest of North America 3D Printing Market By Application, 2023 - 2030, USD Million

- TABLE 263 Rest of North America 3D Printing Market By Vertical, 2019 - 2022, USD Million

- TABLE 264 Rest of North America 3D Printing Market By Vertical, 2023 - 2030, USD Million

The Global 3D Printing Market size is expected to reach $86.4 billion by 2030, rising at a market growth of 21.4% CAGR during the forecast period.

3D printing is transforming healthcare by allowing the production of patient-specific implants, prosthetics, and anatomical models for surgical planning. Consequently, the Healthcare segment would register 1/5th share in the market by 2030. This technology improves patient outcomes, reduces surgery times, and enhances medical training. The dental industry benefits from 3D-printed crowns, bridges, and orthodontic devices. Drug delivery systems and tissue engineering applications have also emerged, offering promising solutions for personalized medicine and regenerative therapies. The efficiency, precision, and customization capabilities of 3D printing in healthcare significantly impacts patient care and the medical field's overall advancement.

The major strategies followed by the market participants are Product Launches as the key developmental strategy to keep pace with the changing demands of end users. For instance, In June, 2023, Voxeljet AG unveiled Cold IOB, a new inorganic 3D process technology. This launch would be an important step towards further adoption of printed cores and molds with inorganic binders in the foundry industry. Additionally, In June, 2022, Stratasys unveiled Stratasys RadioMatrix, to produce 'radio-realistic models' that could be under CT scans & X-rays.

Based on the Analysis presented in the KBV Cardinal matrix; Canon, Inc. is the forerunner in the 3D Printing Market. Companies such as Autodesk, Inc., Stratasys Ltd., and 3D Systems Corporation are some of the key innovators in 3D Printing Market. In May, 2022, Stratasys launched F190 CR and F370 CR machines, F123 Series of FDM 3D printers, and FDM Nylon-CF10 material, new carbon fiber-reinforced, developed for manufacturers & industrial machinists to produce end-use components, and jigs, fixtures & work holding tools.

Market Growth Factors

Rising regulatory support by national and local government bodies

Governments worldwide recognize the potential of 3D printing to drive innovation, boost local manufacturing, and address various societal challenges. China has made significant investments in 3D printing as part of its "Made in China 2025" initiative, which aims to upgrade its manufacturing capabilities. The German government has supported various 3D printing projects and research initiatives, especially in Industry 4.0. Germany's Fraunhofer Institute, a leading research organization, has been involved in numerous additive manufacturing projects. Some governments offer tax incentives and subsidies to encourage the adoption of 3D printing in manufacturing and small businesses. These incentives can help reduce the initial investment required for 3D printing equipment and materials. Thus, the rising support from government bodies is enabling the expansion of the market.

Expansion of the global manufacturing sector

The expansion of the global manufacturing sector profoundly impacts the 3D printing market. One significant effect is the growing adoption of 3D printing technology across various manufacturing industries. As manufacturers seek to streamline their production processes, reduce lead times, and improve cost efficiency, 3D printing offers an attractive solution. Moreover, the expansion has led to greater collaboration between traditional manufacturing processes and 3D printing. Companies are integrating 3D printing to create tooling, molds, and prototypes, supporting a seamless transition from design to production. Therefore, the expansion of the global manufacturing sector has significantly impacted the 3D printing market by driving adoption, fostering innovation, promoting on-demand production, and encouraging collaboration between 3D printing and traditional manufacturing processes.

Market Restraining Factors

High initial costs and limited material selection

The high initial costs associated with 3D printing technology can significantly hinder its broader adoption and growth. For many businesses and organizations, especially smaller enterprises, the substantial upfront investment required to acquire 3D printing equipment and related infrastructure can be a deterrent. These costs encompass the purchase of the 3D printer itself and the expenditure on materials, software, and maintenance. Consequently, the restricted material selection can hinder the adoption of 3D printing in industries that demand a broader range of material options for their production needs. Thus, the high initial costs and limited material selection significantly deter the growth of the 3D printing market.

Component Outlook

Based on components, the 3D printing market is characterized into product, software, and services. The services segment procured a considerable growth rate in the 3D printing market in 2022. The service segment is gaining significant momentum as a source of profit generation as a result of advancements in printing technology and materials. Many businesses across various industries are anticipated to outsource everything, from product design to production, to survive in the fiercely competitive markets, as 3D printing technology makes it possible to manufacture products with complicated shapes and presents competitive pricing in contrast to traditional manufacturing methods.

Product Outlook

The product segment is further segmented into printer and material. The printer segment acquired the largest revenue share in the 3D printing market in 2022. 3D printers are versatile tools that offer rapid prototyping, enabling designers to quickly iterate and test their concepts. These printers are cost-effective for low-volume production, promote customization, and reduce material waste. They support on-demand and localized manufacturing, shortening supply chains, and can serve as educational tools.

Printer Outlook

The printer segment is further bifurcated into industrial and desktop. The desktop segment garnered a remarkable growth rate in the revenue share in the 3D printing market in 2022. Desktop 3D printers are typically more budget-friendly than industrial-grade counterparts, making them accessible to individuals, hobbyists, small businesses, and educational institutions with limited budgets. Many desktop 3D printers are designed to be user-friendly and require minimal setup. They often come with intuitive software interfaces that simplify the 3D printing process, making it accessible to beginners.

Software Outlook

On the basis of software, the 3D printing market is divided into design software, inspection software, printer software, and scanning software. The design software segment recorded the largest revenue share in the 3D printing market in 2022. 3D design software offers a plethora of benefits. It empowers designers and engineers to create intricate 3D models with precision and ease, facilitating rapid prototyping and product development. They often include design validation and analysis features, helping identify and address potential issues early in the design process.

Technology Outlook

By technology, the 3D printing market is segmented into stereolithography, selective laser sintering, electron beam melting, fused deposition modeling, laminated object manufacturing, and others. The stereolithography segment garnered the maximum revenue share in the 3D printing market in 2022. Stereolithography (SLA) is known for its exceptional precision and surface finish. It excels at producing highly detailed and intricate parts, making it ideal for jewelry, dentistry, and medical field applications. SLA's ability to create complex geometries with minimal support structures reduces post-processing efforts, saving time and resources.

Application Outlook

Based on application, the 3D printing market is classified into education/research, visual aids, presentation modeling, fit & assembly, prototype tooling, metal casting, functional parts, and others. The fit and assembly segment witnessed a remarkable growth rate in the 3D printing market in 2022. 3D printing's precision in creating parts with exact fit and assembly capabilities is invaluable. It enables the production of seamlessly integrated components, reducing the need for post-processing adjustments. This leads to enhanced product quality, streamlined manufacturing, and reduced assembly time. The technology also supports just-in-time production, eliminating excess inventory and reducing storage costs.

Vertical Outlook

On the basis of vertical, the 3D printing market is fragmented into education, industrial, automotive, aerospace & defense, healthcare, consumer goods, construction, and others. The aerospace and defense segment recorded a considerable growth rate in the 3D printing market in 2022. 3D printing has become a game-changer in the aerospace and defense sectors by significantly reducing the weight of aircraft and spacecraft components, enhancing fuel efficiency, and lowering production costs. The technology allows for the rapid prototyping and production of complex, lightweight, and high-strength parts, which translates to improved performance, reduced maintenance needs, and faster innovation cycles.

Regional Outlook

Region-wise, the 3D printing market is analyzed across North America, Europe, Asia Pacific, and LAMEA. The North America region procured the maximum revenue share in the 3D printing market in 2022. North American manufacturers increasingly use 3D printing for low-volume and small-batch production runs. The COVID-19 pandemic underscored the importance of supply chain resilience. 3D printing supports localized and on-demand manufacturing, reducing reliance on global supply chains and ensuring a more resilient production process. North America's healthcare industry has embraced 3D printing for applications like patient-specific implants, surgical guides, and medical devices. These applications improve patient outcomes, reduce surgery times, and enhance medical treatment.

The market research report covers the analysis of key stake holders of the market. Key companies profiled in the report include Hoganas AB, 3D Systems Corporation, Materialise NV, General Electric Company, Stratasys Ltd., Autodesk, Inc., The ExOne company (Desktop Metal, Inc.), Organovo Holdings, Inc., voxeljet AG and Canon, Inc.

Recent Strategies Deployed in 3D Printing Market

Product Launches and Product Expansions:

Jun-2023: Voxeljet AG unveiled Cold IOB, a new inorganic 3D process technology. This launch would be an important step towards further adoption of printed cores and molds with inorganic binders in the foundry industry.

Oct-2022: General Electric Company released the Series 3 binder jet platform. The Series 3 has the capability of depositing a proprietary binder into parts with a maximum weight of 25 kilos and 500µm wall thickness. Series 3 is based on the Beta versions of H1 Alpha and H2 models and facilitates continuous production of parts that are of better quality than their casting equivalents.

Jun-2022: Stratasys unveiled Stratasys RadioMatrix, the latest material for its Digital Anatomy 3D printers. This material makes it possible to produce 'radio-realistic models' that could be under CT scans & X-rays. In addition, the material is the first radiopaque material available for polymer 3D printing leading providers to largely adopt Digital Anatomy systems, which would enable consumers to create full color & biomechanically realistic models for training, pre-surgical planning & medical device development.

May-2022: Stratasys launched F190 CR and F370 CR machines, F123 Series of FDM 3D printers, and FDM Nylon-CF10 material, new carbon fiber-reinforced. The latest composite 3D printers are developed for manufacturers & industrial machinists to produce end-use components, and jigs, fixtures & work holding tools.

Nov-2021: General Electric Additive unveiled a cloud-based process management software platform at Formnext. The main advantage of the Print Model module comprises automation of manual tasks, like support generation, nesting & slicing to process an ability to carry out design work while process-intensive tasks run in the background.

Oct-2021: Autodesk unveiled the latest version of its Netfabb 3D printing, design, and simulation platform. This platform is developed to offer customers a more refined experience and update its tool pathing and simulation tools.

May-2021: Stratasys introduced three new 3D printers. These printers together would address a huge portion of the multi-billion-dollar market growth prospect in additive manufacturing of end-use parts. These systems would enhance the shift from conventional to additive manufacturing for low-to-mid-volume production applications underserved by conventional manufacturing ways.

Mar-2021: Stratasys launched the J5 DentaJet 3D printer. The J5 DentaJet is the only multi-material dental 3D printer, that allows technicians to load mixed trays of dental parts. The new 3D printer can give at least five times more dental parts on a single mixed tray than competitive 3D printers, yet its compact footprint takes only 4.6 sq. ft (.43m2) of floor space.

Feb-2021: 3D Systems unveiled a novel High-Speed Fusion industrial 3D printer platform & material portfolio. Under this collaboration with Jabil, this dynamic High-Speed Fusion family of products, comprising the Roadrunner 3D printer, is likely to deliver the best economics of any high throughput industrial fused filament offering in the present market.

Partnerships, Collaborations & Agreements:

May-2023: Materialise NV teamed up with Vuzix Corporation, an optical technology company that specializes in making AR solutions. With this collaboration, the company aims to help industrial smart eyewear advance technologically and accelerate consumer and business market adoption of smart eyewear.

Mar-2022: Stratasys formed a partnership with Oqton and Riven with the continued expansion of the GrabCAD Software Partner Program. This Program is part of the latest unveiled GrabCAD Additive Manufacturing Platform, which would unify GrabCAD applications & third-party GrabCAD Software Partners through the GrabCAD Software Development Kit (SDK).

Mar-2022: Organovo Holdings, Inc. signed an agreement with BICO, a leading provider of life science solutions and laboratory automation. Following this agreement, both companies aimed to widen their product portfolio, and further strengthen it to continue to advance in the 3D bioprinting space.

Feb-2022: 3D Systems Corporations entered into a partnership with Saremco Dental AG. The company aimed to improve its digital dentistry material portfolio. Under this partnership, the companies would expand the distribution of the Swiss manufacturer's CROWNTEC combined resins in the U.S. for 3D printing of biocompatible permanent restorations like onlays, crowns, veneers, inlays, & artificial teeth for dentures within dental clinics & labs.

Nov-2021: Stratasys entered into a partnership with ECCO, a Danish shoe manufacturer and retailer. This partnership aimed to innovate footwear manufacturing using 3D printing technology, which would boost automation and a more simplified development process.

Sep-2021: General Electric Renewable Energy formed a partnership with Fraunhofer and Voxeljet. The companies aimed to create the world's largest 3D printer for offshore wind applications. Under this partnership, the companies would develop a large-format 3D printer capable of producing sand molds to cast metal parts for use in an offshore wind turbine nacelle.

Feb-2021: ExOne came into a partnership with ABC Corporation. This partnership aimed to authorize ABC Corporation as a channel partner to sell ExOne industrial solutions in South Korea.

Mergers & Acquisition:

Sep-2022: Materialise acquired Identify3D, a company that develops software to encrypt, distribute, and trace the flow of digital parts across complex supply chains. With this acquisition, the company would enable the manufacturers to secure the flow of digital parts and maintain a competitive advantage.

Feb-2022: 3D Systems took over Titan Additive, a polymer extrusion 3D printing company. This acquisition aimed at expanding the company's reach in the medical & industrial market, which would enable the company to address its consumers' needs for large build volumes, superior performance & enhanced productivity at a lesser cost.

Feb-2022: 3D Systems signed an agreement to acquire Kumovis, an additive manufacturing solutions provider for personalized healthcare applications. In this acquisition, 3D Systems aimed to add a unique extrusion technology to its extensive polymer printing healthcare portfolio, enabling the company to expand its addressable market for customized healthcare applications.

Nov-2021: Materialize signed an agreement to acquire Link3D, an additive workflow & digital manufacturing software company. By combining Link3D's additive MES (Manufacturing Execution System) solution with the Materialise Magics software suite into a unified, cloud-based software platform, various manufacturers would be able to run and constantly enhance the most efficient, repeatable, automated, and controlled processes to mass-produce identical or personalized products.

Oct-2021: 3D Systems took over Volumetric Biotechnologies, a Houston-based biotech company. Under this acquisition, 3D Systems would establish a top-class research capability in Houston, Texas that would be determined to lead in technologies associated with life sciences.

Apr-2021: The ExOne Company took over Freshmade 3D, an Ohio-based startup. This acquisition aimed to strengthen ExOne's position as a provider of large-format 3D printed tooling for various industrial applications.

Geographical Expansions:

Sep-2022: Autodesk expanded its geographical footprint by opening its UK Technology Centre in Birmingham. This center would assist people in solving the world's most innovative high-value manufacturing challenges. This center would house a variety of tools from subtractive to additive manufacturing (AM) and robotics and would benefit customers such as BMW and GKN Aerospace

Apr-2022: General Electric Company announced the establishment of a new research and development facility in Bergen, New York, United States. The new facility would be used for researching 3D printing of wind turbine's concrete base.

Feb-2021: 3D Systems expanded its geographical footprints in South Carolina headquarters through the addition of 100,000 square feet in space. The expansion is established as a vehicle that would bring to market his Stereolithography 3D printing technology.

Scope of the Study

Market Segments covered in the Report:

By Component

- Product

- Printer

- Industrial

- Desktop

- Material

- Polymer

- Metal & Alloys

- Ceramic

- Others

- Software

- Design Software

- Inspection Software

- Printer Software

- Scanning Software

- Services

By Technology

- Stereolithography

- Fused Deposition Modeling

- Selective Laser Sintering

- Laminated object Manufacturing

- Electron Beam Melting

- Others

By Application

- Functional Parts

- Fit & Assembly

- Prototype Tooling

- Metal Casting

- Visual Aids

- Presentation Modeling

- Education/Research

- Others

By Vertical

- Consumer Goods

- Construction

- Education

- Industrial

- Healthcare

- Aerospace & Defense

- Automotive

- Others

By Geography

- North America

- US

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- UK

- France

- Russia

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Singapore

- Malaysia

- Rest of Asia Pacific

- LAMEA

- Brazil

- Argentina

- UAE

- Saudi Arabia

- South Africa

- Nigeria

- Rest of LAMEA

Companies Profiled

- Hoganas AB

- 3D Systems Corporation

- Materialise NV

- General Electric Company

- Stratasys Ltd.

- Autodesk, Inc.

- The ExOne company (Desktop Metal, Inc.)

- Organovo Holdings, Inc.

- voxeljet AG

- Canon, Inc.

Unique Offerings from KBV Research

- Exhaustive coverage

- Highest number of market tables and figures

- Subscription based model available

- Guaranteed best price

- Assured post sales research support with 10% customization free

Table of Contents

Chapter 1. Market Scope & Methodology

- 1.1 Market Definition

- 1.2 Objectives

- 1.3 Market Scope

- 1.4 Segmentation

- 1.4.1 Global 3D Printing Market, by Component

- 1.4.2 Global 3D Printing Market, by Technology

- 1.4.3 Global 3D Printing Market, by Application

- 1.4.4 Global 3D Printing Market, by Vertical

- 1.4.5 Global 3D Printing Market, by Geography

- 1.5 Methodology for the research

Chapter 2. Market at a Glance

- 2.1 Key highlights

Chapter 3. Market Overview

- 3.1 Introduction

- 3.1.1 Overview

- 3.1.1.1 Market Composition and Scenario

- 3.1.1 Overview

- 3.2 Key Factors Impacting the Market

- 3.2.1 Market Drivers

- 3.2.2 Market Restraints

Chapter 4. Competition Analysis - Global

- 4.1 KBV Cardinal Matrix

- 4.2 Recent Industry Wide Strategic Developments

- 4.2.1 Partnerships, Collaborations and Agreements

- 4.2.2 Product Launches and Product Expansions

- 4.2.3 Acquisition and Mergers

- 4.2.4 Geographical Expansions

- 4.3 Top Winning Strategies

- 4.3.1 Key Leading Strategies: Percentage Distribution (2019-2023)

- 4.3.2 Key Strategic Move: (Product Launches and Product Expansions: 2021, Feb - 2023, Jun) Leading Players

- 4.4 Porter Five Forces Analysis

Chapter 5. Global 3D Printing Market By Component

- 5.1 Global Product Market by Region

- 5.2 Global 3D Printing Market By Product Type

- 5.2.1 Global Printer Market by Region

- 5.2.2 Global Printer Market By Type

- 5.2.2.1 Global Industrial Market by Region

- 5.2.2.2 Global Desktop Market by Region

- 5.2.3 Global Material Market by Region

- 5.2.4 Global 3D Printing Market By Material Type

- 5.2.4.1 Global Polymer Market by Region

- 5.2.4.2 Global Metal & Alloys Market by Region

- 5.2.4.3 Global Ceramic Market by Region

- 5.2.4.4 Global Others Market by Region

- 5.3 Global Software Market by Region

- 5.4 Global 3D Printing Market By Software Type

- 5.4.1 Global Design Software Market by Region

- 5.4.2 Global Inspection Software Market by Region

- 5.4.3 Global Printer Software Market by Region

- 5.4.4 Global Scanning Software Market by Region

- 5.5 Global Services Market by Region

Chapter 6. Global 3D Printing Market By Technology

- 6.1 Global Stereolithography Market by Region

- 6.2 Global Fused Deposition Modeling Market by Region

- 6.3 Global Selective Laser Sintering Market by Region

- 6.4 Global Laminated object Manufacturing Market by Region

- 6.5 Global Electron Beam Melting Market by Region

- 6.6 Global Others Market by Region

Chapter 7. Global 3D Printing Market By Application

- 7.1 Global Functional Parts Market by Region

- 7.2 Global Fit & Assembly Market by Region

- 7.3 Global Prototype Tooling Market by Region

- 7.4 Global Metal Casting Market by Region

- 7.5 Global Visual Aids Market by Region

- 7.6 Global Presentation Modeling Market by Region

- 7.7 Global Education/Research Market by Region

- 7.8 Global Others Market by Region

Chapter 8. Global 3D Printing Market By Vertical

- 8.1 Global Consumer Goods Market by Region

- 8.2 Global Construction Market by Region

- 8.3 Global Education Market by Region

- 8.4 Global Industrial Market by Region

- 8.5 Global Healthcare Market by Region

- 8.6 Global Aerospace & Defense Market by Region

- 8.7 Global Automotive Market by Region

- 8.8 Global Others Market by Region

Chapter 9. Global 3D Printing Market By Region

- 9.1 North America 3D Printing Market

- 9.1.1 North America 3D Printing Market By Component

- 9.1.1.1 North America Product Market by Country

- 9.1.1.2 North America 3D Printing Market By Product Type

- 9.1.1.2.1 North America Printer Market by Region

- 9.1.1.2.2 North America Printer Market By Type

- 9.1.1.2.3 North America Material Market by Region

- 9.1.1.2.4 North America 3D Printing Market By Material Type

- 9.1.1.3 North America Software Market by Country

- 9.1.1.4 North America 3D Printing Market By Software Type

- 9.1.1.4.1 North America Design Software Market by Country

- 9.1.1.4.2 North America Inspection Software Market by Country

- 9.1.1.4.3 North America Printer Software Market by Country

- 9.1.1.4.4 North America Scanning Software Market by Country

- 9.1.1.5 North America Services Market by Country

- 9.1.2 North America 3D Printing Market By Technology

- 9.1.2.1 North America Stereolithography Market by Country

- 9.1.2.2 North America Fused Deposition Modeling Market by Country

- 9.1.2.3 North America Selective Laser Sintering Market by Country

- 9.1.2.4 North America Laminated object Manufacturing Market by Country

- 9.1.2.5 North America Electron Beam Melting Market by Country

- 9.1.2.6 North America Others Market by Country

- 9.1.3 North America 3D Printing Market By Application

- 9.1.3.1 North America Functional Parts Market by Country

- 9.1.3.2 North America Fit & Assembly Market by Country

- 9.1.3.3 North America Prototype Tooling Market by Country

- 9.1.3.4 North America Metal Casting Market by Country

- 9.1.3.5 North America Visual Aids Market by Country

- 9.1.3.6 North America Presentation Modeling Market by Country

- 9.1.3.7 North America Education/Research Market by Country

- 9.1.3.8 North America Others Market by Country

- 9.1.4 North America 3D Printing Market By Vertical

- 9.1.4.1 North America Consumer Goods Market by Country

- 9.1.4.2 North America Construction Market by Country

- 9.1.4.3 North America Education Market by Country

- 9.1.4.4 North America Industrial Market by Country

- 9.1.4.5 North America Healthcare Market by Country

- 9.1.4.6 North America Aerospace & Defense Market by Country

- 9.1.4.7 North America Automotive Market by Country

- 9.1.4.8 North America Others Market by Country

- 9.1.5 North America 3D Printing Market By Country

- 9.1.5.1 US 3D Printing Market

- 9.1.5.1.1 US 3D Printing Market By Component

- 9.1.5.1.2 US 3D Printing Market By Technology

- 9.1.5.1.3 US 3D Printing Market By Application

- 9.1.5.1.4 US 3D Printing Market By Vertical

- 9.1.5.2 Canada 3D Printing Market

- 9.1.5.2.1 Canada 3D Printing Market By Component

- 9.1.5.2.2 Canada 3D Printing Market By Technology

- 9.1.5.2.3 Canada 3D Printing Market By Application

- 9.1.5.2.4 Canada 3D Printing Market By Vertical

- 9.1.5.3 Mexico 3D Printing Market

- 9.1.5.3.1 Mexico 3D Printing Market By Component

- 9.1.5.3.2 Mexico 3D Printing Market By Technology

- 9.1.5.3.3 Mexico 3D Printing Market By Application

- 9.1.5.3.4 Mexico 3D Printing Market By Vertical

- 9.1.5.4 Rest of North America 3D Printing Market

- 9.1.5.4.1 Rest of North America 3D Printing Market By Component

- 9.1.5.4.2 Rest of North America 3D Printing Market By Technology

- 9.1.5.4.3 Rest of North America 3D Printing Market By Application

- 9.1.5.4.4 Rest of North America 3D Printing Market By Vertical

- 9.1.5.1 US 3D Printing Market

- 9.1.1 North America 3D Printing Market By Component

- 9.2 Europe 3D Printing Market

- 9.2.1 Europe 3D Printing Market By Component

- 9.2.1.1 Europe Product Market by Country

- 9.2.1.2 Europe 3D Printing Market By Product Type

- 9.2.1.2.1 Europe Printer Market by Country

- 9.2.1.2.2 Europe Printer Market By Type

- 9.2.1.2.3 Europe Material Market by Country

- 9.2.1.2.4 Europe 3D Printing Market By Material Type

- 9.2.1.3 Europe Software Market by Country

- 9.2.1.4 Europe 3D Printing Market By Software Type

- 9.2.1.4.1 Europe Design Software Market by Country

- 9.2.1.4.2 Europe Inspection Software Market by Country

- 9.2.1.4.3 Europe Printer Software Market by Country

- 9.2.1.4.4 Europe Scanning Software Market by Country

- 9.2.1.5 Europe Services Market by Country

- 9.2.2 Europe 3D Printing Market By Technology

- 9.2.2.1 Europe Stereolithography Market by Country

- 9.2.2.2 Europe Fused Deposition Modeling Market by Country

- 9.2.2.3 Europe Selective Laser Sintering Market by Country

- 9.2.2.4 Europe Laminated object Manufacturing Market by Country

- 9.2.2.5 Europe Electron Beam Melting Market by Country

- 9.2.2.6 Europe Others Market by Country

- 9.2.3 Europe 3D Printing Market By Application

- 9.2.3.1 Europe Functional Parts Market by Country

- 9.2.3.2 Europe Fit & Assembly Market by Country

- 9.2.3.3 Europe Prototype Tooling Market by Country

- 9.2.3.4 Europe Metal Casting Market by Country

- 9.2.3.5 Europe Visual Aids Market by Country

- 9.2.3.6 Europe Presentation Modeling Market by Country

- 9.2.3.7 Europe Education/Research Market by Country

- 9.2.3.8 Europe Others Market by Country

- 9.2.4 Europe 3D Printing Market By Vertical

- 9.2.4.1 Europe Consumer Goods Market by Country

- 9.2.4.2 Europe Construction Market by Country

- 9.2.4.3 Europe Education Market by Country

- 9.2.4.4 Europe Industrial Market by Country

- 9.2.4.5 Europe Healthcare Market by Country

- 9.2.4.6 Europe Aerospace & Defense Market by Country

- 9.2.4.7 Europe Automotive Market by Country

- 9.2.4.8 Europe Others Market by Country

- 9.2.5 Europe 3D Printing Market By Country

- 9.2.5.1 Germany 3D Printing Market

- 9.2.5.1.1 Germany 3D Printing Market By Component

- 9.2.5.1.2 Germany 3D Printing Market By Technology

- 9.2.5.1.3 Germany 3D Printing Market By Application

- 9.2.5.1.4 Germany 3D Printing Market By Vertical

- 9.2.5.2 UK 3D Printing Market

- 9.2.5.2.1 UK 3D Printing Market By Component

- 9.2.5.2.2 UK 3D Printing Market By Technology

- 9.2.5.2.3 UK 3D Printing Market By Application

- 9.2.5.2.4 UK 3D Printing Market By Vertical

- 9.2.5.3 France 3D Printing Market

- 9.2.5.3.1 France 3D Printing Market By Component

- 9.2.5.3.2 France 3D Printing Market By Technology

- 9.2.5.3.3 France 3D Printing Market By Application

- 9.2.5.3.4 France 3D Printing Market By Vertical

- 9.2.5.4 Russia 3D Printing Market

- 9.2.5.4.1 Russia 3D Printing Market By Component

- 9.2.5.4.2 Russia 3D Printing Market By Technology

- 9.2.5.4.3 Russia 3D Printing Market By Application

- 9.2.5.4.4 Russia 3D Printing Market By Vertical

- 9.2.5.5 Spain 3D Printing Market

- 9.2.5.5.1 Spain 3D Printing Market By Component

- 9.2.5.5.2 Spain 3D Printing Market By Technology

- 9.2.5.5.3 Spain 3D Printing Market By Application

- 9.2.5.5.4 Spain 3D Printing Market By Vertical

- 9.2.5.6 Italy 3D Printing Market

- 9.2.5.6.1 Italy 3D Printing Market By Component

- 9.2.5.6.2 Italy 3D Printing Market By Technology

- 9.2.5.6.3 Italy 3D Printing Market By Application

- 9.2.5.6.4 Italy 3D Printing Market By Vertical

- 9.2.5.7 Rest of Europe 3D Printing Market

- 9.2.5.7.1 Rest of Europe 3D Printing Market By Component

- 9.2.5.7.2 Rest of Europe 3D Printing Market By Technology

- 9.2.5.7.3 Rest of Europe 3D Printing Market By Application

- 9.2.5.7.4 Rest of Europe 3D Printing Market By Vertical

- 9.2.5.1 Germany 3D Printing Market

- 9.2.1 Europe 3D Printing Market By Component

- 9.3 Asia Pacific 3D Printing Market

- 9.3.1 Asia Pacific 3D Printing Market By Component

- 9.3.1.1 Asia Pacific Product Market by Country

- 9.3.1.2 Asia Pacific 3D Printing Market By Product Type

- 9.3.1.2.1 Asia Pacific Printer Market by Country

- 9.3.1.2.2 Asia Pacific Printer Market By Type

- 9.3.1.2.3 Asia Pacific Material Market by Country

- 9.3.1.2.4 Asia Pacific 3D Printing Market By Material Type

- 9.3.1.3 Asia Pacific Software Market by Country

- 9.3.1.4 Asia Pacific 3D Printing Market By Software Type

- 9.3.1.4.1 Asia Pacific Design Software Market by Country

- 9.3.1.4.2 Asia Pacific Inspection Software Market by Country

- 9.3.1.4.3 Asia Pacific Printer Software Market by Country

- 9.3.1.4.4 Asia Pacific Scanning Software Market by Country

- 9.3.1.5 Asia Pacific Services Market by Country

- 9.3.2 Asia Pacific 3D Printing Market By Technology

- 9.3.2.1 Asia Pacific Stereolithography Market by Country

- 9.3.2.2 Asia Pacific Fused Deposition Modeling Market by Country

- 9.3.2.3 Asia Pacific Selective Laser Sintering Market by Country

- 9.3.2.4 Asia Pacific Laminated object Manufacturing Market by Country

- 9.3.2.5 Asia Pacific Electron Beam Melting Market by Country

- 9.3.2.6 Asia Pacific Others Market by Country

- 9.3.3 Asia Pacific 3D Printing Market By Application

- 9.3.3.1 Asia Pacific Functional Parts Market by Country

- 9.3.3.2 Asia Pacific Fit & Assembly Market by Country

- 9.3.3.3 Asia Pacific Prototype Tooling Market by Country

- 9.3.3.4 Asia Pacific Metal Casting Market by Country

- 9.3.3.5 Asia Pacific Visual Aids Market by Country

- 9.3.3.6 Asia Pacific Presentation Modeling Market by Country

- 9.3.3.7 Asia Pacific Education/Research Market by Country

- 9.3.3.8 Asia Pacific Others Market by Country

- 9.3.4 Asia Pacific 3D Printing Market By Vertical

- 9.3.4.1 Asia Pacific Consumer Goods Market by Country

- 9.3.4.2 Asia Pacific Construction Market by Country

- 9.3.4.3 Asia Pacific Education Market by Country

- 9.3.4.4 Asia Pacific Industrial Market by Country

- 9.3.4.5 Asia Pacific Healthcare Market by Country

- 9.3.4.6 Asia Pacific Aerospace & Defense Market by Country

- 9.3.4.7 Asia Pacific Automotive Market by Country

- 9.3.4.8 Asia Pacific Others Market by Country

- 9.3.5 Asia Pacific 3D Printing Market By Country

- 9.3.5.1 China 3D Printing Market

- 9.3.5.1.1 China 3D Printing Market By Component

- 9.3.5.1.2 China 3D Printing Market By Technology

- 9.3.5.1.3 China 3D Printing Market By Application

- 9.3.5.1.4 China 3D Printing Market By Vertical

- 9.3.5.2 Japan 3D Printing Market

- 9.3.5.2.1 Japan 3D Printing Market By Component

- 9.3.5.2.2 Japan 3D Printing Market By Technology

- 9.3.5.2.3 Japan 3D Printing Market By Application

- 9.3.5.2.4 Japan 3D Printing Market By Vertical

- 9.3.5.3 India 3D Printing Market

- 9.3.5.3.1 India 3D Printing Market By Component

- 9.3.5.3.2 India 3D Printing Market By Technology

- 9.3.5.3.3 India 3D Printing Market By Application

- 9.3.5.3.4 India 3D Printing Market By Vertical

- 9.3.5.4 South Korea 3D Printing Market

- 9.3.5.4.1 South Korea 3D Printing Market By Component

- 9.3.5.4.2 South Korea 3D Printing Market By Technology

- 9.3.5.4.3 South Korea 3D Printing Market By Application

- 9.3.5.4.4 South Korea 3D Printing Market By Vertical

- 9.3.5.5 Singapore 3D Printing Market

- 9.3.5.5.1 Singapore 3D Printing Market By Component

- 9.3.5.5.2 Singapore 3D Printing Market By Technology

- 9.3.5.5.3 Singapore 3D Printing Market By Application

- 9.3.5.5.4 Singapore 3D Printing Market By Vertical

- 9.3.5.6 Malaysia 3D Printing Market

- 9.3.5.6.1 Malaysia 3D Printing Market By Component

- 9.3.5.6.2 Malaysia 3D Printing Market By Technology

- 9.3.5.6.3 Malaysia 3D Printing Market By Application

- 9.3.5.6.4 Malaysia 3D Printing Market By Vertical

- 9.3.5.7 Rest of Asia Pacific 3D Printing Market

- 9.3.5.7.1 Rest of Asia Pacific 3D Printing Market By Component

- 9.3.5.7.2 Rest of Asia Pacific 3D Printing Market By Technology

- 9.3.5.7.3 Rest of Asia Pacific 3D Printing Market By Application

- 9.3.5.7.4 Rest of Asia Pacific 3D Printing Market By Vertical

- 9.3.5.1 China 3D Printing Market

- 9.3.1 Asia Pacific 3D Printing Market By Component

- 9.4 LAMEA 3D Printing Market

- 9.4.1 LAMEA 3D Printing Market By Component

- 9.4.1.1 LAMEA Product Market by Country

- 9.4.1.2 LAMEA 3D Printing Market By Product Type

- 9.4.1.2.1 LAMEA Printer Market by Country

- 9.4.1.2.2 LAMEA Printer Market By Type

- 9.4.1.2.3 LAMEA Material Market by Country

- 9.4.1.2.4 LAMEA 3D Printing Market By Material Type

- 9.4.1.3 LAMEA Software Market by Country

- 9.4.1.4 LAMEA 3D Printing Market By Software Type

- 9.4.1.4.1 LAMEA Design Software Market by Country

- 9.4.1.4.2 LAMEA Inspection Software Market by Country

- 9.4.1.4.3 LAMEA Printer Software Market by Country

- 9.4.1.4.4 LAMEA Scanning Software Market by Country

- 9.4.1.5 LAMEA Services Market by Country

- 9.4.2 LAMEA 3D Printing Market By Technology

- 9.4.2.1 LAMEA Stereolithography Market by Country

- 9.4.2.2 LAMEA Fused Deposition Modeling Market by Country

- 9.4.2.3 LAMEA Selective Laser Sintering Market by Country

- 9.4.2.4 LAMEA Laminated object Manufacturing Market by Country

- 9.4.2.5 LAMEA Electron Beam Melting Market by Country

- 9.4.2.6 LAMEA Others Market by Country

- 9.4.3 LAMEA 3D Printing Market By Application

- 9.4.3.1 LAMEA Functional Parts Market by Country

- 9.4.3.2 LAMEA Fit & Assembly Market by Country

- 9.4.3.3 LAMEA Prototype Tooling Market by Country

- 9.4.3.4 LAMEA Metal Casting Market by Country

- 9.4.3.5 LAMEA Visual Aids Market by Country

- 9.4.3.6 LAMEA Presentation Modeling Market by Country

- 9.4.3.7 LAMEA Education/Research Market by Country

- 9.4.3.8 LAMEA Others Market by Country

- 9.4.4 LAMEA 3D Printing Market By Vertical

- 9.4.4.1 LAMEA Consumer Goods Market by Country

- 9.4.4.2 LAMEA Construction Market by Country

- 9.4.4.3 LAMEA Education Market by Country

- 9.4.4.4 LAMEA Industrial Market by Country

- 9.4.4.5 LAMEA Healthcare Market by Country

- 9.4.4.6 LAMEA Aerospace & Defense Market by Country

- 9.4.4.7 LAMEA Automotive Market by Country

- 9.4.4.8 LAMEA Others Market by Country

- 9.4.5 LAMEA 3D Printing Market By Country

- 9.4.5.1 Brazil 3D Printing Market

- 9.4.5.1.1 Brazil 3D Printing Market By Component

- 9.4.5.1.2 Brazil 3D Printing Market By Technology

- 9.4.5.1.3 Brazil 3D Printing Market By Application

- 9.4.5.1.4 Brazil 3D Printing Market By Vertical

- 9.4.5.2 Argentina 3D Printing Market

- 9.4.5.2.1 Argentina 3D Printing Market By Component

- 9.4.5.2.2 Argentina 3D Printing Market By Technology

- 9.4.5.2.3 Argentina 3D Printing Market By Application

- 9.4.5.2.4 Argentina 3D Printing Market By Vertical

- 9.4.5.3 UAE 3D Printing Market

- 9.4.5.3.1 UAE 3D Printing Market By Component

- 9.4.5.3.2 UAE 3D Printing Market By Technology

- 9.4.5.3.3 UAE 3D Printing Market By Application

- 9.4.5.3.4 UAE 3D Printing Market By Vertical

- 9.4.5.4 Saudi Arabia 3D Printing Market

- 9.4.5.4.1 Saudi Arabia 3D Printing Market By Component

- 9.4.5.4.2 Saudi Arabia 3D Printing Market By Technology

- 9.4.5.4.3 Saudi Arabia 3D Printing Market By Application

- 9.4.5.4.4 Saudi Arabia 3D Printing Market By Vertical

- 9.4.5.5 South Africa 3D Printing Market

- 9.4.5.5.1 South Africa 3D Printing Market By Component

- 9.4.5.5.2 South Africa 3D Printing Market By Technology

- 9.4.5.5.3 South Africa 3D Printing Market By Application

- 9.4.5.5.4 South Africa 3D Printing Market By Vertical

- 9.4.5.6 Nigeria 3D Printing Market

- 9.4.5.6.1 Nigeria 3D Printing Market By Component

- 9.4.5.6.2 Nigeria 3D Printing Market By Technology

- 9.4.5.6.3 Nigeria 3D Printing Market By Application

- 9.4.5.6.4 Nigeria 3D Printing Market By Vertical

- 9.4.5.7 Rest of LAMEA 3D Printing Market

- 9.4.5.7.1 Rest of LAMEA 3D Printing Market By Component

- 9.4.5.7.2 Rest of LAMEA 3D Printing Market By Technology

- 9.4.5.7.3 Rest of LAMEA 3D Printing Market By Application

- 9.4.5.7.4 Rest of LAMEA 3D Printing Market By Vertical

- 9.4.5.1 Brazil 3D Printing Market

- 9.4.1 LAMEA 3D Printing Market By Component

Chapter 10. Company Profiles

- 10.1 Hoganas AB

- 10.1.1 Company Overview

- 10.1.2 SWOT Analysis

- 10.2 3D Systems Corporation

- 10.2.1 Company Overview

- 10.2.2 Financial Analysis

- 10.2.3 Segmental and Regional Analysis

- 10.2.4 Research & Development Expenses

- 10.2.5 Recent strategies and developments:

- 10.2.5.1 Partnerships, Collaborations, and Agreements:

- 10.2.5.2 Product Launches and Product Expansions:

- 10.2.5.3 Acquisition and Mergers:

- 10.2.5.4 Geographical Expansions:

- 10.2.6 SWOT Analysis

- 10.3 Materialise NV

- 10.3.1 Company Overview

- 10.3.2 Financial Analysis

- 10.3.3 Segmental and Regional Analysis

- 10.3.4 Research & Development Expenses

- 10.3.5 Recent strategies and developments:

- 10.3.5.1 Partnerships, Collaborations, and Agreements:

- 10.3.5.2 Acquisition and Mergers:

- 10.3.6 SWOT Analysis

- 10.4 General Electric Company

- 10.4.1 Company Overview

- 10.4.2 Financial Analysis

- 10.4.3 Segmental and Regional Analysis

- 10.4.4 Research & Development Expense

- 10.4.5 Recent strategies and developments:

- 10.4.5.1 Partnerships, Collaborations, and Agreements:

- 10.4.5.2 Product Launches and Product Expansions:

- 10.4.5.3 Geographical Expansions:

- 10.4.6 SWOT Analysis

- 10.5 Stratasys Ltd.

- 10.5.1 Company Overview

- 10.5.2 Financial Analysis

- 10.5.3 Regional Analysis

- 10.5.4 Research & Development Expenses

- 10.5.5 Recent strategies and developments:

- 10.5.5.1 Partnerships, Collaborations, and Agreements:

- 10.5.5.2 Product Launches and Product Expansions:

- 10.5.5.3 Acquisition and Mergers:

- 10.5.6 SWOT Analysis

- 10.6 Autodesk, Inc.

- 10.6.1 Company Overview

- 10.6.2 Financial Analysis

- 10.6.3 Regional Analysis

- 10.6.4 Research & Development Expenses

- 10.6.5 Recent strategies and developments:

- 10.6.5.1 Product Launches and Product Expansions:

- 10.6.5.2 Acquisition and Mergers:

- 10.6.5.3 Geographical Expansions:

- 10.6.6 SWOT Analysis

- 10.7 The ExOne company (Desktop Metal, Inc.)

- 10.7.1 Company Overview

- 10.7.2 Financial Analysis

- 10.7.3 Regional Analysis

- 10.7.4 Research & Development Expenses

- 10.7.5 Recent strategies and developments:

- 10.7.5.1 Partnerships, Collaborations, and Agreements:

- 10.7.5.2 Acquisition and Mergers:

- 10.7.6 SWOT Analysis

- 10.8 Organovo Holdings, Inc.

- 10.8.1 Company Overview

- 10.8.2 Financial Analysis

- 10.8.3 Research & Development Expenses

- 10.8.4 Recent strategies and developments:

- 10.8.4.1 Partnerships, Collaborations, and Agreements:

- 10.8.5 SWOT Analysis

- 10.9 voxeljet AG

- 10.9.1 Company Overview

- 10.9.2 Financial Analysis

- 10.9.3 Segmental and Regional Analysis

- 10.9.4 Research & Development Expenses

- 10.9.5 Recent strategies and developments:

- 10.9.5.1 Product Launches and Product Expansions:

- 10.9.6 SWOT Analysis

- 10.10. Canon, Inc.

- 10.10.1 Company Overview

- 10.10.2 Financial Analysis

- 10.10.3 Segmental and Regional Analysis

- 10.10.4 Research & Development Expenses

- 10.10.5 SWOT Analysis

Chapter 11. Winning imperative of 3D Printing Market