|

|

市場調査レポート

商品コード

1370273

サーマルインターフェース材料市場:世界の産業動向、シェア、市場規模、成長、機会、2023-2028年予測Thermal Interface Materials Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2023-2028 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| サーマルインターフェース材料市場:世界の産業動向、シェア、市場規模、成長、機会、2023-2028年予測 |

|

出版日: 2023年10月15日

発行: IMARC

ページ情報: 英文 138 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

概要

市場概要:

世界の熱インターフェース材料市場規模は、2022年に32億米ドルに達しました。今後、IMARC Groupは、2023年から2028年にかけて9.4%の成長率(CAGR)を示し、2028年までに55億米ドルに達すると予測しています。効率的な熱管理ソリューションに対する需要の高まり、新しいTIM配合と技術の市場開拓、電子機器需要の高まり、電子部品の小型化、半導体技術の急速な進歩などが市場を後押ししています。

サーマルインターフェイス材料(TIM)は、様々な電子機器において2つの表面間の熱を効率的に伝達する上で重要です。その主な機能は、マイクロプロセッサー、パワートランジスター、LEDモジュール、ヒートシンクやスプレッダーなどの部品間の隙間やエアポケットを埋め、熱放散を最大限に確保することです。ヒートシンクは、熱伝導率が高く、熱抵抗が小さいため、熱伝導が促進されるように設計されています。サーマルグリース、パッド、相変化材料、接着剤など、さまざまな形状があります。TIMはそれぞれ独自の特性と用途を持ち、特定の要件に対応しています。TIMの重要性は、熱抵抗を低減し、電子デバイスの性能、信頼性、寿命に悪影響を及ぼす過熱を防止する能力にあります。効率的な熱放散を促進することで、TIMは最適な動作温度を維持し、サーマルスロットリングを防ぎ、システム全体の性能を向上させます。

世界市場は、スマートフォン、ノートパソコン、車載用電子機器など、電子機器の利用拡大が主な要因となっています。これに伴い、高電力密度化や部品集積度の向上など、半導体技術の急速な進歩が市場に大きく貢献しています。さらに、電気自動車の生産台数の増加により、バッテリー、パワーエレクトロニクス、電気モーターから発生する熱を処理するための効果的な熱管理が必要となり、市場にプラスの影響を与えています。これとは別に、データセンター・インフラの増加が市場を活性化しています。さらに、電子機器のエネルギー効率を向上させる必要性が高まっており、過熱防止、消費電力の削減、全体的なエネルギー効率の向上に役立つため、製品の採用が加速しています。そのほか、研究開発の活発化により、熱伝導性、信頼性、アプリケーションの容易性が改善された新しいTIM配合が開発され、市場に多くの機会を提供しています。さらに、自動車や航空宇宙などさまざまな産業における規制基準やガイドラインは、安全性と信頼性を確保するために効果的な熱管理を義務付けており、市場の成長に寄与しています。

サーマルインターフェイス材料の市場動向と促進要因:

コンシューマーエレクトロニクス産業の著しい成長

コンシューマーエレクトロニクス産業の著しい成長が市場に好影響を与えています。コンシューマーエレクトロニクス分野には、スマートフォン、タブレット、ノートパソコン、ゲーム機、スマートホームデバイス、ウェアラブル技術など、幅広いデバイスが含まれます。この業界の拡大に伴い、TIMの需要も並行して高まっています。民生用電子機器はますます小型化、高性能化、エネルギー効率化が進んでいます。しかし、こうした進歩は同時に、機器内でより多くの熱を発生させます。TIMは、この熱を効果的に放散し、電子部品の適切な機能と寿命を確保する上で重要な役割を果たします。さらに、消費者はデバイスの性能と信頼性に対する期待を高めています。過熱は性能を低下させ、システム障害を引き起こし、さらには安全上の危険にもつながります。そのためメーカーは、効率的な冷却ソリューションに対する消費者の要求に応えるため、TIMを使用した効果的な熱管理を優先しています。さらに、新しく革新的な民生用電子機器のイントロダクションより、熱伝導性、信頼性、アプリケーションの容易性を向上させる高度なTIM配合のニーズが絶えず高まっています。民生用電子機器業界の継続的な成長と技術革新は、市場に大きく貢献しています。

熱関連の問題に関する意識の高まり

過熱がデバイスの性能と寿命に及ぼす悪影響に関する意識の高まりが市場を強化しています。技術が進歩し、デバイスがより小型で高性能になるにつれて、熱の管理が重要になっています。熱に関連する問題は、性能の低下、システムの故障、さらには安全上の危険性にもつながります。このような問題に対する意識の高まりから、メーカー、エンジニア、消費者は、TIMを使用した効果的な熱管理を優先するようになっています。熱放散を最適化し、電子部品の信頼性の高い動作を保証するために、適切なTIMを選択することの重要性を認識する業界関係者が増えています。さらに、消費者は、熱によるデバイスの性能と寿命への影響について、より深く知るようになっています。消費者は、オーバーヒートしたりサーマルスロットリングを経験したりすることなく、要求の厳しいタスクに耐えることができる電子デバイスを求めています。その結果、デバイスメーカーは高品質のTIMを組み込んで熱伝達を強化し、最適な動作温度を維持することで、消費者の満足度と製品の信頼性を向上させています。熱に関連する問題に対する意識の高まりと、効率的で信頼性の高い電子機器への要望が、家電、自動車、通信、データセンターなど、さまざまな業界におけるTIMの採用と需要を後押ししています。

ハイパフォーマンス・コンピューティングの需要拡大

ハイパフォーマンス・コンピューティング(HPC)への需要の高まりが市場を促進しています。人工知能、機械学習、データ分析、科学シミュレーションなどのHPCアプリケーションには、強力なプロセッサーと、かなりの熱を発生する高度なハードウェア構成が必要です。HPCシステムでは、最適なパフォーマンスを維持し、オーバーヒートを防ぐために、効率的な熱管理が極めて重要です。TIMは、高性能プロセッサ、グラフィックスカード、その他のコンポーネント、およびヒートシンクや冷却ソリューション間の熱移動を促進します。金融、ヘルスケア、研究、エンターテインメントなどの業界全体でHPCの需要が増加し続けるにつれ、高度なTIMの必要性が高まっています。これらの材料は、HPCアプリケーションの要求を満たすために、高い熱伝導性、低い熱抵抗、信頼性を備えていなければなりません。さらに、より強力なプロセッサーやGPUの開発など、HPC技術の進歩が進むにつれて、より高い熱負荷に対応し、効率的な熱管理を提供できる高度なTIM配合の必要性が高まっています。高性能コンピューティングに対する需要の高まりと、熱効率を確保する上でTIMが果たす重要な役割は、市場を推進する重要な要因となっています。

サーマルインターフェイス材料産業のセグメンテーション

IMARC Groupは、世界のサーマルインターフェイス材料市場レポートの各セグメントにおける主要動向の分析と、2023年から2028年までの世界、地域、国レベルの予測を提供しています。当レポートでは、製品タイプと用途に基づいて市場を分類しています。

製品タイプ別の内訳

テープとフィルム

エラストマーパッド

グリースと接着剤

相変化材料

金属ベース材料

その他

グリースと接着剤が市場を独占

本レポートでは、製品タイプ別に市場を詳細に区分・分析しています。これには、テープ・フィルム、エラストマーパッド、グリース・接着剤、相変化材料、金属ベース材料、その他が含まれます。報告書によると、グリースと接着剤が最大のセグメントを占めています。

グリースと接着剤は、その熱伝導性、塗布の容易さ、部品間の隙間や空隙を埋める能力により、様々な産業で広く使用されています。電子機器では、部品とヒートシンク間の熱伝達を促進し、効率的な熱管理を保証して過熱を防ぐために一般的に使用されています。

世界中で電気自動車の生産台数が大幅に増加していることが、グリースと接着剤の需要を押し上げる大きな要因となっています。電気自動車はバッテリー、パワーエレクトロニクス、モーターからかなりの熱を発生します。グリースと接着剤は効果的な熱伝導性を提供し、これらの部品の放熱を助け、全体的な性能と寿命に貢献します。

アプリケーション別内訳

電気通信

コンピューター

医療機器

産業機械

耐久消費財

カーエレクトロニクス

その他

コンピュータが最大シェア

本レポートでは、市場を用途別に詳細に区分・分析しています。これには、通信、コンピュータ、医療機器、産業機械、耐久消費財、自動車エレクトロニクス、その他が含まれます。同レポートによると、コンピュータが最大の市場シェアを占めています。

効果的な熱管理ソリューションの必要性は、コンピュータ技術の継続的な進歩と高性能コンピューティングデバイスの需要増加に伴い、極めて重要になっています。コンピュータは、放熱を強化し、プロセッサ、グラフィックスカード、メモリモジュールなどのコンポーネントの全体的な熱性能を向上させるために、サーマルインターフェース材料を使用することが多いです。これらの材料は、これらのコンポーネントから発生する熱をヒートシンクやその他の冷却機構に効率的に伝達し、過熱を防止して最適な動作を保証するのに役立ちます。

コンピューター・システムがより高性能でコンパクトになるにつれ、熱に関する課題はますます大きくなっています。電子部品の小型化により、電力密度が高くなり、発熱量が増加します。このため、優れた熱伝導性、低い熱抵抗、さまざまな条件下での信頼性の高い性能を提供する高度なサーマルインターフェース材料を使用する必要があります。さらに、ゲーミングPC、データセンター、クラウドコンピューティングインフラへの需要の高まりが、コンピューター分野でのサーマルインターフェイス材料の採用をさらに後押ししています。安定した動作温度を維持し、エネルギー効率を向上させる必要性が市場成長の原動力となっており、メーカー各社はコンピュータ業界の新興国市場の需要に対応できる革新的なサーマルインターフェイス材料の開発に取り組んでいます。

地域別内訳

北米

米国

カナダ

アジア太平洋

中国

日本

インド

韓国

オーストラリア

インドネシア

その他

欧州

ドイツ

フランス

英国

イタリア

スペイン

ロシア

その他

ラテンアメリカ

ブラジル

メキシコ

その他

中東・アフリカ

アジア太平洋地域が明確な優位性を示し、最大の熱インターフェース材料市場シェアを占める

本レポートでは、北米(米国、カナダ)、アジア太平洋(中国、日本、インド、韓国、オーストラリア、インドネシア、その他)、欧州(ドイツ、フランス、英国、イタリア、スペイン、ロシア、その他)、ラテンアメリカ(ブラジル、メキシコ、その他)、中東アフリカを含む主要地域市場についても包括的に分析しています。

アジア太平洋地域は、急速な工業化、技術の進歩、主要な電子機器・半導体製造拠点の存在により、サーマル・マテリアル市場の主要市場となっています。アジア太平洋地域には、電子機器や電子部品の主要生産国や消費国があります。この地域は、家電、自動車、通信の各分野で優位を占めており、電子システムの最適な性能と信頼性を確保するための効果的な熱管理ソリューションの必要性が高まっています。

さらに、アジア太平洋地域における都市化の進展、可処分所得の増加、中流階級の人口拡大が、スマートフォン、ノートパソコン、ゲーム機などの電子機器の普及拡大に寄与しています。このため、これらの機器に関連する熱課題に対処するためのサーマルインターフェイス材料の需要が高まっています。さらに、同地域ではエネルギー効率、環境の持続可能性、電子機器の熱管理に関する規制への注目が高まっており、市場の活性化に拍車をかけています。アジア太平洋地域のメーカーは、高熱伝導性、低熱抵抗、環境配慮を実現する先進的なサーマルインターフェイス材料を開発するための研究開発活動に投資しています。

競合情勢:

サーマル・マテリアルのトップ企業は、革新的なソリューションと広範な研究開発努力によって市場を活性化する上で極めて重要です。これらの企業は、さまざまな産業の進化するニーズに対応する先進的な熱インターフェース材料の開発で最先端を走っています。製品の熱伝導性、耐久性、信頼性を高めるため、研究開発に多額の投資を行っています。メーカーや顧客と密接に協力し、彼らの要求を理解し、熱管理の課題に対するオーダーメードのソリューションを開発しています。さらに、これらの企業は、さまざまな用途や業界に適した幅広いサーマルインターフェイス材料を提供するため、製品ポートフォリオの拡大に注力しています。また、補完的な技術や専門知識を活用するための協力関係や戦略的パートナーシップを重視し、総合的な熱管理ソリューションを提供できるようにしています。継続的な技術革新、高品質な製品、強固な顧客関係を通じて、これらの熱インターフェース材料のトップ企業は、業界標準を設定し、様々な分野にわたる効率的な熱管理ソリューションに対する需要の高まりに対応することで、市場を牽引しています。

当レポートでは、熱インターフェース材料市場における競合情勢を包括的に分析しています。主要企業の詳細プロファイルも掲載しています。同市場の主要企業には以下のようなものがある:

3M社

ダウ社

ヘンケルAG &Co.KGaA

ハネウェル・インターナショナル

インジウム・コーポレーション

キタガワ・インダストリーズ・アメリカ

レアード・テクノロジーズ・インク

モメンティブ・パフォーマンス・マテリアルズ

パーカー・ハネフィン株式会社

ザルマンテック株式会社ザルマンテック株式会社

最近の動向

2021年7月、ダウはDOWSIL TC-4551 CVギャップフィラー、DOWSIL TC-2035 CV接着剤、DOWSIL TC-4060 GB250サーマルゲルを上市しました。これらのシリコーン系サーマルインターフェイス材料は、電気自動車やハイブリッド車のエレクトロニクス用途に向けたものです。

2022年4月、信越化学工業株式会社は、電気自動車向けに設計された新しいサーマルインターフェースのシリコーンゴムシートを発売しました。

2022年5月、アリエカはローム株式会社とEV市場向け次世代熱インターフェース材料の共同研究開発で提携しました。

本レポートで扱う主な質問

- 2022年の熱インターフェース材料の世界市場規模は?

- 2023年~2028年の世界の熱インターフェース材料市場の予想成長率は?

- 熱インターフェース材料の世界市場を牽引する主要因は何か

- COVID-19が世界の熱インターフェース材料市場に与えた影響は?

- 熱インターフェース材料の世界市場の製品タイプ別区分は?

- 熱インターフェース材料の世界市場の用途別区分は?

- 熱インターフェース材料の世界市場における主要地域は?

- 熱インターフェース材料の世界市場における主要プレイヤー/企業は?

目次

第1章 序文

第2章 調査範囲と調査手法

- 調査目的

- 利害関係者

- データソース

- 一次情報

- 二次情報

- 市場推定

- ボトムアップアプローチ

- トップダウンアプローチ

- 調査手法

第3章 エグゼクティブサマリー

第4章 イントロダクション

- 概要

- 主要産業動向

第5章 世界の熱インターフェース材料市場

- 市場概要

- 市場実績

- COVID-19の影響

- 市場予測

第6章 市場内訳:製品タイプ別

- テープとフィルム

- 市場動向

- 市場予測

- エラストマーパッド

- 市場動向

- 市場予測

- グリースと接着剤

- 市場動向

- 市場予測

- 相変化材料

- 市場動向

- 市場予測

- 金属ベース材料

- 市場動向

- 市場予測

- その他

- 市場動向

- 市場予測

第7章 市場内訳:アプリケーション別

- テレコム

- 市場動向

- 市場予測

- コンピューター

- 市場動向

- 市場予測

- 医療機器

- 市場動向

- 市場予測

- 産業機械

- 市場動向

- 市場予測

- 耐久消費財

- 市場動向

- 市場予測

- カーエレクトロニクス

- 市場動向

- 市場予測

- その他

- 市場動向

- 市場予測

第8章 市場内訳:地域別

- 北米

- 米国

- 市場動向

- 市場予測

- カナダ

- 市場動向

- 市場予測

- 米国

- アジア太平洋

- 中国

- 市場動向

- 市場予測

- 日本

- 市場動向

- 市場予測

- インド

- 市場動向

- 市場予測

- 韓国

- 市場動向

- 市場予測

- オーストラリア

- 市場動向

- 市場予測

- インドネシア

- 市場動向

- 市場予測

- その他

- 市場動向

- 市場予測

- 中国

- 欧州

- ドイツ

- 市場動向

- 市場予測

- フランス

- 市場動向

- 市場予測

- 英国

- 市場動向

- 市場予測

- イタリア

- 市場動向

- 市場予測

- スペイン

- 市場動向

- 市場予測

- ロシア

- 市場動向

- 市場予測

- その他

- 市場動向

- 市場予測

- ドイツ

- ラテンアメリカ

- ブラジル

- 市場動向

- 市場予測

- メキシコ

- 市場動向

- 市場予測

- その他

- 市場動向

- 市場予測

- ブラジル

- 中東・アフリカ地域

- 市場動向

- 市場内訳:国別

- 市場予測

第9章 SWOT分析

- 概要

- 強み

- 弱み

- 機会

- 脅威

第10章 バリューチェーン分析

第11章 ポーターのファイブフォース分析

- 概要

- 買い手の交渉力

- 供給企業の交渉力

- 競合の程度

- 新規参入業者の脅威

- 代替品の脅威

第12章 価格指標

第13章 競合情勢

- 市場構造

- 主要企業

- 主要企業のプロファイル

- 3M Company

- Dow Inc.

- Henkel AG & Co. KGaA

- Honeywell International Inc.

- Indium Corporation

- Kitagawa Industries America Inc.

- Laird Technologies Inc.

- Momentive Performance Materials Inc.

- Parker-Hannifin Corporation

- Zalman Tech Co., Ltd.

List of Figures

- Figure 1: Global: Thermal Interface Materials Market: Major Drivers and Challenges

- Figure 2: Global: Thermal Interface Materials Market: Sales Value (in Billion US$), 2017-2022

- Figure 3: Global: Thermal Interface Materials Market: Breakup by Product Type (in %), 2022

- Figure 4: Global: Thermal Interface Materials Market: Breakup by Application (in %), 2022

- Figure 5: Global: Thermal Interface Materials Market: Breakup by Region (in %), 2022

- Figure 6: Global: Thermal Interface Materials Market Forecast: Sales Value (in Billion US$), 2023-2028

- Figure 7: Global: Thermal Interface Materials (Tapes and Films) Market: Sales Value (in Million US$), 2017 & 2022

- Figure 8: Global: Thermal Interface Materials (Tapes and Films) Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 9: Global: Thermal Interface Materials (Elastomeric Pads) Market: Sales Value (in Million US$), 2017 & 2022

- Figure 10: Global: Thermal Interface Materials (Elastomeric Pads) Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 11: Global: Thermal Interface Materials (Greases and Adhesives) Market: Sales Value (in Million US$), 2017 & 2022

- Figure 12: Global: Thermal Interface Materials (Greases and Adhesives) Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 13: Global: Thermal Interface Materials (Phase Change Materials) Market: Sales Value (in Million US$), 2017 & 2022

- Figure 14: Global: Thermal Interface Materials (Phase Change Materials) Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 15: Global: Thermal Interface Materials (Metal Based Materials) Market: Sales Value (in Million US$), 2017 & 2022

- Figure 16: Global: Thermal Interface Materials (Metal Based Materials) Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 17: Global: Thermal Interface Materials (Others) Market: Sales Value (in Million US$), 2017 & 2022

- Figure 18: Global: Thermal Interface Materials (Others) Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 19: Global: Thermal Interface Materials (Telecom) Market: Sales Value (in Million US$), 2017 & 2022

- Figure 20: Global: Thermal Interface Materials (Telecom) Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 21: Global: Thermal Interface Materials (Computer) Market: Sales Value (in Million US$), 2017 & 2022

- Figure 22: Global: Thermal Interface Materials (Computer) Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 23: Global: Thermal Interface Materials (Medical Devices) Market: Sales Value (in Million US$), 2017 & 2022

- Figure 24: Global: Thermal Interface Materials (Medical Devices) Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 25: Global: Thermal Interface Materials (Industrial Machinery) Market: Sales Value (in Million US$), 2017 & 2022

- Figure 26: Global: Thermal Interface Materials (Industrial Machinery) Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 27: Global: Thermal Interface Materials (Consumer Durables) Market: Sales Value (in Million US$), 2017 & 2022

- Figure 28: Global: Thermal Interface Materials (Consumer Durables) Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 29: Global: Thermal Interface Materials (Automotive Electronics) Market: Sales Value (in Million US$), 2017 & 2022

- Figure 30: Global: Thermal Interface Materials (Automotive Electronics) Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 31: Global: Thermal Interface Materials (Others) Market: Sales Value (in Million US$), 2017 & 2022

- Figure 32: Global: Thermal Interface Materials (Others) Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 33: North America: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 34: North America: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 35: United States: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 36: United States: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 37: Canada: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 38: Canada: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 39: Asia Pacific: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 40: Asia Pacific: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 41: China: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 42: China: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 43: Japan: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 44: Japan: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 45: India: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 46: India: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 47: South Korea: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 48: South Korea: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 49: Australia: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 50: Australia: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 51: Indonesia: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 52: Indonesia: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 53: Others: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 54: Others: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 55: Europe: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 56: Europe: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 57: Germany: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 58: Germany: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 59: France: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 60: France: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 61: United Kingdom: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 62: United Kingdom: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 63: Italy: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 64: Italy: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 65: Spain: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 66: Spain: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 67: Russia: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 68: Russia: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 69: Others: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 70: Others: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 71: Latin America: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 72: Latin America: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 73: Brazil: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 74: Brazil: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 75: Mexico: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 76: Mexico: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 77: Others: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 78: Others: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 79: Middle East and Africa: Thermal Interface Materials Market: Sales Value (in Million US$), 2017 & 2022

- Figure 80: Middle East and Africa: Thermal Interface Materials Market: Breakup by Country (in %), 2022

- Figure 81: Middle East and Africa: Thermal Interface Materials Market Forecast: Sales Value (in Million US$), 2023-2028

- Figure 82: Global: Thermal Interface Materials Industry: SWOT Analysis

- Figure 83: Global: Thermal Interface Materials Industry: Value Chain Analysis

- Figure 84: Global: Thermal Interface Materials Industry: Porter's Five Forces Analysis

List of Tables

- Table 1: Global: Thermal Interface Materials Market: Key Industry Highlights, 2022 and 2028

- Table 2: Global: Thermal Interface Materials Market Forecast: Breakup by Product Type (in Million US$), 2023-2028

- Table 3: Global: Thermal Interface Materials Market Forecast: Breakup by Application (in Million US$), 2023-2028

- Table 4: Global: Thermal Interface Materials Market Forecast: Breakup by Region (in Million US$), 2023-2028

- Table 5: Global: Thermal Interface Materials Market: Competitive Structure

- Table 6: Global: Thermal Interface Materials Market: Key Players

Abstract

Market Overview:

The global thermal interface materials market size reached US$ 3.2 Billion in 2022. Looking forward, IMARC Group expects the market to reach US$ 5.5 Billion by 2028, exhibiting a growth rate (CAGR) of 9.4% during 2023-2028. The increasing demand for efficient thermal management solutions, the development of new TIM formulations and technologies, the rising demand for electronic devices, the miniaturization of electronic components, and the rapid technological advancements in semiconductor technology are some factors propelling the market.

Thermal interface materials (TIMs) are critical in efficiently transferring heat between two surfaces in various electronic devices. Their primary function is filling gaps and air pockets between components, such as microprocessors, power transistors, LED modules, and heat sinks or spreaders, ensuring maximum heat dissipation. They are designed to have high thermal conductivity and low thermal resistance to facilitate heat transfer. They are available in different forms, including thermal greases, pads, phase change materials, and adhesives. Each type of TIM has unique properties and applications, catering to specific requirements. The importance of TIMs lies in their ability to reduce thermal resistance and prevent overheating, which can negatively impact electronic devices, performance, reliability, and lifespan. By facilitating efficient heat dissipation, TIMs help maintain optimal operating temperatures, prevent thermal throttling, and enhance overall system performance.

The global market is majorly driven by the growing use of electronic devices, such as smartphones, laptops, and automotive electronics. In line with this, the rapid advancements in semiconductor technology, including higher power densities and increased component integration, are significantly contributing to the market. Furthermore, the increasing production of electric vehicles requires effective thermal management to handle the heat generated by batteries, power electronics, and electric motors, positively influencing the market. Apart from this, the rising data center infrastructure is catalyzing the market. Moreover, the escalating need to improve energy efficiency in electronic devices accelerates product adoption, as they help prevent overheating, reduce power consumption, and enhance overall energy efficiency. Besides, the increasing research and development efforts led to the development of new TIM formulations with improved thermal conductivity, reliability, and ease of application, offering numerous opportunities for the market. Additionally, the regulatory standards and guidelines in various industries, such as automotive and aerospace, mandate effective thermal management to ensure safety and reliability, contributing to the market growth.

Thermal Interface Materials Market Trends/Drivers:

Significant growth in the consumer electronics industry

Considerable growth in the consumer electronics industry is favorably impacting the market. The consumer electronics sector encompasses a wide range of devices, including smartphones, tablets, laptops, gaming consoles, smart home devices, and wearable technology. As this industry expands, the demand for TIMs rises in parallel. Consumer electronic devices are becoming increasingly compact, powerful, and energy-efficient. However, these advancements also generate more heat within the devices. TIMs play a crucial role in effectively dissipating this heat, ensuring the proper functioning and longevity of the electronic components. Moreover, consumers have higher expectations for device performance and reliability. Overheating can reduce performance, system failures, and even safety hazards. Therefore, manufacturers prioritize effective thermal management using TIMs to meet consumer demands for efficient cooling solutions. Additionally, the introduction of new and innovative consumer electronic devices constantly drives the need for advanced TIM formulations that offer improved thermal conductivity, reliability, and ease of application. The continuous growth and innovation in the consumer electronics industry significantly contribute to the market.

Increasing awareness regarding heat-related issues

The increasing awareness regarding the adverse effects of overheating on device performance and lifespan is strengthening the market. As technology advances and devices become more compact and powerful, managing heat becomes critical. Heat-related issues can reduce performance, system failures, and even safety hazards. The growing awareness of these issues has prompted manufacturers, engineers, and consumers to prioritize effective thermal management using TIMs. Industry professionals increasingly recognize the importance of selecting appropriate TIMs to optimize heat dissipation and ensure the reliable operation of electronic components. Furthermore, consumers are becoming more informed about the impact of heat on device performance and lifespan. They seek electronic devices that can withstand demanding tasks without overheating or experiencing thermal throttling. As a result, device manufacturers integrate high-quality TIMs to enhance heat transfer and maintain optimal operating temperatures, improving consumer satisfaction and product reliability. The increasing awareness of heat-related issues and the desire for efficient and reliable electronic devices drive the adoption and demand for TIMs in various industries, including consumer electronics, automotive, telecommunications, and data centers.

Growing demand for high-performance computing

The growing demand for high-performance computing (HPC) is fostering the market. HPC applications, such as artificial intelligence, machine learning, data analytics, and scientific simulations, require powerful processors and advanced hardware configurations that generate substantial heat. Efficient thermal management is crucial in HPC systems to maintain optimal performance and prevent overheating. TIMs facilitate heat transfer between high-performance processors, graphics cards, other components, and heat sinks or cooling solutions. As the demand for HPC continues to rise across industries, such as finance, healthcare, research, and entertainment, the need for advanced TIMs increases. These materials must have high thermal conductivity, low thermal resistance, and reliability to meet the demands of HPC applications. Additionally, the ongoing advancements in HPC technologies, such as the development of more powerful processors and GPUs, catalyze the need for advanced TIM formulations that can handle higher heat loads and provide efficient thermal management. The growing demand for high-performance computing and the critical role of TIMs in ensuring thermal efficiency is a key factor propelling the market.

Thermal Interface Materials Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global thermal interface materials market report, along with forecasts at the global, regional and country levels from 2023-2028. Our report has categorized the market based on product type and application.

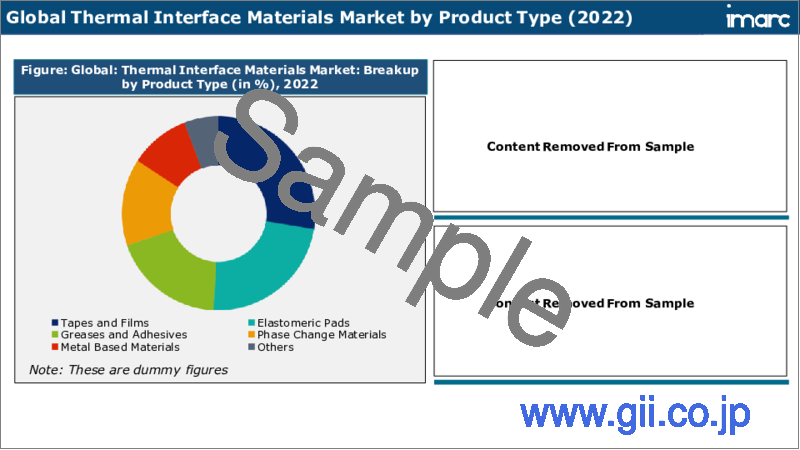

Breakup by Product Type:

Tapes and Films

Elastomeric Pads

Greases and Adhesives

Phase Change Materials

Metal Based Materials

Others

Greases and adhesives dominate the market

The report has provided a detailed breakup and analysis of the market based on product type. This includes tapes and films, elastomeric pads, greases and adhesives, phase change materials, metal based materials, and others. According to the report, greases and adhesives represented the largest segment.

Greases and adhesives are widely used in various industries for their thermal conductivity, ease of application, and ability to fill gaps and voids between components. They are commonly used in electronic devices to facilitate heat transfer between components and heat sinks, ensuring efficient thermal management and preventing overheating.

A considerable rise in electric vehicle production rates across the globe is a significant factor driving the demand for greases and adhesives. Electric vehicles generate substantial heat from batteries, power electronics, and motors. Greases and adhesives provide effective thermal conductivity and help dissipate heat in these components, contributing to overall performance and longevity.

Breakup by Application:

Telecom

Computer

Medical Devices

Industrial Machinery

Consumer Durables

Automotive Electronics

Others

Computer holds the largest share of the market

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes telecom, computer, medical devices, industrial machinery, consumer durables, automotive electronics, and others. According to the report, computer accounted for the largest market share.

The need for effective thermal management solutions has become crucial with the continuous advancement in computer technology and the increasing demand for high-performance computing devices. Computers often use thermal interface materials to enhance heat dissipation and improve the overall thermal performance of components such as processors, graphics cards, and memory modules. These materials help to efficiently transfer heat generated by these components to heat sinks or other cooling mechanisms, preventing overheating and ensuring optimal operation.

As computer systems become more powerful and compact, the thermal challenges intensify. The miniaturization of electronic components leads to higher power densities and increased heat generation. This necessitates using advanced thermal interface materials that offer superior thermal conductivity, low thermal resistance, and reliable performance under varying conditions. Moreover, the growing demand for gaming PCs, data centers, and cloud computing infrastructure further drives the adoption of thermal interface materials in the computer segment. The need to maintain stable operating temperatures and improve energy efficiency fuels the market growth, prompting manufacturers to develop innovative thermal interface materials that can meet the evolving demands of the computer industry.

Breakup by Region:

North America

United States

Canada

Asia Pacific

China

Japan

India

South Korea

Australia

Indonesia

Others

Europe

Germany

France

United Kingdom

Italy

Spain

Russia

Others

Latin America

Brazil

Mexico

Others

Middle East and Africa

Asia Pacific exhibits a clear dominance, accounting for the largest thermal interface materials market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa.

The Asia Pacific region is a major market for thermal interface materials market due to rapid industrialization, technological advancements, and the presence of major electronics and semiconductor manufacturing hubs. Asia Pacific is home to several key countries, major producers, and consumers of electronic devices and components. The region's dominance in the consumer electronics, automotive, and telecommunications sectors drives the need for effective thermal management solutions to ensure optimal performance and reliability of electronic systems.

Furthermore, the rising trend of urbanization, growing disposable incomes, and expanding middle-class population in the Asia Pacific region contribute to the increased adoption of electronic devices such as smartphones, laptops, and gaming consoles. This, in turn, fuels the demand for thermal interface materials to address the thermal challenges associated with these devices. Moreover, the region's increasing focus on energy efficiency, environmental sustainability, and regulations regarding thermal management in electronics further catalyzes the market. Manufacturers in the Asia Pacific are investing in research and development activities to develop advanced thermal interface materials that offer high thermal conductivity, low thermal resistance, and environmental friendliness.

Competitive Landscape:

Top thermal interface materials companies are crucial in catalyzing the market through innovative solutions and extensive research and development efforts. These companies are at the forefront of developing advanced thermal interface materials that cater to the evolving needs of various industries. They invest heavily in research and development to enhance their products' thermal conductivity, durability, and reliability. They work closely with manufacturers and customers to understand their requirements and develop tailored solutions for thermal management challenges. Additionally, these companies focus on expanding their product portfolios to offer a wide range of thermal interface materials suitable for different applications and industries. They also emphasize collaboration and strategic partnerships to leverage complementary technologies and expertise, enabling them to deliver comprehensive thermal management solutions. Through their continuous innovation, quality products, and strong customer relationships, these top thermal interface materials companies are propelling the market by setting industry standards and meeting the growing demand for efficient thermal management solutions across various sectors.

The report has provided a comprehensive analysis of the competitive landscape in the thermal interface materials market. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

3M Company

Dow Inc.

Henkel AG & Co. KGaA

Honeywell International Inc.

Indium Corporation

Kitagawa Industries America Inc.

Laird Technologies Inc.

Momentive Performance Materials Inc.

Parker-Hannifin Corporation

Zalman Tech Co. Ltd.

Recent Developments:

In July 2021, Dow launched DOWSIL TC-4551 CV Gap Filler, DOWSIL TC-2035 CV Adhesive, and DOWSIL TC-4060 GB250 Thermal Gel. These silicone-based thermal interface materials are aimed at electronics applications for electric and hybrid-electric vehicles.

In April 2022, Shin-Etsu Chemical Co., Ltd. launched a new thermal interface silicone rubber sheet designed for applications in electric vehicles.

In May 2022, Arieca partnered with ROHM Co., Ltd. for a joint research agreement to develop next-generation thermal interface materials for the EV market.

Key Questions Answered in This Report

- 1. What was the size of the global thermal interface materials market in 2022?

- 2. What is the expected growth rate of the global thermal interface materials market during 2023-2028?

- 3. What are the key factors driving the global thermal interface materials market?

- 4. What has been the impact of COVID-19 on the global thermal interface materials market?

- 5. What is the breakup of the global thermal interface materials market based on the product type?

- 6. What is the breakup of the global thermal interface materials market based on the application?

- 7. What are the key regions in the global thermal interface materials market?

- 8. Who are the key players/companies in the global thermal interface materials market?

Table of Contents

1 Preface

2 Scope and Methodology

- 2.1 Objectives of the Study

- 2.2 Stakeholders

- 2.3 Data Sources

- 2.3.1 Primary Sources

- 2.3.2 Secondary Sources

- 2.4 Market Estimation

- 2.4.1 Bottom-Up Approach

- 2.4.2 Top-Down Approach

- 2.5 Forecasting Methodology

3 Executive Summary

4 Introduction

- 4.1 Overview

- 4.2 Key Industry Trends

5 Global Thermal Interface Materials Market

- 5.1 Market Overview

- 5.2 Market Performance

- 5.3 Impact of COVID-19

- 5.4 Market Forecast

6 Market Breakup by Product Type

- 6.1 Tapes and Films

- 6.1.1 Market Trends

- 6.1.2 Market Forecast

- 6.2 Elastomeric Pads

- 6.2.1 Market Trends

- 6.2.2 Market Forecast

- 6.3 Greases and Adhesives

- 6.3.1 Market Trends

- 6.3.2 Market Forecast

- 6.4 Phase Change Materials

- 6.4.1 Market Trends

- 6.4.2 Market Forecast

- 6.5 Metal Based Materials

- 6.5.1 Market Trends

- 6.5.2 Market Forecast

- 6.6 Others

- 6.6.1 Market Trends

- 6.6.2 Market Forecast

7 Market Breakup by Application

- 7.1 Telecom

- 7.1.1 Market Trends

- 7.1.2 Market Forecast

- 7.2 Computer

- 7.2.1 Market Trends

- 7.2.2 Market Forecast

- 7.3 Medical Devices

- 7.3.1 Market Trends

- 7.3.2 Market Forecast

- 7.4 Industrial Machinery

- 7.4.1 Market Trends

- 7.4.2 Market Forecast

- 7.5 Consumer Durables

- 7.5.1 Market Trends

- 7.5.2 Market Forecast

- 7.6 Automotive Electronics

- 7.6.1 Market Trends

- 7.6.2 Market Forecast

- 7.7 Others

- 7.7.1 Market Trends

- 7.7.2 Market Forecast

8 Market Breakup by Region

- 8.1 North America

- 8.1.1 United States

- 8.1.1.1 Market Trends

- 8.1.1.2 Market Forecast

- 8.1.2 Canada

- 8.1.2.1 Market Trends

- 8.1.2.2 Market Forecast

- 8.1.1 United States

- 8.2 Asia Pacific

- 8.2.1 China

- 8.2.1.1 Market Trends

- 8.2.1.2 Market Forecast

- 8.2.2 Japan

- 8.2.2.1 Market Trends

- 8.2.2.2 Market Forecast

- 8.2.3 India

- 8.2.3.1 Market Trends

- 8.2.3.2 Market Forecast

- 8.2.4 South Korea

- 8.2.4.1 Market Trends

- 8.2.4.2 Market Forecast

- 8.2.5 Australia

- 8.2.5.1 Market Trends

- 8.2.5.2 Market Forecast

- 8.2.6 Indonesia

- 8.2.6.1 Market Trends

- 8.2.6.2 Market Forecast

- 8.2.7 Others

- 8.2.7.1 Market Trends

- 8.2.7.2 Market Forecast

- 8.2.1 China

- 8.3 Europe

- 8.3.1 Germany

- 8.3.1.1 Market Trends

- 8.3.1.2 Market Forecast

- 8.3.2 France

- 8.3.2.1 Market Trends

- 8.3.2.2 Market Forecast

- 8.3.3 United Kingdom

- 8.3.3.1 Market Trends

- 8.3.3.2 Market Forecast

- 8.3.4 Italy

- 8.3.4.1 Market Trends

- 8.3.4.2 Market Forecast

- 8.3.5 Spain

- 8.3.5.1 Market Trends

- 8.3.5.2 Market Forecast

- 8.3.6 Russia

- 8.3.6.1 Market Trends

- 8.3.6.2 Market Forecast

- 8.3.7 Others

- 8.3.7.1 Market Trends

- 8.3.7.2 Market Forecast

- 8.3.1 Germany

- 8.4 Latin America

- 8.4.1 Brazil

- 8.4.1.1 Market Trends

- 8.4.1.2 Market Forecast

- 8.4.2 Mexico

- 8.4.2.1 Market Trends

- 8.4.2.2 Market Forecast

- 8.4.3 Others

- 8.4.3.1 Market Trends

- 8.4.3.2 Market Forecast

- 8.4.1 Brazil

- 8.5 Middle East and Africa

- 8.5.1 Market Trends

- 8.5.2 Market Breakup by Country

- 8.5.3 Market Forecast

9 SWOT Analysis

- 9.1 Overview

- 9.2 Strengths

- 9.3 Weaknesses

- 9.4 Opportunities

- 9.5 Threats

10 Value Chain Analysis

11 Porters Five Forces Analysis

- 11.1 Overview

- 11.2 Bargaining Power of Buyers

- 11.3 Bargaining Power of Suppliers

- 11.4 Degree of Competition

- 11.5 Threat of New Entrants

- 11.6 Threat of Substitutes

12 Price Indicators

13 Competitive Landscape

- 13.1 Market Structure

- 13.2 Key Players

- 13.3 Profiles of Key Players

- 13.3.1 3M Company

- 13.3.1.1 Company Overview

- 13.3.1.2 Product Portfolio

- 13.3.1.3 Financials

- 13.3.1.4 SWOT Analysis

- 13.3.2 Dow Inc.

- 13.3.2.1 Company Overview

- 13.3.2.2 Product Portfolio

- 13.3.2.3 Financials

- 13.3.3 Henkel AG & Co. KGaA

- 13.3.3.1 Company Overview

- 13.3.3.2 Product Portfolio

- 13.3.3.3 Financials

- 13.3.3.4 SWOT Analysis

- 13.3.4 Honeywell International Inc.

- 13.3.4.1 Company Overview

- 13.3.4.2 Product Portfolio

- 13.3.4.3 Financials

- 13.3.4.4 SWOT Analysis

- 13.3.5 Indium Corporation

- 13.3.5.1 Company Overview

- 13.3.5.2 Product Portfolio

- 13.3.6 Kitagawa Industries America Inc.

- 13.3.6.1 Company Overview

- 13.3.6.2 Product Portfolio

- 13.3.7 Laird Technologies Inc.

- 13.3.7.1 Company Overview

- 13.3.7.2 Product Portfolio

- 13.3.8 Momentive Performance Materials Inc.

- 13.3.8.1 Company Overview

- 13.3.8.2 Product Portfolio

- 13.3.9 Parker-Hannifin Corporation

- 13.3.9.1 Company Overview

- 13.3.9.2 Product Portfolio

- 13.3.9.3 Financials

- 13.3.9.4 SWOT Analysis

- 13.3.10 Zalman Tech Co., Ltd.

- 13.3.10.1 Company Overview

- 13.3.10.2 Product Portfolio

- 13.3.1 3M Company