|

|

市場調査レポート

商品コード

1807946

先端炭素材料市場:材料タイプ、フォームファクター、製造技術、用途、流通チャネル別-2025-2030年世界予測Advanced Carbon Materials Market by Material Type, Form Factor, Manufacturing Technology, Application, Distribution Channel - Global Forecast 2025-2030 |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 先端炭素材料市場:材料タイプ、フォームファクター、製造技術、用途、流通チャネル別-2025-2030年世界予測 |

|

出版日: 2025年08月28日

発行: 360iResearch

ページ情報: 英文 189 Pages

納期: 即日から翌営業日

|

全表示

- 概要

- 図表

- 目次

先端炭素材料市場の2024年の市場規模は58億2,000万米ドルで、2025年にはCAGR 4.82%で60億9,000万米ドルに成長し、2030年には77億2,000万米ドルに達すると予測されています。

| 主な市場の統計 | |

|---|---|

| 基準年2024 | 58億2,000万米ドル |

| 推定年2025 | 60億9,000万米ドル |

| 予測年2030 | 77億2,000万米ドル |

| CAGR(%) | 4.82% |

革新の原動力を明らかにし、将来の成長を形作る技術的情勢を明らかにするために、先端炭素材料の基礎を探る

先端炭素材料は、材料科学分野におけるパラダイムシフトを象徴するものであり、ユニークな構造的、電気的、機械的特性を兼ね備え、多業種にわたる次世代ソリューションを可能にします。輸送やエネルギー貯蔵の分野で電動化が加速する中、炭素繊維やカーボンナノチューブは軽量強度と卓越した導電性を実現し、グラフェンや炭素複合材料は熱管理や電子性能の革命的な向上を約束します。同時に、活性炭やカーボンブラックのような伝統的な形態も進化を続けており、厳しい環境基準やろ過基準を満たすために、新しい活性化技術や製造技術が活用されています。

業界標準を再定義し、かつてない競合優位性をもたらす先端炭素材料技術の重要な変遷を追う

過去10年間、先端炭素材料は、合成・加工技術の飛躍的進歩によって、大きく変貌を遂げてきました。化学気相成長法とエレクトロスピニング法は、実験室での珍奇な技術からスケーラブルな製造法へと成熟し、高純度グラフェンや均一なカーボンナノファイバーの製造を可能にしました。一方、熱分解と水熱炭化の進歩は、エネルギー貯蔵や環境浄化といった特殊な用途向けに多孔性と表面化学を調整する新たな道を開いています。

米国の最近の関税措置が先端炭素材料のサプライチェーンに及ぼす広範な影響イノベーションと市場参入性

米国が2025年に新たな関税措置を導入したことは、先端炭素材料のグローバルなサプライチェーンに波紋を広げています。輸入されるグラファイトとカーボンナノチューブには高い関税が課されるようになり、メーカーは調達戦略を見直し、有利な貿易協定を結んでいる地域の代替サプライヤーを探すようになりました。その結果、いくつかのメーカーは、追加コストを軽減し、重要なインプットの継続性を確保するために、調達の一部を国内または近海産にシフトしています。

材料タイプ、形状、製造方法、多様な応用分野にまたがる先端炭素材料の主要なセグメンテーション・ダイナミクスを明らかにします

材料の種類を細かく調べると、それぞれの最終用途に対応する性能特性のスペクトルが明らかになります。活性炭は環境および医療用途の吸着に優れています。一方、カーボンブラックはファーネス、ガス、サーマルのバリエーションがあり、コーティング、インク、ポリマー補強の要として機能します。炭素複合材料は、PAN系、ピッチ系、レーヨン系などの炭素繊維マトリックスの相乗効果を利用して、強度や剛性のパラメーターを調整することができます。一方、グラフェンの比類なき導電性と単層または多層カーボンナノチューブは、エレクトロニクス、センサー、導電性コーティングの飛躍的進歩を促進します。

南北アメリカ、欧州、中東・アフリカ、アジア太平洋市場における先端炭素材料の採用を形成する地域力学の検証

地域別の洞察は、それぞれの主要地域が先端炭素材料領域で独自の道を切り開いていることを示しています。南北アメリカでは、研究機関の強力な基盤と支援的な政策措置が、航空宇宙と自動車セクター向けの炭素繊維複合材料の急速な進歩を支えています。北米の共同イノベーションハブは、材料開発者と最終用途メーカー間の相乗効果を促進し、次世代カーボンナノ材料の早期採用を推進しています。

先端炭素材料産業を牽引する主要企業の競合戦略と革新的イニシアチブを明らかにします

先端炭素材料分野の主要企業は、未加工の炭素前駆体から高価値のナノ材料に至るまで、エンドツーエンドの能力を統合する能力によって際立っています。カーボンブラックを専門とする企業は、標的を絞った買収と生産能力の拡大を通じてポートフォリオを強化し、タイヤ補強や顔料用途の急増する需要に対応できるようにしています。同時に、炭素繊維の大手企業は、独自の前駆体技術や、サイクルタイムとエネルギー消費を削減する高度なトウ生産ラインへの投資を通じて差別化を図っています。

業界リーダーに実践的な戦略とロードマップを提供することで、新たな動向を活用し、先端炭素材料の市場ポジションを強化します

先端炭素材料の新たなビジネスチャンスを活かそうとする業界のリーダーは、まず、進化する材料仕様に対応できる柔軟な製造プラットフォームを優先すべきです。炭素繊維前駆体や様々なカーボンブラックグレードの切り替えが可能なモジュール式製造ラインを統合することで、企業は変化する用途要件や規制の義務に迅速に対応することができます。

先進炭素材料に関する包括的な知見を支えるデータ収集技術と分析フレームワークの厳密な調査アプローチの詳細

本調査では、最も正確で信頼性の高い知見を得るために、2次データ分析と綿密な1次調査を組み合わせた厳格な調査手法を採用しています。最初の机上調査では、技術白書、特許出願、業界誌をレビューし、先端炭素材料の現状をマッピングしました。この基礎段階は、調査結果を検証し、市場促進要因に関する直接の視点を把握するために、主要地域の経営幹部、研究科学者、調達スペシャリストとの構造的インタビューによって補足されました。

先端炭素材料エコシステムにおける将来の開発に関する首尾一貫したビジョンを提示するために、核となる発見と戦略的重要事項を統合します

核となる調査結果を総合すると、先端炭素材料は、絶え間ない技術的ブレークスルーと持続可能性への関心の高まりに牽引され、広範な産業統合の頂点にあることが明らかになりました。製造イノベーションと戦略的パートナーシップの相互作用が競合力学を形成し、地域貿易政策と関税情勢がサプライチェーン構造に影響を与えると思われます。意思決定者にとっては、モジュール生産の採用、調達戦略の多様化、循環型経済への取り組みへの投資が不可欠です。

目次

第1章 序文

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場の概要

第5章 市場力学

- 次世代フレキシブルエレクトロニクスにおけるグラフェンベース電極の統合

- 持続可能なカーボンナノチューブ製造におけるスケールアップの課題と革新

- 新興の水浄化および空気ろ過システムにおける活性炭の採用

- 高感度バイオイメージングおよび診断のためのグラフェン量子ドットの開発

- 急速充電リチウムイオン電池用バインダーフリー炭素負極の商品化

- 高性能スーパーキャパシタのための階層的多孔質炭素スキャフォールドの進歩

- 循環型経済アプリケーションにおけるバイオマス由来炭素材料の実装

- 自動車メーカーが電気自動車向け炭素繊維複合材の採用を加速

- フレキシブルエレクトロニクスとオプトエレクトロニクスに新たな可能性を開くグラフェン量子ドット

- 持続可能な水浄化ソリューションを目指したバイオマス由来活性炭のイノベーション

第6章 市場洞察

- ポーターのファイブフォース分析

- PESTEL分析

第7章 米国の関税の累積的な影響2025

第8章 先端炭素材料市場:素材タイプ別

- 活性炭

- カーボンブラック

- ファーネスブラック

- ガスブラック

- サーマルブラック

- 炭素複合材料

- カーボンファイバー

- PANベース

- ピッチベース

- レーヨンベース

- カーボンナノチューブ(CNT)

- 多層壁

- 単壁

- グラフェン

- 黒鉛

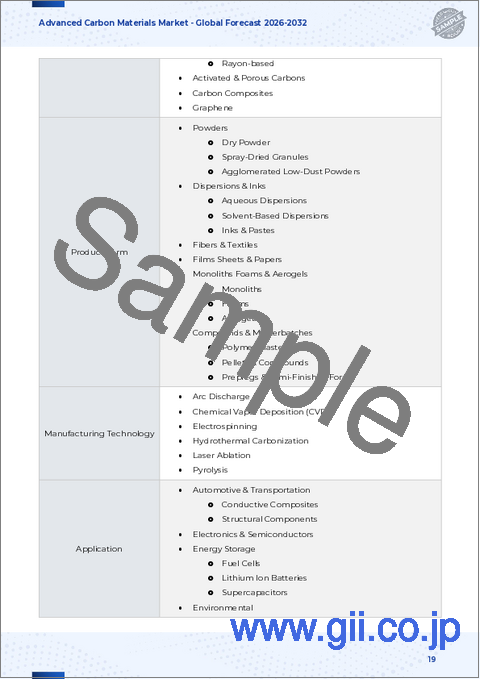

第9章 先端炭素材料市場:フォームファクター別

- コーティング/インク

- 繊維/フィラメント

- フォーム/エアロゲル

- ペレット/顆粒

- 粉

- シート/フィルム

第10章 先端炭素材料市場製造技術

- アーク放電

- 化学蒸着(CVD)

- エレクトロスピニング

- 水熱炭化

- レーザーアブレーション

- 熱分解

第11章 先端炭素材料市場:用途別

- 自動車・航空宇宙

- 導電性複合材料

- 構造部品

- 熱管理

- エレクトロニクスおよび半導体

- 導電性インク

- EMIシールド

- センサー

- エネルギー貯蔵

- 燃料電池

- リチウムイオン電池

- スーパーキャパシタ

- 環境

- 空気ろ過

- 土壌修復

- 水処理

- 産業

- 触媒

- コーティング

- 潤滑剤

- 医学

- バイオセンサー

- ドラッグデリバリー

- 組織工学

第12章 先端炭素材料市場:流通チャネル別

- オフライン

- オンライン

第13章 南北アメリカの先端炭素材料市場

- 米国

- カナダ

- メキシコ

- ブラジル

- アルゼンチン

第14章 欧州・中東・アフリカの先端炭素材料市場

- 英国

- ドイツ

- フランス

- ロシア

- イタリア

- スペイン

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- デンマーク

- オランダ

- カタール

- フィンランド

- スウェーデン

- ナイジェリア

- エジプト

- トルコ

- イスラエル

- ノルウェー

- ポーランド

- スイス

第15章 アジア太平洋地域の先端炭素材料市場

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- インドネシア

- タイ

- フィリピン

- マレーシア

- シンガポール

- ベトナム

- 台湾

第16章 競合情勢

- 市場シェア分析, 2024

- FPNVポジショニングマトリックス, 2024

- 競合分析

- Anaori Carbon Co. Ltd

- Arkema SA

- Birla Carbon USA Inc

- Cabot Corporation

- CVD Equipment Corporation

- Global Graphene Group

- Graphenano Group

- GRUPO ANTOLIN IRAUSA, S.A.

- Haydale Graphene Industries PLC

- Hexcel Corporation

- Jiangsu Cnano Technology Co., Ltd

- LG Chem Ltd

- Mitsubishi Chemical Group Corporation.

- Nanocyl SA

- Nanoshel LLC

- Orion Engineered Carbons GmbH

- SGL Carbon SE

- TEIJIN LIMITED

- Tokai Carbon Co., Ltd.

- Tokyo Chemical Industry Co., Ltd.

- Toyo Tanso Co.,Ltd.

- ZEON CORPORATION

第17章 リサーチAI

第18章 リサーチ統計

第19章 リサーチコンタクト

第20章 リサーチ記事

第21章 付録

LIST OF FIGURES

- FIGURE 1. ADVANCED CARBON MATERIALS MARKET RESEARCH PROCESS

- FIGURE 2. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, 2018-2030 (USD MILLION)

- FIGURE 3. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY REGION, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 4. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY COUNTRY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 5. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY MATERIAL TYPE, 2024 VS 2030 (%)

- FIGURE 6. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY MATERIAL TYPE, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 7. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY FORM FACTOR, 2024 VS 2030 (%)

- FIGURE 8. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY FORM FACTOR, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 9. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY MANUFACTURING TECHNOLOGY, 2024 VS 2030 (%)

- FIGURE 10. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY MANUFACTURING TECHNOLOGY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 11. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY APPLICATION, 2024 VS 2030 (%)

- FIGURE 12. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY APPLICATION, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 13. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY DISTRIBUTION CHANNEL, 2024 VS 2030 (%)

- FIGURE 14. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY DISTRIBUTION CHANNEL, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 15. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY COUNTRY, 2024 VS 2030 (%)

- FIGURE 16. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY COUNTRY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 17. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY STATE, 2024 VS 2030 (%)

- FIGURE 18. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY STATE, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 19. EUROPE, MIDDLE EAST & AFRICA ADVANCED CARBON MATERIALS MARKET SIZE, BY COUNTRY, 2024 VS 2030 (%)

- FIGURE 20. EUROPE, MIDDLE EAST & AFRICA ADVANCED CARBON MATERIALS MARKET SIZE, BY COUNTRY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 21. ASIA-PACIFIC ADVANCED CARBON MATERIALS MARKET SIZE, BY COUNTRY, 2024 VS 2030 (%)

- FIGURE 22. ASIA-PACIFIC ADVANCED CARBON MATERIALS MARKET SIZE, BY COUNTRY, 2024 VS 2025 VS 2030 (USD MILLION)

- FIGURE 23. ADVANCED CARBON MATERIALS MARKET SHARE, BY KEY PLAYER, 2024

- FIGURE 24. ADVANCED CARBON MATERIALS MARKET, FPNV POSITIONING MATRIX, 2024

- FIGURE 25. ADVANCED CARBON MATERIALS MARKET: RESEARCHAI

- FIGURE 26. ADVANCED CARBON MATERIALS MARKET: RESEARCHSTATISTICS

- FIGURE 27. ADVANCED CARBON MATERIALS MARKET: RESEARCHCONTACTS

- FIGURE 28. ADVANCED CARBON MATERIALS MARKET: RESEARCHARTICLES

LIST OF TABLES

- TABLE 1. ADVANCED CARBON MATERIALS MARKET SEGMENTATION & COVERAGE

- TABLE 2. UNITED STATES DOLLAR EXCHANGE RATE, 2018-2024

- TABLE 3. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, 2018-2024 (USD MILLION)

- TABLE 4. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, 2025-2030 (USD MILLION)

- TABLE 5. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY REGION, 2018-2024 (USD MILLION)

- TABLE 6. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY REGION, 2025-2030 (USD MILLION)

- TABLE 7. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY COUNTRY, 2018-2024 (USD MILLION)

- TABLE 8. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 9. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY MATERIAL TYPE, 2018-2024 (USD MILLION)

- TABLE 10. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY MATERIAL TYPE, 2025-2030 (USD MILLION)

- TABLE 11. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ACTIVATED CARBON, BY REGION, 2018-2024 (USD MILLION)

- TABLE 12. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ACTIVATED CARBON, BY REGION, 2025-2030 (USD MILLION)

- TABLE 13. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON BLACK, BY REGION, 2018-2024 (USD MILLION)

- TABLE 14. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON BLACK, BY REGION, 2025-2030 (USD MILLION)

- TABLE 15. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY FURNACE BLACK, BY REGION, 2018-2024 (USD MILLION)

- TABLE 16. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY FURNACE BLACK, BY REGION, 2025-2030 (USD MILLION)

- TABLE 17. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY GAS BLACK, BY REGION, 2018-2024 (USD MILLION)

- TABLE 18. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY GAS BLACK, BY REGION, 2025-2030 (USD MILLION)

- TABLE 19. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY THERMAL BLACK, BY REGION, 2018-2024 (USD MILLION)

- TABLE 20. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY THERMAL BLACK, BY REGION, 2025-2030 (USD MILLION)

- TABLE 21. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON BLACK, 2018-2024 (USD MILLION)

- TABLE 22. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON BLACK, 2025-2030 (USD MILLION)

- TABLE 23. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON COMPOSITES, BY REGION, 2018-2024 (USD MILLION)

- TABLE 24. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON COMPOSITES, BY REGION, 2025-2030 (USD MILLION)

- TABLE 25. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON FIBER, BY REGION, 2018-2024 (USD MILLION)

- TABLE 26. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON FIBER, BY REGION, 2025-2030 (USD MILLION)

- TABLE 27. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY PAN-BASED, BY REGION, 2018-2024 (USD MILLION)

- TABLE 28. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY PAN-BASED, BY REGION, 2025-2030 (USD MILLION)

- TABLE 29. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY PITCH-BASED, BY REGION, 2018-2024 (USD MILLION)

- TABLE 30. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY PITCH-BASED, BY REGION, 2025-2030 (USD MILLION)

- TABLE 31. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY RAYON-BASED, BY REGION, 2018-2024 (USD MILLION)

- TABLE 32. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY RAYON-BASED, BY REGION, 2025-2030 (USD MILLION)

- TABLE 33. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON FIBER, 2018-2024 (USD MILLION)

- TABLE 34. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON FIBER, 2025-2030 (USD MILLION)

- TABLE 35. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON NANOTUBES (CNTS), BY REGION, 2018-2024 (USD MILLION)

- TABLE 36. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON NANOTUBES (CNTS), BY REGION, 2025-2030 (USD MILLION)

- TABLE 37. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY MULTI-WALLED, BY REGION, 2018-2024 (USD MILLION)

- TABLE 38. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY MULTI-WALLED, BY REGION, 2025-2030 (USD MILLION)

- TABLE 39. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY SINGLE-WALLED, BY REGION, 2018-2024 (USD MILLION)

- TABLE 40. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY SINGLE-WALLED, BY REGION, 2025-2030 (USD MILLION)

- TABLE 41. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON NANOTUBES (CNTS), 2018-2024 (USD MILLION)

- TABLE 42. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON NANOTUBES (CNTS), 2025-2030 (USD MILLION)

- TABLE 43. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY GRAPHENE, BY REGION, 2018-2024 (USD MILLION)

- TABLE 44. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY GRAPHENE, BY REGION, 2025-2030 (USD MILLION)

- TABLE 45. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY GRAPHITE, BY REGION, 2018-2024 (USD MILLION)

- TABLE 46. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY GRAPHITE, BY REGION, 2025-2030 (USD MILLION)

- TABLE 47. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY FORM FACTOR, 2018-2024 (USD MILLION)

- TABLE 48. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY FORM FACTOR, 2025-2030 (USD MILLION)

- TABLE 49. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY COATINGS / INKS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 50. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY COATINGS / INKS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 51. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY FIBERS / FILAMENTS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 52. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY FIBERS / FILAMENTS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 53. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY FOAMS / AEROGELS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 54. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY FOAMS / AEROGELS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 55. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY PELLETS / GRANULES, BY REGION, 2018-2024 (USD MILLION)

- TABLE 56. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY PELLETS / GRANULES, BY REGION, 2025-2030 (USD MILLION)

- TABLE 57. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY POWDER, BY REGION, 2018-2024 (USD MILLION)

- TABLE 58. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY POWDER, BY REGION, 2025-2030 (USD MILLION)

- TABLE 59. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY SHEETS / FILMS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 60. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY SHEETS / FILMS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 61. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY MANUFACTURING TECHNOLOGY, 2018-2024 (USD MILLION)

- TABLE 62. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY MANUFACTURING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 63. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ARC DISCHARGE, BY REGION, 2018-2024 (USD MILLION)

- TABLE 64. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ARC DISCHARGE, BY REGION, 2025-2030 (USD MILLION)

- TABLE 65. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CHEMICAL VAPOR DEPOSITION (CVD), BY REGION, 2018-2024 (USD MILLION)

- TABLE 66. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CHEMICAL VAPOR DEPOSITION (CVD), BY REGION, 2025-2030 (USD MILLION)

- TABLE 67. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTROSPINNING, BY REGION, 2018-2024 (USD MILLION)

- TABLE 68. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTROSPINNING, BY REGION, 2025-2030 (USD MILLION)

- TABLE 69. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY HYDROTHERMAL CARBONIZATION, BY REGION, 2018-2024 (USD MILLION)

- TABLE 70. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY HYDROTHERMAL CARBONIZATION, BY REGION, 2025-2030 (USD MILLION)

- TABLE 71. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY LASER ABLATION, BY REGION, 2018-2024 (USD MILLION)

- TABLE 72. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY LASER ABLATION, BY REGION, 2025-2030 (USD MILLION)

- TABLE 73. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY PYROLYSIS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 74. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY PYROLYSIS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 75. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 76. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 77. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY AUTOMOTIVE & AEROSPACE, BY REGION, 2018-2024 (USD MILLION)

- TABLE 78. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY AUTOMOTIVE & AEROSPACE, BY REGION, 2025-2030 (USD MILLION)

- TABLE 79. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CONDUCTIVE COMPOSITES, BY REGION, 2018-2024 (USD MILLION)

- TABLE 80. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CONDUCTIVE COMPOSITES, BY REGION, 2025-2030 (USD MILLION)

- TABLE 81. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY STRUCTURAL COMPONENTS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 82. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY STRUCTURAL COMPONENTS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 83. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY THERMAL MANAGEMENT, BY REGION, 2018-2024 (USD MILLION)

- TABLE 84. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY THERMAL MANAGEMENT, BY REGION, 2025-2030 (USD MILLION)

- TABLE 85. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY AUTOMOTIVE & AEROSPACE, 2018-2024 (USD MILLION)

- TABLE 86. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY AUTOMOTIVE & AEROSPACE, 2025-2030 (USD MILLION)

- TABLE 87. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTRONICS & SEMICONDUCTORS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 88. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTRONICS & SEMICONDUCTORS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 89. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CONDUCTIVE INKS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 90. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CONDUCTIVE INKS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 91. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY EMI SHIELDING, BY REGION, 2018-2024 (USD MILLION)

- TABLE 92. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY EMI SHIELDING, BY REGION, 2025-2030 (USD MILLION)

- TABLE 93. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY SENSORS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 94. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY SENSORS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 95. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTRONICS & SEMICONDUCTORS, 2018-2024 (USD MILLION)

- TABLE 96. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTRONICS & SEMICONDUCTORS, 2025-2030 (USD MILLION)

- TABLE 97. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ENERGY STORAGE, BY REGION, 2018-2024 (USD MILLION)

- TABLE 98. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ENERGY STORAGE, BY REGION, 2025-2030 (USD MILLION)

- TABLE 99. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY FUEL CELLS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 100. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY FUEL CELLS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 101. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY LITHIUM ION BATTERIES, BY REGION, 2018-2024 (USD MILLION)

- TABLE 102. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY LITHIUM ION BATTERIES, BY REGION, 2025-2030 (USD MILLION)

- TABLE 103. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY SUPERCAPACITORS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 104. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY SUPERCAPACITORS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 105. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ENERGY STORAGE, 2018-2024 (USD MILLION)

- TABLE 106. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ENERGY STORAGE, 2025-2030 (USD MILLION)

- TABLE 107. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ENVIRONMENTAL, BY REGION, 2018-2024 (USD MILLION)

- TABLE 108. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ENVIRONMENTAL, BY REGION, 2025-2030 (USD MILLION)

- TABLE 109. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY AIR FILTRATION, BY REGION, 2018-2024 (USD MILLION)

- TABLE 110. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY AIR FILTRATION, BY REGION, 2025-2030 (USD MILLION)

- TABLE 111. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY SOIL REMEDIATION, BY REGION, 2018-2024 (USD MILLION)

- TABLE 112. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY SOIL REMEDIATION, BY REGION, 2025-2030 (USD MILLION)

- TABLE 113. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY WATER TREATMENT, BY REGION, 2018-2024 (USD MILLION)

- TABLE 114. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY WATER TREATMENT, BY REGION, 2025-2030 (USD MILLION)

- TABLE 115. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ENVIRONMENTAL, 2018-2024 (USD MILLION)

- TABLE 116. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ENVIRONMENTAL, 2025-2030 (USD MILLION)

- TABLE 117. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY INDUSTRIAL, BY REGION, 2018-2024 (USD MILLION)

- TABLE 118. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY INDUSTRIAL, BY REGION, 2025-2030 (USD MILLION)

- TABLE 119. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CATALYSIS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 120. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY CATALYSIS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 121. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY COATINGS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 122. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY COATINGS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 123. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY LUBRICANTS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 124. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY LUBRICANTS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 125. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY INDUSTRIAL, 2018-2024 (USD MILLION)

- TABLE 126. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY INDUSTRIAL, 2025-2030 (USD MILLION)

- TABLE 127. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY MEDICAL, BY REGION, 2018-2024 (USD MILLION)

- TABLE 128. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY MEDICAL, BY REGION, 2025-2030 (USD MILLION)

- TABLE 129. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY BIOSENSORS, BY REGION, 2018-2024 (USD MILLION)

- TABLE 130. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY BIOSENSORS, BY REGION, 2025-2030 (USD MILLION)

- TABLE 131. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY DRUG DELIVERY, BY REGION, 2018-2024 (USD MILLION)

- TABLE 132. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY DRUG DELIVERY, BY REGION, 2025-2030 (USD MILLION)

- TABLE 133. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY TISSUE ENGINEERING, BY REGION, 2018-2024 (USD MILLION)

- TABLE 134. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY TISSUE ENGINEERING, BY REGION, 2025-2030 (USD MILLION)

- TABLE 135. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY MEDICAL, 2018-2024 (USD MILLION)

- TABLE 136. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY MEDICAL, 2025-2030 (USD MILLION)

- TABLE 137. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY DISTRIBUTION CHANNEL, 2018-2024 (USD MILLION)

- TABLE 138. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY DISTRIBUTION CHANNEL, 2025-2030 (USD MILLION)

- TABLE 139. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY OFFLINE, BY REGION, 2018-2024 (USD MILLION)

- TABLE 140. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY OFFLINE, BY REGION, 2025-2030 (USD MILLION)

- TABLE 141. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ONLINE, BY REGION, 2018-2024 (USD MILLION)

- TABLE 142. GLOBAL ADVANCED CARBON MATERIALS MARKET SIZE, BY ONLINE, BY REGION, 2025-2030 (USD MILLION)

- TABLE 143. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY MATERIAL TYPE, 2018-2024 (USD MILLION)

- TABLE 144. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY MATERIAL TYPE, 2025-2030 (USD MILLION)

- TABLE 145. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON BLACK, 2018-2024 (USD MILLION)

- TABLE 146. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON BLACK, 2025-2030 (USD MILLION)

- TABLE 147. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON FIBER, 2018-2024 (USD MILLION)

- TABLE 148. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON FIBER, 2025-2030 (USD MILLION)

- TABLE 149. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON NANOTUBES (CNTS), 2018-2024 (USD MILLION)

- TABLE 150. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON NANOTUBES (CNTS), 2025-2030 (USD MILLION)

- TABLE 151. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY FORM FACTOR, 2018-2024 (USD MILLION)

- TABLE 152. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY FORM FACTOR, 2025-2030 (USD MILLION)

- TABLE 153. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY MANUFACTURING TECHNOLOGY, 2018-2024 (USD MILLION)

- TABLE 154. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY MANUFACTURING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 155. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 156. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 157. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY AUTOMOTIVE & AEROSPACE, 2018-2024 (USD MILLION)

- TABLE 158. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY AUTOMOTIVE & AEROSPACE, 2025-2030 (USD MILLION)

- TABLE 159. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTRONICS & SEMICONDUCTORS, 2018-2024 (USD MILLION)

- TABLE 160. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTRONICS & SEMICONDUCTORS, 2025-2030 (USD MILLION)

- TABLE 161. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY ENERGY STORAGE, 2018-2024 (USD MILLION)

- TABLE 162. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY ENERGY STORAGE, 2025-2030 (USD MILLION)

- TABLE 163. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY ENVIRONMENTAL, 2018-2024 (USD MILLION)

- TABLE 164. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY ENVIRONMENTAL, 2025-2030 (USD MILLION)

- TABLE 165. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY INDUSTRIAL, 2018-2024 (USD MILLION)

- TABLE 166. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY INDUSTRIAL, 2025-2030 (USD MILLION)

- TABLE 167. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY MEDICAL, 2018-2024 (USD MILLION)

- TABLE 168. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY MEDICAL, 2025-2030 (USD MILLION)

- TABLE 169. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY DISTRIBUTION CHANNEL, 2018-2024 (USD MILLION)

- TABLE 170. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY DISTRIBUTION CHANNEL, 2025-2030 (USD MILLION)

- TABLE 171. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY COUNTRY, 2018-2024 (USD MILLION)

- TABLE 172. AMERICAS ADVANCED CARBON MATERIALS MARKET SIZE, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 173. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY MATERIAL TYPE, 2018-2024 (USD MILLION)

- TABLE 174. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY MATERIAL TYPE, 2025-2030 (USD MILLION)

- TABLE 175. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON BLACK, 2018-2024 (USD MILLION)

- TABLE 176. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON BLACK, 2025-2030 (USD MILLION)

- TABLE 177. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON FIBER, 2018-2024 (USD MILLION)

- TABLE 178. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON FIBER, 2025-2030 (USD MILLION)

- TABLE 179. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON NANOTUBES (CNTS), 2018-2024 (USD MILLION)

- TABLE 180. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON NANOTUBES (CNTS), 2025-2030 (USD MILLION)

- TABLE 181. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY FORM FACTOR, 2018-2024 (USD MILLION)

- TABLE 182. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY FORM FACTOR, 2025-2030 (USD MILLION)

- TABLE 183. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY MANUFACTURING TECHNOLOGY, 2018-2024 (USD MILLION)

- TABLE 184. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY MANUFACTURING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 185. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 186. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 187. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY AUTOMOTIVE & AEROSPACE, 2018-2024 (USD MILLION)

- TABLE 188. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY AUTOMOTIVE & AEROSPACE, 2025-2030 (USD MILLION)

- TABLE 189. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTRONICS & SEMICONDUCTORS, 2018-2024 (USD MILLION)

- TABLE 190. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTRONICS & SEMICONDUCTORS, 2025-2030 (USD MILLION)

- TABLE 191. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY ENERGY STORAGE, 2018-2024 (USD MILLION)

- TABLE 192. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY ENERGY STORAGE, 2025-2030 (USD MILLION)

- TABLE 193. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY ENVIRONMENTAL, 2018-2024 (USD MILLION)

- TABLE 194. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY ENVIRONMENTAL, 2025-2030 (USD MILLION)

- TABLE 195. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY INDUSTRIAL, 2018-2024 (USD MILLION)

- TABLE 196. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY INDUSTRIAL, 2025-2030 (USD MILLION)

- TABLE 197. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY MEDICAL, 2018-2024 (USD MILLION)

- TABLE 198. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY MEDICAL, 2025-2030 (USD MILLION)

- TABLE 199. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY DISTRIBUTION CHANNEL, 2018-2024 (USD MILLION)

- TABLE 200. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY DISTRIBUTION CHANNEL, 2025-2030 (USD MILLION)

- TABLE 201. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY STATE, 2018-2024 (USD MILLION)

- TABLE 202. UNITED STATES ADVANCED CARBON MATERIALS MARKET SIZE, BY STATE, 2025-2030 (USD MILLION)

- TABLE 203. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY MATERIAL TYPE, 2018-2024 (USD MILLION)

- TABLE 204. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY MATERIAL TYPE, 2025-2030 (USD MILLION)

- TABLE 205. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON BLACK, 2018-2024 (USD MILLION)

- TABLE 206. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON BLACK, 2025-2030 (USD MILLION)

- TABLE 207. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON FIBER, 2018-2024 (USD MILLION)

- TABLE 208. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON FIBER, 2025-2030 (USD MILLION)

- TABLE 209. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON NANOTUBES (CNTS), 2018-2024 (USD MILLION)

- TABLE 210. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON NANOTUBES (CNTS), 2025-2030 (USD MILLION)

- TABLE 211. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY FORM FACTOR, 2018-2024 (USD MILLION)

- TABLE 212. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY FORM FACTOR, 2025-2030 (USD MILLION)

- TABLE 213. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY MANUFACTURING TECHNOLOGY, 2018-2024 (USD MILLION)

- TABLE 214. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY MANUFACTURING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 215. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 216. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 217. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY AUTOMOTIVE & AEROSPACE, 2018-2024 (USD MILLION)

- TABLE 218. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY AUTOMOTIVE & AEROSPACE, 2025-2030 (USD MILLION)

- TABLE 219. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTRONICS & SEMICONDUCTORS, 2018-2024 (USD MILLION)

- TABLE 220. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTRONICS & SEMICONDUCTORS, 2025-2030 (USD MILLION)

- TABLE 221. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY ENERGY STORAGE, 2018-2024 (USD MILLION)

- TABLE 222. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY ENERGY STORAGE, 2025-2030 (USD MILLION)

- TABLE 223. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY ENVIRONMENTAL, 2018-2024 (USD MILLION)

- TABLE 224. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY ENVIRONMENTAL, 2025-2030 (USD MILLION)

- TABLE 225. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY INDUSTRIAL, 2018-2024 (USD MILLION)

- TABLE 226. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY INDUSTRIAL, 2025-2030 (USD MILLION)

- TABLE 227. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY MEDICAL, 2018-2024 (USD MILLION)

- TABLE 228. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY MEDICAL, 2025-2030 (USD MILLION)

- TABLE 229. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY DISTRIBUTION CHANNEL, 2018-2024 (USD MILLION)

- TABLE 230. CANADA ADVANCED CARBON MATERIALS MARKET SIZE, BY DISTRIBUTION CHANNEL, 2025-2030 (USD MILLION)

- TABLE 231. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY MATERIAL TYPE, 2018-2024 (USD MILLION)

- TABLE 232. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY MATERIAL TYPE, 2025-2030 (USD MILLION)

- TABLE 233. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON BLACK, 2018-2024 (USD MILLION)

- TABLE 234. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON BLACK, 2025-2030 (USD MILLION)

- TABLE 235. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON FIBER, 2018-2024 (USD MILLION)

- TABLE 236. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON FIBER, 2025-2030 (USD MILLION)

- TABLE 237. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON NANOTUBES (CNTS), 2018-2024 (USD MILLION)

- TABLE 238. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON NANOTUBES (CNTS), 2025-2030 (USD MILLION)

- TABLE 239. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY FORM FACTOR, 2018-2024 (USD MILLION)

- TABLE 240. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY FORM FACTOR, 2025-2030 (USD MILLION)

- TABLE 241. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY MANUFACTURING TECHNOLOGY, 2018-2024 (USD MILLION)

- TABLE 242. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY MANUFACTURING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 243. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 244. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 245. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY AUTOMOTIVE & AEROSPACE, 2018-2024 (USD MILLION)

- TABLE 246. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY AUTOMOTIVE & AEROSPACE, 2025-2030 (USD MILLION)

- TABLE 247. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTRONICS & SEMICONDUCTORS, 2018-2024 (USD MILLION)

- TABLE 248. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTRONICS & SEMICONDUCTORS, 2025-2030 (USD MILLION)

- TABLE 249. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY ENERGY STORAGE, 2018-2024 (USD MILLION)

- TABLE 250. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY ENERGY STORAGE, 2025-2030 (USD MILLION)

- TABLE 251. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY ENVIRONMENTAL, 2018-2024 (USD MILLION)

- TABLE 252. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY ENVIRONMENTAL, 2025-2030 (USD MILLION)

- TABLE 253. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY INDUSTRIAL, 2018-2024 (USD MILLION)

- TABLE 254. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY INDUSTRIAL, 2025-2030 (USD MILLION)

- TABLE 255. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY MEDICAL, 2018-2024 (USD MILLION)

- TABLE 256. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY MEDICAL, 2025-2030 (USD MILLION)

- TABLE 257. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY DISTRIBUTION CHANNEL, 2018-2024 (USD MILLION)

- TABLE 258. MEXICO ADVANCED CARBON MATERIALS MARKET SIZE, BY DISTRIBUTION CHANNEL, 2025-2030 (USD MILLION)

- TABLE 259. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY MATERIAL TYPE, 2018-2024 (USD MILLION)

- TABLE 260. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY MATERIAL TYPE, 2025-2030 (USD MILLION)

- TABLE 261. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON BLACK, 2018-2024 (USD MILLION)

- TABLE 262. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON BLACK, 2025-2030 (USD MILLION)

- TABLE 263. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON FIBER, 2018-2024 (USD MILLION)

- TABLE 264. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON FIBER, 2025-2030 (USD MILLION)

- TABLE 265. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON NANOTUBES (CNTS), 2018-2024 (USD MILLION)

- TABLE 266. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON NANOTUBES (CNTS), 2025-2030 (USD MILLION)

- TABLE 267. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY FORM FACTOR, 2018-2024 (USD MILLION)

- TABLE 268. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY FORM FACTOR, 2025-2030 (USD MILLION)

- TABLE 269. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY MANUFACTURING TECHNOLOGY, 2018-2024 (USD MILLION)

- TABLE 270. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY MANUFACTURING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 271. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 272. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 273. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY AUTOMOTIVE & AEROSPACE, 2018-2024 (USD MILLION)

- TABLE 274. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY AUTOMOTIVE & AEROSPACE, 2025-2030 (USD MILLION)

- TABLE 275. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTRONICS & SEMICONDUCTORS, 2018-2024 (USD MILLION)

- TABLE 276. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTRONICS & SEMICONDUCTORS, 2025-2030 (USD MILLION)

- TABLE 277. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY ENERGY STORAGE, 2018-2024 (USD MILLION)

- TABLE 278. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY ENERGY STORAGE, 2025-2030 (USD MILLION)

- TABLE 279. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY ENVIRONMENTAL, 2018-2024 (USD MILLION)

- TABLE 280. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY ENVIRONMENTAL, 2025-2030 (USD MILLION)

- TABLE 281. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY INDUSTRIAL, 2018-2024 (USD MILLION)

- TABLE 282. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY INDUSTRIAL, 2025-2030 (USD MILLION)

- TABLE 283. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY MEDICAL, 2018-2024 (USD MILLION)

- TABLE 284. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY MEDICAL, 2025-2030 (USD MILLION)

- TABLE 285. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY DISTRIBUTION CHANNEL, 2018-2024 (USD MILLION)

- TABLE 286. BRAZIL ADVANCED CARBON MATERIALS MARKET SIZE, BY DISTRIBUTION CHANNEL, 2025-2030 (USD MILLION)

- TABLE 287. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY MATERIAL TYPE, 2018-2024 (USD MILLION)

- TABLE 288. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY MATERIAL TYPE, 2025-2030 (USD MILLION)

- TABLE 289. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON BLACK, 2018-2024 (USD MILLION)

- TABLE 290. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON BLACK, 2025-2030 (USD MILLION)

- TABLE 291. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON FIBER, 2018-2024 (USD MILLION)

- TABLE 292. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON FIBER, 2025-2030 (USD MILLION)

- TABLE 293. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON NANOTUBES (CNTS), 2018-2024 (USD MILLION)

- TABLE 294. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY CARBON NANOTUBES (CNTS), 2025-2030 (USD MILLION)

- TABLE 295. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY FORM FACTOR, 2018-2024 (USD MILLION)

- TABLE 296. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY FORM FACTOR, 2025-2030 (USD MILLION)

- TABLE 297. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY MANUFACTURING TECHNOLOGY, 2018-2024 (USD MILLION)

- TABLE 298. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY MANUFACTURING TECHNOLOGY, 2025-2030 (USD MILLION)

- TABLE 299. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY APPLICATION, 2018-2024 (USD MILLION)

- TABLE 300. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY APPLICATION, 2025-2030 (USD MILLION)

- TABLE 301. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY AUTOMOTIVE & AEROSPACE, 2018-2024 (USD MILLION)

- TABLE 302. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY AUTOMOTIVE & AEROSPACE, 2025-2030 (USD MILLION)

- TABLE 303. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTRONICS & SEMICONDUCTORS, 2018-2024 (USD MILLION)

- TABLE 304. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY ELECTRONICS & SEMICONDUCTORS, 2025-2030 (USD MILLION)

- TABLE 305. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY ENERGY STORAGE, 2018-2024 (USD MILLION)

- TABLE 306. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY ENERGY STORAGE, 2025-2030 (USD MILLION)

- TABLE 307. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY ENVIRONMENTAL, 2018-2024 (USD MILLION)

- TABLE 308. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY ENVIRONMENTAL, 2025-2030 (USD MILLION)

- TABLE 309. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY INDUSTRIAL, 2018-2024 (USD MILLION)

- TABLE 310. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY INDUSTRIAL, 2025-2030 (USD MILLION)

- TABLE 311. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY MEDICAL, 2018-2024 (USD MILLION)

- TABLE 312. ARGENTINA ADVANCED CARBON MATERIALS MARKET SIZE, BY MEDICAL, 2025-2030 (USD MILLION)

TABLE 31

The Advanced Carbon Materials Market was valued at USD 5.82 billion in 2024 and is projected to grow to USD 6.09 billion in 2025, with a CAGR of 4.82%, reaching USD 7.72 billion by 2030.

| KEY MARKET STATISTICS | |

|---|---|

| Base Year [2024] | USD 5.82 billion |

| Estimated Year [2025] | USD 6.09 billion |

| Forecast Year [2030] | USD 7.72 billion |

| CAGR (%) | 4.82% |

Exploring the Foundations of Advanced Carbon Materials to Illuminate Innovation Drivers and Unveil the Technological Landscape Shaping Future Growth

Advanced carbon materials represent a paradigm shift in the materials science arena, combining unique structural, electrical, and mechanical properties that enable next-generation solutions across multiple industries. As electrification accelerates in transportation and energy storage, carbon fiber and carbon nanotubes deliver lightweight strength and exceptional conductivity while graphene and carbon composites promise revolutionary enhancements in thermal management and electronic performance. At the same time, traditional forms such as activated carbon and carbon black continue to evolve, leveraging novel activation and production techniques to meet stringent environmental and filtration standards.

Innovation in this field is driven by increasing demand for smaller, more efficient, and more sustainable components. Stakeholders from research institutions, government agencies, and the private sector are collaborating to overcome manufacturing challenges, scale up novel processes, and reduce the carbon footprint of production. Moreover, regulatory frameworks and incentive programs are encouraging the adoption of low-emission materials, compelling companies to invest in research and development. Through these efforts, advanced carbon materials are poised to redefine performance benchmarks and deliver substantial competitive advantages to early adopters seeking to lead in the rapidly evolving landscape.

Tracing the Pivotal Transformations in Advanced Carbon Materials Technologies Redefining Industry Standards and Driving Unprecedented Competitive Advantages

Over the past decade, the advanced carbon materials landscape has undergone transformative shifts driven by breakthroughs in synthesis and processing techniques. Chemical vapor deposition and electrospinning have matured from laboratory curiosities into scalable manufacturing methods, enabling high-purity graphene and uniform carbon nanofiber production. Meanwhile, advancements in pyrolysis and hydrothermal carbonization are unlocking new pathways to tailor porosity and surface chemistry for specialized applications, such as energy storage and environmental remediation.

Furthermore, growing emphasis on circular economy principles has spurred the development of sustainable feedstocks and recycling strategies. Innovations in bio-based precursors and end-of-life recovery processes are mitigating the environmental impact of conventional carbon production. In parallel, digital tools and data-driven process controls are streamlining quality assurance, reducing production variability, and accelerating time to market. As a result, companies that integrate novel manufacturing technologies and embrace sustainability from the outset are gaining a decisive edge, setting the stage for a new era of agile, eco-conscious players in the advanced carbon materials arena.

Assessing the Broad Repercussions of Recent United States Tariff Measures on Advanced Carbon Materials Supply Chains Innovation and Market Accessibility

The introduction of new tariff measures by the United States in 2025 has reverberated across global supply chains for advanced carbon materials. Imported graphite and carbon nanotubes now carry higher duties, prompting manufacturers to reevaluate sourcing strategies and explore alternative suppliers in regions with favorable trade agreements. Consequently, several producers have shifted part of their procurement to domestic or near-shore origins to mitigate added costs and ensure continuity of critical inputs.

This realignment has also accelerated regional partnerships and joint ventures as companies seek to localize high-performance carbon black and fiber production. Although the immediate impact includes increased raw-material prices and extended lead times, industry participants are leveraging the situation to invest in indigenous manufacturing capabilities. In doing so, they not only reduce tariff exposure but also fortify proprietary process know-how. Ultimately, these adjustments are fostering a more resilient and diversified ecosystem that can better withstand future policy fluctuations and global trade uncertainties.

Uncovering Key Segmentation Dynamics in Advanced Carbon Materials Spanning Material Types Form Factors Manufacturing Methods and Diverse Application Verticals

A granular examination of material types reveals a spectrum of performance attributes that cater to distinct end uses. Activated carbon excels in adsorption for environmental and medical applications, whereas carbon black, available in furnace, gas, and thermal variants, serves as a cornerstone in coatings, inks, and polymer reinforcement. Carbon composites harness the synergy of carbon fiber matrices, with PAN-based, pitch-based, and rayon-based fibers delivering tailored strength and stiffness parameters. Meanwhile, graphene's unparalleled conductivity and single-walled or multi-walled carbon nanotubes drive breakthroughs in electronics, sensors, and conductive coatings.

Form factor further influences material selection, as powders, foams, aerogels, and sheets or films each offer unique processing advantages. Pellets and granules facilitate consistent dosing in compounding processes, while fibers and filaments are indispensable in composite manufacture. The choice of manufacturing technology-ranging from arc discharge and laser ablation to chemical vapor deposition and electrospinning-determines purity, morphology, and scalability. Finally, applications span automotive and aerospace thermal management and structural components, electronics and semiconductors requiring EMI shielding and conductive inks, to energy storage solutions in fuel cells and supercapacitors, and environmental sectors utilizing air filtration, water treatment, and soil remediation. Distribution channels balance traditional offline networks with growing online platforms, ensuring that a broad spectrum of end users can access the precise form and function of the carbon material they require.

Examining Regional Dynamics Shaping Advanced Carbon Materials Adoption Across Americas Europe Middle East Africa and Asia-Pacific Markets

Regional insights demonstrate that each major geography is carving its own pathway in the advanced carbon materials domain. In the Americas, a strong foundation of research institutions and supportive policy measures underpin rapid advancement in carbon fiber composites for the aerospace and automotive sectors. Collaborative innovation hubs in North America are fostering synergies between materials developers and end-use manufacturers, driving early adoption of next-generation carbon nanomaterials.

In Europe, the Middle East, and Africa, stringent environmental regulations and a deep commitment to sustainability have catalyzed the deployment of activated carbon and graphene in water treatment and emission control systems. Investments in advanced manufacturing infrastructure and public-private partnerships are accelerating the transition from pilot-scale projects to full commercial operations. Meanwhile, Asia-Pacific is emerging as a powerhouse for cost-competitive production, leveraging economies of scale in countries with established chemical processing capabilities. Local supply chain integration and government incentives support widespread adoption across electronics, energy storage, and industrial applications, positioning the region as a critical growth engine for the global market.

Illuminating Competitive Strategies and Innovative Initiatives of Leading Companies Driving the Advanced Carbon Materials Industry Forward

Leading companies in the advanced carbon materials sphere are distinguished by their ability to integrate end-to-end capabilities-from raw carbon precursors to high-value nanomaterials. Firms specializing in carbon black have bolstered their portfolios through targeted acquisitions and capacity expansions, enabling them to serve burgeoning demand in tire reinforcement and pigment applications. At the same time, corporate leaders in carbon fiber are differentiating through investments in proprietary precursor technologies and advanced tow production lines that reduce cycle times and energy consumption.

On the frontier of nanomaterials, pioneers in graphene and carbon nanotube production are focusing on scalability and quality control. Strategic alliances with automotive and electronics manufacturers are accelerating the commercial integration of conductive inks and EMI shielding components. By harnessing cross-sectoral partnerships and co-development programs, these companies are establishing robust intellectual property frameworks and enhancing their ability to deliver customized solutions. Collectively, these top performers demonstrate that sustained research investments, agile manufacturing strategies, and targeted collaborations are critical levers for maintaining competitive advantage.

Empowering Industry Leaders with Practical Strategies and Roadmaps to Capitalize on Emerging Trends and Strengthen Market Position in Advanced Carbon Materials

Industry leaders seeking to capitalize on emerging opportunities in advanced carbon materials should first prioritize flexible manufacturing platforms that can accommodate evolving material specifications. By integrating modular production lines capable of switching between carbon fiber precursors or varying carbon black grades, organizations can respond swiftly to shifting application requirements and regulatory mandates.

Next, fostering partnerships with academic and research institutions will accelerate the commercialization of breakthrough technologies, such as high-strength graphene composites and multi-walled nanotube-reinforced polymers. Collaborative consortia help de-risk early-stage development while pooling expertise and scaling capabilities more efficiently. Moreover, establishing dedicated initiatives for sustainability-by exploring bio-based feedstocks and end-of-life recycling-will not only satisfy stakeholder expectations but also unlock new revenue streams in circular economy models. Together, these recommendations form a cohesive playbook that empowers decision-makers to drive innovation, optimize resource allocation, and secure resilient supply chain networks.

Detailing Rigorous Research Approaches Data Collection Techniques and Analytical Frameworks Underpinning Comprehensive Insights into Advanced Carbon Materials

This research adopts a rigorous methodology, combining secondary data analysis with in-depth primary research to ensure the most accurate and reliable insights. Initial desk research involved reviewing technical white papers, patent filings, and industry journals to map the current state of advanced carbon materials. This foundational phase was supplemented by structured interviews with senior executives, research scientists, and procurement specialists across key regions to validate findings and capture firsthand perspectives on market drivers.

Quantitative data was triangulated through multiple sources, including production statistics, trade databases, and regulatory filings, to develop a comprehensive understanding of supply chain dynamics and technology adoption rates. Analytical frameworks such as SWOT and Porter's Five Forces were employed to evaluate competitive positioning and assess potential entry barriers. Finally, insights were peer-reviewed by subject-matter experts to eliminate bias and ensure that conclusions reflect the latest industry advancements and real-world challenges.

Synthesizing Core Findings and Strategic Imperatives to Present a Coherent Vision for Future Developments in the Advanced Carbon Materials Ecosystem

In synthesizing the core findings, it becomes clear that advanced carbon materials are at the cusp of broad industrial integration, driven by continuous technological breakthroughs and heightened focus on sustainability. The interplay between manufacturing innovations and strategic partnerships will shape competitive dynamics, while regional trade policies and tariff landscapes will influence supply chain architectures. For decision-makers, embracing modular production, diversifying sourcing strategies, and investing in circular economy initiatives are essential imperatives.

Looking ahead, the maturation of novel feedstocks and scalable nanomaterial processes will create new application frontiers, from ultra-lightweight composites to next-generation energy storage solutions. Those organizations that align their R&D roadmaps with market requirements, forge collaborative ecosystems, and maintain operational agility will be best positioned to capture value. Ultimately, the advanced carbon materials ecosystem offers significant potential for those who navigate its complexities with a clear strategic vision and a commitment to innovation.

Table of Contents

1. Preface

- 1.1. Objectives of the Study

- 1.2. Market Segmentation & Coverage

- 1.3. Years Considered for the Study

- 1.4. Currency & Pricing

- 1.5. Language

- 1.6. Stakeholders

2. Research Methodology

- 2.1. Define: Research Objective

- 2.2. Determine: Research Design

- 2.3. Prepare: Research Instrument

- 2.4. Collect: Data Source

- 2.5. Analyze: Data Interpretation

- 2.6. Formulate: Data Verification

- 2.7. Publish: Research Report

- 2.8. Repeat: Report Update

3. Executive Summary

4. Market Overview

- 4.1. Introduction

- 4.2. Market Sizing & Forecasting

5. Market Dynamics

- 5.1. Integration of graphene-based electrodes in next-generation flexible electronics

- 5.2. Scale-up challenges and innovations in sustainable carbon nanotube manufacturing

- 5.3. Adoption of activated carbon in emerging water purification and air filtration systems

- 5.4. Development of graphene quantum dots for high-sensitivity bioimaging and diagnostics

- 5.5. Commercialization of binder-free carbon anodes for fast-charging lithium-ion batteries

- 5.6. Advances in hierarchical porous carbon scaffolds for high-performance supercapacitors

- 5.7. Implementation of biomass-derived carbon materials in circular economy applications

- 5.8. Automotive manufacturers accelerating adoption of carbon fiber composites for electric vehicles

- 5.9. Graphene quantum dots opening new possibilities in flexible electronics and optoelectronics

- 5.10. Innovation in biomass-derived activated carbon targeting sustainable water purification solutions

6. Market Insights

- 6.1. Porter's Five Forces Analysis

- 6.2. PESTLE Analysis

7. Cumulative Impact of United States Tariffs 2025

8. Advanced Carbon Materials Market, by Material Type

- 8.1. Introduction

- 8.2. Activated Carbon

- 8.3. Carbon Black

- 8.3.1. Furnace Black

- 8.3.2. Gas Black

- 8.3.3. Thermal Black

- 8.4. Carbon Composites

- 8.5. Carbon Fiber

- 8.5.1. PAN-based

- 8.5.2. Pitch-based

- 8.5.3. Rayon-based

- 8.6. Carbon Nanotubes (CNTs)

- 8.6.1. Multi-Walled

- 8.6.2. Single-Walled

- 8.7. Graphene

- 8.8. Graphite

9. Advanced Carbon Materials Market, by Form Factor

- 9.1. Introduction

- 9.2. Coatings / Inks

- 9.3. Fibers / Filaments

- 9.4. Foams / Aerogels

- 9.5. Pellets / Granules

- 9.6. Powder

- 9.7. Sheets / Films

10. Advanced Carbon Materials Market, by Manufacturing Technology

- 10.1. Introduction

- 10.2. Arc Discharge

- 10.3. Chemical Vapor Deposition (CVD)

- 10.4. Electrospinning

- 10.5. Hydrothermal Carbonization

- 10.6. Laser Ablation

- 10.7. Pyrolysis

11. Advanced Carbon Materials Market, by Application

- 11.1. Introduction

- 11.2. Automotive & Aerospace

- 11.2.1. Conductive Composites

- 11.2.2. Structural Components

- 11.2.3. Thermal Management

- 11.3. Electronics & Semiconductors

- 11.3.1. Conductive Inks

- 11.3.2. EMI Shielding

- 11.3.3. Sensors

- 11.4. Energy Storage

- 11.4.1. Fuel Cells

- 11.4.2. Lithium Ion Batteries

- 11.4.3. Supercapacitors

- 11.5. Environmental

- 11.5.1. Air Filtration

- 11.5.2. Soil Remediation

- 11.5.3. Water Treatment

- 11.6. Industrial

- 11.6.1. Catalysis

- 11.6.2. Coatings

- 11.6.3. Lubricants

- 11.7. Medical

- 11.7.1. Biosensors

- 11.7.2. Drug Delivery

- 11.7.3. Tissue Engineering

12. Advanced Carbon Materials Market, by Distribution Channel

- 12.1. Introduction

- 12.2. Offline

- 12.3. Online

13. Americas Advanced Carbon Materials Market

- 13.1. Introduction

- 13.2. United States

- 13.3. Canada

- 13.4. Mexico

- 13.5. Brazil

- 13.6. Argentina

14. Europe, Middle East & Africa Advanced Carbon Materials Market

- 14.1. Introduction

- 14.2. United Kingdom

- 14.3. Germany

- 14.4. France

- 14.5. Russia

- 14.6. Italy

- 14.7. Spain

- 14.8. United Arab Emirates

- 14.9. Saudi Arabia

- 14.10. South Africa

- 14.11. Denmark

- 14.12. Netherlands

- 14.13. Qatar

- 14.14. Finland

- 14.15. Sweden

- 14.16. Nigeria

- 14.17. Egypt

- 14.18. Turkey

- 14.19. Israel

- 14.20. Norway

- 14.21. Poland

- 14.22. Switzerland

15. Asia-Pacific Advanced Carbon Materials Market

- 15.1. Introduction

- 15.2. China

- 15.3. India

- 15.4. Japan

- 15.5. Australia

- 15.6. South Korea

- 15.7. Indonesia

- 15.8. Thailand

- 15.9. Philippines

- 15.10. Malaysia

- 15.11. Singapore

- 15.12. Vietnam

- 15.13. Taiwan

16. Competitive Landscape

- 16.1. Market Share Analysis, 2024

- 16.2. FPNV Positioning Matrix, 2024

- 16.3. Competitive Analysis

- 16.3.1. Anaori Carbon Co. Ltd

- 16.3.2. Arkema SA

- 16.3.3. Birla Carbon USA Inc

- 16.3.4. Cabot Corporation

- 16.3.5. CVD Equipment Corporation

- 16.3.6. Global Graphene Group

- 16.3.7. Graphenano Group

- 16.3.8. GRUPO ANTOLIN IRAUSA, S.A.

- 16.3.9. Haydale Graphene Industries PLC

- 16.3.10. Hexcel Corporation

- 16.3.11. Jiangsu Cnano Technology Co., Ltd

- 16.3.12. LG Chem Ltd

- 16.3.13. Mitsubishi Chemical Group Corporation.

- 16.3.14. Nanocyl SA

- 16.3.15. Nanoshel LLC

- 16.3.16. Orion Engineered Carbons GmbH

- 16.3.17. SGL Carbon SE

- 16.3.18. TEIJIN LIMITED

- 16.3.19. Tokai Carbon Co., Ltd.

- 16.3.20. Tokyo Chemical Industry Co., Ltd.

- 16.3.21. Toyo Tanso Co.,Ltd.

- 16.3.22. ZEON CORPORATION