|

|

市場調査レポート

商品コード

1772197

ドライバーモニタリングシステムの市場規模、シェアと動向分析レポート:コンポーネント別、技術別、機能別、車種別、地域別、セグメント予測、2025年~2033年Driver Monitoring System Market Size, Share & Trends Analysis Report By Component, By Technology By Functionality, By Vehicle Type, By Region, And Segment Forecasts, 2025 - 2033 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| ドライバーモニタリングシステムの市場規模、シェアと動向分析レポート:コンポーネント別、技術別、機能別、車種別、地域別、セグメント予測、2025年~2033年 |

|

出版日: 2025年06月27日

発行: Grand View Research

ページ情報: 英文 130 Pages

納期: 2~10営業日

|

全表示

- 概要

- 図表

- 目次

ドライバーモニタリングシステム市場促進要因概要

ドライバーモニタリングシステムの世界市場規模は2024年に30億3,000万米ドルと推定され、2033年には81億米ドルに達すると予測され、2025~2033年のCAGRは11.7%で成長します。この市場は、新車へのドライバーモニタリングシステム(DMS)搭載を義務付ける世界各国の政府による厳しい規制によって勢いを増しています。

自律性レベルL1からL3までの先進運転支援システム(ADAS)にDMSが統合されつつあることが、OEMからの強い需要を後押しし、より安全で自動化された運転体験を支えています。また、車内の安全性に関する消費者の意識の高まりや、高級車や電気自動車におけるパーソナライズされた機能に対する需要の高まりが、市場の成長をさらに加速させています。商用フリートや公共輸送への拡大は、ドライバーの説明責任を強化し、乗客の安全を確保し、フリート管理規制を遵守する必要性によって、ドライバーモニタリングシステム(DMS)産業の参入企業に大きな成長機会をもたらしています。しかし、システムコストの高さ、統合の複雑さ、データのプライバシーやドライバーの同意に関する懸念が大きな課題となっており、特にコストに敏感な車両セグメントでは、より広範な採用を妨げる可能性があります。

EU、米国、中国の当局は、眠気や注意散漫による交通事故を減らすためにDMSを義務付けています。EUでは、規則(EU)2019/2144により、2026年7月以降、カテゴリーMとNのすべての新車に、視覚的注意をモニタリングし、注意散漫が検出された場合に警告を発することができる高度運転注意散漫警告(ADDW)システムを搭載することが義務付けられています。これを受けて、ソリューションプロバイダは製品展開を加速させています。例えば、Cipiaは2022年2月、注意力、眠気、電話の使用や喫煙などの行動を追跡するよう設計されたDriver Senseシステムを発表しました。乗用車と商用車の両方を対象としたこのシステムは、世界の規制遵守をサポートします。これらの開発は、安全に関する法規制がいかにDMSの革新と展開を積極的に形成しているかを浮き彫りにしています。

車両の半自律化が進むにつれ、ドライバーの継続的な関与と準備態勢の確保は、安全コンプライアンスと事故防止にとって不可欠となります。DMSは、車線維持、衝突回避、ドライバー行動分析を含む総合的な車内安全エコシステムを提供するため、より広範なADASスイートに統合されつつあります。例えば、AddSecureは2023年4月、DMSとADASを組み合わせてあくびやうなずきなどの疲労指標をモニタリングし、居眠り運転事故を防ぐためにリアルタイムで警告を発するAI搭載ビデオテレマティクスソリューションを発表しました。DMSとADASの融合は、多機能プラットフォームが機能を強化し、規制基準をサポートし、次世代車両のハードウェアの冗長性を削減する、システムインテグレーションに向けた産業全体の動向を反映しています。

商業フリートや公共輸送への拡大がドライバーモニタリングシステム(DMS)市場の大きな成長機会となっており、これはフリート事業者が責任の軽減、安全コンプライアンスの改善、規制の義務化を求めているためです。DMSソリューションは、ドライバーの行動をリアルタイムで把握し、疲労や注意散漫、危険な行動の早期発見を可能にします。これらの機能は、ドライバーの注意力が運行の安全性とサービスの信頼性に直接影響する、長距離物流や旅客輸送業務において特に重要です。例えば、2025年3月、三菱エレクトリック・オートモーティブ・アメリカはシーイング・マシーンズと提携し、ガーディアン・ジェネレーション3 DMSを南北アメリカ全域で普及させました。このシステムは、AIを活用したアラートとイベントベースのビデオを使用して、注意散漫や眠気を検知する商用フリート向けです。このような統合は、事故防止、保険コスト削減、高稼働率車両ネットワークでの規制遵守に役立つ技術を優先するフリート管理者の間で支持を集めています。

先進的DMSソリューション、特に赤外線カメラ、AIプロセッサ、リアルタイム分析を組み合わせたソリューションを導入するには、システムの仕様やOEMのカスタマイズ要件にもよりますが、車両1台当たり200~700米ドルの追加費用がかかります。これらのコストは、車両の電子アーキテクチャ、インフォテインメントプラットフォーム、ADASスイートへのシームレスな統合の必要性によってさらに増大します。小規模な自動車メーカーやフリート・オペレーターは、キャリブレーション、ソフトウェアの互換性、規制テストに関連する課題に直面することが多く、展開のタイムラインやテクニカルサポートの必要性がさらに高まります。また、ティア1サプライヤーは、ユーロNCAPやGSRのコンプライアンスを満たすために、ハードウェアとソフトウェアの共同設計の複雑さを乗り越えなければならないです。その結果、規制の圧力が高まっているにもかかわらず、先行投資とエンジニアリングのオーバーヘッドが大きいため、コストに敏感な市場でのDMSの普及は依然として遅れています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 ドライバーモニタリングシステム市場の変数、動向、範囲

- 市場系統の展望

- 市場力学

- 市場促進要因分析

- 市場抑制要因分析

- 産業の課題

- ドライバーモニタリングシステム市場分析ツール

- 産業分析-ポーターのファイブフォース分析

- PESTEL分析

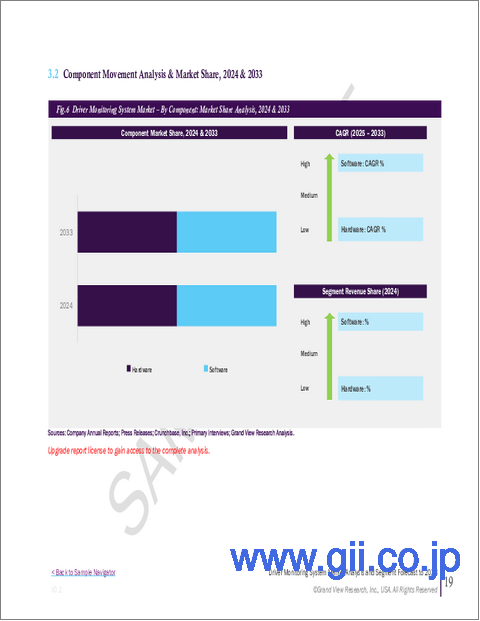

第4章 ドライバーモニタリングシステム市場:コンポーネント別、推定・動向分析

- セグメントダッシュボード

- ドライバーモニタリングシステム市場:コンポーネント変動分析、2024年と2033年

- ハードウェア

- ソフトウェア

第5章 ドライバーモニタリングシステム市場:技術別、推定・動向分析

- セグメントダッシュボード

- ドライバーモニタリングシステム市場:技術変動分析、2024年と2033年

- カメラベースのDMS

- 赤外線LEDベースのDMS

- ステアリング角センサベースのDMS

- 生体認証DMS

第6章 ドライバーモニタリングシステム市場:機能別、推定・動向分析

- セグメントダッシュボード

- ドライバーモニタリングシステム市場:機能別変動分析、2024年と2033年

- ドライバー状態モニタリング

- ドライバーの識別と認証

- 乗員モニタリングシステム(OMS)

- ドライバー行動分析

第7章 ドライバーモニタリングシステム市場:車種別、推定・動向分析

- セグメントダッシュボード

- ドライバーモニタリングシステム市場:車種別変動分析、2024年と2033年

- 乗用車

- 商用車

第8章 ドライバーモニタリングシステム市場:地域別、推定・動向分析

- ドライバーモニタリングシステム市場シェア(地域別、2024年と2033年)、100万米ドル

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第9章 競合情勢

- 企業分類

- 企業の市場ポジショニング

- 企業ヒートマップ分析

- 企業プロファイル/上場企業

- Valeo SA

- Denso Corporation

- Bosch Mobility Solutions(Robert Bosch GmbH)

- Seeing Machines Limited

- Continental AG

- Smart Eye AB

- Aptiv PLC

- Magna International Inc.

- Visteon Corporation

- Lytx Inc.

List of Tables

- Table 1 Global Driver Monitoring System Market size estimates & forecasts 2021 - 2033 (USD Million)

- Table 2 Global Driver Monitoring System Market, by Region 2021 - 2033 (USD Million)

- Table 3 Global Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 4 Global Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 5 Global Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 6 Global Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 7 Hardware market, by region 2021 - 2033 (USD Million)

- Table 8 Software market, by region 2021 - 2033 (USD Million)

- Table 9 Camera-based DMS market, by region 2021 - 2033 (USD Million)

- Table 10 Infrared LED-based DMS market, by region 2021 - 2033 (USD Million)

- Table 11 Steering Angle Sensor-based DMS market, by region 2021 - 2033 (USD Million)

- Table 12 Biometric DMS market, by region 2021 - 2033 (USD Million)

- Table 13 Driver State Monitoring market, by region 2021 - 2033 (USD Million)

- Table 14 Driver Identification & Authentication market, by region 2021 - 2033 (USD Million)

- Table 15 Occupant Monitoring System (OMS) market, by region 2021 - 2033 (USD Million)

- Table 16 Driver Behavior Analysis market, by region 2021 - 2033 (USD Million)

- Table 17 Passenger Vehicles market, by region 2021 - 2033 (USD Million)

- Table 18 Commercial Vehicles market, by region 2021 - 2033 (USD Million)

- Table 19 North America Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 20 North America Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 21 North America Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 22 North America Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 23 U.S. Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 24 U.S. Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 25 U.S. Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 26 U.S. Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 27 Canada Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 28 Canada Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 29 Canada Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 30 Canada Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 31 Mexico Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 32 Mexico Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 33 Mexico Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 34 Mexico Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 35 Europe Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 36 Europe Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 37 Europe Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 38 Europe Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 39 UK Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 40 UK Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 41 UK Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 42 UK Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 43 Germany Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 44 Germany Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 45 Germany Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 46 Germany Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 47 France Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 48 France Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 49 France Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 50 France Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 51 Asia Pacific Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 52 Asia Pacific Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 53 Asia Pacific Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 54 Asia Pacific Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 55 China Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 56 China Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 57 China Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 58 China Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 59 India Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 60 India Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 61 India Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 62 India Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 63 Japan Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 64 Japan Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 65 Japan Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 66 Japan Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 67 Australia Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 68 Australia Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 69 Australia Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 70 Australia Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 71 South Korea Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 72 South Korea Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 73 South Korea Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 74 South Korea Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 75 Latin America Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 76 Latin America Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 77 Latin America Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 78 Latin America Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 79 Brazil Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 80 Brazil Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 81 Brazil Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 82 Brazil Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 83 Middle East & Africa Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 84 Middle East & Africa Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 85 Middle East & Africa Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 86 Middle East & Africa Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 87 Kingdom of Saudi Arabia (KSA) Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 88 Kingdom of Saudi Arabia (KSA) Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 89 Kingdom of Saudi Arabia (KSA) Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 90 Kingdom of Saudi Arabia (KSA) Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 91 UAE Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 92 UAE Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 93 UAE Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 94 UAE Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

- Table 95 South Africa Driver Monitoring System Market, by Component 2021 - 2033 (USD Million)

- Table 96 South Africa Driver Monitoring System Market, by Technology 2021 - 2033 (USD Million)

- Table 97 South Africa Driver Monitoring System Market, by Functionality 2021 - 2033 (USD Million)

- Table 98 South Africa Driver Monitoring System Market, by Vehicle Type 2021 - 2033 (USD Million)

List of Figures

- Fig. 1 Driver Monitoring System Market Segmentation

- Fig. 2 Market research deployment mode

- Fig. 3 Information procurement

- Fig. 4 Primary research pattern

- Fig. 5 Market research approaches

- Fig. 6 Value chain-based sizing & forecasting

- Fig. 7 Parent market analysis

- Fig. 8 Market formulation & validation

- Fig. 9 Driver Monitoring System Market Snapshot

- Fig. 10 Driver Monitoring System Market Segment Snapshot

- Fig. 11 Driver Monitoring System Market Competitive Landscape Snapshot

- Fig. 12 Market research deployment mode

- Fig. 13 Market driver relevance analysis (Current & future impact)

- Fig. 14 Market restraint relevance analysis (Current & future impact)

- Fig. 15 Driver Monitoring System Market: Component Outlook Key Takeaways (USD Million)

- Fig. 16 Driver Monitoring System Market: Component Movement Analysis 2024 & 2033 (USD Million)

- Fig. 17 Hardware market revenue estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 18 Software market revenue estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 19 Driver Monitoring System Market: Technology Outlook Key Takeaways (USD Million)

- Fig. 20 Driver Monitoring System Market: Technology movement analysis 2024 & 2033 (USD Million)

- Fig. 21 Camera-based DMS market revenue estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 22 Infrared LED-based DMS market revenue estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 23 Steering Angle Sensor-based DMS market revenue estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 24 Biometric DMS market revenue estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 25 Driver Monitoring System Market: Functionality Outlook Key Takeaways (USD Million)

- Fig. 26 Driver Monitoring System Market: Functionality Movement Analysis 2024 & 2033 (USD Million)

- Fig. 27 Driver State Monitoring market revenue estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 28 Driver Identification & Authentication market revenue estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 29 Occupant Monitoring System (OMS) market revenue estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 30 Driver Behavior Analysis market revenue estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 31 Driver Monitoring System Market: Vehicle Type Outlook Key Takeaways (USD Million)

- Fig. 32 Driver Monitoring System Market: Vehicle Type Movement Analysis 2024 & 2033 (USD Million)

- Fig. 33 Passenger Vehicles market revenue estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 34 Commercial Vehicles market revenue estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 35 Regional marketplace: Key takeaways

- Fig. 36 Driver Monitoring System Market: Regional Outlook, 2024 & 2033 (USD Million)

- Fig. 37 North America Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 38 U.S. Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 39 Canada Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 40 Mexico Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 41 Europe Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 42 UK Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 43 Germany Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 44 France Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 45 Asia Pacific Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 46 Japan Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 47 China Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 48 India Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 49 Australia Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 50 South Korea Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 51 Latin America Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 52 Brazil Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 53 MEA Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 54 KSA Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 55 UAE Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 56 South Africa Driver Monitoring System Market estimates and forecasts, 2021 - 2033 (USD Million)

- Fig. 57 Strategy framework

- Fig. 58 Company Categorization

Driver Monitoring System Market Summary

The global driver monitoring system market size was estimated at USD 3.03 billion in 2024 and is projected to reach USD 8.10 billion by 2033, growing at a CAGR of 11.7% from 2025 to 2033. The market is gaining momentum, driven by stringent regulatory mandates from governments across the globe requiring driver monitoring system (DMS) installation in new vehicles.

The rising integration of DMS within advanced driver assistance systems (ADAS) across autonomy levels L1 to L3 is driving strong demand from OEMs, supporting safer and more automated driving experiences. Also, increasing consumer awareness around in-cabin safety and growing demand for personalized features in luxury and electric vehicles further accelerate market growth.Expansion into commercial fleets and public transit creates a major growth opportunity for players in the driver monitoring system (DMS) industry, driven by the need to enhance driver accountability, ensure passenger safety, and comply with fleet management regulations. However, high system costs, integration complexities, and concerns around data privacy and driver consent pose significant challenges that may hinder broader adoption, especially in cost-sensitive vehicle segments.

Authorities in the EU, the U.S., and China have mandated DMS to reduce road accidents caused by drowsiness or distraction. In the EU, Regulation (EU) 2019/2144 requires all new vehicles of categories M and N to include advanced driver distraction warning (ADDW) systems from July 2026, capable of monitoring visual attention and issuing alerts when distraction is detected. In response, solution providers are accelerating product rollouts. For example, in February 2022, Cipia introduced its Driver Sense system, designed to track attention, drowsiness, and behaviors such as phone use or smoking. Aimed at both passenger and commercial fleets, it supports global regulatory compliance. These developments highlight how safety legislation is actively shaping DMS innovation and deployment.

As vehicles become increasingly semi-autonomous, ensuring continuous driver engagement and readiness becomes essential for safety compliance and accident prevention. DMS is being integrated into broader ADAS suites to deliver a holistic in-cabin safety ecosystem that includes lane-keeping, collision avoidance, and driver behavior analysis. For instance, in April 2023, AddSecure introduced an AI-powered video telematics solution that combines DMS and ADAS to monitor fatigue indicators such as yawning and head nodding, issuing real-time alerts to prevent drowsy driving incidents. The convergence of DMS with ADAS reflects an industry-wide trend toward system consolidation, where multi-function platforms enhance functionality, support regulatory standards, and reduce hardware redundancy in next-generation vehicles.

Expansion into commercial fleets and public transit represents a major growth opportunity in the driver monitoring system (DMS) market, as fleet operators seek to reduce liability, improve safety compliance, and meet regulatory mandates. DMS solutions provide real-time insights into driver behavior, enabling early detection of fatigue, distraction, or risky actions. These features are particularly critical in long-haul logistics and passenger transport operations, where driver attentiveness directly impacts operational safety and service reliability. For example, in March 2025, Mitsubishi Electric Automotive America partnered with Seeing Machines to promote the Guardian Generation 3 DMS across the Americas. The system targets commercial fleets, using AI-powered alerts and event-based video to detect distraction and drowsiness. Such integrations are gaining traction among fleet managers, who prioritize technologies that help prevent accidents, lower insurance costs, and ensure regulatory compliance across high-utilization vehicle networks.

Implementing advanced DMS solutions, especially those combining infrared cameras, AI processors, and real-time analytics, can add between USD 200 to USD 700 per vehicle, depending on system specifications and OEM customization requirements. These costs are compounded by the need for seamless integration into vehicle electronic architectures, infotainment platforms, and ADAS suites. Smaller automakers and fleet operators often face challenges related to calibration, software compatibility, and regulatory testing, which further increase deployment timelines and technical support needs. Also, Tier 1 suppliers must navigate hardware and software co-design complexities to meet Euro NCAP or GSR compliance. As a result, despite growing regulatory pressure, the high upfront investment and engineering overhead continue to slow DMS penetration in cost-sensitive markets.

Global Driver Monitoring System Market Report Segmentation

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends in each of the sub-segments from 2021 to 2033. For this study, Grand View Research has segmented the global driver monitoring system market report based on component, technology, functionality, vehicle type, and region:

- Component Outlook (Revenue, USD Million, 2021- 2033)

- Hardware

- Software

- Technology Outlook (Revenue, USD Million, 2021- 2033)

- Camera-based DMS

- Infrared LED-based DMS

- Steering Angle Sensor-based DMS

- Biometric DMS

- Functionality Outlook (Revenue, USD Million, 2021- 2033)

- Driver State Monitoring

- Driver Identification & Authentication

- Occupant Monitoring System (OMS)

- Driver Behavior Analysis

- Vehicle Type Outlook (Revenue, USD Million, 2021- 2033)

- Passenger Vehicles

- Commercial Vehicles

- Regional Outlook (Revenue, USD Million, 2021- 2033)

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Asia Pacific

- China

- India

- Japan

- Australia

- South Korea

- Latin America

- Brazil

- Middle East & Africa (MEA)

- UAE

- Kingdom of Saudi Arabia (KSA)

- South Africa

Table of Contents

Chapter 1. Methodology and Scope

- 1.1. Market Segmentation and Scope

- 1.2. Research Methodology

- 1.2.1. Information Procurement

- 1.3. Information or Data Analysis

- 1.4. Methodology

- 1.5. Research Scope and Assumptions

- 1.6. Market Formulation & Validation

- 1.7. List of Data Sources

Chapter 2. Executive Summary

- 2.1. Market Outlook

- 2.2. Segment Outlook

- 2.3. Competitive Insights

Chapter 3. Driver Monitoring System Market Variables, Trends, & Scope

- 3.1. Market Lineage Outlook

- 3.2. Market Dynamics

- 3.2.1. Market Driver Analysis

- 3.2.2. Market Restraint Analysis

- 3.2.3. Industry Challenge

- 3.3. Driver Monitoring System Market Analysis Tools

- 3.3.1. Industry Analysis - Porter's

- 3.3.1.1. Bargaining power of the suppliers

- 3.3.1.2. Bargaining power of the buyers

- 3.3.1.3. Threats of substitution

- 3.3.1.4. Threats from new entrants

- 3.3.1.5. Competitive rivalry

- 3.3.2. PESTEL Analysis

- 3.3.2.1. Political landscape

- 3.3.2.2. Economic landscape

- 3.3.2.3. Social Landscape

- 3.3.2.4. Technological landscape

- 3.3.2.5. Environmental Landscape

- 3.3.2.6. Legal landscape

- 3.3.1. Industry Analysis - Porter's

Chapter 4. Driver Monitoring System Market: Component Estimates & Trend Analysis

- 4.1. Segment Dashboard

- 4.1.1. Driver Monitoring System Market: Component Movement Analysis, 2024 & 2033 (USD Million)

- 4.2. Hardware

- 4.2.1. Hardware Market Revenue Estimates and Forecasts, 2021 - 2033 (USD Million)

- 4.3. Software

- 4.3.1. Software Market Revenue Estimates and Forecasts, 2021 - 2033 (USD Million)

Chapter 5. Driver Monitoring System Market: Technology Estimates & Trend Analysis

- 5.1. Segment Dashboard

- 5.2. Driver Monitoring System Market: Technology Movement Analysis, 2024 & 2033 (USD Million)

- 5.3. Camera-based DMS

- 5.3.1. Camera-based DMS Market Revenue Estimates and Forecasts, 2021 - 2033 (USD Million)

- 5.4. Infrared LED-based DMS

- 5.4.1. Infrared LED-based DMS Market Revenue Estimates and Forecasts, 2021 - 2033 (USD Million)

- 5.5. Steering Angle Sensor-based DMS

- 5.5.1. Steering Angle Sensor-based DMS Market Revenue Estimates and Forecasts, 2021 - 2033 (USD Million)

- 5.6. Biometric DMS

- 5.6.1. Biometric DMS Market Revenue Estimates and Forecasts, 2021 - 2033 (USD Million)

Chapter 6. Driver Monitoring System Market: Functionality Estimates & Trend Analysis

- 6.1. Segment Dashboard

- 6.2. Driver Monitoring System Market: By Functionality Movement Analysis, 2024 & 2033 (USD Million)

- 6.3. Driver State Monitoring

- 6.3.1. Driver State Monitoring Market Revenue Estimates and Forecasts, 2021 - 2033 (USD Million)

- 6.4. Driver Identification & Authentication

- 6.4.1. Driver Identification & Authentication Market Revenue Estimates and Forecasts, 2021 - 2033 (USD Million)

- 6.5. Occupant Monitoring System (OMS)

- 6.5.1. Occupant Monitoring System (OMS) Market Revenue Estimates and Forecasts, 2021 - 2033 (USD Million)

- 6.6. Driver Behavior Analysis

- 6.6.1. Driver Behavior Analysis Market Revenue Estimates and Forecasts, 2021 - 2033 (USD Million)

Chapter 7. Driver Monitoring System Market: Vehicle Type Estimates & Trend Analysis

- 7.1. Segment Dashboard

- 7.2. Driver Monitoring System Market: By Vehicle Type Movement Analysis, 2024 & 2033 (USD Million)

- 7.3. Passenger Vehicles

- 7.3.1. Passenger Vehicles Market Revenue Estimates and Forecasts, 2021 - 2033 (USD Million)

- 7.4. Commercial Vehicles

- 7.4.1. Commercial Vehicles Market Revenue Estimates and Forecasts, 2021 - 2033 (USD Million)

Chapter 8. Driver Monitoring System Market: Regional Estimates & Trend Analysis

- 8.1. Driver Monitoring System Market Share, By Region, 2024 & 2033, USD Million

- 8.2. North America

- 8.2.1. North America Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.2.2. U.S.

- 8.2.2.1. U.S. Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.2.3. Canada

- 8.2.3.1. Canada Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.2.4. Mexico

- 8.2.4.1. Mexico Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.3. Europe

- 8.3.1. Europe Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.3.2. UK

- 8.3.2.1. UK Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.3.3. Germany

- 8.3.3.1. Germany Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.3.4. France

- 8.3.4.1. Italy Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.4. Asia Pacific

- 8.4.1. Asia Pacific Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.4.2. China

- 8.4.2.1. China Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.4.3. Japan

- 8.4.3.1. Japan Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.4.4. India

- 8.4.4.1. India Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.4.5. South Korea

- 8.4.5.1. South Korea Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.4.6. Australia

- 8.4.6.1. Australia Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.5. Latin America

- 8.5.1. Latin America Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.5.2. Brazil

- 8.5.2.1. Brazil Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.6. Middle East and Africa

- 8.6.1. Middle East and Africa Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.6.2. UAE

- 8.6.2.1. UAE Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.6.3. KSA

- 8.6.3.1. KSA Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

- 8.6.4. South Africa

- 8.6.4.1. South Africa Driver Monitoring System Market Estimates and Forecasts, 2021 - 2033 (USD Million)

Chapter 9. Competitive Landscape

- 9.1. Company Categorization

- 9.2. Company Market Positioning

- 9.3. Company Heat Map Analysis

- 9.4. Company Profiles/Listing

- 9.4.1. Valeo S.A.

- 9.4.1.1. Participant's Overview

- 9.4.1.2. Financial Performance

- 9.4.1.3. Product Benchmarking

- 9.4.1.4. Strategic Initiatives

- 9.4.2. Denso Corporation

- 9.4.2.1. Participant's Overview

- 9.4.2.2. Financial Performance

- 9.4.2.3. Product Benchmarking

- 9.4.2.4. Strategic Initiatives

- 9.4.3. Bosch Mobility Solutions (Robert Bosch GmbH)

- 9.4.3.1. Participant's Overview

- 9.4.3.2. Financial Performance

- 9.4.3.3. Product Benchmarking

- 9.4.3.4. Strategic Initiatives

- 9.4.4. Seeing Machines Limited

- 9.4.4.1. Participant's Overview

- 9.4.4.2. Financial Performance

- 9.4.4.3. Product Benchmarking

- 9.4.4.4. Strategic Initiatives

- 9.4.5. Continental AG

- 9.4.5.1. Participant's Overview

- 9.4.5.2. Financial Performance

- 9.4.5.3. Product Benchmarking

- 9.4.5.4. Strategic Initiatives

- 9.4.6. Smart Eye AB

- 9.4.6.1. Participant's Overview

- 9.4.6.2. Financial Performance

- 9.4.6.3. Product Benchmarking

- 9.4.6.4. Strategic Initiatives

- 9.4.7. Aptiv PLC

- 9.4.7.1. Participant's Overview

- 9.4.7.2. Financial Performance

- 9.4.7.3. Product Benchmarking

- 9.4.7.4. Strategic Initiatives

- 9.4.8. Magna International Inc.

- 9.4.8.1. Participant's Overview

- 9.4.8.2. Financial Performance

- 9.4.8.3. Product Benchmarking

- 9.4.8.4. Strategic Initiatives

- 9.4.9. Visteon Corporation

- 9.4.9.1. Participant's Overview

- 9.4.9.2. Financial Performance

- 9.4.9.3. Product Benchmarking

- 9.4.9.4. Strategic Initiatives

- 9.4.10. Lytx Inc.

- 9.4.10.1. Participant's Overview

- 9.4.10.2. Financial Performance

- 9.4.10.3. Product Benchmarking

- 9.4.10.4. Strategic Initiatives

- 9.4.1. Valeo S.A.